TAXATION LAW

VerifiedAdded on 2019/10/31

|9

|1296

|151

Report

AI Summary

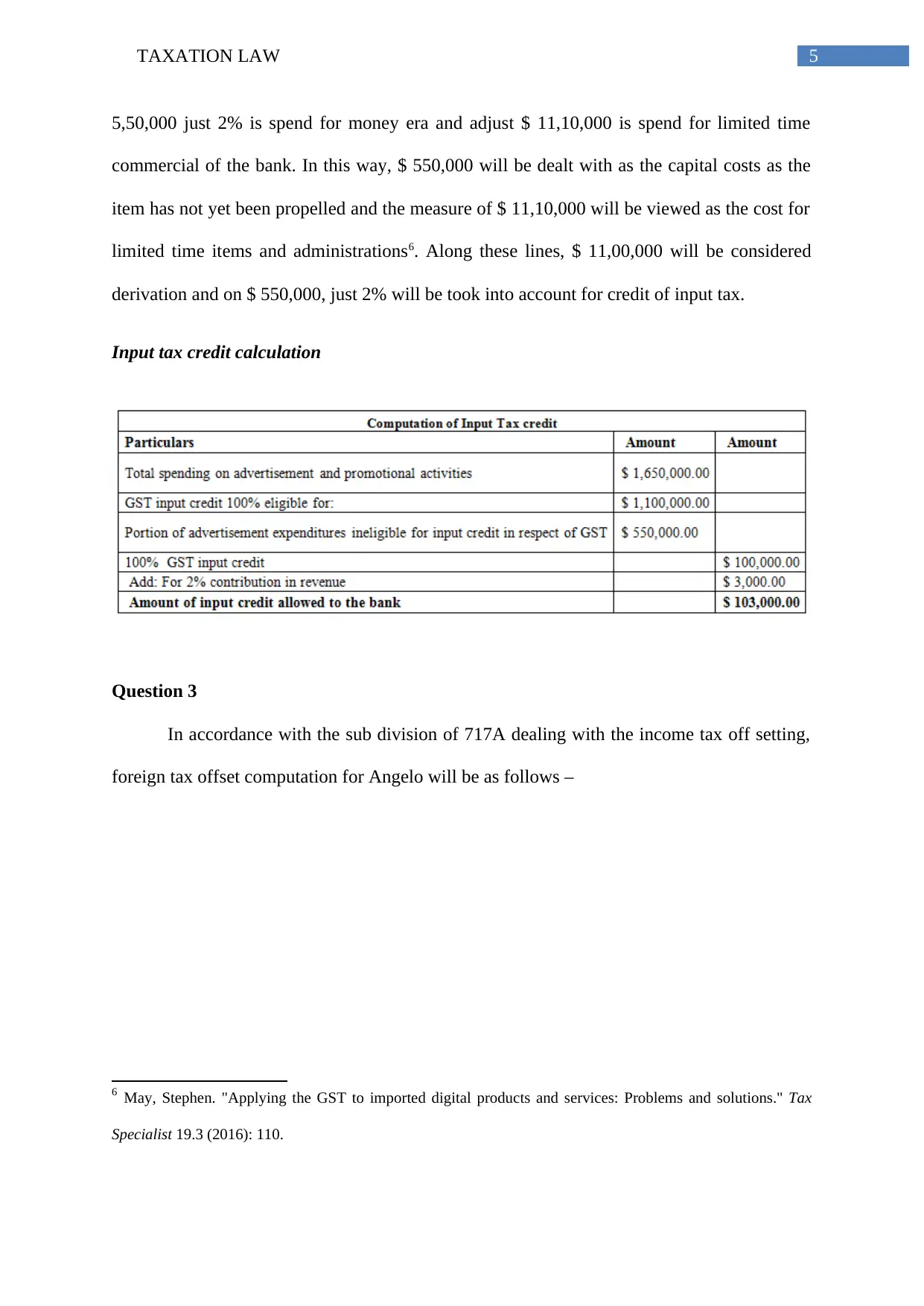

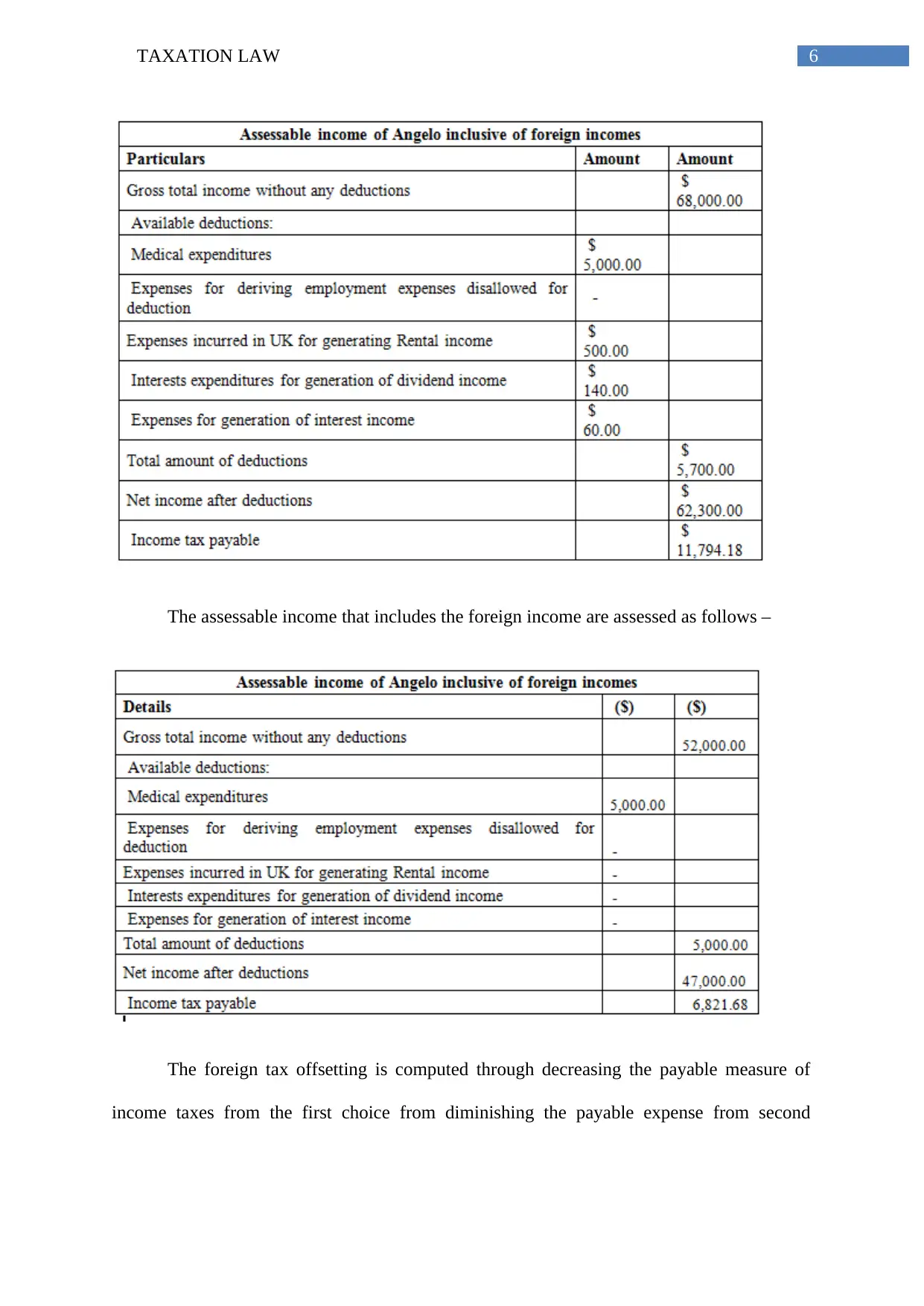

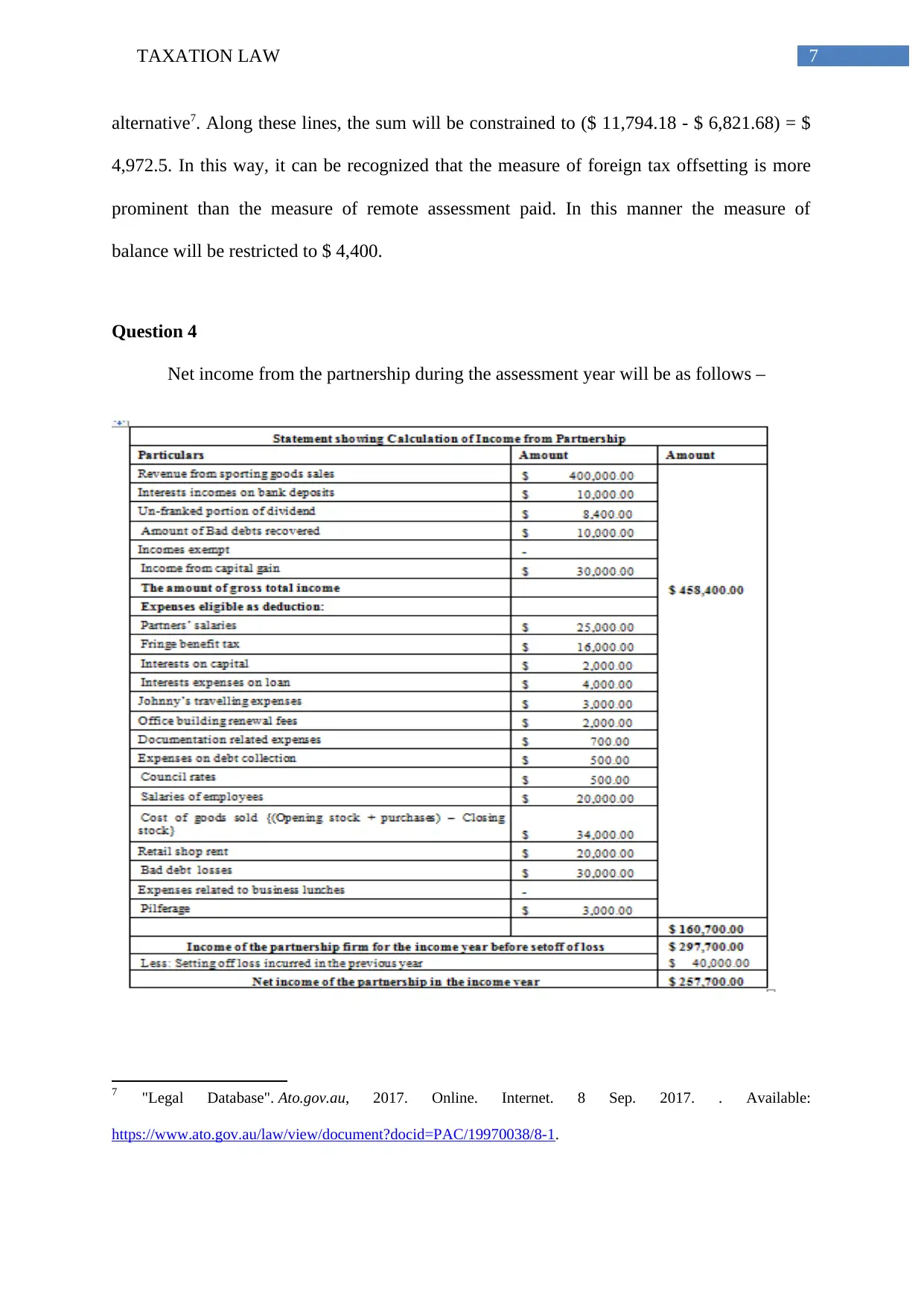

The assignment content discusses taxation law, specifically focusing on the views of the Australian Taxation Office (ATO) regarding the term 'incurred' under Section 8-1 of the Income Tax Assessment Act (ITAA) 1997. The content also explores the treatment of various expenses under ITAA 1997, including machinery moving costs, revaluation cost of assets for insurance offset, and legal expenses for fighting against winding up petitions or hiring solicitor services. Additionally, it covers input tax credit calculation and foreign tax offset computation, as well as net income from a partnership during an assessment year.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.