Western Sydney University: Taxation Law Assignment - Autumn 2018

VerifiedAdded on 2023/06/04

|13

|2236

|212

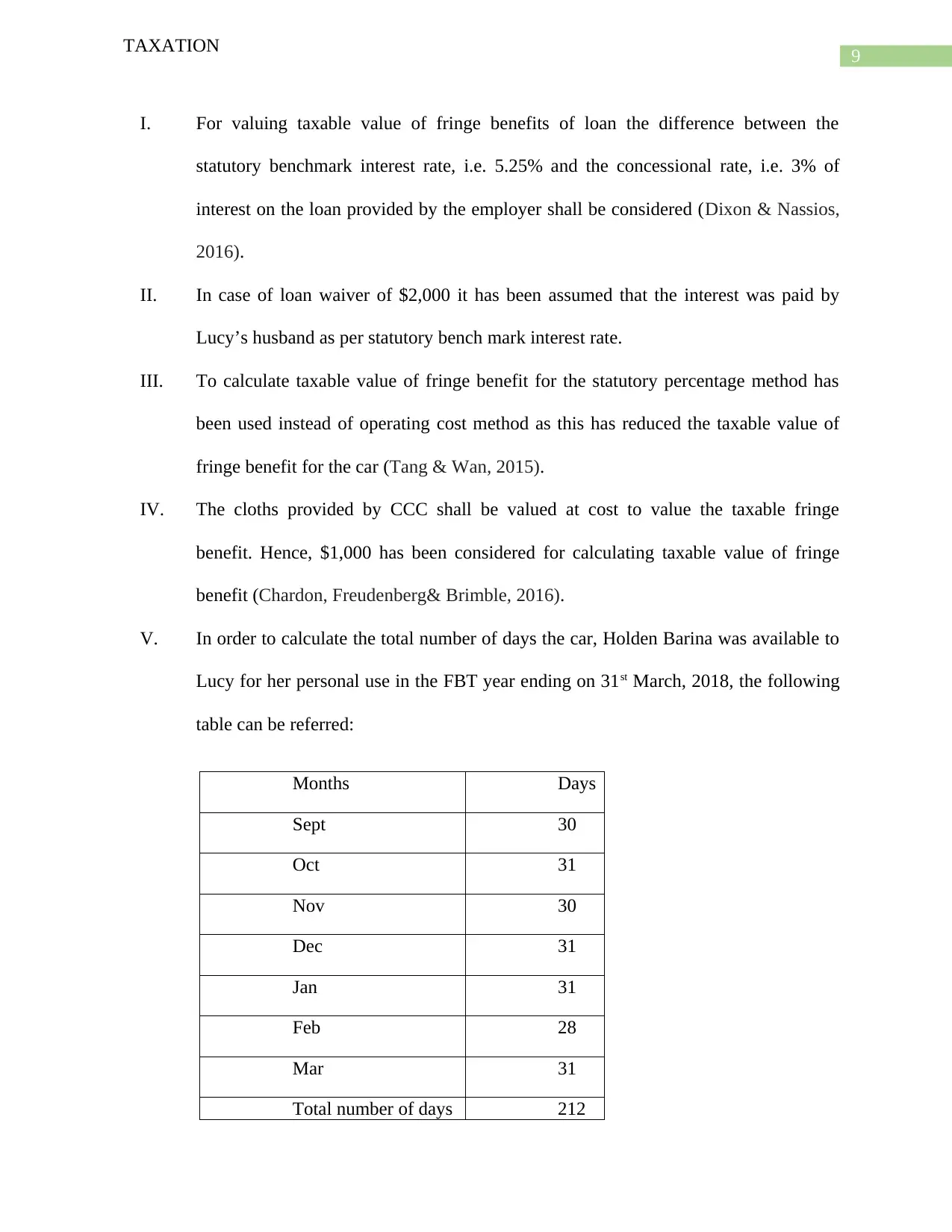

Homework Assignment

AI Summary

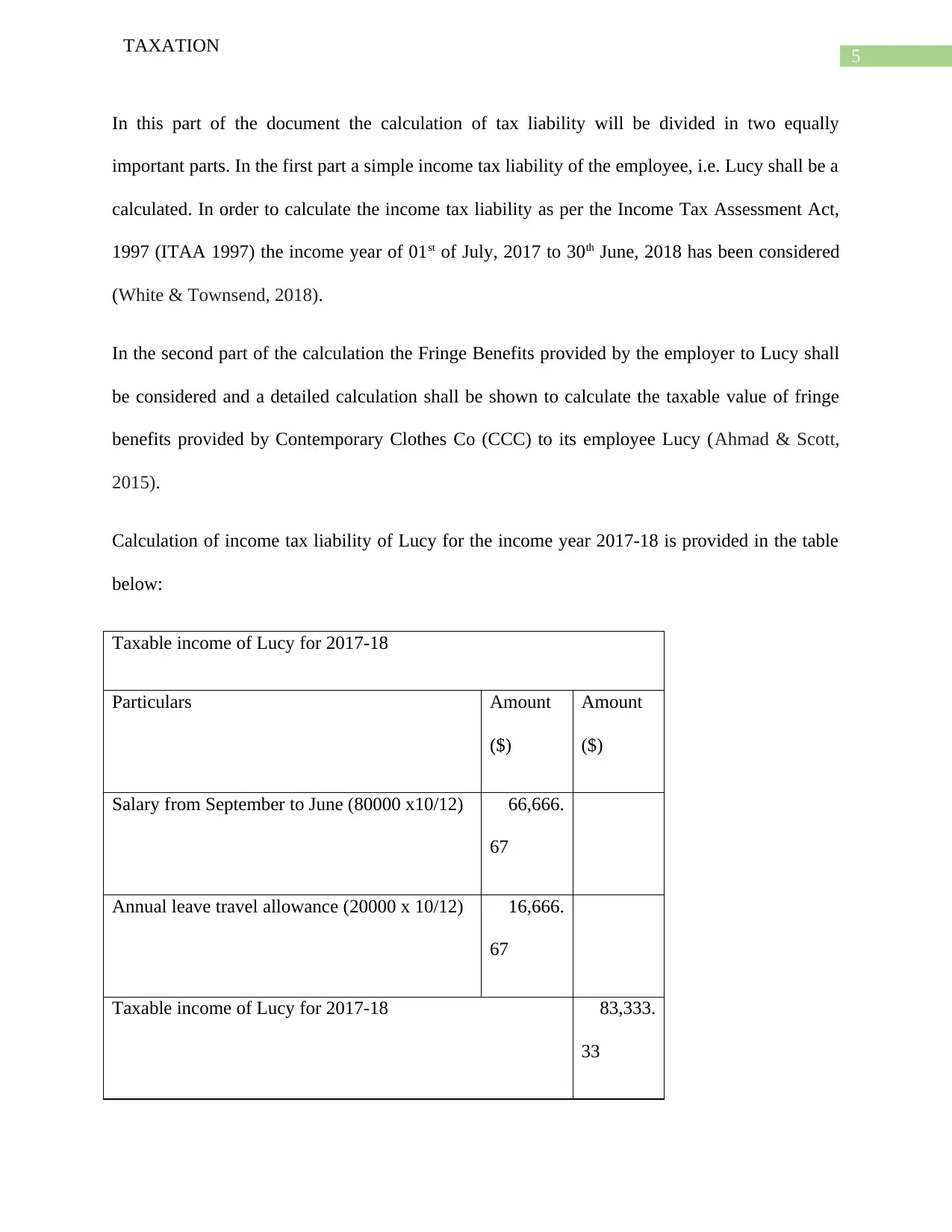

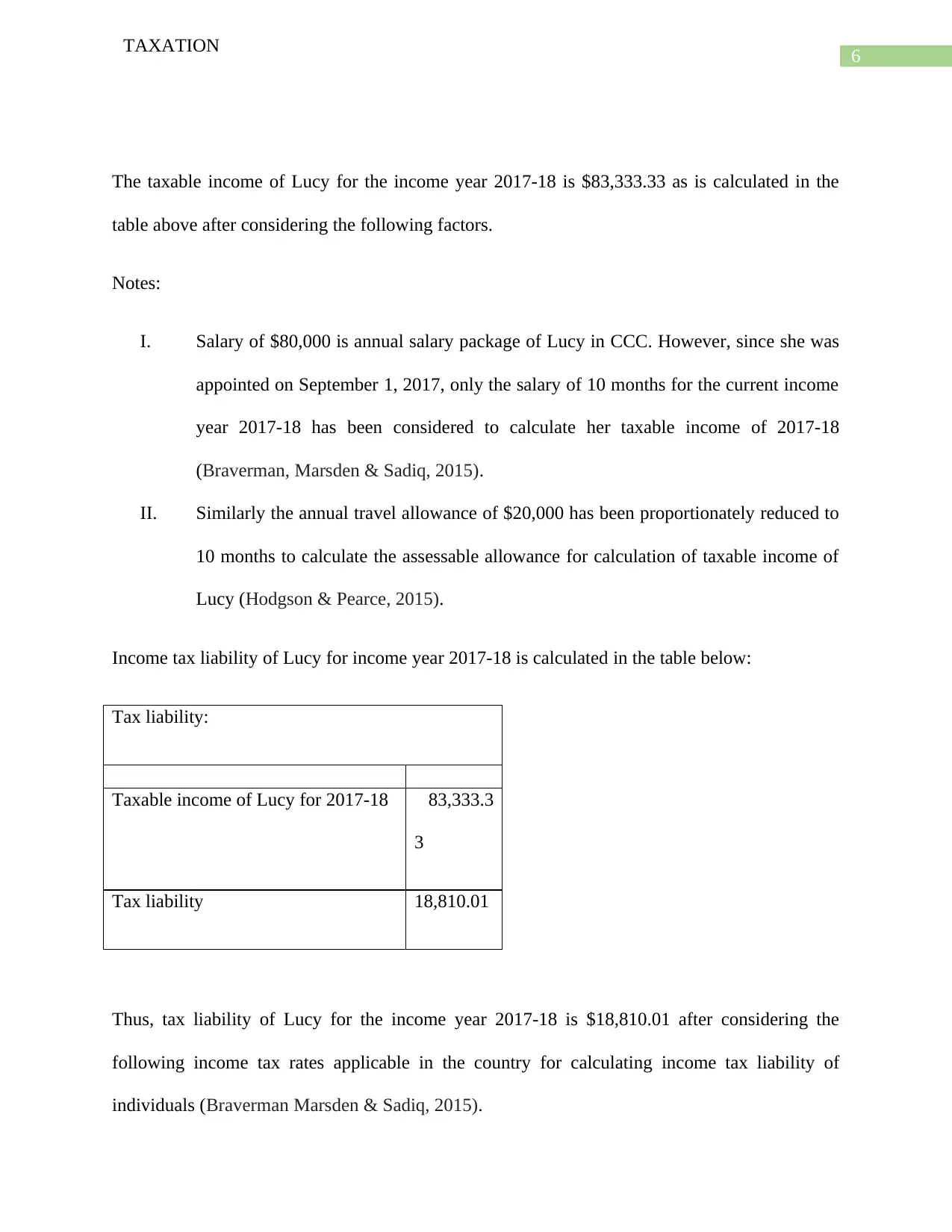

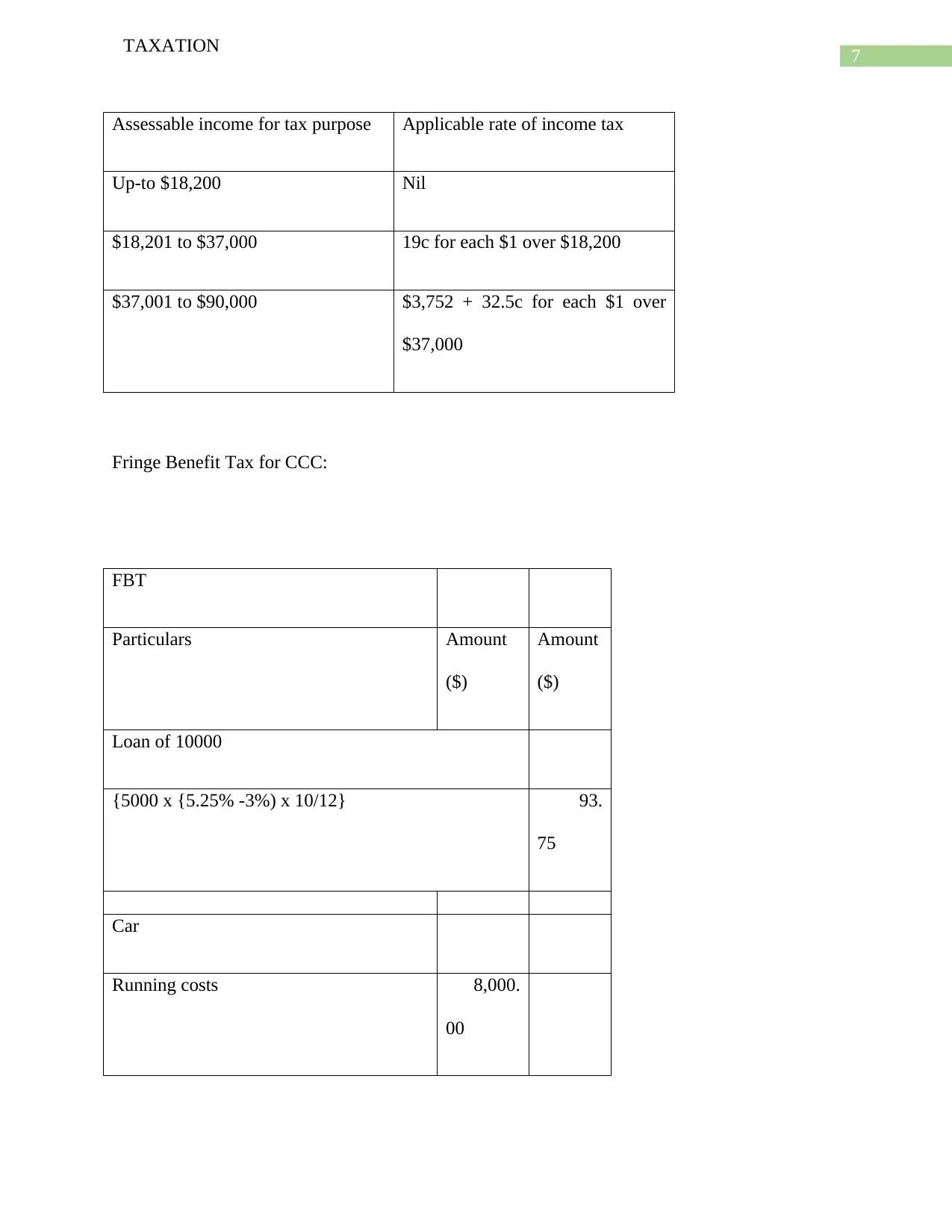

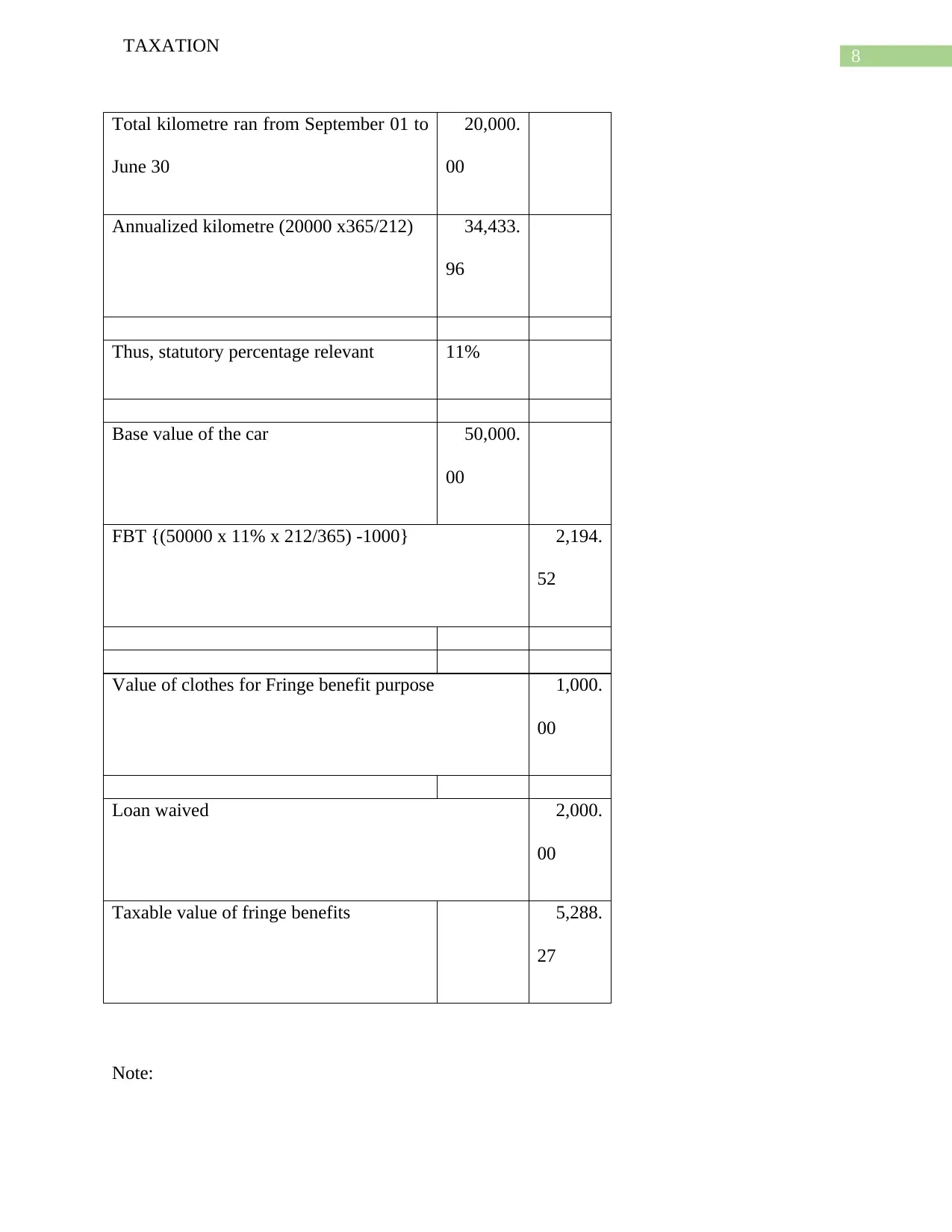

This document presents a detailed analysis of Australian taxation law, specifically addressing the tax implications of share trading and fringe benefits. The assignment begins by examining the tax treatment of a resident individual's losses from share trading, differentiating between holding shares as an investment versus share trading as a business. It references the Income Tax Assessment Act 1997 (ITAA 1997) and relevant ATO guidelines. The second part of the assignment delves into fringe benefits tax (FBT), calculating both an employee's income tax liability and the FBT liability of the employer, Contemporary Clothes Co (CCC). This includes calculations for salary, travel allowances, and various fringe benefits such as loans, car running costs, and clothing provided to the employee. The calculations adhere to the FBT year (April 1 to March 31) and incorporate relevant tax rates and statutory benchmarks. The assignment concludes with a comprehensive list of references.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.