Taxation of Superannuation: Cooper Fund Analysis, Brett and Karen

VerifiedAdded on 2023/03/17

|9

|1883

|32

Homework Assignment

AI Summary

This assignment analyzes the taxation of the Cooper Superannuation Fund for the 2018-2019 income year, exploring both complying and non-complying fund scenarios. It examines the tax implications for two members, Brett (in pension mode) and Karen (in accumulation mode), detailing inflows (superannuation guarantee contributions, personal contributions, dividend income, sale of debentures, and capital gains) and outflows (audit fees, legal fees, and financial advisor fees). The assignment involves preparing tax returns, calculating superannuation fund balances, and explaining the tax treatment of various items under ITAA1997 and the Superannuation Industry (Supervision) Act 1993. The analysis includes calculations of taxable income and tax payable under both scenarios, highlighting the differences in tax rates (15% for complying and 45% for non-complying funds). The assignment also references relevant legislation, rulings, and case law to support the tax treatment of the items.

Running head: TAXATION OF SUPERANNUATION

Taxation of Superannuation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation of Superannuation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION OF SUPERANNUATION

Table of Contents

Part A:..............................................................................................................................................2

Explaining what is complying superannuation fund, while indicating the difference between the

pension and accumulation mode:.....................................................................................................2

Explaining the legislation, ruling and case law how each of those items will be treated for

taxation purposes in 2019:250.........................................................................................................3

Preparing a tax return and superannuation fund balance calculations for both Brett and Karen:...3

Part B:..............................................................................................................................................4

Stating how inflow and cashflow items be treated for tax purposes if the superannuation fund

with non-complying superannuation fund in respect of the 2018-2019 income year:....................4

Including the explanation with reference to specific and legislation from ITAA1997:..................6

References:......................................................................................................................................7

Table of Contents

Part A:..............................................................................................................................................2

Explaining what is complying superannuation fund, while indicating the difference between the

pension and accumulation mode:.....................................................................................................2

Explaining the legislation, ruling and case law how each of those items will be treated for

taxation purposes in 2019:250.........................................................................................................3

Preparing a tax return and superannuation fund balance calculations for both Brett and Karen:...3

Part B:..............................................................................................................................................4

Stating how inflow and cashflow items be treated for tax purposes if the superannuation fund

with non-complying superannuation fund in respect of the 2018-2019 income year:....................4

Including the explanation with reference to specific and legislation from ITAA1997:..................6

References:......................................................................................................................................7

2TAXATION OF SUPERANNUATION

Part A:

Explaining what is complying superannuation fund, while indicating the difference

between the pension and accumulation mode:

There is relevant difference between the superannuation fund pension and accumulation

mode, which could have direct impact on the current tax liability of the individual. The

superannuation fund is relevantly associated with pensions and accumulation mode, which can

help in detecting the total taxable income of the individuals. Moreover, under the taxation

conditions of sections and legislation from ITAA1997 the overall difference in both pension and

accumulation mode. Under the sections and legislation from ITAA1997 the superannuation fund

associated with pension will have no relevant changes on the investments1. In addition, the

individuals could not control the relevant investment of the superannuation pension fund.

Furthermore, employees in the pension fund are not allowed to select relevant investment

decisions, which relevantly reduces the level of investment risk that is been faced by the

employee. As per the sections and legislation from ITAA1997, pension fun is manged by

investment professional, who is responsible to generate higher rate of return in the long run2.

On the other hand, the accumulation mode superannuation fund could directly have direct

impact on the performance of the organisation, where the relevant changes would alter over the

1 Hanrahan, P. A. M. E. L. A. "Legal framework governing aspects of the Australian

superannuation system." Background Paper 25 (2018).

2 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

Part A:

Explaining what is complying superannuation fund, while indicating the difference

between the pension and accumulation mode:

There is relevant difference between the superannuation fund pension and accumulation

mode, which could have direct impact on the current tax liability of the individual. The

superannuation fund is relevantly associated with pensions and accumulation mode, which can

help in detecting the total taxable income of the individuals. Moreover, under the taxation

conditions of sections and legislation from ITAA1997 the overall difference in both pension and

accumulation mode. Under the sections and legislation from ITAA1997 the superannuation fund

associated with pension will have no relevant changes on the investments1. In addition, the

individuals could not control the relevant investment of the superannuation pension fund.

Furthermore, employees in the pension fund are not allowed to select relevant investment

decisions, which relevantly reduces the level of investment risk that is been faced by the

employee. As per the sections and legislation from ITAA1997, pension fun is manged by

investment professional, who is responsible to generate higher rate of return in the long run2.

On the other hand, the accumulation mode superannuation fund could directly have direct

impact on the performance of the organisation, where the relevant changes would alter over the

1 Hanrahan, P. A. M. E. L. A. "Legal framework governing aspects of the Australian

superannuation system." Background Paper 25 (2018).

2 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION OF SUPERANNUATION

period of time. The accumulation mode of superannuation fund under sections and legislation

from ITAA1997 relevantly indicates about the first stage of everyone’s superannuation life. In

addition, the contribution that is made, where relevant locked away phase is started, where the

fund could be accessed until the retirement. In addition, the first stage of the of the accumulation

stage is considered to be retirement phase and second phase is pension phase3.

Explaining the legislation, ruling and case law how each of those items will be treated for

taxation purposes in 2019:250

The relevant legislation, ruling and case law how each of those items will be treated for

taxation purposes in 2019 are depicted as follows.

ITAA1997: Directly states about the Superannuation Industry (Supervision) Act 1993 ss 10

(definitions of ‘superannuation fund’ and ‘regulated superannuation fund’), 19, 42, 62(1)

Superannuation Industry (Supervision) Act 1993: The SIS Act 1993 has mainly indicated that

relevant funds need to be conducted by the individual. There are many different type of

classifying the superannuation fund, which are depicted as follows

o Funds which provide pension benefits • funds which provide lump sum benefits

o Funds which are open to members of the public

o Private funds which are established by an employer for the benefit of its employees

o Government funds (so-called public sector funds)4

o Funds established for people who work in a particular industry (industry funds).

3 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

4 Ingles, David, and Miranda Stewart. "Reforming Australia's Superannuation Tax System and

the Age Pension to Improve Work and Savings Incentives." Asia & the Pacific Policy Studies 4.3

(2017): 417-436.

period of time. The accumulation mode of superannuation fund under sections and legislation

from ITAA1997 relevantly indicates about the first stage of everyone’s superannuation life. In

addition, the contribution that is made, where relevant locked away phase is started, where the

fund could be accessed until the retirement. In addition, the first stage of the of the accumulation

stage is considered to be retirement phase and second phase is pension phase3.

Explaining the legislation, ruling and case law how each of those items will be treated for

taxation purposes in 2019:250

The relevant legislation, ruling and case law how each of those items will be treated for

taxation purposes in 2019 are depicted as follows.

ITAA1997: Directly states about the Superannuation Industry (Supervision) Act 1993 ss 10

(definitions of ‘superannuation fund’ and ‘regulated superannuation fund’), 19, 42, 62(1)

Superannuation Industry (Supervision) Act 1993: The SIS Act 1993 has mainly indicated that

relevant funds need to be conducted by the individual. There are many different type of

classifying the superannuation fund, which are depicted as follows

o Funds which provide pension benefits • funds which provide lump sum benefits

o Funds which are open to members of the public

o Private funds which are established by an employer for the benefit of its employees

o Government funds (so-called public sector funds)4

o Funds established for people who work in a particular industry (industry funds).

3 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

4 Ingles, David, and Miranda Stewart. "Reforming Australia's Superannuation Tax System and

the Age Pension to Improve Work and Savings Incentives." Asia & the Pacific Policy Studies 4.3

(2017): 417-436.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION OF SUPERANNUATION

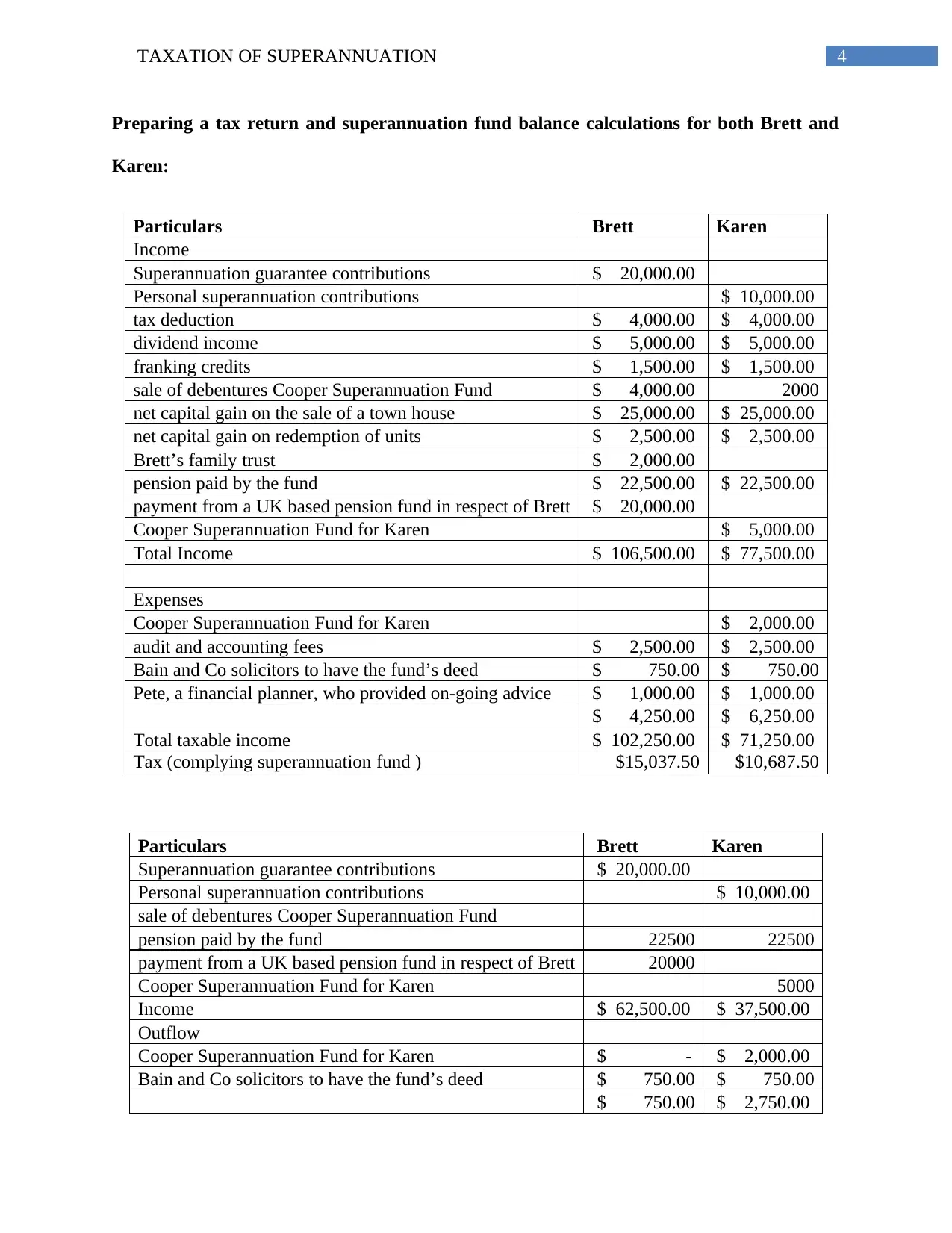

Preparing a tax return and superannuation fund balance calculations for both Brett and

Karen:

Particulars Brett Karen

Income

Superannuation guarantee contributions $ 20,000.00

Personal superannuation contributions $ 10,000.00

tax deduction $ 4,000.00 $ 4,000.00

dividend income $ 5,000.00 $ 5,000.00

franking credits $ 1,500.00 $ 1,500.00

sale of debentures Cooper Superannuation Fund $ 4,000.00 2000

net capital gain on the sale of a town house $ 25,000.00 $ 25,000.00

net capital gain on redemption of units $ 2,500.00 $ 2,500.00

Brett’s family trust $ 2,000.00

pension paid by the fund $ 22,500.00 $ 22,500.00

payment from a UK based pension fund in respect of Brett $ 20,000.00

Cooper Superannuation Fund for Karen $ 5,000.00

Total Income $ 106,500.00 $ 77,500.00

Expenses

Cooper Superannuation Fund for Karen $ 2,000.00

audit and accounting fees $ 2,500.00 $ 2,500.00

Bain and Co solicitors to have the fund’s deed $ 750.00 $ 750.00

Pete, a financial planner, who provided on-going advice $ 1,000.00 $ 1,000.00

$ 4,250.00 $ 6,250.00

Total taxable income $ 102,250.00 $ 71,250.00

Tax (complying superannuation fund ) $15,037.50 $10,687.50

Particulars Brett Karen

Superannuation guarantee contributions $ 20,000.00

Personal superannuation contributions $ 10,000.00

sale of debentures Cooper Superannuation Fund

pension paid by the fund 22500 22500

payment from a UK based pension fund in respect of Brett 20000

Cooper Superannuation Fund for Karen 5000

Income $ 62,500.00 $ 37,500.00

Outflow

Cooper Superannuation Fund for Karen $ - $ 2,000.00

Bain and Co solicitors to have the fund’s deed $ 750.00 $ 750.00

$ 750.00 $ 2,750.00

Preparing a tax return and superannuation fund balance calculations for both Brett and

Karen:

Particulars Brett Karen

Income

Superannuation guarantee contributions $ 20,000.00

Personal superannuation contributions $ 10,000.00

tax deduction $ 4,000.00 $ 4,000.00

dividend income $ 5,000.00 $ 5,000.00

franking credits $ 1,500.00 $ 1,500.00

sale of debentures Cooper Superannuation Fund $ 4,000.00 2000

net capital gain on the sale of a town house $ 25,000.00 $ 25,000.00

net capital gain on redemption of units $ 2,500.00 $ 2,500.00

Brett’s family trust $ 2,000.00

pension paid by the fund $ 22,500.00 $ 22,500.00

payment from a UK based pension fund in respect of Brett $ 20,000.00

Cooper Superannuation Fund for Karen $ 5,000.00

Total Income $ 106,500.00 $ 77,500.00

Expenses

Cooper Superannuation Fund for Karen $ 2,000.00

audit and accounting fees $ 2,500.00 $ 2,500.00

Bain and Co solicitors to have the fund’s deed $ 750.00 $ 750.00

Pete, a financial planner, who provided on-going advice $ 1,000.00 $ 1,000.00

$ 4,250.00 $ 6,250.00

Total taxable income $ 102,250.00 $ 71,250.00

Tax (complying superannuation fund ) $15,037.50 $10,687.50

Particulars Brett Karen

Superannuation guarantee contributions $ 20,000.00

Personal superannuation contributions $ 10,000.00

sale of debentures Cooper Superannuation Fund

pension paid by the fund 22500 22500

payment from a UK based pension fund in respect of Brett 20000

Cooper Superannuation Fund for Karen 5000

Income $ 62,500.00 $ 37,500.00

Outflow

Cooper Superannuation Fund for Karen $ - $ 2,000.00

Bain and Co solicitors to have the fund’s deed $ 750.00 $ 750.00

$ 750.00 $ 2,750.00

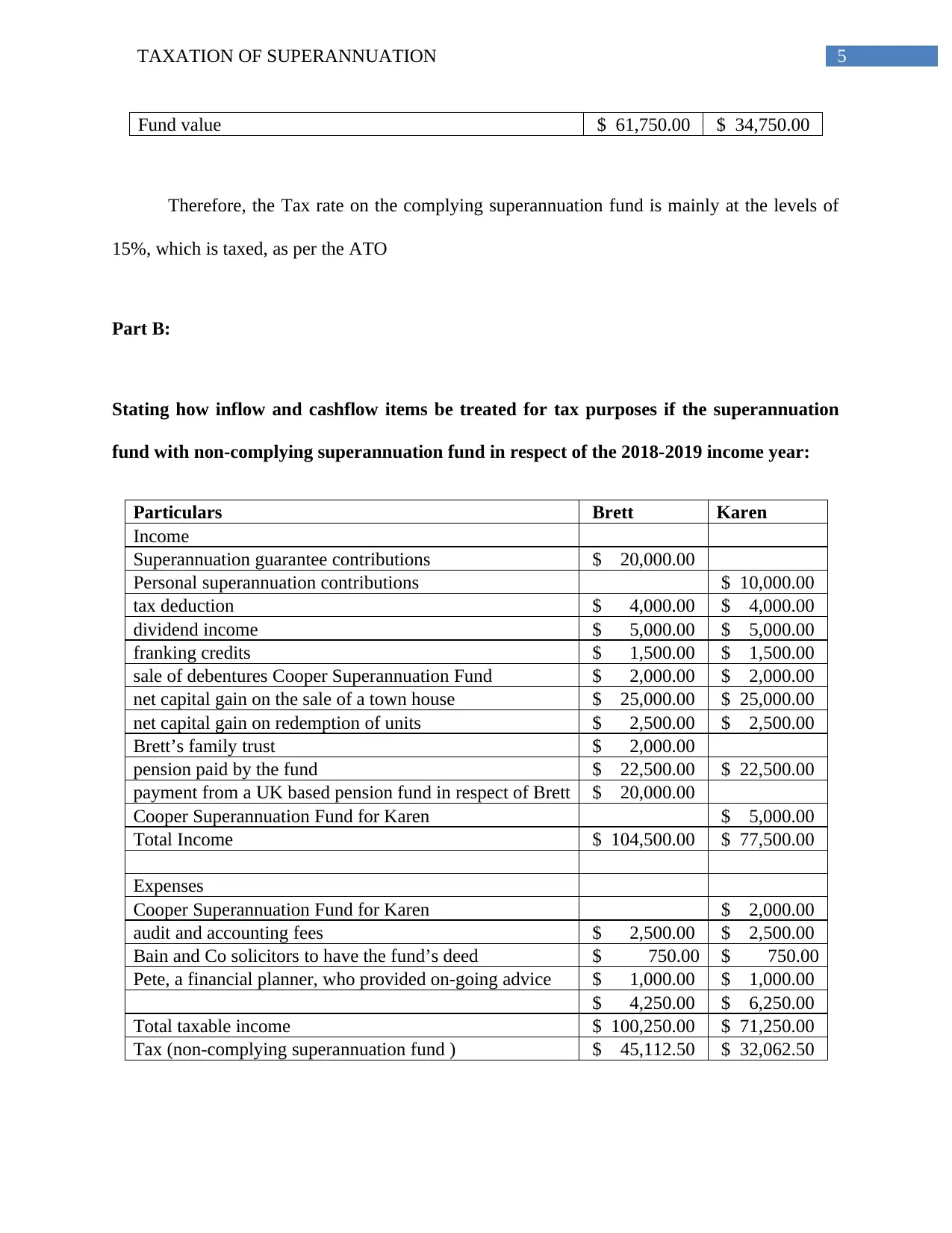

5TAXATION OF SUPERANNUATION

Fund value $ 61,750.00 $ 34,750.00

Therefore, the Tax rate on the complying superannuation fund is mainly at the levels of

15%, which is taxed, as per the ATO

Part B:

Stating how inflow and cashflow items be treated for tax purposes if the superannuation

fund with non-complying superannuation fund in respect of the 2018-2019 income year:

Particulars Brett Karen

Income

Superannuation guarantee contributions $ 20,000.00

Personal superannuation contributions $ 10,000.00

tax deduction $ 4,000.00 $ 4,000.00

dividend income $ 5,000.00 $ 5,000.00

franking credits $ 1,500.00 $ 1,500.00

sale of debentures Cooper Superannuation Fund $ 2,000.00 $ 2,000.00

net capital gain on the sale of a town house $ 25,000.00 $ 25,000.00

net capital gain on redemption of units $ 2,500.00 $ 2,500.00

Brett’s family trust $ 2,000.00

pension paid by the fund $ 22,500.00 $ 22,500.00

payment from a UK based pension fund in respect of Brett $ 20,000.00

Cooper Superannuation Fund for Karen $ 5,000.00

Total Income $ 104,500.00 $ 77,500.00

Expenses

Cooper Superannuation Fund for Karen $ 2,000.00

audit and accounting fees $ 2,500.00 $ 2,500.00

Bain and Co solicitors to have the fund’s deed $ 750.00 $ 750.00

Pete, a financial planner, who provided on-going advice $ 1,000.00 $ 1,000.00

$ 4,250.00 $ 6,250.00

Total taxable income $ 100,250.00 $ 71,250.00

Tax (non-complying superannuation fund ) $ 45,112.50 $ 32,062.50

Fund value $ 61,750.00 $ 34,750.00

Therefore, the Tax rate on the complying superannuation fund is mainly at the levels of

15%, which is taxed, as per the ATO

Part B:

Stating how inflow and cashflow items be treated for tax purposes if the superannuation

fund with non-complying superannuation fund in respect of the 2018-2019 income year:

Particulars Brett Karen

Income

Superannuation guarantee contributions $ 20,000.00

Personal superannuation contributions $ 10,000.00

tax deduction $ 4,000.00 $ 4,000.00

dividend income $ 5,000.00 $ 5,000.00

franking credits $ 1,500.00 $ 1,500.00

sale of debentures Cooper Superannuation Fund $ 2,000.00 $ 2,000.00

net capital gain on the sale of a town house $ 25,000.00 $ 25,000.00

net capital gain on redemption of units $ 2,500.00 $ 2,500.00

Brett’s family trust $ 2,000.00

pension paid by the fund $ 22,500.00 $ 22,500.00

payment from a UK based pension fund in respect of Brett $ 20,000.00

Cooper Superannuation Fund for Karen $ 5,000.00

Total Income $ 104,500.00 $ 77,500.00

Expenses

Cooper Superannuation Fund for Karen $ 2,000.00

audit and accounting fees $ 2,500.00 $ 2,500.00

Bain and Co solicitors to have the fund’s deed $ 750.00 $ 750.00

Pete, a financial planner, who provided on-going advice $ 1,000.00 $ 1,000.00

$ 4,250.00 $ 6,250.00

Total taxable income $ 100,250.00 $ 71,250.00

Tax (non-complying superannuation fund ) $ 45,112.50 $ 32,062.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION OF SUPERANNUATION

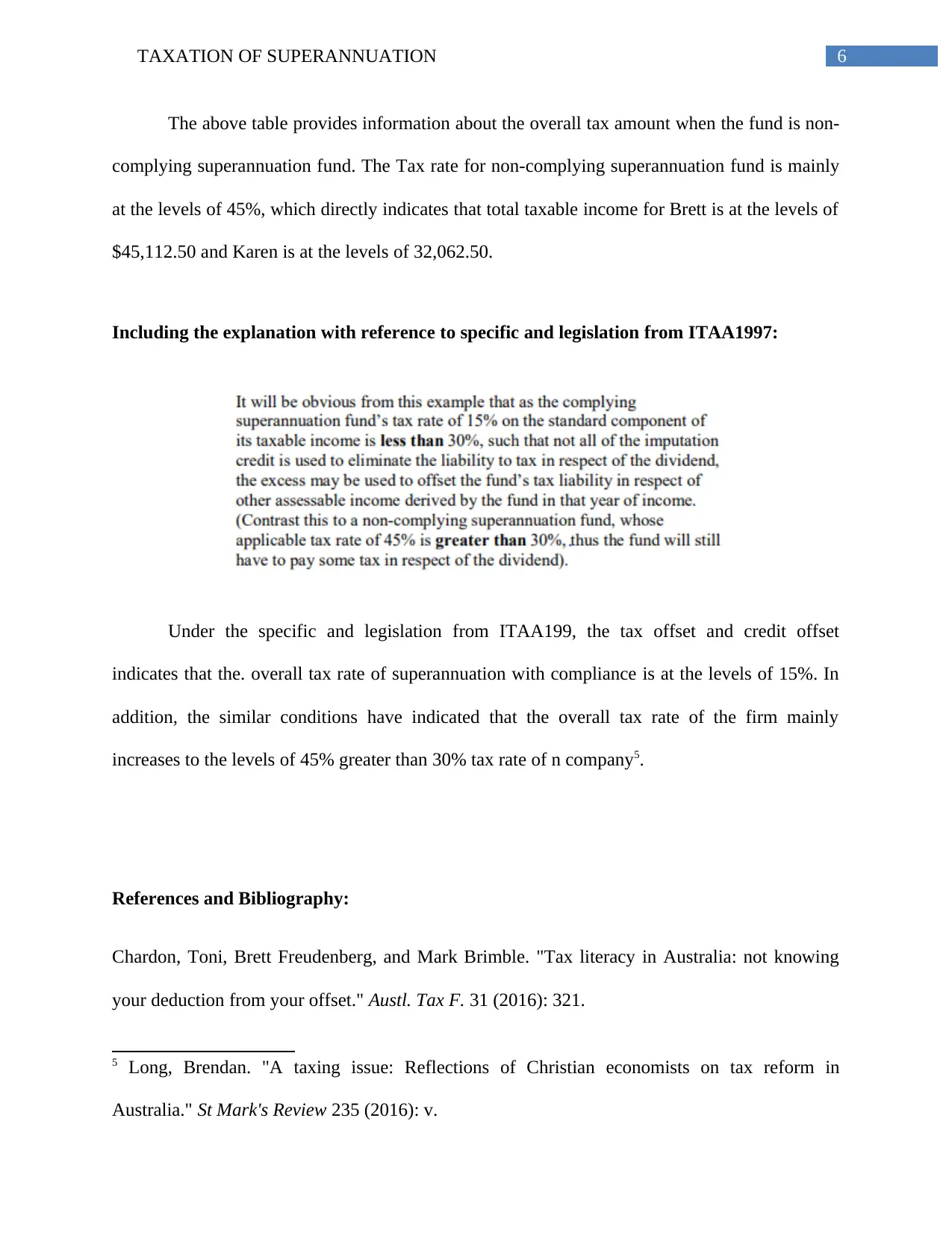

The above table provides information about the overall tax amount when the fund is non-

complying superannuation fund. The Tax rate for non-complying superannuation fund is mainly

at the levels of 45%, which directly indicates that total taxable income for Brett is at the levels of

$45,112.50 and Karen is at the levels of 32,062.50.

Including the explanation with reference to specific and legislation from ITAA1997:

Under the specific and legislation from ITAA199, the tax offset and credit offset

indicates that the. overall tax rate of superannuation with compliance is at the levels of 15%. In

addition, the similar conditions have indicated that the overall tax rate of the firm mainly

increases to the levels of 45% greater than 30% tax rate of n company5.

References and Bibliography:

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

5 Long, Brendan. "A taxing issue: Reflections of Christian economists on tax reform in

Australia." St Mark's Review 235 (2016): v.

The above table provides information about the overall tax amount when the fund is non-

complying superannuation fund. The Tax rate for non-complying superannuation fund is mainly

at the levels of 45%, which directly indicates that total taxable income for Brett is at the levels of

$45,112.50 and Karen is at the levels of 32,062.50.

Including the explanation with reference to specific and legislation from ITAA1997:

Under the specific and legislation from ITAA199, the tax offset and credit offset

indicates that the. overall tax rate of superannuation with compliance is at the levels of 15%. In

addition, the similar conditions have indicated that the overall tax rate of the firm mainly

increases to the levels of 45% greater than 30% tax rate of n company5.

References and Bibliography:

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

5 Long, Brendan. "A taxing issue: Reflections of Christian economists on tax reform in

Australia." St Mark's Review 235 (2016): v.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION OF SUPERANNUATION

Chardon, Toni, Mark Brimble, and Brett Freudenberg. "Tax and superannuation literacy:

Australian and New Zealand perspectives." (2016).

Edmonds, Mark, Christian Holle, and Wendy Hartanti. "Alternative assets insights: Super funds-

tax impediments to going global." Taxation in Australia 49.7 (2015): 413.

Evans, John, and Abdul Razeed. "An Analysis of the Australian Superannuation System's Taxes

and Transfers." Economic Papers: A journal of applied economics and policy37.3 (2018): 299-

312.

Hanrahan, P. A. M. E. L. A. "Legal framework governing aspects of the Australian

superannuation system." Background Paper 25 (2018).

Hellwig, Timothy, and Ian McAllister. "The impact of economic assets on party choice in

Australia." Journal of Elections, Public Opinion and Parties 28.4 (2018): 516-534.

Ingles, David, and Miranda Stewart. "Reforming Australia's Superannuation Tax System and the

Age Pension to Improve Work and Savings Incentives." Asia & the Pacific Policy Studies 4.3

(2017): 417-436.

Ingram, Paul. "Is your unit trust a." Bulletin (Law Society of South Australia) 40.5 (2018): 32.

Joseph, Sally-Ann. "An Examination of the Congruence of the Mining Site Rehabilitation Tax

Deductions & Queensland's Chain of Responsibility Legislation." AJEL (2017): 29.

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Chardon, Toni, Mark Brimble, and Brett Freudenberg. "Tax and superannuation literacy:

Australian and New Zealand perspectives." (2016).

Edmonds, Mark, Christian Holle, and Wendy Hartanti. "Alternative assets insights: Super funds-

tax impediments to going global." Taxation in Australia 49.7 (2015): 413.

Evans, John, and Abdul Razeed. "An Analysis of the Australian Superannuation System's Taxes

and Transfers." Economic Papers: A journal of applied economics and policy37.3 (2018): 299-

312.

Hanrahan, P. A. M. E. L. A. "Legal framework governing aspects of the Australian

superannuation system." Background Paper 25 (2018).

Hellwig, Timothy, and Ian McAllister. "The impact of economic assets on party choice in

Australia." Journal of Elections, Public Opinion and Parties 28.4 (2018): 516-534.

Ingles, David, and Miranda Stewart. "Reforming Australia's Superannuation Tax System and the

Age Pension to Improve Work and Savings Incentives." Asia & the Pacific Policy Studies 4.3

(2017): 417-436.

Ingram, Paul. "Is your unit trust a." Bulletin (Law Society of South Australia) 40.5 (2018): 32.

Joseph, Sally-Ann. "An Examination of the Congruence of the Mining Site Rehabilitation Tax

Deductions & Queensland's Chain of Responsibility Legislation." AJEL (2017): 29.

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

8TAXATION OF SUPERANNUATION

Long, Brendan. "A taxing issue: Reflections of Christian economists on tax reform in

Australia." St Mark's Review 235 (2016): v.

Sy, Wilson N. "Financial Performance Trends of Australian Superannuation: System and

Sectors." (2018).

Long, Brendan. "A taxing issue: Reflections of Christian economists on tax reform in

Australia." St Mark's Review 235 (2016): v.

Sy, Wilson N. "Financial Performance Trends of Australian Superannuation: System and

Sectors." (2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.