Taxation Principles Report: Assessment of Daniel and Joyce's Taxation

VerifiedAdded on 2020/06/04

|11

|3189

|48

Report

AI Summary

This report delves into Australian taxation principles, focusing on the tax implications for two individuals, Daniel and Joyce. It begins by determining Daniel's residential status, assessing whether he's a resident or non-resident for tax purposes based on various tests like the domicile test, 183-day test, and superannuation test. The report then calculates Daniel's tax payable, considering his income from various sources, allowable deductions, and the applicable tax rates. A detailed income statement is provided, outlining revenue, deductions, and the final tax liability. Furthermore, the report discusses Daniel's tax consequences in the 2017/18 assessment year, taking into account his potential relocation and changes in income. The second part of the report analyzes the tax implications for Joyce, focusing on FBT or income tax, and calculating her FBT liability. It examines her income statement, including salary, bonuses, and various deductions, and calculates her net assessable income and tax payable. The report also offers advice to Escape Vacations regarding tax implications and liabilities, including recommendations for reducing tax burdens. The report uses various sections, laws, acts, and legislation to make the fair taxation in the country.

TAXATION PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

1. Residential status of Daniel as resident or non resident for tax purpose............................1

2. Calculation tax payable for Daniel.....................................................................................3

3. Discussion over Daniel's tax consequences in 2017/18.....................................................4

QUESTION 2...................................................................................................................................5

A.............................................................................................................................................5

1. Analysing the tax implication of FBT or Income tax....................................................5

2.Calculation FBT liability for Joyce................................................................................7

B.............................................................................................................................................7

1.Advising Escape Vacations over tax implication...........................................................7

2.Calculating tax liabilities for Escape Vacations.............................................................7

3.Advising Escape Vacations to reduce the tax liability...................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

1. Residential status of Daniel as resident or non resident for tax purpose............................1

2. Calculation tax payable for Daniel.....................................................................................3

3. Discussion over Daniel's tax consequences in 2017/18.....................................................4

QUESTION 2...................................................................................................................................5

A.............................................................................................................................................5

1. Analysing the tax implication of FBT or Income tax....................................................5

2.Calculation FBT liability for Joyce................................................................................7

B.............................................................................................................................................7

1.Advising Escape Vacations over tax implication...........................................................7

2.Calculating tax liabilities for Escape Vacations.............................................................7

3.Advising Escape Vacations to reduce the tax liability...................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Taxation proceeds as to make fruitful legislation over income or revenue generated by

individual as well as corporations. Taxes are in force by ATO and federal register of legislation

which contains various sections, laws, acts as well as legislation to make the fair taxation in

country. In the present report, Daniel and Joyce are the two individuals who are earning through

Australian sources as well as they are also making payments of taxes over their income.

However, with the help of various deductions or exemptions they will be liable to claim several

incomes or expenses. There has been calculations for FBT and tax liabilities as well as allowable

reductions

QUESTION 1

1. Residential status of Daniel as resident or non resident for tax purpose

Daniel is a Malaysian resident and moved America for work purpose in the Mining

capital corporation (Vann, 2016). He than moved to Australia for working in franchisee of the

same organisation on 1st November 2016. As per the Australian legislation authorities, for being

a resident in Australia one has to pass the several tests such as:

Domicile test: Under this test an individual should have taken birth in Australia and must

have acquired the permanent residency (Miller and Oats, 2016). As per the scenario, Daniel is a

Malaysian resident and has the native home there so, I this case he is denoted as the non-resident

in Australia and would not be liable to make payment of taxes.

183 Days test: As per conditions contained it this test is that, an individual must have

stayed for more than or equal to 183 days in Australia. The persona must have completed 183

days in Australian territory may be in alteration or frequent visits within the assessable year

(Tran, 2015). Daniel will be eligible for making the tax payments as he has acquired joined

Australian company in 1st November 2016, which is taxable year of 1st July 2016 to 30th June

2017. He has passed the conditions implicated in this test and will be liable to make payments for

taxes.

Superannuation test: In this test, ATO1 has made the condition that if a person is

employed in Australia and has the superannuation benefits from Australian government will be

liable to pay tax (Pearce, 2014). Daniel has employment in American originated company's

1 Australian Taxation Office

1

Taxation proceeds as to make fruitful legislation over income or revenue generated by

individual as well as corporations. Taxes are in force by ATO and federal register of legislation

which contains various sections, laws, acts as well as legislation to make the fair taxation in

country. In the present report, Daniel and Joyce are the two individuals who are earning through

Australian sources as well as they are also making payments of taxes over their income.

However, with the help of various deductions or exemptions they will be liable to claim several

incomes or expenses. There has been calculations for FBT and tax liabilities as well as allowable

reductions

QUESTION 1

1. Residential status of Daniel as resident or non resident for tax purpose

Daniel is a Malaysian resident and moved America for work purpose in the Mining

capital corporation (Vann, 2016). He than moved to Australia for working in franchisee of the

same organisation on 1st November 2016. As per the Australian legislation authorities, for being

a resident in Australia one has to pass the several tests such as:

Domicile test: Under this test an individual should have taken birth in Australia and must

have acquired the permanent residency (Miller and Oats, 2016). As per the scenario, Daniel is a

Malaysian resident and has the native home there so, I this case he is denoted as the non-resident

in Australia and would not be liable to make payment of taxes.

183 Days test: As per conditions contained it this test is that, an individual must have

stayed for more than or equal to 183 days in Australia. The persona must have completed 183

days in Australian territory may be in alteration or frequent visits within the assessable year

(Tran, 2015). Daniel will be eligible for making the tax payments as he has acquired joined

Australian company in 1st November 2016, which is taxable year of 1st July 2016 to 30th June

2017. He has passed the conditions implicated in this test and will be liable to make payments for

taxes.

Superannuation test: In this test, ATO1 has made the condition that if a person is

employed in Australia and has the superannuation benefits from Australian government will be

liable to pay tax (Pearce, 2014). Daniel has employment in American originated company's

1 Australian Taxation Office

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

franchisee in Australia. This firm has made the annual payment of 250000 of salary with

superannuation benefits to him. In this case can claim deductions over superannuation but he is

also liable to make tax payments.

TR 98/17: As per this taxation ruling, an individual can acquired residential status in

Australia on the basis of several terms like:

The individual should be migrant from Australia, as he has taken birth in the national

territory and living outside the country (Kreiser and et al., 2014).

Students acquiring visa for studying in Australian university, schools or colleges.

Teaching such as professor or lecturer like guest faculty in any educational institution

were also denoted as the Australian resident.

Tourists or the temporary visitors in Australia, they are also known as the residents.

A person is employed in any Australian company on the basis of contract will also be

denoted as the resident for tax purposes.

On the basis of above condition in TR 98/17, Daniel comes under condition of

employment in Australia. As per norms set by ATO he can be denoted as the Australian resident

and is liable to make payments of tax over his assessable income.

Section (6)2: This section is related with the conditions and various legislation over

assessable income of residents or visitors in Australia. It will be fruitful in understanding the

terms and conditions for acquiring the residential stratus in Australia. Daniel has been employed

in ans Australian firm as well as generating income from there, so he will be liable to make the

tax payments (Dumiter and et.al., 2016). He has generated income through Australian sources as

well as from his rented property at Malaysia which has deposition of payments in Australian

bank. Daniel; is also receiving the annual interests from both the banks and has income through

dividends or incentives, so he is liable to make payments for the taxes over his generated income.

As per above mentioned various terms, laws, sections or ruling awarded by ATO in

context with residential status of Daniel, he can be denoted as resident in some terms as well as

non resident. As per residential test he has fulfilled the conditions of two aspects such as 183

2 Income tax assessment act, 1936

2

superannuation benefits to him. In this case can claim deductions over superannuation but he is

also liable to make tax payments.

TR 98/17: As per this taxation ruling, an individual can acquired residential status in

Australia on the basis of several terms like:

The individual should be migrant from Australia, as he has taken birth in the national

territory and living outside the country (Kreiser and et al., 2014).

Students acquiring visa for studying in Australian university, schools or colleges.

Teaching such as professor or lecturer like guest faculty in any educational institution

were also denoted as the Australian resident.

Tourists or the temporary visitors in Australia, they are also known as the residents.

A person is employed in any Australian company on the basis of contract will also be

denoted as the resident for tax purposes.

On the basis of above condition in TR 98/17, Daniel comes under condition of

employment in Australia. As per norms set by ATO he can be denoted as the Australian resident

and is liable to make payments of tax over his assessable income.

Section (6)2: This section is related with the conditions and various legislation over

assessable income of residents or visitors in Australia. It will be fruitful in understanding the

terms and conditions for acquiring the residential stratus in Australia. Daniel has been employed

in ans Australian firm as well as generating income from there, so he will be liable to make the

tax payments (Dumiter and et.al., 2016). He has generated income through Australian sources as

well as from his rented property at Malaysia which has deposition of payments in Australian

bank. Daniel; is also receiving the annual interests from both the banks and has income through

dividends or incentives, so he is liable to make payments for the taxes over his generated income.

As per above mentioned various terms, laws, sections or ruling awarded by ATO in

context with residential status of Daniel, he can be denoted as resident in some terms as well as

non resident. As per residential test he has fulfilled the conditions of two aspects such as 183

2 Income tax assessment act, 1936

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

days test and superannuation. Where he has denoted as an Australian resident for making the tax

payments (Frecknall-Hughes, 2014). Taxation ruling for the residential status, Daniel has

acquired the last condition such as he has been employed in the Australian Company and having

revenue benefits from it. As in section 6 of ITAA36 he can be denoted as the resident in

Australia on the basis of receiving income or earning through Australian sources as well as from

other countries.

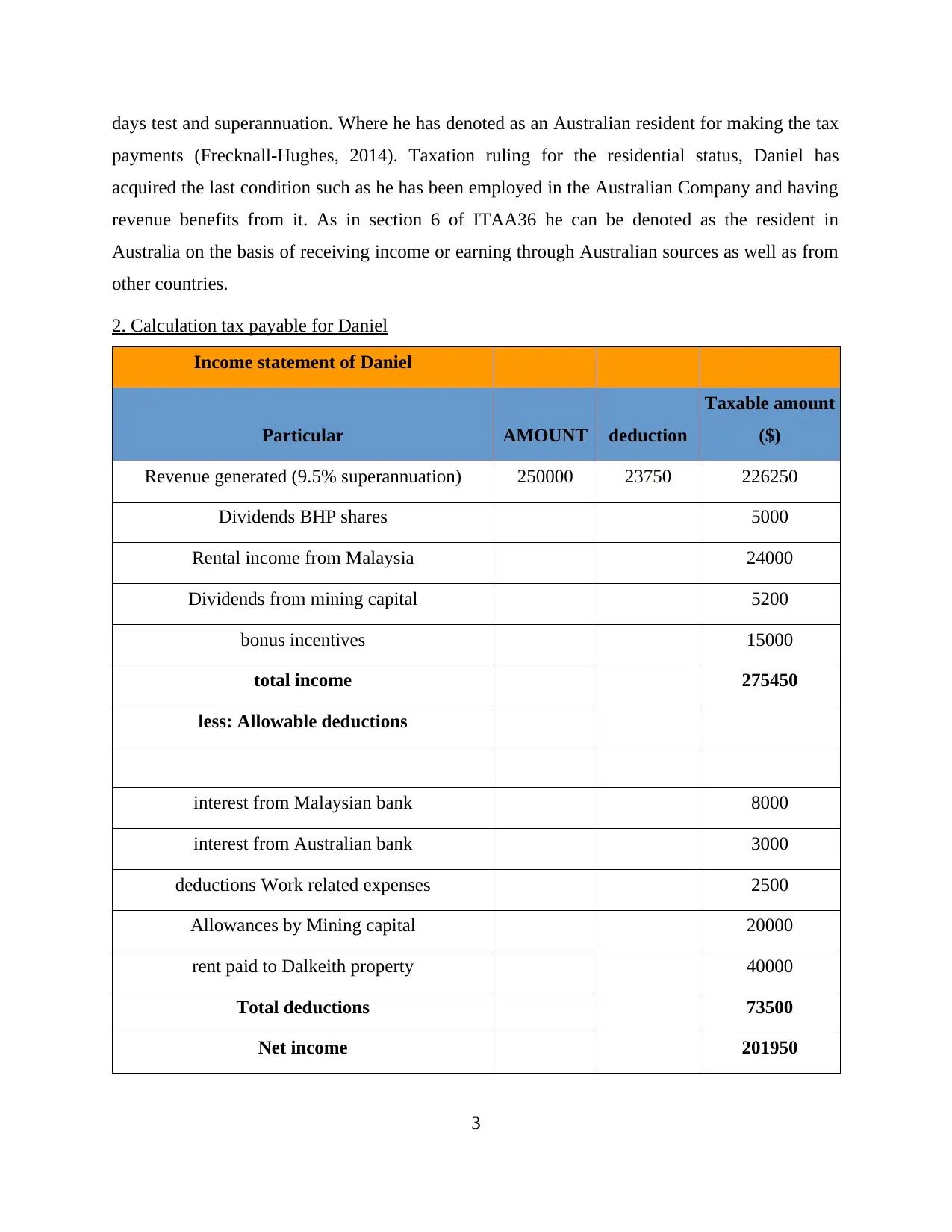

2. Calculation tax payable for Daniel

Income statement of Daniel

Particular AMOUNT deduction

Taxable amount

($)

Revenue generated (9.5% superannuation) 250000 23750 226250

Dividends BHP shares 5000

Rental income from Malaysia 24000

Dividends from mining capital 5200

bonus incentives 15000

total income 275450

less: Allowable deductions

interest from Malaysian bank 8000

interest from Australian bank 3000

deductions Work related expenses 2500

Allowances by Mining capital 20000

rent paid to Dalkeith property 40000

Total deductions 73500

Net income 201950

3

payments (Frecknall-Hughes, 2014). Taxation ruling for the residential status, Daniel has

acquired the last condition such as he has been employed in the Australian Company and having

revenue benefits from it. As in section 6 of ITAA36 he can be denoted as the resident in

Australia on the basis of receiving income or earning through Australian sources as well as from

other countries.

2. Calculation tax payable for Daniel

Income statement of Daniel

Particular AMOUNT deduction

Taxable amount

($)

Revenue generated (9.5% superannuation) 250000 23750 226250

Dividends BHP shares 5000

Rental income from Malaysia 24000

Dividends from mining capital 5200

bonus incentives 15000

total income 275450

less: Allowable deductions

interest from Malaysian bank 8000

interest from Australian bank 3000

deductions Work related expenses 2500

Allowances by Mining capital 20000

rent paid to Dalkeith property 40000

Total deductions 73500

Net income 201950

3

Franking credits 2142

net assessable income 199808

less: tax (45%) 89913.6

54232

Taxable payments 144145.6

Interpretation: Present calculation is based on the assessable income generated by Daniel

through his employment at Australia as well as through dividends, rental income and bonus

through his company. Daniel has the annual income of $250000 with the superannuation scheme

which was facilitated by Mining capital corporation. The rate over superannuation is 9.5% so it

will be exempted from his taxable income and has the revenue for $226250. Further addition to

be made by Daniel as he has gains through dividends from shares as well as from Mining capital

for $5000 and $5200. He has surplus in income with rent received from Malaysian property, this

amount is fully taxable as it has the monthly revenue for 2000 and the allowable deduction over

rent is $1500, so this will be taxable. He was allowed exemption over several incomes and

expenses which is total of $73500, it will be deductible from the total income and brings the

assessable income of $199808. Thus, these amount of income fall in to the 45% of taxation slab

by adding $54232 the amount will be tax payable by him is $144145.6. He will not been

benefited with Medicare levy of 2% because he is not an Australian resident. The Medicare levy

is awarded by Australian government as give cure and medical benefits such as, heath and safety

as well as security to its citizens.

3. Discussion over Daniel's tax consequences in 2017/18

Daniel paid taxes in the assessment year 2016-2017, he has generated taxable payment

for $144145.6. It can be assumed that he will be earning the same income in 2017-18 amounted

at $250000 along with the superannuation paid by his employer. The super annunciation scheme

is facilitated by Australian legislative to citizens as to give them monetary benefits after

retirement. In June 2017 the mining company has the downturn and its planing to close all the

subsidiary companies to over come with the losses. Daniel is planning to move back to his native

country Malaysia along with his wife and son. They will leave Australia after September 2017,

4

net assessable income 199808

less: tax (45%) 89913.6

54232

Taxable payments 144145.6

Interpretation: Present calculation is based on the assessable income generated by Daniel

through his employment at Australia as well as through dividends, rental income and bonus

through his company. Daniel has the annual income of $250000 with the superannuation scheme

which was facilitated by Mining capital corporation. The rate over superannuation is 9.5% so it

will be exempted from his taxable income and has the revenue for $226250. Further addition to

be made by Daniel as he has gains through dividends from shares as well as from Mining capital

for $5000 and $5200. He has surplus in income with rent received from Malaysian property, this

amount is fully taxable as it has the monthly revenue for 2000 and the allowable deduction over

rent is $1500, so this will be taxable. He was allowed exemption over several incomes and

expenses which is total of $73500, it will be deductible from the total income and brings the

assessable income of $199808. Thus, these amount of income fall in to the 45% of taxation slab

by adding $54232 the amount will be tax payable by him is $144145.6. He will not been

benefited with Medicare levy of 2% because he is not an Australian resident. The Medicare levy

is awarded by Australian government as give cure and medical benefits such as, heath and safety

as well as security to its citizens.

3. Discussion over Daniel's tax consequences in 2017/18

Daniel paid taxes in the assessment year 2016-2017, he has generated taxable payment

for $144145.6. It can be assumed that he will be earning the same income in 2017-18 amounted

at $250000 along with the superannuation paid by his employer. The super annunciation scheme

is facilitated by Australian legislative to citizens as to give them monetary benefits after

retirement. In June 2017 the mining company has the downturn and its planing to close all the

subsidiary companies to over come with the losses. Daniel is planning to move back to his native

country Malaysia along with his wife and son. They will leave Australia after September 2017,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

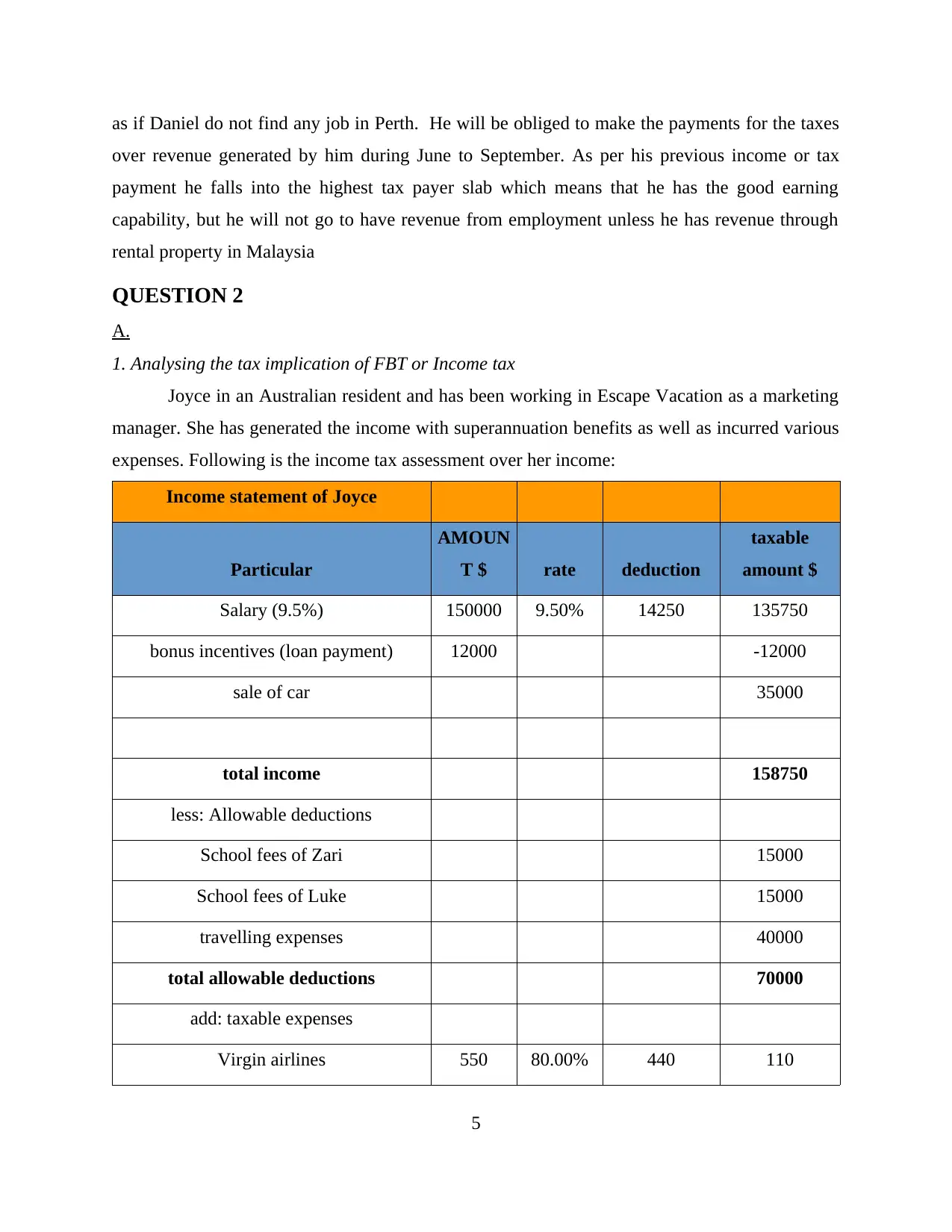

as if Daniel do not find any job in Perth. He will be obliged to make the payments for the taxes

over revenue generated by him during June to September. As per his previous income or tax

payment he falls into the highest tax payer slab which means that he has the good earning

capability, but he will not go to have revenue from employment unless he has revenue through

rental property in Malaysia

QUESTION 2

A.

1. Analysing the tax implication of FBT or Income tax

Joyce in an Australian resident and has been working in Escape Vacation as a marketing

manager. She has generated the income with superannuation benefits as well as incurred various

expenses. Following is the income tax assessment over her income:

Income statement of Joyce

Particular

AMOUN

T $ rate deduction

taxable

amount $

Salary (9.5%) 150000 9.50% 14250 135750

bonus incentives (loan payment) 12000 -12000

sale of car 35000

total income 158750

less: Allowable deductions

School fees of Zari 15000

School fees of Luke 15000

travelling expenses 40000

total allowable deductions 70000

add: taxable expenses

Virgin airlines 550 80.00% 440 110

5

over revenue generated by him during June to September. As per his previous income or tax

payment he falls into the highest tax payer slab which means that he has the good earning

capability, but he will not go to have revenue from employment unless he has revenue through

rental property in Malaysia

QUESTION 2

A.

1. Analysing the tax implication of FBT or Income tax

Joyce in an Australian resident and has been working in Escape Vacation as a marketing

manager. She has generated the income with superannuation benefits as well as incurred various

expenses. Following is the income tax assessment over her income:

Income statement of Joyce

Particular

AMOUN

T $ rate deduction

taxable

amount $

Salary (9.5%) 150000 9.50% 14250 135750

bonus incentives (loan payment) 12000 -12000

sale of car 35000

total income 158750

less: Allowable deductions

School fees of Zari 15000

School fees of Luke 15000

travelling expenses 40000

total allowable deductions 70000

add: taxable expenses

Virgin airlines 550 80.00% 440 110

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

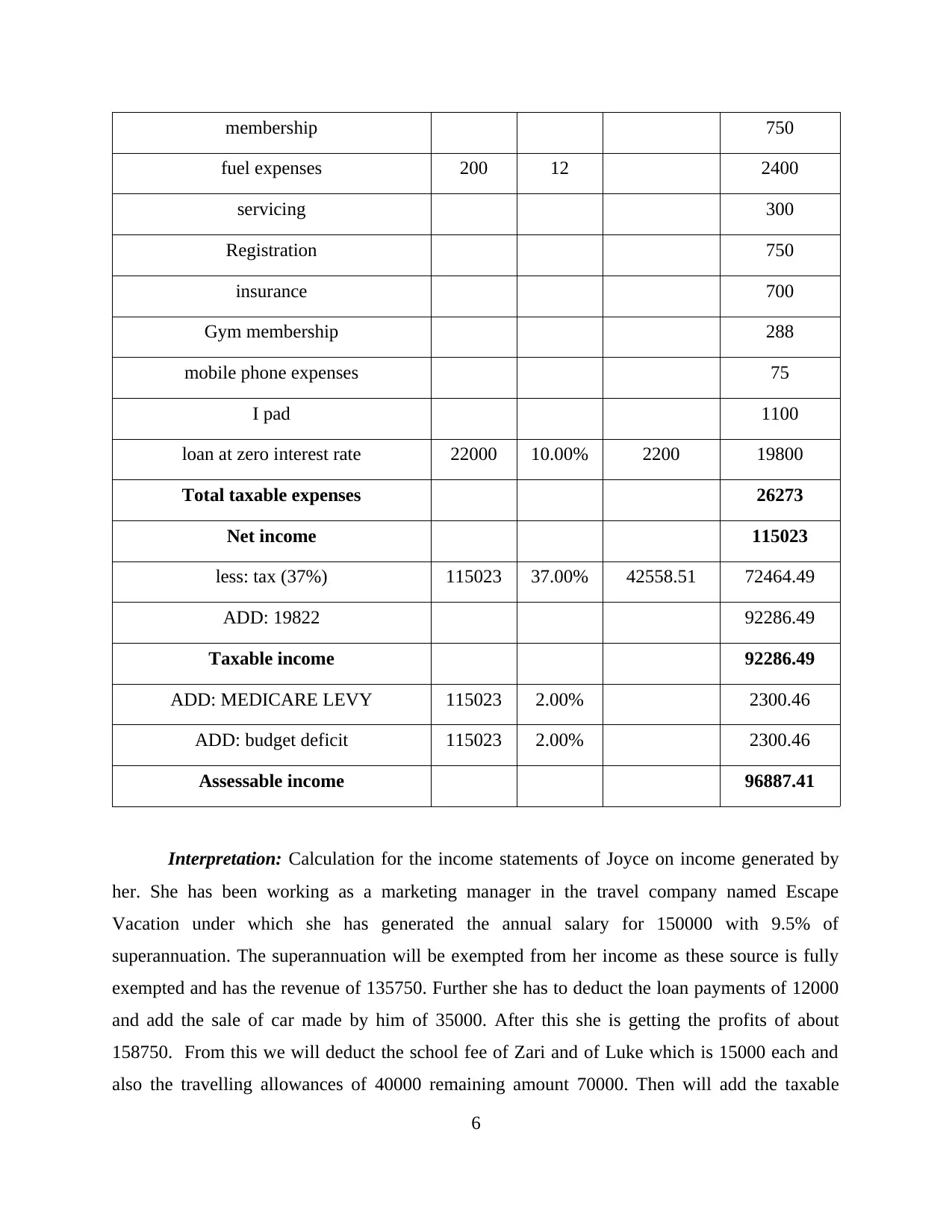

membership 750

fuel expenses 200 12 2400

servicing 300

Registration 750

insurance 700

Gym membership 288

mobile phone expenses 75

I pad 1100

loan at zero interest rate 22000 10.00% 2200 19800

Total taxable expenses 26273

Net income 115023

less: tax (37%) 115023 37.00% 42558.51 72464.49

ADD: 19822 92286.49

Taxable income 92286.49

ADD: MEDICARE LEVY 115023 2.00% 2300.46

ADD: budget deficit 115023 2.00% 2300.46

Assessable income 96887.41

Interpretation: Calculation for the income statements of Joyce on income generated by

her. She has been working as a marketing manager in the travel company named Escape

Vacation under which she has generated the annual salary for 150000 with 9.5% of

superannuation. The superannuation will be exempted from her income as these source is fully

exempted and has the revenue of 135750. Further she has to deduct the loan payments of 12000

and add the sale of car made by him of 35000. After this she is getting the profits of about

158750. From this we will deduct the school fee of Zari and of Luke which is 15000 each and

also the travelling allowances of 40000 remaining amount 70000. Then will add the taxable

6

fuel expenses 200 12 2400

servicing 300

Registration 750

insurance 700

Gym membership 288

mobile phone expenses 75

I pad 1100

loan at zero interest rate 22000 10.00% 2200 19800

Total taxable expenses 26273

Net income 115023

less: tax (37%) 115023 37.00% 42558.51 72464.49

ADD: 19822 92286.49

Taxable income 92286.49

ADD: MEDICARE LEVY 115023 2.00% 2300.46

ADD: budget deficit 115023 2.00% 2300.46

Assessable income 96887.41

Interpretation: Calculation for the income statements of Joyce on income generated by

her. She has been working as a marketing manager in the travel company named Escape

Vacation under which she has generated the annual salary for 150000 with 9.5% of

superannuation. The superannuation will be exempted from her income as these source is fully

exempted and has the revenue of 135750. Further she has to deduct the loan payments of 12000

and add the sale of car made by him of 35000. After this she is getting the profits of about

158750. From this we will deduct the school fee of Zari and of Luke which is 15000 each and

also the travelling allowances of 40000 remaining amount 70000. Then will add the taxable

6

expenses like Virgin Airlines of 550 from which the deductible amount is 80% i.e. 110 and also

loan at zero interest rate from which total taxable income will be 10%of 22000 i.e. 19800. Then

the total taxable expense are 26273. Then net income of her will be 115023 form which we less

take out the tax of 37% which will be 72464.49. Then she will take the 37% above from the tax

slab of 19822 which equals to 92286.49. This 92286.49 would be the actual taxable income. In

this figure we will be adding medical levy and budget deficit which are 2% of net income each

I.e . 2% of 115023 this equals to 2300.46 each. So the net assessable income will be 92286.49

adding 2300.46 and 2300.46 equals to 96887.41. She is the resident in Australia so she will be

benefited with the Australian Government scheme of allowing the Medicare levy which in

context with giving the health and security to their citizens.

It will be fruitful for Joyce to prefer income tax legislations over the income she has

generated through her employments (Creighton, 2014). Here she will be benefited with the

deduction or exemptions levied over her income and expenditure made within assessable year.

However, she will be benefited with the implication of various tax rate which as lower down the

taxable return paid by her (FBT exemptions and concessions, 2017).

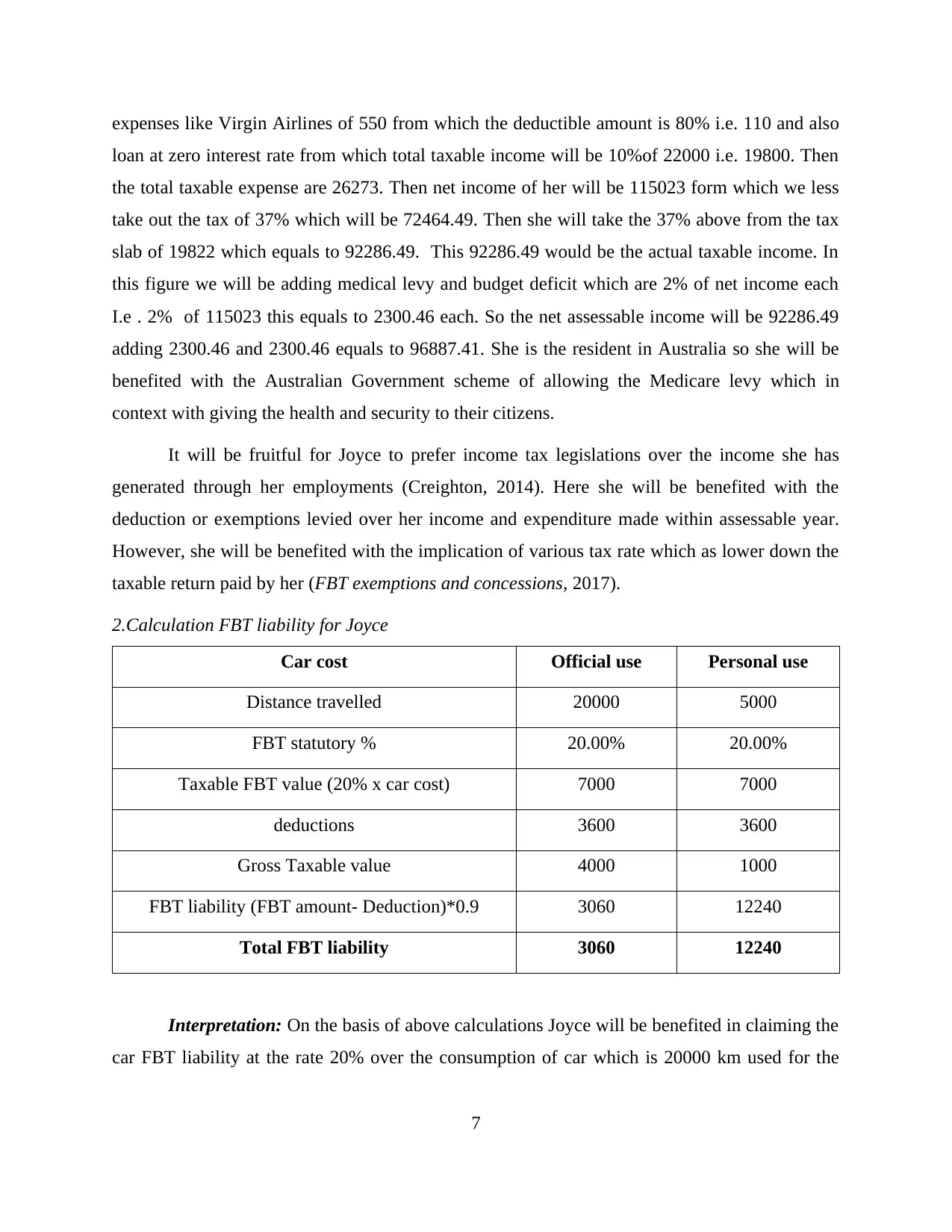

2.Calculation FBT liability for Joyce

Car cost Official use Personal use

Distance travelled 20000 5000

FBT statutory % 20.00% 20.00%

Taxable FBT value (20% x car cost) 7000 7000

deductions 3600 3600

Gross Taxable value 4000 1000

FBT liability (FBT amount- Deduction)*0.9 3060 12240

Total FBT liability 3060 12240

Interpretation: On the basis of above calculations Joyce will be benefited in claiming the

car FBT liability at the rate 20% over the consumption of car which is 20000 km used for the

7

loan at zero interest rate from which total taxable income will be 10%of 22000 i.e. 19800. Then

the total taxable expense are 26273. Then net income of her will be 115023 form which we less

take out the tax of 37% which will be 72464.49. Then she will take the 37% above from the tax

slab of 19822 which equals to 92286.49. This 92286.49 would be the actual taxable income. In

this figure we will be adding medical levy and budget deficit which are 2% of net income each

I.e . 2% of 115023 this equals to 2300.46 each. So the net assessable income will be 92286.49

adding 2300.46 and 2300.46 equals to 96887.41. She is the resident in Australia so she will be

benefited with the Australian Government scheme of allowing the Medicare levy which in

context with giving the health and security to their citizens.

It will be fruitful for Joyce to prefer income tax legislations over the income she has

generated through her employments (Creighton, 2014). Here she will be benefited with the

deduction or exemptions levied over her income and expenditure made within assessable year.

However, she will be benefited with the implication of various tax rate which as lower down the

taxable return paid by her (FBT exemptions and concessions, 2017).

2.Calculation FBT liability for Joyce

Car cost Official use Personal use

Distance travelled 20000 5000

FBT statutory % 20.00% 20.00%

Taxable FBT value (20% x car cost) 7000 7000

deductions 3600 3600

Gross Taxable value 4000 1000

FBT liability (FBT amount- Deduction)*0.9 3060 12240

Total FBT liability 3060 12240

Interpretation: On the basis of above calculations Joyce will be benefited in claiming the

car FBT liability at the rate 20% over the consumption of car which is 20000 km used for the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

office purpose as well as 5000 km for personal use. After measuring the FBT taxes, the total

FBT liability over the office use and personal use of car such as 3060 and 12240 respectively.

B.

There has been calculations for the tax liability of Escape Vacation as the company is

being planning to make the holiday package for the 2500 at 30 employees including GST. Firm

has planned the budget which will be costs for 150000 for 60 employees. There has been

calculation over the tax liability of this organisation as well as advising them to reduce the tax

liabilities.

1.Advising Escape Vacations over tax implication

The company has planned the holiday package for 30 employees at $2500 which will be

$75000. They have estimated the budget for 60 employees which will be costed at $150000. The

taxes will be levied over cost of granting free holiday packages to its employees.

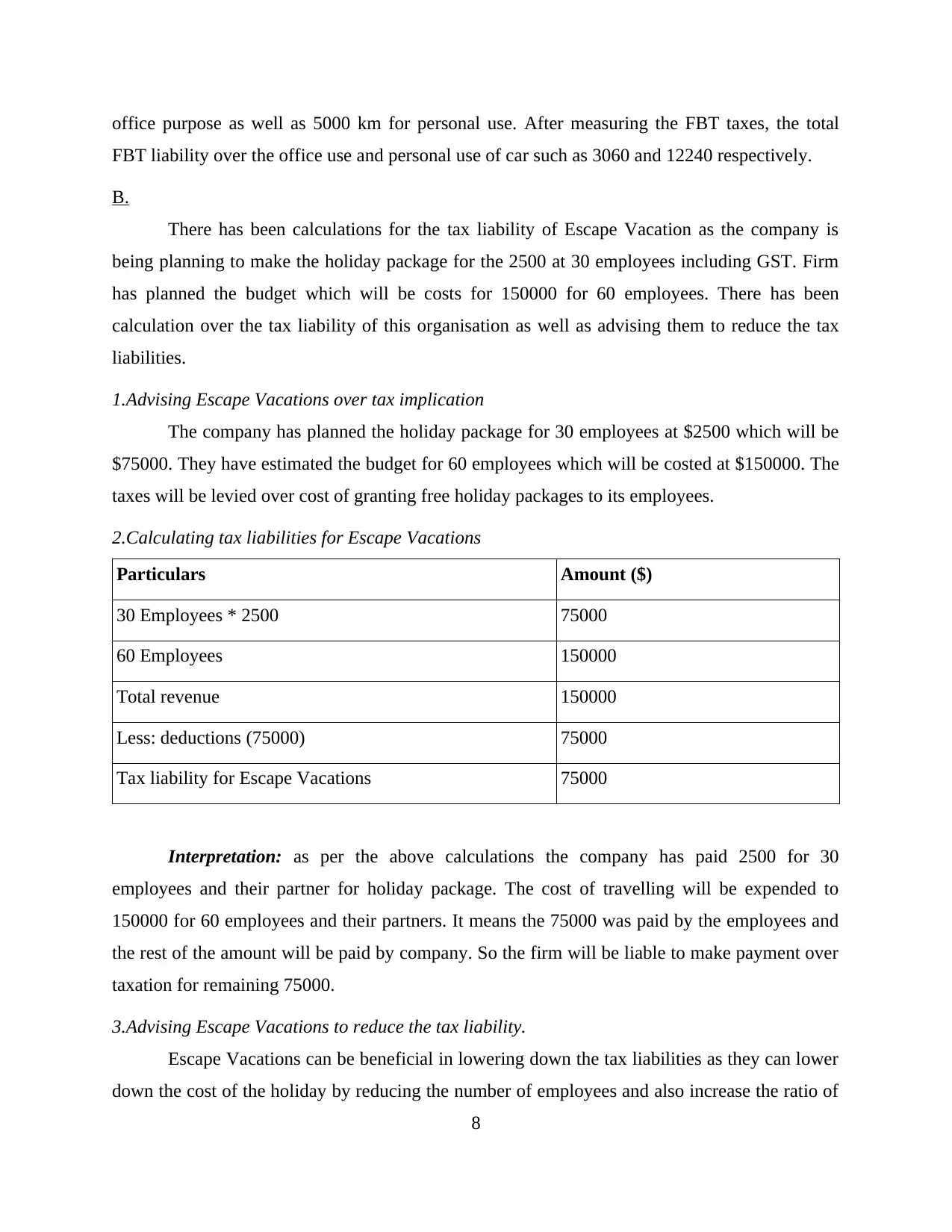

2.Calculating tax liabilities for Escape Vacations

Particulars Amount ($)

30 Employees * 2500 75000

60 Employees 150000

Total revenue 150000

Less: deductions (75000) 75000

Tax liability for Escape Vacations 75000

Interpretation: as per the above calculations the company has paid 2500 for 30

employees and their partner for holiday package. The cost of travelling will be expended to

150000 for 60 employees and their partners. It means the 75000 was paid by the employees and

the rest of the amount will be paid by company. So the firm will be liable to make payment over

taxation for remaining 75000.

3.Advising Escape Vacations to reduce the tax liability.

Escape Vacations can be beneficial in lowering down the tax liabilities as they can lower

down the cost of the holiday by reducing the number of employees and also increase the ratio of

8

FBT liability over the office use and personal use of car such as 3060 and 12240 respectively.

B.

There has been calculations for the tax liability of Escape Vacation as the company is

being planning to make the holiday package for the 2500 at 30 employees including GST. Firm

has planned the budget which will be costs for 150000 for 60 employees. There has been

calculation over the tax liability of this organisation as well as advising them to reduce the tax

liabilities.

1.Advising Escape Vacations over tax implication

The company has planned the holiday package for 30 employees at $2500 which will be

$75000. They have estimated the budget for 60 employees which will be costed at $150000. The

taxes will be levied over cost of granting free holiday packages to its employees.

2.Calculating tax liabilities for Escape Vacations

Particulars Amount ($)

30 Employees * 2500 75000

60 Employees 150000

Total revenue 150000

Less: deductions (75000) 75000

Tax liability for Escape Vacations 75000

Interpretation: as per the above calculations the company has paid 2500 for 30

employees and their partner for holiday package. The cost of travelling will be expended to

150000 for 60 employees and their partners. It means the 75000 was paid by the employees and

the rest of the amount will be paid by company. So the firm will be liable to make payment over

taxation for remaining 75000.

3.Advising Escape Vacations to reduce the tax liability.

Escape Vacations can be beneficial in lowering down the tax liabilities as they can lower

down the cost of the holiday by reducing the number of employees and also increase the ratio of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making payment for the travelling package. As the employees should make payments for their

travelling competitively more than the company.

CONCLUSION

As per present assessment report related with the various tax legislation over the income

or revenue generated by Joyce and Daniel as well as Escape Vacations. Several rates of taxes as

well as various deductions are to allowed to them which helps in reducing the taxable amount.

The taxable amount can be paid by Daniel over the income he has generated through his

employment in Mining Capital corporation at Australian branch for $144145.6. He was non

resident to Australia so he will not being benefited with the governmental rewards of Medicare

levy. On the other site, Joyce is an Australasian resident and has generated income through her

employment in Escape Vacation.

9

travelling competitively more than the company.

CONCLUSION

As per present assessment report related with the various tax legislation over the income

or revenue generated by Joyce and Daniel as well as Escape Vacations. Several rates of taxes as

well as various deductions are to allowed to them which helps in reducing the taxable amount.

The taxable amount can be paid by Daniel over the income he has generated through his

employment in Mining Capital corporation at Australian branch for $144145.6. He was non

resident to Australia so he will not being benefited with the governmental rewards of Medicare

levy. On the other site, Joyce is an Australasian resident and has generated income through her

employment in Escape Vacation.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.