Taxation Report

VerifiedAdded on 2020/03/23

|10

|1977

|361

Report

AI Summary

This report delves into the intricacies of taxation law, focusing on the Income Tax Assessment Act and its implications for businesses like Big Bank. It covers various aspects of tax deductions, GST input credits, and relevant case studies to illustrate the application of tax regulations in real-world scenari...

Running head: TAXATION

Taxation

University Name

Student Name

Authors’ Note

Taxation

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2TAXATION

Task 1:

As rightly put forward by Barkoczy (2016), taxation ruling asserted under the rule segment 4-

15 of specifically Income Tax Assessment Act pronounced during 1997 cites that computable

income is estimated by fitting subtraction of acceptable spending from the chargeable

income. Basically, people disbursing specific amount of tax might claim for deductions from

the assessable income. In line with the regulation pronounced in 8-1 (1) issued by ITAA in

1997 spells out that a particular person can seek subtraction for the below mentioned reasons:

- For the purpose of creation of quantifiable income

- For carrying out important business actions that can one after another generate

measurable income (Chaudhry et al. 2015)

The particular ruling segment that talks about the subtractions stated under segment 8.1 of

particularly the act (Income Tax Assessment Act) pronounced in 1997. This necessarily also

asserts that it is not feasible to undertake subtractions of different losses suffered by the

business provided the given conditions mentioned below:

- Firm’s losses otherwise retiring of capital are capital in nature

- Losses otherwise retiring are of private or else regional in features

- Firm’s losses are carried out to acquire or else to produce the amount of earnings that

is let off

- Particular provisions of the income tax regulation limits the process of subtraction of

the same (Coleman 2016)

Evaluation of the regulation of taxation assists in attainment of all-inclusive conception with

regards to different aspects mentioned herein below:

Task 1:

As rightly put forward by Barkoczy (2016), taxation ruling asserted under the rule segment 4-

15 of specifically Income Tax Assessment Act pronounced during 1997 cites that computable

income is estimated by fitting subtraction of acceptable spending from the chargeable

income. Basically, people disbursing specific amount of tax might claim for deductions from

the assessable income. In line with the regulation pronounced in 8-1 (1) issued by ITAA in

1997 spells out that a particular person can seek subtraction for the below mentioned reasons:

- For the purpose of creation of quantifiable income

- For carrying out important business actions that can one after another generate

measurable income (Chaudhry et al. 2015)

The particular ruling segment that talks about the subtractions stated under segment 8.1 of

particularly the act (Income Tax Assessment Act) pronounced in 1997. This necessarily also

asserts that it is not feasible to undertake subtractions of different losses suffered by the

business provided the given conditions mentioned below:

- Firm’s losses otherwise retiring of capital are capital in nature

- Losses otherwise retiring are of private or else regional in features

- Firm’s losses are carried out to acquire or else to produce the amount of earnings that

is let off

- Particular provisions of the income tax regulation limits the process of subtraction of

the same (Coleman 2016)

Evaluation of the regulation of taxation assists in attainment of all-inclusive conception with

regards to different aspects mentioned herein below:

3TAXATION

- Corporations spending money for transference of plants as well as machineries can be

enumerated for subtraction only at the time when plants and machineries are used up

for generation of quantifiable as well as assessable income as cited under the dictate

8-1 issued by ITAA. Lawful confirmation in this case on “Granite Supply

Association Ltd vKitton of 190” supports in the process of validating certain facts.

This is regarding outlays of firms on altering the site of plants as well as machineries

of corporations. However, this amount can be considered for deduction since these

expenses are capital in features/characteristics. Furthermore, the results of the lawful

case Smith v Westinghouse Brake Company of 1888 also aids in confirmation of

deductions asserted in the authorized case dictate of Granite Supply Association Ltd

vKitton of 190. (Fraser et al. 2015)

The legal case ““British Insulated & Helsby Cables” can be referred to in this

case. In this case the firm bears costs of transportation and delivers substantiation

regarding the fact that there subsists a constant benefit for the business by transferring

specific depreciable resources. Essentially the taxation directive mentioned under

TD92/126 refers to the fact that there is installation of different machines and

initiating business operations in which costs is considered as a fraction of revenue. In

addition to this, this can be hereby mentioned that the costs borne for relocation of

machines from one site to another can be treated as the capital cost and cannot be

endorsed for claiming subtractions (Jordan 2016)

- Taxation pronouncement pronounced under 8-1 of the ruling issued by ITAA in 1997

cite that costs borne by corporations for re-estimation of firm’s assets/reserves cannot

be considered as expense that can be subtracted

- Taxation dictate specified under decree 8-1 issued by ITAA states that business

spending by different legal officials for generation of earnings can be acknowledged

- Corporations spending money for transference of plants as well as machineries can be

enumerated for subtraction only at the time when plants and machineries are used up

for generation of quantifiable as well as assessable income as cited under the dictate

8-1 issued by ITAA. Lawful confirmation in this case on “Granite Supply

Association Ltd vKitton of 190” supports in the process of validating certain facts.

This is regarding outlays of firms on altering the site of plants as well as machineries

of corporations. However, this amount can be considered for deduction since these

expenses are capital in features/characteristics. Furthermore, the results of the lawful

case Smith v Westinghouse Brake Company of 1888 also aids in confirmation of

deductions asserted in the authorized case dictate of Granite Supply Association Ltd

vKitton of 190. (Fraser et al. 2015)

The legal case ““British Insulated & Helsby Cables” can be referred to in this

case. In this case the firm bears costs of transportation and delivers substantiation

regarding the fact that there subsists a constant benefit for the business by transferring

specific depreciable resources. Essentially the taxation directive mentioned under

TD92/126 refers to the fact that there is installation of different machines and

initiating business operations in which costs is considered as a fraction of revenue. In

addition to this, this can be hereby mentioned that the costs borne for relocation of

machines from one site to another can be treated as the capital cost and cannot be

endorsed for claiming subtractions (Jordan 2016)

- Taxation pronouncement pronounced under 8-1 of the ruling issued by ITAA in 1997

cite that costs borne by corporations for re-estimation of firm’s assets/reserves cannot

be considered as expense that can be subtracted

- Taxation dictate specified under decree 8-1 issued by ITAA states that business

spending by different legal officials for generation of earnings can be acknowledged

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4TAXATION

as a specific amount that can be considered for subtraction in the process of

assessment of payable tax. Furthermore, the taxation ruling sited under the ID 2004-

367 refers to the fact that the cost that is lawfully incurred during releasing business

operations is normally considered as the permitted subtractions. However, the causes

behind taking into consideration these kinds of deductible spending is that the

individual payers of tax acquires the expend so that revenue can be produced. In this

connection, the case on “FC of T v Snowden and Wilson Pty Ltd (1958)” explicates

that in cases where spending are not normal and no prior situations the payers of tax

needed to incur spending, then in that circumstances it averts the expenditure from

being considered as the permissible subtraction (Miller and Oats 2016). In addition to

this, the officially permitted cost that payers of tax bears essentially to oppose the

winding of certain petition cannot be properly treated as the permissible deduction.

The main cause behind not taking into account these kinds of costs for deductions

from the assessable income is mainly due to the fact that they are proportion of

business expenditure. Essentially, the overall happening of legal expenditure for

terminating the petition cannot be treated as the acceptable subtractions as they

possess the capital feature.

Task 2:

The given case evidently talks about the banking business Big Bank that carries out

operations in excess of 50 diverse branches and runs numerous call centres. The headquarter

of the banking firm Big Bank is situated in a 10 storied office block. Comprehensive analysis

of taxation regulation aids in acquiring knowledge concerning input credit of particularly

GST (goods as well as service tax). Guidelines asserts that the input credit in particularly

GST is inevitably permitted only when the process of acquirement is taken on by the

as a specific amount that can be considered for subtraction in the process of

assessment of payable tax. Furthermore, the taxation ruling sited under the ID 2004-

367 refers to the fact that the cost that is lawfully incurred during releasing business

operations is normally considered as the permitted subtractions. However, the causes

behind taking into consideration these kinds of deductible spending is that the

individual payers of tax acquires the expend so that revenue can be produced. In this

connection, the case on “FC of T v Snowden and Wilson Pty Ltd (1958)” explicates

that in cases where spending are not normal and no prior situations the payers of tax

needed to incur spending, then in that circumstances it averts the expenditure from

being considered as the permissible subtraction (Miller and Oats 2016). In addition to

this, the officially permitted cost that payers of tax bears essentially to oppose the

winding of certain petition cannot be properly treated as the permissible deduction.

The main cause behind not taking into account these kinds of costs for deductions

from the assessable income is mainly due to the fact that they are proportion of

business expenditure. Essentially, the overall happening of legal expenditure for

terminating the petition cannot be treated as the acceptable subtractions as they

possess the capital feature.

Task 2:

The given case evidently talks about the banking business Big Bank that carries out

operations in excess of 50 diverse branches and runs numerous call centres. The headquarter

of the banking firm Big Bank is situated in a 10 storied office block. Comprehensive analysis

of taxation regulation aids in acquiring knowledge concerning input credit of particularly

GST (goods as well as service tax). Guidelines asserts that the input credit in particularly

GST is inevitably permitted only when the process of acquirement is taken on by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5TAXATION

corporation and the apposite article linked to this specific kind of business are fittingly

maintained. GST –pronouncements of 1999 stresses on the fact that banking firm that

operates for generating higher income have the faculty to get hold of input credit (Parker

2013). As such, this aids the bank Big bank to lay out the required amount for goods as well

as service tax (GST). In essence, this refers to purchasing of assets/reserves of the

corporation.

Issue deciphered from the current case

Investigation of the case on the bank Big Bank assists in disclosing that the firm is indexed

for purpose of functioning of GST. In essence, the current report on the Big Bank mentions

that the bank spends around $1650000 and this specific amount necessarily is inclusive of the

goods and service tax applied on the amount expended on advertisement functions.

Additionally, Big Bank also intends to deliver assurance as regards whether disbursement

amount can be authoritatively identified as input credit. This is because the expenditure

amount is encompassing Goods and services (Tax Peetz 2014).

Tax Guideline that can be referred to in this present case

Illustrative analysis of the taxation regulation appropriately asserted in the 2nd section of the

GST pronounced in 1999 helps in acquiring conception regarding utilities that are officially

recognized to acquire input tax credit. In essence, these are essentially burnt up by the bank

right the way through the usual course of operations of firm. Nevertheless, it can be hereby

mentioned that expenses in real effect encompasses GST (Sawyer 2013).

Specific application of dictates of taxation

The provided case speaks about keen financial services offered by the bank Big Bank. As

such, the presented case also explicates about the backdrop of functionalities of the business

corporation and the apposite article linked to this specific kind of business are fittingly

maintained. GST –pronouncements of 1999 stresses on the fact that banking firm that

operates for generating higher income have the faculty to get hold of input credit (Parker

2013). As such, this aids the bank Big bank to lay out the required amount for goods as well

as service tax (GST). In essence, this refers to purchasing of assets/reserves of the

corporation.

Issue deciphered from the current case

Investigation of the case on the bank Big Bank assists in disclosing that the firm is indexed

for purpose of functioning of GST. In essence, the current report on the Big Bank mentions

that the bank spends around $1650000 and this specific amount necessarily is inclusive of the

goods and service tax applied on the amount expended on advertisement functions.

Additionally, Big Bank also intends to deliver assurance as regards whether disbursement

amount can be authoritatively identified as input credit. This is because the expenditure

amount is encompassing Goods and services (Tax Peetz 2014).

Tax Guideline that can be referred to in this present case

Illustrative analysis of the taxation regulation appropriately asserted in the 2nd section of the

GST pronounced in 1999 helps in acquiring conception regarding utilities that are officially

recognized to acquire input tax credit. In essence, these are essentially burnt up by the bank

right the way through the usual course of operations of firm. Nevertheless, it can be hereby

mentioned that expenses in real effect encompasses GST (Sawyer 2013).

Specific application of dictates of taxation

The provided case speaks about keen financial services offered by the bank Big Bank. As

such, the presented case also explicates about the backdrop of functionalities of the business

6TAXATION

entity. Explanations of case on Big Bank concentrate on the functions of the business

companies. This tells about the initiation of deliverance of insurance arrangements, home

substance in the open market along with bank’s provision of loan as well as deposit facility to

their clients. Administration of the bank Big Bank also allotted a specific amount for carrying

out advertisement intended towards promotion of financial services for particularly home.

Even so, out of the available amount, the particular amount that remains leftover is

necessarily up to $1100000. Inevitably, this particular amount assigned for undertaking

projects on undertaking advertisements of specialised financial products as well as facilities is

counts GST within it (Woellner et al. 2016).

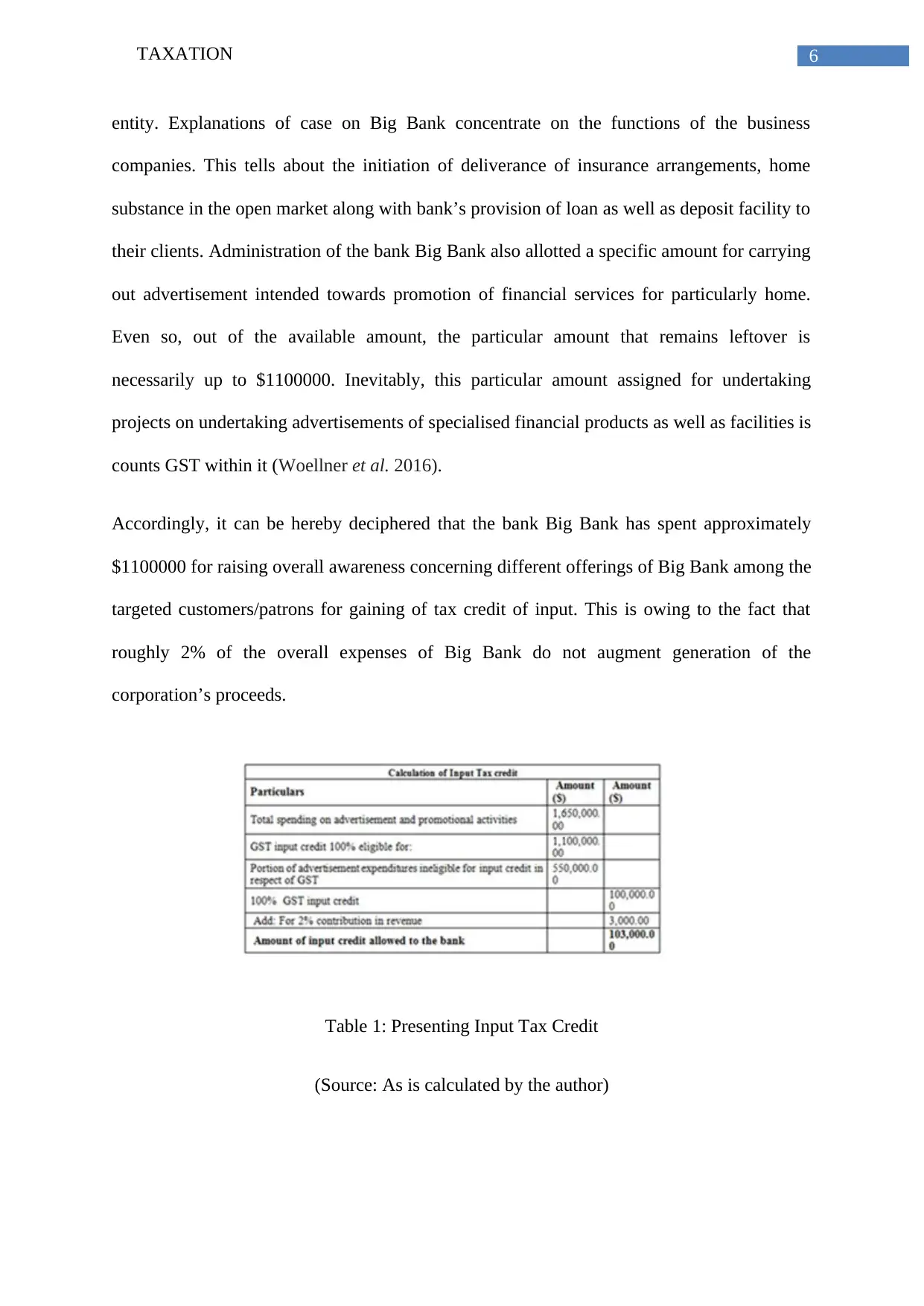

Accordingly, it can be hereby deciphered that the bank Big Bank has spent approximately

$1100000 for raising overall awareness concerning different offerings of Big Bank among the

targeted customers/patrons for gaining of tax credit of input. This is owing to the fact that

roughly 2% of the overall expenses of Big Bank do not augment generation of the

corporation’s proceeds.

Table 1: Presenting Input Tax Credit

(Source: As is calculated by the author)

entity. Explanations of case on Big Bank concentrate on the functions of the business

companies. This tells about the initiation of deliverance of insurance arrangements, home

substance in the open market along with bank’s provision of loan as well as deposit facility to

their clients. Administration of the bank Big Bank also allotted a specific amount for carrying

out advertisement intended towards promotion of financial services for particularly home.

Even so, out of the available amount, the particular amount that remains leftover is

necessarily up to $1100000. Inevitably, this particular amount assigned for undertaking

projects on undertaking advertisements of specialised financial products as well as facilities is

counts GST within it (Woellner et al. 2016).

Accordingly, it can be hereby deciphered that the bank Big Bank has spent approximately

$1100000 for raising overall awareness concerning different offerings of Big Bank among the

targeted customers/patrons for gaining of tax credit of input. This is owing to the fact that

roughly 2% of the overall expenses of Big Bank do not augment generation of the

corporation’s proceeds.

Table 1: Presenting Input Tax Credit

(Source: As is calculated by the author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7TAXATION

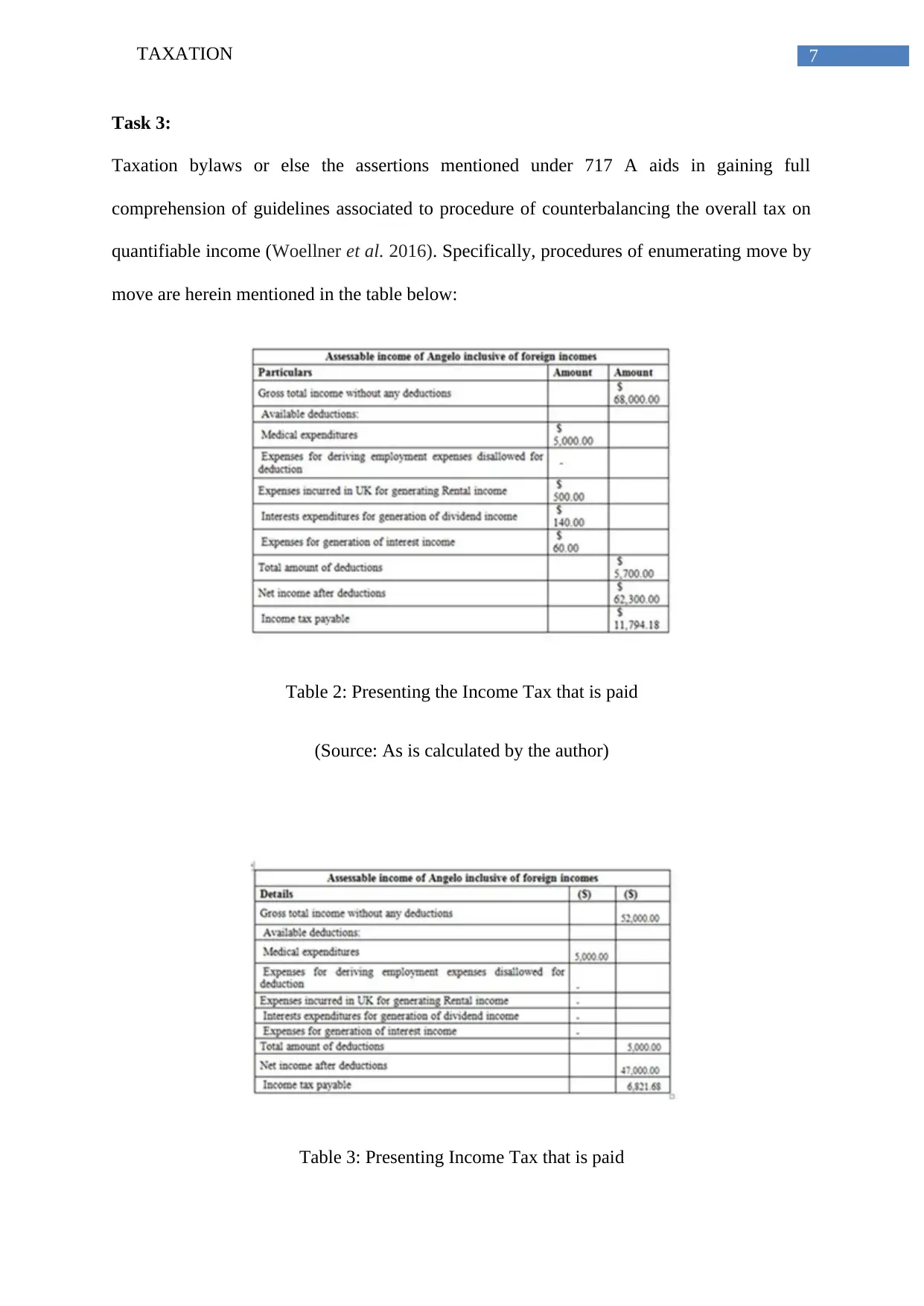

Task 3:

Taxation bylaws or else the assertions mentioned under 717 A aids in gaining full

comprehension of guidelines associated to procedure of counterbalancing the overall tax on

quantifiable income (Woellner et al. 2016). Specifically, procedures of enumerating move by

move are herein mentioned in the table below:

Table 2: Presenting the Income Tax that is paid

(Source: As is calculated by the author)

Table 3: Presenting Income Tax that is paid

Task 3:

Taxation bylaws or else the assertions mentioned under 717 A aids in gaining full

comprehension of guidelines associated to procedure of counterbalancing the overall tax on

quantifiable income (Woellner et al. 2016). Specifically, procedures of enumerating move by

move are herein mentioned in the table below:

Table 2: Presenting the Income Tax that is paid

(Source: As is calculated by the author)

Table 3: Presenting Income Tax that is paid

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8TAXATION

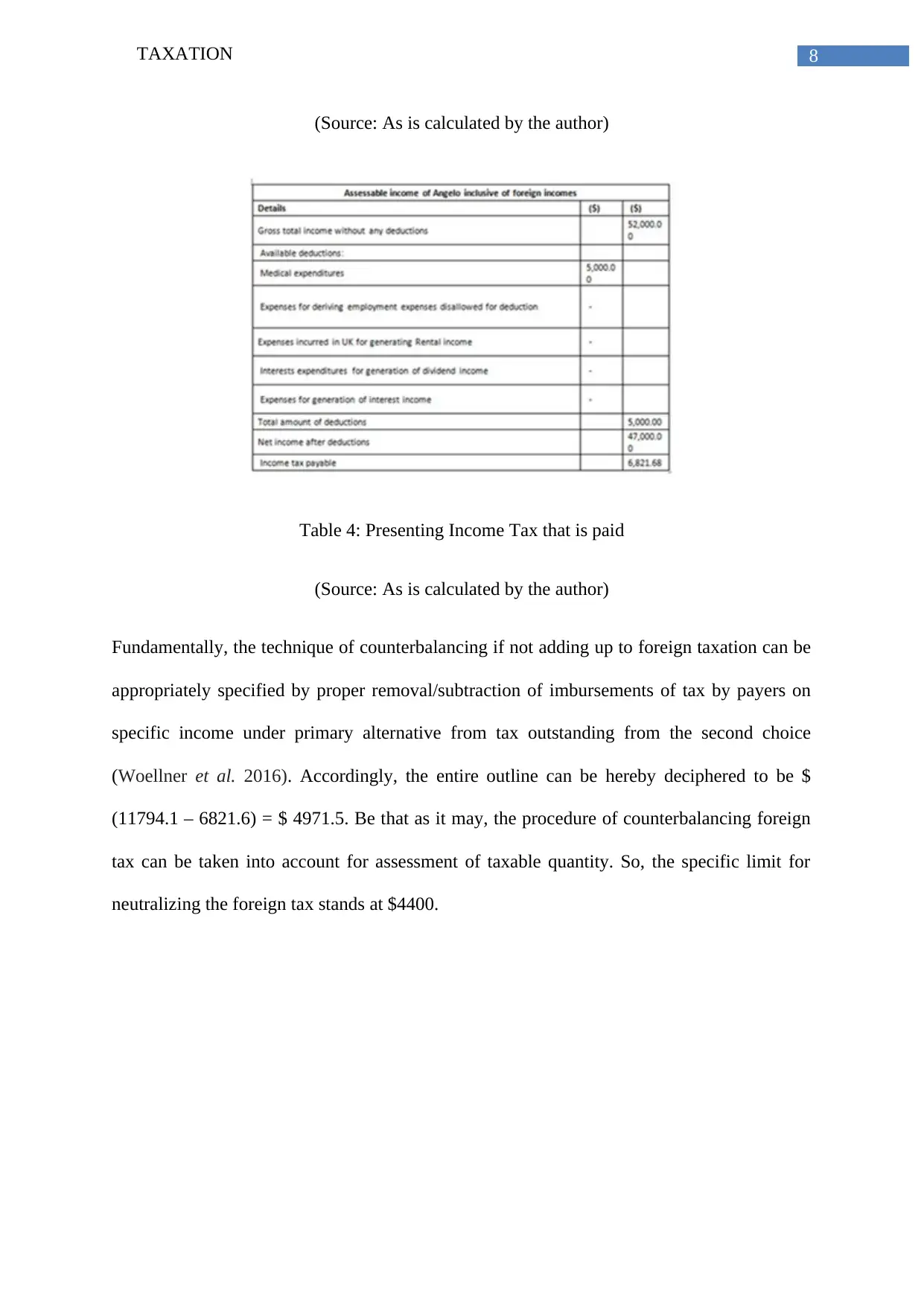

(Source: As is calculated by the author)

Table 4: Presenting Income Tax that is paid

(Source: As is calculated by the author)

Fundamentally, the technique of counterbalancing if not adding up to foreign taxation can be

appropriately specified by proper removal/subtraction of imbursements of tax by payers on

specific income under primary alternative from tax outstanding from the second choice

(Woellner et al. 2016). Accordingly, the entire outline can be hereby deciphered to be $

(11794.1 – 6821.6) = $ 4971.5. Be that as it may, the procedure of counterbalancing foreign

tax can be taken into account for assessment of taxable quantity. So, the specific limit for

neutralizing the foreign tax stands at $4400.

(Source: As is calculated by the author)

Table 4: Presenting Income Tax that is paid

(Source: As is calculated by the author)

Fundamentally, the technique of counterbalancing if not adding up to foreign taxation can be

appropriately specified by proper removal/subtraction of imbursements of tax by payers on

specific income under primary alternative from tax outstanding from the second choice

(Woellner et al. 2016). Accordingly, the entire outline can be hereby deciphered to be $

(11794.1 – 6821.6) = $ 4971.5. Be that as it may, the procedure of counterbalancing foreign

tax can be taken into account for assessment of taxable quantity. So, the specific limit for

neutralizing the foreign tax stands at $4400.

9TAXATION

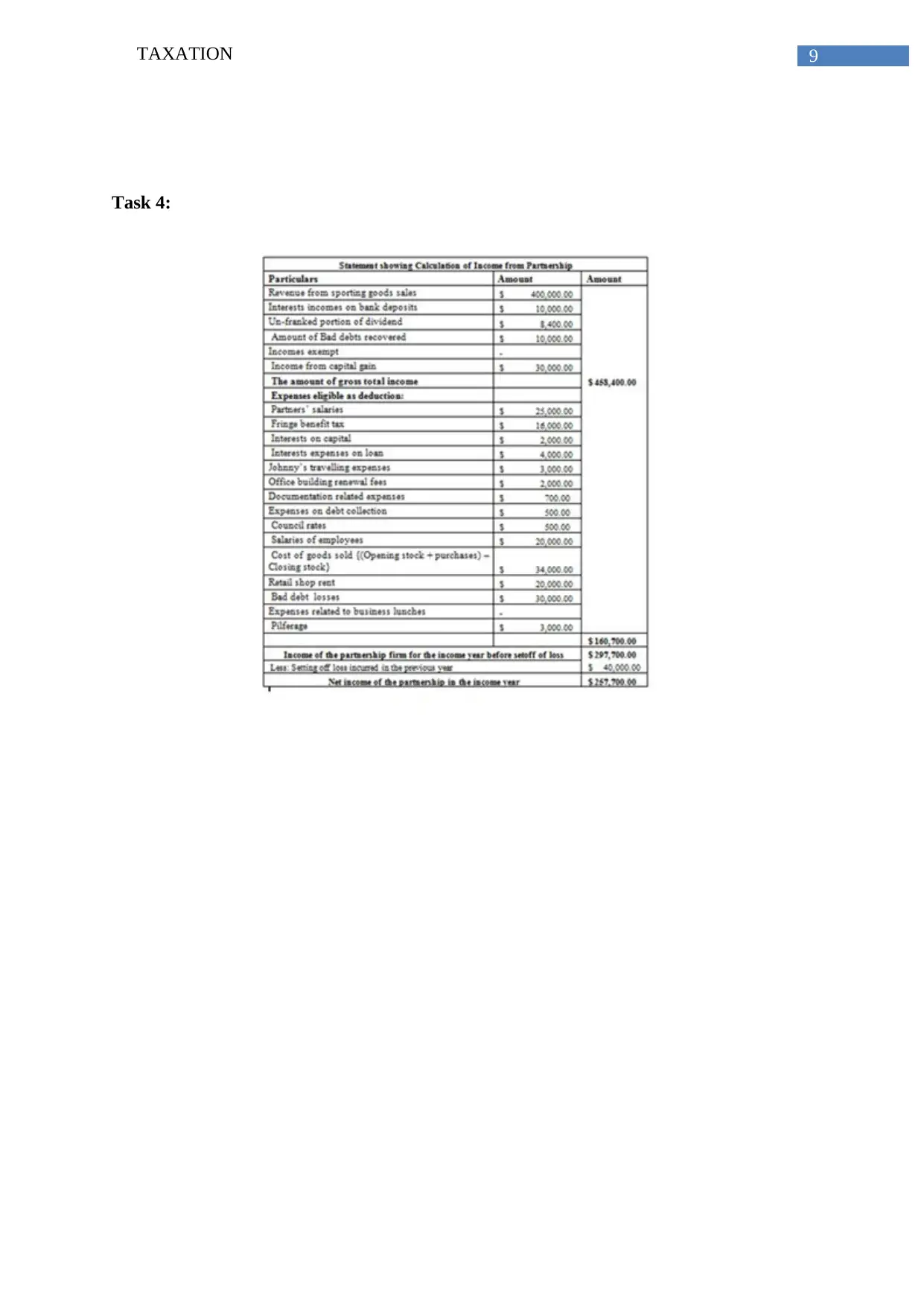

Task 4:

Task 4:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10TAXATION

References

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Chaudhry, S.M., Mullineux, A. and Agarwal, N., 2015. Balancing the regulation and taxation

of banking. International Review of Financial Analysis, 42, pp.38-52.

Coleman, W. ed., 2016. Only in Australia: The history, politics, and economics of Australian

exceptionalism. Oxford University Press.

Fraser, D., Weier, M., Keane, H. and Gartner, C., 2015. Vapers’ perspectives on electronic

cigarette regulation in Australia. International Journal of Drug Policy, 26(6), pp.589-594.

Jordan, C., 2016. Commissioner of Taxation, Chris Jordan AO on Corporate Tax

Transparency 2015–16. Press release, December 9. Australian Taxation Office (Canberra).

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Parker, C., 2013. Twenty years of responsive regulation: An appreciation and

appraisal. Regulation & Governance, 7(1), pp.2-13.

Peetz, D., 2014. Regulation distance, labour segmentation and gender gaps. Cambridge

Journal of Economics, 39(2), pp.345-362.

Sawyer, A., 2013. Rewriting Tax Legislation-Can Polishing Silver Really Turn It into

Gold. J. Austl. Tax'n, 15, p.1.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

References

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Chaudhry, S.M., Mullineux, A. and Agarwal, N., 2015. Balancing the regulation and taxation

of banking. International Review of Financial Analysis, 42, pp.38-52.

Coleman, W. ed., 2016. Only in Australia: The history, politics, and economics of Australian

exceptionalism. Oxford University Press.

Fraser, D., Weier, M., Keane, H. and Gartner, C., 2015. Vapers’ perspectives on electronic

cigarette regulation in Australia. International Journal of Drug Policy, 26(6), pp.589-594.

Jordan, C., 2016. Commissioner of Taxation, Chris Jordan AO on Corporate Tax

Transparency 2015–16. Press release, December 9. Australian Taxation Office (Canberra).

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Parker, C., 2013. Twenty years of responsive regulation: An appreciation and

appraisal. Regulation & Governance, 7(1), pp.2-13.

Peetz, D., 2014. Regulation distance, labour segmentation and gender gaps. Cambridge

Journal of Economics, 39(2), pp.345-362.

Sawyer, A., 2013. Rewriting Tax Legislation-Can Polishing Silver Really Turn It into

Gold. J. Austl. Tax'n, 15, p.1.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.