AC50029E Taxation: UK Self-Assessment, National Insurance, and Equity

VerifiedAdded on 2023/06/16

|7

|1900

|281

Essay

AI Summary

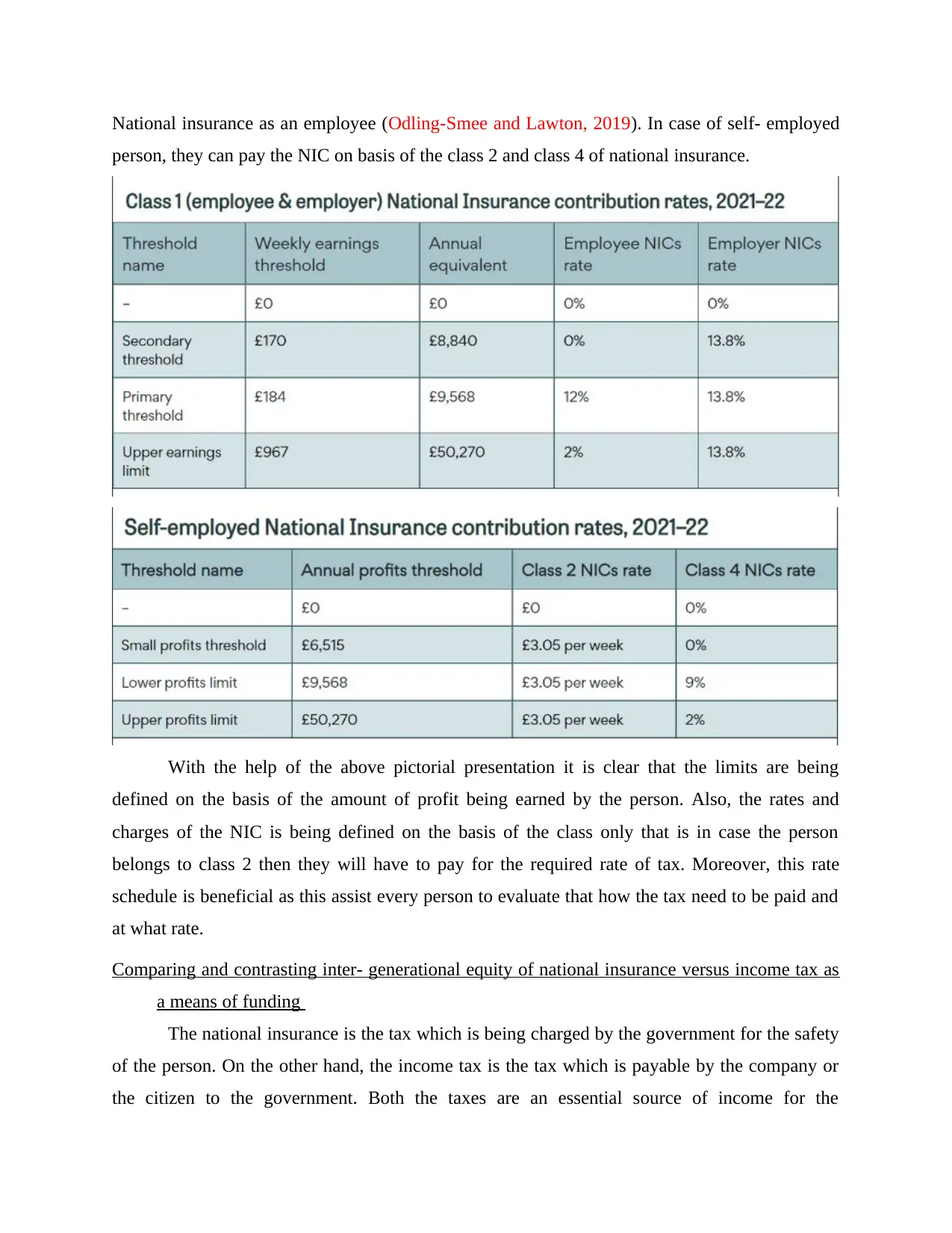

This essay provides a comprehensive overview of the UK taxation system, with a specific focus on self-assessment and National Insurance contributions (NIC). It evaluates the self-assessment system in the UK for 2021-22, explaining the operation and scope of income tax, filing obligations, and the implications of non-compliance. The essay also examines the National Insurance system, detailing the different classes of contributions and their respective scopes. Furthermore, it compares and contrasts the inter-generational equity of National Insurance versus income tax as methods of funding. The analysis covers the importance of tax compliance, the role of NIC in social security benefits, and the potential for merging income tax and NIC to enhance transparency and efficiency. The essay concludes by underscoring the essential role of taxation as a source of government income and the need for businesses and individuals to comply with tax regulations, with resources available on Desklib.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.