Analysis of UK Taxation: Taxpayers, Practitioners, and Calculations

VerifiedAdded on 2020/07/23

|6

|5330

|47

Report

AI Summary

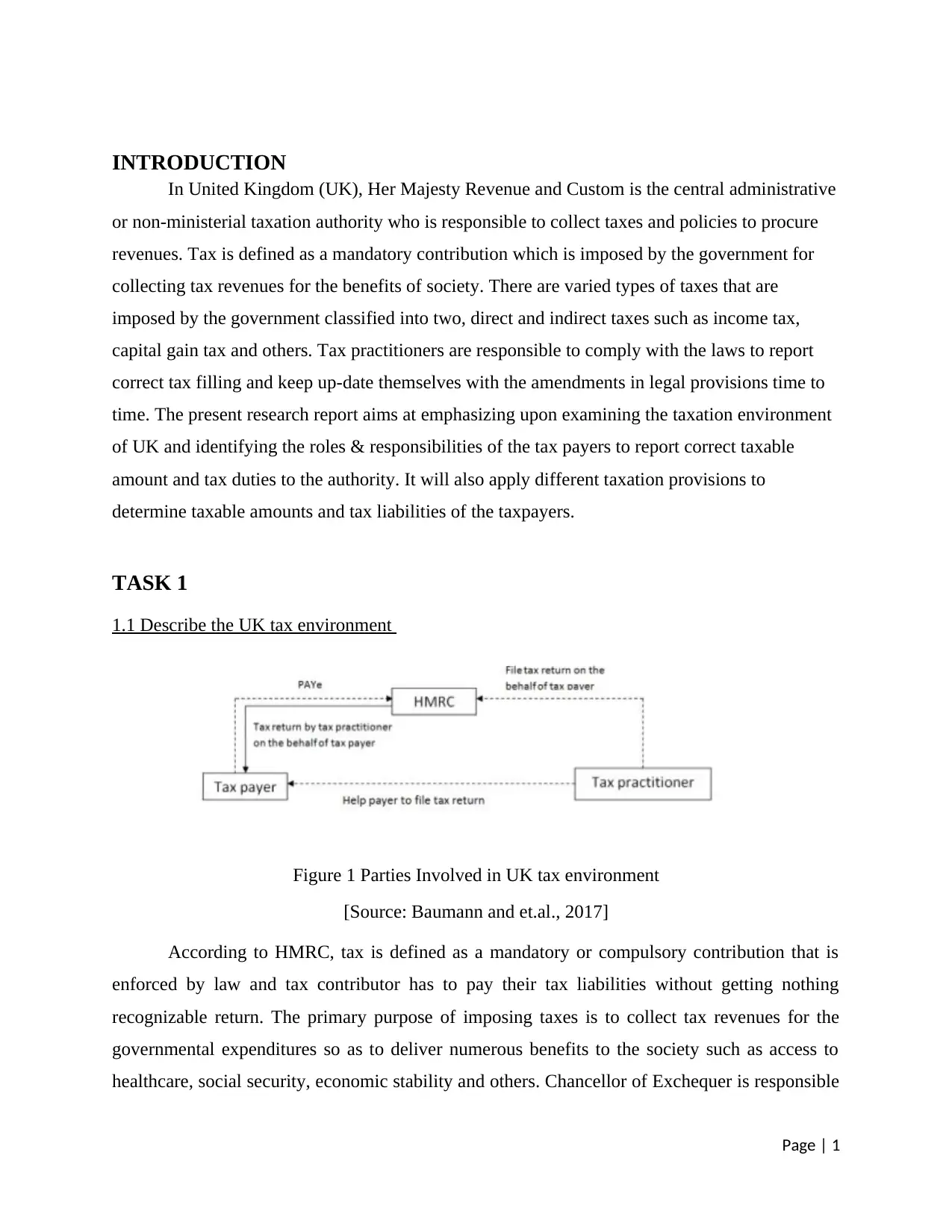

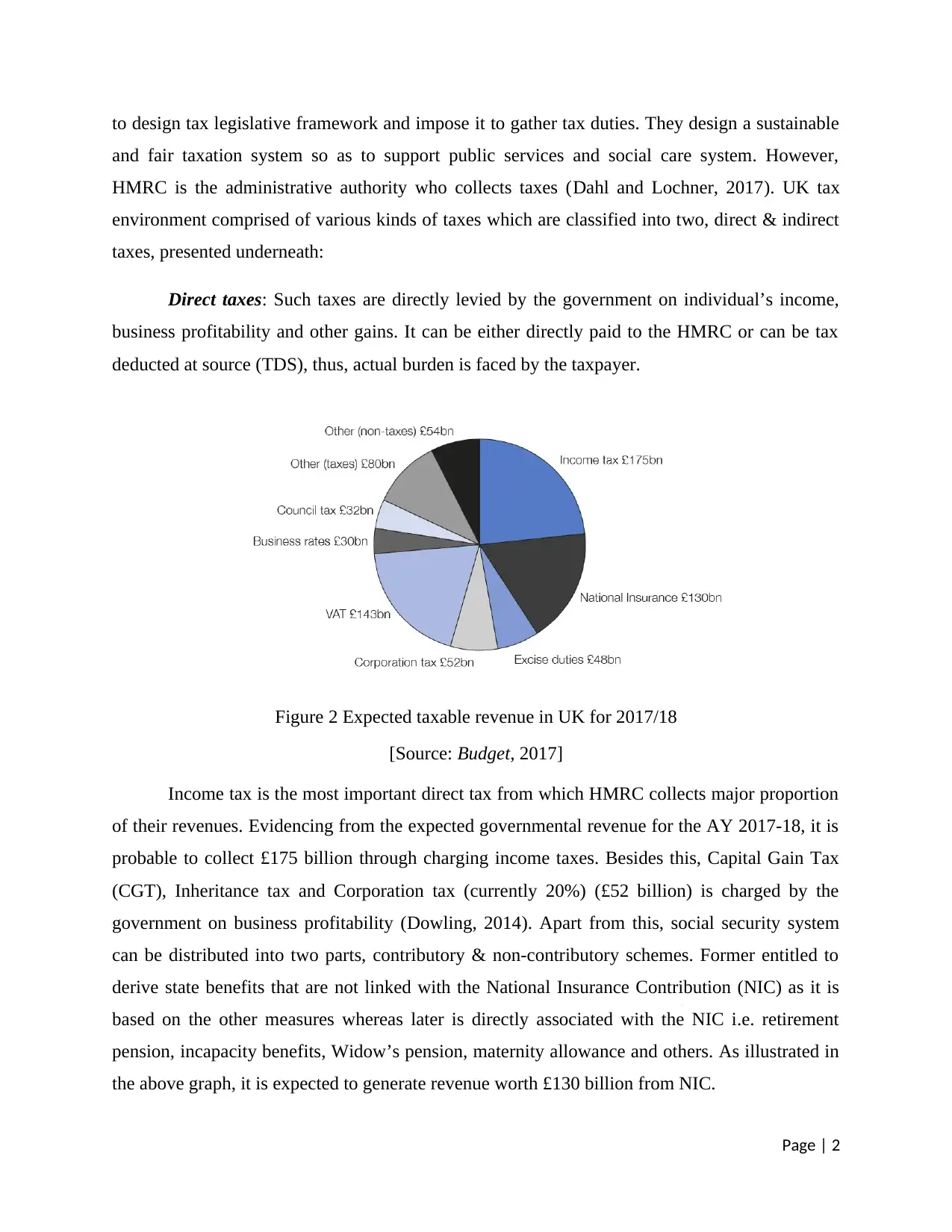

This report provides a comprehensive overview of the UK taxation system. It begins by describing the UK tax environment, including direct and indirect taxes, and the role of Her Majesty's Revenue and Customs (HMRC). It then analyzes the roles and responsibilities of tax practitioners, emphasizing their importance in assisting taxpayers with compliance and providing expert advice. The report also explains the taxation obligations of taxpayers and the implications of non-compliance, including penalties for late payments and incorrect filings. Furthermore, it delves into practical applications by demonstrating the calculation of relevant income, expenses, allowances, and taxable amounts for both employment and self-employment income. The report includes detailed examples of tax calculations, such as those for income tax and capital gains tax, providing a clear understanding of how tax liabilities are determined. Finally, the report offers a conclusion summarizing the key findings and provides references for further study. The report is a valuable resource for students studying finance and taxation.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.