Taxation Report: UK Tax Environment, Practitioner Roles, Calculations

VerifiedAdded on 2020/06/06

|14

|3904

|39

Report

AI Summary

This report provides a comprehensive overview of the UK taxation system. It begins by outlining the tax environment in the UK, categorizing taxes as direct and indirect, and illustrating revenue sources with a diagram. The report then delves into the roles and responsibilities of tax practitioners, emphasizing their obligations to clients and the importance of compliance with HMRC regulations. It further explains the obligations of taxpayers and the consequences of non-compliance, including penalties for late payments and return filings. The report includes calculations for income, expenses, and allowances, demonstrating the computation of taxable income and tax liability, including examples of income from employment and self-employment, and computations of capital gains. Finally, it concludes with a summary of the key aspects of UK taxation discussed throughout the report and provides references for further reading.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Tax environment which is there in UK.................................................................................1

1.2 Roles and responsibilities of Tax practitioner.......................................................................2

1.3 Obligations of tax payer and effect of non compliance........................................................4

2.1 Calculation of income, expenses and other allowances........................................................5

2.2 Computation of taxable sum.................................................................................................6

2.3 Computation of relevant tax return and its documentation...................................................8

TASK 2............................................................................................................................................9

3.1 Chargeable profits.................................................................................................................9

3.2 Tax liability to be paid..........................................................................................................9

3.3 Dealing with tax deductions................................................................................................10

4.1 Chargeable assets................................................................................................................10

4.2 Capital gain and loss...........................................................................................................10

4.3 Tax payable on capital gain.................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Tax environment which is there in UK.................................................................................1

1.2 Roles and responsibilities of Tax practitioner.......................................................................2

1.3 Obligations of tax payer and effect of non compliance........................................................4

2.1 Calculation of income, expenses and other allowances........................................................5

2.2 Computation of taxable sum.................................................................................................6

2.3 Computation of relevant tax return and its documentation...................................................8

TASK 2............................................................................................................................................9

3.1 Chargeable profits.................................................................................................................9

3.2 Tax liability to be paid..........................................................................................................9

3.3 Dealing with tax deductions................................................................................................10

4.1 Chargeable assets................................................................................................................10

4.2 Capital gain and loss...........................................................................................................10

4.3 Tax payable on capital gain.................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

In any country there are different laws in respect of taxation which are required to be

complied with. There are various levels at which it will be required to be paid and basically

classified in three stages which are central, devolved national and local government. It is

considered that tax is the major source from which revenue is earned by authorities and that will

be used for development of nation as whole (Bird, 2011). There are various aspects which will

have to be understood in this relation so that proper calculations can be made. Tax will be

calculated in different manner for individuals and different entities and for that regulations shall

be taken into consideration. In this report the taxation environment will be discussed in context

of United Kingdom.

TASK 1

1.1 Tax environment which is there in UK.

Government of any country will be imposing an obligation on all under which they will

be required to pay certain part of their income to them and that amount in known as tax. The

payer will not be receiving any direct benefit for the contribution made but will be provided with

various benefits in indirect manner (Adam, Browne and Heady, 2010). This is because the funds

will be utilised for the benefit of whole society. Tax will be categorised in various forms and that

will be imposed on all. In UK it has been mainly classified in two ways which are direct and

indirect taxes which are explained here under:

Direct taxes: These are those taxes which will be charged directly from any individual or

any other businesses and they will be required to pay the needed amount to authorities. In

this the burden of tax will have to be borne by directly by tax payer and can be paid in

two manner which will be direct payment or deduction made from income known as

TDS. Some of them are as follows:

Income tax: The amount that will be paid on total earnings will be covered under this. For this

purpose taxable income will have to be calculated in which various consideration will have to be

made. The main part of revenue is collected from this source only.

Corporation tax: The tax which will be paid by all the companies and organisations will be

included under it. If the business will not be UK based then tax will be payable on that income

which will be earned from activities that are carried out in UK.

1

In any country there are different laws in respect of taxation which are required to be

complied with. There are various levels at which it will be required to be paid and basically

classified in three stages which are central, devolved national and local government. It is

considered that tax is the major source from which revenue is earned by authorities and that will

be used for development of nation as whole (Bird, 2011). There are various aspects which will

have to be understood in this relation so that proper calculations can be made. Tax will be

calculated in different manner for individuals and different entities and for that regulations shall

be taken into consideration. In this report the taxation environment will be discussed in context

of United Kingdom.

TASK 1

1.1 Tax environment which is there in UK.

Government of any country will be imposing an obligation on all under which they will

be required to pay certain part of their income to them and that amount in known as tax. The

payer will not be receiving any direct benefit for the contribution made but will be provided with

various benefits in indirect manner (Adam, Browne and Heady, 2010). This is because the funds

will be utilised for the benefit of whole society. Tax will be categorised in various forms and that

will be imposed on all. In UK it has been mainly classified in two ways which are direct and

indirect taxes which are explained here under:

Direct taxes: These are those taxes which will be charged directly from any individual or

any other businesses and they will be required to pay the needed amount to authorities. In

this the burden of tax will have to be borne by directly by tax payer and can be paid in

two manner which will be direct payment or deduction made from income known as

TDS. Some of them are as follows:

Income tax: The amount that will be paid on total earnings will be covered under this. For this

purpose taxable income will have to be calculated in which various consideration will have to be

made. The main part of revenue is collected from this source only.

Corporation tax: The tax which will be paid by all the companies and organisations will be

included under it. If the business will not be UK based then tax will be payable on that income

which will be earned from activities that are carried out in UK.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Indirect taxes: The payment in which burden will not be directly on the tax payer will

be covered in this. In this buyers will be responsible to pay the taxes which have been

determined (Mirrlees, 2010). The sales price will be identified and then on that amount

they will be required to be charged. By this buyer is the person who will be bearing

burden of taxes which will be paid to government. Some of the taxes which will be

included in this category are custom duty, value added tax and excise duty.

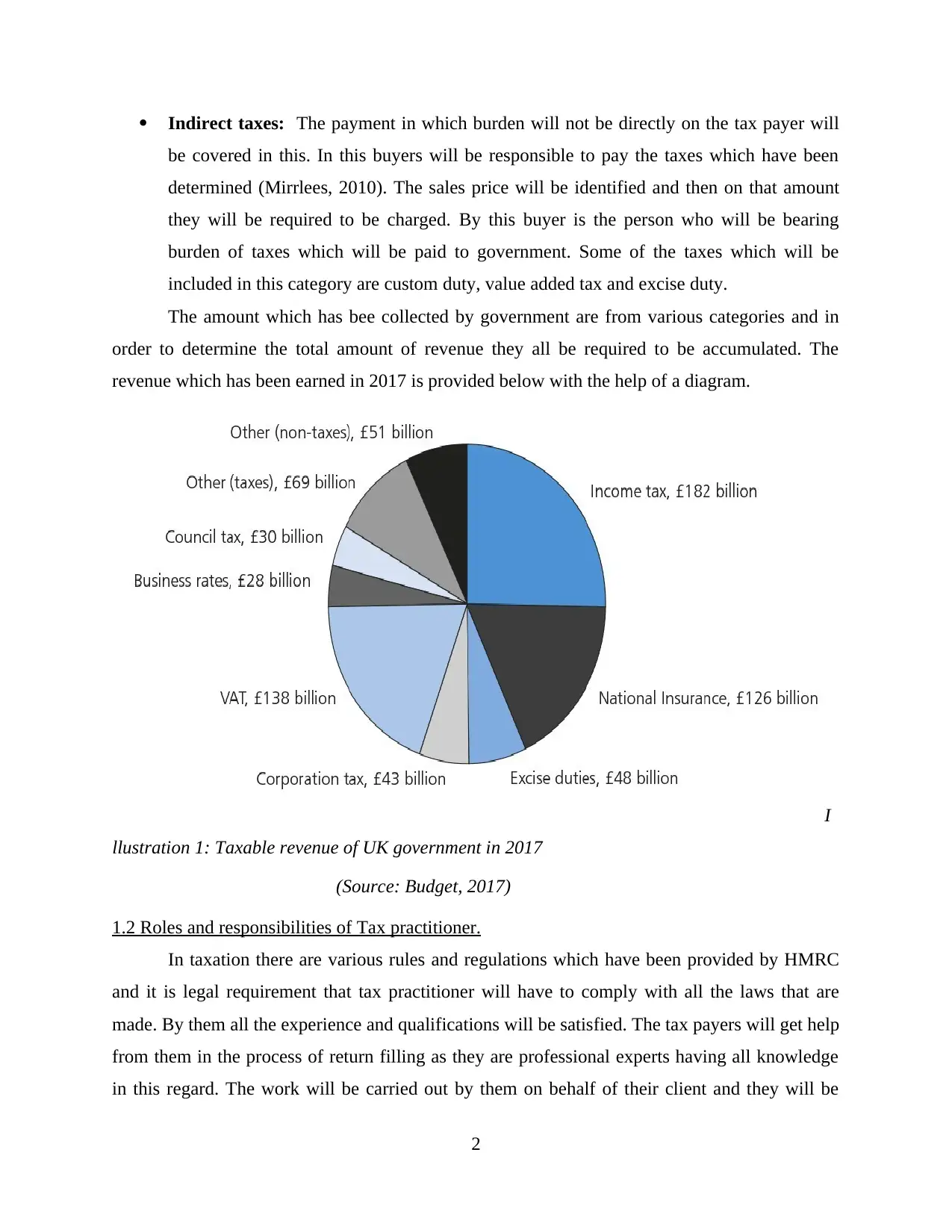

The amount which has bee collected by government are from various categories and in

order to determine the total amount of revenue they all be required to be accumulated. The

revenue which has been earned in 2017 is provided below with the help of a diagram.

I

llustration 1: Taxable revenue of UK government in 2017

(Source: Budget, 2017)

1.2 Roles and responsibilities of Tax practitioner.

In taxation there are various rules and regulations which have been provided by HMRC

and it is legal requirement that tax practitioner will have to comply with all the laws that are

made. By them all the experience and qualifications will be satisfied. The tax payers will get help

from them in the process of return filling as they are professional experts having all knowledge

in this regard. The work will be carried out by them on behalf of their client and they will be

2

be covered in this. In this buyers will be responsible to pay the taxes which have been

determined (Mirrlees, 2010). The sales price will be identified and then on that amount

they will be required to be charged. By this buyer is the person who will be bearing

burden of taxes which will be paid to government. Some of the taxes which will be

included in this category are custom duty, value added tax and excise duty.

The amount which has bee collected by government are from various categories and in

order to determine the total amount of revenue they all be required to be accumulated. The

revenue which has been earned in 2017 is provided below with the help of a diagram.

I

llustration 1: Taxable revenue of UK government in 2017

(Source: Budget, 2017)

1.2 Roles and responsibilities of Tax practitioner.

In taxation there are various rules and regulations which have been provided by HMRC

and it is legal requirement that tax practitioner will have to comply with all the laws that are

made. By them all the experience and qualifications will be satisfied. The tax payers will get help

from them in the process of return filling as they are professional experts having all knowledge

in this regard. The work will be carried out by them on behalf of their client and they will be

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

responsible to complete it and then present it before revenue and custom authority (Grown and

Valodia, 2010). There are various roles and responsibilities which will have to be fulfilled by

them and some of them are presented below:

Responsibilities which are to be fulfilled by Tax practitioner:

In the return which will be filed, it is necessary that all the information that is to be

provided shall be true and fair. So it will be required by practitioner to tell his client

regarding this and also in respect of different issues which may be faced by the

organisation about needs of audit.

There are many laws and rules which are prescribed and it is needed that they shall

perform their work in such manner by which all of them will be complied with in best

possible manner. This will be required in both cases that is while providing services to

client and also in conduction of private affairs.

It will be required that proper assistance shall be provided to client so that they can

follow all rules so that it can be ensured that calculation of tax liability is as per the

requirements.

The main aspect which is to be considered is confidentiality which means that

information of client shall not be provided to anyone without his consent.

There are various amendments which takes place in respect of provisions to be followed

and so it must be ensured that practitioner shall have adequate knowledge regarding

them. This will be necessary as then only they will be able to provide proper guidance to

their client.

Roles played by tax practitioner:

There is legal system and procedure according to which reporting is required to be done

and for that it is needed that proper knowledge shall be attained by tax practitioner (Oats,

2012). With the help of them they will be able to save their client from payment of

excessive tax. Also proper advice will be provided to client so that they can report the

information in proper manner.

The regulations, norms and standards which have been provided by HMRC shall be

complied by tax practitioner. All the relevant information will be collected by them so

that they can help their client in tax payments. With the help of data tax will be calculated

which will have to be paid on the earnings at the specified rate.

3

Valodia, 2010). There are various roles and responsibilities which will have to be fulfilled by

them and some of them are presented below:

Responsibilities which are to be fulfilled by Tax practitioner:

In the return which will be filed, it is necessary that all the information that is to be

provided shall be true and fair. So it will be required by practitioner to tell his client

regarding this and also in respect of different issues which may be faced by the

organisation about needs of audit.

There are many laws and rules which are prescribed and it is needed that they shall

perform their work in such manner by which all of them will be complied with in best

possible manner. This will be required in both cases that is while providing services to

client and also in conduction of private affairs.

It will be required that proper assistance shall be provided to client so that they can

follow all rules so that it can be ensured that calculation of tax liability is as per the

requirements.

The main aspect which is to be considered is confidentiality which means that

information of client shall not be provided to anyone without his consent.

There are various amendments which takes place in respect of provisions to be followed

and so it must be ensured that practitioner shall have adequate knowledge regarding

them. This will be necessary as then only they will be able to provide proper guidance to

their client.

Roles played by tax practitioner:

There is legal system and procedure according to which reporting is required to be done

and for that it is needed that proper knowledge shall be attained by tax practitioner (Oats,

2012). With the help of them they will be able to save their client from payment of

excessive tax. Also proper advice will be provided to client so that they can report the

information in proper manner.

The regulations, norms and standards which have been provided by HMRC shall be

complied by tax practitioner. All the relevant information will be collected by them so

that they can help their client in tax payments. With the help of data tax will be calculated

which will have to be paid on the earnings at the specified rate.

3

All the legal matter in respect of tax that will be faced by client will be dealt in proper

manner and this will be possible as taxpayers will be getting help from the information

which is submitted by practitioner to government in legal format.

All the opportunities and risk which is present in relation to policies of tax will be

understood by client with the help of assistance that will be provided by tax practitioner

(Ehrlich and Radulescu, 2017). So it will also be role of him to provide suitable advice.

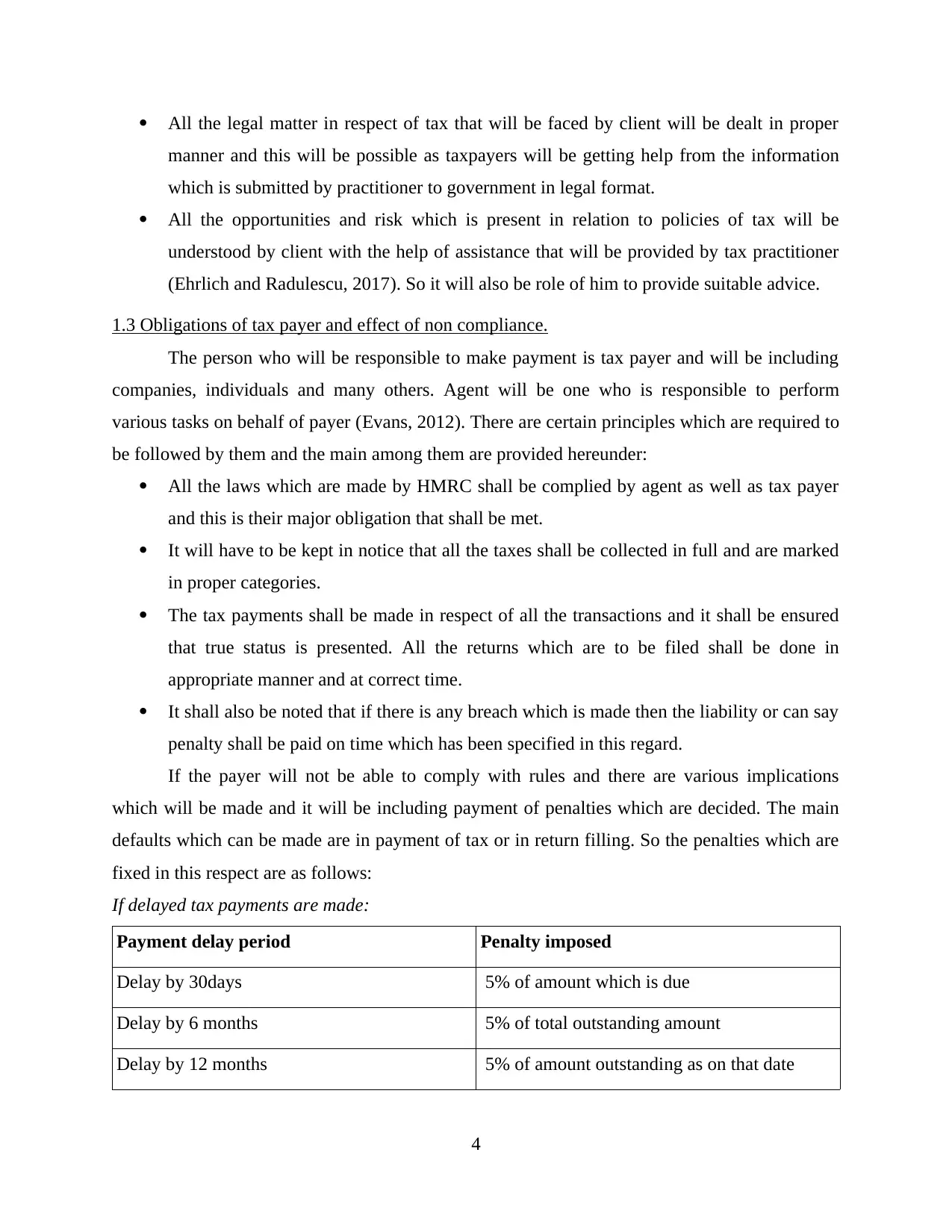

1.3 Obligations of tax payer and effect of non compliance.

The person who will be responsible to make payment is tax payer and will be including

companies, individuals and many others. Agent will be one who is responsible to perform

various tasks on behalf of payer (Evans, 2012). There are certain principles which are required to

be followed by them and the main among them are provided hereunder:

All the laws which are made by HMRC shall be complied by agent as well as tax payer

and this is their major obligation that shall be met.

It will have to be kept in notice that all the taxes shall be collected in full and are marked

in proper categories.

The tax payments shall be made in respect of all the transactions and it shall be ensured

that true status is presented. All the returns which are to be filed shall be done in

appropriate manner and at correct time.

It shall also be noted that if there is any breach which is made then the liability or can say

penalty shall be paid on time which has been specified in this regard.

If the payer will not be able to comply with rules and there are various implications

which will be made and it will be including payment of penalties which are decided. The main

defaults which can be made are in payment of tax or in return filling. So the penalties which are

fixed in this respect are as follows:

If delayed tax payments are made:

Payment delay period Penalty imposed

Delay by 30days 5% of amount which is due

Delay by 6 months 5% of total outstanding amount

Delay by 12 months 5% of amount outstanding as on that date

4

manner and this will be possible as taxpayers will be getting help from the information

which is submitted by practitioner to government in legal format.

All the opportunities and risk which is present in relation to policies of tax will be

understood by client with the help of assistance that will be provided by tax practitioner

(Ehrlich and Radulescu, 2017). So it will also be role of him to provide suitable advice.

1.3 Obligations of tax payer and effect of non compliance.

The person who will be responsible to make payment is tax payer and will be including

companies, individuals and many others. Agent will be one who is responsible to perform

various tasks on behalf of payer (Evans, 2012). There are certain principles which are required to

be followed by them and the main among them are provided hereunder:

All the laws which are made by HMRC shall be complied by agent as well as tax payer

and this is their major obligation that shall be met.

It will have to be kept in notice that all the taxes shall be collected in full and are marked

in proper categories.

The tax payments shall be made in respect of all the transactions and it shall be ensured

that true status is presented. All the returns which are to be filed shall be done in

appropriate manner and at correct time.

It shall also be noted that if there is any breach which is made then the liability or can say

penalty shall be paid on time which has been specified in this regard.

If the payer will not be able to comply with rules and there are various implications

which will be made and it will be including payment of penalties which are decided. The main

defaults which can be made are in payment of tax or in return filling. So the penalties which are

fixed in this respect are as follows:

If delayed tax payments are made:

Payment delay period Penalty imposed

Delay by 30days 5% of amount which is due

Delay by 6 months 5% of total outstanding amount

Delay by 12 months 5% of amount outstanding as on that date

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

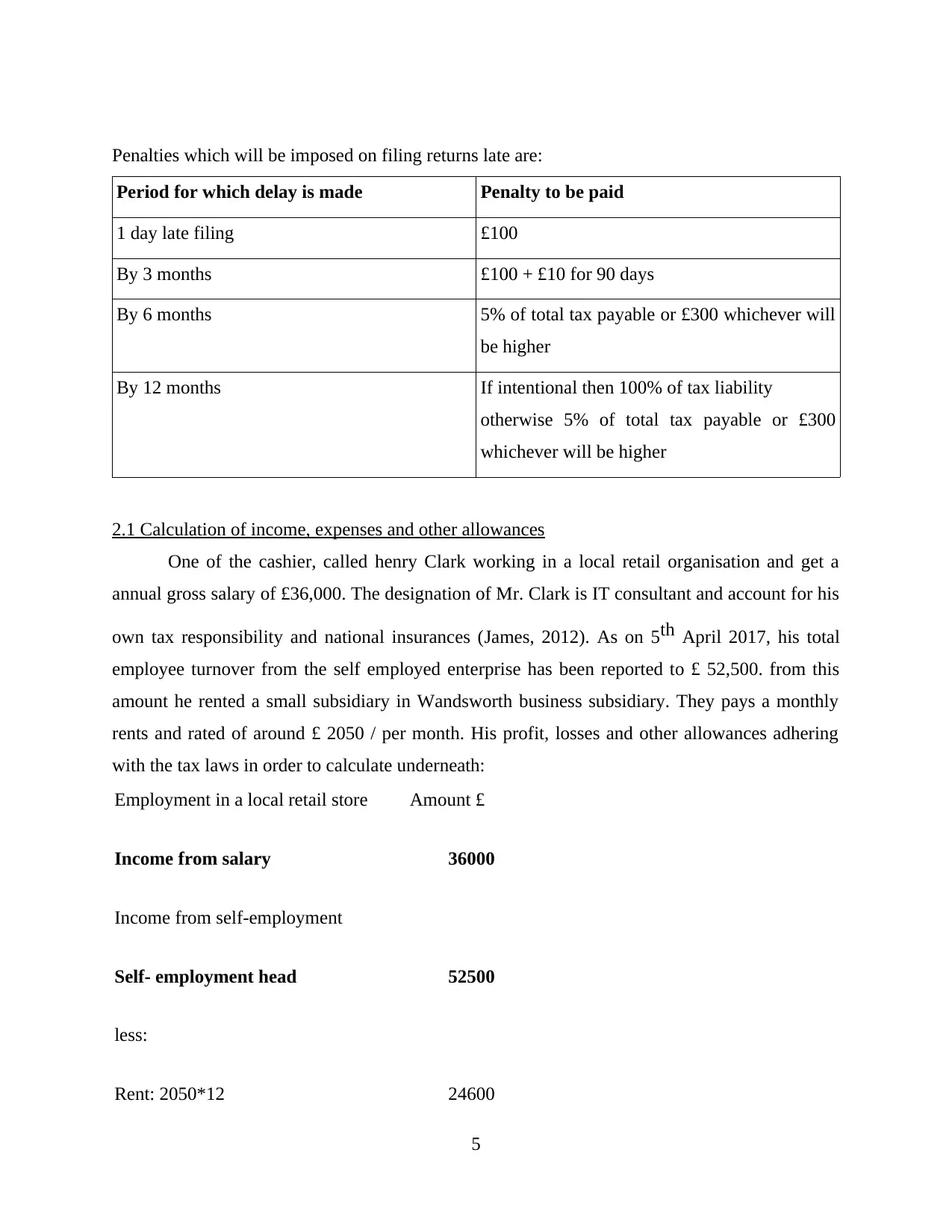

Penalties which will be imposed on filing returns late are:

Period for which delay is made Penalty to be paid

1 day late filing £100

By 3 months £100 + £10 for 90 days

By 6 months 5% of total tax payable or £300 whichever will

be higher

By 12 months If intentional then 100% of tax liability

otherwise 5% of total tax payable or £300

whichever will be higher

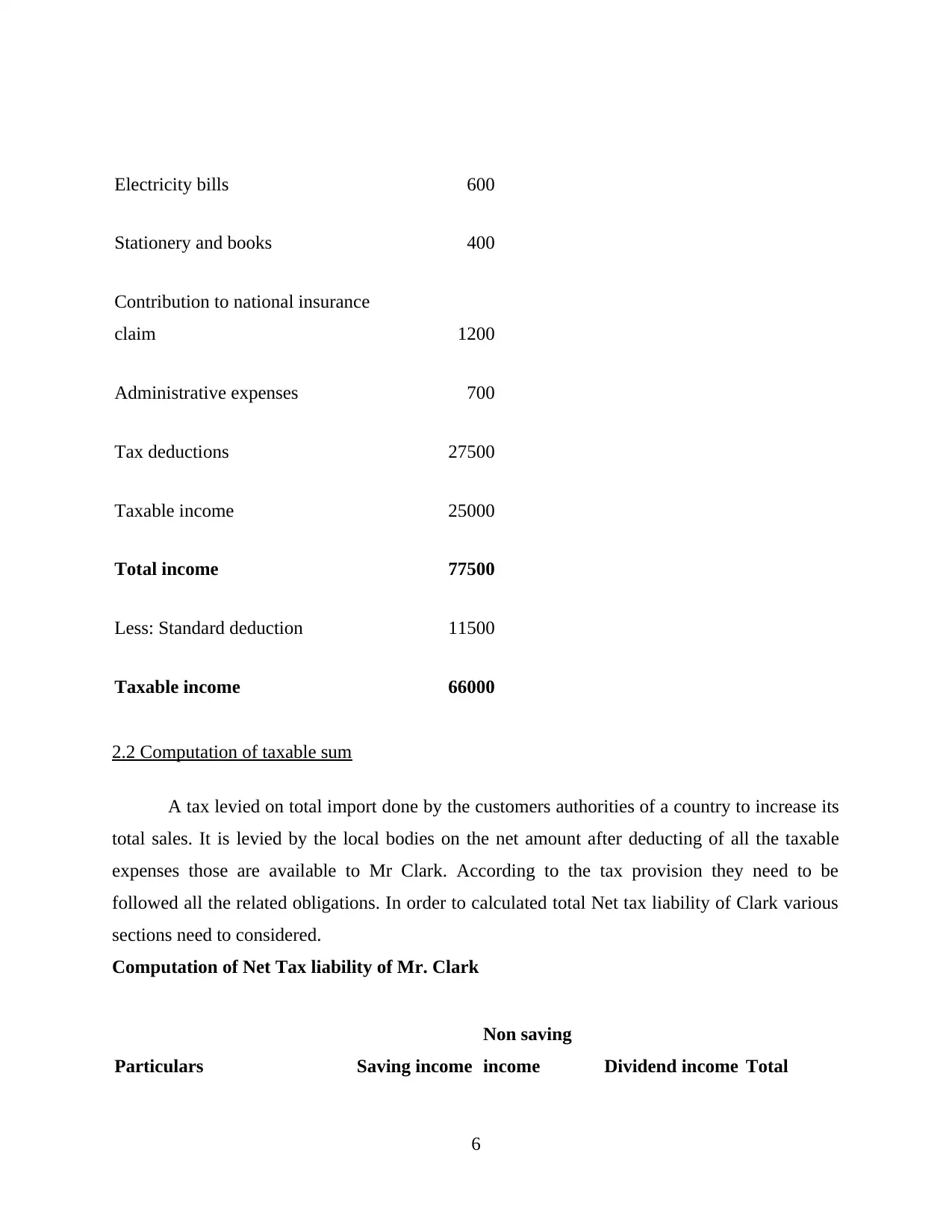

2.1 Calculation of income, expenses and other allowances

One of the cashier, called henry Clark working in a local retail organisation and get a

annual gross salary of £36,000. The designation of Mr. Clark is IT consultant and account for his

own tax responsibility and national insurances (James, 2012). As on 5th April 2017, his total

employee turnover from the self employed enterprise has been reported to £ 52,500. from this

amount he rented a small subsidiary in Wandsworth business subsidiary. They pays a monthly

rents and rated of around £ 2050 / per month. His profit, losses and other allowances adhering

with the tax laws in order to calculate underneath:

Employment in a local retail store Amount £

Income from salary 36000

Income from self-employment

Self- employment head 52500

less:

Rent: 2050*12 24600

5

Period for which delay is made Penalty to be paid

1 day late filing £100

By 3 months £100 + £10 for 90 days

By 6 months 5% of total tax payable or £300 whichever will

be higher

By 12 months If intentional then 100% of tax liability

otherwise 5% of total tax payable or £300

whichever will be higher

2.1 Calculation of income, expenses and other allowances

One of the cashier, called henry Clark working in a local retail organisation and get a

annual gross salary of £36,000. The designation of Mr. Clark is IT consultant and account for his

own tax responsibility and national insurances (James, 2012). As on 5th April 2017, his total

employee turnover from the self employed enterprise has been reported to £ 52,500. from this

amount he rented a small subsidiary in Wandsworth business subsidiary. They pays a monthly

rents and rated of around £ 2050 / per month. His profit, losses and other allowances adhering

with the tax laws in order to calculate underneath:

Employment in a local retail store Amount £

Income from salary 36000

Income from self-employment

Self- employment head 52500

less:

Rent: 2050*12 24600

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Electricity bills 600

Stationery and books 400

Contribution to national insurance

claim 1200

Administrative expenses 700

Tax deductions 27500

Taxable income 25000

Total income 77500

Less: Standard deduction 11500

Taxable income 66000

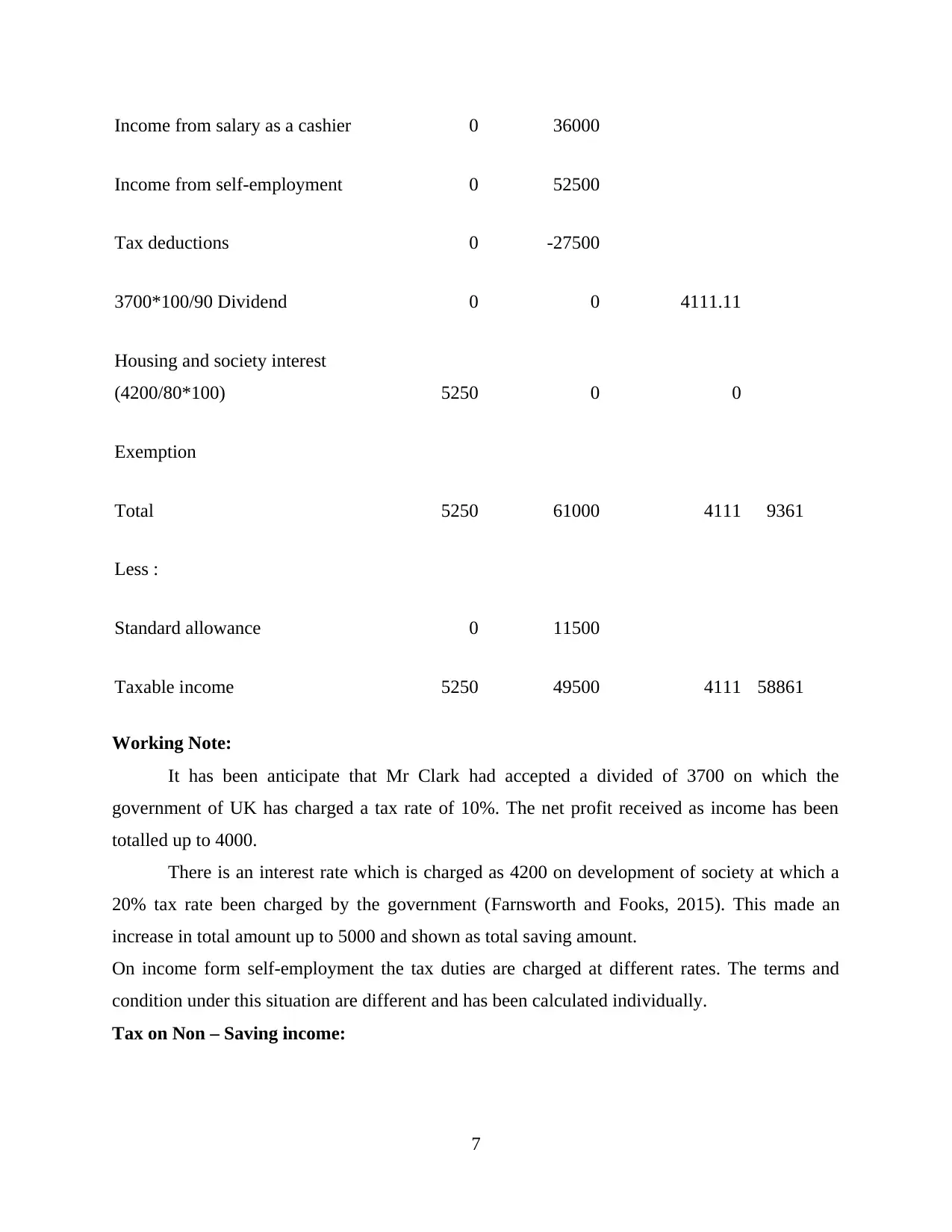

2.2 Computation of taxable sum

A tax levied on total import done by the customers authorities of a country to increase its

total sales. It is levied by the local bodies on the net amount after deducting of all the taxable

expenses those are available to Mr Clark. According to the tax provision they need to be

followed all the related obligations. In order to calculated total Net tax liability of Clark various

sections need to considered.

Computation of Net Tax liability of Mr. Clark

Particulars Saving income

Non saving

income Dividend income Total

6

Stationery and books 400

Contribution to national insurance

claim 1200

Administrative expenses 700

Tax deductions 27500

Taxable income 25000

Total income 77500

Less: Standard deduction 11500

Taxable income 66000

2.2 Computation of taxable sum

A tax levied on total import done by the customers authorities of a country to increase its

total sales. It is levied by the local bodies on the net amount after deducting of all the taxable

expenses those are available to Mr Clark. According to the tax provision they need to be

followed all the related obligations. In order to calculated total Net tax liability of Clark various

sections need to considered.

Computation of Net Tax liability of Mr. Clark

Particulars Saving income

Non saving

income Dividend income Total

6

Income from salary as a cashier 0 36000

Income from self-employment 0 52500

Tax deductions 0 -27500

3700*100/90 Dividend 0 0 4111.11

Housing and society interest

(4200/80*100) 5250 0 0

Exemption

Total 5250 61000 4111 9361

Less :

Standard allowance 0 11500

Taxable income 5250 49500 4111 58861

Working Note:

It has been anticipate that Mr Clark had accepted a divided of 3700 on which the

government of UK has charged a tax rate of 10%. The net profit received as income has been

totalled up to 4000.

There is an interest rate which is charged as 4200 on development of society at which a

20% tax rate been charged by the government (Farnsworth and Fooks, 2015). This made an

increase in total amount up to 5000 and shown as total saving amount.

On income form self-employment the tax duties are charged at different rates. The terms and

condition under this situation are different and has been calculated individually.

Tax on Non – Saving income:

7

Income from self-employment 0 52500

Tax deductions 0 -27500

3700*100/90 Dividend 0 0 4111.11

Housing and society interest

(4200/80*100) 5250 0 0

Exemption

Total 5250 61000 4111 9361

Less :

Standard allowance 0 11500

Taxable income 5250 49500 4111 58861

Working Note:

It has been anticipate that Mr Clark had accepted a divided of 3700 on which the

government of UK has charged a tax rate of 10%. The net profit received as income has been

totalled up to 4000.

There is an interest rate which is charged as 4200 on development of society at which a

20% tax rate been charged by the government (Farnsworth and Fooks, 2015). This made an

increase in total amount up to 5000 and shown as total saving amount.

On income form self-employment the tax duties are charged at different rates. The terms and

condition under this situation are different and has been calculated individually.

Tax on Non – Saving income:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

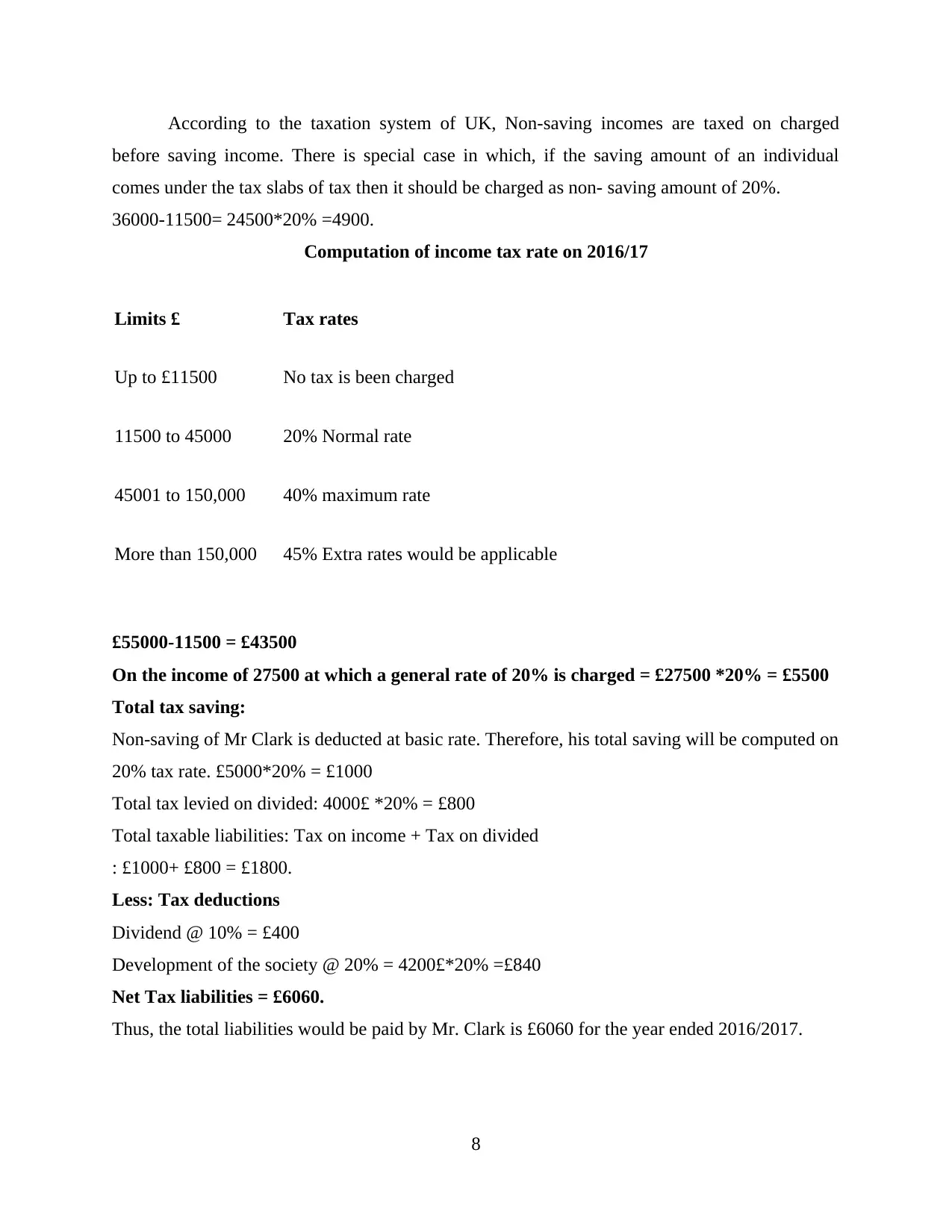

According to the taxation system of UK, Non-saving incomes are taxed on charged

before saving income. There is special case in which, if the saving amount of an individual

comes under the tax slabs of tax then it should be charged as non- saving amount of 20%.

36000-11500= 24500*20% =4900.

Computation of income tax rate on 2016/17

Limits £ Tax rates

Up to £11500 No tax is been charged

11500 to 45000 20% Normal rate

45001 to 150,000 40% maximum rate

More than 150,000 45% Extra rates would be applicable

£55000-11500 = £43500

On the income of 27500 at which a general rate of 20% is charged = £27500 *20% = £5500

Total tax saving:

Non-saving of Mr Clark is deducted at basic rate. Therefore, his total saving will be computed on

20% tax rate. £5000*20% = £1000

Total tax levied on divided: 4000£ *20% = £800

Total taxable liabilities: Tax on income + Tax on divided

: £1000+ £800 = £1800.

Less: Tax deductions

Dividend @ 10% = £400

Development of the society @ 20% = 4200£*20% =£840

Net Tax liabilities = £6060.

Thus, the total liabilities would be paid by Mr. Clark is £6060 for the year ended 2016/2017.

8

before saving income. There is special case in which, if the saving amount of an individual

comes under the tax slabs of tax then it should be charged as non- saving amount of 20%.

36000-11500= 24500*20% =4900.

Computation of income tax rate on 2016/17

Limits £ Tax rates

Up to £11500 No tax is been charged

11500 to 45000 20% Normal rate

45001 to 150,000 40% maximum rate

More than 150,000 45% Extra rates would be applicable

£55000-11500 = £43500

On the income of 27500 at which a general rate of 20% is charged = £27500 *20% = £5500

Total tax saving:

Non-saving of Mr Clark is deducted at basic rate. Therefore, his total saving will be computed on

20% tax rate. £5000*20% = £1000

Total tax levied on divided: 4000£ *20% = £800

Total taxable liabilities: Tax on income + Tax on divided

: £1000+ £800 = £1800.

Less: Tax deductions

Dividend @ 10% = £400

Development of the society @ 20% = 4200£*20% =£840

Net Tax liabilities = £6060.

Thus, the total liabilities would be paid by Mr. Clark is £6060 for the year ended 2016/2017.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Computation of relevant tax return and its documentation

According to the tax atmosphere, there are various paper and documentation is been

required in order to fill and tax return. Different taxation requirement must be fulfilled. So that

tax contributor needs to comply with its concern statements. Those are mentioned underneath:

Form no. 64 – 8: Under this form various deals and contracts are mentioned among tax payer

and tax professional. Government can uses it in order to interact with the tax agents, accountant

and other concern advisors those are working on the behalf of tax payer (Winer, Profeta and

Hettich, 2013). This form explains official document for which professional has been authorised

to communicated with individual and other businesses taxation system.

Form SA 10 3S: It consist of details regarding income from self-employment, VAT, applicable

and non applicable allowances those are required under taxable head.

Form SA 102: It is related with the individual employment form which is related with those

people who are part time and full time employed. It is important for them to file tax return in

order to save their income.

SA 105: It is said to be UK property form which is used by an individual or other rental

businesses those are associated with generating more income form their land and properties.

P60: It is necessary to all the employers to provide a P60 form to their employees at the last

financial year. It is related with total earning, pension and NIC contribution and other tax

deductions.

P87: It is that form which is related with those claims which are work based expenses and used

by the tax contributors not the self-employed customers.

TASK 2

3.1 Chargeable profits.

The amount on which tax will be paid is chargeable profit. Robin limited is one of the

business which is operating in UK and its profits for year ending 2017 as as follows:

Particulars Amount

Operating profit for the year 125600

Income earned from property 3600

Capital gain 28000

9

According to the tax atmosphere, there are various paper and documentation is been

required in order to fill and tax return. Different taxation requirement must be fulfilled. So that

tax contributor needs to comply with its concern statements. Those are mentioned underneath:

Form no. 64 – 8: Under this form various deals and contracts are mentioned among tax payer

and tax professional. Government can uses it in order to interact with the tax agents, accountant

and other concern advisors those are working on the behalf of tax payer (Winer, Profeta and

Hettich, 2013). This form explains official document for which professional has been authorised

to communicated with individual and other businesses taxation system.

Form SA 10 3S: It consist of details regarding income from self-employment, VAT, applicable

and non applicable allowances those are required under taxable head.

Form SA 102: It is related with the individual employment form which is related with those

people who are part time and full time employed. It is important for them to file tax return in

order to save their income.

SA 105: It is said to be UK property form which is used by an individual or other rental

businesses those are associated with generating more income form their land and properties.

P60: It is necessary to all the employers to provide a P60 form to their employees at the last

financial year. It is related with total earning, pension and NIC contribution and other tax

deductions.

P87: It is that form which is related with those claims which are work based expenses and used

by the tax contributors not the self-employed customers.

TASK 2

3.1 Chargeable profits.

The amount on which tax will be paid is chargeable profit. Robin limited is one of the

business which is operating in UK and its profits for year ending 2017 as as follows:

Particulars Amount

Operating profit for the year 125600

Income earned from property 3600

Capital gain 28000

9

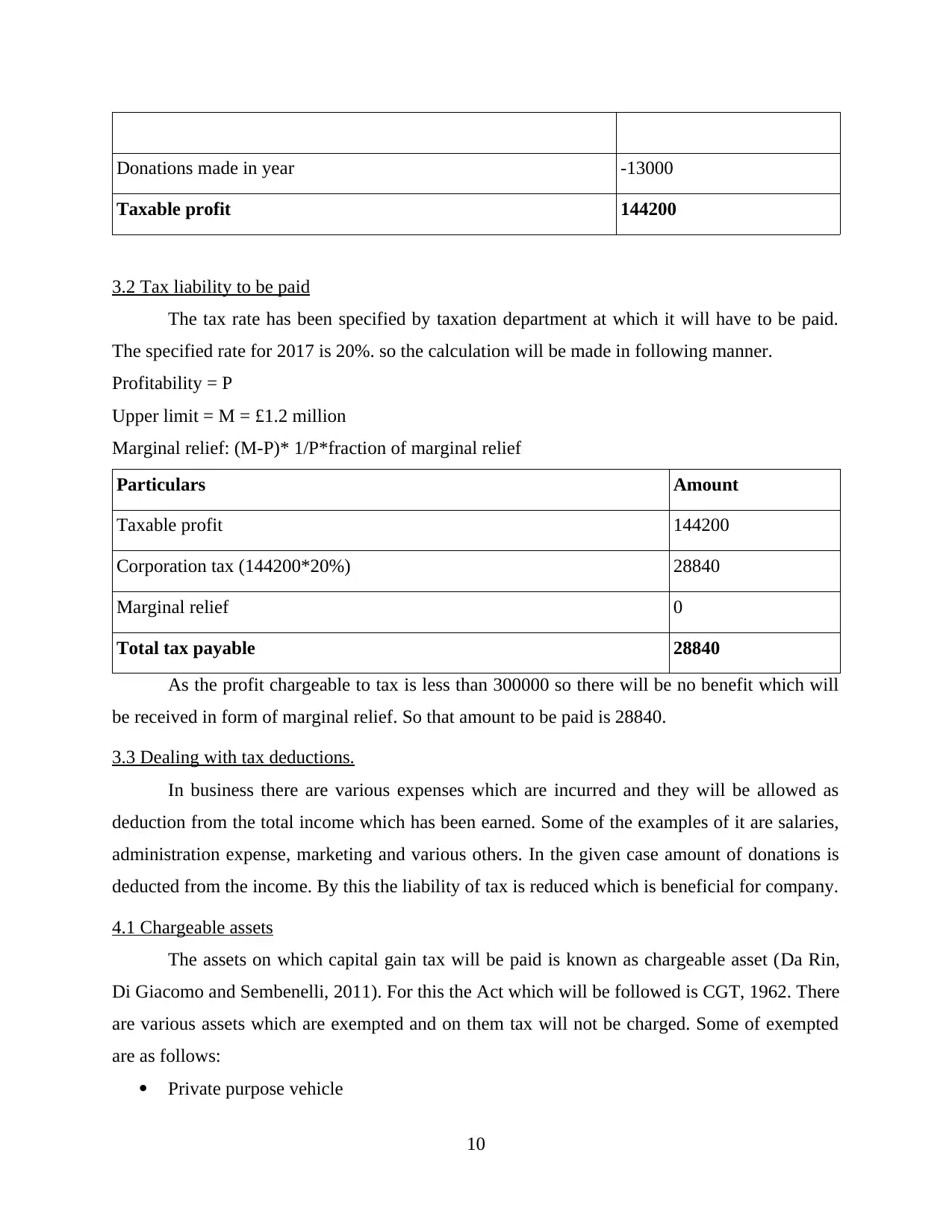

Donations made in year -13000

Taxable profit 144200

3.2 Tax liability to be paid

The tax rate has been specified by taxation department at which it will have to be paid.

The specified rate for 2017 is 20%. so the calculation will be made in following manner.

Profitability = P

Upper limit = M = £1.2 million

Marginal relief: (M-P)* 1/P*fraction of marginal relief

Particulars Amount

Taxable profit 144200

Corporation tax (144200*20%) 28840

Marginal relief 0

Total tax payable 28840

As the profit chargeable to tax is less than 300000 so there will be no benefit which will

be received in form of marginal relief. So that amount to be paid is 28840.

3.3 Dealing with tax deductions.

In business there are various expenses which are incurred and they will be allowed as

deduction from the total income which has been earned. Some of the examples of it are salaries,

administration expense, marketing and various others. In the given case amount of donations is

deducted from the income. By this the liability of tax is reduced which is beneficial for company.

4.1 Chargeable assets

The assets on which capital gain tax will be paid is known as chargeable asset (Da Rin,

Di Giacomo and Sembenelli, 2011). For this the Act which will be followed is CGT, 1962. There

are various assets which are exempted and on them tax will not be charged. Some of exempted

are as follows:

Private purpose vehicle

10

Taxable profit 144200

3.2 Tax liability to be paid

The tax rate has been specified by taxation department at which it will have to be paid.

The specified rate for 2017 is 20%. so the calculation will be made in following manner.

Profitability = P

Upper limit = M = £1.2 million

Marginal relief: (M-P)* 1/P*fraction of marginal relief

Particulars Amount

Taxable profit 144200

Corporation tax (144200*20%) 28840

Marginal relief 0

Total tax payable 28840

As the profit chargeable to tax is less than 300000 so there will be no benefit which will

be received in form of marginal relief. So that amount to be paid is 28840.

3.3 Dealing with tax deductions.

In business there are various expenses which are incurred and they will be allowed as

deduction from the total income which has been earned. Some of the examples of it are salaries,

administration expense, marketing and various others. In the given case amount of donations is

deducted from the income. By this the liability of tax is reduced which is beneficial for company.

4.1 Chargeable assets

The assets on which capital gain tax will be paid is known as chargeable asset (Da Rin,

Di Giacomo and Sembenelli, 2011). For this the Act which will be followed is CGT, 1962. There

are various assets which are exempted and on them tax will not be charged. Some of exempted

are as follows:

Private purpose vehicle

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.