Taxation System Analysis: Ford Motor Corp Operations

VerifiedAdded on 2021/01/03

|14

|4115

|495

Report

AI Summary

This report provides a comprehensive analysis of taxation systems, focusing on the operations of Ford Motor Corp in the UK, US, and Hungary. It delves into the intricacies of taxation, examining tax liabilities for both unincorporated and incorporated industries. The report explores the impact of legal ...

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Analysing the taxation system with consideration of legislations based on scenario............1

M1 Critical examination of taxation system in several countries................................................3

TASK 2............................................................................................................................................4

P2 Determining the tax liabilities for unincorporated industries.................................................4

M2 Implicating models and interpretation of outcomes..............................................................6

TASK 3............................................................................................................................................6

P3 Identifying tax liabilities for incorporated industry................................................................6

M3 Application of relevant models and interpretation of outcomes...........................................8

TASK 4............................................................................................................................................9

P4 Determination of impacts of key legal and ethical constraints on different industry.............9

M4 Critical evaluation of impacts key legal and ethical constraints on application to different

organisation................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Analysing the taxation system with consideration of legislations based on scenario............1

M1 Critical examination of taxation system in several countries................................................3

TASK 2............................................................................................................................................4

P2 Determining the tax liabilities for unincorporated industries.................................................4

M2 Implicating models and interpretation of outcomes..............................................................6

TASK 3............................................................................................................................................6

P3 Identifying tax liabilities for incorporated industry................................................................6

M3 Application of relevant models and interpretation of outcomes...........................................8

TASK 4............................................................................................................................................9

P4 Determination of impacts of key legal and ethical constraints on different industry.............9

M4 Critical evaluation of impacts key legal and ethical constraints on application to different

organisation................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

To analyse charges on revenue and income generated throughout a year by individual as

well as a business unit on which influences of legislations will help in presenting an appropriate

analysis over data base. In the present report, there will be discussion based on Ford Motor Corp.

and its operations in UK, US and Hungary. It also identifies the differences between taxation

system and legal consequences which are being used in determining tax liabilities of

organisation. Moreover, this report will also suggest techniques to improves profitability as well

as various ways to meet taxable requirements at right time.

TASK 1

P1 Analysing the taxation system with consideration of legislations based on scenario

Introduction to given scenario

Ford Motor Corp had been operating in various countries on which they are performing

trading activities in UK, US and Hungary branches. It had been analysed that, Ford is retaining

profitable revenue through UK and Hungary while US is comparatively having poor

performance as they are in losses from several years. It has been estimated by these branches that

they will retain profitability in upcoming period.

Defining taxation and explaining taxation system

Taxation:

Taxation is a process on which income of an individual or a corporation has been

measured on tax liabilities. The charges on income have been charged with influences of

government authorities and legislatures in country (A survey of the UK tax system, 2016).

However, there have been differences in taxable charges which were being charged on income

and revenue generated by any concern. There have been differences in forms of payment and

market exchanges which compiles government for implicating legal actions and implication of

implicit or explicit threat of force.

Taxation system:

It is a system where all revenue and income generated by an individual and corporation

will be charged on the basis of income scales and tax slabs. There are various acts and

amendments which are being presented by legal authorities in UK, US and Hungary with respect

to make appropriate development of policies (Public Economics: Indirect Taxation, 2016). The

purpose behind charging taxes on commodities and earnings is for generating reserves and

1

To analyse charges on revenue and income generated throughout a year by individual as

well as a business unit on which influences of legislations will help in presenting an appropriate

analysis over data base. In the present report, there will be discussion based on Ford Motor Corp.

and its operations in UK, US and Hungary. It also identifies the differences between taxation

system and legal consequences which are being used in determining tax liabilities of

organisation. Moreover, this report will also suggest techniques to improves profitability as well

as various ways to meet taxable requirements at right time.

TASK 1

P1 Analysing the taxation system with consideration of legislations based on scenario

Introduction to given scenario

Ford Motor Corp had been operating in various countries on which they are performing

trading activities in UK, US and Hungary branches. It had been analysed that, Ford is retaining

profitable revenue through UK and Hungary while US is comparatively having poor

performance as they are in losses from several years. It has been estimated by these branches that

they will retain profitability in upcoming period.

Defining taxation and explaining taxation system

Taxation:

Taxation is a process on which income of an individual or a corporation has been

measured on tax liabilities. The charges on income have been charged with influences of

government authorities and legislatures in country (A survey of the UK tax system, 2016).

However, there have been differences in taxable charges which were being charged on income

and revenue generated by any concern. There have been differences in forms of payment and

market exchanges which compiles government for implicating legal actions and implication of

implicit or explicit threat of force.

Taxation system:

It is a system where all revenue and income generated by an individual and corporation

will be charged on the basis of income scales and tax slabs. There are various acts and

amendments which are being presented by legal authorities in UK, US and Hungary with respect

to make appropriate development of policies (Public Economics: Indirect Taxation, 2016). The

purpose behind charging taxes on commodities and earnings is for generating reserves and

1

You're viewing a preview

Unlock full access by subscribing today!

revenue for government for their capital expenditures. It includes developing infrastructural

facilities in country, improving wealth of society as well as funding in various development or

disaster management activities.

In UK there have been influences of HMRC or central government in tax planning and

controlling the taxation system of economy. They primarily consider the income tax, national

insurance contribution, value added tax, fuel duty, corporation tax etc. to manage the economic

stability.

Clear analysis over UK taxation system with identifying 4 direct and indirect taxation

systems

The clear examination over the UK taxation system on which there are various direct and

indirect taxes which have been levied by government in respect to make appropriate

ascertainment of the charges which are to be collected from the individual (von Ehrlich and

Radulescu, 2017). However, in this country there is taxes have been based on central and local

governmental operations which are to be charged by them with respect to generated reserves for

capital expenditures. There are various direct and indirect taxes which are currently enacted by

UK government in practice such as:

Direct taxes:

In accordance with the influences of central government on which HMRC makes plans

and policies for analysing the costs implicated in various activities. These governs the taxation

system for the major tax practices in the country (Liu, 2018). It includes the taxation for practices

which includes:

Income tax

Corporation tax

inheritance tax

capital gain tax

Indirect taxes:

In respect with considering the indirect taxes which are to be payable and legislated by

the local and state government. These are the taxes which were charged on product and services

along with its total price (Onaran, Nikolaidi and Obst, 2017). There will be influences of the

central government only for passing the bills or making changes in the rates of taxes. It includes

the taxes such as:

2

facilities in country, improving wealth of society as well as funding in various development or

disaster management activities.

In UK there have been influences of HMRC or central government in tax planning and

controlling the taxation system of economy. They primarily consider the income tax, national

insurance contribution, value added tax, fuel duty, corporation tax etc. to manage the economic

stability.

Clear analysis over UK taxation system with identifying 4 direct and indirect taxation

systems

The clear examination over the UK taxation system on which there are various direct and

indirect taxes which have been levied by government in respect to make appropriate

ascertainment of the charges which are to be collected from the individual (von Ehrlich and

Radulescu, 2017). However, in this country there is taxes have been based on central and local

governmental operations which are to be charged by them with respect to generated reserves for

capital expenditures. There are various direct and indirect taxes which are currently enacted by

UK government in practice such as:

Direct taxes:

In accordance with the influences of central government on which HMRC makes plans

and policies for analysing the costs implicated in various activities. These governs the taxation

system for the major tax practices in the country (Liu, 2018). It includes the taxation for practices

which includes:

Income tax

Corporation tax

inheritance tax

capital gain tax

Indirect taxes:

In respect with considering the indirect taxes which are to be payable and legislated by

the local and state government. These are the taxes which were charged on product and services

along with its total price (Onaran, Nikolaidi and Obst, 2017). There will be influences of the

central government only for passing the bills or making changes in the rates of taxes. It includes

the taxes such as:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales tax

Value Added tax

Excise duties

Stamp duty

Taxation legislations in UK which have implications for national taxation

In UK there have been consideration of various legislative influences which have been

enacted by the government in context with developing fair taxation practices (Sikka, 2017).

However, there are various laws and amendments which have been made by legislative

authorities stated in UK and various countries. EU have made various laws which are relevance

with the taxation and the civil operations in country. In approach towards it there have been

influences of various taxation legislations such as custom duties, CJEU etc.

Along with this there are various taxable remedies which were being presented by the EU

laws in UK which helps in protecting SME's to have fair operational practices which will be

adequate in managing their growth in the society (McCluskey and Franzsen, 2017). Moreover,

there have been various taxation which were levied on the transportation of the goods such as

Vehicle excise duty, fuel duty, air passenger duty.

M1 Critical examination of taxation system in several countries

Critical analysis on the different taxation system which are operating close economic and

trade practices with UK

In relation with analysing the trader practices made by various other nations with UK on

which they various wants and requirements which will be attentive and helpful to the

government in meeting the targets at the right time. EU countries are highly engaged with

making trade practices as well as operating close economic practices with UK. There have been

various amendments and legislation which have been made by the government of these countries

to protect the rights of individual as well as corporations in UK (Cromwell, 2017). There have

been special allowances and remedies which are being involved in country which helps them in

taking advantages of such policies. UK has implications to the national taxation system where

countries are members of trade blocs.

In consideration with APEC (Asia- Pacific Economic Cooperation) which is facilitating

the free trade services in entire Asia- Pacific regime. The motive is for financially developing the

organisation to have appropriate independent growth in the time. However, it was being

3

Value Added tax

Excise duties

Stamp duty

Taxation legislations in UK which have implications for national taxation

In UK there have been consideration of various legislative influences which have been

enacted by the government in context with developing fair taxation practices (Sikka, 2017).

However, there are various laws and amendments which have been made by legislative

authorities stated in UK and various countries. EU have made various laws which are relevance

with the taxation and the civil operations in country. In approach towards it there have been

influences of various taxation legislations such as custom duties, CJEU etc.

Along with this there are various taxable remedies which were being presented by the EU

laws in UK which helps in protecting SME's to have fair operational practices which will be

adequate in managing their growth in the society (McCluskey and Franzsen, 2017). Moreover,

there have been various taxation which were levied on the transportation of the goods such as

Vehicle excise duty, fuel duty, air passenger duty.

M1 Critical examination of taxation system in several countries

Critical analysis on the different taxation system which are operating close economic and

trade practices with UK

In relation with analysing the trader practices made by various other nations with UK on

which they various wants and requirements which will be attentive and helpful to the

government in meeting the targets at the right time. EU countries are highly engaged with

making trade practices as well as operating close economic practices with UK. There have been

various amendments and legislation which have been made by the government of these countries

to protect the rights of individual as well as corporations in UK (Cromwell, 2017). There have

been special allowances and remedies which are being involved in country which helps them in

taking advantages of such policies. UK has implications to the national taxation system where

countries are members of trade blocs.

In consideration with APEC (Asia- Pacific Economic Cooperation) which is facilitating

the free trade services in entire Asia- Pacific regime. The motive is for financially developing the

organisation to have appropriate independent growth in the time. However, it was being

3

established with respect to promoting the trade practices among nations as well as having

favourable economic growth in the times (Chepulis and et.al., 2018). Along with this this trade

bloc have helped in developing the agriculture and raw material businesses other than EU.

Moreover, NAFTA (North American Free Trade Agreement) However, this agreement

will be based on facilitating the adequate free trade practices among the nations. Thus, on which

there will no duty charges levied on the material which are delivered and received by the

member countries.

Interrelationship between two taxation system which are performing in 2 different

countries

As per considering taxation operations which are being performed in US and UK have

various similarities in the legislations, laws and regulations. Therefore, it can be said that, the

corporate tax rates in both the nation have comparatively similar rates. UK has 20% while US

has 21% of the rate. In respect with such rates on which it can be said that US is charging

comparatively higher corporate tax than UK (Hirsbrunner and Lauterjung, 2017). Therefore, in

accordance with OECD US have corporation tax of 39% on average which is twice of that which

is paid in UK. However, there have been taxation rates which varies between states.

TASK 2

P2 Determining the tax liabilities for unincorporated industries

Unincorporated organisation:

These are the business ventures on which there are influences of group of individuals

which come across of various nations in relation with retaining proportionality. Thus, they

operate the business as voluntary practice on which they require contractual agreements,

responsibilities for debts as well as contractual obligations (McKee, Muir and Moore, 2017).

There has been variation in taxable implications as many of them will be charged on the profits

earned by them on the corporate rate taxes while clubs, association, community and society are

also being liable to make taxable payment on the basis of corporate tax rates.

Characteristics and background:

There have been various features and characteristics of these unincorporated associations

which are based on several variations in the skills and innovations such as:

Establishment costs: In relation with launching an unincorporated firm in the market

there will be no requirement for having any registration of the firm (Moore, 2018).

4

favourable economic growth in the times (Chepulis and et.al., 2018). Along with this this trade

bloc have helped in developing the agriculture and raw material businesses other than EU.

Moreover, NAFTA (North American Free Trade Agreement) However, this agreement

will be based on facilitating the adequate free trade practices among the nations. Thus, on which

there will no duty charges levied on the material which are delivered and received by the

member countries.

Interrelationship between two taxation system which are performing in 2 different

countries

As per considering taxation operations which are being performed in US and UK have

various similarities in the legislations, laws and regulations. Therefore, it can be said that, the

corporate tax rates in both the nation have comparatively similar rates. UK has 20% while US

has 21% of the rate. In respect with such rates on which it can be said that US is charging

comparatively higher corporate tax than UK (Hirsbrunner and Lauterjung, 2017). Therefore, in

accordance with OECD US have corporation tax of 39% on average which is twice of that which

is paid in UK. However, there have been taxation rates which varies between states.

TASK 2

P2 Determining the tax liabilities for unincorporated industries

Unincorporated organisation:

These are the business ventures on which there are influences of group of individuals

which come across of various nations in relation with retaining proportionality. Thus, they

operate the business as voluntary practice on which they require contractual agreements,

responsibilities for debts as well as contractual obligations (McKee, Muir and Moore, 2017).

There has been variation in taxable implications as many of them will be charged on the profits

earned by them on the corporate rate taxes while clubs, association, community and society are

also being liable to make taxable payment on the basis of corporate tax rates.

Characteristics and background:

There have been various features and characteristics of these unincorporated associations

which are based on several variations in the skills and innovations such as:

Establishment costs: In relation with launching an unincorporated firm in the market

there will be no requirement for having any registration of the firm (Moore, 2018).

4

You're viewing a preview

Unlock full access by subscribing today!

Therefore, there will be no requirement of large amount of funds which will be invested

in the business.

Liabilities: These organisations do not have any legal identity in the market. Therefore,

the group of individuals which have planned to operate a voluntary business with a

motive to retain the profits which do not support any identification in the market.

Therefore, in respect with this, there will be no such liabilities and trade of ownership

(Haag, 2017). Along with this, these businesses are self-governed of in partnership where

no more than 10 employees will work so their only liabilities and debts are associated

with making payment to the staff, suppliers and interest in bank as if they took any loan.

Tax treatment: In relation with analysing the tax consequences which are associated

with the unincorporated association on which majority of them make payments on the

corporate tax rates (Rowland, 2017). Club members, sports and various relevant business

may also make payment to the government on their earned revenue.

Ongoing governance and regulatory obligations: There have not been any obligation

and influences of government in voluntary business as if there are any unlawful and

illegal activities performed by any individual.

Advantages and disadvantages of unincorporated industry:

In respect to the operational performance and the activities which are being performed

under Unincorporated organisation there can be various benefits and loopholes associated with

the trade practices and the operational activities by such industries.

Advantages

No restrictions on the entry and exit

No requirement of registering the

organisation

Lower cost implication in various

activities.

Requirement of small workforce as it is

self-governed business.

Higher profitability.

Disadvantages

It does not become able to create the

identity in the market.

Improper ascertainment of cost implied

in the business as there is lack of

accountability.

Lack of appropriate governance in

terms of partnership business as there

will be chances of having various

loopholes.

5

in the business.

Liabilities: These organisations do not have any legal identity in the market. Therefore,

the group of individuals which have planned to operate a voluntary business with a

motive to retain the profits which do not support any identification in the market.

Therefore, in respect with this, there will be no such liabilities and trade of ownership

(Haag, 2017). Along with this, these businesses are self-governed of in partnership where

no more than 10 employees will work so their only liabilities and debts are associated

with making payment to the staff, suppliers and interest in bank as if they took any loan.

Tax treatment: In relation with analysing the tax consequences which are associated

with the unincorporated association on which majority of them make payments on the

corporate tax rates (Rowland, 2017). Club members, sports and various relevant business

may also make payment to the government on their earned revenue.

Ongoing governance and regulatory obligations: There have not been any obligation

and influences of government in voluntary business as if there are any unlawful and

illegal activities performed by any individual.

Advantages and disadvantages of unincorporated industry:

In respect to the operational performance and the activities which are being performed

under Unincorporated organisation there can be various benefits and loopholes associated with

the trade practices and the operational activities by such industries.

Advantages

No restrictions on the entry and exit

No requirement of registering the

organisation

Lower cost implication in various

activities.

Requirement of small workforce as it is

self-governed business.

Higher profitability.

Disadvantages

It does not become able to create the

identity in the market.

Improper ascertainment of cost implied

in the business as there is lack of

accountability.

Lack of appropriate governance in

terms of partnership business as there

will be chances of having various

loopholes.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Personal taxation and taxation relevant with partnership and sole traders

The term personal taxation is referring to the taxation practices which have been made by a

person on their own such as analysis over the own tax consequences as well as remedies

associated with the business (Lacey, McMunn and Webb, 2017). Moreover, there will be less

influences of any legal tax practitioner who would make efforts and analysis over the income

generated by the organisation.

Sole trader: Here the business is governed by a single person which is liable for collecting

all the information and making appropriate cost analysis based on various operations in the

organisation. Therefore, in respect with this, there are various tax consequence which allows the

professionals in making qualitative efforts. Here the owner will analyse the income generated by

his business throughout year on which they measure taxable income (Theodore, Theodore and

Syrrakos, 2017). The identification of such taxable income will be based on analysing the

remedies and allowansce3s which have been awarded by government will be adjusted by their

own.

Partnership: In partnership firms there will be influences of more than 1 person. Thus, in

rems of decsidi9mn g the tax remedies and payments which are to be made by them on their

generated income which requires them to make planning and decision based on such issues (von

Ehrlich and Radulescu, 2017). Moreover, here the company is itself makes payment to taxes on

the basis of analysing the charges, taxable slab as well as deductions.

M2 Implicating models and interpretation of outcomes.

Calculating taxation liabilities

In relation with analysing the tax consequences as well as various liabilities’, remedies

which are being associated with the unincorporated organisation will be measured in

identification of tax liabilities.

TASK 3

P3 Identifying tax liabilities for incorporated industry

Incorporated organisation: In respect with analysing the legal structure of the

incorporated business unit which has their own legal identity in the market. These are denoted

similar as a person who is being operating the trade practices among the society. therefore, in

respect with the framework of these organisations where group is not being liable personally for

the group actions (Onaran, Nikolaidi and Obst, 2017). Therefore, there will be requirement of

6

The term personal taxation is referring to the taxation practices which have been made by a

person on their own such as analysis over the own tax consequences as well as remedies

associated with the business (Lacey, McMunn and Webb, 2017). Moreover, there will be less

influences of any legal tax practitioner who would make efforts and analysis over the income

generated by the organisation.

Sole trader: Here the business is governed by a single person which is liable for collecting

all the information and making appropriate cost analysis based on various operations in the

organisation. Therefore, in respect with this, there are various tax consequence which allows the

professionals in making qualitative efforts. Here the owner will analyse the income generated by

his business throughout year on which they measure taxable income (Theodore, Theodore and

Syrrakos, 2017). The identification of such taxable income will be based on analysing the

remedies and allowansce3s which have been awarded by government will be adjusted by their

own.

Partnership: In partnership firms there will be influences of more than 1 person. Thus, in

rems of decsidi9mn g the tax remedies and payments which are to be made by them on their

generated income which requires them to make planning and decision based on such issues (von

Ehrlich and Radulescu, 2017). Moreover, here the company is itself makes payment to taxes on

the basis of analysing the charges, taxable slab as well as deductions.

M2 Implicating models and interpretation of outcomes.

Calculating taxation liabilities

In relation with analysing the tax consequences as well as various liabilities’, remedies

which are being associated with the unincorporated organisation will be measured in

identification of tax liabilities.

TASK 3

P3 Identifying tax liabilities for incorporated industry

Incorporated organisation: In respect with analysing the legal structure of the

incorporated business unit which has their own legal identity in the market. These are denoted

similar as a person who is being operating the trade practices among the society. therefore, in

respect with the framework of these organisations where group is not being liable personally for

the group actions (Onaran, Nikolaidi and Obst, 2017). Therefore, there will be requirement of

6

intention of the group in respect with making trade practices as well as raising the large sum of

money. On the other side, there will be issues and consequences relevant with the legally binding

contracts with approach toward generating large sum of profits such as Ford Motor Corp.

Characteristics:

There are various key aspects which will be helpful in terms of determining the features

and characteristics of these organisations stated in the market. Therefore, there are several

elements which are to be analysed and recognised such as:

Liability and risks: There will be benefits to the group of people operating a business.

Thus, if there are any consequences incurred the individual liabilities have been reduced

by them. Moreover, there will be reduction in the risks which are associated with the

debts of the business (McCluskey and Franzsen, 2017). If Ford faces any issues and

problems which is not being personally bared by any individual while the entire group

will look to it.

Ownership: In relation with ascertaining the information relevant with the ownership of

the incorporated groups where they can own a property as well as can enter into

contractual agreements with others. Therefore, they have rights to make contracts and can

make capital expenditures.

Cost: There have been incurrence of costs which will be required for making start up in

the business (Hirsbrunner and Lauterjung, 2017). Therefore, there will be fees which has

to be payable by the organisation in terms of making registration where it depends on the

variation in its structure.

Regulations: there can be various legislations and regulation which will affect the

performance of the organisation. Therefore, here one or two legal bodies which will

create administrative burden on the business. However, in respect with Ford Motor Corp.

they will be influences by variations in legal structure from UK, US and Hungary.

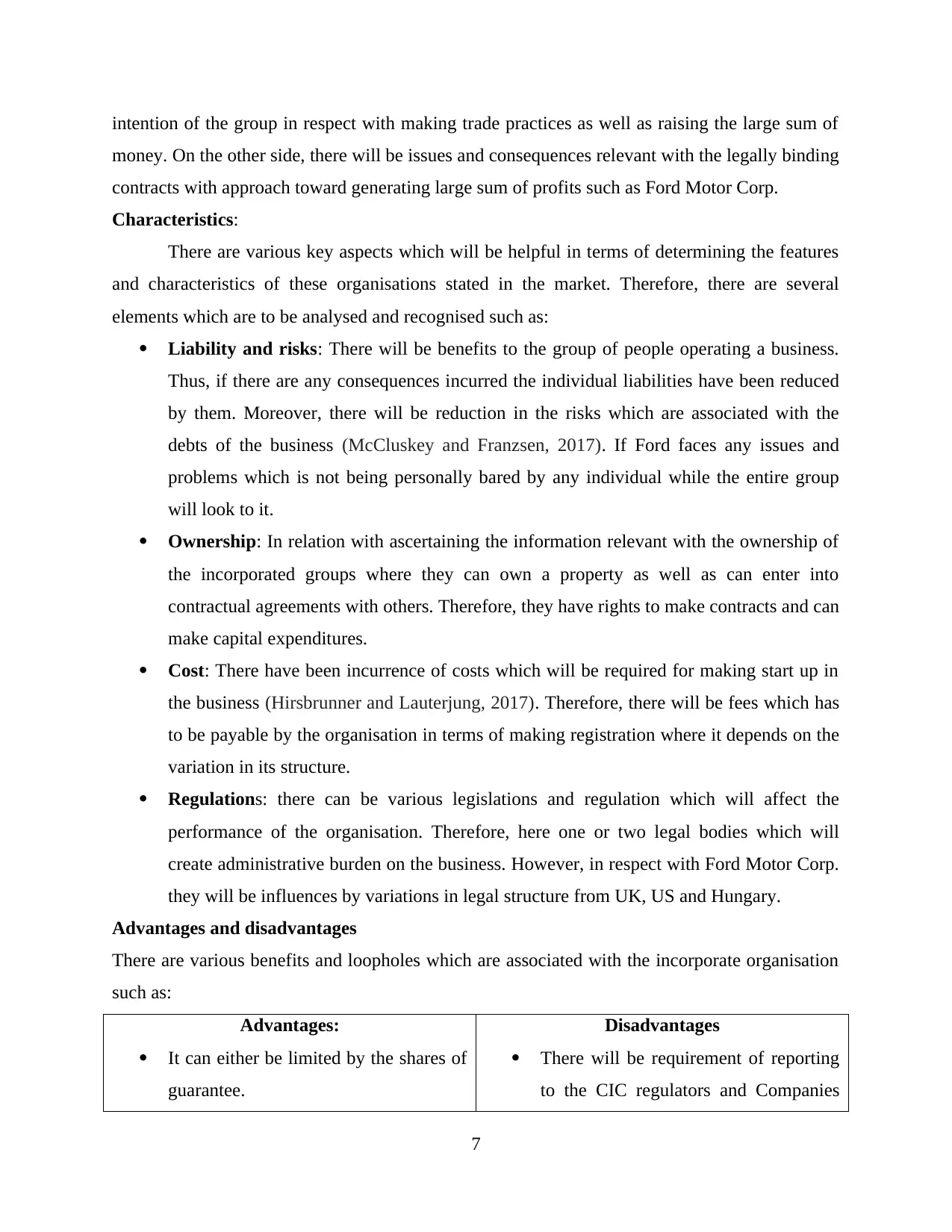

Advantages and disadvantages

There are various benefits and loopholes which are associated with the incorporate organisation

such as:

Advantages:

It can either be limited by the shares of

guarantee.

Disadvantages

There will be requirement of reporting

to the CIC regulators and Companies

7

money. On the other side, there will be issues and consequences relevant with the legally binding

contracts with approach toward generating large sum of profits such as Ford Motor Corp.

Characteristics:

There are various key aspects which will be helpful in terms of determining the features

and characteristics of these organisations stated in the market. Therefore, there are several

elements which are to be analysed and recognised such as:

Liability and risks: There will be benefits to the group of people operating a business.

Thus, if there are any consequences incurred the individual liabilities have been reduced

by them. Moreover, there will be reduction in the risks which are associated with the

debts of the business (McCluskey and Franzsen, 2017). If Ford faces any issues and

problems which is not being personally bared by any individual while the entire group

will look to it.

Ownership: In relation with ascertaining the information relevant with the ownership of

the incorporated groups where they can own a property as well as can enter into

contractual agreements with others. Therefore, they have rights to make contracts and can

make capital expenditures.

Cost: There have been incurrence of costs which will be required for making start up in

the business (Hirsbrunner and Lauterjung, 2017). Therefore, there will be fees which has

to be payable by the organisation in terms of making registration where it depends on the

variation in its structure.

Regulations: there can be various legislations and regulation which will affect the

performance of the organisation. Therefore, here one or two legal bodies which will

create administrative burden on the business. However, in respect with Ford Motor Corp.

they will be influences by variations in legal structure from UK, US and Hungary.

Advantages and disadvantages

There are various benefits and loopholes which are associated with the incorporate organisation

such as:

Advantages:

It can either be limited by the shares of

guarantee.

Disadvantages

There will be requirement of reporting

to the CIC regulators and Companies

7

You're viewing a preview

Unlock full access by subscribing today!

It allows payment to directors.

There will be no restrictions relevant

with the aims of the business which

defines as for the public benefits

House.

There will not be any taxable

advantages

Difference between private and public limited companies:

Particulars Private Public

Meaning There will be no minimum paid up

capitals as well as there are proper

rights to transfer the shares which

are restricted.

Similarly, there will be no paid-

up capital. Moreover, the

subsidise organisation in public

company will be denoted as

public company of the

organisation.

Formation There will be minimum number of

people which are operating the

business activities are 2 while the

maximum is 200

In this aspect there are minimum

number of members are 7 while

maximum number of members

are limitless.

Taxation advantages for each organisation

Private organisation:

In relation with analysing the operations of the private organisation on they have to make

payment for the taxes on the basis of corporate tax rates.

Public Organisation:

In respect with analysing the operational aspect there are various field on they will be

awarded deductions which will be helpful to them in meeting the tax consequences.

M3 Application of relevant models and interpretation of outcomes

In relation with analysing the tax consequences as well as various liabilities’, remedies

which are being associated with the Incorporated organisation will be measured in identification

of tax liabilities.

8

There will be no restrictions relevant

with the aims of the business which

defines as for the public benefits

House.

There will not be any taxable

advantages

Difference between private and public limited companies:

Particulars Private Public

Meaning There will be no minimum paid up

capitals as well as there are proper

rights to transfer the shares which

are restricted.

Similarly, there will be no paid-

up capital. Moreover, the

subsidise organisation in public

company will be denoted as

public company of the

organisation.

Formation There will be minimum number of

people which are operating the

business activities are 2 while the

maximum is 200

In this aspect there are minimum

number of members are 7 while

maximum number of members

are limitless.

Taxation advantages for each organisation

Private organisation:

In relation with analysing the operations of the private organisation on they have to make

payment for the taxes on the basis of corporate tax rates.

Public Organisation:

In respect with analysing the operational aspect there are various field on they will be

awarded deductions which will be helpful to them in meeting the tax consequences.

M3 Application of relevant models and interpretation of outcomes

In relation with analysing the tax consequences as well as various liabilities’, remedies

which are being associated with the Incorporated organisation will be measured in identification

of tax liabilities.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P4 Determination of impacts of key legal and ethical constraints on different industry

Ethics:

Ethics are the morals, beliefs, values, knowledge and learning of people that govern

individual action. Managing ethical business function is necessary for the organization because it

helps the management in deriving wrong and right of the situation with regard to stakeholders. It

is important for the automotive firm to work under ethical constraints because it assists in

protecting interest of stakeholders (McKee, Muir and Moore, 2017). For example, fair

presentation of expenses and accounts is the ethical constraint for Ford which helps in

organization in reducing risks of tax avoidance which is ultimately contribution for economic

development. Further, ethics constraint to Ford are also related with consumer concern where it

is necessary for the organization to demonstrate fair and true advertisement because it is a long-

term investment for shoppers.

Ethics constraints across different nation

Ethics vary nation to nation because every region has own cultural, values, beliefs and

morals which governs individual action. Further, ethical constraints of every region differ

according to situation of the particular nation. Like business ethics are shaped by legislation

followed in different nations (Moore, 2018). Further, ethical constraints of Ford differ according

to responsibility and role of management in different regions which changes according to

consumers response towards services. However, it can be said that business ethics is the core

aspect of ford which support its international expansion.

Key legal and ethical constraints on various organisation such as unincorporated and

incorporated.

There will be various differences in the legal and ethical constraints of the unincorporated

and incorporated organisation. Therefore, unincorporated industries are legally not bound with

getting registration as well as meeting the legal aspects of the firm (Theodore, Theodore and

Syrrakos, 2017). While incorporated industries are legally bound for making qualitative efforts

as well as ascertainment of the ethical constraints.

9

P4 Determination of impacts of key legal and ethical constraints on different industry

Ethics:

Ethics are the morals, beliefs, values, knowledge and learning of people that govern

individual action. Managing ethical business function is necessary for the organization because it

helps the management in deriving wrong and right of the situation with regard to stakeholders. It

is important for the automotive firm to work under ethical constraints because it assists in

protecting interest of stakeholders (McKee, Muir and Moore, 2017). For example, fair

presentation of expenses and accounts is the ethical constraint for Ford which helps in

organization in reducing risks of tax avoidance which is ultimately contribution for economic

development. Further, ethics constraint to Ford are also related with consumer concern where it

is necessary for the organization to demonstrate fair and true advertisement because it is a long-

term investment for shoppers.

Ethics constraints across different nation

Ethics vary nation to nation because every region has own cultural, values, beliefs and

morals which governs individual action. Further, ethical constraints of every region differ

according to situation of the particular nation. Like business ethics are shaped by legislation

followed in different nations (Moore, 2018). Further, ethical constraints of Ford differ according

to responsibility and role of management in different regions which changes according to

consumers response towards services. However, it can be said that business ethics is the core

aspect of ford which support its international expansion.

Key legal and ethical constraints on various organisation such as unincorporated and

incorporated.

There will be various differences in the legal and ethical constraints of the unincorporated

and incorporated organisation. Therefore, unincorporated industries are legally not bound with

getting registration as well as meeting the legal aspects of the firm (Theodore, Theodore and

Syrrakos, 2017). While incorporated industries are legally bound for making qualitative efforts

as well as ascertainment of the ethical constraints.

9

M4 Critical evaluation of impacts key legal and ethical constraints on application to different

organisation.

In relation with analysing the key legal aspect which are associated with the taxation

purposes that determines the purpose and role of business in collecting taxes. Therefore, there are

several indirect taxes which are to be considered by the professionals in industry such as value

added tax, national insurance, PAYE as Income tax. Therefore, influences of various legislations

which will be adequate in meeting the taxable payment of organisation at the right time.

CONCLUSION

On the basis of above report, it can be said that taxable legalisation over the earnings and

revenue generated by the organisation as well as individual are required to be taxable. Thus,

there had been determination over the various abatable liability of unincorporated as well as

incorporated organisation which will be beneficial in making appropriate taxable payments.

10

organisation.

In relation with analysing the key legal aspect which are associated with the taxation

purposes that determines the purpose and role of business in collecting taxes. Therefore, there are

several indirect taxes which are to be considered by the professionals in industry such as value

added tax, national insurance, PAYE as Income tax. Therefore, influences of various legislations

which will be adequate in meeting the taxable payment of organisation at the right time.

CONCLUSION

On the basis of above report, it can be said that taxable legalisation over the earnings and

revenue generated by the organisation as well as individual are required to be taxable. Thus,

there had been determination over the various abatable liability of unincorporated as well as

incorporated organisation which will be beneficial in making appropriate taxable payments.

10

You're viewing a preview

Unlock full access by subscribing today!

REFERENCES

Books and Journals

Chepulis, L. and et.al., 2018. The nutritional content of supermarket beverages: a cross-sectional

analysis of New Zealand, Australia, Canada and the UK. Public health nutrition. pp.1-10.

Cromwell, J., 2017. New Texts from Early Islamic Egypt: A Bilingual Taxation

Archive. Zeitschrift FÜr Papyrologie und Epigraphik. 201. pp.232-252.

Haag, M., 2017. The implications of ‘Brexit’under German tax law: expected changes for UK

businesses, corporations, and trusts with Germany-based owners and beneficiaries. Trusts

& Trustees.23(6). pp.664-668.

Hirsbrunner, S. and Lauterjung, A., 2017. Without EU State Aid Control No EU-UK Free Trade

Deal. Eur. St. Aid LQ, p.288.

Lacey, R., McMunn, A. and Webb, E., 2017. OP91 Informal caregiving and markers of adiposity

in the uk household longitudinal study.

Liu, M. L., 2018. Where does multinational investment go with territorial taxation? Evidence

from the UK. International Monetary Fund.

McCluskey, W. J. and Franzsen, R. C., 2017. Land value taxation: An applied analysis.

Routledge.

McKee, K., Muir, J. and Moore, T., 2017. Housing policy in the UK: The importance of spatial

nuance. Housing Studies.32(1). pp.60-72.

Moore, M., 2018. Taxation and development (No. 14008).

Onaran, Ö., Nikolaidi, M. and Obst, T., 2017. The role of public spending and incomes policies

for investment and equality-led development in the UK.

Rowland, N., 2017. Farewell message. Taxation in Australia.52(4). p.175.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Theodore, J., Theodore, J. and Syrrakos, D., 2017. The EU, Taxation and the Multinationals.

In The European Union and the Eurozone under Stress (pp. 191-202). Palgrave

Macmillan, Cham.

von Ehrlich, M. and Radulescu, D., 2017. The taxation of bonuses and its effect on executive

compensation and risk‐taking: Evidence from the UK experience. Journal of Economics

& Management Strategy. 26(3). pp.712-731.

11

Books and Journals

Chepulis, L. and et.al., 2018. The nutritional content of supermarket beverages: a cross-sectional

analysis of New Zealand, Australia, Canada and the UK. Public health nutrition. pp.1-10.

Cromwell, J., 2017. New Texts from Early Islamic Egypt: A Bilingual Taxation

Archive. Zeitschrift FÜr Papyrologie und Epigraphik. 201. pp.232-252.

Haag, M., 2017. The implications of ‘Brexit’under German tax law: expected changes for UK

businesses, corporations, and trusts with Germany-based owners and beneficiaries. Trusts

& Trustees.23(6). pp.664-668.

Hirsbrunner, S. and Lauterjung, A., 2017. Without EU State Aid Control No EU-UK Free Trade

Deal. Eur. St. Aid LQ, p.288.

Lacey, R., McMunn, A. and Webb, E., 2017. OP91 Informal caregiving and markers of adiposity

in the uk household longitudinal study.

Liu, M. L., 2018. Where does multinational investment go with territorial taxation? Evidence

from the UK. International Monetary Fund.

McCluskey, W. J. and Franzsen, R. C., 2017. Land value taxation: An applied analysis.

Routledge.

McKee, K., Muir, J. and Moore, T., 2017. Housing policy in the UK: The importance of spatial

nuance. Housing Studies.32(1). pp.60-72.

Moore, M., 2018. Taxation and development (No. 14008).

Onaran, Ö., Nikolaidi, M. and Obst, T., 2017. The role of public spending and incomes policies

for investment and equality-led development in the UK.

Rowland, N., 2017. Farewell message. Taxation in Australia.52(4). p.175.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Theodore, J., Theodore, J. and Syrrakos, D., 2017. The EU, Taxation and the Multinationals.

In The European Union and the Eurozone under Stress (pp. 191-202). Palgrave

Macmillan, Cham.

von Ehrlich, M. and Radulescu, D., 2017. The taxation of bonuses and its effect on executive

compensation and risk‐taking: Evidence from the UK experience. Journal of Economics

& Management Strategy. 26(3). pp.712-731.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Online

A survey of the UK tax system. 2016. [Online]. Available through :<

https://www.ifs.org.uk/bns/bn09.pdf >.

Corporation tax: UK vs USA. 2018. [Online]. Available through

:<https://fullfact.org/economy/corporation-tax-uk-vs-usa/>.

Public Economics: Indirect Taxation. 2016. [Online]. Available through :<

https://www.ifs.org.uk/uploads/Presentations/Public%20Economics%20Lectures/Public

%20Economics%20Indirect%20Taxation.pdf >.

12

A survey of the UK tax system. 2016. [Online]. Available through :<

https://www.ifs.org.uk/bns/bn09.pdf >.

Corporation tax: UK vs USA. 2018. [Online]. Available through

:<https://fullfact.org/economy/corporation-tax-uk-vs-usa/>.

Public Economics: Indirect Taxation. 2016. [Online]. Available through :<

https://www.ifs.org.uk/uploads/Presentations/Public%20Economics%20Lectures/Public

%20Economics%20Indirect%20Taxation.pdf >.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.