Taxation Law 200187 Assignment: Spring 2019 Take-Home Exam Solution

VerifiedAdded on 2022/10/16

|8

|1575

|125

Homework Assignment

AI Summary

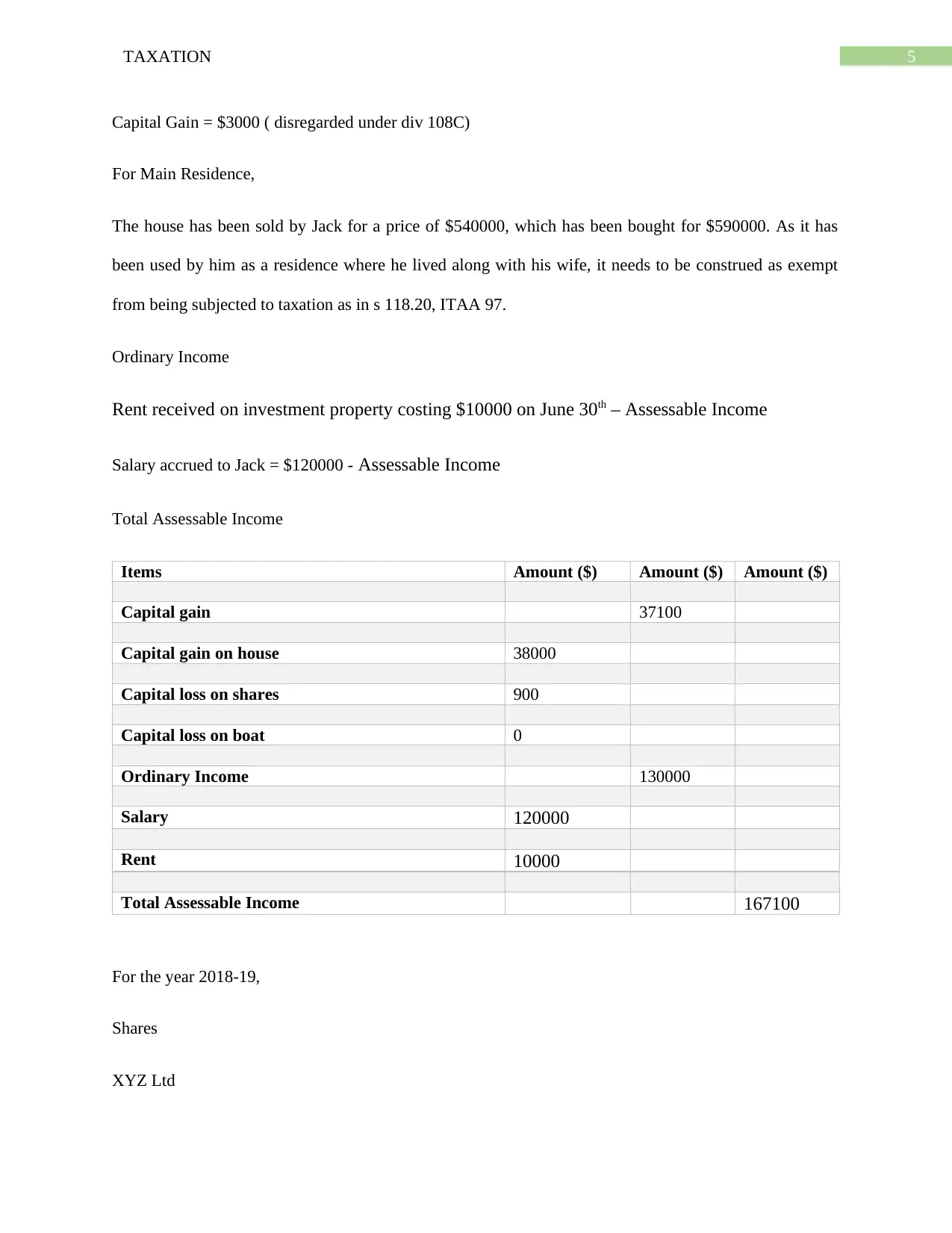

This assignment solution addresses two key taxation law issues. The first issue concerns whether payments made for the sale of trademarks should be included as taxable income, analyzing the application of ordinary income concepts, capital gains, and relevant case law such as Scott & Ors v FC of T and Kwikspan Purlin System Pty Ltd v FC of T. The second issue examines the taxation implications of transactions made by an individual, Jack, including capital gains tax (CGT) on the sale of shares, a house, and a boat, as well as ordinary income from rent and salary. It applies the Income Tax Assessment Act 1997 (Cth), including sections on capital assets, cost base, capital proceeds, and CGT discounts, to calculate assessable income for the years 2017-18 and 2018-19. The analysis considers relevant provisions and precedents like Eisner v Macomber and Pritchard v Arundale to determine the tax liabilities and implications for both scenarios, ultimately providing detailed calculations of capital gains and total assessable income.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.