TAX 305: Taxation Law Assignment 1 - Case Study Solutions, CDU, 2019

VerifiedAdded on 2022/10/19

|11

|2311

|87

Case Study

AI Summary

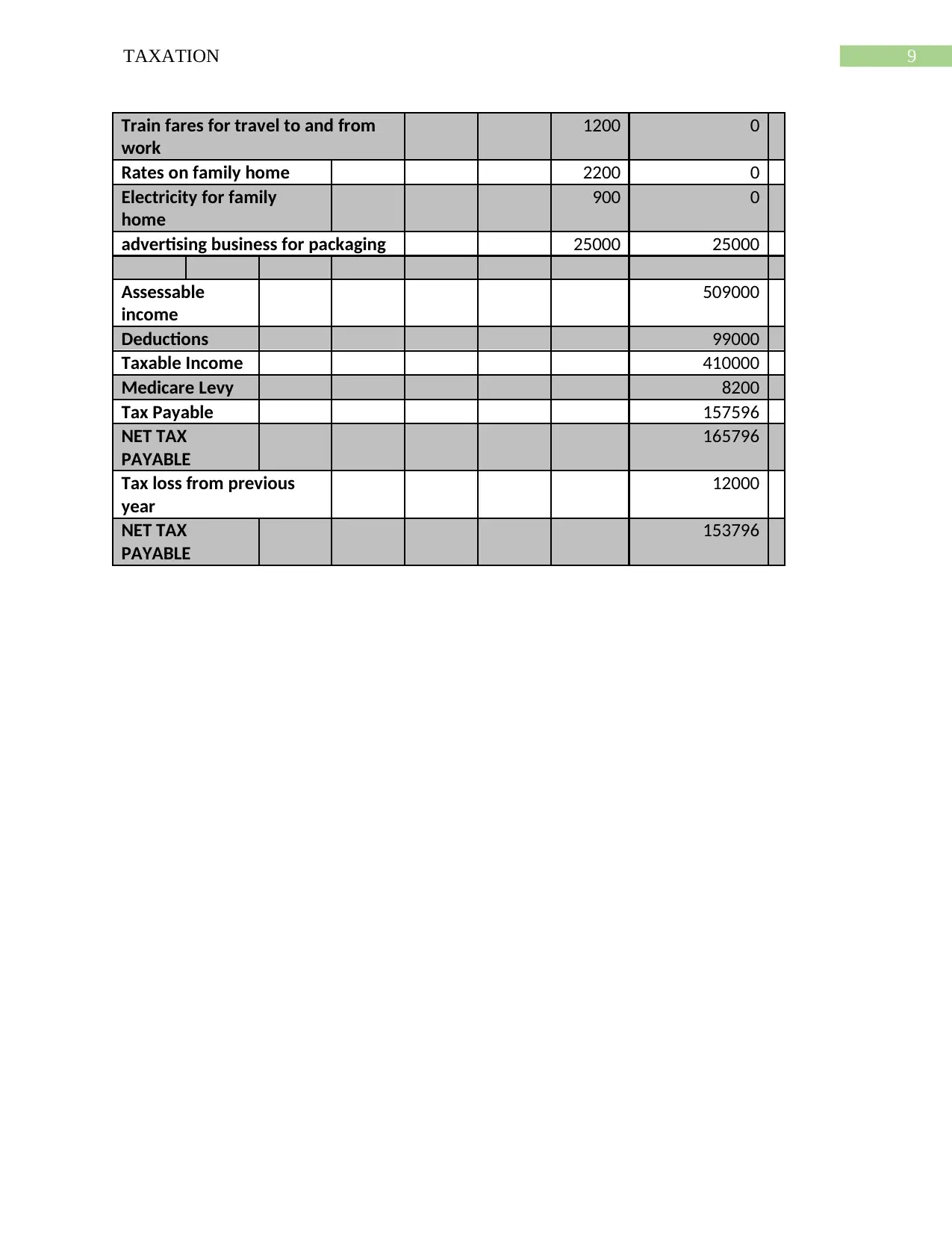

This document provides a comprehensive solution to a taxation law assignment, addressing three distinct case studies. The first case study examines the residency status of an individual under Australian tax law, analyzing the application of the 183-day test and the implications of having a permanent place of abode outside Australia. The second case study delves into the determination of whether an individual is carrying on a business for taxation purposes, considering various indicators outlined in Taxation Ruling 97/11 and relevant case law. The third case study focuses on identifying different types of income (ordinary and statutory), deductible expenses, and the application of relevant tax rates. The solution analyzes each scenario, providing detailed rules, applications, and conclusions based on relevant legislation (ITAA 36, ITAA 97) and case law, such as Harding v Commissioner of Taxation and Ferguson v Federal Commissioner of Taxation. The assignment also considers the tax treatment of various income sources and expenses, providing a complete overview of the taxation principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.