Taxation Assignment: Analyzing Tax Consequences for Our Earth and Sam

VerifiedAdded on 2022/12/26

|14

|3903

|45

Homework Assignment

AI Summary

This assignment analyzes the tax implications for Our Earth Pty Ltd, a company that manufactures biodegradable coffee cups, and Sam, an individual who owns farmland. The first part of the assignment addresses the tax consequences of compensation received by Our Earth Pty Ltd due to design patent infringement, lost revenue, interest on damages, and reimbursement of legal fees. The analysis classifies these amounts as either capital gains or ordinary income based on relevant tax laws and case precedents, including the Income Tax Assessment Act 1997. The second part focuses on Sam's farmland, evaluating the tax implications of selling the land after subdivision and the associated costs. The assignment considers the initial purchase, operational activities, and the impact of rezoning the land for subdivision on the ultimate tax liability. The document provides a detailed breakdown of assessable income and the application of tax principles to specific scenarios.

Running head: TAXATION

Taxation

Name of the Student

Name of the University

Author Note

Taxation

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Answer 1....................................................................................................................................2

Issue........................................................................................................................................2

Rule........................................................................................................................................2

Application.............................................................................................................................4

Conclusion..............................................................................................................................7

Answer 2....................................................................................................................................7

Issue........................................................................................................................................7

Rule........................................................................................................................................8

Application.............................................................................................................................9

Conclusion............................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Answer 1....................................................................................................................................2

Issue........................................................................................................................................2

Rule........................................................................................................................................2

Application.............................................................................................................................4

Conclusion..............................................................................................................................7

Answer 2....................................................................................................................................7

Issue........................................................................................................................................7

Rule........................................................................................................................................8

Application.............................................................................................................................9

Conclusion............................................................................................................................11

Reference..................................................................................................................................12

2TAXATION

Answer 1

Issue

In the given instance, the issue is to evaluate the tax consequences pertaining to the below

mentioned transactions as accrued to the Our Earth Pty Ltd.

Firstly, the issue is the tax implications that Our Earth Pty Ltd has incurred owing to the

compensation of $300,000 received against the damages for design patent infringement.

Secondly, the issue is the tax implications for the compensation amounting to $200,000

received for the loss of revenue that has been caused to Our Earth Pty Ltd for the 12-month

period that Coffee Bean Pty Ltd had been using the other product.

Thirdly, the issue is the tax implication with respect to the interest amounting to $15,000

that has been received on the damages payout.

Fourthly, the issue is the tax implications for the amount of $40,000 received as a

reimbursement of legal fees incurred by Our Earth Pty Ltd.

Rule

The compensations that are received against any loss of items of income are to be treated

in accordance with the doctrine of replacement. Under this doctrine, the compensation that

has been received against any item of income or any prospect that might ensure income needs

to be treated in a similar manner as that of the income that it has been replacing for the

purpose of taxation. This is because the item against which the compensation has been

received, would be have the probability of accruing an income and has the prospect of being

assessed under taxation. The loss of the same has made that probability to disappear and no

tax can be charged with respect to the same. Hence, applying the doctrine of replacement, it

can be stated that the compensation would be construed to have replaced the item against

Answer 1

Issue

In the given instance, the issue is to evaluate the tax consequences pertaining to the below

mentioned transactions as accrued to the Our Earth Pty Ltd.

Firstly, the issue is the tax implications that Our Earth Pty Ltd has incurred owing to the

compensation of $300,000 received against the damages for design patent infringement.

Secondly, the issue is the tax implications for the compensation amounting to $200,000

received for the loss of revenue that has been caused to Our Earth Pty Ltd for the 12-month

period that Coffee Bean Pty Ltd had been using the other product.

Thirdly, the issue is the tax implication with respect to the interest amounting to $15,000

that has been received on the damages payout.

Fourthly, the issue is the tax implications for the amount of $40,000 received as a

reimbursement of legal fees incurred by Our Earth Pty Ltd.

Rule

The compensations that are received against any loss of items of income are to be treated

in accordance with the doctrine of replacement. Under this doctrine, the compensation that

has been received against any item of income or any prospect that might ensure income needs

to be treated in a similar manner as that of the income that it has been replacing for the

purpose of taxation. This is because the item against which the compensation has been

received, would be have the probability of accruing an income and has the prospect of being

assessed under taxation. The loss of the same has made that probability to disappear and no

tax can be charged with respect to the same. Hence, applying the doctrine of replacement, it

can be stated that the compensation would be construed to have replaced the item against

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

which it has been replaced. Similarly, the tax implications that was supposed to accrue to the

items as a replacement of which the compensation has been incurred would also accrue in a

similar manner to the compensation as well. This comes in line with the case of Haritos v

Commissioner of Taxation [2015] FCAFC 92. In this case, it has been contended by the court

that the tax implications that was supposed to be accrued to the to the items of income would

also accrue to the compensation that has been received as a replacement of the same. In this

case, the compensation in question would be treated in the same as that of the item of income

it has been replacing.

The main object of the compensation is to neutralize the losses that has been caused owing

to the destruction of the income or a prospect of income. Hence, it can be illustrated in that

context, the items of income that has been rendered to be an ordinary income under the

section 6.5 of the Income Tax Assessment Act 1997 (Cth), would also be render any

compensation that has been received in place of that as an ordinary income under the same as

well. In this context, it can be stated that the compensation that has been extended towards

the loss of an ordinary income has the effect of appropriating the loss and owing to its effect

of the appropriation of the ordinary income, it also needs to be construed to be an ordinary

income. In the same way, it can be stated that the income, which has the implication for the

purpose of taxation pertaining to capital gain would render the compensation received against

the loss of the same to be directed towards the capital gain. This can further be supported by

the case of August v Commissioner of Taxation [2013] FCAFC 85. In this case, it has been

contended by the court that factory, which is permanent would be construed to be a capital

asset under section 104.5 of the Income Tax Assessment Act 1997 (Cth). Losses that has

been accrued by virtue of the destruction in the same would also be treated as a loss of capital

asset. This would render any loss pertaining to the same to be loss of capital asset. Any

compensation that has been accrued for the loss of the such capital asset would be treated as a

which it has been replaced. Similarly, the tax implications that was supposed to accrue to the

items as a replacement of which the compensation has been incurred would also accrue in a

similar manner to the compensation as well. This comes in line with the case of Haritos v

Commissioner of Taxation [2015] FCAFC 92. In this case, it has been contended by the court

that the tax implications that was supposed to be accrued to the to the items of income would

also accrue to the compensation that has been received as a replacement of the same. In this

case, the compensation in question would be treated in the same as that of the item of income

it has been replacing.

The main object of the compensation is to neutralize the losses that has been caused owing

to the destruction of the income or a prospect of income. Hence, it can be illustrated in that

context, the items of income that has been rendered to be an ordinary income under the

section 6.5 of the Income Tax Assessment Act 1997 (Cth), would also be render any

compensation that has been received in place of that as an ordinary income under the same as

well. In this context, it can be stated that the compensation that has been extended towards

the loss of an ordinary income has the effect of appropriating the loss and owing to its effect

of the appropriation of the ordinary income, it also needs to be construed to be an ordinary

income. In the same way, it can be stated that the income, which has the implication for the

purpose of taxation pertaining to capital gain would render the compensation received against

the loss of the same to be directed towards the capital gain. This can further be supported by

the case of August v Commissioner of Taxation [2013] FCAFC 85. In this case, it has been

contended by the court that factory, which is permanent would be construed to be a capital

asset under section 104.5 of the Income Tax Assessment Act 1997 (Cth). Losses that has

been accrued by virtue of the destruction in the same would also be treated as a loss of capital

asset. This would render any loss pertaining to the same to be loss of capital asset. Any

compensation that has been accrued for the loss of the such capital asset would be treated as a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

capital gain for the purpose of taxation. This is because the capital asset has the prospect of

earning a capital gain if the same has been sold. In this case, the compensation can be

construed to have the same implications as that of the proceeds that has been received from

the sale of the capital asset (Woellner et al, 2016).

It has been contended in the case of News Australia Holdings Pty Ltd v Commissioner of

Taxation [2017] FCA 645, that any exclusive right that a person paying the tax owns with

respect to a particular product would be treated as an capital asset and the same has the

prospect of earning capital gain when sold. This requires any compensation that has been

received for the loss of such a capital asset would also be treated as a capital gain as the same

is construed to be a proceed that has been received from the sale of the same. Any

infringement of such right would have two implications, firstly the capital loss and secondly

the loss of profit that has been expected to incur from the right. Any compensation that will

follow such a loss of profit would also be considered to be an ordinary income. This can

further be extended with the case of Federal Commissioner of Taxation v Northumberland

Development Co Pty Ltd 95 ATC 4483. Any profit that has been accrued from a right would

be treated as ordinary income and so the compensation that has been received from the loss of

the same.

It can be stated that any interest that has been accrued to any of the damages when paid

will have the same tax implication of an ordinary income as given under section 6.5 of the

Income Tax Assessment Act 1997 (Cth). This can further be elucidated with the case of Mills

v Commissioner of Taxation [2012] HCA 51. Again, it can be stated that legal expenses and

costs pertaining to the legal proceedings are treated as general deductions under section 8.1 of

the the Income Tax Assessment Act 1997 (Cth), Hence, any reimbursement of the same

would also be treated as an ordinary income.

capital gain for the purpose of taxation. This is because the capital asset has the prospect of

earning a capital gain if the same has been sold. In this case, the compensation can be

construed to have the same implications as that of the proceeds that has been received from

the sale of the capital asset (Woellner et al, 2016).

It has been contended in the case of News Australia Holdings Pty Ltd v Commissioner of

Taxation [2017] FCA 645, that any exclusive right that a person paying the tax owns with

respect to a particular product would be treated as an capital asset and the same has the

prospect of earning capital gain when sold. This requires any compensation that has been

received for the loss of such a capital asset would also be treated as a capital gain as the same

is construed to be a proceed that has been received from the sale of the same. Any

infringement of such right would have two implications, firstly the capital loss and secondly

the loss of profit that has been expected to incur from the right. Any compensation that will

follow such a loss of profit would also be considered to be an ordinary income. This can

further be extended with the case of Federal Commissioner of Taxation v Northumberland

Development Co Pty Ltd 95 ATC 4483. Any profit that has been accrued from a right would

be treated as ordinary income and so the compensation that has been received from the loss of

the same.

It can be stated that any interest that has been accrued to any of the damages when paid

will have the same tax implication of an ordinary income as given under section 6.5 of the

Income Tax Assessment Act 1997 (Cth). This can further be elucidated with the case of Mills

v Commissioner of Taxation [2012] HCA 51. Again, it can be stated that legal expenses and

costs pertaining to the legal proceedings are treated as general deductions under section 8.1 of

the the Income Tax Assessment Act 1997 (Cth), Hence, any reimbursement of the same

would also be treated as an ordinary income.

5TAXATION

Application

In the instant situation, Our Earth Pty Ltd was the sole supplier as well as manufacturers of

specially designed biodegradable coffee cups, which are made from sustainable materials.

They had the sole right to deal in that cups and no other business operating in Australia has

the supply rights of the same. However, afterwards it came to the notice of Our Earth Pty Ltd

that another business owner namely Coffee Bean Pty Ltd has been supplying similar cups.

The cups that they have been selling were at a cheaper price than that of the cups sold by the

Our Earth Pty Ltd. Moreover, Coffee Bean Pty Ltd has failed to mention to their customers

that the cups they have been supplying were not original Our Earth Pty Ltd cups but the same

has been supplied from an overseas company. This has caused a considerable amount of loss

to the Our Earth Pty Ltd that has compelled them to opt for a legal proceeding. This

proceeding has earned Our Earth Pty Ltd certain compensation and the tax implications of the

same can be summed up as follows:

1. Owing to this proceeding Our Earth Pty Ltd has received $300,000 damages for

design patent infringement, This needs to be construed as a capital gain as it has

been contended in the case of News Australia Holdings Pty Ltd v Commissioner of

Taxation [2017] FCA 645, that any exclusive right that a person paying the tax

owns with respect to a particular product would be treated as an capital asset and

the same has the prospect of earning capital gain when sold. This requires any

compensation that has been received for the loss of such a capital asset would also

be treated as a capital gain as the same is construed to be a proceed that has been

received from the sale of the same.

2. Owing to this proceeding Our Earth Pty Ltd has received $200,000 for expected

lost revenue over the 12 month period that Coffee Bean Pty Ltd had been using the

other product. This can be construed as an ordinary income as any compensation

Application

In the instant situation, Our Earth Pty Ltd was the sole supplier as well as manufacturers of

specially designed biodegradable coffee cups, which are made from sustainable materials.

They had the sole right to deal in that cups and no other business operating in Australia has

the supply rights of the same. However, afterwards it came to the notice of Our Earth Pty Ltd

that another business owner namely Coffee Bean Pty Ltd has been supplying similar cups.

The cups that they have been selling were at a cheaper price than that of the cups sold by the

Our Earth Pty Ltd. Moreover, Coffee Bean Pty Ltd has failed to mention to their customers

that the cups they have been supplying were not original Our Earth Pty Ltd cups but the same

has been supplied from an overseas company. This has caused a considerable amount of loss

to the Our Earth Pty Ltd that has compelled them to opt for a legal proceeding. This

proceeding has earned Our Earth Pty Ltd certain compensation and the tax implications of the

same can be summed up as follows:

1. Owing to this proceeding Our Earth Pty Ltd has received $300,000 damages for

design patent infringement, This needs to be construed as a capital gain as it has

been contended in the case of News Australia Holdings Pty Ltd v Commissioner of

Taxation [2017] FCA 645, that any exclusive right that a person paying the tax

owns with respect to a particular product would be treated as an capital asset and

the same has the prospect of earning capital gain when sold. This requires any

compensation that has been received for the loss of such a capital asset would also

be treated as a capital gain as the same is construed to be a proceed that has been

received from the sale of the same.

2. Owing to this proceeding Our Earth Pty Ltd has received $200,000 for expected

lost revenue over the 12 month period that Coffee Bean Pty Ltd had been using the

other product. This can be construed as an ordinary income as any compensation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

that will follow such a loss of profit would also be considered to be an ordinary

income. This can further be extended with the case of Federal Commissioner of

Taxation v Northumberland Development Co Pty Ltd 95 ATC 4483. Any profit

that has been accrued from a right would be treated as ordinary income and so the

compensation that has been received from the loss of the same.

3. Owing to this proceeding Our Earth Pty Ltd has received $15,000 interest on the

damages payout. This would be construed to be an ordinary income as it can be

stated that any interest that has been accrued to any of the damages when paid will

have the same tax implication of an ordinary income as given under section 6.5 of

the Income Tax Assessment Act 1997 (Cth). This can further be elucidated with

the case of Mills v Commissioner of Taxation [2012] HCA 51.

4. Owing to this proceeding Our Earth Pty Ltd has received $40,000 reimbursement

of legal fees incurred by Our Earth Pty Ltd. This can be construed to be an

ordinary income as it can be stated that legal expenses and costs pertaining to the

legal proceedings are treated as general deductions under section 8.1 of the the

Income Tax Assessment Act 1997 (Cth), Hence, any reimbursement of the same

would also be treated as an ordinary income.

In the Books of Our Earth Pty Ltd

Computation of Assessable Income

For the Period ended 30 June 2019

Particulars Amount Amount

Damages for Design Patent Infringement (A) $ 300,000

Expected Loss Receipts (B) $ 200, 000

Interest Receipts (C) $ 15, 000

that will follow such a loss of profit would also be considered to be an ordinary

income. This can further be extended with the case of Federal Commissioner of

Taxation v Northumberland Development Co Pty Ltd 95 ATC 4483. Any profit

that has been accrued from a right would be treated as ordinary income and so the

compensation that has been received from the loss of the same.

3. Owing to this proceeding Our Earth Pty Ltd has received $15,000 interest on the

damages payout. This would be construed to be an ordinary income as it can be

stated that any interest that has been accrued to any of the damages when paid will

have the same tax implication of an ordinary income as given under section 6.5 of

the Income Tax Assessment Act 1997 (Cth). This can further be elucidated with

the case of Mills v Commissioner of Taxation [2012] HCA 51.

4. Owing to this proceeding Our Earth Pty Ltd has received $40,000 reimbursement

of legal fees incurred by Our Earth Pty Ltd. This can be construed to be an

ordinary income as it can be stated that legal expenses and costs pertaining to the

legal proceedings are treated as general deductions under section 8.1 of the the

Income Tax Assessment Act 1997 (Cth), Hence, any reimbursement of the same

would also be treated as an ordinary income.

In the Books of Our Earth Pty Ltd

Computation of Assessable Income

For the Period ended 30 June 2019

Particulars Amount Amount

Damages for Design Patent Infringement (A) $ 300,000

Expected Loss Receipts (B) $ 200, 000

Interest Receipts (C) $ 15, 000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

Reimbursement of Legal Expenses (D) $ 40, 000

Total Assessable Income (A) + (B) + (C) +

(D)

$ 555, 000

Conclusion

Hence, it can be concluded that tax implication pertaining to the Our Earth Pty Ltd owing

to the mentioned transactions can be summarised as follows:

1. $300,000 damages for design patent infringement will be construed as a capital

gain.

2. $200,000 for expected lost revenue over the 12 month period that Coffee Bean Pty

Ltd had been using the other product will be construed as an ordinary income.

3. $15,000 interest on the damages payout would be construed to be an ordinary

income.

4. $40,000 reimbursement of legal fees would be construed to be an ordinary income.

Answer 2

Issue

Sam has bought 80 acres of farmland in 1984 for $270,000 and has been running a beef

cattle breeding operation. Again, an extra 20 acres of the adjoining land has also been

purchased by the Sam. However, owing to drought and his advancing age, Sam has been been

considering the selling of the land. It has been found by Sam, while attempting to sell his land

that it can only earn him $440,000. This has not been satisfying for Sam as he has put a

considerable amount of effort and has incurred a considerable amount of cost for the purpose

of modifying the land. He has availed an advice from a local real estate advisor who has

advised to make the sale of the land after subdivision. Sam has acted in accordance with the

Reimbursement of Legal Expenses (D) $ 40, 000

Total Assessable Income (A) + (B) + (C) +

(D)

$ 555, 000

Conclusion

Hence, it can be concluded that tax implication pertaining to the Our Earth Pty Ltd owing

to the mentioned transactions can be summarised as follows:

1. $300,000 damages for design patent infringement will be construed as a capital

gain.

2. $200,000 for expected lost revenue over the 12 month period that Coffee Bean Pty

Ltd had been using the other product will be construed as an ordinary income.

3. $15,000 interest on the damages payout would be construed to be an ordinary

income.

4. $40,000 reimbursement of legal fees would be construed to be an ordinary income.

Answer 2

Issue

Sam has bought 80 acres of farmland in 1984 for $270,000 and has been running a beef

cattle breeding operation. Again, an extra 20 acres of the adjoining land has also been

purchased by the Sam. However, owing to drought and his advancing age, Sam has been been

considering the selling of the land. It has been found by Sam, while attempting to sell his land

that it can only earn him $440,000. This has not been satisfying for Sam as he has put a

considerable amount of effort and has incurred a considerable amount of cost for the purpose

of modifying the land. He has availed an advice from a local real estate advisor who has

advised to make the sale of the land after subdivision. Sam has acted in accordance with the

8TAXATION

advice and re-zoned his land for sub-division. This has made Sam spent $450,000 as sub-

division costs such as surveyor fees, electricity and water connections and main road access,

a local construction company agreed to buy the entire sub-division for $1,100,000. All these

has earned Sam a contract for sale of the land at $1,100,000. He has further incurred an

expense of $45,000 towards legal fees and agent’s commission. The issue arising from the

given situation is whether the proceeds of the sale would incur tax implications as a capital

gain or an ordinary income accruing from business.

Rule

Income, which would be incurred from the use or exploitation of property would be

treated as ordinary income as has been provided under the Income Tax Assessment Act 1997

(Cth) under section 6.5. However, the property would be construed as an asset of capital

nature. this needs to be illustrated with the case of Riches v Westminster Bank Ltd [1947] AC

390. It has also been held by the court that in the case of Steele v Deputy Commissioner of

Taxation [1999] HCA 7 that the utilisation of the property would include business, interest,

rents and any other profit earning activity pertaining to the land.

Again, it can be stated that the amount which would be earned as a proceed incurred from

the sale of the property would be rendered as capital gain as evident from the section 100.35

and the tax consequence of the same would be treated accordingly. The reason behind this

treatment is because the property owing to which the proceeds has been incurred is construed

to be a capital asset under section 100.25 and any proceeds pertaining to the same would be

construed to be a capital asset. It has been held in the case of Visy Industries USA Pty Ltd v

Commissioner of Taxation [2011] FCA 1065 that a property has the status of a capital asset

for the purpose of taxation and any monetary benefit that can be availed by the permanent

disposing off of the same would also be treated to be a capital gain (Barkoczy, 2016).

advice and re-zoned his land for sub-division. This has made Sam spent $450,000 as sub-

division costs such as surveyor fees, electricity and water connections and main road access,

a local construction company agreed to buy the entire sub-division for $1,100,000. All these

has earned Sam a contract for sale of the land at $1,100,000. He has further incurred an

expense of $45,000 towards legal fees and agent’s commission. The issue arising from the

given situation is whether the proceeds of the sale would incur tax implications as a capital

gain or an ordinary income accruing from business.

Rule

Income, which would be incurred from the use or exploitation of property would be

treated as ordinary income as has been provided under the Income Tax Assessment Act 1997

(Cth) under section 6.5. However, the property would be construed as an asset of capital

nature. this needs to be illustrated with the case of Riches v Westminster Bank Ltd [1947] AC

390. It has also been held by the court that in the case of Steele v Deputy Commissioner of

Taxation [1999] HCA 7 that the utilisation of the property would include business, interest,

rents and any other profit earning activity pertaining to the land.

Again, it can be stated that the amount which would be earned as a proceed incurred from

the sale of the property would be rendered as capital gain as evident from the section 100.35

and the tax consequence of the same would be treated accordingly. The reason behind this

treatment is because the property owing to which the proceeds has been incurred is construed

to be a capital asset under section 100.25 and any proceeds pertaining to the same would be

construed to be a capital asset. It has been held in the case of Visy Industries USA Pty Ltd v

Commissioner of Taxation [2011] FCA 1065 that a property has the status of a capital asset

for the purpose of taxation and any monetary benefit that can be availed by the permanent

disposing off of the same would also be treated to be a capital gain (Barkoczy, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

However, any income that has been earned as an outcome of a business activity is required

to be treated as an ordinary income for the assessment of tax. The definition of the business

activity has been provided in section 995 of the Income Tax Assessment Act 1997 (Cth). This

definition includes any activity that has a commercial essence. The TR 97/11 contains certain

indicators applying which an activity can be brought under the purview of business activity.

These indicators can be discussed as follows. Para. 28-38 of the ruling would require the

activity to be of commercial nature. Para. 39-46 of the ruling would require the activity to

have to be backed by an intention of carrying on a business. Para. 47-54 would require the

activity to be for the sole purpose of earning profit. Para 55-62 would require the activity to

have a regularity and recurrence. Para. 63-67 would require the activity to be similar. Para.

68-76 would require the work to be effected in a planned and organised manner. Para. 77-85

requires the activity to be permanent. Para 86-93 restricts any activity, which is more of a

hobby to be included as a business activity. This can be illustrated with the case of Grapsas v

Commissioner of Taxation [2011] FCA 1465.

Application

In the present situation, Sam has bought 80 acres of farmland in 1984 for $270,000 and

has been running a beef cattle breeding operation. Again, an extra 20 acres of the adjoining

land has also been purchased by the Sam. This needs to be construed as an income, which

would be incurred from the use or exploitation of property would be treated as ordinary

income as has been provided under the Income Tax Assessment Act 1997 (Cth) under section

6.5. However, the property would be construed as an asset of capital nature. this needs to be

illustrated with the case of Riches v Westminster Bank Ltd [1947] AC 390. It has also been

held by the court that in the case of Steele v Deputy Commissioner of Taxation [1999] HCA

7 that the utilisation of the property would include business, interest, rents and any other

profit earning activity pertaining to the land.

However, any income that has been earned as an outcome of a business activity is required

to be treated as an ordinary income for the assessment of tax. The definition of the business

activity has been provided in section 995 of the Income Tax Assessment Act 1997 (Cth). This

definition includes any activity that has a commercial essence. The TR 97/11 contains certain

indicators applying which an activity can be brought under the purview of business activity.

These indicators can be discussed as follows. Para. 28-38 of the ruling would require the

activity to be of commercial nature. Para. 39-46 of the ruling would require the activity to

have to be backed by an intention of carrying on a business. Para. 47-54 would require the

activity to be for the sole purpose of earning profit. Para 55-62 would require the activity to

have a regularity and recurrence. Para. 63-67 would require the activity to be similar. Para.

68-76 would require the work to be effected in a planned and organised manner. Para. 77-85

requires the activity to be permanent. Para 86-93 restricts any activity, which is more of a

hobby to be included as a business activity. This can be illustrated with the case of Grapsas v

Commissioner of Taxation [2011] FCA 1465.

Application

In the present situation, Sam has bought 80 acres of farmland in 1984 for $270,000 and

has been running a beef cattle breeding operation. Again, an extra 20 acres of the adjoining

land has also been purchased by the Sam. This needs to be construed as an income, which

would be incurred from the use or exploitation of property would be treated as ordinary

income as has been provided under the Income Tax Assessment Act 1997 (Cth) under section

6.5. However, the property would be construed as an asset of capital nature. this needs to be

illustrated with the case of Riches v Westminster Bank Ltd [1947] AC 390. It has also been

held by the court that in the case of Steele v Deputy Commissioner of Taxation [1999] HCA

7 that the utilisation of the property would include business, interest, rents and any other

profit earning activity pertaining to the land.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

However, owing to drought and his advancing age, Sam has been considering the selling

of the land. It has been found by Sam, while attempting to sell his land that it can only earn

him $440,000. This needs to be treated as a capital gain as it can be stated that the amount

which would be earned as a proceed incurred from the sale of the property would be rendered

as capital gain as evident from the section 100.35 and the tax consequence of the same would

be treated accordingly. The reason behind this treatment is because the property owing to

which the proceeds has been incurred is construed to be a capital asset under section 100.25

and any proceeds pertaining to the same would be construed to be a capital asset. It has been

held in the case of Visy Industries USA Pty Ltd v Commissioner of Taxation [2011] FCA

1065 that a property has the status of a capital asset for the purpose of taxation and any

monetary benefit that can be availed by the permanent disposing off of the same would also

be treated to be a capital gain.

This has not been satisfying for Sam as he has put a considerable amount of effort and has

incurred a considerable amount of cost for the purpose of modifying the land. He has availed

an advice from a local real estate advisor who has advised to make the sale of the land after

subdivision. Sam has acted in accordance with the advice and re-zoned his land for sub-

division. This has made Sam spent $450,000 as sub-division costs such as surveyor fees,

electricity and water connections and main road access, a local construction company agreed

to buy the entire sub-division for $1,100,000. All these has earned Sam a contract for sale of

the land at $1,100,000. He has further incurred an expense of $45,000 towards legal fees and

agent’s commission. This needs to be considered as a business activity and any income that

has been earned as an outcome of a business activity is required to be treated as an ordinary

income for the assessment of tax. The definition of the business activity has been provided in

section 995 of the Income Tax Assessment Act 1997 (Cth). This definition includes any

activity that has a commercial essence. The TR 97/11 contains certain indicators applying

However, owing to drought and his advancing age, Sam has been considering the selling

of the land. It has been found by Sam, while attempting to sell his land that it can only earn

him $440,000. This needs to be treated as a capital gain as it can be stated that the amount

which would be earned as a proceed incurred from the sale of the property would be rendered

as capital gain as evident from the section 100.35 and the tax consequence of the same would

be treated accordingly. The reason behind this treatment is because the property owing to

which the proceeds has been incurred is construed to be a capital asset under section 100.25

and any proceeds pertaining to the same would be construed to be a capital asset. It has been

held in the case of Visy Industries USA Pty Ltd v Commissioner of Taxation [2011] FCA

1065 that a property has the status of a capital asset for the purpose of taxation and any

monetary benefit that can be availed by the permanent disposing off of the same would also

be treated to be a capital gain.

This has not been satisfying for Sam as he has put a considerable amount of effort and has

incurred a considerable amount of cost for the purpose of modifying the land. He has availed

an advice from a local real estate advisor who has advised to make the sale of the land after

subdivision. Sam has acted in accordance with the advice and re-zoned his land for sub-

division. This has made Sam spent $450,000 as sub-division costs such as surveyor fees,

electricity and water connections and main road access, a local construction company agreed

to buy the entire sub-division for $1,100,000. All these has earned Sam a contract for sale of

the land at $1,100,000. He has further incurred an expense of $45,000 towards legal fees and

agent’s commission. This needs to be considered as a business activity and any income that

has been earned as an outcome of a business activity is required to be treated as an ordinary

income for the assessment of tax. The definition of the business activity has been provided in

section 995 of the Income Tax Assessment Act 1997 (Cth). This definition includes any

activity that has a commercial essence. The TR 97/11 contains certain indicators applying

11TAXATION

which an activity can be brought under the purview of business activity. These indicators can

be discussed as follows. Para. 28-38 of the ruling would require the activity to be of

commercial nature. Para. 39-46 of the ruling would require the activity to have to be backed

by an intention of carrying on a business. Para. 47-54 would require the activity to be for the

sole purpose of earning profit. Para 55-62 would require the activity to have a regularity and

recurrence. Para. 63-67 would require the activity to be similar. Para. 68-76 would require the

work to be effected in a planned and organised manner. Para. 77-85 requires the activity to be

permanent. Para 86-93 restricts any activity, which is more of a hobby to be included as a

business activity. This can be illustrated with the case of Grapsas v Commissioner of

Taxation [2011] FCA 1465.

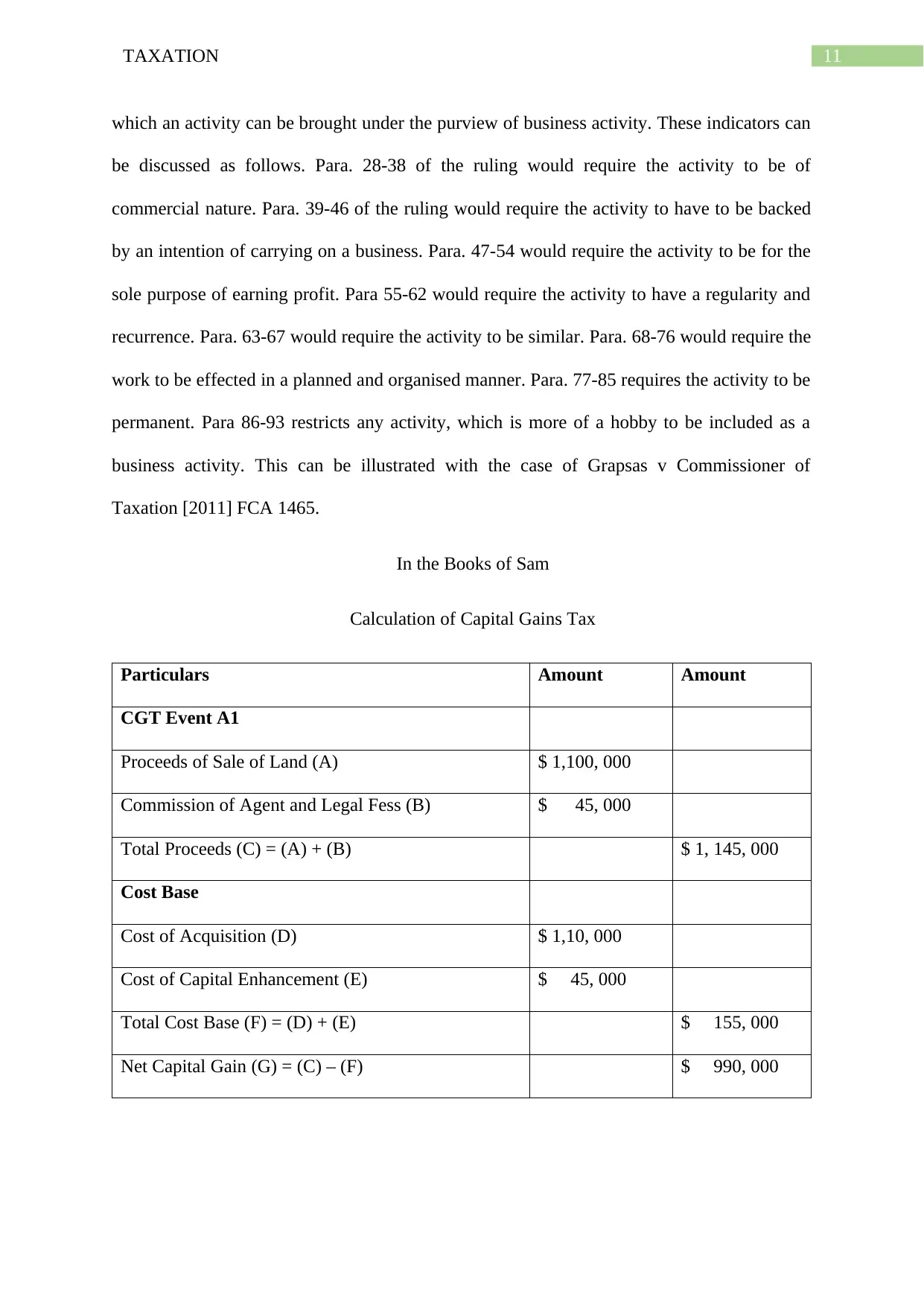

In the Books of Sam

Calculation of Capital Gains Tax

Particulars Amount Amount

CGT Event A1

Proceeds of Sale of Land (A) $ 1,100, 000

Commission of Agent and Legal Fess (B) $ 45, 000

Total Proceeds (C) = (A) + (B) $ 1, 145, 000

Cost Base

Cost of Acquisition (D) $ 1,10, 000

Cost of Capital Enhancement (E) $ 45, 000

Total Cost Base (F) = (D) + (E) $ 155, 000

Net Capital Gain (G) = (C) – (F) $ 990, 000

which an activity can be brought under the purview of business activity. These indicators can

be discussed as follows. Para. 28-38 of the ruling would require the activity to be of

commercial nature. Para. 39-46 of the ruling would require the activity to have to be backed

by an intention of carrying on a business. Para. 47-54 would require the activity to be for the

sole purpose of earning profit. Para 55-62 would require the activity to have a regularity and

recurrence. Para. 63-67 would require the activity to be similar. Para. 68-76 would require the

work to be effected in a planned and organised manner. Para. 77-85 requires the activity to be

permanent. Para 86-93 restricts any activity, which is more of a hobby to be included as a

business activity. This can be illustrated with the case of Grapsas v Commissioner of

Taxation [2011] FCA 1465.

In the Books of Sam

Calculation of Capital Gains Tax

Particulars Amount Amount

CGT Event A1

Proceeds of Sale of Land (A) $ 1,100, 000

Commission of Agent and Legal Fess (B) $ 45, 000

Total Proceeds (C) = (A) + (B) $ 1, 145, 000

Cost Base

Cost of Acquisition (D) $ 1,10, 000

Cost of Capital Enhancement (E) $ 45, 000

Total Cost Base (F) = (D) + (E) $ 155, 000

Net Capital Gain (G) = (C) – (F) $ 990, 000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.