Taxation Theory Assignment - Finance, University of XYZ

VerifiedAdded on 2020/04/01

|4

|1455

|41

Homework Assignment

AI Summary

This document provides a comprehensive analysis of taxation theory through the lens of several case studies and scenarios. The assignment begins by examining the tax implications of capital gains and losses on various assets, including collectables, personal use assets, and shares in a listed co...

TAXATION THEORY

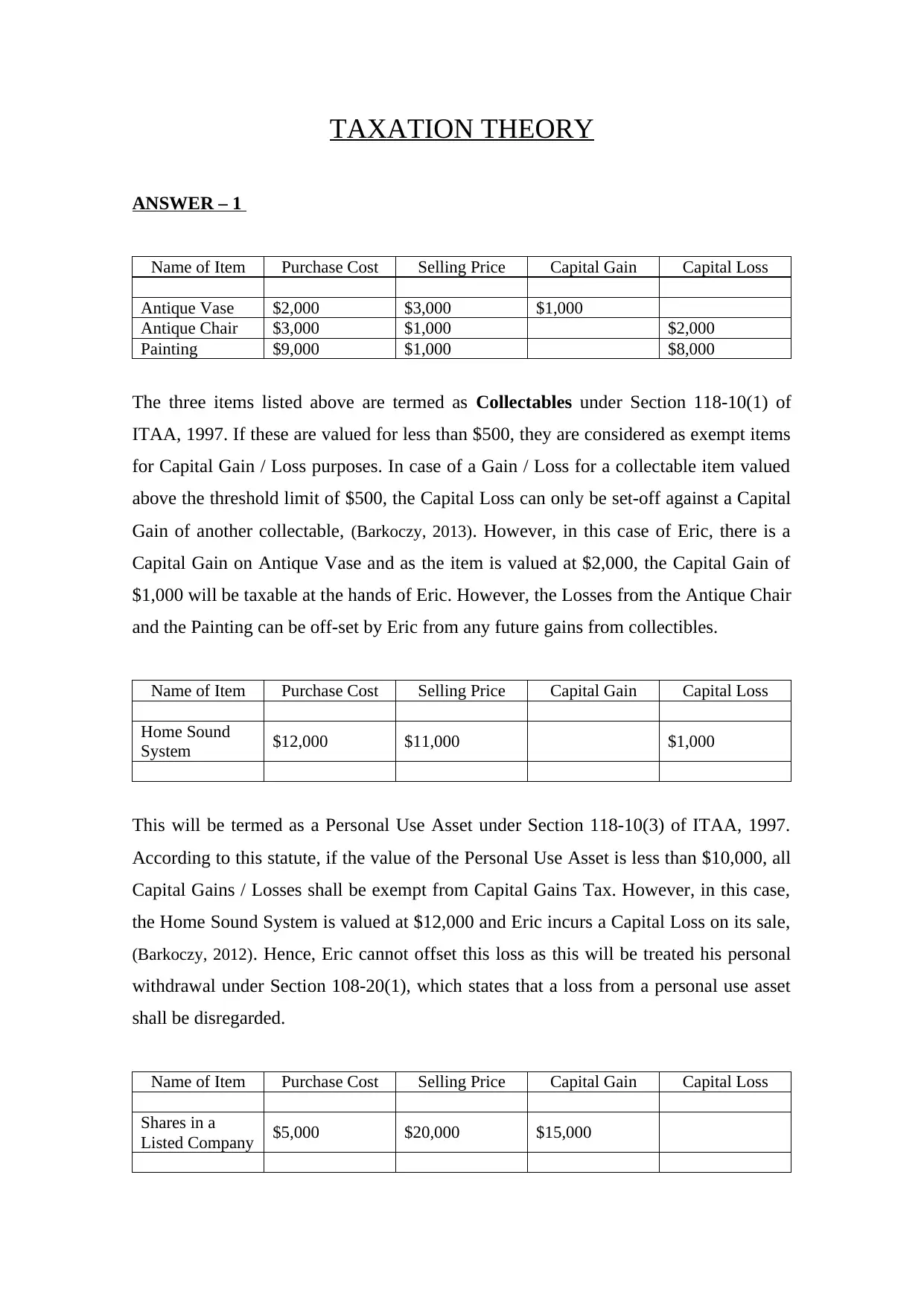

ANSWER – 1

Name of Item Purchase Cost Selling Price Capital Gain Capital Loss

Antique Vase $2,000 $3,000 $1,000

Antique Chair $3,000 $1,000 $2,000

Painting $9,000 $1,000 $8,000

The three items listed above are termed as Collectables under Section 118-10(1) of

ITAA, 1997. If these are valued for less than $500, they are considered as exempt items

for Capital Gain / Loss purposes. In case of a Gain / Loss for a collectable item valued

above the threshold limit of $500, the Capital Loss can only be set-off against a Capital

Gain of another collectable, (Barkoczy, 2013). However, in this case of Eric, there is a

Capital Gain on Antique Vase and as the item is valued at $2,000, the Capital Gain of

$1,000 will be taxable at the hands of Eric. However, the Losses from the Antique Chair

and the Painting can be off-set by Eric from any future gains from collectibles.

Name of Item Purchase Cost Selling Price Capital Gain Capital Loss

Home Sound

System $12,000 $11,000 $1,000

This will be termed as a Personal Use Asset under Section 118-10(3) of ITAA, 1997.

According to this statute, if the value of the Personal Use Asset is less than $10,000, all

Capital Gains / Losses shall be exempt from Capital Gains Tax. However, in this case,

the Home Sound System is valued at $12,000 and Eric incurs a Capital Loss on its sale,

(Barkoczy, 2012). Hence, Eric cannot offset this loss as this will be treated his personal

withdrawal under Section 108-20(1), which states that a loss from a personal use asset

shall be disregarded.

Name of Item Purchase Cost Selling Price Capital Gain Capital Loss

Shares in a

Listed Company $5,000 $20,000 $15,000

ANSWER – 1

Name of Item Purchase Cost Selling Price Capital Gain Capital Loss

Antique Vase $2,000 $3,000 $1,000

Antique Chair $3,000 $1,000 $2,000

Painting $9,000 $1,000 $8,000

The three items listed above are termed as Collectables under Section 118-10(1) of

ITAA, 1997. If these are valued for less than $500, they are considered as exempt items

for Capital Gain / Loss purposes. In case of a Gain / Loss for a collectable item valued

above the threshold limit of $500, the Capital Loss can only be set-off against a Capital

Gain of another collectable, (Barkoczy, 2013). However, in this case of Eric, there is a

Capital Gain on Antique Vase and as the item is valued at $2,000, the Capital Gain of

$1,000 will be taxable at the hands of Eric. However, the Losses from the Antique Chair

and the Painting can be off-set by Eric from any future gains from collectibles.

Name of Item Purchase Cost Selling Price Capital Gain Capital Loss

Home Sound

System $12,000 $11,000 $1,000

This will be termed as a Personal Use Asset under Section 118-10(3) of ITAA, 1997.

According to this statute, if the value of the Personal Use Asset is less than $10,000, all

Capital Gains / Losses shall be exempt from Capital Gains Tax. However, in this case,

the Home Sound System is valued at $12,000 and Eric incurs a Capital Loss on its sale,

(Barkoczy, 2012). Hence, Eric cannot offset this loss as this will be treated his personal

withdrawal under Section 108-20(1), which states that a loss from a personal use asset

shall be disregarded.

Name of Item Purchase Cost Selling Price Capital Gain Capital Loss

Shares in a

Listed Company $5,000 $20,000 $15,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is a CGT Asset as described in Section 108-5(1) of ITAA, 1997. Eric can claim a

Capital Loss on a CGT Asset as a deductible expenses from his Assessable Income.

Similarly, a Capital Gain will be added to the Assessable Income of Eric and he shall

pay tax on it. As the shares were acquired within 12 months from their disposal date,

Eric is not eligible for any discount on the Capital Gain and will be liable to pay tax on

Capital Gain of $15,000, (Barkoczy, 2011).

ANSWER – 2

A loan fringe benefit tax on the part of the employer arises when the employer provide a

loan to an employee at a subsidised rate of interest during a FBT year. A low rate of

interest is applicable when it is less than the applicable statutory rate of interest, which

is also known as “benchmark interest rate”. As on 1 April 2016, this benchmark interest

rate was 5.65%, (Alexander & Fogarty, 2009). For taxation purposes, the taxable value of

a loan fringe benefit is calculated as the difference between:

(a) the interest which would have accrued during the FBT year in case the

benchmark interest rate had been applied to the outstanding monthly balance of

the loan, and

(b) the amount of interest that actually accrued at the subsidised rate of interest.

Now, if the employee uses a part or whole of the loan to make investments in interest-

bearing instruments, then the interest payable on the loan would be wholly deductible at

the hands of the employee for income tax purposes. So, under such a deductible rule, the

taxable value of such a loan fringe benefit will be nil, regardless of whether the

employer charges a low, or even a nil, rate of interest on the loan. This happens because

the employee becomes entitled to income tax deduction on the interest charged from

him on that portion of the loan which he is using for earning an assessable income.

Whereas, this is not applicable on that interest which is charged from the employee on

that portion of the loan which he solely uses for his domestic purposes, (Alexander &

Fogarty, 2009).

ANSWER – 3

Capital Loss on a CGT Asset as a deductible expenses from his Assessable Income.

Similarly, a Capital Gain will be added to the Assessable Income of Eric and he shall

pay tax on it. As the shares were acquired within 12 months from their disposal date,

Eric is not eligible for any discount on the Capital Gain and will be liable to pay tax on

Capital Gain of $15,000, (Barkoczy, 2011).

ANSWER – 2

A loan fringe benefit tax on the part of the employer arises when the employer provide a

loan to an employee at a subsidised rate of interest during a FBT year. A low rate of

interest is applicable when it is less than the applicable statutory rate of interest, which

is also known as “benchmark interest rate”. As on 1 April 2016, this benchmark interest

rate was 5.65%, (Alexander & Fogarty, 2009). For taxation purposes, the taxable value of

a loan fringe benefit is calculated as the difference between:

(a) the interest which would have accrued during the FBT year in case the

benchmark interest rate had been applied to the outstanding monthly balance of

the loan, and

(b) the amount of interest that actually accrued at the subsidised rate of interest.

Now, if the employee uses a part or whole of the loan to make investments in interest-

bearing instruments, then the interest payable on the loan would be wholly deductible at

the hands of the employee for income tax purposes. So, under such a deductible rule, the

taxable value of such a loan fringe benefit will be nil, regardless of whether the

employer charges a low, or even a nil, rate of interest on the loan. This happens because

the employee becomes entitled to income tax deduction on the interest charged from

him on that portion of the loan which he is using for earning an assessable income.

Whereas, this is not applicable on that interest which is charged from the employee on

that portion of the loan which he solely uses for his domestic purposes, (Alexander &

Fogarty, 2009).

ANSWER – 3

It is clear from the agreement entered between Jack and Jill that ONLY profit will be

distributed as 10% to Jack and 90% to Jill, whereas the loss will be 100% liability of

Jack. Hence, Jack will claim the amount of $10,000 as a deductible amount under

section 8-1 of the ITAA, 1997 from his Assessable Income for the year. Under the

provisions of Joint Tenants, the law is clear that both the partners shall be eligible to

claim all Capital Gains / Losses in EQUAL proportions, (Cch, 2012).

ANSWER – 4

The principle established by the case of IRC v Duke of Westminster (1936) stated that

tax evasion happens when taxpayers deliberately start misrepresenting or concealing the

true state of their affairs to the taxation authorities in order to reduce their tax payments,

whereas tax avoidance is considered as acceptable and legal. Unsurprisingly, this

principle is still relevant in Australia and most other developed as well as developing

economies, (Cch, 2012). The Australian authorities state that more than a sixth of tax

loss is due to tax evasion and a further one sixth is caused by tax avoidance, whereas the

balance is just uncollected taxes. Taxation authorities in Australia still do not like

taxpayers’ trying tax avoidance although such actions are viewed as actions taken by

taxpayer for taking advantage of a tax relief in a legal manner, (Barkoczy, 2013).

ANSWER – 5

Income can be classified either as –

(A) Ordinary Income

Ordinary Income includes incomes earned by personal exertion, carrying on a business

or income from properties, as is defined under sections 6-5(1) to (4) of ITAA, 1997.

(B) Statutory Income

All incomes not covered under ordinary income are termed as Statutory Incomes, as is

defined under sections 6-10(1) to (5) of ITAA, 1997.

(C) Windfall Income

Winnings from lotteries and inheritances are examples of Windfall Incomes and these

are also covered under sections 6-10(1) to (5) of ITAA, 1997.

(D) Capital Gains

distributed as 10% to Jack and 90% to Jill, whereas the loss will be 100% liability of

Jack. Hence, Jack will claim the amount of $10,000 as a deductible amount under

section 8-1 of the ITAA, 1997 from his Assessable Income for the year. Under the

provisions of Joint Tenants, the law is clear that both the partners shall be eligible to

claim all Capital Gains / Losses in EQUAL proportions, (Cch, 2012).

ANSWER – 4

The principle established by the case of IRC v Duke of Westminster (1936) stated that

tax evasion happens when taxpayers deliberately start misrepresenting or concealing the

true state of their affairs to the taxation authorities in order to reduce their tax payments,

whereas tax avoidance is considered as acceptable and legal. Unsurprisingly, this

principle is still relevant in Australia and most other developed as well as developing

economies, (Cch, 2012). The Australian authorities state that more than a sixth of tax

loss is due to tax evasion and a further one sixth is caused by tax avoidance, whereas the

balance is just uncollected taxes. Taxation authorities in Australia still do not like

taxpayers’ trying tax avoidance although such actions are viewed as actions taken by

taxpayer for taking advantage of a tax relief in a legal manner, (Barkoczy, 2013).

ANSWER – 5

Income can be classified either as –

(A) Ordinary Income

Ordinary Income includes incomes earned by personal exertion, carrying on a business

or income from properties, as is defined under sections 6-5(1) to (4) of ITAA, 1997.

(B) Statutory Income

All incomes not covered under ordinary income are termed as Statutory Incomes, as is

defined under sections 6-10(1) to (5) of ITAA, 1997.

(C) Windfall Income

Winnings from lotteries and inheritances are examples of Windfall Incomes and these

are also covered under sections 6-10(1) to (5) of ITAA, 1997.

(D) Capital Gains

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All profits derived from sale of assets are termed as Capital Gains, as is defined under

sections 104-10(4) of ITAA, 1997, (Barkoczy, 2013).

In case Bill wants to avail the first option, it will be assumed for taxation purposes that

he is carrying on a business and the income which he derives from the sale of the timber

will be considered his “Ordinary Income” and added to his Assessable Income under

section 6-1(1) of ITAA, 1997. However, in case Bill goes for the second option, then

the timber would be considered as a “Capital Asset” as it is part of the land owned by

Bill. Thus, the lump sum payment of $50,000 which Bill receives shall be considered as

Capital Gain, (Barkoczy, 2012). Although this will also be added to his Assessable

Income under section 6-1(1), Bill can avail the 50% Discount under the Discount

Method on the Gross Capital Gain which he makes.

LIST OF REFERENCES

Alexander, Dr. R. and Fogarty, H. J. (2009) Australian Master Family Law Guide, (3rd ed.)

Sydney, NSW: CCH Australia Limited.

Barkoczy, S. (2011) Core Tax Legislation and Study Guide (16th ed.) North Ryde, NSW: CCH

Australia Limited.

Barkoczy, S. (2012) Australian Tax Case book (10th ed.) North Ryde, NSW: CCH Australia

Limited.

Barkoczy, S. (2013) Foundations of Taxation Law (5th ed.) North Ryde, NSW: CCH Australia

Limited.

Cch, (2012) Australian Master Tax Guide. Sydney, NSW: CCH Australia Limited.

sections 104-10(4) of ITAA, 1997, (Barkoczy, 2013).

In case Bill wants to avail the first option, it will be assumed for taxation purposes that

he is carrying on a business and the income which he derives from the sale of the timber

will be considered his “Ordinary Income” and added to his Assessable Income under

section 6-1(1) of ITAA, 1997. However, in case Bill goes for the second option, then

the timber would be considered as a “Capital Asset” as it is part of the land owned by

Bill. Thus, the lump sum payment of $50,000 which Bill receives shall be considered as

Capital Gain, (Barkoczy, 2012). Although this will also be added to his Assessable

Income under section 6-1(1), Bill can avail the 50% Discount under the Discount

Method on the Gross Capital Gain which he makes.

LIST OF REFERENCES

Alexander, Dr. R. and Fogarty, H. J. (2009) Australian Master Family Law Guide, (3rd ed.)

Sydney, NSW: CCH Australia Limited.

Barkoczy, S. (2011) Core Tax Legislation and Study Guide (16th ed.) North Ryde, NSW: CCH

Australia Limited.

Barkoczy, S. (2012) Australian Tax Case book (10th ed.) North Ryde, NSW: CCH Australia

Limited.

Barkoczy, S. (2013) Foundations of Taxation Law (5th ed.) North Ryde, NSW: CCH Australia

Limited.

Cch, (2012) Australian Master Tax Guide. Sydney, NSW: CCH Australia Limited.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.