Taxation Law: Analysis of Capital Gains, Personal Exertion & Gift Tax

VerifiedAdded on 2023/04/04

|13

|2145

|358

Report

AI Summary

This report delves into Australian income tax law, examining capital gains, personal exertion income, and gift tax provisions. It analyzes Helen's asset sales, determining capital gains or losses using the indexation method. Barbara's income from writing and selling books is classified as personal exertion income, supported by legal precedents. The report also discusses the tax implications of Patrick providing a loan to his son, differentiating between loans and gifts, and considering potential gift tax liabilities. The conclusion summarizes the findings, emphasizing the importance of understanding these tax concepts and their practical applications.

Taxation theory,

Practice and Law

Practice and Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question 1..............................................................................................................................................3

Question 2..............................................................................................................................................7

Question 3..............................................................................................................................................9

CONCLUSION........................................................................................................................................11

REFERENCES..............................................................................................................................................12

Question 1..............................................................................................................................................3

Question 2..............................................................................................................................................7

Question 3..............................................................................................................................................9

CONCLUSION........................................................................................................................................11

REFERENCES..............................................................................................................................................12

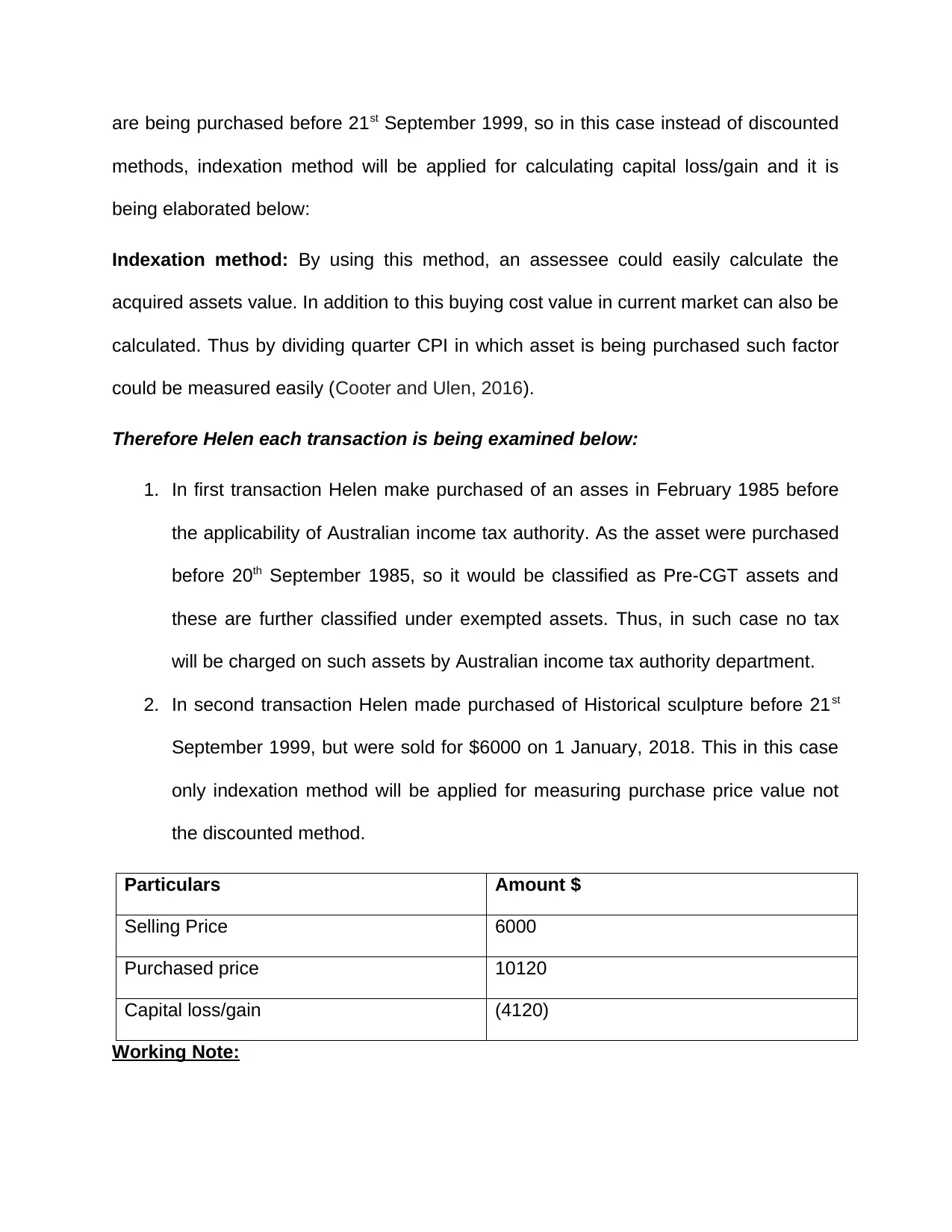

Question 1

When a taxpayer sells the asset at higher than the purchase amount then it take place

capital gain or loss. The variation between the buying cost and the selling price will be

term to be the capital gain (Dietschand Rixen, 2014). As per the question in the current

year, Helen sold out her assets. In case while selling out her assets, if the Helen come

up with capital gain then she will be liable to pay tax in the current financial year. This is

so because separate provision regarding capital gain tax is being maintained by the

Australian tax. Beside this, capital gain also leads towards shifting of tax burden to the

taxpayer. On the other hand, if by selling its asset, assessee possess capital loss then

such loss will be carried forward and will be managed or it can be said that such loss

will be set off with the capital gain in current year. Those assets which acquired after

20th September, 1985 will come under CGT tax. Beside this, rate for capital gain is also

not specified by the Australian income tax. But in case, if an assessee retain assets for

12 months or more, then its capital gain would be taxed by 23.5% (Vatn, 2015). Such

rate is being availed only if a discount aspect is being availed by assesse and if assets

are being retained for 12 months or more. Moreover, discount facility is not being

availed by those assesse who retained by assessee before 21st September, 1999.

Furthermore, indexation method is applied if the assesse make the purchase of an

asset before the aforementioned date. Beside this, assessee could make use of

indexation or discounted method for the purpose of calculation of capital gain income

only in case of assesse make purchase of asset before 21st September, 1999. Whereas

in case if assess hold assets for 12 or more than 12 months then neither the discounted

nor the indexation method could be applied. Thus, as per the question 1 all the assets

When a taxpayer sells the asset at higher than the purchase amount then it take place

capital gain or loss. The variation between the buying cost and the selling price will be

term to be the capital gain (Dietschand Rixen, 2014). As per the question in the current

year, Helen sold out her assets. In case while selling out her assets, if the Helen come

up with capital gain then she will be liable to pay tax in the current financial year. This is

so because separate provision regarding capital gain tax is being maintained by the

Australian tax. Beside this, capital gain also leads towards shifting of tax burden to the

taxpayer. On the other hand, if by selling its asset, assessee possess capital loss then

such loss will be carried forward and will be managed or it can be said that such loss

will be set off with the capital gain in current year. Those assets which acquired after

20th September, 1985 will come under CGT tax. Beside this, rate for capital gain is also

not specified by the Australian income tax. But in case, if an assessee retain assets for

12 months or more, then its capital gain would be taxed by 23.5% (Vatn, 2015). Such

rate is being availed only if a discount aspect is being availed by assesse and if assets

are being retained for 12 months or more. Moreover, discount facility is not being

availed by those assesse who retained by assessee before 21st September, 1999.

Furthermore, indexation method is applied if the assesse make the purchase of an

asset before the aforementioned date. Beside this, assessee could make use of

indexation or discounted method for the purpose of calculation of capital gain income

only in case of assesse make purchase of asset before 21st September, 1999. Whereas

in case if assess hold assets for 12 or more than 12 months then neither the discounted

nor the indexation method could be applied. Thus, as per the question 1 all the assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

are being purchased before 21st September 1999, so in this case instead of discounted

methods, indexation method will be applied for calculating capital loss/gain and it is

being elaborated below:

Indexation method: By using this method, an assessee could easily calculate the

acquired assets value. In addition to this buying cost value in current market can also be

calculated. Thus by dividing quarter CPI in which asset is being purchased such factor

could be measured easily (Cooter and Ulen, 2016).

Therefore Helen each transaction is being examined below:

1. In first transaction Helen make purchased of an asses in February 1985 before

the applicability of Australian income tax authority. As the asset were purchased

before 20th September 1985, so it would be classified as Pre-CGT assets and

these are further classified under exempted assets. Thus, in such case no tax

will be charged on such assets by Australian income tax authority department.

2. In second transaction Helen made purchased of Historical sculpture before 21st

September 1999, but were sold for $6000 on 1 January, 2018. This in this case

only indexation method will be applied for measuring purchase price value not

the discounted method.

Particulars Amount $

Selling Price 6000

Purchased price 10120

Capital loss/gain (4120)

Working Note:

methods, indexation method will be applied for calculating capital loss/gain and it is

being elaborated below:

Indexation method: By using this method, an assessee could easily calculate the

acquired assets value. In addition to this buying cost value in current market can also be

calculated. Thus by dividing quarter CPI in which asset is being purchased such factor

could be measured easily (Cooter and Ulen, 2016).

Therefore Helen each transaction is being examined below:

1. In first transaction Helen make purchased of an asses in February 1985 before

the applicability of Australian income tax authority. As the asset were purchased

before 20th September 1985, so it would be classified as Pre-CGT assets and

these are further classified under exempted assets. Thus, in such case no tax

will be charged on such assets by Australian income tax authority department.

2. In second transaction Helen made purchased of Historical sculpture before 21st

September 1999, but were sold for $6000 on 1 January, 2018. This in this case

only indexation method will be applied for measuring purchase price value not

the discounted method.

Particulars Amount $

Selling Price 6000

Purchased price 10120

Capital loss/gain (4120)

Working Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

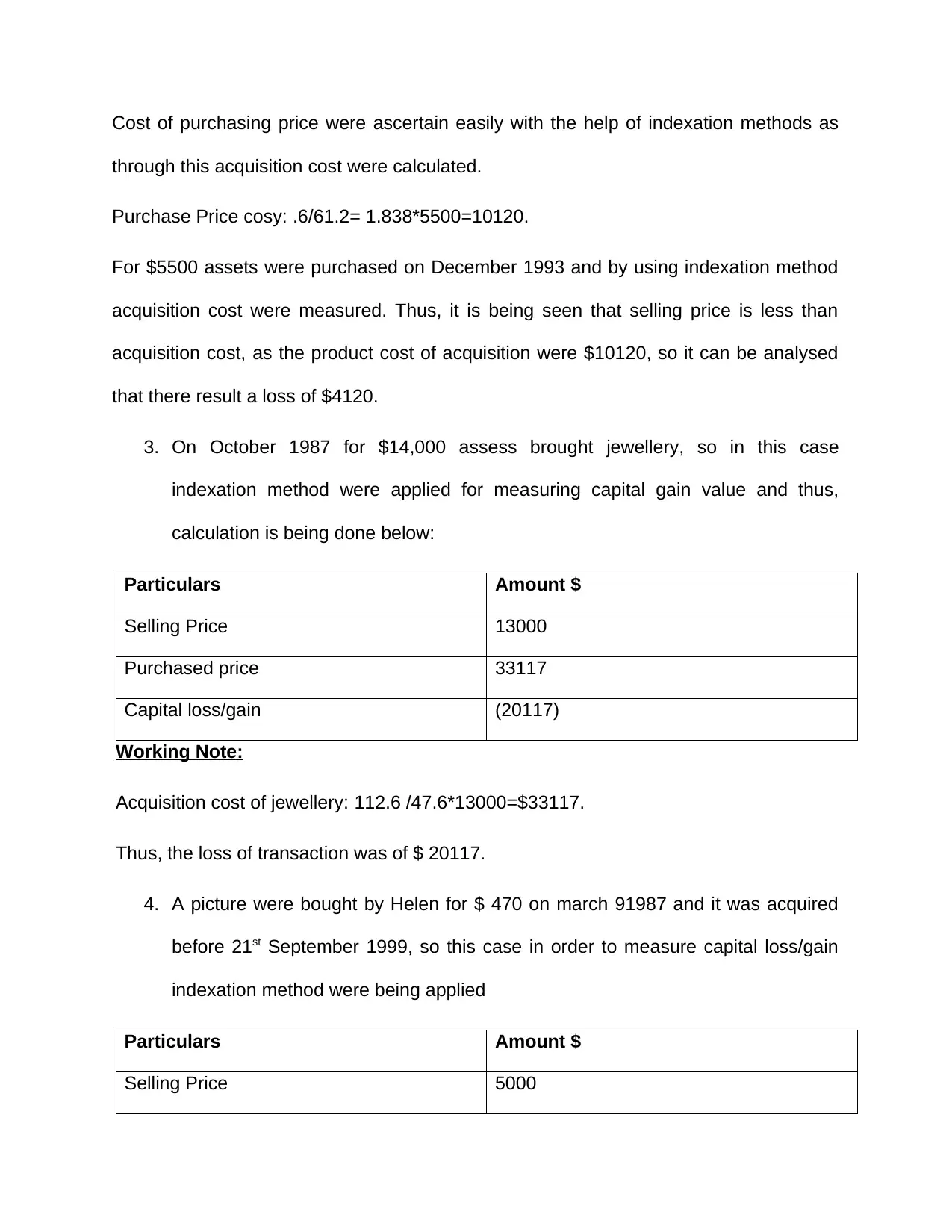

Cost of purchasing price were ascertain easily with the help of indexation methods as

through this acquisition cost were calculated.

Purchase Price cosy: .6/61.2= 1.838*5500=10120.

For $5500 assets were purchased on December 1993 and by using indexation method

acquisition cost were measured. Thus, it is being seen that selling price is less than

acquisition cost, as the product cost of acquisition were $10120, so it can be analysed

that there result a loss of $4120.

3. On October 1987 for $14,000 assess brought jewellery, so in this case

indexation method were applied for measuring capital gain value and thus,

calculation is being done below:

Particulars Amount $

Selling Price 13000

Purchased price 33117

Capital loss/gain (20117)

Working Note:

Acquisition cost of jewellery: 112.6 /47.6*13000=$33117.

Thus, the loss of transaction was of $ 20117.

4. A picture were bought by Helen for $ 470 on march 91987 and it was acquired

before 21st September 1999, so this case in order to measure capital loss/gain

indexation method were being applied

Particulars Amount $

Selling Price 5000

through this acquisition cost were calculated.

Purchase Price cosy: .6/61.2= 1.838*5500=10120.

For $5500 assets were purchased on December 1993 and by using indexation method

acquisition cost were measured. Thus, it is being seen that selling price is less than

acquisition cost, as the product cost of acquisition were $10120, so it can be analysed

that there result a loss of $4120.

3. On October 1987 for $14,000 assess brought jewellery, so in this case

indexation method were applied for measuring capital gain value and thus,

calculation is being done below:

Particulars Amount $

Selling Price 13000

Purchased price 33117

Capital loss/gain (20117)

Working Note:

Acquisition cost of jewellery: 112.6 /47.6*13000=$33117.

Thus, the loss of transaction was of $ 20117.

4. A picture were bought by Helen for $ 470 on march 91987 and it was acquired

before 21st September 1999, so this case in order to measure capital loss/gain

indexation method were being applied

Particulars Amount $

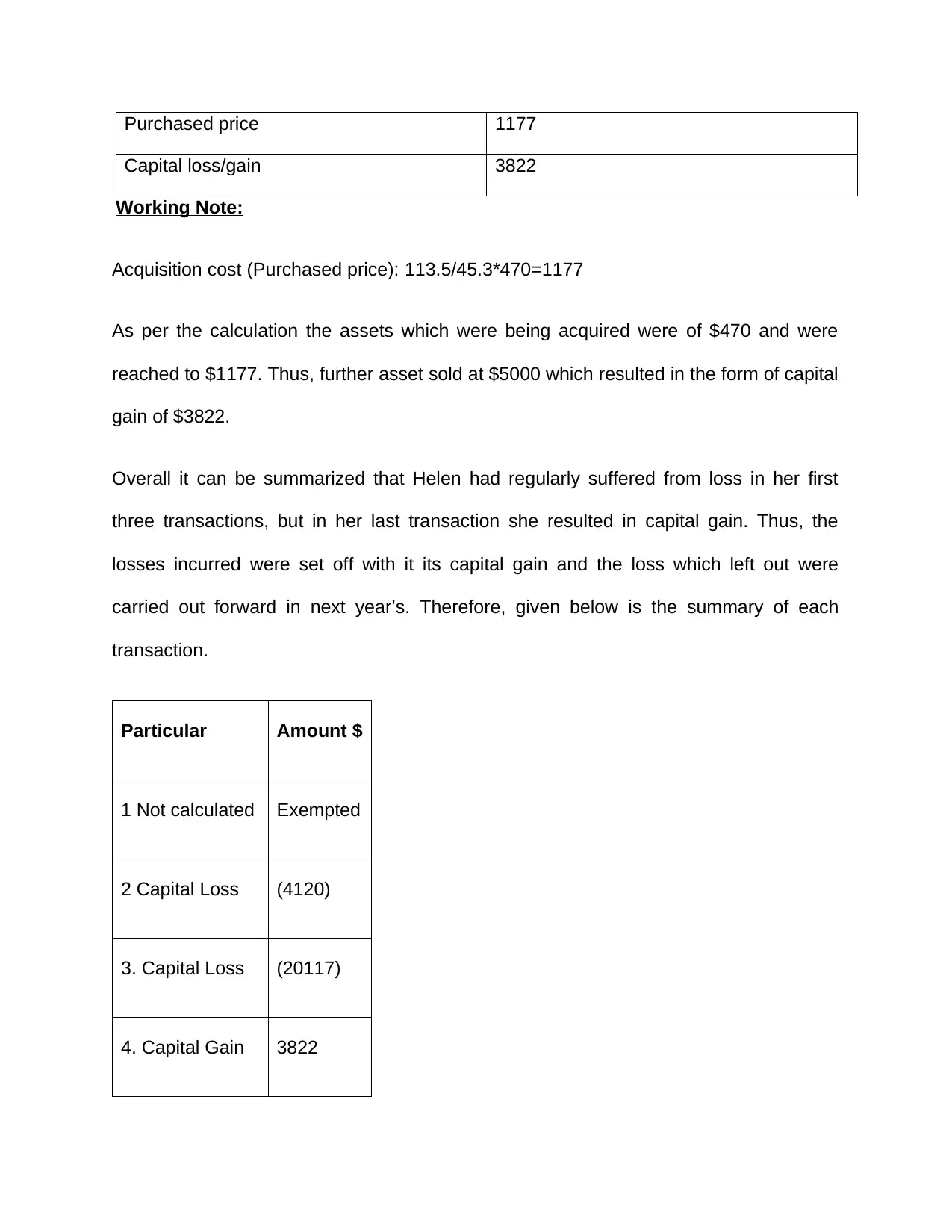

Selling Price 5000

Purchased price 1177

Capital loss/gain 3822

Working Note:

Acquisition cost (Purchased price): 113.5/45.3*470=1177

As per the calculation the assets which were being acquired were of $470 and were

reached to $1177. Thus, further asset sold at $5000 which resulted in the form of capital

gain of $3822.

Overall it can be summarized that Helen had regularly suffered from loss in her first

three transactions, but in her last transaction she resulted in capital gain. Thus, the

losses incurred were set off with it its capital gain and the loss which left out were

carried out forward in next year’s. Therefore, given below is the summary of each

transaction.

Particular Amount $

1 Not calculated Exempted

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Capital loss/gain 3822

Working Note:

Acquisition cost (Purchased price): 113.5/45.3*470=1177

As per the calculation the assets which were being acquired were of $470 and were

reached to $1177. Thus, further asset sold at $5000 which resulted in the form of capital

gain of $3822.

Overall it can be summarized that Helen had regularly suffered from loss in her first

three transactions, but in her last transaction she resulted in capital gain. Thus, the

losses incurred were set off with it its capital gain and the loss which left out were

carried out forward in next year’s. Therefore, given below is the summary of each

transaction.

Particular Amount $

1 Not calculated Exempted

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total capital

loss

(20415)

Question 2

As per the ITAA 1997 provision, Personal exertion income refers to the earned income

as per ITAA, 1997 Section 393(10). Given below are some the incomes which are being

treated as Ordinary income:

1. Subsidy or grant received

2. Wages and salary

3. Fees and commission

4. Income from business and profession

5. Income from disposed property

6. In capacity of workers, allowances earned by an assessee.

CASE 1:

First Payment:

As per the above mentioned clarification it is being cleared that income which is being

earned from personal skill, knowledge and expertise then such income will be

considered under personal exertion income not in capital gain/loss. So the income

earned of $13,400 by writing books from own personal skills will be said to be personal

exertion income. This explanation is being well supported by the case of ‘Brent v FCT

(1971) 125 CLR 418’ (Snape, 2015). In this case, an assessee sold out the copyright of

his own written book name ‘Husband story of life’ for which an assessee received

revenue. Such revenue will not be counted under the head of capital gain as it will be

loss

(20415)

Question 2

As per the ITAA 1997 provision, Personal exertion income refers to the earned income

as per ITAA, 1997 Section 393(10). Given below are some the incomes which are being

treated as Ordinary income:

1. Subsidy or grant received

2. Wages and salary

3. Fees and commission

4. Income from business and profession

5. Income from disposed property

6. In capacity of workers, allowances earned by an assessee.

CASE 1:

First Payment:

As per the above mentioned clarification it is being cleared that income which is being

earned from personal skill, knowledge and expertise then such income will be

considered under personal exertion income not in capital gain/loss. So the income

earned of $13,400 by writing books from own personal skills will be said to be personal

exertion income. This explanation is being well supported by the case of ‘Brent v FCT

(1971) 125 CLR 418’ (Snape, 2015). In this case, an assessee sold out the copyright of

his own written book name ‘Husband story of life’ for which an assessee received

revenue. Such revenue will not be counted under the head of capital gain as it will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

counted under the head of personal exertion income, as by selling out own written book

which was published through own skills and effort will be considered as personal

income (Dafflon, 2015). Therefore, same case is being applied upon Barbara. Who sold

out its own written books and her income will not be considered under capital gain.

Second Payment

Barbara received $4350 for selling out its book name ‘Economics Principles’ to Eco

Books Ltd. Thus, such income received by Barbara will be considered under her

personal income from exertion. This statement has been made clear in the above

mentioned case of ‘Brent v FCT (1971) 125 CLR 418’ in which a lady rendered the right

to copy out her written book name ‘Husband story of life’ to newspaper agency

(Paolella and Durand, 2016).

Third payment

While collecting several interview manuscripts during writing of book name ‘Economics

Principles’, income received were of $3200 and it will be counted under the personal

exertion income heading. Thus, the income earned by Barbara for collecting

manuscripts which has helped her to write a book involves her own personal exertion;

Hence, it will be right to include such earned income under personal exertion ( Filatova,

2014).

CASE 2

If Barbara write her book before contract signing and sell it later on to Eco book

Ltd.

which was published through own skills and effort will be considered as personal

income (Dafflon, 2015). Therefore, same case is being applied upon Barbara. Who sold

out its own written books and her income will not be considered under capital gain.

Second Payment

Barbara received $4350 for selling out its book name ‘Economics Principles’ to Eco

Books Ltd. Thus, such income received by Barbara will be considered under her

personal income from exertion. This statement has been made clear in the above

mentioned case of ‘Brent v FCT (1971) 125 CLR 418’ in which a lady rendered the right

to copy out her written book name ‘Husband story of life’ to newspaper agency

(Paolella and Durand, 2016).

Third payment

While collecting several interview manuscripts during writing of book name ‘Economics

Principles’, income received were of $3200 and it will be counted under the personal

exertion income heading. Thus, the income earned by Barbara for collecting

manuscripts which has helped her to write a book involves her own personal exertion;

Hence, it will be right to include such earned income under personal exertion ( Filatova,

2014).

CASE 2

If Barbara write her book before contract signing and sell it later on to Eco book

Ltd.

Whether Barbara write book before or after signing a contract does not matter, this is so

because still the income earned by Barbara will be from selling of her own personal

written book which she wrote from her own personal skills and knowledge. This in case

even the same case of ‘Brent v FCT (1971) 125 CLR 418’ will be applied and so the

income received by Barbara will term to be the personal exertion income not the capital

gain.

Question 3

In accordance to Australian gift tax, If any financial assistance is being provided by

parents to their daughter or son and they return to their parents back the money. Then

in that case the money received back by parents from son or daughter will be

considered as taxable income in the hands of parents.

Similarly Patrick has rendered a financial assistance help of $52,000 to his sons so that

son can start up his own new business. Later on after five years Patrick son returned

the excess payment to Patrick of $6000 ($58,000- $52,000) would be considered under

taxable income. This is so because the money rendered by Patrick was a loan to his

son not a gift (Pavkovic and Radan, 2016).

However, $52,000 will not be considered under assessable income of Patrick, but the

interest which is being earned by Patrick on $52,000 will be charged under taxable

income at the end of fifth year when he actually receives the full returned value from his

son. Thus, the excess income over $52,000 which the Patrick will get in the form of

interest from his son will be shown under taxable income heading as per the Australian

income tax authority department (Weber, 2014).

because still the income earned by Barbara will be from selling of her own personal

written book which she wrote from her own personal skills and knowledge. This in case

even the same case of ‘Brent v FCT (1971) 125 CLR 418’ will be applied and so the

income received by Barbara will term to be the personal exertion income not the capital

gain.

Question 3

In accordance to Australian gift tax, If any financial assistance is being provided by

parents to their daughter or son and they return to their parents back the money. Then

in that case the money received back by parents from son or daughter will be

considered as taxable income in the hands of parents.

Similarly Patrick has rendered a financial assistance help of $52,000 to his sons so that

son can start up his own new business. Later on after five years Patrick son returned

the excess payment to Patrick of $6000 ($58,000- $52,000) would be considered under

taxable income. This is so because the money rendered by Patrick was a loan to his

son not a gift (Pavkovic and Radan, 2016).

However, $52,000 will not be considered under assessable income of Patrick, but the

interest which is being earned by Patrick on $52,000 will be charged under taxable

income at the end of fifth year when he actually receives the full returned value from his

son. Thus, the excess income over $52,000 which the Patrick will get in the form of

interest from his son will be shown under taxable income heading as per the Australian

income tax authority department (Weber, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the other hand after re-examining the above situation in which Patrick render loan

to his son without signing out any kind of contract nor demanding for any kind of

security and goes for simply verbal foregoing of interest income communication with

son. The in this case the repayment done by Patrick son to Patrick of $52,000 will not

be termed as taxable income for Patrick neither it will attract any kind of gift tax liability.

Whereas, the loan that were repaid by Patrick son after 2 years to Patrick with an

interest of $2400 (S6, 000/5*2) will be treated as taxable income in the hand of Patrick.

Thus, the excess income which is being earned by Patrick would be assessable under

tax after two years when Patrick actually receives the entire value from his son (Hanley,

Shogren and White, 2016).

Thus, in this case the most effective mode of payment will be cheque as it does not

affect upon the accessibility of income liability. Most important of all parties’ intention

matters a lot by the Australian income tax authority. Beside this gift tax liability also may

result in affecting the payment of pension which was received by parents and this would

result in the increment of assessable income of Patrick. Therefore gift tax liability can be

availed by Patrick to $10,000 per month or $30,000 per year whichever is term to be

less. Thus, in case if any payment or gift made exceed the set prescribed limit then it

would term as assessable income part of parent in an assessment year.

to his son without signing out any kind of contract nor demanding for any kind of

security and goes for simply verbal foregoing of interest income communication with

son. The in this case the repayment done by Patrick son to Patrick of $52,000 will not

be termed as taxable income for Patrick neither it will attract any kind of gift tax liability.

Whereas, the loan that were repaid by Patrick son after 2 years to Patrick with an

interest of $2400 (S6, 000/5*2) will be treated as taxable income in the hand of Patrick.

Thus, the excess income which is being earned by Patrick would be assessable under

tax after two years when Patrick actually receives the entire value from his son (Hanley,

Shogren and White, 2016).

Thus, in this case the most effective mode of payment will be cheque as it does not

affect upon the accessibility of income liability. Most important of all parties’ intention

matters a lot by the Australian income tax authority. Beside this gift tax liability also may

result in affecting the payment of pension which was received by parents and this would

result in the increment of assessable income of Patrick. Therefore gift tax liability can be

availed by Patrick to $10,000 per month or $30,000 per year whichever is term to be

less. Thus, in case if any payment or gift made exceed the set prescribed limit then it

would term as assessable income part of parent in an assessment year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report, it can be concluded that the whole project is based on income

from personal exertion, capital gain provisions of income tax and other types of income.

In this report, three questions were covered up and related to Australian Income tax

Law. As in first question, it can be concluded that Helen, who is an assessee, suffer

from capital loss in her first three transactions and in last transaction she earned capital

gain. So, capital loss suffered by Helen were set off to the capital gain and the

remaining loss left were further transferred for next assessment year. In second

question, personal exertion income were discussed on the basis of case scenario

mentioned. Whereas, third question discussed about the Income Tax provisions which

are related to Gift Tax.

From the above report, it can be concluded that the whole project is based on income

from personal exertion, capital gain provisions of income tax and other types of income.

In this report, three questions were covered up and related to Australian Income tax

Law. As in first question, it can be concluded that Helen, who is an assessee, suffer

from capital loss in her first three transactions and in last transaction she earned capital

gain. So, capital loss suffered by Helen were set off to the capital gain and the

remaining loss left were further transferred for next assessment year. In second

question, personal exertion income were discussed on the basis of case scenario

mentioned. Whereas, third question discussed about the Income Tax provisions which

are related to Gift Tax.

REFERENCES

Cooter, R. and Ulen, T., 2016. Law and economics. Addison-Wesley.

Dafflon, B., 2015. The assignment of functions to decentralized government: from

theory to practice. Handbook of multilevel finance, Edward Elgar, Cheltenham, pp.163-

199.

Dietsch, P. and Rixen, T., 2014. Tax competition and global background justice. Journal

of political philosophy, 22(2), pp.150-177.

Filatova, T., 2014. Market-based instruments for flood risk management: a review of

theory, practice and perspectives for climate adaptation policy. Environmental science

& policy, 37, pp.227-242.

Hanley, N., Shogren, J.F. and White, B., 2016. Environmental economics: in theory and

practice. Macmillan International Higher Education.

Paolella, L. and Durand, R., 2016. Category spanning, evaluation, and performance:

Revised theory and test on the corporate law market. Academy of Management

Journal, 59(1), pp.330-351.

Pavkovic, A. and Radan, P., 2016. Creating new states: theory and practice of

secession. Routledge.

Snape, J., 2015. Tax law: Complexity, politics and policymaking. Social & Legal

Studies, 24(2), pp.155-163.

Vatn, A., 2015. Markets in environmental governance. From theory to

practice. Ecological Economics, 117, pp.225-233.

Cooter, R. and Ulen, T., 2016. Law and economics. Addison-Wesley.

Dafflon, B., 2015. The assignment of functions to decentralized government: from

theory to practice. Handbook of multilevel finance, Edward Elgar, Cheltenham, pp.163-

199.

Dietsch, P. and Rixen, T., 2014. Tax competition and global background justice. Journal

of political philosophy, 22(2), pp.150-177.

Filatova, T., 2014. Market-based instruments for flood risk management: a review of

theory, practice and perspectives for climate adaptation policy. Environmental science

& policy, 37, pp.227-242.

Hanley, N., Shogren, J.F. and White, B., 2016. Environmental economics: in theory and

practice. Macmillan International Higher Education.

Paolella, L. and Durand, R., 2016. Category spanning, evaluation, and performance:

Revised theory and test on the corporate law market. Academy of Management

Journal, 59(1), pp.330-351.

Pavkovic, A. and Radan, P., 2016. Creating new states: theory and practice of

secession. Routledge.

Snape, J., 2015. Tax law: Complexity, politics and policymaking. Social & Legal

Studies, 24(2), pp.155-163.

Vatn, A., 2015. Markets in environmental governance. From theory to

practice. Ecological Economics, 117, pp.225-233.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.