Taxation Theory, Practice & Law Report: Capital Gain and FBT Analysis

VerifiedAdded on 2020/12/09

|20

|3032

|421

Report

AI Summary

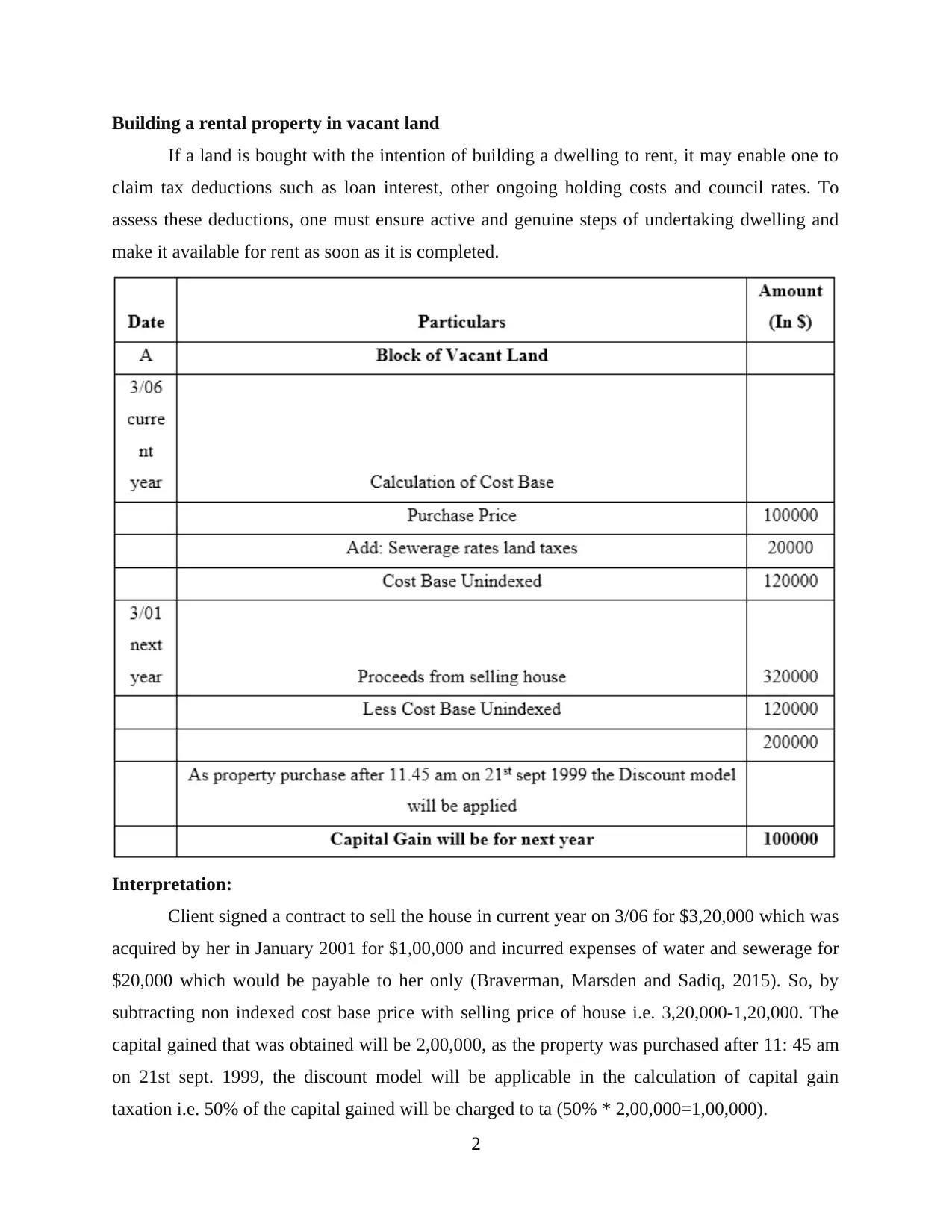

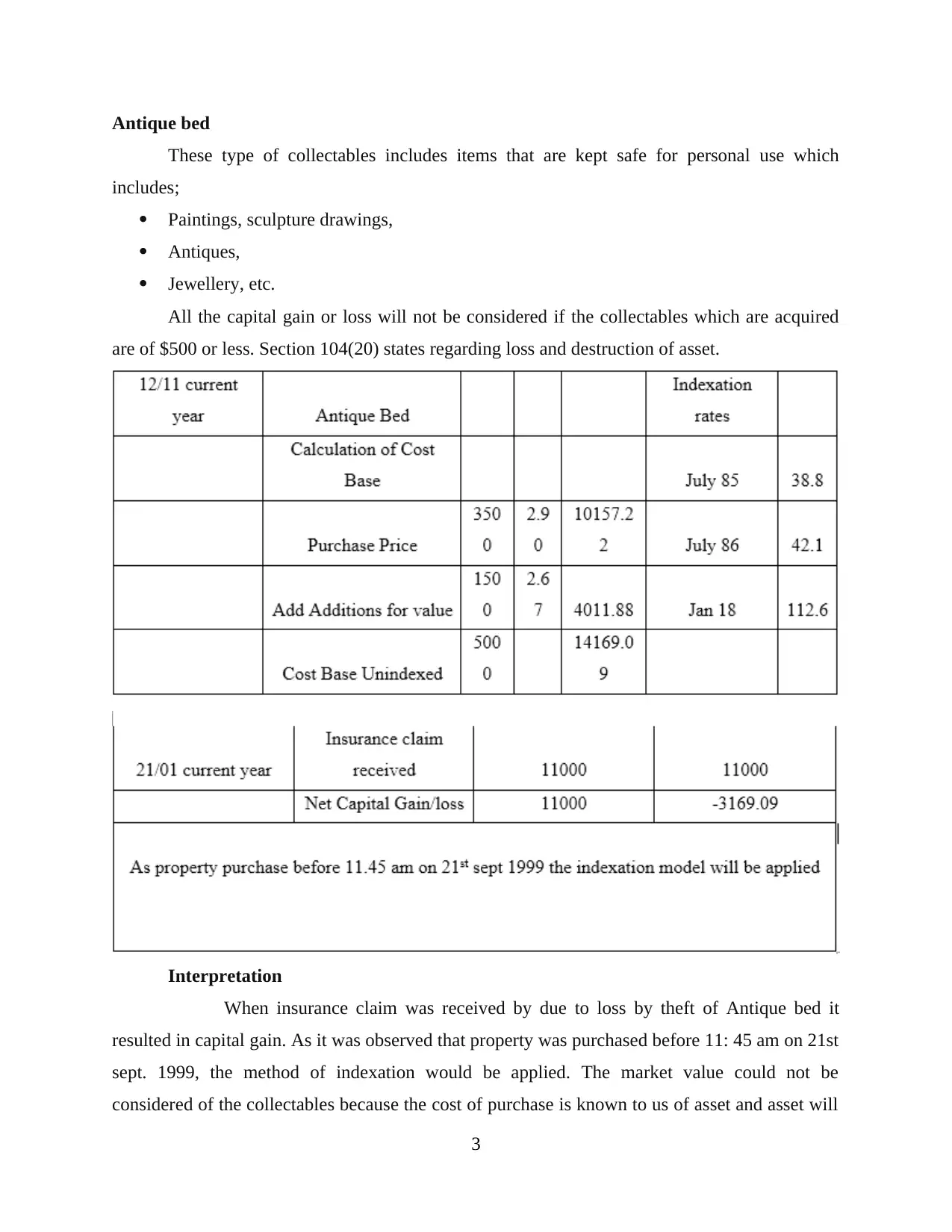

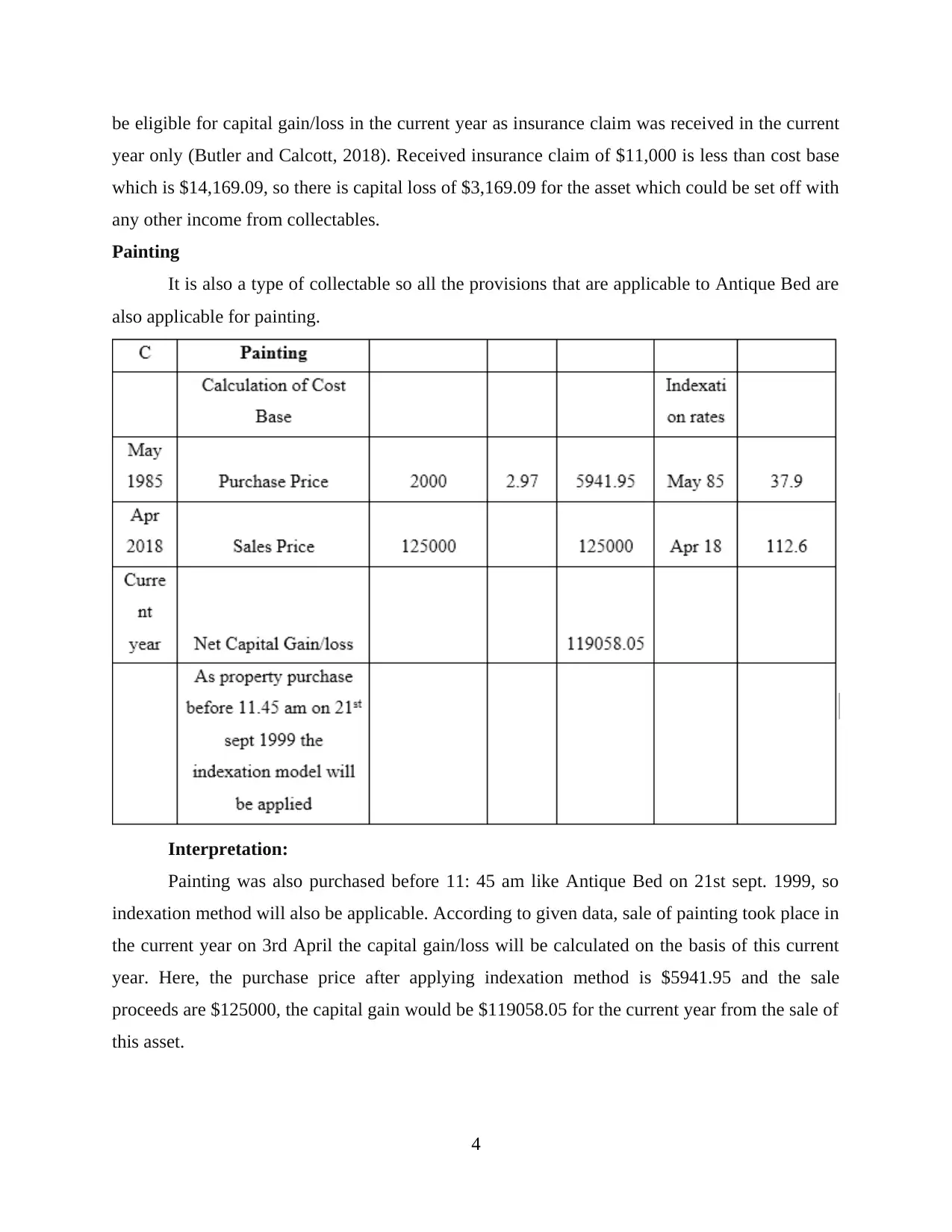

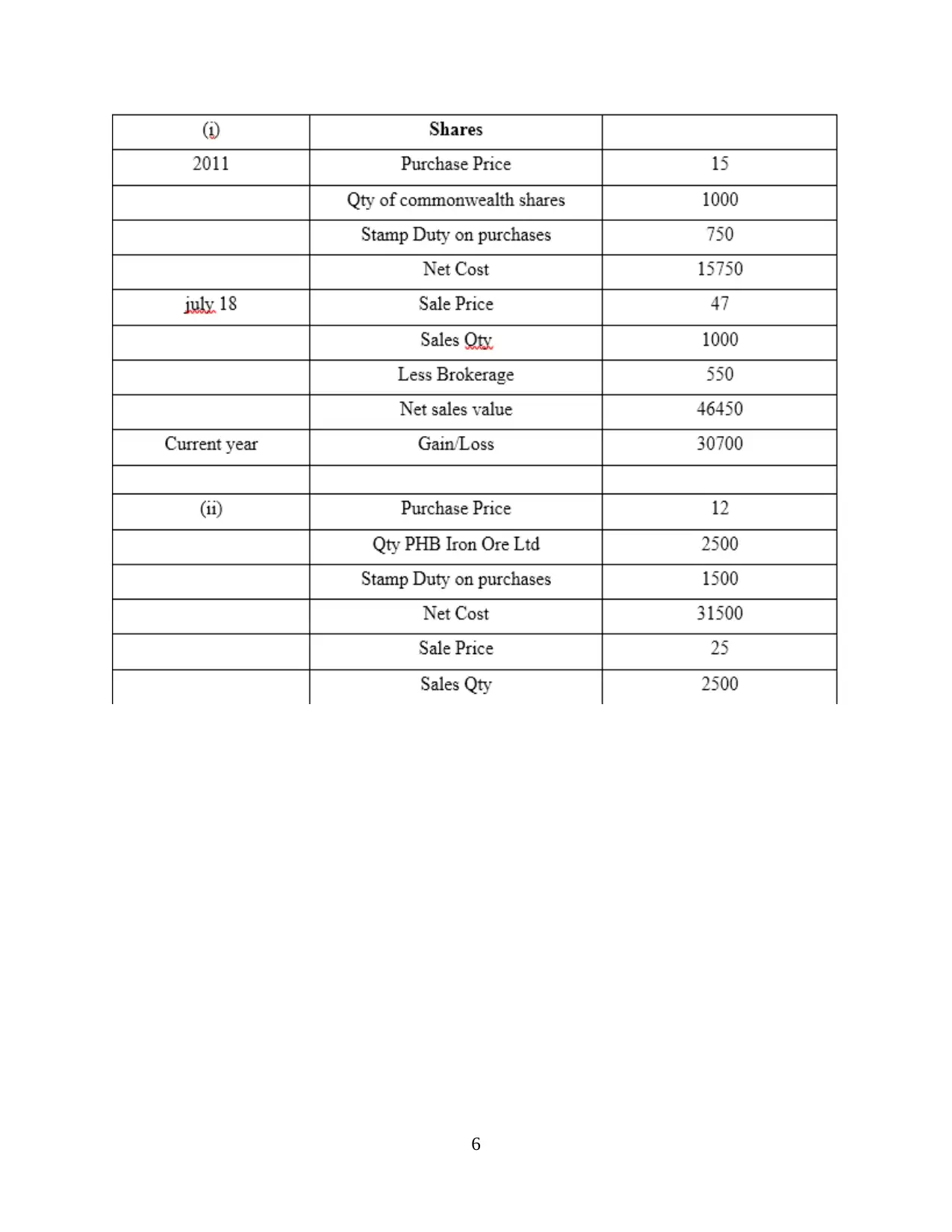

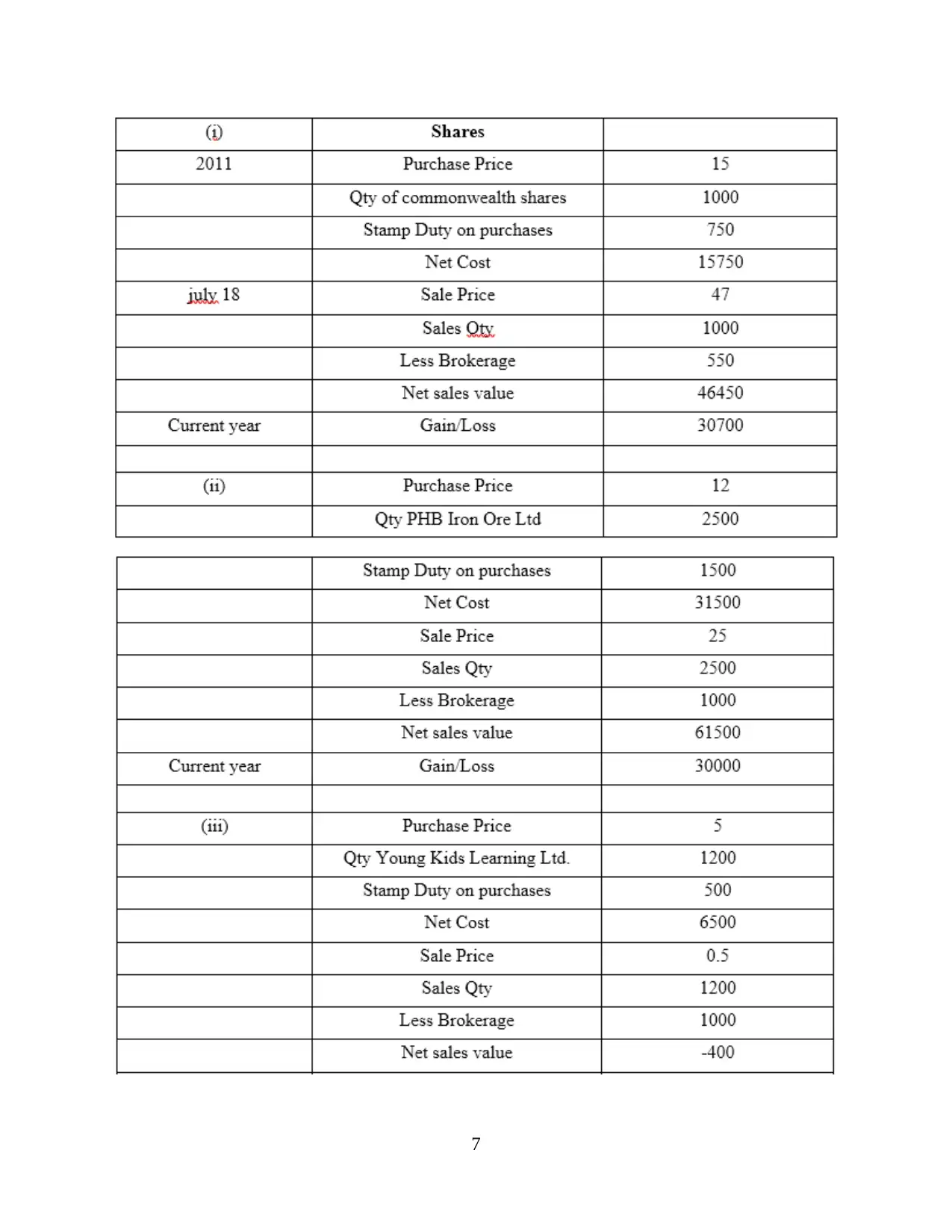

This report provides a detailed analysis of taxation principles, focusing on capital gains tax (CGT) and fringe benefit tax (FBT) within the Australian context. The report addresses specific scenarios involving a client's assets, including a house, antique bed, painting, shares, and a violin, to determine the net capital gain as of June 30, 2018. It also advises on fringe benefit tax implications for assets like a car and a loan, examining different methods for calculating FBT, such as the statutory and cost methods, and analyzing the tax consequences based on how a loan amount is used, including purchasing a holiday house and securities. The report offers legal references and suggestions, adhering to the regulations set by the Federal Registrar of Legislation and the Australian Taxation Office.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.