Taxation Theory Practice and Law

VerifiedAdded on 2023/03/30

|11

|2410

|371

AI Summary

This document provides answers to questions related to taxation theory, practice, and law. It covers topics such as CGT, collectables, personal exertion income, and tax liability. The document includes case studies and explanations to help readers understand the concepts better.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION THEORY PRACTICE AND LAW

Taxation Theory Practice and Law

Name of the Student

Name of the University

Author’s Note

Taxation Theory Practice and Law

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION THEORY PRACTICE AND LAW

Table of Contents

Answer to Question 1.................................................................................................................2

Requirement 1........................................................................................................................2

Requirement 2........................................................................................................................2

Requirement 3........................................................................................................................2

Requirement 4........................................................................................................................3

Answer to Question 2.................................................................................................................4

Answer to Question 3.................................................................................................................6

References..................................................................................................................................9

Table of Contents

Answer to Question 1.................................................................................................................2

Requirement 1........................................................................................................................2

Requirement 2........................................................................................................................2

Requirement 3........................................................................................................................2

Requirement 4........................................................................................................................3

Answer to Question 2.................................................................................................................4

Answer to Question 3.................................................................................................................6

References..................................................................................................................................9

2TAXATION THEORY PRACTICE AND LAW

Answer to Question 1

Requirement 1

Helen did same certain assets in order to fund her business that is set on fashion

designing and the painting that Helen’s father did buy in February 1995 was included in the

sold assets. The cost of painting was $4,000 and Helen did sale it for $12,000. In this

situation, it is noteworthy to mention that CGT needs to be applied on the assets bought after

20.09.1985. Two specific words that are post-CGT and pre-CGT are used in order to classify

the assets that were purchased after or before the above-mentioned date. The painting sold by

Helen needs to be considered as the pre-CGT asset since it was purchased before the date.

Thus, it is needed to ignore the capital gain from the paining and it exempted from CGT date

(Harding 2013).

Requirement 2

As per “s104-10(1), ITAA 1997”, a CGT event A1 regarded as asset disposal. As per

“s108-10(2) and (3)”, a collectable needs to be considered as any item that a taxpayer uses

for the purpose of private enjoyment. Some examples of collectables are postage stamps,

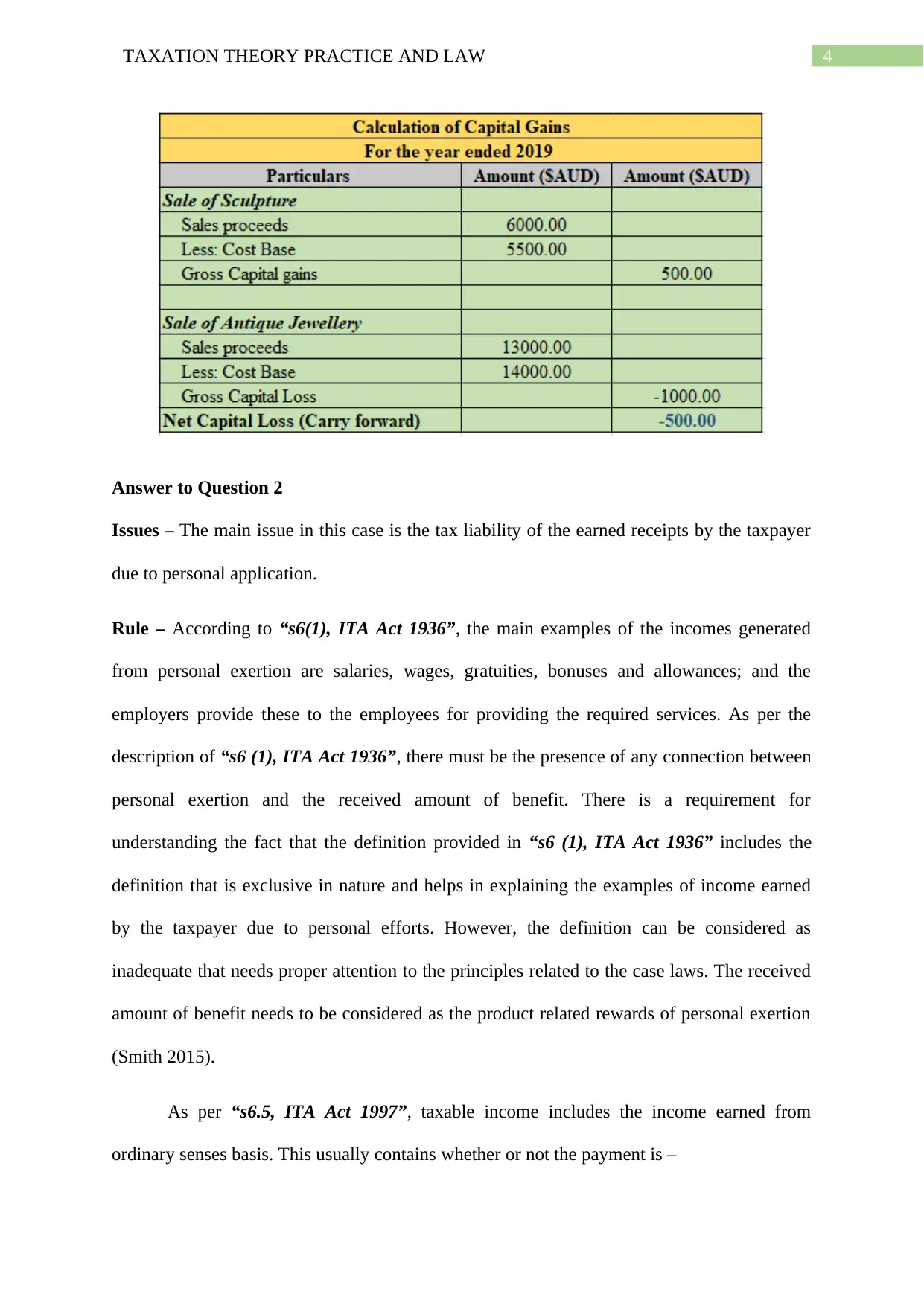

jewellery, antique, rate folio and artwork. As per the case, Helen did sales the sculpture

purchased for $5,500 in 1993 in order to fund her business and it was sold in 2018 for $6,000.

As per “s104-10(1), ITAA 1997”, there was an occurrence of CGT event A1 due to the

disposal of the sculpture since it was required to consider the sculpture as a collectable in

accordance with “s108-10(2)”. Thus, the statutory income that Helen earned from the

disposal of the collectable is subject to taxation and will be considered as Helen’s taxable

earnings’ part (Burkhauser, Hahn and Wilkins 2015).

Answer to Question 1

Requirement 1

Helen did same certain assets in order to fund her business that is set on fashion

designing and the painting that Helen’s father did buy in February 1995 was included in the

sold assets. The cost of painting was $4,000 and Helen did sale it for $12,000. In this

situation, it is noteworthy to mention that CGT needs to be applied on the assets bought after

20.09.1985. Two specific words that are post-CGT and pre-CGT are used in order to classify

the assets that were purchased after or before the above-mentioned date. The painting sold by

Helen needs to be considered as the pre-CGT asset since it was purchased before the date.

Thus, it is needed to ignore the capital gain from the paining and it exempted from CGT date

(Harding 2013).

Requirement 2

As per “s104-10(1), ITAA 1997”, a CGT event A1 regarded as asset disposal. As per

“s108-10(2) and (3)”, a collectable needs to be considered as any item that a taxpayer uses

for the purpose of private enjoyment. Some examples of collectables are postage stamps,

jewellery, antique, rate folio and artwork. As per the case, Helen did sales the sculpture

purchased for $5,500 in 1993 in order to fund her business and it was sold in 2018 for $6,000.

As per “s104-10(1), ITAA 1997”, there was an occurrence of CGT event A1 due to the

disposal of the sculpture since it was required to consider the sculpture as a collectable in

accordance with “s108-10(2)”. Thus, the statutory income that Helen earned from the

disposal of the collectable is subject to taxation and will be considered as Helen’s taxable

earnings’ part (Burkhauser, Hahn and Wilkins 2015).

3TAXATION THEORY PRACTICE AND LAW

Requirement 3

According to “s108-10(1), ITA Act 1997”, collectable related capital losses can only

be allowed to offset against the capital gains together with the collectable related future gains.

The fact can be seen from the provided scenario of Helen that Helen did purchases a piece of

antique jewellery in the year 1987 for $14,000 since it was the cost price. Helen did sale this

antique jewellery for $13,000 in the presence of a loss of $13,000. As per “s108-10(2)”, the

antique needs to be classified as collectable (Daley and Wood 2015). In accordance with

“s108-10(1), ITA Act 1997”, Helen suffered from capital losses due to the sale of the

collectable and this loss can only be offset against the collectable related capital gains. Thus,

Helen has the option of offsetting the sculpture related capital gain against the jewels related

loss because both these two assets as collectable (Chardon, Freudenberg and Brimble 2016).

Requirement 4

Helen did sale the picture for funding her business. Helen received $5,000 by selling

the picture which has the cost base of $470. As per “Subdivision 108-c”, assets for personal

use are non-collectable in nature since they are used for personal use. As per “s118-10(3)”, it

is needed to neglect any capital gain from collectables the personal use asset was bought for

$10,000 or less. It can be said based on the ruling that the picture was kept for Helen’s

mother’s own personal use. Thus, as per “s118-10(3)”, since the picture’s cost was less than

$10,000, the capital from the sale of the picture needs to be neglected (Wilkins 2015).

Requirement 3

According to “s108-10(1), ITA Act 1997”, collectable related capital losses can only

be allowed to offset against the capital gains together with the collectable related future gains.

The fact can be seen from the provided scenario of Helen that Helen did purchases a piece of

antique jewellery in the year 1987 for $14,000 since it was the cost price. Helen did sale this

antique jewellery for $13,000 in the presence of a loss of $13,000. As per “s108-10(2)”, the

antique needs to be classified as collectable (Daley and Wood 2015). In accordance with

“s108-10(1), ITA Act 1997”, Helen suffered from capital losses due to the sale of the

collectable and this loss can only be offset against the collectable related capital gains. Thus,

Helen has the option of offsetting the sculpture related capital gain against the jewels related

loss because both these two assets as collectable (Chardon, Freudenberg and Brimble 2016).

Requirement 4

Helen did sale the picture for funding her business. Helen received $5,000 by selling

the picture which has the cost base of $470. As per “Subdivision 108-c”, assets for personal

use are non-collectable in nature since they are used for personal use. As per “s118-10(3)”, it

is needed to neglect any capital gain from collectables the personal use asset was bought for

$10,000 or less. It can be said based on the ruling that the picture was kept for Helen’s

mother’s own personal use. Thus, as per “s118-10(3)”, since the picture’s cost was less than

$10,000, the capital from the sale of the picture needs to be neglected (Wilkins 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION THEORY PRACTICE AND LAW

Answer to Question 2

Issues – The main issue in this case is the tax liability of the earned receipts by the taxpayer

due to personal application.

Rule – According to “s6(1), ITA Act 1936”, the main examples of the incomes generated

from personal exertion are salaries, wages, gratuities, bonuses and allowances; and the

employers provide these to the employees for providing the required services. As per the

description of “s6 (1), ITA Act 1936”, there must be the presence of any connection between

personal exertion and the received amount of benefit. There is a requirement for

understanding the fact that the definition provided in “s6 (1), ITA Act 1936” includes the

definition that is exclusive in nature and helps in explaining the examples of income earned

by the taxpayer due to personal efforts. However, the definition can be considered as

inadequate that needs proper attention to the principles related to the case laws. The received

amount of benefit needs to be considered as the product related rewards of personal exertion

(Smith 2015).

As per “s6.5, ITA Act 1997”, taxable income includes the income earned from

ordinary senses basis. This usually contains whether or not the payment is –

Answer to Question 2

Issues – The main issue in this case is the tax liability of the earned receipts by the taxpayer

due to personal application.

Rule – According to “s6(1), ITA Act 1936”, the main examples of the incomes generated

from personal exertion are salaries, wages, gratuities, bonuses and allowances; and the

employers provide these to the employees for providing the required services. As per the

description of “s6 (1), ITA Act 1936”, there must be the presence of any connection between

personal exertion and the received amount of benefit. There is a requirement for

understanding the fact that the definition provided in “s6 (1), ITA Act 1936” includes the

definition that is exclusive in nature and helps in explaining the examples of income earned

by the taxpayer due to personal efforts. However, the definition can be considered as

inadequate that needs proper attention to the principles related to the case laws. The received

amount of benefit needs to be considered as the product related rewards of personal exertion

(Smith 2015).

As per “s6.5, ITA Act 1997”, taxable income includes the income earned from

ordinary senses basis. This usually contains whether or not the payment is –

5TAXATION THEORY PRACTICE AND LAW

i. Part of the regular payment receipts

ii. A prize related to the personal service

iii. Services provided in order to receive payment (Richardson 2014)

In the decision of whether a particular receipt needs to be considered as income, the lack

or presence of any solitary indicator is not considered as a decisive factor. The judgment

provided in the case of “Brent v FCT (1971)” is required to consider as the mean to support

the payment as an income. In this case, the federal court considered the payment as income

where the payment was provided to the robber’s wife for telling her life story for the purpose

of publication. The court considered the payment as income because of the presence of

charter or ordinary earrings in accordance with “s6-5, ITA Act 1997”.

The case of “Hobbs v Hussey (1942)” can also be considered where the payment for

service was regarded as income. As per the case, £1,500 was provided to the taxpayer to

assign the regarding his autobiography printed in the newspaper and it was considered as

assessable income.

Another case can be presented in here that is “Houden v Marshall (1958)” where the

taxpayer was agreed to share his experience as a jockey while including photographs and

newspaper cuttings. The received amount of him was considered as income from the personal

exertion and thus, was considered as taxable income in accordance with “s6-5, ITAA 1997”

(Bray 2015).

Application – The above-discussed rules are applicable in this scenario of Barbara who is a

research in economics. As per the scenario, Barbara was approached by a publisher named

Eco Book Ltd for writing a book. She decided to write the book named “Principles of

Economics” since the offer was attractive. Eco Book Ltd made a payment of $13,000 to

Barbara after the successful completion of writing the book and as per “s6 (1), ITAA 1936”,

i. Part of the regular payment receipts

ii. A prize related to the personal service

iii. Services provided in order to receive payment (Richardson 2014)

In the decision of whether a particular receipt needs to be considered as income, the lack

or presence of any solitary indicator is not considered as a decisive factor. The judgment

provided in the case of “Brent v FCT (1971)” is required to consider as the mean to support

the payment as an income. In this case, the federal court considered the payment as income

where the payment was provided to the robber’s wife for telling her life story for the purpose

of publication. The court considered the payment as income because of the presence of

charter or ordinary earrings in accordance with “s6-5, ITA Act 1997”.

The case of “Hobbs v Hussey (1942)” can also be considered where the payment for

service was regarded as income. As per the case, £1,500 was provided to the taxpayer to

assign the regarding his autobiography printed in the newspaper and it was considered as

assessable income.

Another case can be presented in here that is “Houden v Marshall (1958)” where the

taxpayer was agreed to share his experience as a jockey while including photographs and

newspaper cuttings. The received amount of him was considered as income from the personal

exertion and thus, was considered as taxable income in accordance with “s6-5, ITAA 1997”

(Bray 2015).

Application – The above-discussed rules are applicable in this scenario of Barbara who is a

research in economics. As per the scenario, Barbara was approached by a publisher named

Eco Book Ltd for writing a book. She decided to write the book named “Principles of

Economics” since the offer was attractive. Eco Book Ltd made a payment of $13,000 to

Barbara after the successful completion of writing the book and as per “s6 (1), ITAA 1936”,

6TAXATION THEORY PRACTICE AND LAW

it is needed to consider this whole amount as income derived from personal effort. It needs to

be mentioned that the payment made to Barbara has adequate connection with the received

amount and personal exertion. As per the court judgement in the case of “Brent v FCT

(1971)”, the received amount is considered as the reward of the personal effort. The payment

was regarded as income since it has the ordinary earnings’ characteristics and subject to

taxation in accordance with “s6-5, ITA Act 1997”

In addition, Eco Books Ltd also acquired the copyright of the book from Barbara for

$13,400. Same as the condition in “Hobbs v Hussey (1942)”, Barbara receives the payment

for providing service which is subject to taxation as per “s6-5, ITA Act 1997”. In order to

provide service, it was needed for Barbara to write the book for providing service and thus,

receiving the payment for assigning the book’s copyright was income from personal exertion

(Luxford 2014).

It needs to be mentioned that Barbara also did sell the manuscripts and manuscript of

the interview; and thus, she receives sums of $4,350 and $3,200 respectively. Same as the

condition in “Houden v Marshall (1958)”, there is a need to treat the amount that Barbara

received as income from personal efforts and thus, it is subject to taxation in accordance with

“s6-5, ITAA 1997” (Cox and Harg 2018).

By taking into consideration the above discussion, in case it was the case that Barbara

wrote the book in her leisure time and she was selling the book copyright for the purposes of

printing and publication, then the requirement was to consider the amount received by her as

the income from personal exertion. Thus, in accordance with “s6-5, ITA Act 1997”, this

income from personal exertion would be considered as taxable.

it is needed to consider this whole amount as income derived from personal effort. It needs to

be mentioned that the payment made to Barbara has adequate connection with the received

amount and personal exertion. As per the court judgement in the case of “Brent v FCT

(1971)”, the received amount is considered as the reward of the personal effort. The payment

was regarded as income since it has the ordinary earnings’ characteristics and subject to

taxation in accordance with “s6-5, ITA Act 1997”

In addition, Eco Books Ltd also acquired the copyright of the book from Barbara for

$13,400. Same as the condition in “Hobbs v Hussey (1942)”, Barbara receives the payment

for providing service which is subject to taxation as per “s6-5, ITA Act 1997”. In order to

provide service, it was needed for Barbara to write the book for providing service and thus,

receiving the payment for assigning the book’s copyright was income from personal exertion

(Luxford 2014).

It needs to be mentioned that Barbara also did sell the manuscripts and manuscript of

the interview; and thus, she receives sums of $4,350 and $3,200 respectively. Same as the

condition in “Houden v Marshall (1958)”, there is a need to treat the amount that Barbara

received as income from personal efforts and thus, it is subject to taxation in accordance with

“s6-5, ITAA 1997” (Cox and Harg 2018).

By taking into consideration the above discussion, in case it was the case that Barbara

wrote the book in her leisure time and she was selling the book copyright for the purposes of

printing and publication, then the requirement was to consider the amount received by her as

the income from personal exertion. Thus, in accordance with “s6-5, ITA Act 1997”, this

income from personal exertion would be considered as taxable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION THEORY PRACTICE AND LAW

Conclusion – On the basis of the above discussion, it can be said that the characteristic of the

payments received by Barbara from the writing of the book makes this income subject to

taxation in accordance with the ruling of “s6-5, ITA Act 1997”.

Answer to Question 3

Issue – In this particular case, the main fundamental issue can be seen in relation to tax

liability of interest earned by the taxpayer from interest on loan from giving loan.

Rule – The main component of the taxable income of the taxpayer is the income on the basis

of ordinary meanings and the statutory earnings. Ordinary earnings are considered as income

the receipts are determined by the courts through the implementation of the definition of

earnings regarding the ordinary concepts. Statutory earnings are considered as the income

that needs to be specified as taxable income regarding different types of provisions in the act

of assessing taxation named the net capital gains (Daley, McGannon and Hunter 2014).

The statutory earnings provision is needed to be taken into consideration before

applying the ordinary earnings and this considered as the amount that can be subject to

taxation as per “s6-25(2), ITA Act 1997”. The gains can be described from the most

fundamental aspects to impose income tax rule and regulations. It is needed to take into

consideration that receipts will not be considered as ordinary income unless it satisfies both

the perquisites. The main component of the perquisites of the ordinary income is cash or

aspect that can be easily converted into cash and it is considered as the taxpayer’s real gain. It

is needed to be mentioned that the court decision in “Mayes v Hochstrasser (1980)” stated

that the receipts need to be actual gain and it needs to be held as the ordinary earnings

(Delpachitra and Lester 2013).

In case the nature of a gain is periodic or regular, then it can be said that there is

characteristics of ordinary earnings in it as compared to the receipts that the taxpayer earned

Conclusion – On the basis of the above discussion, it can be said that the characteristic of the

payments received by Barbara from the writing of the book makes this income subject to

taxation in accordance with the ruling of “s6-5, ITA Act 1997”.

Answer to Question 3

Issue – In this particular case, the main fundamental issue can be seen in relation to tax

liability of interest earned by the taxpayer from interest on loan from giving loan.

Rule – The main component of the taxable income of the taxpayer is the income on the basis

of ordinary meanings and the statutory earnings. Ordinary earnings are considered as income

the receipts are determined by the courts through the implementation of the definition of

earnings regarding the ordinary concepts. Statutory earnings are considered as the income

that needs to be specified as taxable income regarding different types of provisions in the act

of assessing taxation named the net capital gains (Daley, McGannon and Hunter 2014).

The statutory earnings provision is needed to be taken into consideration before

applying the ordinary earnings and this considered as the amount that can be subject to

taxation as per “s6-25(2), ITA Act 1997”. The gains can be described from the most

fundamental aspects to impose income tax rule and regulations. It is needed to take into

consideration that receipts will not be considered as ordinary income unless it satisfies both

the perquisites. The main component of the perquisites of the ordinary income is cash or

aspect that can be easily converted into cash and it is considered as the taxpayer’s real gain. It

is needed to be mentioned that the court decision in “Mayes v Hochstrasser (1980)” stated

that the receipts need to be actual gain and it needs to be held as the ordinary earnings

(Delpachitra and Lester 2013).

In case the nature of a gain is periodic or regular, then it can be said that there is

characteristics of ordinary earnings in it as compared to the receipts that the taxpayer earned

8TAXATION THEORY PRACTICE AND LAW

as a huge amount. It is noteworthy to mention the fact in this case that the large amount of

gains need to be treated as the ordinary income. The one off receipts interests can be included

in this under the agreement of loan and this needs to be considered as a gain (Greenville,

Pobke and Rogers 2013).

Application – On the basis of the above discussion, the above cases are referred in this

situation of Patrick where he made a payment worth $52,000 to his son David and the term

was that David needed to repay the sum at the end of five years. $58,000 was the repayment

amount which includes interest on the loan of $6,000. It can be seen in this case that David

made the repayment of the sum to Patrick within a period of two years where 5% interest was

included on the basis of the amount borrowed (Chester 2013).

It needs to be mentioned that the sum received by Patrick needs to be considered as an

income in the presence of both the income related perquisites like real gain and cash

convertible. By referring to the judgment of the commissioner in the case of “Mayes v

Hochstrasser (1980)”, it can be said that the receipt is an actual gain for Patrick and this

needs to be take into consideration for Patrick’s statutory income in accordance with “s6-

25(2), ITAA 1997”. This amount is needed to be considered as the loan’s one off received

interest and thus, it is needed to include the interest in Patrick’s assessable income as

statutory earnings (Mays, Marston and Tomlinson 2016).

Conclusion – It can be said on the basis of the above discussion that the money received by

Patrick as the interest on loan should be treated as the assessable statutory income because of

the fact that this amount creates real gain.

as a huge amount. It is noteworthy to mention the fact in this case that the large amount of

gains need to be treated as the ordinary income. The one off receipts interests can be included

in this under the agreement of loan and this needs to be considered as a gain (Greenville,

Pobke and Rogers 2013).

Application – On the basis of the above discussion, the above cases are referred in this

situation of Patrick where he made a payment worth $52,000 to his son David and the term

was that David needed to repay the sum at the end of five years. $58,000 was the repayment

amount which includes interest on the loan of $6,000. It can be seen in this case that David

made the repayment of the sum to Patrick within a period of two years where 5% interest was

included on the basis of the amount borrowed (Chester 2013).

It needs to be mentioned that the sum received by Patrick needs to be considered as an

income in the presence of both the income related perquisites like real gain and cash

convertible. By referring to the judgment of the commissioner in the case of “Mayes v

Hochstrasser (1980)”, it can be said that the receipt is an actual gain for Patrick and this

needs to be take into consideration for Patrick’s statutory income in accordance with “s6-

25(2), ITAA 1997”. This amount is needed to be considered as the loan’s one off received

interest and thus, it is needed to include the interest in Patrick’s assessable income as

statutory earnings (Mays, Marston and Tomlinson 2016).

Conclusion – It can be said on the basis of the above discussion that the money received by

Patrick as the interest on loan should be treated as the assessable statutory income because of

the fact that this amount creates real gain.

9TAXATION THEORY PRACTICE AND LAW

References

Bray, J.R., 2015. 100 Years of the Minimum Wage and the Australian Tax and Transfer

System: What Has Happened, What Have We Learnt and What Are the Challenges. Austl.

Tax F., 30, p.819.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Chester, L., 2013. The impacts and consequences for low-income Australian households of

rising energy prices. University of Sydney, Sydney.

Cox, M. and Harg, R., 2018. The ethics of settlement negotiations in employment

disputes. Brief, 45(11), p.28.

Daley, J. and Wood, D., 2015. Fiscal challenges for Australia. Grattan Institute.

Daley, J., McGannon, C. and Hunter, A., 2014. Budget pressures on Australian governments

2014. Grattan Institute.

Delpachitra, S. and Lester, L., 2013. Non‐Interest Income: Are Australian Banks Moving

Away from their Traditional Businesses?. Economic Papers: A journal of applied economics

and policy, 32(2), pp.190-199.

Greenville, J., Pobke, C. and Rogers, N., 2013. Trends in the Distribution of Income in

Australia. Canberra: Productivity Commission.

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

References

Bray, J.R., 2015. 100 Years of the Minimum Wage and the Australian Tax and Transfer

System: What Has Happened, What Have We Learnt and What Are the Challenges. Austl.

Tax F., 30, p.819.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Chester, L., 2013. The impacts and consequences for low-income Australian households of

rising energy prices. University of Sydney, Sydney.

Cox, M. and Harg, R., 2018. The ethics of settlement negotiations in employment

disputes. Brief, 45(11), p.28.

Daley, J. and Wood, D., 2015. Fiscal challenges for Australia. Grattan Institute.

Daley, J., McGannon, C. and Hunter, A., 2014. Budget pressures on Australian governments

2014. Grattan Institute.

Delpachitra, S. and Lester, L., 2013. Non‐Interest Income: Are Australian Banks Moving

Away from their Traditional Businesses?. Economic Papers: A journal of applied economics

and policy, 32(2), pp.190-199.

Greenville, J., Pobke, C. and Rogers, N., 2013. Trends in the Distribution of Income in

Australia. Canberra: Productivity Commission.

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION THEORY PRACTICE AND LAW

Luxford, S.L., 2014. The history and development of the choice principle.

Mays, J., Marston, G. and Tomlinson, J. eds., 2016. Basic income in Australia and New

Zealand: perspectives from the neoliberal frontier. Springer.

Richardson, D., 2014. The taxation of capital in Australia: Should it be lower?.

In Challenging the Orthodoxy (pp. 181-199). Springer, Berlin, Heidelberg.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30, p.679.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

Luxford, S.L., 2014. The history and development of the choice principle.

Mays, J., Marston, G. and Tomlinson, J. eds., 2016. Basic income in Australia and New

Zealand: perspectives from the neoliberal frontier. Springer.

Richardson, D., 2014. The taxation of capital in Australia: Should it be lower?.

In Challenging the Orthodoxy (pp. 181-199). Springer, Berlin, Heidelberg.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30, p.679.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.