HI6028 Taxation Theory, Practice & Law Assignment: T1 2019, Holmes

VerifiedAdded on 2022/11/16

|10

|3348

|183

Homework Assignment

AI Summary

This assignment explores the Australian taxation system, covering income tax, capital gains tax (CGT), fringe benefits tax (FBT), and Goods and Services Tax (GST). It delves into the concepts of income and deductions, examining the progressive income tax rates for residents and non-residents, as well as the impact of withholding taxes. The assignment further analyzes CGT, including its historical development and the current discount rates for assets held over a year. It also discusses FBT, including the types of benefits subject to taxation and relevant tax rates. Furthermore, the assignment examines the GST general anti-avoidance provision (Part IVA) and the challenges in interpreting and applying it. Finally, the assignment highlights key taxation issues, such as the impact of technology and globalization on tax collection, and the importance of tax reforms in Australia. The paper also provides an overview of the relevant taxation legislations and case laws.

Taxation theory, practice in Law 1

TAXATION THEORY, PRACTICE IN LAW.

Student Name

Professors Name

University

City/State

Date

TAXATION THEORY, PRACTICE IN LAW.

Student Name

Professors Name

University

City/State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation theory, practice in Law 2

Taxation theory, practice and law

Introduction

Taxable incomes in Australia are assessed on the basis of personal incomes

during a given period and allowable deductions by the federal government. Individual

incomes are assessed on three basis as; Personal income which is mainly composed of

people salaries and wages, business income which is that source of income derived

from people owned businesses and capital gain which is a rise in value of assets. Our

discussion will focus on concept of this income taxes, concept of income and deduction,

capital gain taxes, fringe benefit taxes and GST general anti avoidance provision and

income tax administration

Australia income tax system.

The main statute underlying income tax in Australia is income tax assessment

act 1997. Income tax is levied on a progressive basis meaning that the higher the

income the higher the tax paid. Australian income tax is imposed on citizens and

companies taxable income by the federal government. Paying taxes is important to

Australia (Body, 2015, p.900) since it contributes to revenue. Though imposed by the

federal government, this form of tax is collected and administered by the Australian

taxation office. Income tax is administered under progressive rate of between 0-45%

including a Medicare levy of 2% different from corporations tax which is between 27.5%-

30%(ACOSS, 2011, pp.345-347) depending on turnover generated annually while taxes

on capital gains are only effected if a gain is realized on capital assets attracting 50%

allowance if the asset was held for more than one year. It is also important to note

taxations on partnerships and trusts which is not administered directly but through

beneficiary and tax distribution to partners.

Concept of income and deduction

As discussed previously, income tax is levied on progressive basis for personal

taxes. In Australia, there are resident individual and non-resident individual tax payers

having different rates of tax payment for example most Australia citizens are liable to

pay Medicare of 2% standard rate on taxable income, a levy that is not imposed on non-

resident individual tax payers. Existence of withholding taxes has helped employees in

several instance due to refunds that such taxes bear. It is an obligation therefore for an

employer to withhold tax from wages and salaries of an employee after provision of tax

file number. In case where this number is not available then a requirement is imposed

on taxpayers to deduct 47%(ACOSS,2011, pp.345-347). Interest earned from financial

institutions that is due to individuals is also subject to the highest marginal rate of

income tax in the absence of tax file number. Likewise, failure to provide this number by

businesses to financial institution for tax levy, they should provide an Australian

business number otherwise the highest rate of income tax will be withheld.

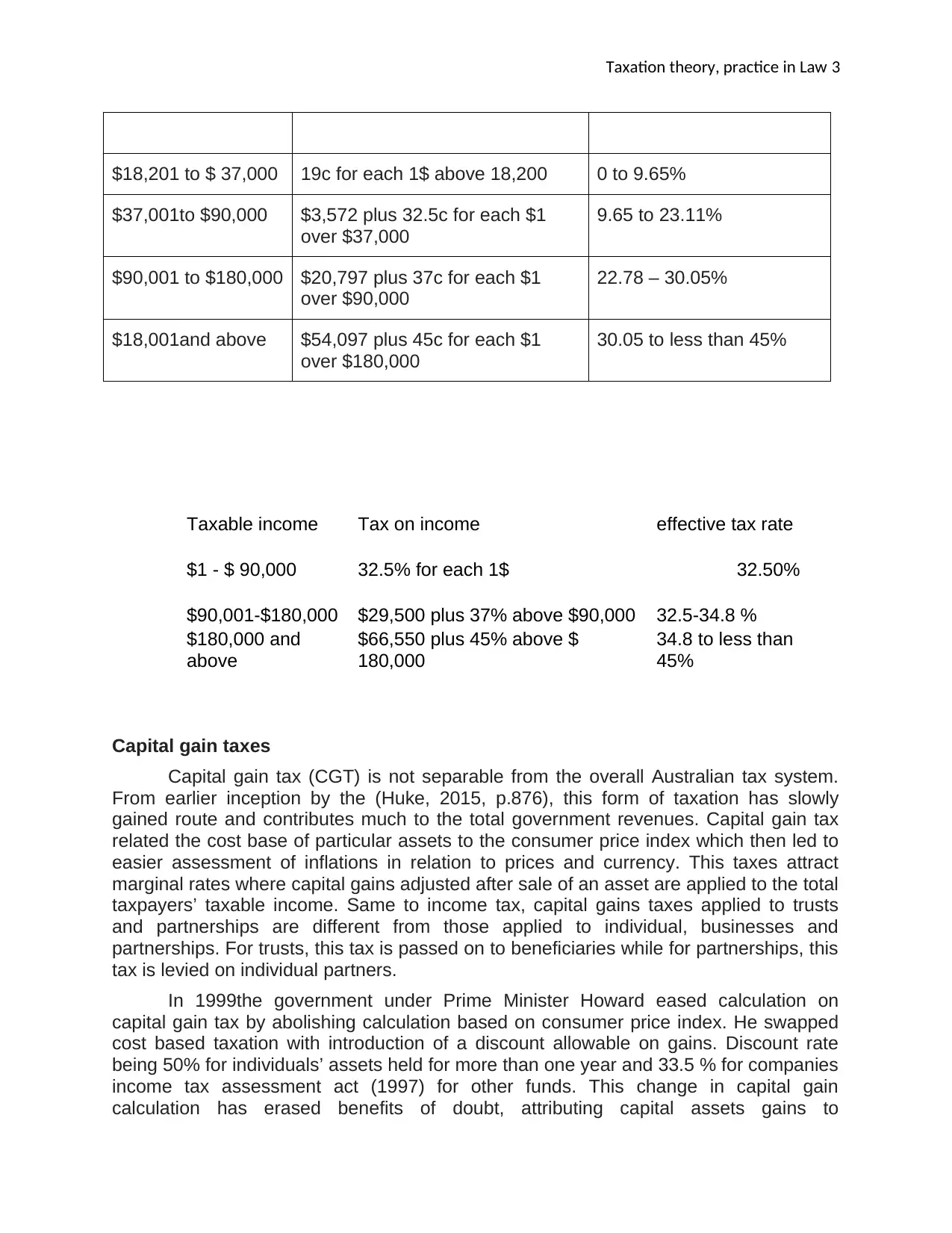

The tables below illustrates income tax rates for Australians residents and not residents

respectively (income tax Act 1997)

Taxable income Tax on this potion of income Effective tax rate

$1 to $18,200 Nil 0

Taxation theory, practice and law

Introduction

Taxable incomes in Australia are assessed on the basis of personal incomes

during a given period and allowable deductions by the federal government. Individual

incomes are assessed on three basis as; Personal income which is mainly composed of

people salaries and wages, business income which is that source of income derived

from people owned businesses and capital gain which is a rise in value of assets. Our

discussion will focus on concept of this income taxes, concept of income and deduction,

capital gain taxes, fringe benefit taxes and GST general anti avoidance provision and

income tax administration

Australia income tax system.

The main statute underlying income tax in Australia is income tax assessment

act 1997. Income tax is levied on a progressive basis meaning that the higher the

income the higher the tax paid. Australian income tax is imposed on citizens and

companies taxable income by the federal government. Paying taxes is important to

Australia (Body, 2015, p.900) since it contributes to revenue. Though imposed by the

federal government, this form of tax is collected and administered by the Australian

taxation office. Income tax is administered under progressive rate of between 0-45%

including a Medicare levy of 2% different from corporations tax which is between 27.5%-

30%(ACOSS, 2011, pp.345-347) depending on turnover generated annually while taxes

on capital gains are only effected if a gain is realized on capital assets attracting 50%

allowance if the asset was held for more than one year. It is also important to note

taxations on partnerships and trusts which is not administered directly but through

beneficiary and tax distribution to partners.

Concept of income and deduction

As discussed previously, income tax is levied on progressive basis for personal

taxes. In Australia, there are resident individual and non-resident individual tax payers

having different rates of tax payment for example most Australia citizens are liable to

pay Medicare of 2% standard rate on taxable income, a levy that is not imposed on non-

resident individual tax payers. Existence of withholding taxes has helped employees in

several instance due to refunds that such taxes bear. It is an obligation therefore for an

employer to withhold tax from wages and salaries of an employee after provision of tax

file number. In case where this number is not available then a requirement is imposed

on taxpayers to deduct 47%(ACOSS,2011, pp.345-347). Interest earned from financial

institutions that is due to individuals is also subject to the highest marginal rate of

income tax in the absence of tax file number. Likewise, failure to provide this number by

businesses to financial institution for tax levy, they should provide an Australian

business number otherwise the highest rate of income tax will be withheld.

The tables below illustrates income tax rates for Australians residents and not residents

respectively (income tax Act 1997)

Taxable income Tax on this potion of income Effective tax rate

$1 to $18,200 Nil 0

Taxation theory, practice in Law 3

$18,201 to $ 37,000 19c for each 1$ above 18,200 0 to 9.65%

$37,001to $90,000 $3,572 plus 32.5c for each $1

over $37,000

9.65 to 23.11%

$90,001 to $180,000 $20,797 plus 37c for each $1

over $90,000

22.78 – 30.05%

$18,001and above $54,097 plus 45c for each $1

over $180,000

30.05 to less than 45%

Taxable income Tax on income effective tax rate

$1 - $ 90,000 32.5% for each 1$ 32.50%

$90,001-$180,000 $29,500 plus 37% above $90,000 32.5-34.8 %

$180,000 and

above

$66,550 plus 45% above $

180,000

34.8 to less than

45%

Capital gain taxes

Capital gain tax (CGT) is not separable from the overall Australian tax system.

From earlier inception by the (Huke, 2015, p.876), this form of taxation has slowly

gained route and contributes much to the total government revenues. Capital gain tax

related the cost base of particular assets to the consumer price index which then led to

easier assessment of inflations in relation to prices and currency. This taxes attract

marginal rates where capital gains adjusted after sale of an asset are applied to the total

taxpayers’ taxable income. Same to income tax, capital gains taxes applied to trusts

and partnerships are different from those applied to individual, businesses and

partnerships. For trusts, this tax is passed on to beneficiaries while for partnerships, this

tax is levied on individual partners.

In 1999the government under Prime Minister Howard eased calculation on

capital gain tax by abolishing calculation based on consumer price index. He swapped

cost based taxation with introduction of a discount allowable on gains. Discount rate

being 50% for individuals’ assets held for more than one year and 33.5 % for companies

income tax assessment act (1997) for other funds. This change in capital gain

calculation has erased benefits of doubt, attributing capital assets gains to

$18,201 to $ 37,000 19c for each 1$ above 18,200 0 to 9.65%

$37,001to $90,000 $3,572 plus 32.5c for each $1

over $37,000

9.65 to 23.11%

$90,001 to $180,000 $20,797 plus 37c for each $1

over $90,000

22.78 – 30.05%

$18,001and above $54,097 plus 45c for each $1

over $180,000

30.05 to less than 45%

Taxable income Tax on income effective tax rate

$1 - $ 90,000 32.5% for each 1$ 32.50%

$90,001-$180,000 $29,500 plus 37% above $90,000 32.5-34.8 %

$180,000 and

above

$66,550 plus 45% above $

180,000

34.8 to less than

45%

Capital gain taxes

Capital gain tax (CGT) is not separable from the overall Australian tax system.

From earlier inception by the (Huke, 2015, p.876), this form of taxation has slowly

gained route and contributes much to the total government revenues. Capital gain tax

related the cost base of particular assets to the consumer price index which then led to

easier assessment of inflations in relation to prices and currency. This taxes attract

marginal rates where capital gains adjusted after sale of an asset are applied to the total

taxpayers’ taxable income. Same to income tax, capital gains taxes applied to trusts

and partnerships are different from those applied to individual, businesses and

partnerships. For trusts, this tax is passed on to beneficiaries while for partnerships, this

tax is levied on individual partners.

In 1999the government under Prime Minister Howard eased calculation on

capital gain tax by abolishing calculation based on consumer price index. He swapped

cost based taxation with introduction of a discount allowable on gains. Discount rate

being 50% for individuals’ assets held for more than one year and 33.5 % for companies

income tax assessment act (1997) for other funds. This change in capital gain

calculation has erased benefits of doubt, attributing capital assets gains to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation theory, practice in Law 4

inflationwithout any contribution achieved by gains in purchasing power. There are

points to note about capital gain tax; firstly, the gains realized by companies are not

discounted, trustees are taxed on capital gains with regard to exceptions and that

capital assets before 1985 are exempt from capital gain taxes.

Fringe benefits tax

Employees are always entitled to certain benefits which are provided by the

employer in exception to the salary and wages paid. This benefits may also be

associated to family members. Tax on this benefits are separated from income taxes

and calculated on the value of that fringe benefits provided. Examples of fringe benefits

are private health cares and cars benefits.

In Australia, all this benefits are provided by an employer for the benefit of an

employee or a representative and this benefits may be enjoyed depending on whether

this employee is current, former or future employee. However it is important to note that

these benefits are not related whatsoever when contractors are considered.

Fringe benefits considered in the tax regulations are an example of housing

fringe benefits, care fringe benefits, benefits on work related items, benefits on

relocations and loan fringe benefits. There are only some fringe benefits that are subject

to taxation, some are exempt from taxation and others are tax free benefits for example

living away work related expenses, salary and wages and remote area housing. There

are also other benefits provided by charitable and public benevolent institutions that are

exempt from this taxes up to a certain amount on the ground of being provide by such

institutions. Notably, on 13th may 2008 exemption related to laptops and other

technological items were scraped since employees could purchase these items by

themselves and as well save on taxes.

Some employers always give and advance salary in form of fringe benefits to

employees as salary packaging to reduce income tax paid by such employees.

However, these benefits may be recovered back. The law requires employers to also

include on employees paymentsummary the benefits received due to fringe benefits tax

however, these taxes are paid by the latter as reported as fringe benefits with a value

above $2,000. FBT are only included as a means of income testing and are not in any

other reasons included in employees paymentsummary.

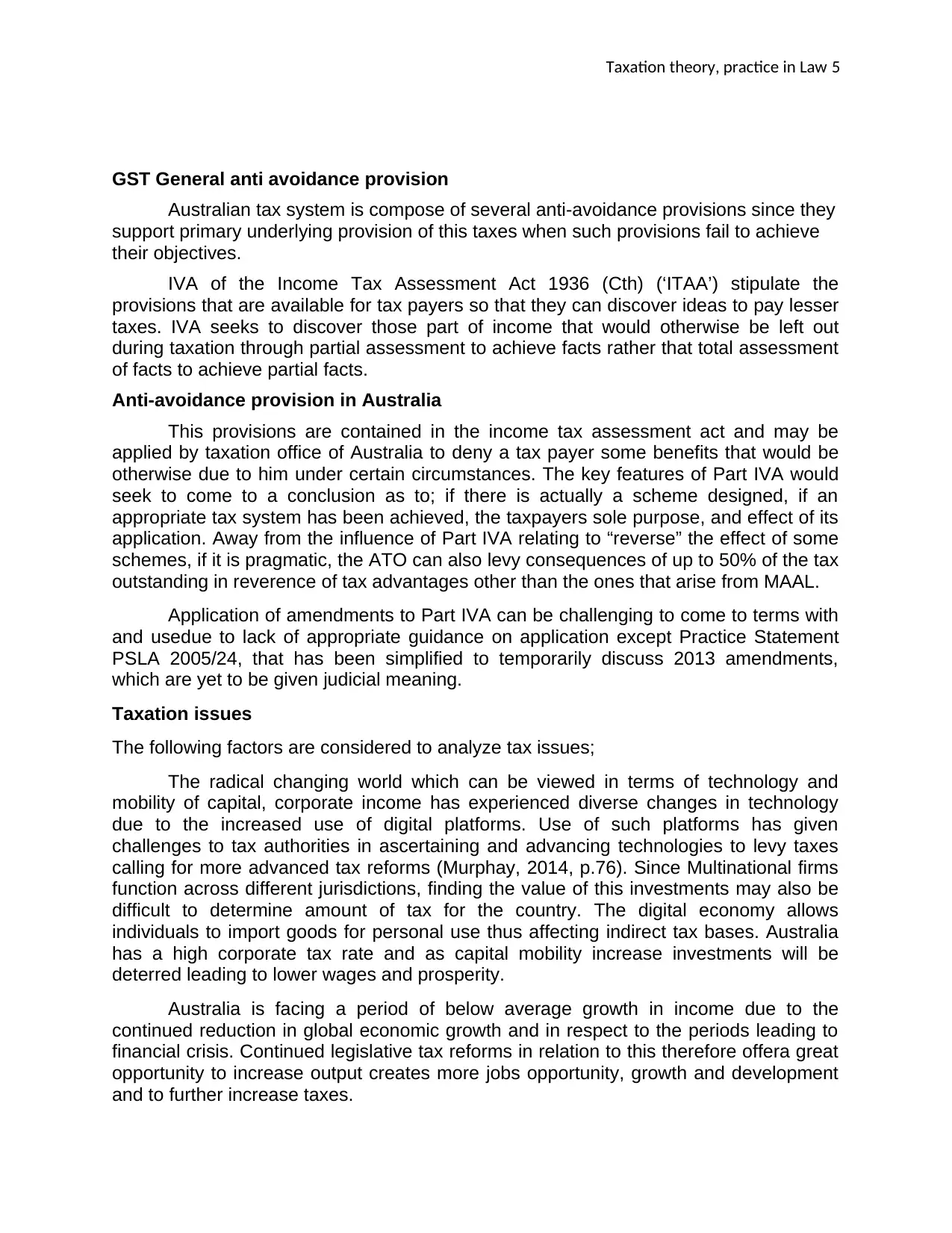

Below summary shows the rates applicable for fringe benefits tax rates,

From 2014 to 2018

Mar-14 46.50%

Mar-15 47%

Mar-16 49%

Mar-17 49%

Mar-18 47%

inflationwithout any contribution achieved by gains in purchasing power. There are

points to note about capital gain tax; firstly, the gains realized by companies are not

discounted, trustees are taxed on capital gains with regard to exceptions and that

capital assets before 1985 are exempt from capital gain taxes.

Fringe benefits tax

Employees are always entitled to certain benefits which are provided by the

employer in exception to the salary and wages paid. This benefits may also be

associated to family members. Tax on this benefits are separated from income taxes

and calculated on the value of that fringe benefits provided. Examples of fringe benefits

are private health cares and cars benefits.

In Australia, all this benefits are provided by an employer for the benefit of an

employee or a representative and this benefits may be enjoyed depending on whether

this employee is current, former or future employee. However it is important to note that

these benefits are not related whatsoever when contractors are considered.

Fringe benefits considered in the tax regulations are an example of housing

fringe benefits, care fringe benefits, benefits on work related items, benefits on

relocations and loan fringe benefits. There are only some fringe benefits that are subject

to taxation, some are exempt from taxation and others are tax free benefits for example

living away work related expenses, salary and wages and remote area housing. There

are also other benefits provided by charitable and public benevolent institutions that are

exempt from this taxes up to a certain amount on the ground of being provide by such

institutions. Notably, on 13th may 2008 exemption related to laptops and other

technological items were scraped since employees could purchase these items by

themselves and as well save on taxes.

Some employers always give and advance salary in form of fringe benefits to

employees as salary packaging to reduce income tax paid by such employees.

However, these benefits may be recovered back. The law requires employers to also

include on employees paymentsummary the benefits received due to fringe benefits tax

however, these taxes are paid by the latter as reported as fringe benefits with a value

above $2,000. FBT are only included as a means of income testing and are not in any

other reasons included in employees paymentsummary.

Below summary shows the rates applicable for fringe benefits tax rates,

From 2014 to 2018

Mar-14 46.50%

Mar-15 47%

Mar-16 49%

Mar-17 49%

Mar-18 47%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation theory, practice in Law 5

GST General anti avoidance provision

Australian tax system is compose of several anti-avoidance provisions since they

support primary underlying provision of this taxes when such provisions fail to achieve

their objectives.

IVA of the Income Tax Assessment Act 1936 (Cth) (‘ITAA’) stipulate the

provisions that are available for tax payers so that they can discover ideas to pay lesser

taxes. IVA seeks to discover those part of income that would otherwise be left out

during taxation through partial assessment to achieve facts rather that total assessment

of facts to achieve partial facts.

Anti-avoidance provision in Australia

This provisions are contained in the income tax assessment act and may be

applied by taxation office of Australia to deny a tax payer some benefits that would be

otherwise due to him under certain circumstances. The key features of Part IVA would

seek to come to a conclusion as to; if there is actually a scheme designed, if an

appropriate tax system has been achieved, the taxpayers sole purpose, and effect of its

application. Away from the influence of Part IVA relating to “reverse” the effect of some

schemes, if it is pragmatic, the ATO can also levy consequences of up to 50% of the tax

outstanding in reverence of tax advantages other than the ones that arise from MAAL.

Application of amendments to Part IVA can be challenging to come to terms with

and usedue to lack of appropriate guidance on application except Practice Statement

PSLA 2005/24, that has been simplified to temporarily discuss 2013 amendments,

which are yet to be given judicial meaning.

Taxation issues

The following factors are considered to analyze tax issues;

The radical changing world which can be viewed in terms of technology and

mobility of capital, corporate income has experienced diverse changes in technology

due to the increased use of digital platforms. Use of such platforms has given

challenges to tax authorities in ascertaining and advancing technologies to levy taxes

calling for more advanced tax reforms (Murphay, 2014, p.76). Since Multinational firms

function across different jurisdictions, finding the value of this investments may also be

difficult to determine amount of tax for the country. The digital economy allows

individuals to import goods for personal use thus affecting indirect tax bases. Australia

has a high corporate tax rate and as capital mobility increase investments will be

deterred leading to lower wages and prosperity.

Australia is facing a period of below average growth in income due to the

continued reduction in global economic growth and in respect to the periods leading to

financial crisis. Continued legislative tax reforms in relation to this therefore offera great

opportunity to increase output creates more jobs opportunity, growth and development

and to further increase taxes.

GST General anti avoidance provision

Australian tax system is compose of several anti-avoidance provisions since they

support primary underlying provision of this taxes when such provisions fail to achieve

their objectives.

IVA of the Income Tax Assessment Act 1936 (Cth) (‘ITAA’) stipulate the

provisions that are available for tax payers so that they can discover ideas to pay lesser

taxes. IVA seeks to discover those part of income that would otherwise be left out

during taxation through partial assessment to achieve facts rather that total assessment

of facts to achieve partial facts.

Anti-avoidance provision in Australia

This provisions are contained in the income tax assessment act and may be

applied by taxation office of Australia to deny a tax payer some benefits that would be

otherwise due to him under certain circumstances. The key features of Part IVA would

seek to come to a conclusion as to; if there is actually a scheme designed, if an

appropriate tax system has been achieved, the taxpayers sole purpose, and effect of its

application. Away from the influence of Part IVA relating to “reverse” the effect of some

schemes, if it is pragmatic, the ATO can also levy consequences of up to 50% of the tax

outstanding in reverence of tax advantages other than the ones that arise from MAAL.

Application of amendments to Part IVA can be challenging to come to terms with

and usedue to lack of appropriate guidance on application except Practice Statement

PSLA 2005/24, that has been simplified to temporarily discuss 2013 amendments,

which are yet to be given judicial meaning.

Taxation issues

The following factors are considered to analyze tax issues;

The radical changing world which can be viewed in terms of technology and

mobility of capital, corporate income has experienced diverse changes in technology

due to the increased use of digital platforms. Use of such platforms has given

challenges to tax authorities in ascertaining and advancing technologies to levy taxes

calling for more advanced tax reforms (Murphay, 2014, p.76). Since Multinational firms

function across different jurisdictions, finding the value of this investments may also be

difficult to determine amount of tax for the country. The digital economy allows

individuals to import goods for personal use thus affecting indirect tax bases. Australia

has a high corporate tax rate and as capital mobility increase investments will be

deterred leading to lower wages and prosperity.

Australia is facing a period of below average growth in income due to the

continued reduction in global economic growth and in respect to the periods leading to

financial crisis. Continued legislative tax reforms in relation to this therefore offera great

opportunity to increase output creates more jobs opportunity, growth and development

and to further increase taxes.

Taxation theory, practice in Law 6

Today, developed countries like Australia’s, have increasingly opened their

borders to trade and investments. Increasingdigitization of worldwide digital

platformshave also recently opened the Australian economy to the world changes that

have enormously changed the jurisdiction of tax system.

Australia’s population is expected to have an upward trends in the coming years.

An increase in population translates to more taxes to the government and demand for

adjustments into the tax reforms to accommodate this increase and advance new tax

products for the population. Reports illustrate that Australians aged above 65 years are

expected to increase in the coming years. This is an incentive to assist the government

in advancing tax reforms.

Possible increase in production due to more advanced tax system is expected

from economies sectors. Therefore, reforms should be aligned accordingly to achieve

this objective.

Interpretation of relevant taxation legislations and case laws

We can elucidate the constitution taxation basis in Australia from sections 51, 90,

53, 55 and 96 of the Australian constitution. Evolution of this constitution has been due

to several interpretations by the courts. Both the commonwealth and the state have

contributed to formation of this constitution that governs taxation. Section 96 states that

commonwealth has the power to collect taxes and latter distribute these taxes to state in

exercising its jurisdiction. Sec 51 enumerates authorities of commonwealth. These

influences are passed from period to period with limited check from the state for

example in section 53, the states cannot check on federal public service and in cases of

inconsistency, then commonwealth laws prevail.

Section 51(ii) state that commonwealth can enact laws in relation to;

All these laws must be assented to by the queen after passing through a rigorous

referendum

The broad Commonwealth power is also considered in broad when before this taxes are

imposed on tax payers. Since 1942, all powers to levy income taxes were monopolized

to commonwealth and state were only given this funds later on. This powers were held

in section 90

Tax of goods of a particular country is referred to as Custom duty. From The High Court

interpretation, all taxes that increases prices of goods are also regarded as Custom

duty. For example, in Ha v New South Wales (1997) a State tobacco license fee, which

consisted of a fixed amount plus an amount calculated by reference to the value of

tobacco sold, was struck down as custom duty.

It is not within the law for commonwealth to task state property and neither is the vice

versa (section 114 of income tax act).This exemption only relate to those

commonwealth or state properties and not any property controlled. For example, if a

state controls a construction, it does not necessarily own that construction. The courts

have had to deal with cases as to whether a tax is levied on property or something else.

Today, developed countries like Australia’s, have increasingly opened their

borders to trade and investments. Increasingdigitization of worldwide digital

platformshave also recently opened the Australian economy to the world changes that

have enormously changed the jurisdiction of tax system.

Australia’s population is expected to have an upward trends in the coming years.

An increase in population translates to more taxes to the government and demand for

adjustments into the tax reforms to accommodate this increase and advance new tax

products for the population. Reports illustrate that Australians aged above 65 years are

expected to increase in the coming years. This is an incentive to assist the government

in advancing tax reforms.

Possible increase in production due to more advanced tax system is expected

from economies sectors. Therefore, reforms should be aligned accordingly to achieve

this objective.

Interpretation of relevant taxation legislations and case laws

We can elucidate the constitution taxation basis in Australia from sections 51, 90,

53, 55 and 96 of the Australian constitution. Evolution of this constitution has been due

to several interpretations by the courts. Both the commonwealth and the state have

contributed to formation of this constitution that governs taxation. Section 96 states that

commonwealth has the power to collect taxes and latter distribute these taxes to state in

exercising its jurisdiction. Sec 51 enumerates authorities of commonwealth. These

influences are passed from period to period with limited check from the state for

example in section 53, the states cannot check on federal public service and in cases of

inconsistency, then commonwealth laws prevail.

Section 51(ii) state that commonwealth can enact laws in relation to;

All these laws must be assented to by the queen after passing through a rigorous

referendum

The broad Commonwealth power is also considered in broad when before this taxes are

imposed on tax payers. Since 1942, all powers to levy income taxes were monopolized

to commonwealth and state were only given this funds later on. This powers were held

in section 90

Tax of goods of a particular country is referred to as Custom duty. From The High Court

interpretation, all taxes that increases prices of goods are also regarded as Custom

duty. For example, in Ha v New South Wales (1997) a State tobacco license fee, which

consisted of a fixed amount plus an amount calculated by reference to the value of

tobacco sold, was struck down as custom duty.

It is not within the law for commonwealth to task state property and neither is the vice

versa (section 114 of income tax act).This exemption only relate to those

commonwealth or state properties and not any property controlled. For example, if a

state controls a construction, it does not necessarily own that construction. The courts

have had to deal with cases as to whether a tax is levied on property or something else.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation theory, practice in Law 7

The High Court of Australia has strived to interpret this provisions in broad perspectives

to inhibit any clash in controls. For example In South Australia v Commonwealth (1942)

65 CLR 373 (the First Uniform Tax case) , the scheme by Commonwealth to take over

the income tax field was upheld and commonwealth has continually been involve to levy

this taxes to increase government revenue.

Requirement by section 55 is that Legislation dealing with imposing taxes be involved

only with those duties. This requirement is dominant over other provisions of taxation.

Non tax provisions are rendered useless if they are found within the operative of tax

provisions since they are not contained in the mentioned section. Say a tax is

introduced for amendment, then only the amending instrument is considered

inoperative. This is what occurred in Air Caledonie International v Commonwealth.

Application of taxation principles to real life situation

Taxation legislations and tax laws that we will take into consideration for our discussion

are those related to income tax systems, capital gain taxes and fringe benefits taxes.

There are several principles of a good tax system according to latest scholars such as

Equity, ability to pay, benefits, and economic efficiency however; these principles are an

advancement of four major principles that were developed by Adam Smith (1776) that

will form the basis of our discussion. These principles are;

Equality principle. Every person should only pay to the government whatever they are

able to pay. In reality, people can only live according to their means and purchase only

what the can afford. Therefore if there are to pay taxes, then this should directly be

related to ability

Certaintyprinciple. To achieve results, an economy should require people especially

those involved in businessto be certain about the amount of tax they have to pay since

practically they are aware of the income they receive and therefore theyshould be given

this information to help them with economic planning.

Principle of convenience.The time and manner of taxpayment should be clear just like

structures are available in other sectors and in personalorganization.

Principle of economy. Revenue collected should be morethan costs used to collect

them for the system to be economical. Similarly, Corporations and businesses that

continually make losses may be forced to run down and dissolve.

Individual assessment tasks

Capital gain tax consequences

cost in $ capital gain

12,000-4,000 8,000

The High Court of Australia has strived to interpret this provisions in broad perspectives

to inhibit any clash in controls. For example In South Australia v Commonwealth (1942)

65 CLR 373 (the First Uniform Tax case) , the scheme by Commonwealth to take over

the income tax field was upheld and commonwealth has continually been involve to levy

this taxes to increase government revenue.

Requirement by section 55 is that Legislation dealing with imposing taxes be involved

only with those duties. This requirement is dominant over other provisions of taxation.

Non tax provisions are rendered useless if they are found within the operative of tax

provisions since they are not contained in the mentioned section. Say a tax is

introduced for amendment, then only the amending instrument is considered

inoperative. This is what occurred in Air Caledonie International v Commonwealth.

Application of taxation principles to real life situation

Taxation legislations and tax laws that we will take into consideration for our discussion

are those related to income tax systems, capital gain taxes and fringe benefits taxes.

There are several principles of a good tax system according to latest scholars such as

Equity, ability to pay, benefits, and economic efficiency however; these principles are an

advancement of four major principles that were developed by Adam Smith (1776) that

will form the basis of our discussion. These principles are;

Equality principle. Every person should only pay to the government whatever they are

able to pay. In reality, people can only live according to their means and purchase only

what the can afford. Therefore if there are to pay taxes, then this should directly be

related to ability

Certaintyprinciple. To achieve results, an economy should require people especially

those involved in businessto be certain about the amount of tax they have to pay since

practically they are aware of the income they receive and therefore theyshould be given

this information to help them with economic planning.

Principle of convenience.The time and manner of taxpayment should be clear just like

structures are available in other sectors and in personalorganization.

Principle of economy. Revenue collected should be morethan costs used to collect

them for the system to be economical. Similarly, Corporations and businesses that

continually make losses may be forced to run down and dissolve.

Individual assessment tasks

Capital gain tax consequences

cost in $ capital gain

12,000-4,000 8,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation theory, practice in Law 8

6,000-5,500 500

13,000-14,000 -1,000

5,000-470 4,530

Net capital gain 12,030

Applicable discount rate 50%

chargeable capital gain 6,015

Antique jewelry piece purchase on October 1987 attracted a capital loss thereby

reducing net capital gains.

All the other assets attracted a capital gain. The discount rate applicable for this asset is

50 % since they are held for more than one year.

Therefore taxable income will increase by $ 6,015.

Discussion of transaction consequences

13,000. The amount she has signed in the contract for the book being her income

13,400 since she does not want to claim ownership of the book, this amount signifies

that the ownership is transferred and is regarded as personal efforts

4350. This is the hand written copy amount that she receives due to personal efforts

3200. Amount received due to interview manuscript. This manuscript is necessary for

conducting questionnaires and is due to personal efforts

Yes, Barbara will not receive the total amount she received due to contract from the Eco

books limited. Amount she will receive in this case will be a little lesser since she will

sell the whole pack at a go.

Effect of loan arrangement on Patrick’s income

Amount due to Patrick is;

Amount in $

Loan amount 52000

Additional interest 5% *52,000

6,000-5,500 500

13,000-14,000 -1,000

5,000-470 4,530

Net capital gain 12,030

Applicable discount rate 50%

chargeable capital gain 6,015

Antique jewelry piece purchase on October 1987 attracted a capital loss thereby

reducing net capital gains.

All the other assets attracted a capital gain. The discount rate applicable for this asset is

50 % since they are held for more than one year.

Therefore taxable income will increase by $ 6,015.

Discussion of transaction consequences

13,000. The amount she has signed in the contract for the book being her income

13,400 since she does not want to claim ownership of the book, this amount signifies

that the ownership is transferred and is regarded as personal efforts

4350. This is the hand written copy amount that she receives due to personal efforts

3200. Amount received due to interview manuscript. This manuscript is necessary for

conducting questionnaires and is due to personal efforts

Yes, Barbara will not receive the total amount she received due to contract from the Eco

books limited. Amount she will receive in this case will be a little lesser since she will

sell the whole pack at a go.

Effect of loan arrangement on Patrick’s income

Amount due to Patrick is;

Amount in $

Loan amount 52000

Additional interest 5% *52,000

Taxation theory, practice in Law 9

Additional amount 2600

Total amount received =

Total amount received

52,000+2600

$54,600

Since this amount is paid through the bank, then it may be subject to taxations if the

source is justified.

Interest earned from this arrangement may be subject to taxation by the Australian tax

authority which requires this income to be declared.

The amount paid as tax on this interest will depend on the graduated scale applicable

on the overall income earned.

Additional amount 2600

Total amount received =

Total amount received

52,000+2600

$54,600

Since this amount is paid through the bank, then it may be subject to taxations if the

source is justified.

Interest earned from this arrangement may be subject to taxation by the Australian tax

authority which requires this income to be declared.

The amount paid as tax on this interest will depend on the graduated scale applicable

on the overall income earned.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation theory, practice in Law 10

References

Australian council of social services ACOSS 2011

Body, J., 2015. Design in the Australian taxation office. Design Issues, 24(1), pp.55-67.

Braithwaite, V.A., 2009. Defiance in taxation and governance: Resisting and dismissing

authority in a democracy. Edward Elgar Publishing.

Huke 2011, Lobar Government.

Job, J. and Honaker, D., 2016. Short-term experience with responsive regulation in the

Australian Taxation Office. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, the Australian National University.

Murphy, K., 2014. Moving towards a more effective model of regulatory

enforcement in the Australian Taxation Office.

Murphy K. Procedural justice and the Australian Taxation Office: A study of scheme

investors. Centre forTax System Integrity; 2002 Oct.

Oats, L. ed., 2012. Taxation: a fieldwork research handbook. Routledge.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian

taxation law. CCH Australia.

1 See G T Pagone, ‘Tax Planning or Tax Avoidance’ (2010) 29 Australian Tax Review

96

South Australia v Commonwealth (1942) 65 CLR 373 (the First Uniform Tax case).

References

Australian council of social services ACOSS 2011

Body, J., 2015. Design in the Australian taxation office. Design Issues, 24(1), pp.55-67.

Braithwaite, V.A., 2009. Defiance in taxation and governance: Resisting and dismissing

authority in a democracy. Edward Elgar Publishing.

Huke 2011, Lobar Government.

Job, J. and Honaker, D., 2016. Short-term experience with responsive regulation in the

Australian Taxation Office. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, the Australian National University.

Murphy, K., 2014. Moving towards a more effective model of regulatory

enforcement in the Australian Taxation Office.

Murphy K. Procedural justice and the Australian Taxation Office: A study of scheme

investors. Centre forTax System Integrity; 2002 Oct.

Oats, L. ed., 2012. Taxation: a fieldwork research handbook. Routledge.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian

taxation law. CCH Australia.

1 See G T Pagone, ‘Tax Planning or Tax Avoidance’ (2010) 29 Australian Tax Review

96

South Australia v Commonwealth (1942) 65 CLR 373 (the First Uniform Tax case).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.