Taxation Theory, Practice and Law - Desklib

Added on 2022-11-16

10 Pages3348 Words183 Views

Taxation theory, practice in Law 1

TAXATION THEORY, PRACTICE IN LAW.

Student Name

Professors Name

University

City/State

Date

TAXATION THEORY, PRACTICE IN LAW.

Student Name

Professors Name

University

City/State

Date

Taxation theory, practice in Law 2

Taxation theory, practice and law

Introduction

Taxable incomes in Australia are assessed on the basis of personal incomes

during a given period and allowable deductions by the federal government. Individual

incomes are assessed on three basis as; Personal income which is mainly composed of

people salaries and wages, business income which is that source of income derived

from people owned businesses and capital gain which is a rise in value of assets. Our

discussion will focus on concept of this income taxes, concept of income and deduction,

capital gain taxes, fringe benefit taxes and GST general anti avoidance provision and

income tax administration

Australia income tax system.

The main statute underlying income tax in Australia is income tax assessment

act 1997. Income tax is levied on a progressive basis meaning that the higher the

income the higher the tax paid. Australian income tax is imposed on citizens and

companies taxable income by the federal government. Paying taxes is important to

Australia (Body, 2015, p.900) since it contributes to revenue. Though imposed by the

federal government, this form of tax is collected and administered by the Australian

taxation office. Income tax is administered under progressive rate of between 0-45%

including a Medicare levy of 2% different from corporations tax which is between 27.5%-

30%(ACOSS, 2011, pp.345-347) depending on turnover generated annually while taxes

on capital gains are only effected if a gain is realized on capital assets attracting 50%

allowance if the asset was held for more than one year. It is also important to note

taxations on partnerships and trusts which is not administered directly but through

beneficiary and tax distribution to partners.

Concept of income and deduction

As discussed previously, income tax is levied on progressive basis for personal

taxes. In Australia, there are resident individual and non-resident individual tax payers

having different rates of tax payment for example most Australia citizens are liable to

pay Medicare of 2% standard rate on taxable income, a levy that is not imposed on non-

resident individual tax payers. Existence of withholding taxes has helped employees in

several instance due to refunds that such taxes bear. It is an obligation therefore for an

employer to withhold tax from wages and salaries of an employee after provision of tax

file number. In case where this number is not available then a requirement is imposed

on taxpayers to deduct 47%(ACOSS,2011, pp.345-347). Interest earned from financial

institutions that is due to individuals is also subject to the highest marginal rate of

income tax in the absence of tax file number. Likewise, failure to provide this number by

businesses to financial institution for tax levy, they should provide an Australian

business number otherwise the highest rate of income tax will be withheld.

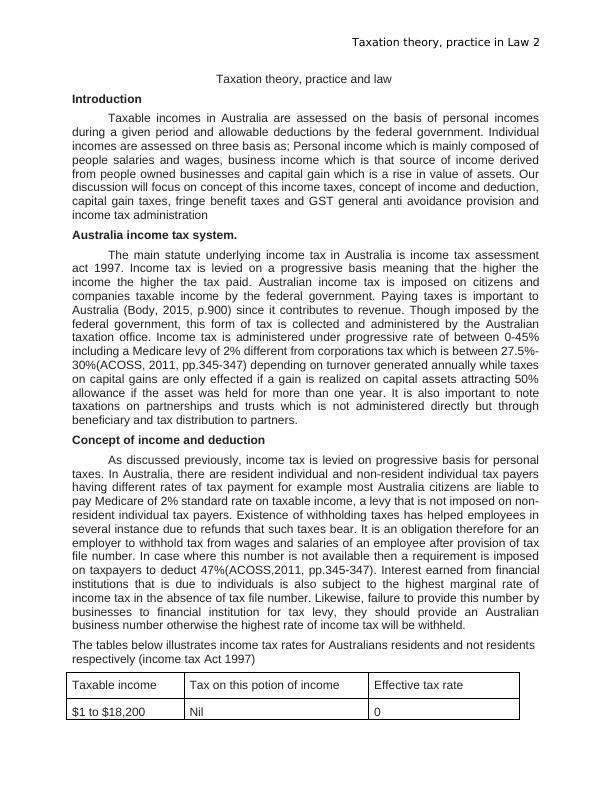

The tables below illustrates income tax rates for Australians residents and not residents

respectively (income tax Act 1997)

Taxable income Tax on this potion of income Effective tax rate

$1 to $18,200 Nil 0

Taxation theory, practice and law

Introduction

Taxable incomes in Australia are assessed on the basis of personal incomes

during a given period and allowable deductions by the federal government. Individual

incomes are assessed on three basis as; Personal income which is mainly composed of

people salaries and wages, business income which is that source of income derived

from people owned businesses and capital gain which is a rise in value of assets. Our

discussion will focus on concept of this income taxes, concept of income and deduction,

capital gain taxes, fringe benefit taxes and GST general anti avoidance provision and

income tax administration

Australia income tax system.

The main statute underlying income tax in Australia is income tax assessment

act 1997. Income tax is levied on a progressive basis meaning that the higher the

income the higher the tax paid. Australian income tax is imposed on citizens and

companies taxable income by the federal government. Paying taxes is important to

Australia (Body, 2015, p.900) since it contributes to revenue. Though imposed by the

federal government, this form of tax is collected and administered by the Australian

taxation office. Income tax is administered under progressive rate of between 0-45%

including a Medicare levy of 2% different from corporations tax which is between 27.5%-

30%(ACOSS, 2011, pp.345-347) depending on turnover generated annually while taxes

on capital gains are only effected if a gain is realized on capital assets attracting 50%

allowance if the asset was held for more than one year. It is also important to note

taxations on partnerships and trusts which is not administered directly but through

beneficiary and tax distribution to partners.

Concept of income and deduction

As discussed previously, income tax is levied on progressive basis for personal

taxes. In Australia, there are resident individual and non-resident individual tax payers

having different rates of tax payment for example most Australia citizens are liable to

pay Medicare of 2% standard rate on taxable income, a levy that is not imposed on non-

resident individual tax payers. Existence of withholding taxes has helped employees in

several instance due to refunds that such taxes bear. It is an obligation therefore for an

employer to withhold tax from wages and salaries of an employee after provision of tax

file number. In case where this number is not available then a requirement is imposed

on taxpayers to deduct 47%(ACOSS,2011, pp.345-347). Interest earned from financial

institutions that is due to individuals is also subject to the highest marginal rate of

income tax in the absence of tax file number. Likewise, failure to provide this number by

businesses to financial institution for tax levy, they should provide an Australian

business number otherwise the highest rate of income tax will be withheld.

The tables below illustrates income tax rates for Australians residents and not residents

respectively (income tax Act 1997)

Taxable income Tax on this potion of income Effective tax rate

$1 to $18,200 Nil 0

Taxation theory, practice in Law 3

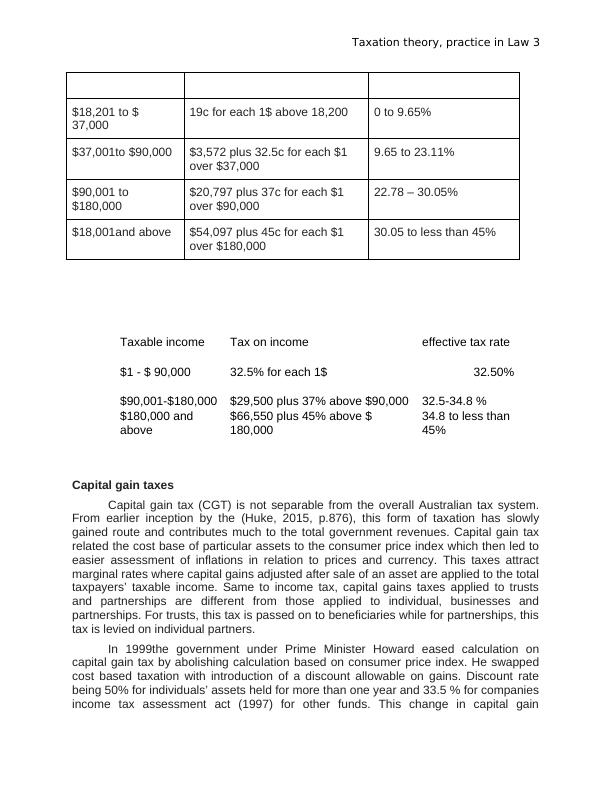

$18,201 to $

37,000

19c for each 1$ above 18,200 0 to 9.65%

$37,001to $90,000 $3,572 plus 32.5c for each $1

over $37,000

9.65 to 23.11%

$90,001 to

$180,000

$20,797 plus 37c for each $1

over $90,000

22.78 – 30.05%

$18,001and above $54,097 plus 45c for each $1

over $180,000

30.05 to less than 45%

Taxable income Tax on income effective tax rate

$1 - $ 90,000 32.5% for each 1$ 32.50%

$90,001-$180,000 $29,500 plus 37% above $90,000 32.5-34.8 %

$180,000 and

above

$66,550 plus 45% above $

180,000

34.8 to less than

45%

Capital gain taxes

Capital gain tax (CGT) is not separable from the overall Australian tax system.

From earlier inception by the (Huke, 2015, p.876), this form of taxation has slowly

gained route and contributes much to the total government revenues. Capital gain tax

related the cost base of particular assets to the consumer price index which then led to

easier assessment of inflations in relation to prices and currency. This taxes attract

marginal rates where capital gains adjusted after sale of an asset are applied to the total

taxpayers’ taxable income. Same to income tax, capital gains taxes applied to trusts

and partnerships are different from those applied to individual, businesses and

partnerships. For trusts, this tax is passed on to beneficiaries while for partnerships, this

tax is levied on individual partners.

In 1999the government under Prime Minister Howard eased calculation on

capital gain tax by abolishing calculation based on consumer price index. He swapped

cost based taxation with introduction of a discount allowable on gains. Discount rate

being 50% for individuals’ assets held for more than one year and 33.5 % for companies

income tax assessment act (1997) for other funds. This change in capital gain

$18,201 to $

37,000

19c for each 1$ above 18,200 0 to 9.65%

$37,001to $90,000 $3,572 plus 32.5c for each $1

over $37,000

9.65 to 23.11%

$90,001 to

$180,000

$20,797 plus 37c for each $1

over $90,000

22.78 – 30.05%

$18,001and above $54,097 plus 45c for each $1

over $180,000

30.05 to less than 45%

Taxable income Tax on income effective tax rate

$1 - $ 90,000 32.5% for each 1$ 32.50%

$90,001-$180,000 $29,500 plus 37% above $90,000 32.5-34.8 %

$180,000 and

above

$66,550 plus 45% above $

180,000

34.8 to less than

45%

Capital gain taxes

Capital gain tax (CGT) is not separable from the overall Australian tax system.

From earlier inception by the (Huke, 2015, p.876), this form of taxation has slowly

gained route and contributes much to the total government revenues. Capital gain tax

related the cost base of particular assets to the consumer price index which then led to

easier assessment of inflations in relation to prices and currency. This taxes attract

marginal rates where capital gains adjusted after sale of an asset are applied to the total

taxpayers’ taxable income. Same to income tax, capital gains taxes applied to trusts

and partnerships are different from those applied to individual, businesses and

partnerships. For trusts, this tax is passed on to beneficiaries while for partnerships, this

tax is levied on individual partners.

In 1999the government under Prime Minister Howard eased calculation on

capital gain tax by abolishing calculation based on consumer price index. He swapped

cost based taxation with introduction of a discount allowable on gains. Discount rate

being 50% for individuals’ assets held for more than one year and 33.5 % for companies

income tax assessment act (1997) for other funds. This change in capital gain

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Australia Taxation Lawlg...

|12

|2554

|97

Taxation Law: Tax Treatments for Foreigners and Residents Comparedlg...

|7

|1423

|234

Australian Tax Legislationslg...

|13

|2707

|146

Taxation Law: Capital Gains and Deductionslg...

|10

|2626

|21

Australian Tax Law - Income Deduction, FBT, GST, CGT, Anti-Avoidance Provisions and Income Administrationlg...

|13

|2820

|137

Introduction to Income Tax Law - Doclg...

|9

|2263

|35