Taxation Theory, Practice & Law Report - Taxation Analysis and Advice

VerifiedAdded on 2020/12/09

|14

|3697

|56

Report

AI Summary

This report provides a detailed analysis of Australian taxation, focusing on capital gains tax (CGT) and fringe benefit tax (FBT). It examines the CGT implications of various assets, including vacant land, antiques, paintings, and shares, calculating taxable capital gains or losses based on relevan...

TAXATION THEORY,

PRACTICE & LAW

1

PRACTICE & LAW

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................1

QUESTION 1.......................................................................................................................................1

Determination of Net Capital Gains/Loss for the current tax year ending 30th June........................1

QUESTION 2.......................................................................................................................................9

a. Advising Rapid-Heat about its fringe benefit tax.........................................................................9

(B) Stating recommendation if Jasmine will use money for purchasing shares.............................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION................................................................................................................................1

QUESTION 1.......................................................................................................................................1

Determination of Net Capital Gains/Loss for the current tax year ending 30th June........................1

QUESTION 2.......................................................................................................................................9

a. Advising Rapid-Heat about its fringe benefit tax.........................................................................9

(B) Stating recommendation if Jasmine will use money for purchasing shares.............................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION

Taxes in Australia are levied and collected by Federal Government through Australian

taxation office. There are various tax laws and regulations which are imposed on different segment

of society. Income tax in Australia is imposed at progressive rates which means amount of tax

increases as taxable amount increases The two statues which covers them are Income Tax

Assessment Act 1936 followed by Income Tax Assessment Act 1997. The Goods and Services tax

are also collected and levied by the Federal Government and distributed to different States on

formula defined by Commonwealth Grants Commission. The legislation which covers GST is A

New Tax System (Goods and Services Tax) Act 1989. This Project report consists of analysis of

data given by the client which includes Capital gain tax on various assets, its GST implications, the

Fringe Benefit provided to the employee’s which is governed by FBT Act 1986. This reports also

depicts ways for savings in the tax for client and provides alternatives for solving different issues

occurred by the tax implications.

QUESTION 1

Determination of Net Capital Gains/Loss for the current tax year ending 30th June

To determine CGT on various assets provided by the client the act which covers them is

Income Tax Assessment Act 1997. Capital gain tax are taxes which are levied on purchase and sale

of assets provided by act (Evans, 2015). This law covers different methods to calculate CGT on the

basis of utilization of asset.

(A)Block of Vacant Land

The CGT treatment on sales of land generally depend upon whether it is considered as

capital asset or for commercial transaction (Feld, 2016). The Block of vacant land is usually

considered as capital asset I.e. why it is subject to CGT but if is used for trading stock in any real

estate business than income from sale proceeds will be treated as ordinary income (O'Connor,

2018). If the land is acquired before 11:45am on the 21st September 1999 and held for more than 12

months, then “Indexation Method” will apply otherwise “Discount Method” will be applied. The

cost base includes all expenses in acquiring the asset which includes stamp duty, brokerage etc.

Sec 104(35) of the Act describes the contractual rights-:

1. the time of event is when you enter into contract or create other rights to acquire

asset.

2. If you dispose of asset the CGT event will occur when you stop being the owners of

1

Taxes in Australia are levied and collected by Federal Government through Australian

taxation office. There are various tax laws and regulations which are imposed on different segment

of society. Income tax in Australia is imposed at progressive rates which means amount of tax

increases as taxable amount increases The two statues which covers them are Income Tax

Assessment Act 1936 followed by Income Tax Assessment Act 1997. The Goods and Services tax

are also collected and levied by the Federal Government and distributed to different States on

formula defined by Commonwealth Grants Commission. The legislation which covers GST is A

New Tax System (Goods and Services Tax) Act 1989. This Project report consists of analysis of

data given by the client which includes Capital gain tax on various assets, its GST implications, the

Fringe Benefit provided to the employee’s which is governed by FBT Act 1986. This reports also

depicts ways for savings in the tax for client and provides alternatives for solving different issues

occurred by the tax implications.

QUESTION 1

Determination of Net Capital Gains/Loss for the current tax year ending 30th June

To determine CGT on various assets provided by the client the act which covers them is

Income Tax Assessment Act 1997. Capital gain tax are taxes which are levied on purchase and sale

of assets provided by act (Evans, 2015). This law covers different methods to calculate CGT on the

basis of utilization of asset.

(A)Block of Vacant Land

The CGT treatment on sales of land generally depend upon whether it is considered as

capital asset or for commercial transaction (Feld, 2016). The Block of vacant land is usually

considered as capital asset I.e. why it is subject to CGT but if is used for trading stock in any real

estate business than income from sale proceeds will be treated as ordinary income (O'Connor,

2018). If the land is acquired before 11:45am on the 21st September 1999 and held for more than 12

months, then “Indexation Method” will apply otherwise “Discount Method” will be applied. The

cost base includes all expenses in acquiring the asset which includes stamp duty, brokerage etc.

Sec 104(35) of the Act describes the contractual rights-:

1. the time of event is when you enter into contract or create other rights to acquire

asset.

2. If you dispose of asset the CGT event will occur when you stop being the owners of

1

You're viewing a preview

Unlock full access by subscribing today!

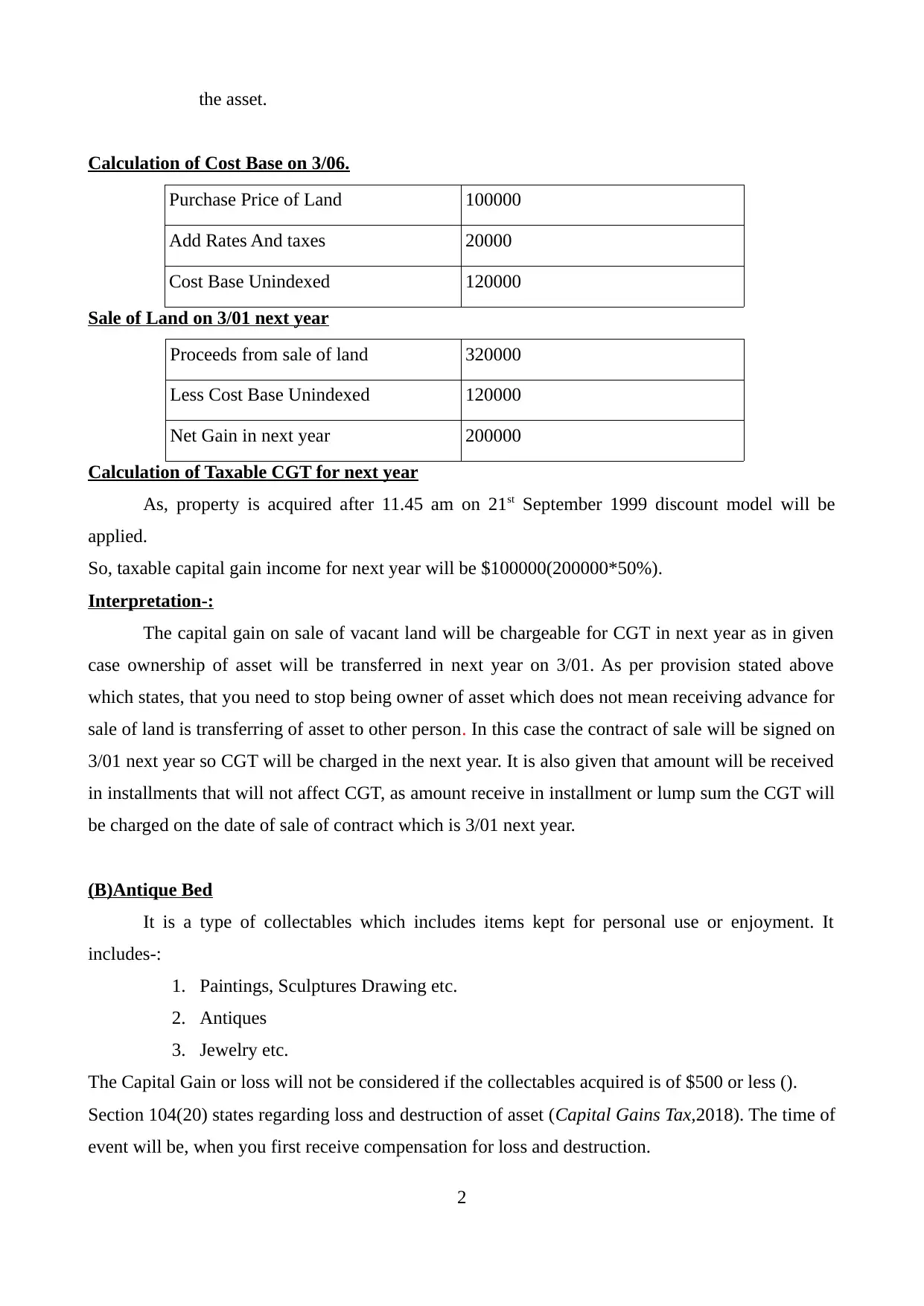

the asset.

Calculation of Cost Base on 3/06.

Purchase Price of Land 100000

Add Rates And taxes 20000

Cost Base Unindexed 120000

Sale of Land on 3/01 next year

Proceeds from sale of land 320000

Less Cost Base Unindexed 120000

Net Gain in next year 200000

Calculation of Taxable CGT for next year

As, property is acquired after 11.45 am on 21st September 1999 discount model will be

applied.

So, taxable capital gain income for next year will be $100000(200000*50%).

Interpretation-:

The capital gain on sale of vacant land will be chargeable for CGT in next year as in given

case ownership of asset will be transferred in next year on 3/01. As per provision stated above

which states, that you need to stop being owner of asset which does not mean receiving advance for

sale of land is transferring of asset to other person. In this case the contract of sale will be signed on

3/01 next year so CGT will be charged in the next year. It is also given that amount will be received

in installments that will not affect CGT, as amount receive in installment or lump sum the CGT will

be charged on the date of sale of contract which is 3/01 next year.

(B)Antique Bed

It is a type of collectables which includes items kept for personal use or enjoyment. It

includes-:

1. Paintings, Sculptures Drawing etc.

2. Antiques

3. Jewelry etc.

The Capital Gain or loss will not be considered if the collectables acquired is of $500 or less ().

Section 104(20) states regarding loss and destruction of asset (Capital Gains Tax,2018). The time of

event will be, when you first receive compensation for loss and destruction.

2

Calculation of Cost Base on 3/06.

Purchase Price of Land 100000

Add Rates And taxes 20000

Cost Base Unindexed 120000

Sale of Land on 3/01 next year

Proceeds from sale of land 320000

Less Cost Base Unindexed 120000

Net Gain in next year 200000

Calculation of Taxable CGT for next year

As, property is acquired after 11.45 am on 21st September 1999 discount model will be

applied.

So, taxable capital gain income for next year will be $100000(200000*50%).

Interpretation-:

The capital gain on sale of vacant land will be chargeable for CGT in next year as in given

case ownership of asset will be transferred in next year on 3/01. As per provision stated above

which states, that you need to stop being owner of asset which does not mean receiving advance for

sale of land is transferring of asset to other person. In this case the contract of sale will be signed on

3/01 next year so CGT will be charged in the next year. It is also given that amount will be received

in installments that will not affect CGT, as amount receive in installment or lump sum the CGT will

be charged on the date of sale of contract which is 3/01 next year.

(B)Antique Bed

It is a type of collectables which includes items kept for personal use or enjoyment. It

includes-:

1. Paintings, Sculptures Drawing etc.

2. Antiques

3. Jewelry etc.

The Capital Gain or loss will not be considered if the collectables acquired is of $500 or less ().

Section 104(20) states regarding loss and destruction of asset (Capital Gains Tax,2018). The time of

event will be, when you first receive compensation for loss and destruction.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

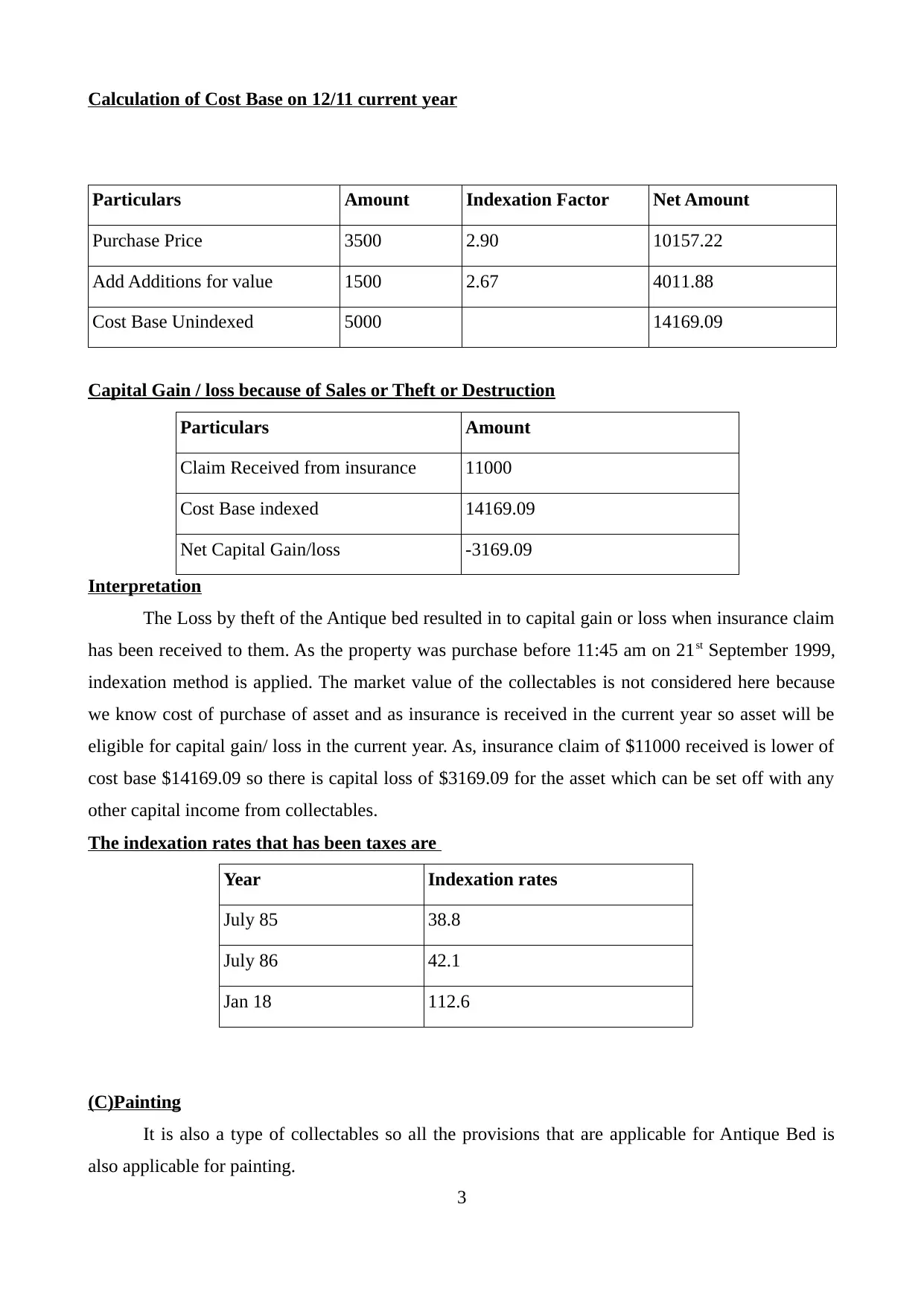

Calculation of Cost Base on 12/11 current year

Particulars Amount Indexation Factor Net Amount

Purchase Price 3500 2.90 10157.22

Add Additions for value 1500 2.67 4011.88

Cost Base Unindexed 5000 14169.09

Capital Gain / loss because of Sales or Theft or Destruction

Particulars Amount

Claim Received from insurance 11000

Cost Base indexed 14169.09

Net Capital Gain/loss -3169.09

Interpretation

The Loss by theft of the Antique bed resulted in to capital gain or loss when insurance claim

has been received to them. As the property was purchase before 11:45 am on 21st September 1999,

indexation method is applied. The market value of the collectables is not considered here because

we know cost of purchase of asset and as insurance is received in the current year so asset will be

eligible for capital gain/ loss in the current year. As, insurance claim of $11000 received is lower of

cost base $14169.09 so there is capital loss of $3169.09 for the asset which can be set off with any

other capital income from collectables.

The indexation rates that has been taxes are

Year Indexation rates

July 85 38.8

July 86 42.1

Jan 18 112.6

(C)Painting

It is also a type of collectables so all the provisions that are applicable for Antique Bed is

also applicable for painting.

3

Particulars Amount Indexation Factor Net Amount

Purchase Price 3500 2.90 10157.22

Add Additions for value 1500 2.67 4011.88

Cost Base Unindexed 5000 14169.09

Capital Gain / loss because of Sales or Theft or Destruction

Particulars Amount

Claim Received from insurance 11000

Cost Base indexed 14169.09

Net Capital Gain/loss -3169.09

Interpretation

The Loss by theft of the Antique bed resulted in to capital gain or loss when insurance claim

has been received to them. As the property was purchase before 11:45 am on 21st September 1999,

indexation method is applied. The market value of the collectables is not considered here because

we know cost of purchase of asset and as insurance is received in the current year so asset will be

eligible for capital gain/ loss in the current year. As, insurance claim of $11000 received is lower of

cost base $14169.09 so there is capital loss of $3169.09 for the asset which can be set off with any

other capital income from collectables.

The indexation rates that has been taxes are

Year Indexation rates

July 85 38.8

July 86 42.1

Jan 18 112.6

(C)Painting

It is also a type of collectables so all the provisions that are applicable for Antique Bed is

also applicable for painting.

3

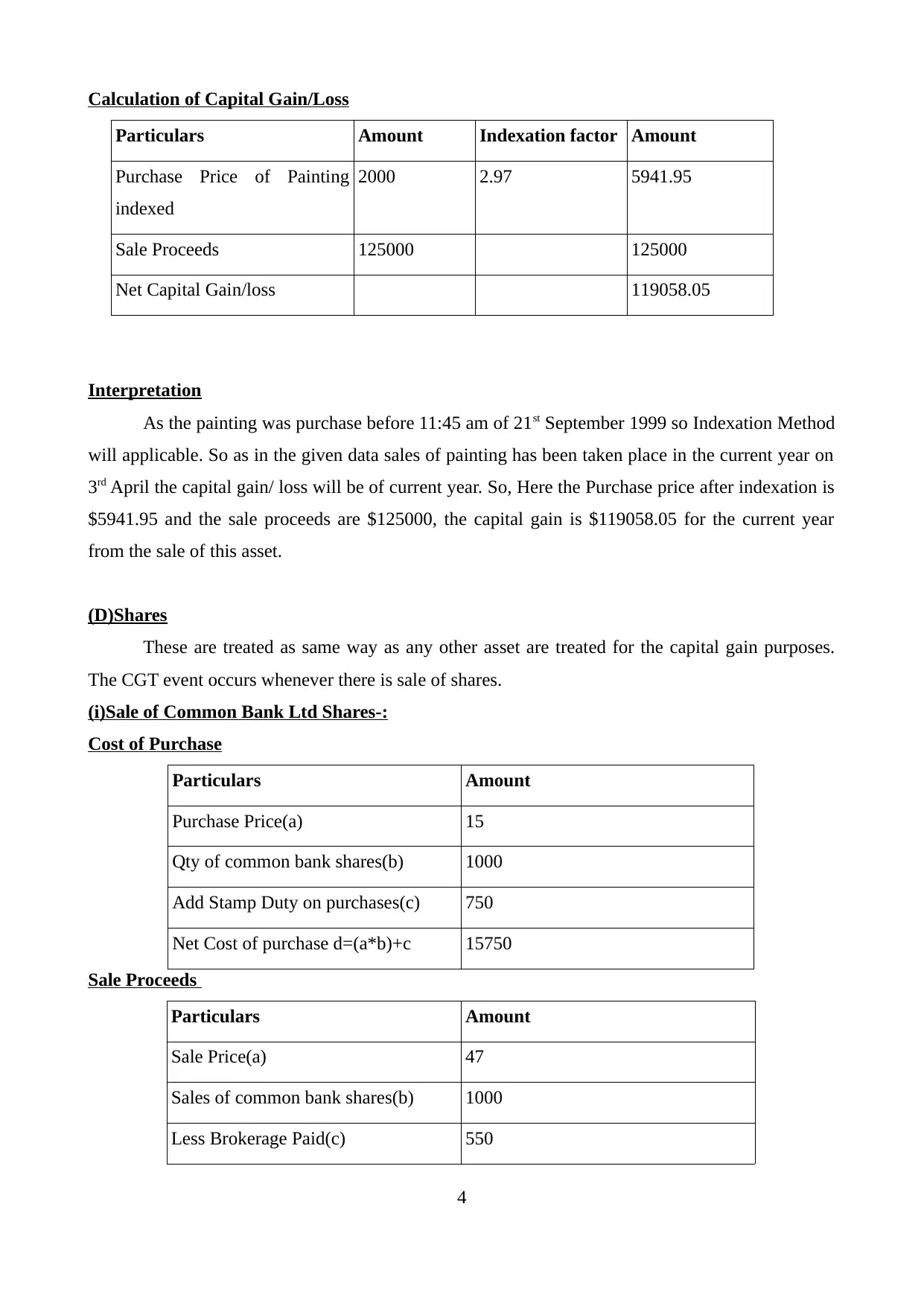

Calculation of Capital Gain/Loss

Particulars Amount Indexation factor Amount

Purchase Price of Painting

indexed

2000 2.97 5941.95

Sale Proceeds 125000 125000

Net Capital Gain/loss 119058.05

Interpretation

As the painting was purchase before 11:45 am of 21st September 1999 so Indexation Method

will applicable. So as in the given data sales of painting has been taken place in the current year on

3rd April the capital gain/ loss will be of current year. So, Here the Purchase price after indexation is

$5941.95 and the sale proceeds are $125000, the capital gain is $119058.05 for the current year

from the sale of this asset.

(D)Shares

These are treated as same way as any other asset are treated for the capital gain purposes.

The CGT event occurs whenever there is sale of shares.

(i)Sale of Common Bank Ltd Shares-:

Cost of Purchase

Particulars Amount

Purchase Price(a) 15

Qty of common bank shares(b) 1000

Add Stamp Duty on purchases(c) 750

Net Cost of purchase d=(a*b)+c 15750

Sale Proceeds

Particulars Amount

Sale Price(a) 47

Sales of common bank shares(b) 1000

Less Brokerage Paid(c) 550

4

Particulars Amount Indexation factor Amount

Purchase Price of Painting

indexed

2000 2.97 5941.95

Sale Proceeds 125000 125000

Net Capital Gain/loss 119058.05

Interpretation

As the painting was purchase before 11:45 am of 21st September 1999 so Indexation Method

will applicable. So as in the given data sales of painting has been taken place in the current year on

3rd April the capital gain/ loss will be of current year. So, Here the Purchase price after indexation is

$5941.95 and the sale proceeds are $125000, the capital gain is $119058.05 for the current year

from the sale of this asset.

(D)Shares

These are treated as same way as any other asset are treated for the capital gain purposes.

The CGT event occurs whenever there is sale of shares.

(i)Sale of Common Bank Ltd Shares-:

Cost of Purchase

Particulars Amount

Purchase Price(a) 15

Qty of common bank shares(b) 1000

Add Stamp Duty on purchases(c) 750

Net Cost of purchase d=(a*b)+c 15750

Sale Proceeds

Particulars Amount

Sale Price(a) 47

Sales of common bank shares(b) 1000

Less Brokerage Paid(c) 550

4

You're viewing a preview

Unlock full access by subscribing today!

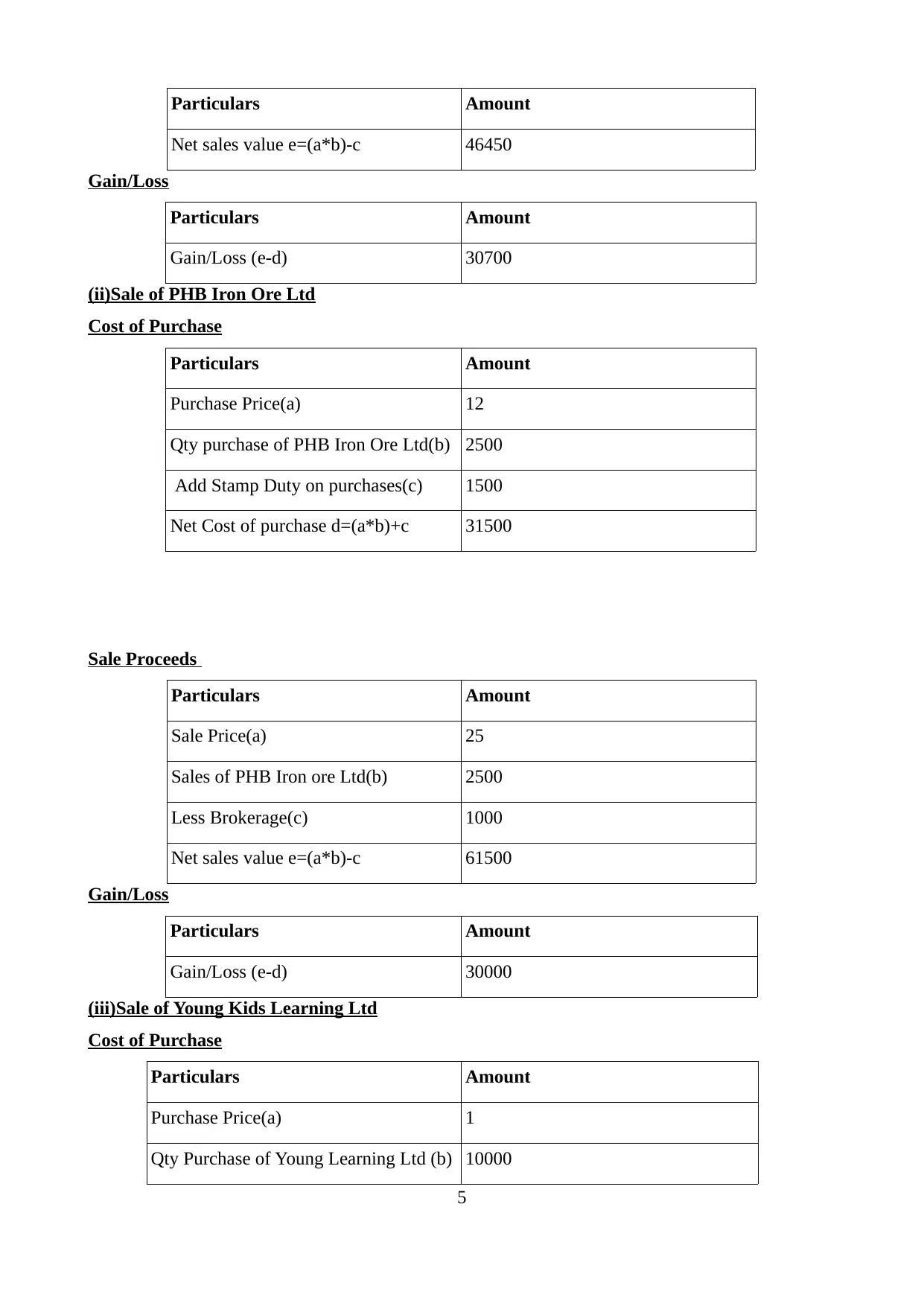

Particulars Amount

Net sales value e=(a*b)-c 46450

Gain/Loss

Particulars Amount

Gain/Loss (e-d) 30700

(ii)Sale of PHB Iron Ore Ltd

Cost of Purchase

Particulars Amount

Purchase Price(a) 12

Qty purchase of PHB Iron Ore Ltd(b) 2500

Add Stamp Duty on purchases(c) 1500

Net Cost of purchase d=(a*b)+c 31500

Sale Proceeds

Particulars Amount

Sale Price(a) 25

Sales of PHB Iron ore Ltd(b) 2500

Less Brokerage(c) 1000

Net sales value e=(a*b)-c 61500

Gain/Loss

Particulars Amount

Gain/Loss (e-d) 30000

(iii)Sale of Young Kids Learning Ltd

Cost of Purchase

Particulars Amount

Purchase Price(a) 1

Qty Purchase of Young Learning Ltd (b) 10000

5

Net sales value e=(a*b)-c 46450

Gain/Loss

Particulars Amount

Gain/Loss (e-d) 30700

(ii)Sale of PHB Iron Ore Ltd

Cost of Purchase

Particulars Amount

Purchase Price(a) 12

Qty purchase of PHB Iron Ore Ltd(b) 2500

Add Stamp Duty on purchases(c) 1500

Net Cost of purchase d=(a*b)+c 31500

Sale Proceeds

Particulars Amount

Sale Price(a) 25

Sales of PHB Iron ore Ltd(b) 2500

Less Brokerage(c) 1000

Net sales value e=(a*b)-c 61500

Gain/Loss

Particulars Amount

Gain/Loss (e-d) 30000

(iii)Sale of Young Kids Learning Ltd

Cost of Purchase

Particulars Amount

Purchase Price(a) 1

Qty Purchase of Young Learning Ltd (b) 10000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

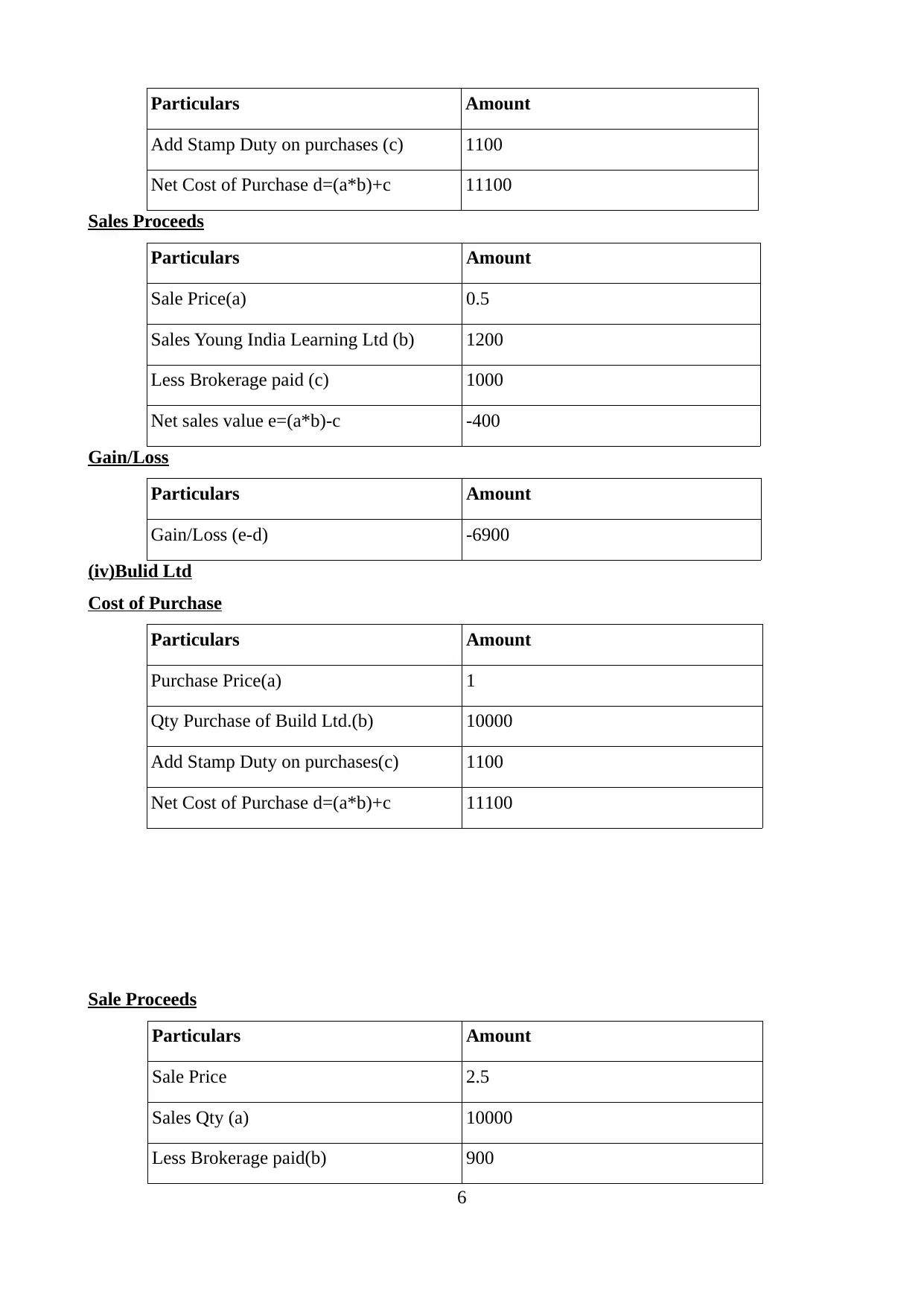

Particulars Amount

Add Stamp Duty on purchases (c) 1100

Net Cost of Purchase d=(a*b)+c 11100

Sales Proceeds

Particulars Amount

Sale Price(a) 0.5

Sales Young India Learning Ltd (b) 1200

Less Brokerage paid (c) 1000

Net sales value e=(a*b)-c -400

Gain/Loss

Particulars Amount

Gain/Loss (e-d) -6900

(iv)Bulid Ltd

Cost of Purchase

Particulars Amount

Purchase Price(a) 1

Qty Purchase of Build Ltd.(b) 10000

Add Stamp Duty on purchases(c) 1100

Net Cost of Purchase d=(a*b)+c 11100

Sale Proceeds

Particulars Amount

Sale Price 2.5

Sales Qty (a) 10000

Less Brokerage paid(b) 900

6

Add Stamp Duty on purchases (c) 1100

Net Cost of Purchase d=(a*b)+c 11100

Sales Proceeds

Particulars Amount

Sale Price(a) 0.5

Sales Young India Learning Ltd (b) 1200

Less Brokerage paid (c) 1000

Net sales value e=(a*b)-c -400

Gain/Loss

Particulars Amount

Gain/Loss (e-d) -6900

(iv)Bulid Ltd

Cost of Purchase

Particulars Amount

Purchase Price(a) 1

Qty Purchase of Build Ltd.(b) 10000

Add Stamp Duty on purchases(c) 1100

Net Cost of Purchase d=(a*b)+c 11100

Sale Proceeds

Particulars Amount

Sale Price 2.5

Sales Qty (a) 10000

Less Brokerage paid(b) 900

6

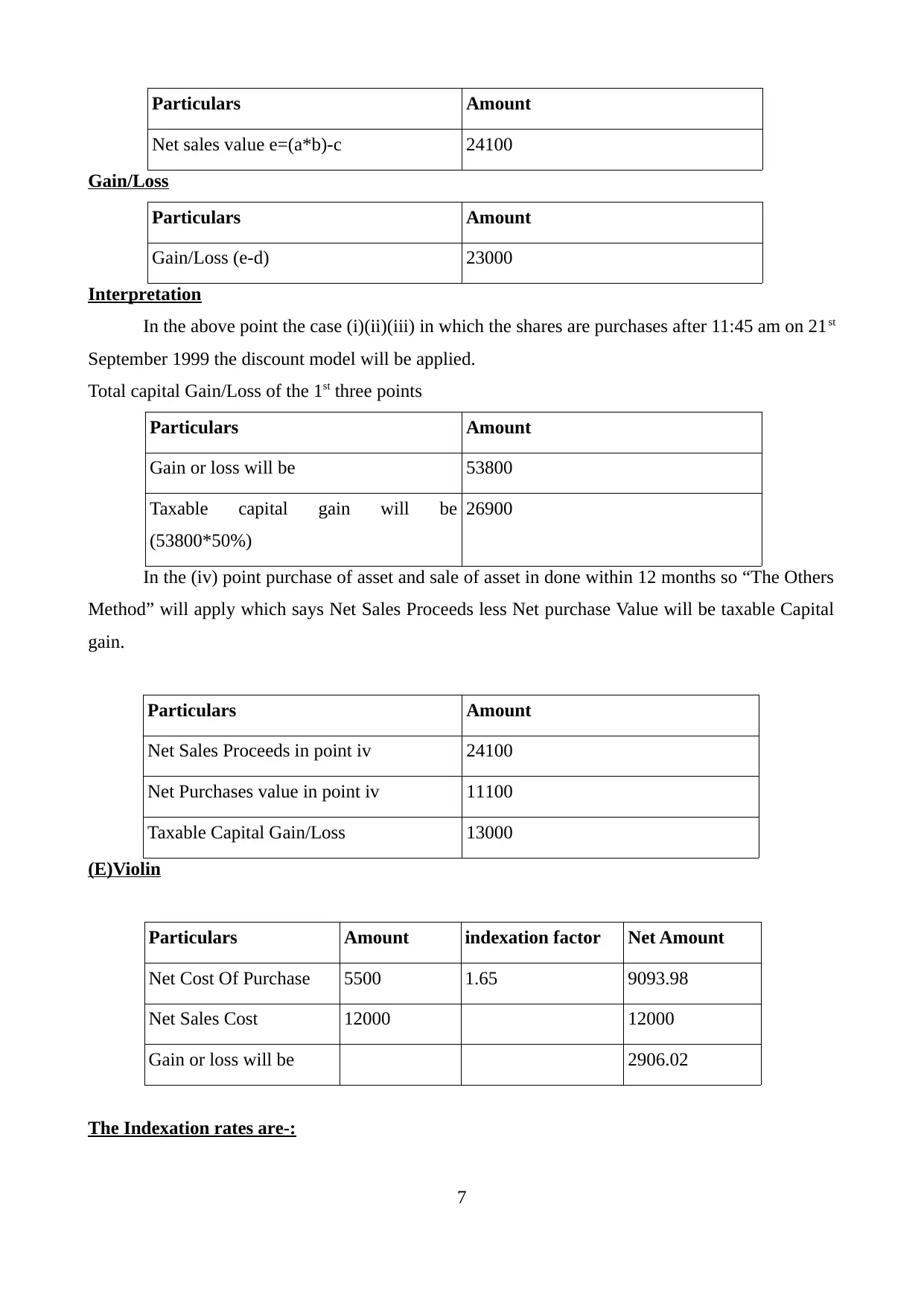

Particulars Amount

Net sales value e=(a*b)-c 24100

Gain/Loss

Particulars Amount

Gain/Loss (e-d) 23000

Interpretation

In the above point the case (i)(ii)(iii) in which the shares are purchases after 11:45 am on 21st

September 1999 the discount model will be applied.

Total capital Gain/Loss of the 1st three points

Particulars Amount

Gain or loss will be 53800

Taxable capital gain will be

(53800*50%)

26900

In the (iv) point purchase of asset and sale of asset in done within 12 months so “The Others

Method” will apply which says Net Sales Proceeds less Net purchase Value will be taxable Capital

gain.

Particulars Amount

Net Sales Proceeds in point iv 24100

Net Purchases value in point iv 11100

Taxable Capital Gain/Loss 13000

(E)Violin

Particulars Amount indexation factor Net Amount

Net Cost Of Purchase 5500 1.65 9093.98

Net Sales Cost 12000 12000

Gain or loss will be 2906.02

The Indexation rates are-:

7

Net sales value e=(a*b)-c 24100

Gain/Loss

Particulars Amount

Gain/Loss (e-d) 23000

Interpretation

In the above point the case (i)(ii)(iii) in which the shares are purchases after 11:45 am on 21st

September 1999 the discount model will be applied.

Total capital Gain/Loss of the 1st three points

Particulars Amount

Gain or loss will be 53800

Taxable capital gain will be

(53800*50%)

26900

In the (iv) point purchase of asset and sale of asset in done within 12 months so “The Others

Method” will apply which says Net Sales Proceeds less Net purchase Value will be taxable Capital

gain.

Particulars Amount

Net Sales Proceeds in point iv 24100

Net Purchases value in point iv 11100

Taxable Capital Gain/Loss 13000

(E)Violin

Particulars Amount indexation factor Net Amount

Net Cost Of Purchase 5500 1.65 9093.98

Net Sales Cost 12000 12000

Gain or loss will be 2906.02

The Indexation rates are-:

7

You're viewing a preview

Unlock full access by subscribing today!

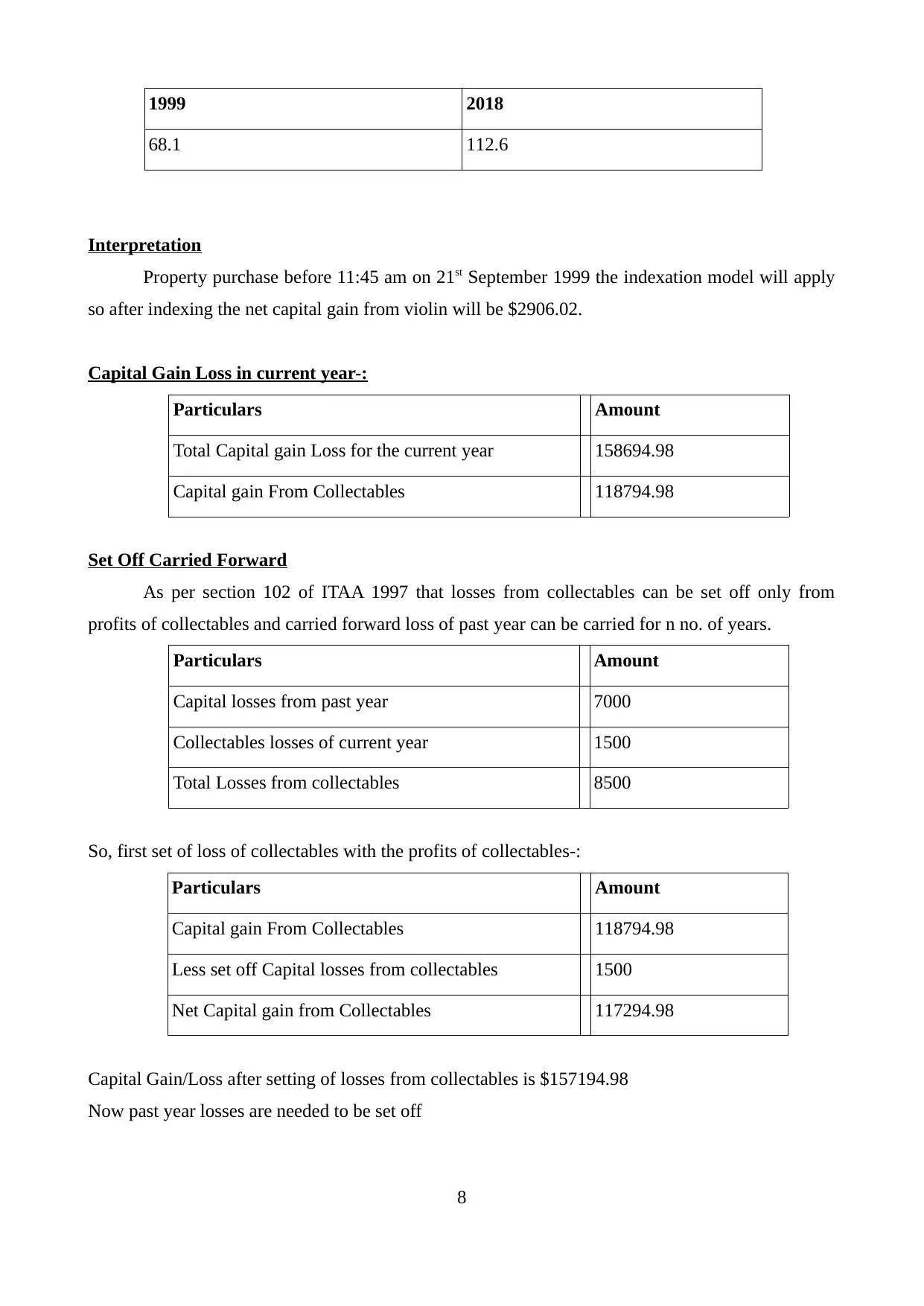

1999 2018

68.1 112.6

Interpretation

Property purchase before 11:45 am on 21st September 1999 the indexation model will apply

so after indexing the net capital gain from violin will be $2906.02.

Capital Gain Loss in current year-:

Particulars Amount

Total Capital gain Loss for the current year 158694.98

Capital gain From Collectables 118794.98

Set Off Carried Forward

As per section 102 of ITAA 1997 that losses from collectables can be set off only from

profits of collectables and carried forward loss of past year can be carried for n no. of years.

Particulars Amount

Capital losses from past year 7000

Collectables losses of current year 1500

Total Losses from collectables 8500

So, first set of loss of collectables with the profits of collectables-:

Particulars Amount

Capital gain From Collectables 118794.98

Less set off Capital losses from collectables 1500

Net Capital gain from Collectables 117294.98

Capital Gain/Loss after setting of losses from collectables is $157194.98

Now past year losses are needed to be set off

8

68.1 112.6

Interpretation

Property purchase before 11:45 am on 21st September 1999 the indexation model will apply

so after indexing the net capital gain from violin will be $2906.02.

Capital Gain Loss in current year-:

Particulars Amount

Total Capital gain Loss for the current year 158694.98

Capital gain From Collectables 118794.98

Set Off Carried Forward

As per section 102 of ITAA 1997 that losses from collectables can be set off only from

profits of collectables and carried forward loss of past year can be carried for n no. of years.

Particulars Amount

Capital losses from past year 7000

Collectables losses of current year 1500

Total Losses from collectables 8500

So, first set of loss of collectables with the profits of collectables-:

Particulars Amount

Capital gain From Collectables 118794.98

Less set off Capital losses from collectables 1500

Net Capital gain from Collectables 117294.98

Capital Gain/Loss after setting of losses from collectables is $157194.98

Now past year losses are needed to be set off

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

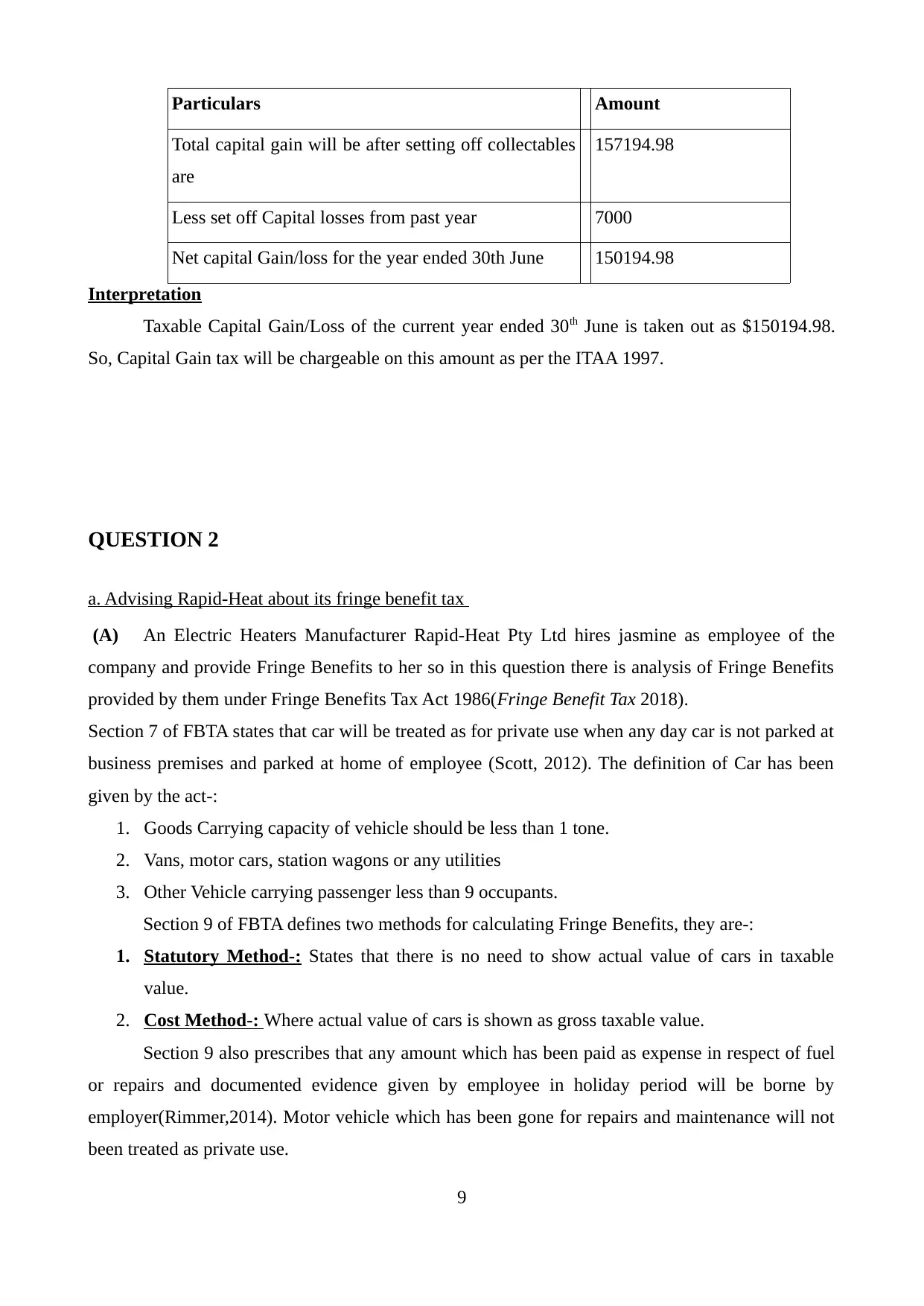

Particulars Amount

Total capital gain will be after setting off collectables

are

157194.98

Less set off Capital losses from past year 7000

Net capital Gain/loss for the year ended 30th June 150194.98

Interpretation

Taxable Capital Gain/Loss of the current year ended 30th June is taken out as $150194.98.

So, Capital Gain tax will be chargeable on this amount as per the ITAA 1997.

QUESTION 2

a. Advising Rapid-Heat about its fringe benefit tax

(A) An Electric Heaters Manufacturer Rapid-Heat Pty Ltd hires jasmine as employee of the

company and provide Fringe Benefits to her so in this question there is analysis of Fringe Benefits

provided by them under Fringe Benefits Tax Act 1986(Fringe Benefit Tax 2018).

Section 7 of FBTA states that car will be treated as for private use when any day car is not parked at

business premises and parked at home of employee (Scott, 2012). The definition of Car has been

given by the act-:

1. Goods Carrying capacity of vehicle should be less than 1 tone.

2. Vans, motor cars, station wagons or any utilities

3. Other Vehicle carrying passenger less than 9 occupants.

Section 9 of FBTA defines two methods for calculating Fringe Benefits, they are-:

1. Statutory Method-: States that there is no need to show actual value of cars in taxable

value.

2. Cost Method-: Where actual value of cars is shown as gross taxable value.

Section 9 also prescribes that any amount which has been paid as expense in respect of fuel

or repairs and documented evidence given by employee in holiday period will be borne by

employer(Rimmer,2014). Motor vehicle which has been gone for repairs and maintenance will not

been treated as private use.

9

Total capital gain will be after setting off collectables

are

157194.98

Less set off Capital losses from past year 7000

Net capital Gain/loss for the year ended 30th June 150194.98

Interpretation

Taxable Capital Gain/Loss of the current year ended 30th June is taken out as $150194.98.

So, Capital Gain tax will be chargeable on this amount as per the ITAA 1997.

QUESTION 2

a. Advising Rapid-Heat about its fringe benefit tax

(A) An Electric Heaters Manufacturer Rapid-Heat Pty Ltd hires jasmine as employee of the

company and provide Fringe Benefits to her so in this question there is analysis of Fringe Benefits

provided by them under Fringe Benefits Tax Act 1986(Fringe Benefit Tax 2018).

Section 7 of FBTA states that car will be treated as for private use when any day car is not parked at

business premises and parked at home of employee (Scott, 2012). The definition of Car has been

given by the act-:

1. Goods Carrying capacity of vehicle should be less than 1 tone.

2. Vans, motor cars, station wagons or any utilities

3. Other Vehicle carrying passenger less than 9 occupants.

Section 9 of FBTA defines two methods for calculating Fringe Benefits, they are-:

1. Statutory Method-: States that there is no need to show actual value of cars in taxable

value.

2. Cost Method-: Where actual value of cars is shown as gross taxable value.

Section 9 also prescribes that any amount which has been paid as expense in respect of fuel

or repairs and documented evidence given by employee in holiday period will be borne by

employer(Rimmer,2014). Motor vehicle which has been gone for repairs and maintenance will not

been treated as private use.

9

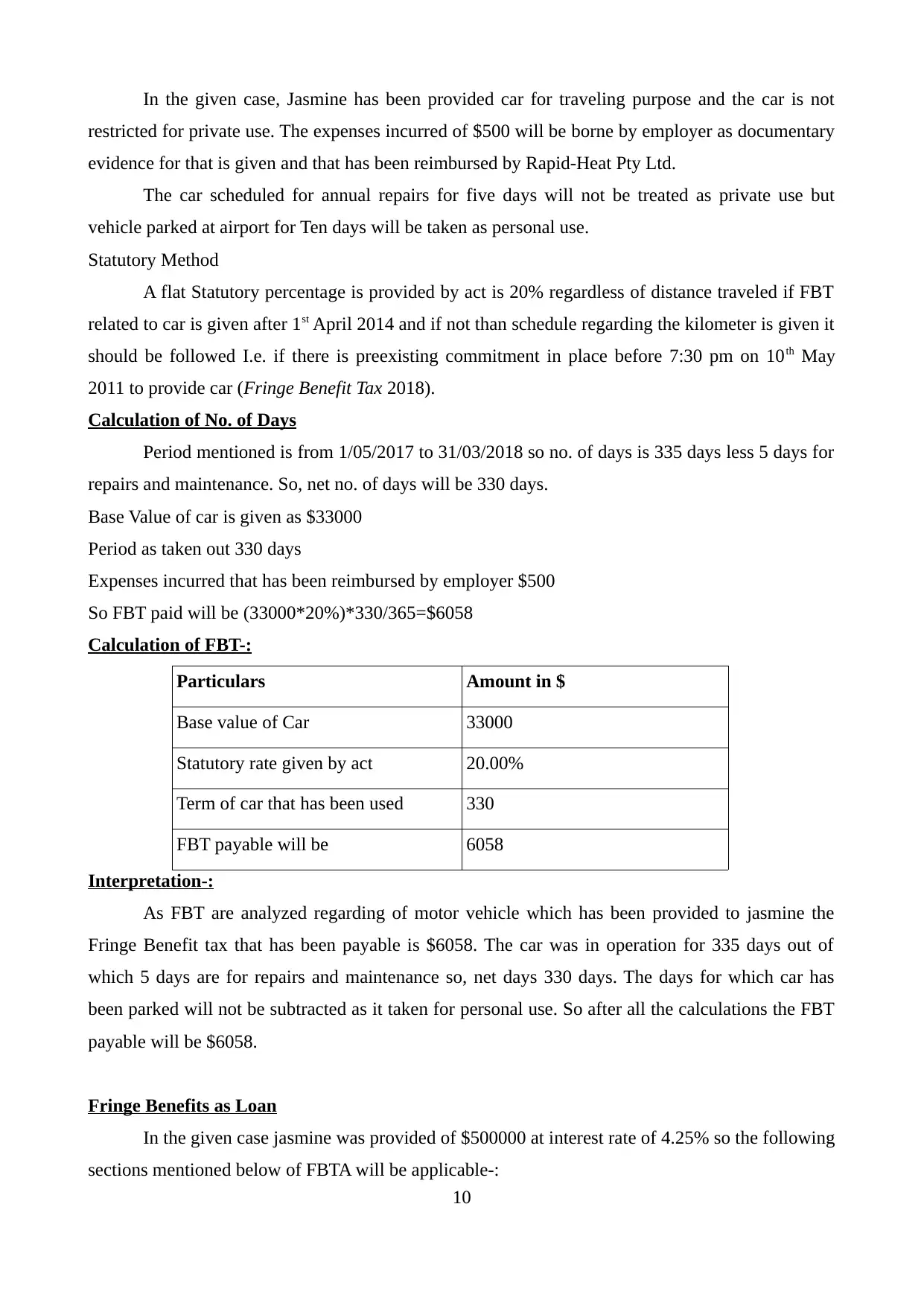

In the given case, Jasmine has been provided car for traveling purpose and the car is not

restricted for private use. The expenses incurred of $500 will be borne by employer as documentary

evidence for that is given and that has been reimbursed by Rapid-Heat Pty Ltd.

The car scheduled for annual repairs for five days will not be treated as private use but

vehicle parked at airport for Ten days will be taken as personal use.

Statutory Method

A flat Statutory percentage is provided by act is 20% regardless of distance traveled if FBT

related to car is given after 1st April 2014 and if not than schedule regarding the kilometer is given it

should be followed I.e. if there is preexisting commitment in place before 7:30 pm on 10th May

2011 to provide car (Fringe Benefit Tax 2018).

Calculation of No. of Days

Period mentioned is from 1/05/2017 to 31/03/2018 so no. of days is 335 days less 5 days for

repairs and maintenance. So, net no. of days will be 330 days.

Base Value of car is given as $33000

Period as taken out 330 days

Expenses incurred that has been reimbursed by employer $500

So FBT paid will be (33000*20%)*330/365=$6058

Calculation of FBT-:

Particulars Amount in $

Base value of Car 33000

Statutory rate given by act 20.00%

Term of car that has been used 330

FBT payable will be 6058

Interpretation-:

As FBT are analyzed regarding of motor vehicle which has been provided to jasmine the

Fringe Benefit tax that has been payable is $6058. The car was in operation for 335 days out of

which 5 days are for repairs and maintenance so, net days 330 days. The days for which car has

been parked will not be subtracted as it taken for personal use. So after all the calculations the FBT

payable will be $6058.

Fringe Benefits as Loan

In the given case jasmine was provided of $500000 at interest rate of 4.25% so the following

sections mentioned below of FBTA will be applicable-:

10

restricted for private use. The expenses incurred of $500 will be borne by employer as documentary

evidence for that is given and that has been reimbursed by Rapid-Heat Pty Ltd.

The car scheduled for annual repairs for five days will not be treated as private use but

vehicle parked at airport for Ten days will be taken as personal use.

Statutory Method

A flat Statutory percentage is provided by act is 20% regardless of distance traveled if FBT

related to car is given after 1st April 2014 and if not than schedule regarding the kilometer is given it

should be followed I.e. if there is preexisting commitment in place before 7:30 pm on 10th May

2011 to provide car (Fringe Benefit Tax 2018).

Calculation of No. of Days

Period mentioned is from 1/05/2017 to 31/03/2018 so no. of days is 335 days less 5 days for

repairs and maintenance. So, net no. of days will be 330 days.

Base Value of car is given as $33000

Period as taken out 330 days

Expenses incurred that has been reimbursed by employer $500

So FBT paid will be (33000*20%)*330/365=$6058

Calculation of FBT-:

Particulars Amount in $

Base value of Car 33000

Statutory rate given by act 20.00%

Term of car that has been used 330

FBT payable will be 6058

Interpretation-:

As FBT are analyzed regarding of motor vehicle which has been provided to jasmine the

Fringe Benefit tax that has been payable is $6058. The car was in operation for 335 days out of

which 5 days are for repairs and maintenance so, net days 330 days. The days for which car has

been parked will not be subtracted as it taken for personal use. So after all the calculations the FBT

payable will be $6058.

Fringe Benefits as Loan

In the given case jasmine was provided of $500000 at interest rate of 4.25% so the following

sections mentioned below of FBTA will be applicable-:

10

You're viewing a preview

Unlock full access by subscribing today!

Section 16 provides loan as a FBT wherein employer provides loan to their employee at some low

rates of interest other than statutory rates provided by the Reserve Bank of Australia(Burkhauser,

2015). The taxable value which is needed to be taken out of loan will be-:

1. Difference between amount calculated as interest if the statutory rates are applicable on the

outstanding daily balance of loan.

2. Any Accrued interest.

Section 16 also mentions that if any asset purchases by using loan doesn't generate any income than

FBT will be NIL (Fringe Benefit Tax 2018). For ex-: If loan taken for house purchase for residential

purpose will be free from FBT and if it has been rented and source of income started from that FBT

will be charged.

Interpretation-:

So, in the loan provided by Rapid-Heat of $500000 out of which $450000 has been

purchased for holiday home (assumed to be for residential purpose) and $50000 has been lent

interest free to her husband. So the FBT charged will be NIL as both the activities which are done

using loan doesn't generate any income.

Electric Heater

Calculation of FBT

Particulars Amount in $

Electric Heaters Sold to Jasmine(a) 1300

Cost to Rapid-Heat(b) 700

Sold in market(c) 2600

Loss in sale to jasmine d=c-(a+b) 600

FBT rate @ 47% 282

Interpretation

The heater is sold is less than market price as sold to general public so there is loss of $600.

So, FBT will be charged @47 % on $600 which is $282.

GST act 1999 defines that input tax credit will be available for things that are used for

business like motor car etc. (O'Connor, 2018). So here in the given question Car that is purchased is

for employee and expenses on that car is also for business purpose so company can claim Input

credit on both items.

11

rates of interest other than statutory rates provided by the Reserve Bank of Australia(Burkhauser,

2015). The taxable value which is needed to be taken out of loan will be-:

1. Difference between amount calculated as interest if the statutory rates are applicable on the

outstanding daily balance of loan.

2. Any Accrued interest.

Section 16 also mentions that if any asset purchases by using loan doesn't generate any income than

FBT will be NIL (Fringe Benefit Tax 2018). For ex-: If loan taken for house purchase for residential

purpose will be free from FBT and if it has been rented and source of income started from that FBT

will be charged.

Interpretation-:

So, in the loan provided by Rapid-Heat of $500000 out of which $450000 has been

purchased for holiday home (assumed to be for residential purpose) and $50000 has been lent

interest free to her husband. So the FBT charged will be NIL as both the activities which are done

using loan doesn't generate any income.

Electric Heater

Calculation of FBT

Particulars Amount in $

Electric Heaters Sold to Jasmine(a) 1300

Cost to Rapid-Heat(b) 700

Sold in market(c) 2600

Loss in sale to jasmine d=c-(a+b) 600

FBT rate @ 47% 282

Interpretation

The heater is sold is less than market price as sold to general public so there is loss of $600.

So, FBT will be charged @47 % on $600 which is $282.

GST act 1999 defines that input tax credit will be available for things that are used for

business like motor car etc. (O'Connor, 2018). So here in the given question Car that is purchased is

for employee and expenses on that car is also for business purpose so company can claim Input

credit on both items.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(B) Stating recommendation if Jasmine will use money for purchasing shares

If Jasmine has used $50000 for purchase of shares which is an income bearing asset so FBT

will be chargeable on interest of $50000.

The FBT that will be charged is mentioned below in the table-:

Particulars Amount

Interest rate charged 4.25%

Statutory Interest Rate as per Reserve Bank 5.50%

Difference between rates 1.25%

Days for which it will be charged

1st September 2017 to 31st March 2018

212 Days

Loan which is used for income bearing activities $50000

FBT Charged will be (50000*1.25%)212/365 $363

Interpretation

If loan will be used for income bearing activities, then FBT will be calculated for difference

in the statutory rates of interest and the rates provided by the company I.e. 1.25% for the days i.e.

212 which it has been used for that in fiscal year. So, the chargeable FBT will be $363.

CONCLUSION

In present scenario the economic growth has brought fast reforms in taxation system. The

above reports examine the process of defining the structure of tax payer by means of which taxable

income is acquired. This report will help in analyzing the assessable income of any individual or

organization. It consists the provision of capital gain, fringe benefit tax, income tax and analysis

with calculations of all of them as required by client.

12

If Jasmine has used $50000 for purchase of shares which is an income bearing asset so FBT

will be chargeable on interest of $50000.

The FBT that will be charged is mentioned below in the table-:

Particulars Amount

Interest rate charged 4.25%

Statutory Interest Rate as per Reserve Bank 5.50%

Difference between rates 1.25%

Days for which it will be charged

1st September 2017 to 31st March 2018

212 Days

Loan which is used for income bearing activities $50000

FBT Charged will be (50000*1.25%)212/365 $363

Interpretation

If loan will be used for income bearing activities, then FBT will be calculated for difference

in the statutory rates of interest and the rates provided by the company I.e. 1.25% for the days i.e.

212 which it has been used for that in fiscal year. So, the chargeable FBT will be $363.

CONCLUSION

In present scenario the economic growth has brought fast reforms in taxation system. The

above reports examine the process of defining the structure of tax payer by means of which taxable

income is acquired. This report will help in analyzing the assessable income of any individual or

organization. It consists the provision of capital gain, fringe benefit tax, income tax and analysis

with calculations of all of them as required by client.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.