Taxation Theory, Practice and Law

VerifiedAdded on 2023/01/13

|11

|2580

|36

AI Summary

This document provides an introduction to the Australian taxation system, focusing on income tax and capital gains. It includes explanations and calculations for assessable income, taxable income, and tax liabilities. It also discusses the tax implications of various scenarios, such as tips from customers, income from employment, gifts, and the sale of assets. The document is relevant for students studying taxation theory, practice, and law.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION THEORY,

PRACTICE AND LAW

PRACTICE AND LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

a) Tips from customers. ..............................................................................................................2

b) Income from employment.......................................................................................................2

c) Perfume received from customer ............................................................................................3

d) Entertainment event paid by restaurant owner........................................................................3

e) Christmas gift from father of $ 15000.....................................................................................4

Question 2 .......................................................................................................................................4

a) Sale of house............................................................................................................................5

b) Sale of Car ..............................................................................................................................6

c) Sale of Small business enterprise.............................................................................................6

d) Sale of furniture ......................................................................................................................7

e) Sale of paintings ......................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

a) Tips from customers. ..............................................................................................................2

b) Income from employment.......................................................................................................2

c) Perfume received from customer ............................................................................................3

d) Entertainment event paid by restaurant owner........................................................................3

e) Christmas gift from father of $ 15000.....................................................................................4

Question 2 .......................................................................................................................................4

a) Sale of house............................................................................................................................5

b) Sale of Car ..............................................................................................................................6

c) Sale of Small business enterprise.............................................................................................6

d) Sale of furniture ......................................................................................................................7

e) Sale of paintings ......................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Australian Taxation systems is one in the most complex tax systems in the world. It is

made of more than 125 tax including taxes like Capital gain, income tax, fringe benefit tax and

GST. There are number of organisations which are playing varied and different roles within the

system for ensuring integrity of taxation system, including equitable tax treatment of all the

Australians. Persons considering to become part of the Australian taxation system is required to

have detailed knowledge of system. The report will be addressing the concepts regarding the

income tax and capital gains of individual. Report will two questions for having more clear

understanding of the concepts of income tax system of Australia.

Question 1

Australian Taxation System

Taxation system of Australia relies heavily on the personal income tax. An individual

may receive income from working or from investment. Income may not be in monetary terms

like it may be in form of gifts or goods or services. Amounts received on winning prizes or gifts

usually do not form part of income. Income are classified into assessable, exempt and taxable.

Assessable income refers to income which could be taxed after crossing the threshold

limit. Examples of assessable income are ; salary & wages, gratitudes, tips or payments for

services, allowances by employer, interests on banks, dividends, bonuses, commission, pensions,

rent and like transactions (Mclaren and Passant, 2017).

Taxable income is defined as income on which tax is to be paid. It is the amount that is

left after claiming all the deductions for the expenses incurred from the assessable income.

Deductions are applied for reducing the taxable income and not over the tax liability.

The legislations governing the income tax of individuals & companies are Income Tax

Assessment Act, 1936 (ITAA, 1936) and Income Tax Assessment Act,1997 (ITAA, 1997) and

Fringe Benefits Tax Assessment Act, 1986. Capital gain taxation rules and provisions are include

in ITAA 97.

Assessable Income of Emmi

1

Australian Taxation systems is one in the most complex tax systems in the world. It is

made of more than 125 tax including taxes like Capital gain, income tax, fringe benefit tax and

GST. There are number of organisations which are playing varied and different roles within the

system for ensuring integrity of taxation system, including equitable tax treatment of all the

Australians. Persons considering to become part of the Australian taxation system is required to

have detailed knowledge of system. The report will be addressing the concepts regarding the

income tax and capital gains of individual. Report will two questions for having more clear

understanding of the concepts of income tax system of Australia.

Question 1

Australian Taxation System

Taxation system of Australia relies heavily on the personal income tax. An individual

may receive income from working or from investment. Income may not be in monetary terms

like it may be in form of gifts or goods or services. Amounts received on winning prizes or gifts

usually do not form part of income. Income are classified into assessable, exempt and taxable.

Assessable income refers to income which could be taxed after crossing the threshold

limit. Examples of assessable income are ; salary & wages, gratitudes, tips or payments for

services, allowances by employer, interests on banks, dividends, bonuses, commission, pensions,

rent and like transactions (Mclaren and Passant, 2017).

Taxable income is defined as income on which tax is to be paid. It is the amount that is

left after claiming all the deductions for the expenses incurred from the assessable income.

Deductions are applied for reducing the taxable income and not over the tax liability.

The legislations governing the income tax of individuals & companies are Income Tax

Assessment Act, 1936 (ITAA, 1936) and Income Tax Assessment Act,1997 (ITAA, 1997) and

Fringe Benefits Tax Assessment Act, 1986. Capital gain taxation rules and provisions are include

in ITAA 97.

Assessable Income of Emmi

1

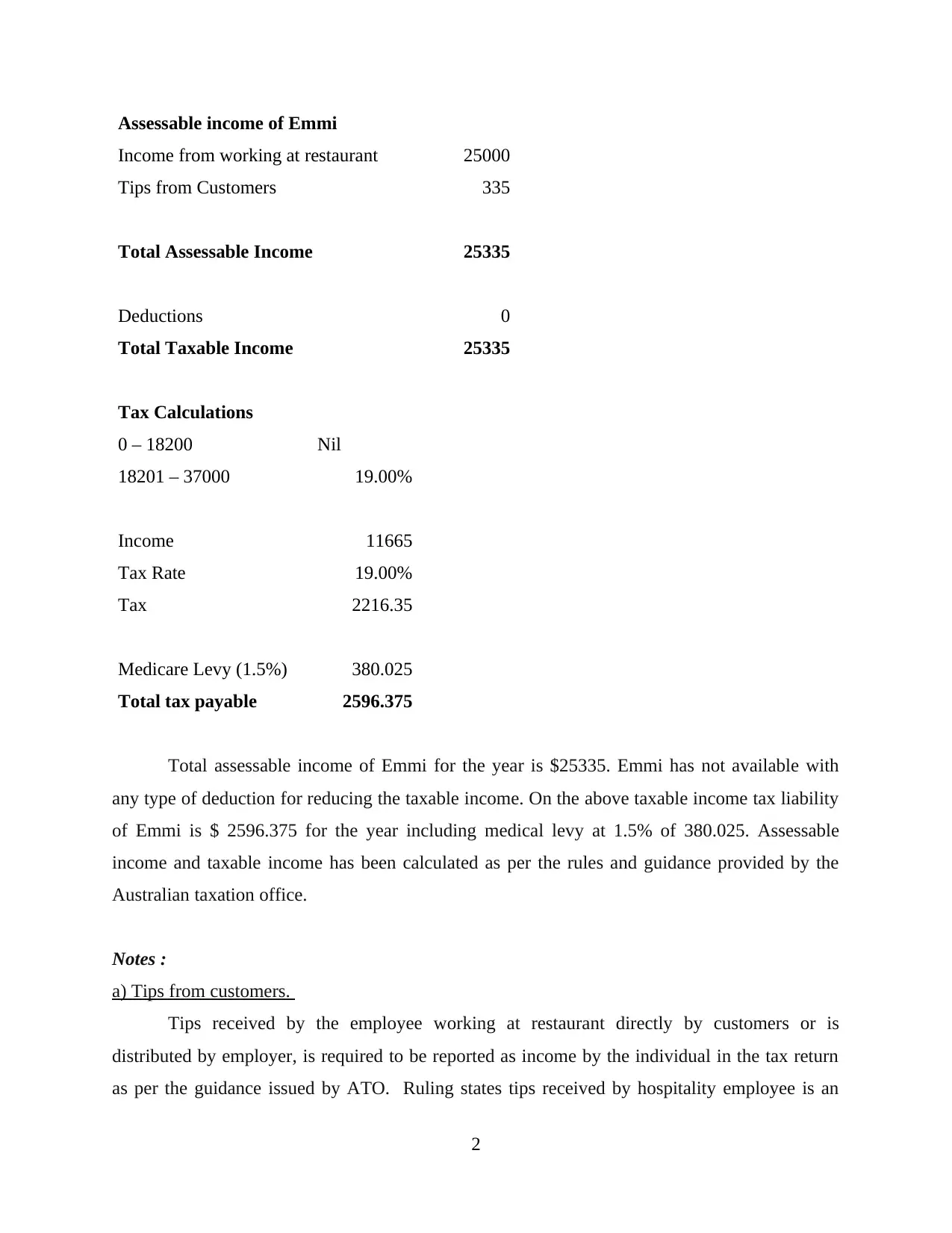

Assessable income of Emmi

Income from working at restaurant 25000

Tips from Customers 335

Total Assessable Income 25335

Deductions 0

Total Taxable Income 25335

Tax Calculations

0 – 18200 Nil

18201 – 37000 19.00%

Income 11665

Tax Rate 19.00%

Tax 2216.35

Medicare Levy (1.5%) 380.025

Total tax payable 2596.375

Total assessable income of Emmi for the year is $25335. Emmi has not available with

any type of deduction for reducing the taxable income. On the above taxable income tax liability

of Emmi is $ 2596.375 for the year including medical levy at 1.5% of 380.025. Assessable

income and taxable income has been calculated as per the rules and guidance provided by the

Australian taxation office.

Notes :

a) Tips from customers.

Tips received by the employee working at restaurant directly by customers or is

distributed by employer, is required to be reported as income by the individual in the tax return

as per the guidance issued by ATO. Ruling states tips received by hospitality employee is an

2

Income from working at restaurant 25000

Tips from Customers 335

Total Assessable Income 25335

Deductions 0

Total Taxable Income 25335

Tax Calculations

0 – 18200 Nil

18201 – 37000 19.00%

Income 11665

Tax Rate 19.00%

Tax 2216.35

Medicare Levy (1.5%) 380.025

Total tax payable 2596.375

Total assessable income of Emmi for the year is $25335. Emmi has not available with

any type of deduction for reducing the taxable income. On the above taxable income tax liability

of Emmi is $ 2596.375 for the year including medical levy at 1.5% of 380.025. Assessable

income and taxable income has been calculated as per the rules and guidance provided by the

Australian taxation office.

Notes :

a) Tips from customers.

Tips received by the employee working at restaurant directly by customers or is

distributed by employer, is required to be reported as income by the individual in the tax return

as per the guidance issued by ATO. Ruling states tips received by hospitality employee is an

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

assessable income as per para 26(e) of Act. The tips amounting to $335 for the year by Emmi is

assessable under income tax and tax is required to be paid.

b) Income from employment.

Income received from employment is taxable as per section 15 of ITAA '1997. Tax is to

be paid after the amount exceeds threshold limit of $18200. Emmi is required to pay tax over the

income received as result of working at restaurant and this is assessable income of Emmi as per

the Australian taxation office. If the individual has to pay tax even if the income is generated

from working at two jobs separately (Chau and Butler, 2017). The threshold limit is to be

deducted by the employer paying highest salary. Since she works only at restaurant her taxable

income will be deducted on this income only. She is not required to pay tax upto limit of $18200.

c) Perfume received from customer

Perfume received by Emmi from customer is tax free as it is paid out of gratitude by

customer. Perfume worth $ 250 has been gifted on Christmas occasion is exempt and will not be

forming party of the assessable income of individual. The gift is not received from employer and

is not more than the threshold limit. As per the ITAA 1997 and Australian taxation office gifts

are exempt and are not assessable in the income tax return of the employee. Emmi gifted the

same perfume to her mother. Deductions cannot be claimed by Emmi for gift as she had not

incurred expenses for the purchase of perfume and also the gift is not paid to charity. Deductions

would be available if Emmi had incurred expenses and was for charitable purpose. Gifting the

perfume to mother does not amounts to donation.

d) Entertainment event paid by restaurant owner

Fringe benefits are the benefits that are received in addition to wages and salary of

employees as per Section 32 of ITAA 1997. It is benefit provided to employee in respect of

employment by the employer. As per the income tax act if the fringe benefits are less than $

2000 employee is not required to report this in the income tax return. Fringe benefits are taxable

if total taxable values of the fringe benefits provided by the employer are exceeding $2000. On

the other hand if the events fees paid by the employer is entertainment gift than it will be exempt

from FBT if below $300. FBT are taxed separately from the income tax. Emmi would be

3

assessable under income tax and tax is required to be paid.

b) Income from employment.

Income received from employment is taxable as per section 15 of ITAA '1997. Tax is to

be paid after the amount exceeds threshold limit of $18200. Emmi is required to pay tax over the

income received as result of working at restaurant and this is assessable income of Emmi as per

the Australian taxation office. If the individual has to pay tax even if the income is generated

from working at two jobs separately (Chau and Butler, 2017). The threshold limit is to be

deducted by the employer paying highest salary. Since she works only at restaurant her taxable

income will be deducted on this income only. She is not required to pay tax upto limit of $18200.

c) Perfume received from customer

Perfume received by Emmi from customer is tax free as it is paid out of gratitude by

customer. Perfume worth $ 250 has been gifted on Christmas occasion is exempt and will not be

forming party of the assessable income of individual. The gift is not received from employer and

is not more than the threshold limit. As per the ITAA 1997 and Australian taxation office gifts

are exempt and are not assessable in the income tax return of the employee. Emmi gifted the

same perfume to her mother. Deductions cannot be claimed by Emmi for gift as she had not

incurred expenses for the purchase of perfume and also the gift is not paid to charity. Deductions

would be available if Emmi had incurred expenses and was for charitable purpose. Gifting the

perfume to mother does not amounts to donation.

d) Entertainment event paid by restaurant owner

Fringe benefits are the benefits that are received in addition to wages and salary of

employees as per Section 32 of ITAA 1997. It is benefit provided to employee in respect of

employment by the employer. As per the income tax act if the fringe benefits are less than $

2000 employee is not required to report this in the income tax return. Fringe benefits are taxable

if total taxable values of the fringe benefits provided by the employer are exceeding $2000. On

the other hand if the events fees paid by the employer is entertainment gift than it will be exempt

from FBT if below $300. FBT are taxed separately from the income tax. Emmi would be

3

required to pay FBT over the events meals fee of $385 is an entertainment gift from owner.

However, this will not form part of the assessable income of Emmi (Fringe Benefit Tax

Assessment Act 1986, 2019).

e) Christmas gift from father of $ 15000.

Giving away of money is not taxable event for recipient. Income or gains generated on

sale of monetary gifts are taxable. Monetary gifts from parents do not form part of the assessable

income on following conditions or circumstances.

Provided gift out of love and affection for financial support.

Gift is provided individually or may be with spouse.

Gift is given voluntary.

Gift is not having connection with income producing activities for person.

Gifts are sourced from the funds beneficially owned by the parents.

Provided these gift of $15000 do not have any connection with income producing activities.

Therefore cash gift of $15000 will not be forming part of the assessable income of Emmi as it is

given on occasion of Christmas out of love and affection as per Section 30 of ITAA 1997(Gifts

and Contributions, 2019).

Question 2

Capital gain refers to difference between the price paid for an asset and the consideration

received on sale. As per Australian CGT levy on gain is to be paid in year when the asset is

disposed. Capital gain tax applies to contractual rights, shares, licences, personal collectables,

real estate and many more. Capital gains or losses are required to be reported on the income tax

returns of the individual. It forms part of income and is not charged separately. Individual can

claim the capital losses only against the capital and not over any other income . All the assets

that are acquired after the capital gain tax was started ( 20 September 1985) attract the CGT

unless excluded specifically.

4

However, this will not form part of the assessable income of Emmi (Fringe Benefit Tax

Assessment Act 1986, 2019).

e) Christmas gift from father of $ 15000.

Giving away of money is not taxable event for recipient. Income or gains generated on

sale of monetary gifts are taxable. Monetary gifts from parents do not form part of the assessable

income on following conditions or circumstances.

Provided gift out of love and affection for financial support.

Gift is provided individually or may be with spouse.

Gift is given voluntary.

Gift is not having connection with income producing activities for person.

Gifts are sourced from the funds beneficially owned by the parents.

Provided these gift of $15000 do not have any connection with income producing activities.

Therefore cash gift of $15000 will not be forming part of the assessable income of Emmi as it is

given on occasion of Christmas out of love and affection as per Section 30 of ITAA 1997(Gifts

and Contributions, 2019).

Question 2

Capital gain refers to difference between the price paid for an asset and the consideration

received on sale. As per Australian CGT levy on gain is to be paid in year when the asset is

disposed. Capital gain tax applies to contractual rights, shares, licences, personal collectables,

real estate and many more. Capital gains or losses are required to be reported on the income tax

returns of the individual. It forms part of income and is not charged separately. Individual can

claim the capital losses only against the capital and not over any other income . All the assets

that are acquired after the capital gain tax was started ( 20 September 1985) attract the CGT

unless excluded specifically.

4

Personal assets are mostly exempted from the CGT like home car, assets for personal use

like furniture. CGT also do not apply over the depreciating assets which are solely used for the

taxable purpose like business equipments or the fittings of rental property. CGT event arise when

the capital asset is sold (Brydges, 2019). However taxation department also provides for the

exemptions over capital gains. Guide to Capital gains tax for 2019 provides for the capital gains

tax works that will help in calculating the capital gains tax. The capital gains tax are covered

under ITAA 1997 division 100 Chapter 3. Section 100 & 102 of the Act governs the provisions

related to Capital gain.

There are two methods for working out capital gains for the assets that are Discounting

method where the 50% of the gain is exempt after providing for the capital losses this method is

applicable if assets acquired are held for more than 12 months before CGT event. . Other method

is indexation method where is cost base is calculated using CPI index rates. This is applicable for

assets acquired before 21 September 1999.

Liu is an Australian resident aged 65 is retiring from business and is selling all its Australian

assets.

a) Sale of house

On selling the house which was purchased in 1981 at $ 55000 at $ 630000 will attract

capital gain event. The property is acquired before 1985 therefore it is eligible for the indexation

method of calculating tax. Section 112 of ITAA 1997 provides for indexation of cost base. The

indexation will be made only considering CPI of 1999 and not of 1981. On calculating the

indexation factor the cost base of house comes to $156716. It is used as the increased cost base

for calculating the capital gain on house. Capital gain will be taxable as the part of taxable

income of Liu as per the Australian taxation office (CGT event, 2019).

Sale of House

CPI 2019 115.4

CPI September 1999 40.5

Indexation factor 2.849

5

like furniture. CGT also do not apply over the depreciating assets which are solely used for the

taxable purpose like business equipments or the fittings of rental property. CGT event arise when

the capital asset is sold (Brydges, 2019). However taxation department also provides for the

exemptions over capital gains. Guide to Capital gains tax for 2019 provides for the capital gains

tax works that will help in calculating the capital gains tax. The capital gains tax are covered

under ITAA 1997 division 100 Chapter 3. Section 100 & 102 of the Act governs the provisions

related to Capital gain.

There are two methods for working out capital gains for the assets that are Discounting

method where the 50% of the gain is exempt after providing for the capital losses this method is

applicable if assets acquired are held for more than 12 months before CGT event. . Other method

is indexation method where is cost base is calculated using CPI index rates. This is applicable for

assets acquired before 21 September 1999.

Liu is an Australian resident aged 65 is retiring from business and is selling all its Australian

assets.

a) Sale of house

On selling the house which was purchased in 1981 at $ 55000 at $ 630000 will attract

capital gain event. The property is acquired before 1985 therefore it is eligible for the indexation

method of calculating tax. Section 112 of ITAA 1997 provides for indexation of cost base. The

indexation will be made only considering CPI of 1999 and not of 1981. On calculating the

indexation factor the cost base of house comes to $156716. It is used as the increased cost base

for calculating the capital gain on house. Capital gain will be taxable as the part of taxable

income of Liu as per the Australian taxation office (CGT event, 2019).

Sale of House

CPI 2019 115.4

CPI September 1999 40.5

Indexation factor 2.849

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost base 55000

Indexation factor 2.849

Indexation cost base 156716.049

Sales proceeds 630000

Indexed cost base 156716.049

Capital gain 473283.951

b) Sale of Car

Liu owned a car costing $37000 which is now valued only $8000. In the present case car

for personal use are covered under the personal assets of an individual. As the guidance provided

by the Australian Taxation Office car used for personal purpose is exempt from capital gain tax.

Also the loss over personal assets is allowed for deductions under capital losses as the assets are

exempt (Exemptions, 2019) .

c) Sale of Small business enterprise

Small business is business if it has turnover below 2 million. Business may avail the

benefit under the CGT Exemptions and concessions for small business. There are four

conditions that may allow to defer capital gains. Concessions are ; 15 year exemption , 50%

active assets reduction, retirement exemption and roll-over (Peiros and Smyth, 2017). There also

other eligibility conditions that are required to be satisfied. Since the photograph do not satisfy

the conditions for active assets. If the photograph equipments are hold for more than 7.5 years

than concession may be held. Liu may measure the capital gains separately over the photograph

equipments and goodwill. Capital loss over the photograph equipments may claim capital

deductions. Goodwill is treated separately. There are many issues held regarding the sale of

Goodwill. As per Taxation Ruling 1996 goodwill of business is taxable (Taxation Ruling

1999/16, 2019).

6

Indexation factor 2.849

Indexation cost base 156716.049

Sales proceeds 630000

Indexed cost base 156716.049

Capital gain 473283.951

b) Sale of Car

Liu owned a car costing $37000 which is now valued only $8000. In the present case car

for personal use are covered under the personal assets of an individual. As the guidance provided

by the Australian Taxation Office car used for personal purpose is exempt from capital gain tax.

Also the loss over personal assets is allowed for deductions under capital losses as the assets are

exempt (Exemptions, 2019) .

c) Sale of Small business enterprise

Small business is business if it has turnover below 2 million. Business may avail the

benefit under the CGT Exemptions and concessions for small business. There are four

conditions that may allow to defer capital gains. Concessions are ; 15 year exemption , 50%

active assets reduction, retirement exemption and roll-over (Peiros and Smyth, 2017). There also

other eligibility conditions that are required to be satisfied. Since the photograph do not satisfy

the conditions for active assets. If the photograph equipments are hold for more than 7.5 years

than concession may be held. Liu may measure the capital gains separately over the photograph

equipments and goodwill. Capital loss over the photograph equipments may claim capital

deductions. Goodwill is treated separately. There are many issues held regarding the sale of

Goodwill. As per Taxation Ruling 1996 goodwill of business is taxable (Taxation Ruling

1999/16, 2019).

6

Sale of Business

Sale consideration 125000

Photography equipments 53000

Cost base 63000

Capital loss -10000

Goodwill 50000

Capital gain 50000

50% Discount 25000

less capital loss -10000

Taxable Capital gain 15000

d) Sale of furniture

Australian taxation has provided guidelines regarding the furniture. The furniture used for

personal purpose are exempts from capital gains. Individual is not required to report gains over

the personal assets at the same time capital losses also cannot be claimed over the exempt assets.

The selling price is not considered since the furniture is exempt asset. Section 108 of ITAA 1997

provides for personal use assets. (CGT Exemptions, 2019) .

e) Sale of paintings

Paintings are covered under the collectables of the individuals. ATO provides for the

exemption of collectables. Department provides for the exemptions if the single painting is not

purchased for more than $ 500. Liu among the paintings purchased one painting costing $1000

and it was sold for $8000 this attract the capital gain tax. Liu except the one painting is not

required to pay capital tax as all other paintings are exempt. The tax office provides that loss

over collectable sis allowed for deduction against capital gain of other collectables. (Section 108

of ITAA 1997). (Australian Taxation Office, 2019).

7

Sale consideration 125000

Photography equipments 53000

Cost base 63000

Capital loss -10000

Goodwill 50000

Capital gain 50000

50% Discount 25000

less capital loss -10000

Taxable Capital gain 15000

d) Sale of furniture

Australian taxation has provided guidelines regarding the furniture. The furniture used for

personal purpose are exempts from capital gains. Individual is not required to report gains over

the personal assets at the same time capital losses also cannot be claimed over the exempt assets.

The selling price is not considered since the furniture is exempt asset. Section 108 of ITAA 1997

provides for personal use assets. (CGT Exemptions, 2019) .

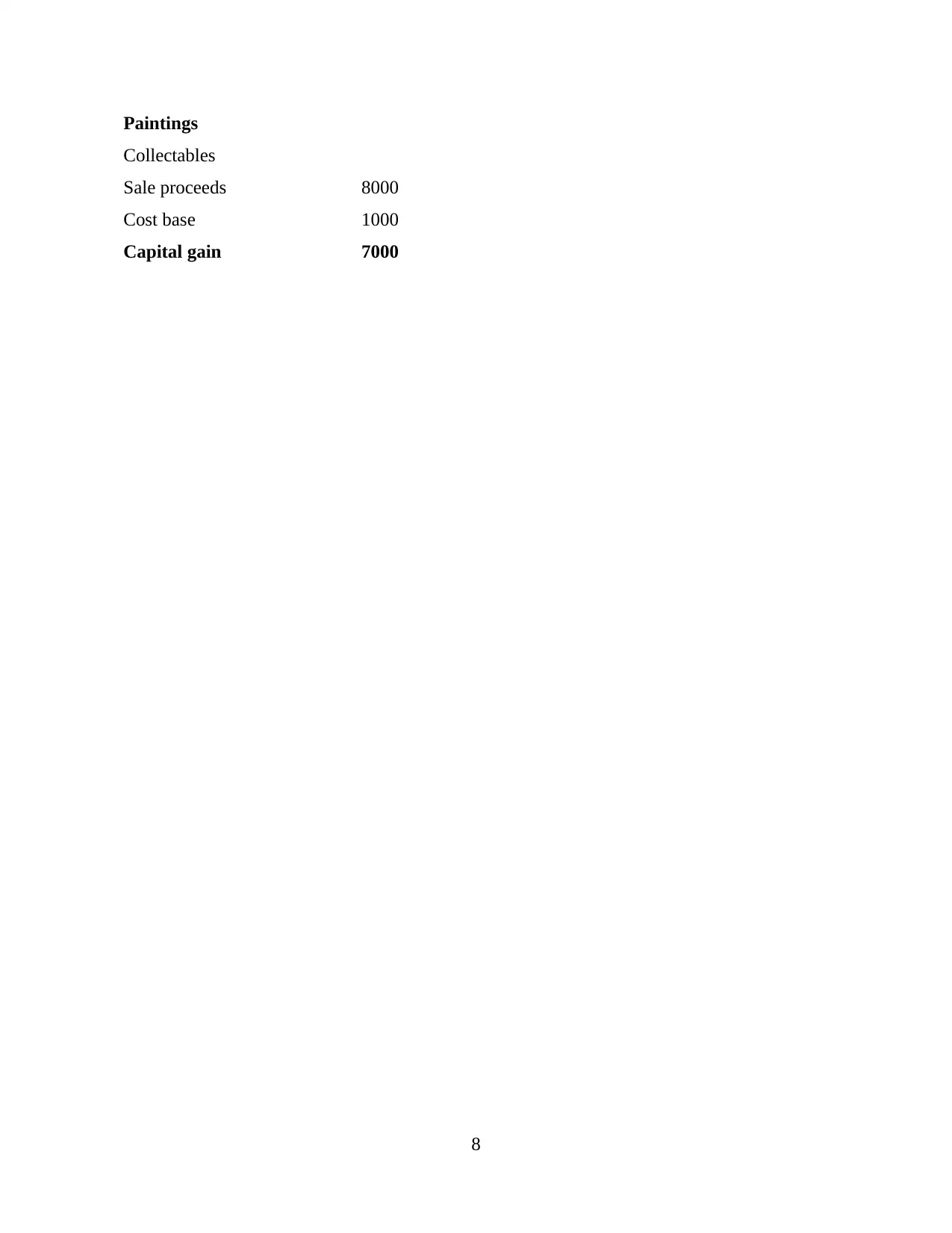

e) Sale of paintings

Paintings are covered under the collectables of the individuals. ATO provides for the

exemption of collectables. Department provides for the exemptions if the single painting is not

purchased for more than $ 500. Liu among the paintings purchased one painting costing $1000

and it was sold for $8000 this attract the capital gain tax. Liu except the one painting is not

required to pay capital tax as all other paintings are exempt. The tax office provides that loss

over collectable sis allowed for deduction against capital gain of other collectables. (Section 108

of ITAA 1997). (Australian Taxation Office, 2019).

7

Paintings

Collectables

Sale proceeds 8000

Cost base 1000

Capital gain 7000

8

Collectables

Sale proceeds 8000

Cost base 1000

Capital gain 7000

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Mclaren, J. and Passant, J., 2017. Leasehold property and the deductibiIity of stamp

duty. Australian Tax Law Bulletin.4(3).pp.44-46.

Chau, G. and Butler, D., 2017. Fundamentals of the proportioning rule. Taxation in

Australia.52(2). p.87.

Brydges, N., 2019. Residency of a trust: Don't get it wrong. Taxation in Australia, 54(2), p.90.

Peiros, K. and Smyth, C., 2017. Successful succession: Tax treatment of executor's

commission. Taxation in Australia.51(7). p.394.

Online

Australian Taxation Office. 2019. [Online]. Available through :

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>.

Taxation Ruling 1999/16. 2019. [Online]. Available through :

<https://www.ato.gov.au/law/view/document?Docid=TXR/TR199916/NAT/ATO/

00001&PiT=99991231235958>.

Exemptions. 2019. [Online]. Available through : <https://www.ato.gov.au/general/capital-gains-

tax/cgt-assets-and-exemptions/>.

Gifts and Contributions. 2019.[Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s30.15.html>.

Fringe Benefit Tax Assessment Act 1986. 2019. [Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s32.20.html>.

CGT event. 2019. [Online]. Available through : <https://www.ato.gov.au/Individuals/Tax-

return/2019/Supplementary-tax-return/Income-questions-13-24/18-Capital-gains-2019/>.

9

Books and Journals

Mclaren, J. and Passant, J., 2017. Leasehold property and the deductibiIity of stamp

duty. Australian Tax Law Bulletin.4(3).pp.44-46.

Chau, G. and Butler, D., 2017. Fundamentals of the proportioning rule. Taxation in

Australia.52(2). p.87.

Brydges, N., 2019. Residency of a trust: Don't get it wrong. Taxation in Australia, 54(2), p.90.

Peiros, K. and Smyth, C., 2017. Successful succession: Tax treatment of executor's

commission. Taxation in Australia.51(7). p.394.

Online

Australian Taxation Office. 2019. [Online]. Available through :

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>.

Taxation Ruling 1999/16. 2019. [Online]. Available through :

<https://www.ato.gov.au/law/view/document?Docid=TXR/TR199916/NAT/ATO/

00001&PiT=99991231235958>.

Exemptions. 2019. [Online]. Available through : <https://www.ato.gov.au/general/capital-gains-

tax/cgt-assets-and-exemptions/>.

Gifts and Contributions. 2019.[Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s30.15.html>.

Fringe Benefit Tax Assessment Act 1986. 2019. [Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s32.20.html>.

CGT event. 2019. [Online]. Available through : <https://www.ato.gov.au/Individuals/Tax-

return/2019/Supplementary-tax-return/Income-questions-13-24/18-Capital-gains-2019/>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.