University Taxation Advice: Asset Sales and Fringe Benefits Analysis

VerifiedAdded on 2023/06/05

|13

|2785

|333

Homework Assignment

AI Summary

This assignment analyzes the taxation implications of various asset sales and fringe benefits. The first part focuses on providing tax advice regarding asset sales, differentiating between revenue and capital receipts, and calculating capital gains tax (CGT) liabilities. It considers CGT exemptions for pre-CGT assets, collectables, and items of personal use, and details the process of computing taxable capital gains, including cost base calculations, capital losses, and the application of indexation or discount methods. The second part examines fringe benefits tax (FBT) implications, specifically addressing car fringe benefits, loan fringe benefits, and internal expense fringe benefits. It outlines the relevant legislation and provides calculations for each type of benefit, including taxable value and FBT liability. The assignment applies these principles to specific scenarios involving asset sales and employee benefits, providing a comprehensive overview of the relevant tax laws and calculations.

Taxation Theory, Practice & Law

Student Name

[Pick the date]

Student Name

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

Issue

The key objective is to outline tax related advice for the client on the backdrop of various asset

sale that have been concluded in the given tax year. In this regards, the given information would

be utilised so as to hint at the potential tax burden on the client.

Law

Receipts Nature

Whenever a taxpayer receives some cash, the pivotal concern from the tax perspective is to label

these proceeds either within the category or revenue or capital. These two are possible and the

precise determination of the correct nature of the proceeds would require consideration to the

underlying circumstances and taxpayer motive. An example of this could be provided through

the property sale which if done by builder would result in revenue receipts while the same

transaction if done by investor would result in capital receipts (Woellner, 2017). Thus, a key

understanding derived from the above example is that revenue receipts are essentially obtained

when the underlying taxpayer is involved in normal business activity. The tax treatment to the

two types of proceeds shows significant difference with revenue receipts contributing to

assessable income while capital receipts being tax exempted. However, any capital gains or

capital losses linked with capital proceeds would attract Capital Gains Tax (CGT) (Nethercott,

Richardson and Devos, 2016).

CGT Exempt Assets

A blanket exemption of CGT can be availed if the underlying asset is part of pre-CGT asset. A

unifying character of these assets is these have been acquired at a time when the Australian

government had not decided to tax the capital gains or losses (Coleman, 2016). Since, no CGT

was applicable at the time of acquisition of these assets, hence even today these assets would be

considered CGT exempt. The date on which CGT was enforced is September 20, 1985 and hence

it automatically becomes the cut-off date to decide the pre-CGT assets (Hodgson, Mortimer and

Butler, 2016).

1

Issue

The key objective is to outline tax related advice for the client on the backdrop of various asset

sale that have been concluded in the given tax year. In this regards, the given information would

be utilised so as to hint at the potential tax burden on the client.

Law

Receipts Nature

Whenever a taxpayer receives some cash, the pivotal concern from the tax perspective is to label

these proceeds either within the category or revenue or capital. These two are possible and the

precise determination of the correct nature of the proceeds would require consideration to the

underlying circumstances and taxpayer motive. An example of this could be provided through

the property sale which if done by builder would result in revenue receipts while the same

transaction if done by investor would result in capital receipts (Woellner, 2017). Thus, a key

understanding derived from the above example is that revenue receipts are essentially obtained

when the underlying taxpayer is involved in normal business activity. The tax treatment to the

two types of proceeds shows significant difference with revenue receipts contributing to

assessable income while capital receipts being tax exempted. However, any capital gains or

capital losses linked with capital proceeds would attract Capital Gains Tax (CGT) (Nethercott,

Richardson and Devos, 2016).

CGT Exempt Assets

A blanket exemption of CGT can be availed if the underlying asset is part of pre-CGT asset. A

unifying character of these assets is these have been acquired at a time when the Australian

government had not decided to tax the capital gains or losses (Coleman, 2016). Since, no CGT

was applicable at the time of acquisition of these assets, hence even today these assets would be

considered CGT exempt. The date on which CGT was enforced is September 20, 1985 and hence

it automatically becomes the cut-off date to decide the pre-CGT assets (Hodgson, Mortimer and

Butler, 2016).

1

While the above exemption is quite broad in scope considering that it applies to all possible

assets, there are specific exemptions available for certain particular asset type. The first

noteworthy exemption is for the class of assets known as collectables (s. 118-10) where for CGT

to apply, the minimum purchase price must be higher than $ 500 (Krever, 2017). Another

noteworthy exemption is for the class of assets known as items of personal use (s. 108-20(1))

where for CGT to apply, the minimum purchase price must be higher than $ 10,000. Failure on

the part of respective assets to comply with these thresholds would result in CGT exemption

without any regards to the underlying gains and holding period (Gilders, et. al., 2015).

Taxable capital gains

For the computation of the CGT liability, the critical aspect is to compute the net capital gains

that are taxable.

In order to arrive at the net capital gains, a series of steps ought to be adhered to. The beginning

of the process is done with the occurrence of a CGT event. There are several possible CGT

events as per s. 104-5 but A1 CGT event is relevant for the discussion in this case. The

identification of the appropriate capital event is also essential since there is an attached

computation methodology of capital gains with each event (Sadiq, et.al., 2015).

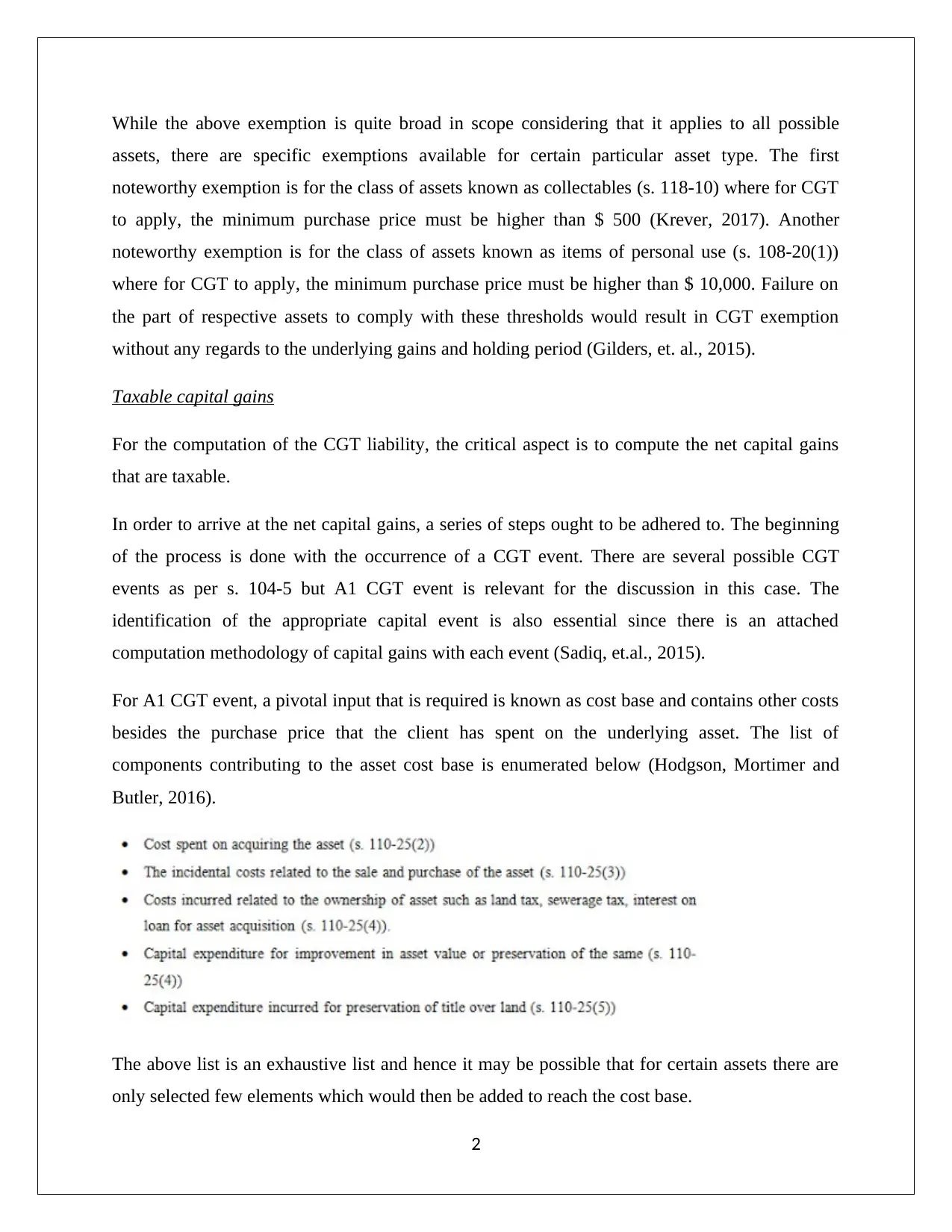

For A1 CGT event, a pivotal input that is required is known as cost base and contains other costs

besides the purchase price that the client has spent on the underlying asset. The list of

components contributing to the asset cost base is enumerated below (Hodgson, Mortimer and

Butler, 2016).

The above list is an exhaustive list and hence it may be possible that for certain assets there are

only selected few elements which would then be added to reach the cost base.

2

assets, there are specific exemptions available for certain particular asset type. The first

noteworthy exemption is for the class of assets known as collectables (s. 118-10) where for CGT

to apply, the minimum purchase price must be higher than $ 500 (Krever, 2017). Another

noteworthy exemption is for the class of assets known as items of personal use (s. 108-20(1))

where for CGT to apply, the minimum purchase price must be higher than $ 10,000. Failure on

the part of respective assets to comply with these thresholds would result in CGT exemption

without any regards to the underlying gains and holding period (Gilders, et. al., 2015).

Taxable capital gains

For the computation of the CGT liability, the critical aspect is to compute the net capital gains

that are taxable.

In order to arrive at the net capital gains, a series of steps ought to be adhered to. The beginning

of the process is done with the occurrence of a CGT event. There are several possible CGT

events as per s. 104-5 but A1 CGT event is relevant for the discussion in this case. The

identification of the appropriate capital event is also essential since there is an attached

computation methodology of capital gains with each event (Sadiq, et.al., 2015).

For A1 CGT event, a pivotal input that is required is known as cost base and contains other costs

besides the purchase price that the client has spent on the underlying asset. The list of

components contributing to the asset cost base is enumerated below (Hodgson, Mortimer and

Butler, 2016).

The above list is an exhaustive list and hence it may be possible that for certain assets there are

only selected few elements which would then be added to reach the cost base.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Using the cost base computed for the asset along with the selling price, capital gains or

associated losses may be computed (Barkoczy, 2017). However, these needs to be capital losses

related adjustment as the capital losses cannot be balanced against taxable income and instead

can be adjusted only against capital gains (s. 102-5). These capital losses would comprise of both

current year losses as well as past year capital losses. Capital losses do not expire and can be

carried forward year on year till they are adjusted against the available capital gains (Deutsch,

et.al., 2015).

Post the process, concessions in capital gains need to be provided using either the indexation

approach or discount approach. The latter is more popular especially when the capital gains are

high since the underlying discount is higher. The indexation approach has limitations in terms of

being useful for assets bought prior to 1999 with limited utility for those assets born post 1999.

The discount method does not suffer from this demerit. It allows for a 50 % decline in the

capital gains value before the same is subject to CGT (Coleman, 2016).

The only condition to be met for application of this discount is that the asset should have been

held by the taxpayer for a time period in excess of one year. Only then would the capital gains be

long term or else these would be short term. The net capital gains arrived after application of

concession using appropriate approach would then be levied CGT and determine the net tax

payable for the taxpayer (Gilders, et. al., 2015).

Timing aspect in CGT

In certain cases, a unique problem may arise due to the innate timing gap between the date on

which the contract for asset sale is executed and the date on which the related proceeds are

gained by the seller of the asset (Barkoczy, 2017). Hence, in such cases, problem arises with

regards to the correct tax year when the tax implications of the capital asset must be included. In

this context, TR 94/29 provides resolution of the situation by highlighting that irrespective of the

timing of the proceeds, the tax implications must be captured in the tax returns of the same year

when the sale contract regarding the asset is enacted (Reuters, 2017).

Application

Receipts Nature

3

associated losses may be computed (Barkoczy, 2017). However, these needs to be capital losses

related adjustment as the capital losses cannot be balanced against taxable income and instead

can be adjusted only against capital gains (s. 102-5). These capital losses would comprise of both

current year losses as well as past year capital losses. Capital losses do not expire and can be

carried forward year on year till they are adjusted against the available capital gains (Deutsch,

et.al., 2015).

Post the process, concessions in capital gains need to be provided using either the indexation

approach or discount approach. The latter is more popular especially when the capital gains are

high since the underlying discount is higher. The indexation approach has limitations in terms of

being useful for assets bought prior to 1999 with limited utility for those assets born post 1999.

The discount method does not suffer from this demerit. It allows for a 50 % decline in the

capital gains value before the same is subject to CGT (Coleman, 2016).

The only condition to be met for application of this discount is that the asset should have been

held by the taxpayer for a time period in excess of one year. Only then would the capital gains be

long term or else these would be short term. The net capital gains arrived after application of

concession using appropriate approach would then be levied CGT and determine the net tax

payable for the taxpayer (Gilders, et. al., 2015).

Timing aspect in CGT

In certain cases, a unique problem may arise due to the innate timing gap between the date on

which the contract for asset sale is executed and the date on which the related proceeds are

gained by the seller of the asset (Barkoczy, 2017). Hence, in such cases, problem arises with

regards to the correct tax year when the tax implications of the capital asset must be included. In

this context, TR 94/29 provides resolution of the situation by highlighting that irrespective of the

timing of the proceeds, the tax implications must be captured in the tax returns of the same year

when the sale contract regarding the asset is enacted (Reuters, 2017).

Application

Receipts Nature

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The information provided clearly highlights the fact that the transactions involving the asset sale

are non-business transactions. This is indication of the client not having any business related to

trading of assets. Further, evidence is available considering the fact that the client is an investor.

The net result would be that the underlying proceeds that arise from the sale would be termed as

proceeds having capital nature. Owing to this classification, there would not be any application

of tax on the proceeds, however the capital gains would not be exempt and CGT liability would

suitably be computed.

CGT Exempt Assets

Considering possible exemption for pre-CGT assets, hence it is worthwhile to take into

consideration the respective dates of asset acquisition in order to analyse if any asset is pre-CGT

or not. Considering these dates, it is apparent that a particular asset painting is recognised as a

pre-CGT asset as the asset purchase predates the application of CGT by the government. The

result is that CGT liability in connection with painting sale is zero.

The antique bed falls within the sub-category of collectables but will not have exemption from

CGT owing to $ 3,500 being the purchase price which satisfies the threshold limit. Another asset

worth consideration is the violin. If this asset was not regularly used by client for deriving

satisfaction coupled with entertainment on personal level, then this could have well being

classified as a collectable. The violin has cost of $ 5,500 and hence this is lower than $ 10,000

which implies in zero CGT implication on account of violin sale.

Taxable capital gains

For the assets that are not CGT exempt, the requisite computations are carried out below.

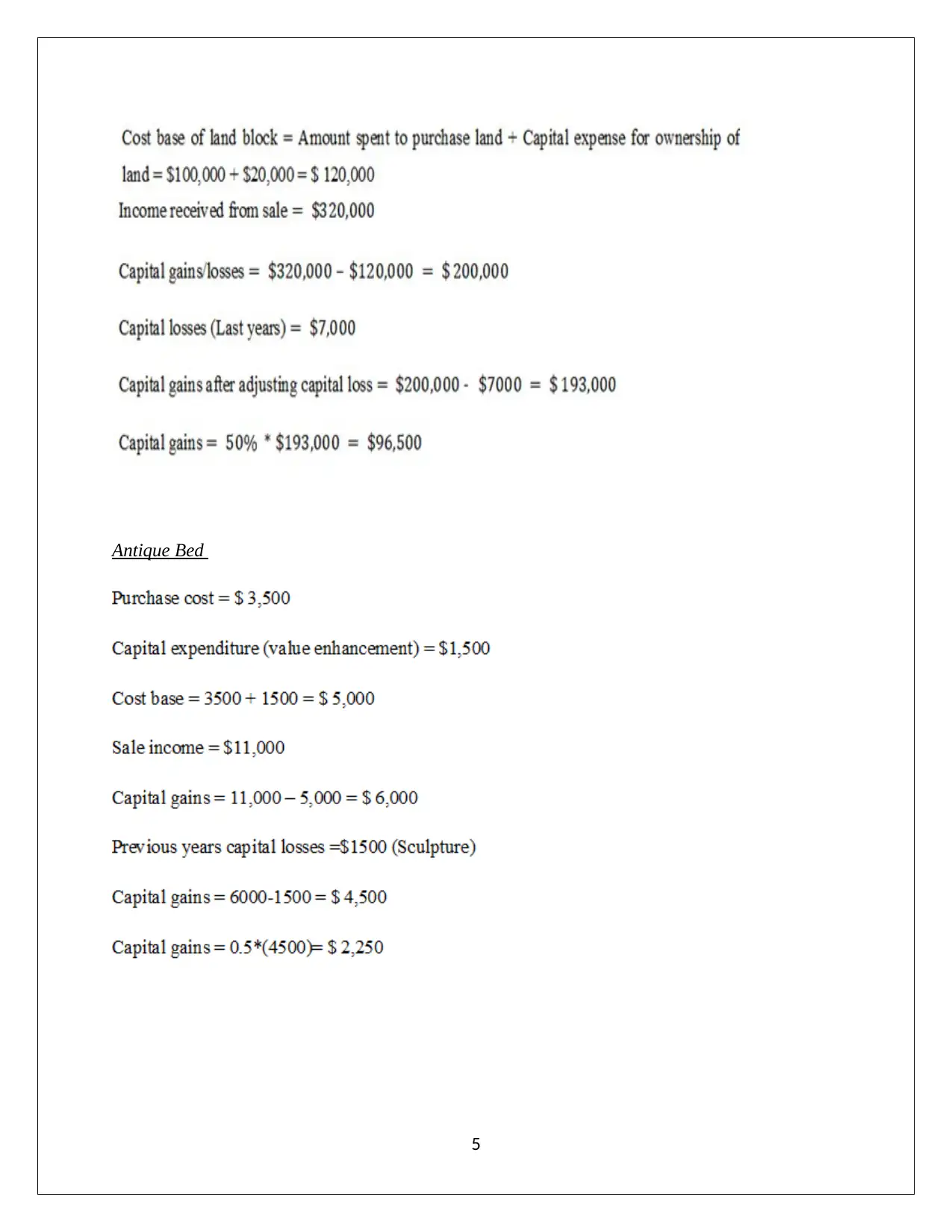

Block of Land

4

are non-business transactions. This is indication of the client not having any business related to

trading of assets. Further, evidence is available considering the fact that the client is an investor.

The net result would be that the underlying proceeds that arise from the sale would be termed as

proceeds having capital nature. Owing to this classification, there would not be any application

of tax on the proceeds, however the capital gains would not be exempt and CGT liability would

suitably be computed.

CGT Exempt Assets

Considering possible exemption for pre-CGT assets, hence it is worthwhile to take into

consideration the respective dates of asset acquisition in order to analyse if any asset is pre-CGT

or not. Considering these dates, it is apparent that a particular asset painting is recognised as a

pre-CGT asset as the asset purchase predates the application of CGT by the government. The

result is that CGT liability in connection with painting sale is zero.

The antique bed falls within the sub-category of collectables but will not have exemption from

CGT owing to $ 3,500 being the purchase price which satisfies the threshold limit. Another asset

worth consideration is the violin. If this asset was not regularly used by client for deriving

satisfaction coupled with entertainment on personal level, then this could have well being

classified as a collectable. The violin has cost of $ 5,500 and hence this is lower than $ 10,000

which implies in zero CGT implication on account of violin sale.

Taxable capital gains

For the assets that are not CGT exempt, the requisite computations are carried out below.

Block of Land

4

Antique Bed

5

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

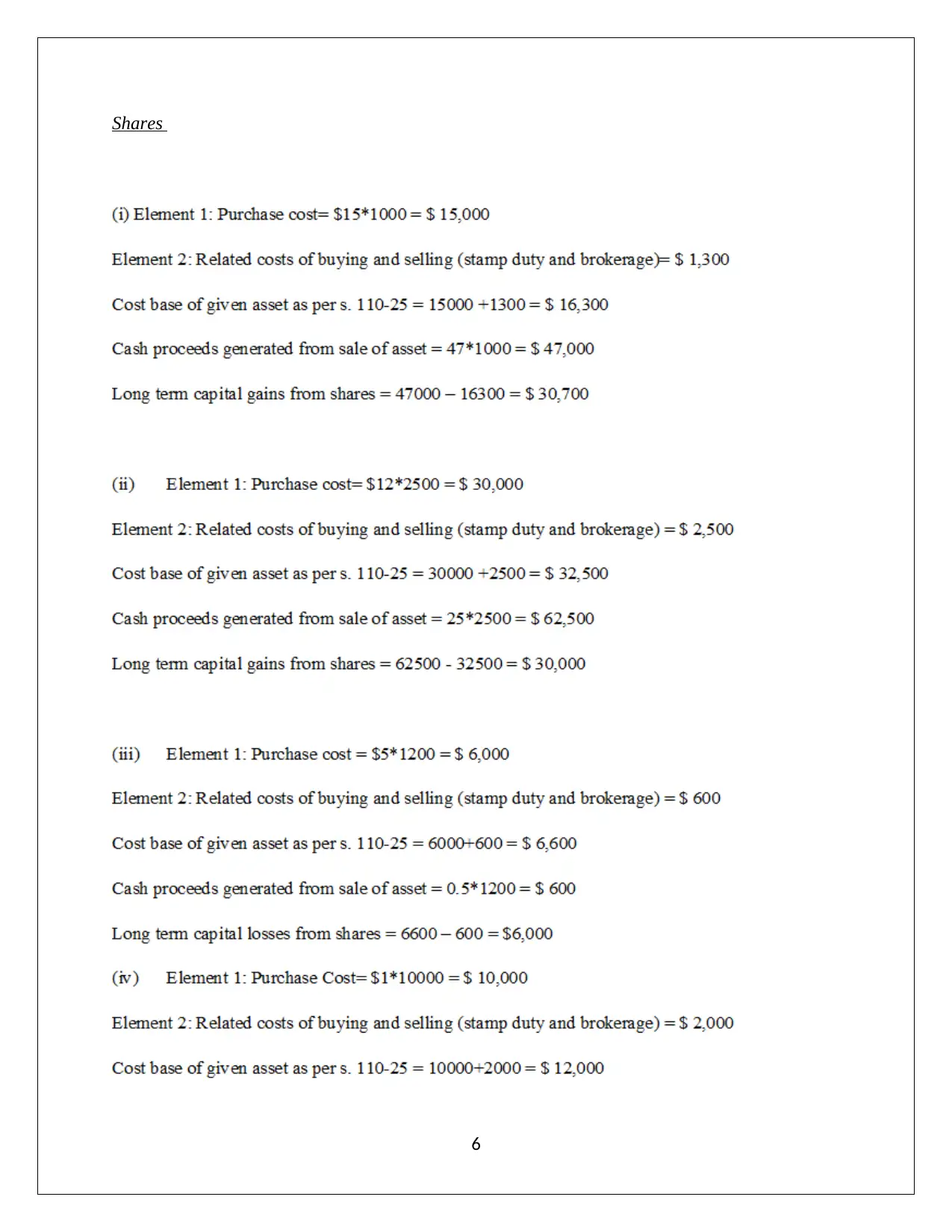

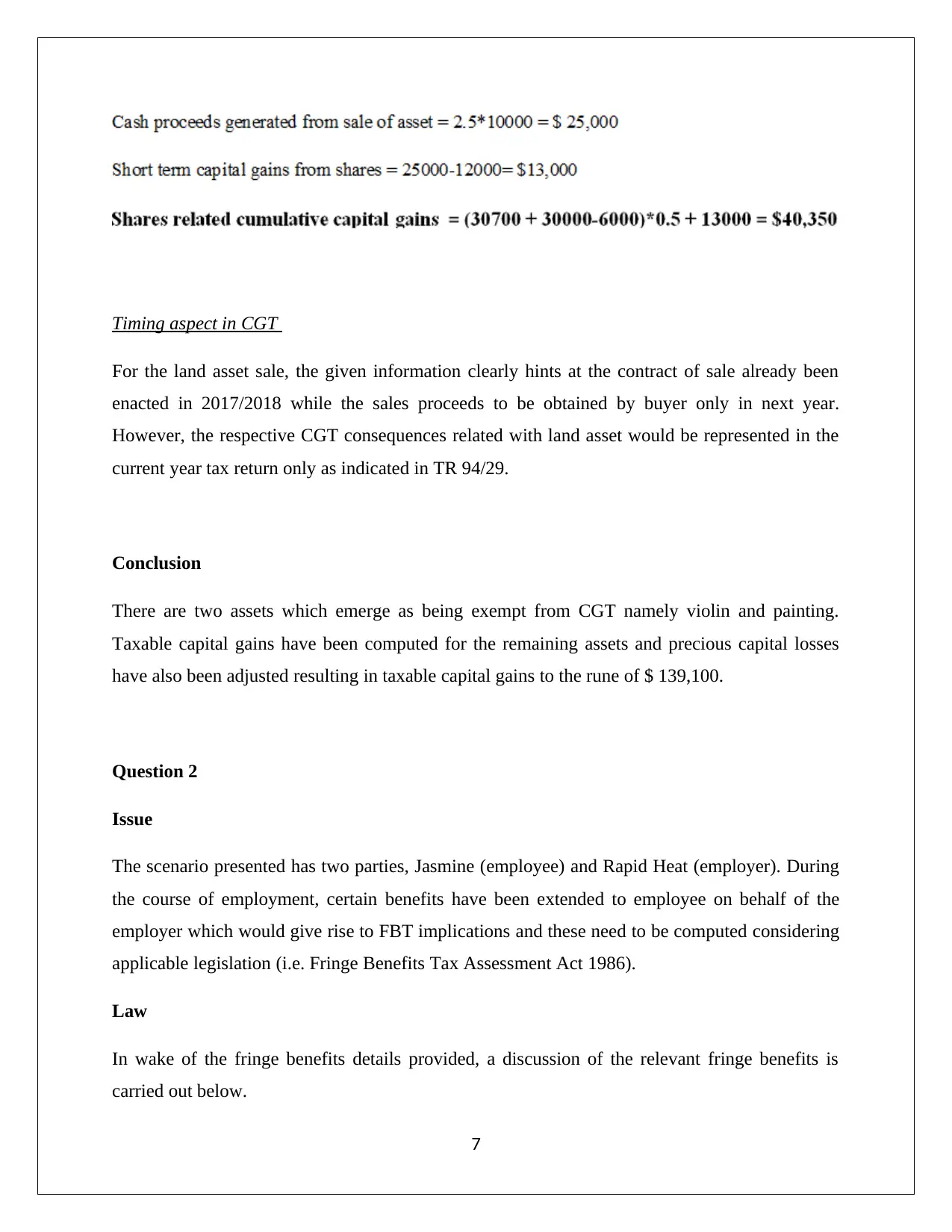

Shares

6

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Timing aspect in CGT

For the land asset sale, the given information clearly hints at the contract of sale already been

enacted in 2017/2018 while the sales proceeds to be obtained by buyer only in next year.

However, the respective CGT consequences related with land asset would be represented in the

current year tax return only as indicated in TR 94/29.

Conclusion

There are two assets which emerge as being exempt from CGT namely violin and painting.

Taxable capital gains have been computed for the remaining assets and precious capital losses

have also been adjusted resulting in taxable capital gains to the rune of $ 139,100.

Question 2

Issue

The scenario presented has two parties, Jasmine (employee) and Rapid Heat (employer). During

the course of employment, certain benefits have been extended to employee on behalf of the

employer which would give rise to FBT implications and these need to be computed considering

applicable legislation (i.e. Fringe Benefits Tax Assessment Act 1986).

Law

In wake of the fringe benefits details provided, a discussion of the relevant fringe benefits is

carried out below.

7

For the land asset sale, the given information clearly hints at the contract of sale already been

enacted in 2017/2018 while the sales proceeds to be obtained by buyer only in next year.

However, the respective CGT consequences related with land asset would be represented in the

current year tax return only as indicated in TR 94/29.

Conclusion

There are two assets which emerge as being exempt from CGT namely violin and painting.

Taxable capital gains have been computed for the remaining assets and precious capital losses

have also been adjusted resulting in taxable capital gains to the rune of $ 139,100.

Question 2

Issue

The scenario presented has two parties, Jasmine (employee) and Rapid Heat (employer). During

the course of employment, certain benefits have been extended to employee on behalf of the

employer which would give rise to FBT implications and these need to be computed considering

applicable legislation (i.e. Fringe Benefits Tax Assessment Act 1986).

Law

In wake of the fringe benefits details provided, a discussion of the relevant fringe benefits is

carried out below.

7

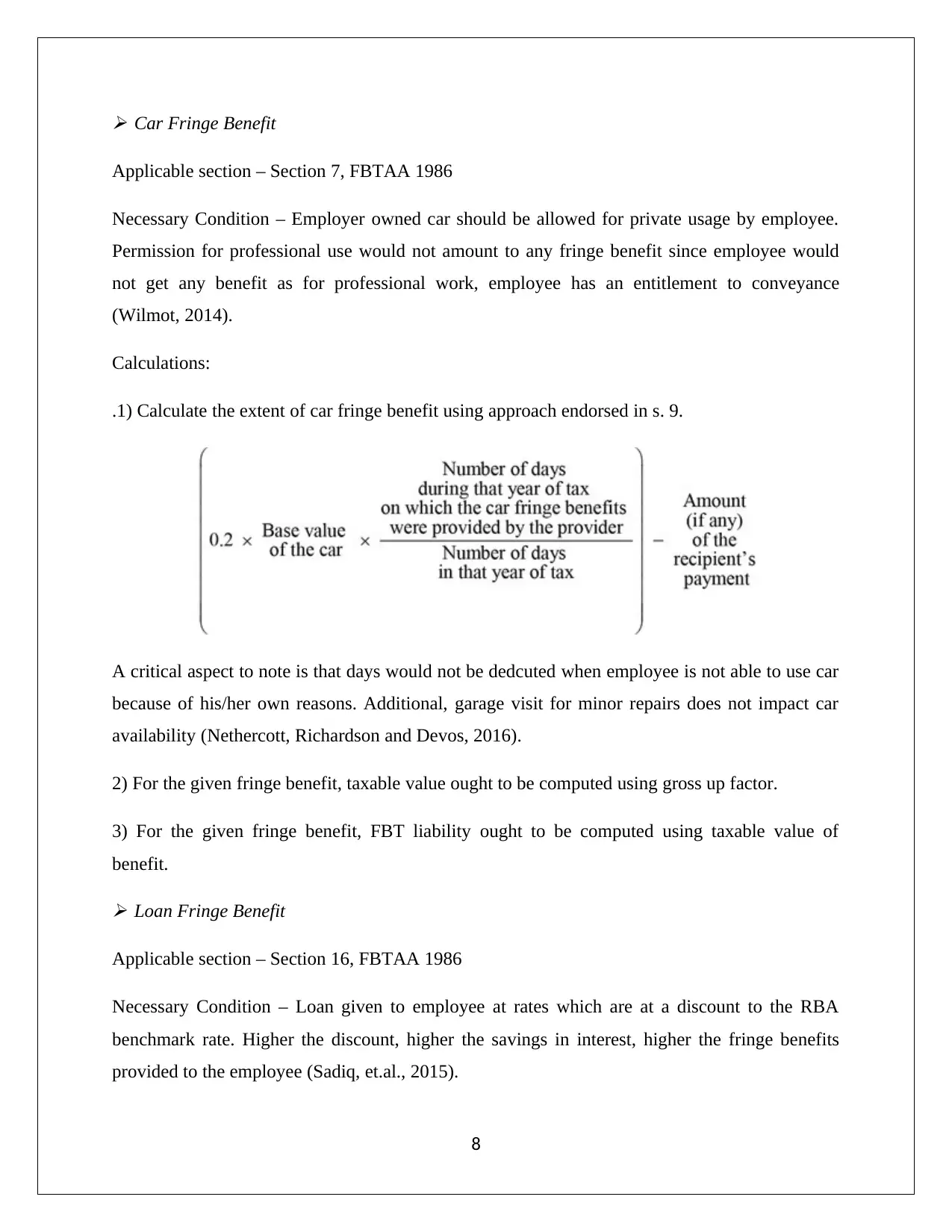

Car Fringe Benefit

Applicable section – Section 7, FBTAA 1986

Necessary Condition – Employer owned car should be allowed for private usage by employee.

Permission for professional use would not amount to any fringe benefit since employee would

not get any benefit as for professional work, employee has an entitlement to conveyance

(Wilmot, 2014).

Calculations:

.1) Calculate the extent of car fringe benefit using approach endorsed in s. 9.

A critical aspect to note is that days would not be dedcuted when employee is not able to use car

because of his/her own reasons. Additional, garage visit for minor repairs does not impact car

availability (Nethercott, Richardson and Devos, 2016).

2) For the given fringe benefit, taxable value ought to be computed using gross up factor.

3) For the given fringe benefit, FBT liability ought to be computed using taxable value of

benefit.

Loan Fringe Benefit

Applicable section – Section 16, FBTAA 1986

Necessary Condition – Loan given to employee at rates which are at a discount to the RBA

benchmark rate. Higher the discount, higher the savings in interest, higher the fringe benefits

provided to the employee (Sadiq, et.al., 2015).

8

Applicable section – Section 7, FBTAA 1986

Necessary Condition – Employer owned car should be allowed for private usage by employee.

Permission for professional use would not amount to any fringe benefit since employee would

not get any benefit as for professional work, employee has an entitlement to conveyance

(Wilmot, 2014).

Calculations:

.1) Calculate the extent of car fringe benefit using approach endorsed in s. 9.

A critical aspect to note is that days would not be dedcuted when employee is not able to use car

because of his/her own reasons. Additional, garage visit for minor repairs does not impact car

availability (Nethercott, Richardson and Devos, 2016).

2) For the given fringe benefit, taxable value ought to be computed using gross up factor.

3) For the given fringe benefit, FBT liability ought to be computed using taxable value of

benefit.

Loan Fringe Benefit

Applicable section – Section 16, FBTAA 1986

Necessary Condition – Loan given to employee at rates which are at a discount to the RBA

benchmark rate. Higher the discount, higher the savings in interest, higher the fringe benefits

provided to the employee (Sadiq, et.al., 2015).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculations:

1) Considering the discount in interest rate, amount of loan, and time period, the interest saving

ought to be computed which forms the value of fringe benefit (Krever, 2017).

2) For the given fringe benefit, taxable value ought to be computed using gross up factor.

3) For the given fringe benefit, FBT liability ought to be computed using taxable value of

benefit.

Section 18 provides for a deduction rule whereby CGT deductions can be taken by employer to

the extent the loan amount is utilised by employer only for taxable income production (Hodgson,

Mortimer and Butler, 2016).

Internal expense fringe benefit

Applicable section – Section 20, FBTAA 1986

Necessary Condition – Employer to contribute in paying for personal expenses of employee so as

to lower the spending by employee (Gilders, et. al., 2015).

Calculations:

1) The amount of personal expense that employer pays for is the extent of fringe benefit which is

modified owing to internal benefit.

2) For the given fringe benefit, taxable value ought to be computed using gross up factor.

3) For the given fringe benefit, FBT liability ought to be computed using taxable value of benefit

(Deutsch, et.al., 2015).

Application

(a) In wake of the relevant law, the fringe benefits provided by Rapid Heat ought to be discussed

to work out the FBT consequences for the employer.

Car fringe benefit

9

1) Considering the discount in interest rate, amount of loan, and time period, the interest saving

ought to be computed which forms the value of fringe benefit (Krever, 2017).

2) For the given fringe benefit, taxable value ought to be computed using gross up factor.

3) For the given fringe benefit, FBT liability ought to be computed using taxable value of

benefit.

Section 18 provides for a deduction rule whereby CGT deductions can be taken by employer to

the extent the loan amount is utilised by employer only for taxable income production (Hodgson,

Mortimer and Butler, 2016).

Internal expense fringe benefit

Applicable section – Section 20, FBTAA 1986

Necessary Condition – Employer to contribute in paying for personal expenses of employee so as

to lower the spending by employee (Gilders, et. al., 2015).

Calculations:

1) The amount of personal expense that employer pays for is the extent of fringe benefit which is

modified owing to internal benefit.

2) For the given fringe benefit, taxable value ought to be computed using gross up factor.

3) For the given fringe benefit, FBT liability ought to be computed using taxable value of benefit

(Deutsch, et.al., 2015).

Application

(a) In wake of the relevant law, the fringe benefits provided by Rapid Heat ought to be discussed

to work out the FBT consequences for the employer.

Car fringe benefit

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

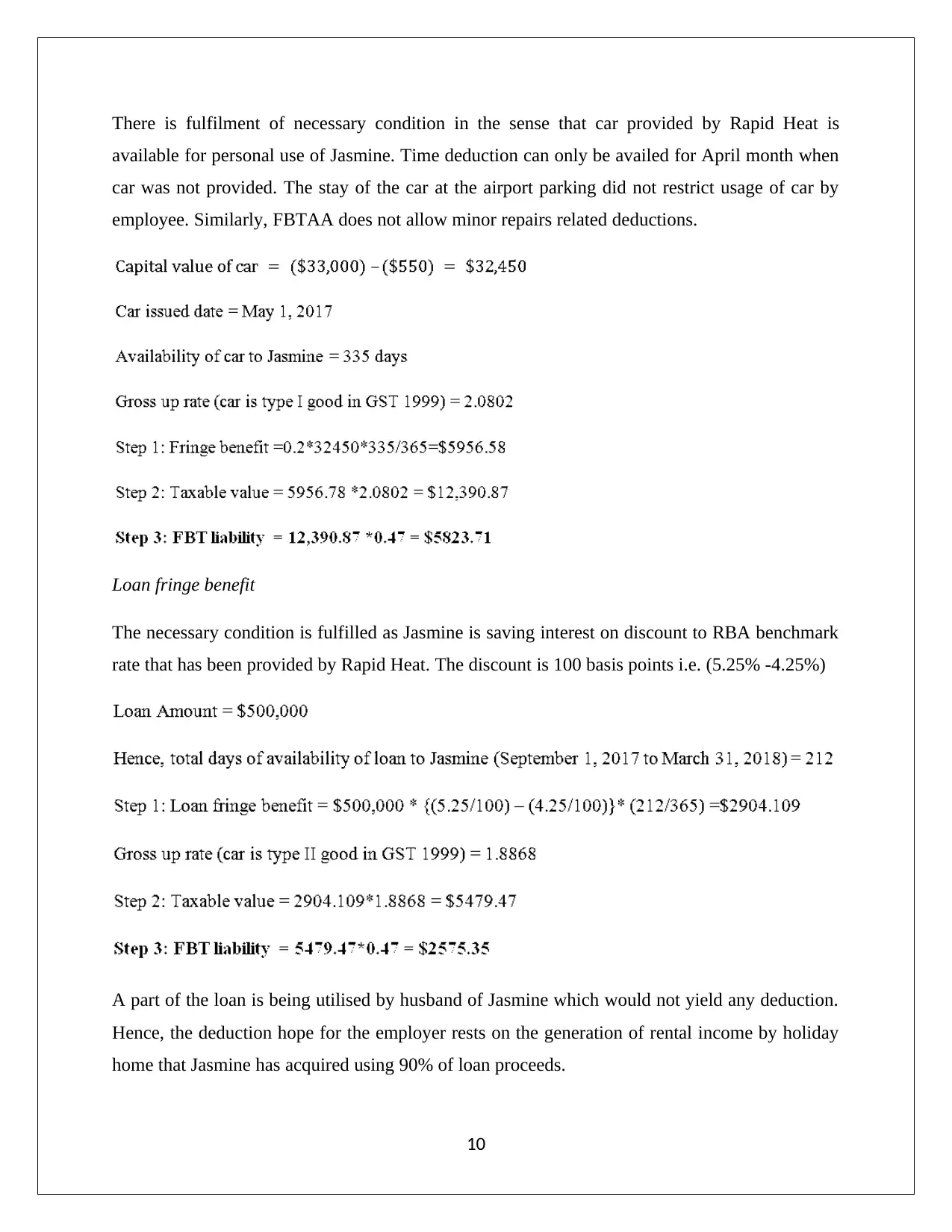

There is fulfilment of necessary condition in the sense that car provided by Rapid Heat is

available for personal use of Jasmine. Time deduction can only be availed for April month when

car was not provided. The stay of the car at the airport parking did not restrict usage of car by

employee. Similarly, FBTAA does not allow minor repairs related deductions.

Loan fringe benefit

The necessary condition is fulfilled as Jasmine is saving interest on discount to RBA benchmark

rate that has been provided by Rapid Heat. The discount is 100 basis points i.e. (5.25% -4.25%)

A part of the loan is being utilised by husband of Jasmine which would not yield any deduction.

Hence, the deduction hope for the employer rests on the generation of rental income by holiday

home that Jasmine has acquired using 90% of loan proceeds.

10

available for personal use of Jasmine. Time deduction can only be availed for April month when

car was not provided. The stay of the car at the airport parking did not restrict usage of car by

employee. Similarly, FBTAA does not allow minor repairs related deductions.

Loan fringe benefit

The necessary condition is fulfilled as Jasmine is saving interest on discount to RBA benchmark

rate that has been provided by Rapid Heat. The discount is 100 basis points i.e. (5.25% -4.25%)

A part of the loan is being utilised by husband of Jasmine which would not yield any deduction.

Hence, the deduction hope for the employer rests on the generation of rental income by holiday

home that Jasmine has acquired using 90% of loan proceeds.

10

Internal expense fringe benefit

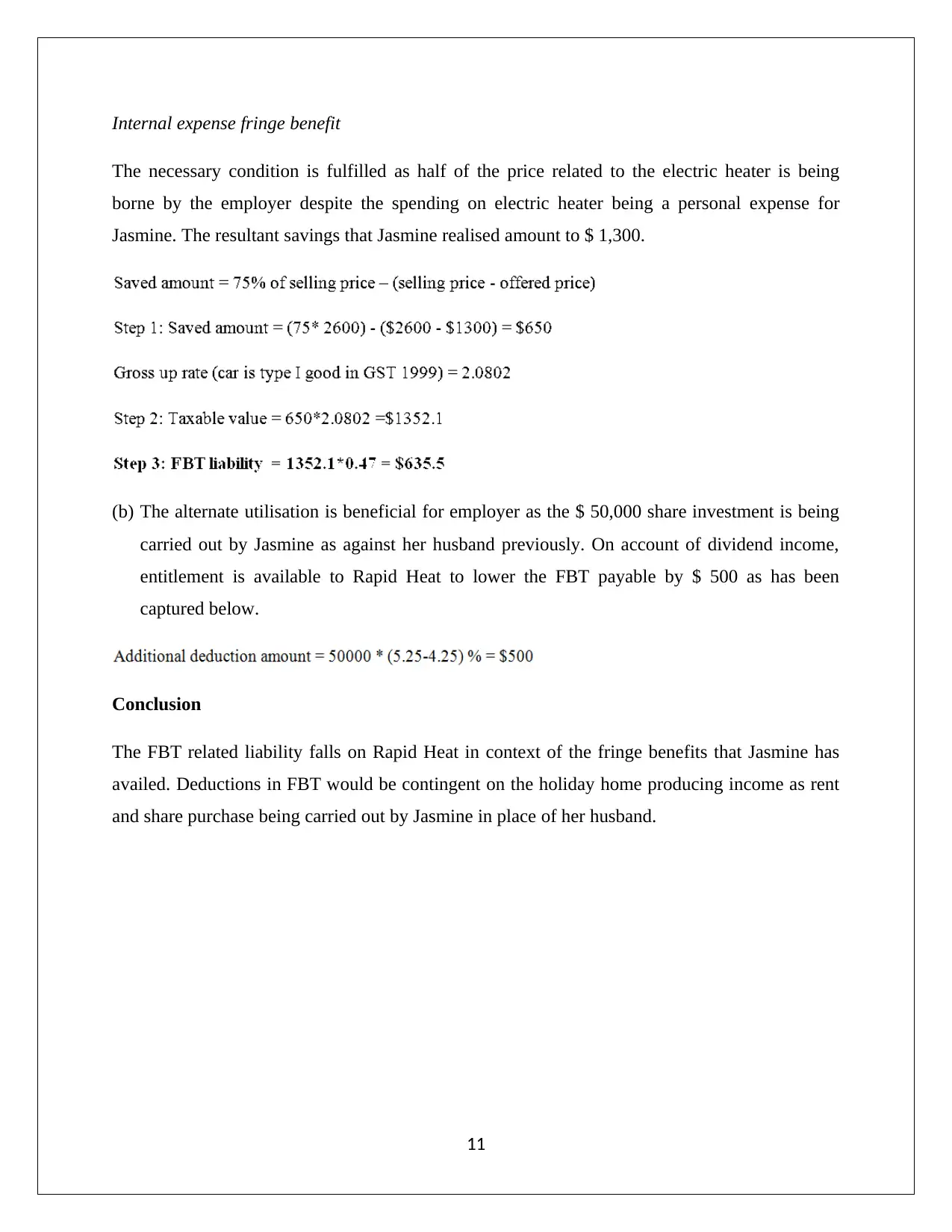

The necessary condition is fulfilled as half of the price related to the electric heater is being

borne by the employer despite the spending on electric heater being a personal expense for

Jasmine. The resultant savings that Jasmine realised amount to $ 1,300.

(b) The alternate utilisation is beneficial for employer as the $ 50,000 share investment is being

carried out by Jasmine as against her husband previously. On account of dividend income,

entitlement is available to Rapid Heat to lower the FBT payable by $ 500 as has been

captured below.

Conclusion

The FBT related liability falls on Rapid Heat in context of the fringe benefits that Jasmine has

availed. Deductions in FBT would be contingent on the holiday home producing income as rent

and share purchase being carried out by Jasmine in place of her husband.

11

The necessary condition is fulfilled as half of the price related to the electric heater is being

borne by the employer despite the spending on electric heater being a personal expense for

Jasmine. The resultant savings that Jasmine realised amount to $ 1,300.

(b) The alternate utilisation is beneficial for employer as the $ 50,000 share investment is being

carried out by Jasmine as against her husband previously. On account of dividend income,

entitlement is available to Rapid Heat to lower the FBT payable by $ 500 as has been

captured below.

Conclusion

The FBT related liability falls on Rapid Heat in context of the fringe benefits that Jasmine has

availed. Deductions in FBT would be contingent on the holiday home producing income as rent

and share purchase being carried out by Jasmine in place of her husband.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.