Taxation Theory, Practice & Law

VerifiedAdded on 2022/11/30

|11

|2411

|161

AI Summary

This assignment focuses on understanding the Australian Income Tax Appraisal Act, as well as various aspects of FBT, revenue, and allowances. It includes a case study on tax liability and calculations. The second part discusses fringe benefits tax (FBT) and the taxable value of FBT. The assignment provides a comprehensive overview of taxation theory, practice, and law.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation Theory, Practice &

Law

Law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

Identification of facts...................................................................................................................3

Rulings.........................................................................................................................................3

Application..................................................................................................................................4

Conclusion...................................................................................................................................7

Question 2........................................................................................................................................8

Part-A (FBT)................................................................................................................................8

Part-B Taxable value of FBT.......................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

Identification of facts...................................................................................................................3

Rulings.........................................................................................................................................3

Application..................................................................................................................................4

Conclusion...................................................................................................................................7

Question 2........................................................................................................................................8

Part-A (FBT)................................................................................................................................8

Part-B Taxable value of FBT.......................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

The assignment takes into consideration an understanding of the Australian Income Tax

Appraisal Act, as well as various meanings of FBT, revenue, and allowances, as well as various

other criteria. It will continue with the terms of gross obtainable profit, tax liability, tax benefit,

as well as other income tax-related matters. Susanne, whom resides in Australia as well as being

unmarried, has a first concern about her tax liability. She has an outstanding home mortgage but

has not taken out such a life insurance policy. Her employer also pays a 9.5 percent

superannuation contribution. She earns the majority of her income from wages and passive

income provided from stock investments. The ideals of FBT are taken into consideration in the

second mission. An example of FBT as well as its distinguishing characteristics is already given.

The taxable value of remuneration also was calculated using a system of statutory formulae.

Eventually, the paper summarises the total information obtained and includes a summary of the

research.

Question 1

Identification of facts

In this case, taxable sales, taxable profits, tax obligations, and student debt are all factored

into the equation. Susanne seems to be the individual citizen in Australia that has to file taxes in

2020-21. Susanne's gross net income is S90,000, with withheld tax, although she does not really

have a private health insurance scheme. Her prior college loan with Sydney University, which

totals $53,000, is now outstanding. There is a 9.5 percent workplace pension plan fee, which will

be the maximum payroll of the specified fund. Susanne have additional sources of profits, such

as the $10,000 of earnings from correctly used in the very same taxable year. Susanne has a

variety of sources of revenue in addition to her salary. In any case, the net total income, taxable

income, tax liability, college debt, Medicare levy, as well as Medicare levy must be determined

based on the information provided.

Rulings

The net taxable income, where specified more by Income Tax Act of 1997, contains income

derived from usual sources of revenue through adjusted as specified also by income tax act

(Nery, Sadler and White, 2019). Non-assessable taxes, also known as withholding taxes or non-

exempt revenue, is income that is not subject to the Internal Revenue Code. The income that can

The assignment takes into consideration an understanding of the Australian Income Tax

Appraisal Act, as well as various meanings of FBT, revenue, and allowances, as well as various

other criteria. It will continue with the terms of gross obtainable profit, tax liability, tax benefit,

as well as other income tax-related matters. Susanne, whom resides in Australia as well as being

unmarried, has a first concern about her tax liability. She has an outstanding home mortgage but

has not taken out such a life insurance policy. Her employer also pays a 9.5 percent

superannuation contribution. She earns the majority of her income from wages and passive

income provided from stock investments. The ideals of FBT are taken into consideration in the

second mission. An example of FBT as well as its distinguishing characteristics is already given.

The taxable value of remuneration also was calculated using a system of statutory formulae.

Eventually, the paper summarises the total information obtained and includes a summary of the

research.

Question 1

Identification of facts

In this case, taxable sales, taxable profits, tax obligations, and student debt are all factored

into the equation. Susanne seems to be the individual citizen in Australia that has to file taxes in

2020-21. Susanne's gross net income is S90,000, with withheld tax, although she does not really

have a private health insurance scheme. Her prior college loan with Sydney University, which

totals $53,000, is now outstanding. There is a 9.5 percent workplace pension plan fee, which will

be the maximum payroll of the specified fund. Susanne have additional sources of profits, such

as the $10,000 of earnings from correctly used in the very same taxable year. Susanne has a

variety of sources of revenue in addition to her salary. In any case, the net total income, taxable

income, tax liability, college debt, Medicare levy, as well as Medicare levy must be determined

based on the information provided.

Rulings

The net taxable income, where specified more by Income Tax Act of 1997, contains income

derived from usual sources of revenue through adjusted as specified also by income tax act

(Nery, Sadler and White, 2019). Non-assessable taxes, also known as withholding taxes or non-

exempt revenue, is income that is not subject to the Internal Revenue Code. The income that can

be measured includes interest income through banks profitability, donations from workers that

reduce FBT, as well as other considerations. Before determining the tax liability, it is therefore

important to decide if the claimant is a resident. In which a resident citizen has no personal

medical benefits other than a Medicare fee, the reduction is also allowable, taking into

consideration the individual's and partner's circumstances, and can take into consideration a

deductible credit of 2% of tax liability in return for an insurance charge (Barkoczy and

Wilkinson, 2019). The income is derived by the taxation of payroll taxes. The gross amount

provided by that of the Medicare levy is equal to the number of the PAYG refused by the

contractor.

Application

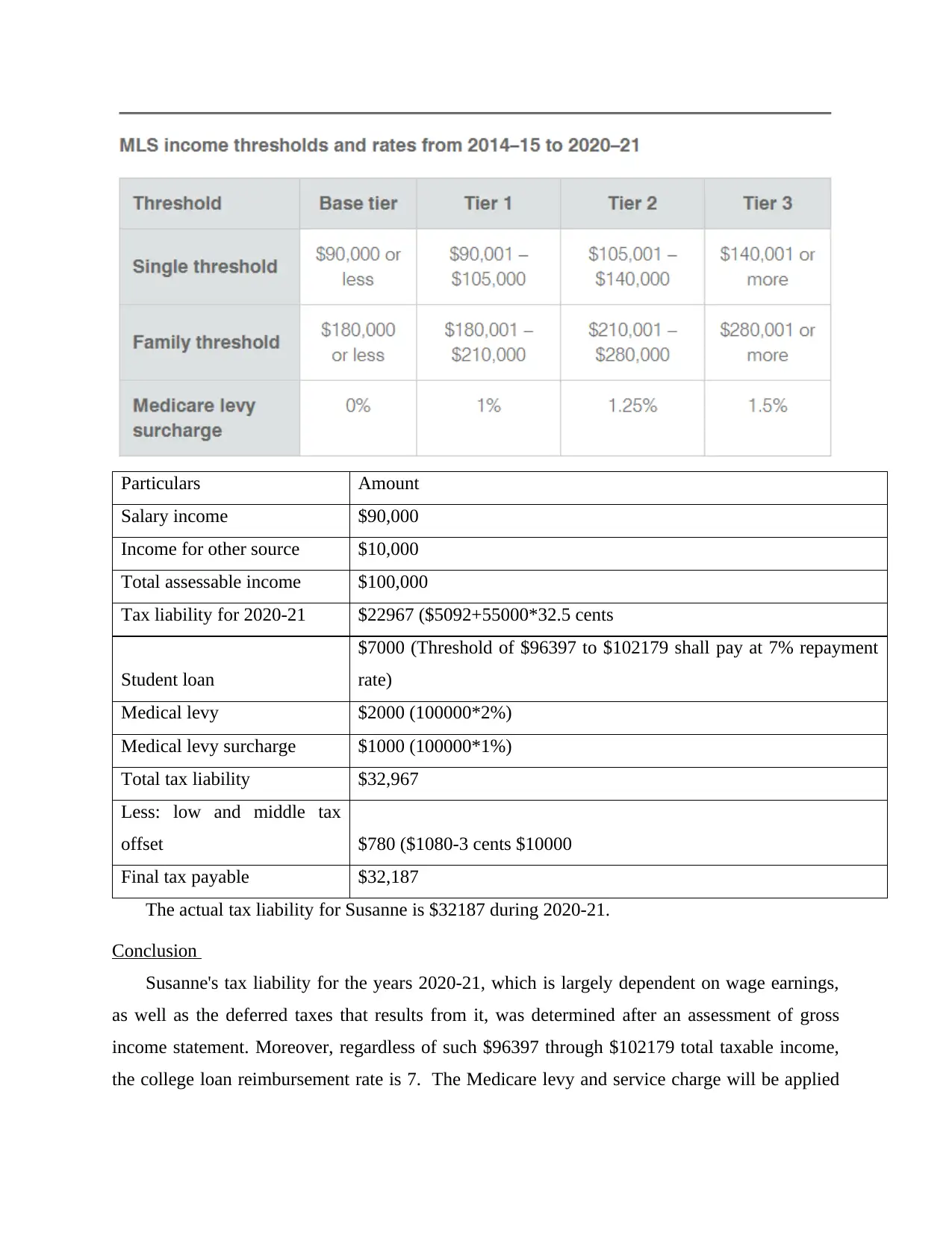

The taxes are based at the moment the taxable income is filed, considering the MLS. If the

spouse and younger siblings do not have enough medical benefits, the Medicare tax monthly

charge of 1% of that same tax burden is required to be paid.

The refund threshold towards 2020-21 will be seen in light of the repayment of higher education

loans. The donation cap for 2020-21 is $46,620. In terms of superannuation payments, they will

either be included in the wages or paid separately. Susanne's most recent case study is

considered. Susanne has indeed been determined and must file her returns as a single Australian

resident for the years 2020-21. Susanne's net taxable salary is $90,000 after taxes, and she does

not have a corporate health insurance scheme. She already has a $53,000 non-student mortgage

for her studies at Radcliffe College. Susanne would also receive annual passive income of

$10,000 throughout the year as the employer pays a 9.5 percent superannuation over the income.

The following estimate has been performed:

reduce FBT, as well as other considerations. Before determining the tax liability, it is therefore

important to decide if the claimant is a resident. In which a resident citizen has no personal

medical benefits other than a Medicare fee, the reduction is also allowable, taking into

consideration the individual's and partner's circumstances, and can take into consideration a

deductible credit of 2% of tax liability in return for an insurance charge (Barkoczy and

Wilkinson, 2019). The income is derived by the taxation of payroll taxes. The gross amount

provided by that of the Medicare levy is equal to the number of the PAYG refused by the

contractor.

Application

The taxes are based at the moment the taxable income is filed, considering the MLS. If the

spouse and younger siblings do not have enough medical benefits, the Medicare tax monthly

charge of 1% of that same tax burden is required to be paid.

The refund threshold towards 2020-21 will be seen in light of the repayment of higher education

loans. The donation cap for 2020-21 is $46,620. In terms of superannuation payments, they will

either be included in the wages or paid separately. Susanne's most recent case study is

considered. Susanne has indeed been determined and must file her returns as a single Australian

resident for the years 2020-21. Susanne's net taxable salary is $90,000 after taxes, and she does

not have a corporate health insurance scheme. She already has a $53,000 non-student mortgage

for her studies at Radcliffe College. Susanne would also receive annual passive income of

$10,000 throughout the year as the employer pays a 9.5 percent superannuation over the income.

The following estimate has been performed:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

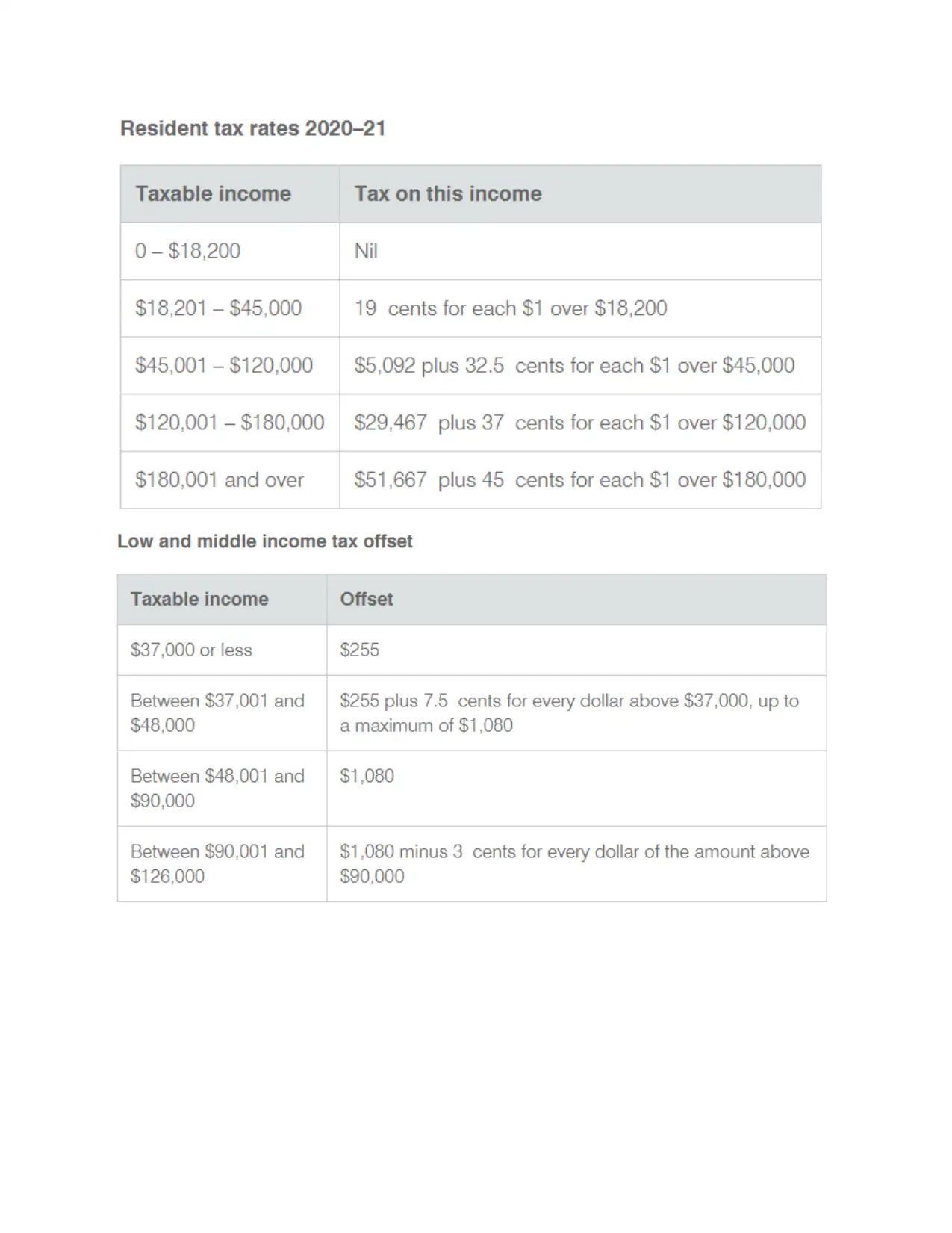

Particulars Amount

Salary income $90,000

Income for other source $10,000

Total assessable income $100,000

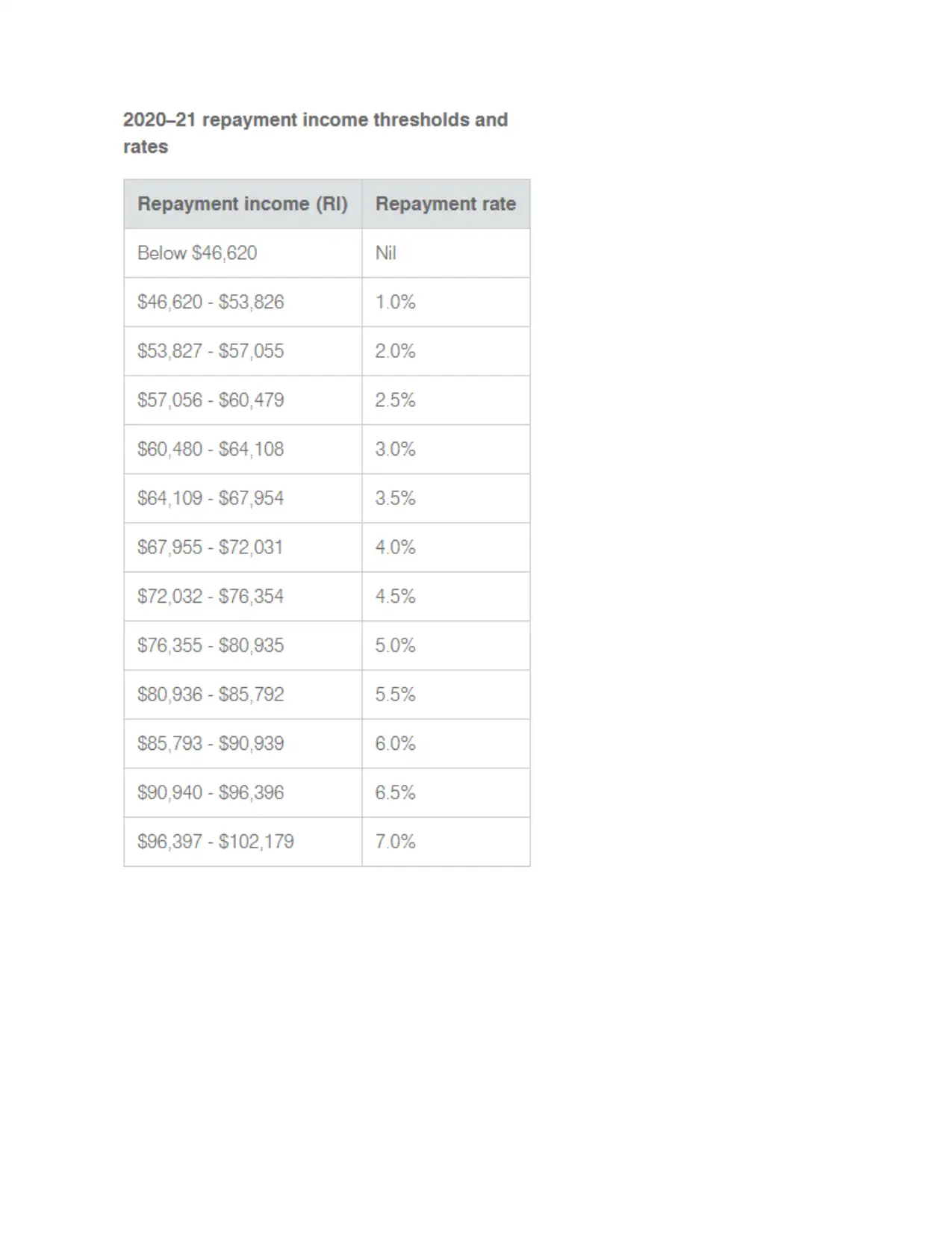

Tax liability for 2020-21 $22967 ($5092+55000*32.5 cents

Student loan

$7000 (Threshold of $96397 to $102179 shall pay at 7% repayment

rate)

Medical levy $2000 (100000*2%)

Medical levy surcharge $1000 (100000*1%)

Total tax liability $32,967

Less: low and middle tax

offset $780 ($1080-3 cents $10000

Final tax payable $32,187

The actual tax liability for Susanne is $32187 during 2020-21.

Conclusion

Susanne's tax liability for the years 2020-21, which is largely dependent on wage earnings,

as well as the deferred taxes that results from it, was determined after an assessment of gross

income statement. Moreover, regardless of such $96397 through $102179 total taxable income,

the college loan reimbursement rate is 7. The Medicare levy and service charge will be applied

Salary income $90,000

Income for other source $10,000

Total assessable income $100,000

Tax liability for 2020-21 $22967 ($5092+55000*32.5 cents

Student loan

$7000 (Threshold of $96397 to $102179 shall pay at 7% repayment

rate)

Medical levy $2000 (100000*2%)

Medical levy surcharge $1000 (100000*1%)

Total tax liability $32,967

Less: low and middle tax

offset $780 ($1080-3 cents $10000

Final tax payable $32,187

The actual tax liability for Susanne is $32187 during 2020-21.

Conclusion

Susanne's tax liability for the years 2020-21, which is largely dependent on wage earnings,

as well as the deferred taxes that results from it, was determined after an assessment of gross

income statement. Moreover, regardless of such $96397 through $102179 total taxable income,

the college loan reimbursement rate is 7. The Medicare levy and service charge will be applied

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

at a level of 2% as well as 1% of gross revenue, respectively. It also refers to low- and middle-

income compensation. Susanne's total taxable revenue per year 2020-21, according to

calculations, is $32187.

Question 2

Part-A (FBT)

Employers are compensated fringe incentives to their workers, family members, or other

spouses in addition to compensation they provide. Employees are expected to pay the

government another major benefit levy. FBT may not function until a third party grants the right

in collaboration with an employer (Whiteford and Heron, 2018). FBT is really a form of

marginal social cost tax that is distinct from taxes on a taxable sum. Employers are liable for

their FBT obligations and must file an FBT request for each FBT year (April 1 to March 31).

Businesses will normally exclude the costs of providing marginal wages and also FBTs charged

on their returns. In most cases, companies may claim GST credits as just a supplementary

reimbursement for benefits received. In the case of the FBT, current and former directors,

business administrators, and stakeholders has to be employees if the confidence is to work for the

corporation (McClure, Lanis and Govendir, 2017). That is a separate levy, and the gross benefit

taxation value is estimated. The contractor must assess FBT's liability for the FBT year before

issuing a refund. The employer can seek a tax refund for the side benefit cost as well as the FBT

charged. Employers must claim GST credits for goods that are sold at a small profit. As a result,

workers pay FBT mostly at a flat rate. As a result, companies pay FBT mostly to support

employees or the households of shareholders and investors. This is so where the benefit is

distributed to external parties in accordance with an arrangement with the employer.

The success is attributed a variety of extrinsic rewards, including a discounted loan, the

firm's gym processing fee, entertainment in the form of free theatre tickets, as well as other

perks. Pay as well as salaries, workplace contributions to superfunds, termination insurance, as

well as other costs are not included in the so-called fringe benefits (Black, 2018). The below are

the key characteristics of FBT:

Fringe Benefit Tax payable by a corporation is calculated in terms of monetary

income or earnings received this year in view of recruitment and fringe benefits

provided to or believed to have been granted to the largest corporations. A

income compensation. Susanne's total taxable revenue per year 2020-21, according to

calculations, is $32187.

Question 2

Part-A (FBT)

Employers are compensated fringe incentives to their workers, family members, or other

spouses in addition to compensation they provide. Employees are expected to pay the

government another major benefit levy. FBT may not function until a third party grants the right

in collaboration with an employer (Whiteford and Heron, 2018). FBT is really a form of

marginal social cost tax that is distinct from taxes on a taxable sum. Employers are liable for

their FBT obligations and must file an FBT request for each FBT year (April 1 to March 31).

Businesses will normally exclude the costs of providing marginal wages and also FBTs charged

on their returns. In most cases, companies may claim GST credits as just a supplementary

reimbursement for benefits received. In the case of the FBT, current and former directors,

business administrators, and stakeholders has to be employees if the confidence is to work for the

corporation (McClure, Lanis and Govendir, 2017). That is a separate levy, and the gross benefit

taxation value is estimated. The contractor must assess FBT's liability for the FBT year before

issuing a refund. The employer can seek a tax refund for the side benefit cost as well as the FBT

charged. Employers must claim GST credits for goods that are sold at a small profit. As a result,

workers pay FBT mostly at a flat rate. As a result, companies pay FBT mostly to support

employees or the households of shareholders and investors. This is so where the benefit is

distributed to external parties in accordance with an arrangement with the employer.

The success is attributed a variety of extrinsic rewards, including a discounted loan, the

firm's gym processing fee, entertainment in the form of free theatre tickets, as well as other

perks. Pay as well as salaries, workplace contributions to superfunds, termination insurance, as

well as other costs are not included in the so-called fringe benefits (Black, 2018). The below are

the key characteristics of FBT:

Fringe Benefit Tax payable by a corporation is calculated in terms of monetary

income or earnings received this year in view of recruitment and fringe benefits

provided to or believed to have been granted to the largest corporations. A

corporation is also reimbursed Fringe Benefits Tax where no payroll payments are

due on net revenue.

The Fringe Benefit Levy, along with all other taxes, is not an allowable deduction

when determining taxable income. In addition, the Fringe Benefit Tax is due on the

taxable income charged.

For employee benefits, the Benefit Tax mostly on Fringe Amount is paid at the rate

applicable. The value of something like the margins is calculated based on the

information given (Ssennyonjo, 2019).

The FBT is not really a deductible expense and can be used to reduce tax liability.

Fringe Benefit Tax must be charged at the rate applicable on the employers' fringe

benefits. The number of extrinsic incentives is calculated in accordance with the

provisions 115WC of the Income Tax Assessment act of 1961.

Part-B Taxable value of FBT

The assessment of fringe benefits to use the permissible formula methodology has already

been put into consideration in the present situation. Carron, who gives his employee Rabbie a

vehicle which he needs, is the subject of the report. The car is a Nissan Xtrail was used for 196

days during the FBT year. The car travelled 15,000 kilometres during the FBT period, which this

purchased for $45,000. Rabbie charged $1,500 also for cost of running the generator and gave

Carron all necessary paperwork. It's time to figure out how much the motor's fringe value tax

is discussed below:

Rulings

The benefit of car fringes happens when the organisation provides the car for private use

among its workers, as per Chapter 7 of ITAA, 1997. Automobiles, station waggons, service cars,

and other automobiles, freight vehicles, and good public transport vehicles, are also considered

vehicles with FBT (Maurer and Walker, 2017). The car available to employees for personal

usage will be used for personal usage or by employees any other day. The car is called private on

any particular day, i.e. because it is not in operation and the worker could use it for individual

matters, or when it is parked in the individual employee office drive. The taxable benefit of a car

can be calculated using two methods: the statutory formula scheme and the operating cost

process.

due on net revenue.

The Fringe Benefit Levy, along with all other taxes, is not an allowable deduction

when determining taxable income. In addition, the Fringe Benefit Tax is due on the

taxable income charged.

For employee benefits, the Benefit Tax mostly on Fringe Amount is paid at the rate

applicable. The value of something like the margins is calculated based on the

information given (Ssennyonjo, 2019).

The FBT is not really a deductible expense and can be used to reduce tax liability.

Fringe Benefit Tax must be charged at the rate applicable on the employers' fringe

benefits. The number of extrinsic incentives is calculated in accordance with the

provisions 115WC of the Income Tax Assessment act of 1961.

Part-B Taxable value of FBT

The assessment of fringe benefits to use the permissible formula methodology has already

been put into consideration in the present situation. Carron, who gives his employee Rabbie a

vehicle which he needs, is the subject of the report. The car is a Nissan Xtrail was used for 196

days during the FBT year. The car travelled 15,000 kilometres during the FBT period, which this

purchased for $45,000. Rabbie charged $1,500 also for cost of running the generator and gave

Carron all necessary paperwork. It's time to figure out how much the motor's fringe value tax

is discussed below:

Rulings

The benefit of car fringes happens when the organisation provides the car for private use

among its workers, as per Chapter 7 of ITAA, 1997. Automobiles, station waggons, service cars,

and other automobiles, freight vehicles, and good public transport vehicles, are also considered

vehicles with FBT (Maurer and Walker, 2017). The car available to employees for personal

usage will be used for personal usage or by employees any other day. The car is called private on

any particular day, i.e. because it is not in operation and the worker could use it for individual

matters, or when it is parked in the individual employee office drive. The taxable benefit of a car

can be calculated using two methods: the statutory formula scheme and the operating cost

process.

Formula:

Taxable value = [Cost of Car x Statutory Rate* x Days Private Use] ÷ 365

-Employee Contributions

Application:

(The applicable statutory rate for a $50,000 car is 20%)

Statutory Rate= 20%

Hence, the taxable value is as:

Taxable value = [(45,000 x 20% x 196) / 365] - 1,500

Taxable value = $3333

Final outcome

By using the legal formula scheme, the car taxable value is calculated to be $3333 in

total. The benefit of car fringes happens when the organisation provides the car for private use

through its workers. Automobiles, station waggons, utility vans, and certain other cars and

trucks, as well as passenger vehicles as well as decent transportation vehicles, are included in

FBT's definition of vehicles. Staff can use the vehicle available to them for personal use on any

day of the week. When the car is not used as well as the worker may use that for personal

reasons, or if the car is parked in the customer's office parking, the vehicle is deemed private on

every particular day.

CONCLUSION

Following the completion of the study, it was decided that a systematic oversimplifying of

numerous aspects of the Australian Income Tax Appraisal Act should always be required in

determining the taxable income. Furthermore, based on the situation, various provisions may be

added. Susanne's taxation duty is estimated in the report after the enforcement of various

legislation and is estimated as S32187. The FBT measurement was also done for automobile

fringe of society, which yielded $3333 after the statutory formula procedure was applied.

Taxable value = [Cost of Car x Statutory Rate* x Days Private Use] ÷ 365

-Employee Contributions

Application:

(The applicable statutory rate for a $50,000 car is 20%)

Statutory Rate= 20%

Hence, the taxable value is as:

Taxable value = [(45,000 x 20% x 196) / 365] - 1,500

Taxable value = $3333

Final outcome

By using the legal formula scheme, the car taxable value is calculated to be $3333 in

total. The benefit of car fringes happens when the organisation provides the car for private use

through its workers. Automobiles, station waggons, utility vans, and certain other cars and

trucks, as well as passenger vehicles as well as decent transportation vehicles, are included in

FBT's definition of vehicles. Staff can use the vehicle available to them for personal use on any

day of the week. When the car is not used as well as the worker may use that for personal

reasons, or if the car is parked in the customer's office parking, the vehicle is deemed private on

every particular day.

CONCLUSION

Following the completion of the study, it was decided that a systematic oversimplifying of

numerous aspects of the Australian Income Tax Appraisal Act should always be required in

determining the taxable income. Furthermore, based on the situation, various provisions may be

added. Susanne's taxation duty is estimated in the report after the enforcement of various

legislation and is estimated as S32187. The FBT measurement was also done for automobile

fringe of society, which yielded $3333 after the statutory formula procedure was applied.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Barkoczy, S. and Wilkinson, T., 2019. Australia’s Formal Venture Capital Tax Incentive

Programs. In Incentivising Angels (pp. 29-39). Springer, Singapore.

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax

Treaties", IBFD: Amsterdam.

Maurer, L. and Walker, J., 2017. A Brave New Post-BEPS World: New Double Tax Treaty

Between Germany and Australia Implements BEPS Measures. Intertax, 45(4).

McClure, R., Lanis, R. and Govendir, B., 2017. Investigation into the Petroleum Resource Rent

Tax and Debt Loading in Australia–2012 to 2016.

Nery, T., Polyakov, M., Sadler, R. and White, B., 2019. Spatial patterns of boom and bust

forestry investment development: A case study from Western Australia. Land Use

Policy, 86, pp.67-77.

Ssennyonjo, P., 2019. A comparative study of tax incentives for small businesses in South Africa,

Australia, India and the United Kingdom (Doctoral dissertation).

Whiteford, P. and Heron, A., 2018. Australia: Providing social protection to non-standard

workers with tax financing.

Books and Journals

Barkoczy, S. and Wilkinson, T., 2019. Australia’s Formal Venture Capital Tax Incentive

Programs. In Incentivising Angels (pp. 29-39). Springer, Singapore.

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax

Treaties", IBFD: Amsterdam.

Maurer, L. and Walker, J., 2017. A Brave New Post-BEPS World: New Double Tax Treaty

Between Germany and Australia Implements BEPS Measures. Intertax, 45(4).

McClure, R., Lanis, R. and Govendir, B., 2017. Investigation into the Petroleum Resource Rent

Tax and Debt Loading in Australia–2012 to 2016.

Nery, T., Polyakov, M., Sadler, R. and White, B., 2019. Spatial patterns of boom and bust

forestry investment development: A case study from Western Australia. Land Use

Policy, 86, pp.67-77.

Ssennyonjo, P., 2019. A comparative study of tax incentives for small businesses in South Africa,

Australia, India and the United Kingdom (Doctoral dissertation).

Whiteford, P. and Heron, A., 2018. Australia: Providing social protection to non-standard

workers with tax financing.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.