Comprehensive Analysis of Capital Gains and FBT - HI6028 Taxation

VerifiedAdded on 2023/06/05

|13

|3074

|116

Report

AI Summary

This assignment solution provides a detailed analysis of capital gains tax (CGT) implications for various asset disposals, including vacant land, an antique bed, paintings, and shares, considering pre-CGT status and applicable concessions. It also examines fringe benefits tax (FBT) liabilities related to a car and a loan provided to an employee, calculating taxable amounts based on statutory formulas and relevant tax rates. The analysis incorporates relevant sections of the ITAA 1997 and FBTAA 1986, along with tax rulings, to provide comprehensive advice on the tax consequences of these transactions. Desklib offers a wide range of study tools, including past papers and solved assignments, to support students in their academic endeavors.

a ation heory ractice awT x T , P & L

HI6028

Student ameN

[Pick the date]

HI6028

Student ameN

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

As a tax consultant, the objective here is to offer tax advice to the client keeping in mind the

relevant tax legislations and the taxpayer details with regards to the transactions enacted during

the given year i.e. 2017/2018. Pivotal information has been provided which serves as a starting

point. This relates to the fact that neither of the given transactions relate to business by client

which implies that any proceeds that is generated from the liquidation of various assets would be

capital in nature. Considering that capital proceeds do not attract any tax burden, hence the

relevant aspect would be only to focus on any capital gains or loss which would be derived and

hence may be subject to CGT.

Vacant Land

With regards to definition of capital asset in s. 108-5 ITAA 1997, it is apparent that vacant land

would be a capital asset. In relation to CGT application, a key aspect is the purchase data since it

is the deciding factor to separate the pre-CGT asset and non-pre-CGT assets. Any capital asset

purchased by taxpayer on or before September 19, 1985 will be labelled as pre-CGT assets while

others would not be pre-CGT assets (Wilmot, 2014). This separation is significant since s. 149-

10 ITAA 1997 states that pre-CGT assets capital gains or losses would be exempt from CGT

(Austlii, 2018).

The process of computation of capital gains is initiated with the obtaining of capital proceeds on

any asset which is referred to as a CGT event. The various CGT events are summarised in s. 104-

5. It is imperative to refer to the relevant CGT event which takes place as the underlying

computation of capital gains is driven by the type of CGT event. The relevant event when

disposal of an asset take place is referred to as A1. For computation of capital gains under this

event, a critical input that is required is cost base which has been explained in s. 110-25 ITAA

1997 (Krever, 2017). The key components accordingly that are included in cost base

computation as listed below.

1

As a tax consultant, the objective here is to offer tax advice to the client keeping in mind the

relevant tax legislations and the taxpayer details with regards to the transactions enacted during

the given year i.e. 2017/2018. Pivotal information has been provided which serves as a starting

point. This relates to the fact that neither of the given transactions relate to business by client

which implies that any proceeds that is generated from the liquidation of various assets would be

capital in nature. Considering that capital proceeds do not attract any tax burden, hence the

relevant aspect would be only to focus on any capital gains or loss which would be derived and

hence may be subject to CGT.

Vacant Land

With regards to definition of capital asset in s. 108-5 ITAA 1997, it is apparent that vacant land

would be a capital asset. In relation to CGT application, a key aspect is the purchase data since it

is the deciding factor to separate the pre-CGT asset and non-pre-CGT assets. Any capital asset

purchased by taxpayer on or before September 19, 1985 will be labelled as pre-CGT assets while

others would not be pre-CGT assets (Wilmot, 2014). This separation is significant since s. 149-

10 ITAA 1997 states that pre-CGT assets capital gains or losses would be exempt from CGT

(Austlii, 2018).

The process of computation of capital gains is initiated with the obtaining of capital proceeds on

any asset which is referred to as a CGT event. The various CGT events are summarised in s. 104-

5. It is imperative to refer to the relevant CGT event which takes place as the underlying

computation of capital gains is driven by the type of CGT event. The relevant event when

disposal of an asset take place is referred to as A1. For computation of capital gains under this

event, a critical input that is required is cost base which has been explained in s. 110-25 ITAA

1997 (Krever, 2017). The key components accordingly that are included in cost base

computation as listed below.

1

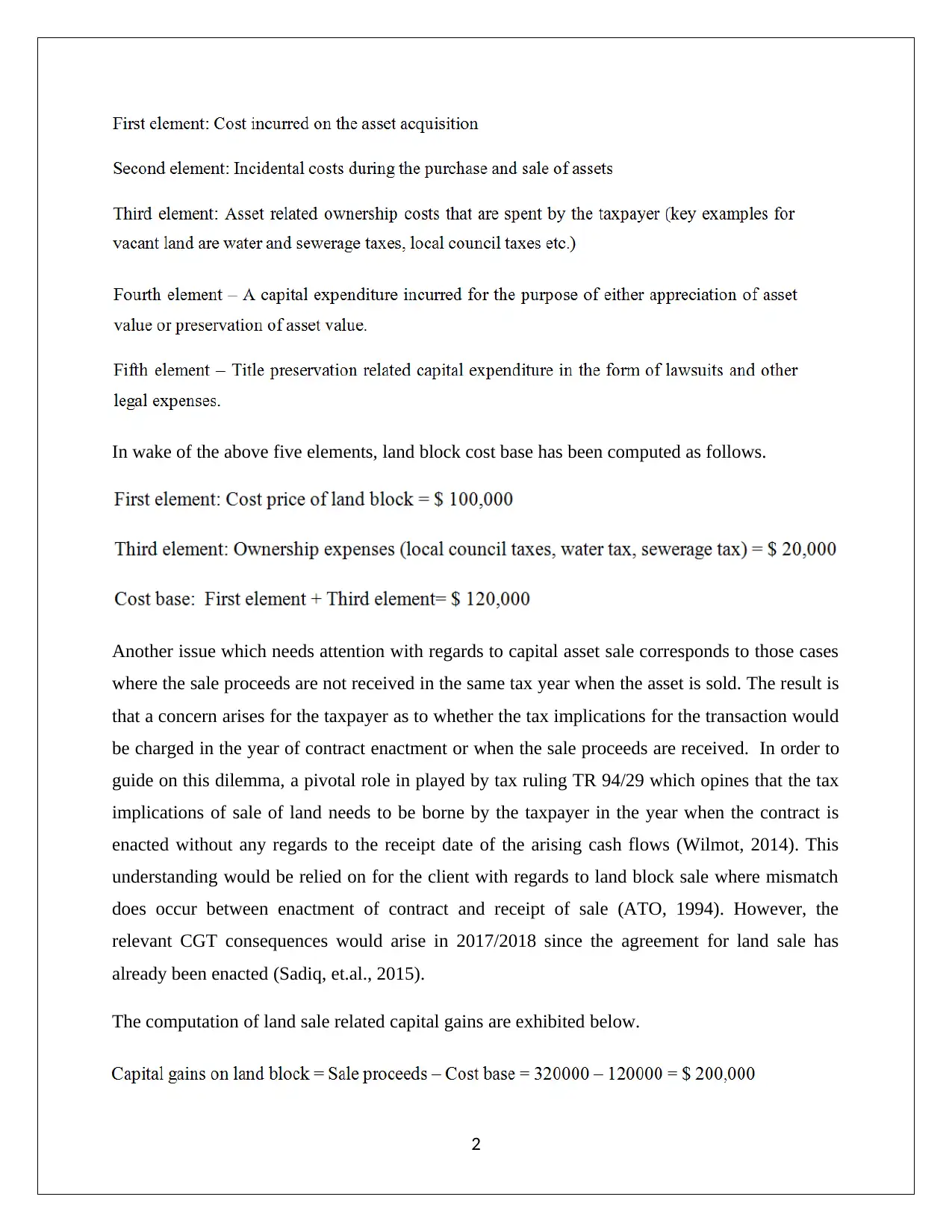

In wake of the above five elements, land block cost base has been computed as follows.

Another issue which needs attention with regards to capital asset sale corresponds to those cases

where the sale proceeds are not received in the same tax year when the asset is sold. The result is

that a concern arises for the taxpayer as to whether the tax implications for the transaction would

be charged in the year of contract enactment or when the sale proceeds are received. In order to

guide on this dilemma, a pivotal role in played by tax ruling TR 94/29 which opines that the tax

implications of sale of land needs to be borne by the taxpayer in the year when the contract is

enacted without any regards to the receipt date of the arising cash flows (Wilmot, 2014). This

understanding would be relied on for the client with regards to land block sale where mismatch

does occur between enactment of contract and receipt of sale (ATO, 1994). However, the

relevant CGT consequences would arise in 2017/2018 since the agreement for land sale has

already been enacted (Sadiq, et.al., 2015).

The computation of land sale related capital gains are exhibited below.

2

Another issue which needs attention with regards to capital asset sale corresponds to those cases

where the sale proceeds are not received in the same tax year when the asset is sold. The result is

that a concern arises for the taxpayer as to whether the tax implications for the transaction would

be charged in the year of contract enactment or when the sale proceeds are received. In order to

guide on this dilemma, a pivotal role in played by tax ruling TR 94/29 which opines that the tax

implications of sale of land needs to be borne by the taxpayer in the year when the contract is

enacted without any regards to the receipt date of the arising cash flows (Wilmot, 2014). This

understanding would be relied on for the client with regards to land block sale where mismatch

does occur between enactment of contract and receipt of sale (ATO, 1994). However, the

relevant CGT consequences would arise in 2017/2018 since the agreement for land sale has

already been enacted (Sadiq, et.al., 2015).

The computation of land sale related capital gains are exhibited below.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Additional consideration needs to be given to the capital losses which have come forward and

stand at $ 7,000 (excluding sculpture losses) and the same be used to lower the capital gains

computed above. Post adjustment capital gains = 20000 – 7000 = $ 193,000

Concessions on the above capital gains can be gained in line with s. 115-25 ITAA 1997 which

highlights that as per the discount method, 50% of the capital gains can be reduced provided

these are long term in nature. The capital gains would be long term only if the ownership period

of the asset has exceeded 1 year period (Nethercott, Richardson and Devos, 2016). This is true

for the given asset.

Antique Bed

The act of stealing of the antique bed (which is not a pre-CGT asset) has triggered the CGT event

A1 as mentioned in a. 104-5 ITAA 1997. Thus, there is a need to determine the underlying

capital gains or losses on the antique bed by subtracting the cost base (computed as per s. 110-

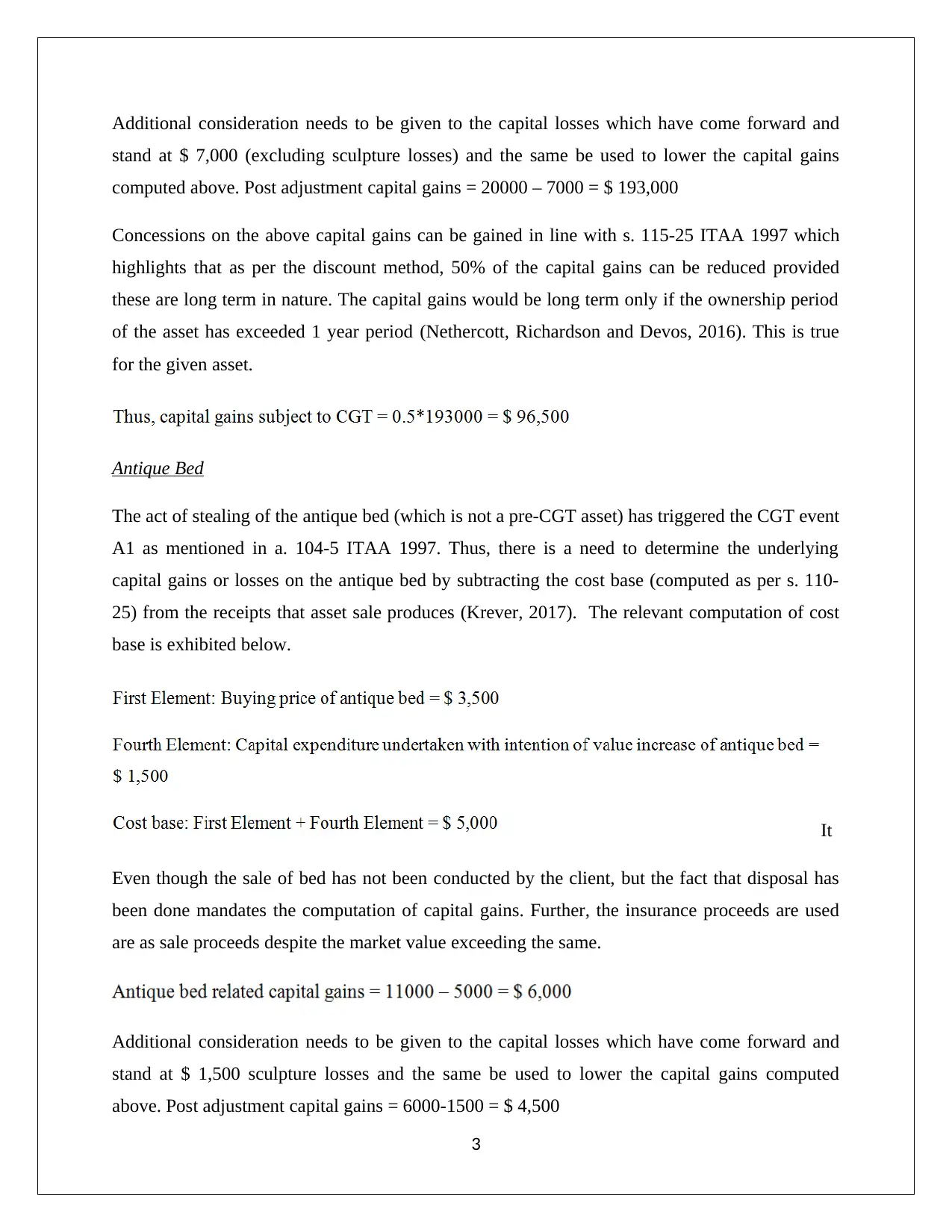

25) from the receipts that asset sale produces (Krever, 2017). The relevant computation of cost

base is exhibited below.

It

Even though the sale of bed has not been conducted by the client, but the fact that disposal has

been done mandates the computation of capital gains. Further, the insurance proceeds are used

are as sale proceeds despite the market value exceeding the same.

Additional consideration needs to be given to the capital losses which have come forward and

stand at $ 1,500 sculpture losses and the same be used to lower the capital gains computed

above. Post adjustment capital gains = 6000-1500 = $ 4,500

3

stand at $ 7,000 (excluding sculpture losses) and the same be used to lower the capital gains

computed above. Post adjustment capital gains = 20000 – 7000 = $ 193,000

Concessions on the above capital gains can be gained in line with s. 115-25 ITAA 1997 which

highlights that as per the discount method, 50% of the capital gains can be reduced provided

these are long term in nature. The capital gains would be long term only if the ownership period

of the asset has exceeded 1 year period (Nethercott, Richardson and Devos, 2016). This is true

for the given asset.

Antique Bed

The act of stealing of the antique bed (which is not a pre-CGT asset) has triggered the CGT event

A1 as mentioned in a. 104-5 ITAA 1997. Thus, there is a need to determine the underlying

capital gains or losses on the antique bed by subtracting the cost base (computed as per s. 110-

25) from the receipts that asset sale produces (Krever, 2017). The relevant computation of cost

base is exhibited below.

It

Even though the sale of bed has not been conducted by the client, but the fact that disposal has

been done mandates the computation of capital gains. Further, the insurance proceeds are used

are as sale proceeds despite the market value exceeding the same.

Additional consideration needs to be given to the capital losses which have come forward and

stand at $ 1,500 sculpture losses and the same be used to lower the capital gains computed

above. Post adjustment capital gains = 6000-1500 = $ 4,500

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Concessions on the above capital gains can be gained in line with s. 115-25 ITAA 1997 which

highlights that as per the discount method, 50% of the capital gains can be reduced provided

these are long term in nature (Woellner, 2017). The capital gains would be long term only if the

ownership period of the asset has exceeded 1 year period. This is true for the given asset.

Painting

The critical factor with regards to this asset is the purchase date which dates before September

19, 1985, thus implying that the given asset is a pre-CGT asset owing to purchase being made in

the era when CGT was not applicable on capital gains (Nethercott, Richardson and Devos,

2016). As a result, for this asset CGT consequences would not arise as per s. 149-10 ITAA 1997

and hence capital gains /losses derived from asset sale are ignored.

Shares

The sale of shares would trigger a CGT event named as A1 in accordance with s. 104-5 ITAA

1997 (Hodgson,Mortimer and Butler, 2016). The requisition capital gains or losses derived for

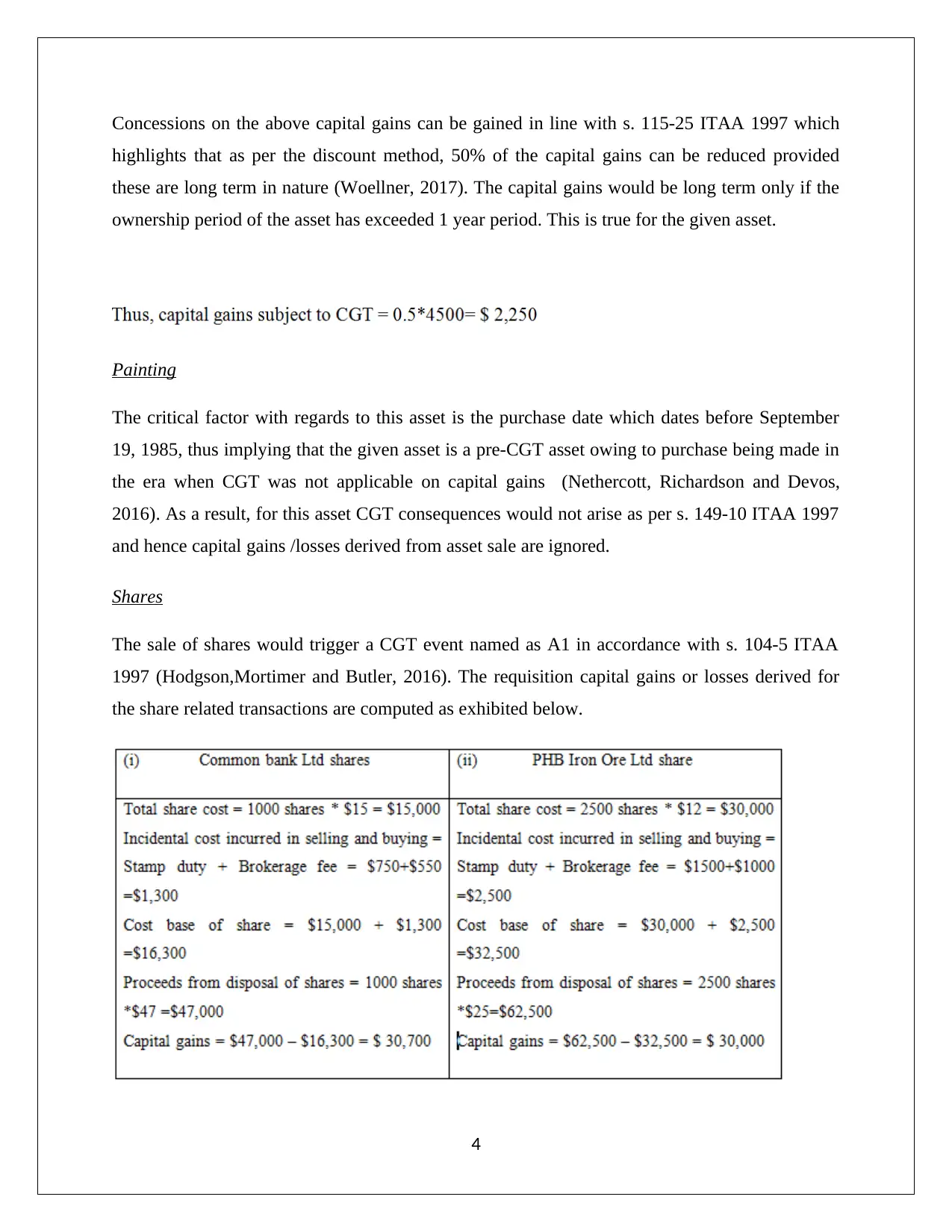

the share related transactions are computed as exhibited below.

4

highlights that as per the discount method, 50% of the capital gains can be reduced provided

these are long term in nature (Woellner, 2017). The capital gains would be long term only if the

ownership period of the asset has exceeded 1 year period. This is true for the given asset.

Painting

The critical factor with regards to this asset is the purchase date which dates before September

19, 1985, thus implying that the given asset is a pre-CGT asset owing to purchase being made in

the era when CGT was not applicable on capital gains (Nethercott, Richardson and Devos,

2016). As a result, for this asset CGT consequences would not arise as per s. 149-10 ITAA 1997

and hence capital gains /losses derived from asset sale are ignored.

Shares

The sale of shares would trigger a CGT event named as A1 in accordance with s. 104-5 ITAA

1997 (Hodgson,Mortimer and Butler, 2016). The requisition capital gains or losses derived for

the share related transactions are computed as exhibited below.

4

Concessions on the above capital gains can be gained in line with s. 115-25 ITAA 1997 which

highlights that as per the discount method, 50% of the capital gains can be reduced provided

these are long term in nature. The capital gains would be long term only if the ownership period

of the asset has exceeded 1 year period. This is true for the all the given shares besides Build Ltd

where the holding period is lesser than a month.

Violin

With regards to the information provided in this context, the client comes across as a person who

is really fond of violins and can play violin very well. Further, the client maintains a lot of

violins and she tends to use these for her entertainment whereby she plays them (Coleman,

2016). As a result, the given violin instead of being termed as a collectable would be more an

object for the personal use of the client. In case of such items, CGT consequences tend to be

levied only when the underlying asset has been bought by the taxpayer for an amount not lesser

than $ 10,000. This limit is clearly not being met for the violin under consideration which has

been bought for a mere consideration of $ 5,500. As a result, no CGT would apply on the

obtained capital gains from the violin sale.

Cumulative Capital Gains

5

highlights that as per the discount method, 50% of the capital gains can be reduced provided

these are long term in nature. The capital gains would be long term only if the ownership period

of the asset has exceeded 1 year period. This is true for the all the given shares besides Build Ltd

where the holding period is lesser than a month.

Violin

With regards to the information provided in this context, the client comes across as a person who

is really fond of violins and can play violin very well. Further, the client maintains a lot of

violins and she tends to use these for her entertainment whereby she plays them (Coleman,

2016). As a result, the given violin instead of being termed as a collectable would be more an

object for the personal use of the client. In case of such items, CGT consequences tend to be

levied only when the underlying asset has been bought by the taxpayer for an amount not lesser

than $ 10,000. This limit is clearly not being met for the violin under consideration which has

been bought for a mere consideration of $ 5,500. As a result, no CGT would apply on the

obtained capital gains from the violin sale.

Cumulative Capital Gains

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

(a) Fringe Benefits

There are certain personal benefits (non-cash form) which the employer gives to employees

(and/or associates) and these are referred to fringe benefits). These benefits are unique in the

sense that the tax consequences of these is not borne by the recipient of benefit but by the entity

which provides the benefit. As a result, in accordance with Fringe Benefits Assessment Act 1986

(FBTAA 1986), employer has to bear the complete tax liability arising from consumption of

these benefits by the employer. The various steps involved in the computation of FBT liability

for the various fringe benefits are extended below (Barkoczy, 2017).

Key information that would be used for computation of FBT liability for the employer includes

that the relevant tax year is 2017/2018 with the employee being Jasmine and employer being

Rapid Heat Pty Ltd. Further, the tax implications need to be highlighted in the wake of FBTAA

1986 (Coleman, 2016).

Car - First benefit

If an employer offers car to employer for his/her use, then the nature of use determines the

extension of car fringe benefits. In accordance with s. 7, FBTAA 1986, car fringe benefit would

only extend when the car is permissible for personal use by the employee. The actual use and the

underlying extent in this regards are not pivotal factor especially if s. 9 FBTAA 1986 statutory

formula approach is being used for computation of taxable car fringe benefits

(Hodgson,Mortimer and Butler, 2016). The key inputs required in this regards are discussed as

shown below.

6

(a) Fringe Benefits

There are certain personal benefits (non-cash form) which the employer gives to employees

(and/or associates) and these are referred to fringe benefits). These benefits are unique in the

sense that the tax consequences of these is not borne by the recipient of benefit but by the entity

which provides the benefit. As a result, in accordance with Fringe Benefits Assessment Act 1986

(FBTAA 1986), employer has to bear the complete tax liability arising from consumption of

these benefits by the employer. The various steps involved in the computation of FBT liability

for the various fringe benefits are extended below (Barkoczy, 2017).

Key information that would be used for computation of FBT liability for the employer includes

that the relevant tax year is 2017/2018 with the employee being Jasmine and employer being

Rapid Heat Pty Ltd. Further, the tax implications need to be highlighted in the wake of FBTAA

1986 (Coleman, 2016).

Car - First benefit

If an employer offers car to employer for his/her use, then the nature of use determines the

extension of car fringe benefits. In accordance with s. 7, FBTAA 1986, car fringe benefit would

only extend when the car is permissible for personal use by the employee. The actual use and the

underlying extent in this regards are not pivotal factor especially if s. 9 FBTAA 1986 statutory

formula approach is being used for computation of taxable car fringe benefits

(Hodgson,Mortimer and Butler, 2016). The key inputs required in this regards are discussed as

shown below.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Car Cost Base

The car cost base would be arrived after making deduction for any repairs from the purchase

price of the vehicle (Gilders, et. al., 2015). Based on the given information, it is apparent that the

car has been purchased by Rapid Heat for $ 33,000 with expenses on minor repairs to the extent

of $ 550 which have been borne by the employer.

Period of car assess ability

Another key factor is the duration in the given tax year for which the employee could use the car

provided by employer for personal use. The information provided clearly highlights that

extension of car by Rapid Heat to Jasmine was done on 1st May, 2017 and till the end of the

financial year FY2018, the car was with Jasmine with permission for personal use. Hence,

deduction of 30 days would be done for the month of April 2017 when the car was not available.

Based on the information provided, car was in the garage for five days with the purpose of

getting minor repairs done. Also, in relation to the car being parked at the airport parking for a

period of 10 days no deduction is permissible as the car was available for use but the employee

was absent from the town and the associates decided not to use the same.

Gross up factor

In accordance with GST Act 1999, it is apparent that car does attract GST and hence the

appropriate gross up factor for the given year would be 2.0802.

Fringe benefits tax rate

For FY2018, the relevant FBT rate has been declared as 47%.

7

The car cost base would be arrived after making deduction for any repairs from the purchase

price of the vehicle (Gilders, et. al., 2015). Based on the given information, it is apparent that the

car has been purchased by Rapid Heat for $ 33,000 with expenses on minor repairs to the extent

of $ 550 which have been borne by the employer.

Period of car assess ability

Another key factor is the duration in the given tax year for which the employee could use the car

provided by employer for personal use. The information provided clearly highlights that

extension of car by Rapid Heat to Jasmine was done on 1st May, 2017 and till the end of the

financial year FY2018, the car was with Jasmine with permission for personal use. Hence,

deduction of 30 days would be done for the month of April 2017 when the car was not available.

Based on the information provided, car was in the garage for five days with the purpose of

getting minor repairs done. Also, in relation to the car being parked at the airport parking for a

period of 10 days no deduction is permissible as the car was available for use but the employee

was absent from the town and the associates decided not to use the same.

Gross up factor

In accordance with GST Act 1999, it is apparent that car does attract GST and hence the

appropriate gross up factor for the given year would be 2.0802.

Fringe benefits tax rate

For FY2018, the relevant FBT rate has been declared as 47%.

7

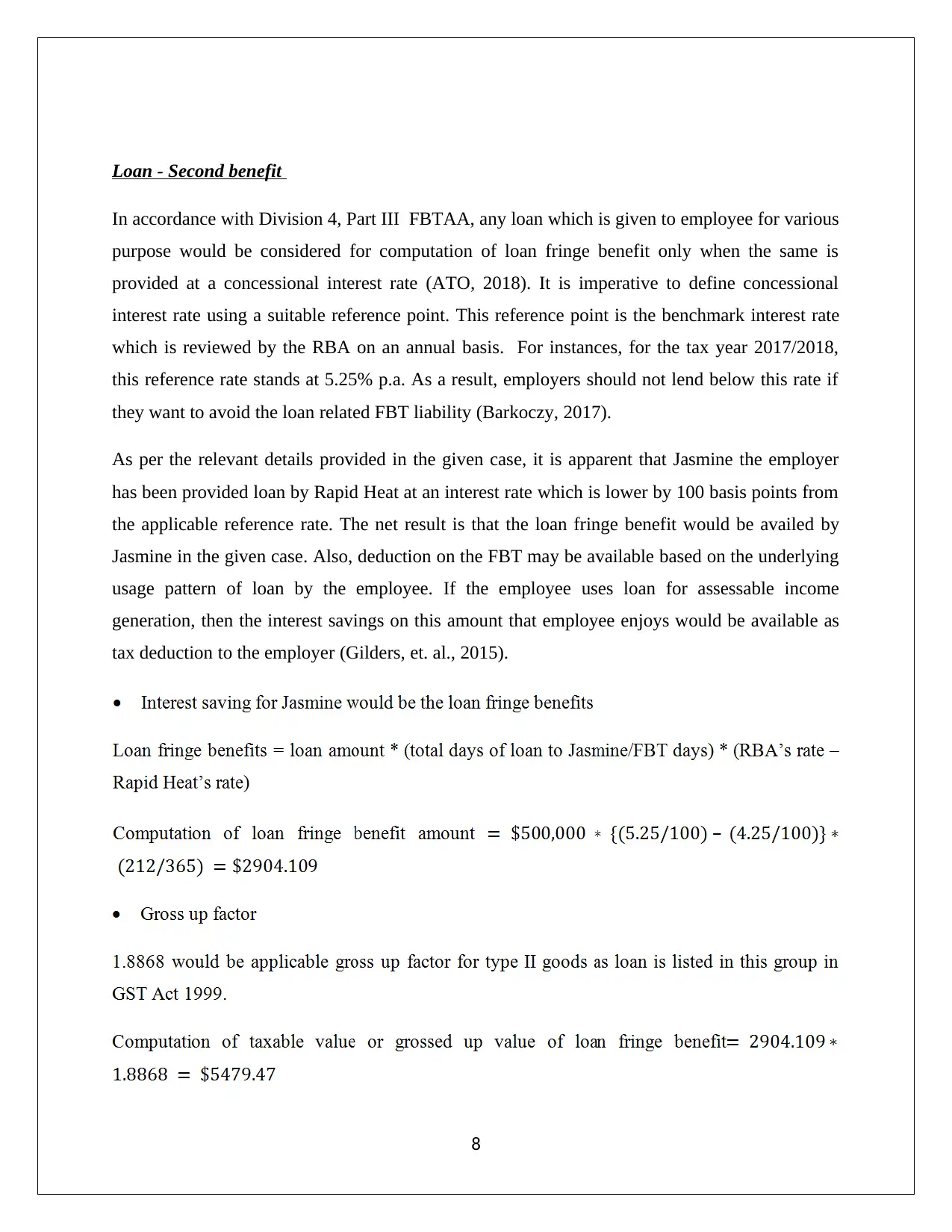

Loan - Second benefit

In accordance with Division 4, Part III FBTAA, any loan which is given to employee for various

purpose would be considered for computation of loan fringe benefit only when the same is

provided at a concessional interest rate (ATO, 2018). It is imperative to define concessional

interest rate using a suitable reference point. This reference point is the benchmark interest rate

which is reviewed by the RBA on an annual basis. For instances, for the tax year 2017/2018,

this reference rate stands at 5.25% p.a. As a result, employers should not lend below this rate if

they want to avoid the loan related FBT liability (Barkoczy, 2017).

As per the relevant details provided in the given case, it is apparent that Jasmine the employer

has been provided loan by Rapid Heat at an interest rate which is lower by 100 basis points from

the applicable reference rate. The net result is that the loan fringe benefit would be availed by

Jasmine in the given case. Also, deduction on the FBT may be available based on the underlying

usage pattern of loan by the employee. If the employee uses loan for assessable income

generation, then the interest savings on this amount that employee enjoys would be available as

tax deduction to the employer (Gilders, et. al., 2015).

8

In accordance with Division 4, Part III FBTAA, any loan which is given to employee for various

purpose would be considered for computation of loan fringe benefit only when the same is

provided at a concessional interest rate (ATO, 2018). It is imperative to define concessional

interest rate using a suitable reference point. This reference point is the benchmark interest rate

which is reviewed by the RBA on an annual basis. For instances, for the tax year 2017/2018,

this reference rate stands at 5.25% p.a. As a result, employers should not lend below this rate if

they want to avoid the loan related FBT liability (Barkoczy, 2017).

As per the relevant details provided in the given case, it is apparent that Jasmine the employer

has been provided loan by Rapid Heat at an interest rate which is lower by 100 basis points from

the applicable reference rate. The net result is that the loan fringe benefit would be availed by

Jasmine in the given case. Also, deduction on the FBT may be available based on the underlying

usage pattern of loan by the employee. If the employee uses loan for assessable income

generation, then the interest savings on this amount that employee enjoys would be available as

tax deduction to the employer (Gilders, et. al., 2015).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The loan amount which has been extended to Jasmine is $ 500,000. This has been divided into

two tranches of $ 450,000 and $ 50,000. The first tranche of $ 450,000 has been used by Jasmine

to buy a holiday home and it is reasonable that the same would be used for income producing as

rent. Hence, employer (Rapid Heat) would be able to claim for deduction on the interest savings

provided to employee on this amount. But, the second tranche comprising of $ 50,000 is used by

Jasmine’s husband for making investments in share. Even though it is likely that assessable

income is generated from shares especially from dividend but still the employer is not benefitted

in the form of tax deduction since as per FBTAA 1986, deduction is limited for the use by

employer only and not by associate (Reuters, 2017).

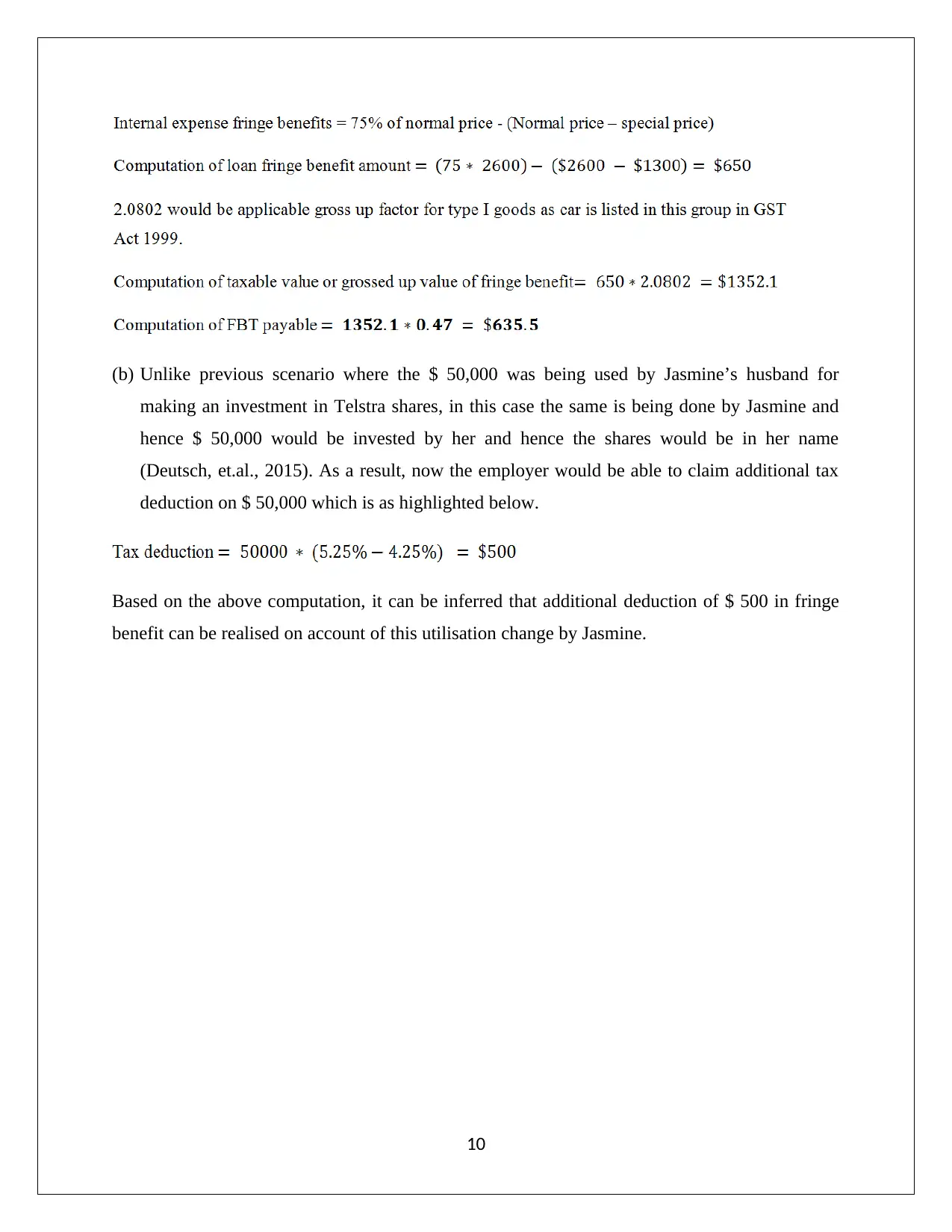

Electric Heater - Third benefit

Employers may also reduce the personal expenses for employees by meeting some of their

personal expenses. In this regards, a special case arises when the employer tends to pay for an

internally produced product which would culminate in the form of internal expense fringe

benefits (Deutsch, et.al., 2015). As per the information provided, the heater manufactured by the

company (Rapid Heat) tends to sold to any customer at a retail price of $ 1,300. Hence, in the

lack of any fringe benefits, the same amount would have to be spent by Jasmine. But the

employer only takes half of this amount from Jasmine and pays the remaining half on its own.

This benefit in regards to personal expense of Jasmine does give rise to internal expense fringe

benefit.

9

two tranches of $ 450,000 and $ 50,000. The first tranche of $ 450,000 has been used by Jasmine

to buy a holiday home and it is reasonable that the same would be used for income producing as

rent. Hence, employer (Rapid Heat) would be able to claim for deduction on the interest savings

provided to employee on this amount. But, the second tranche comprising of $ 50,000 is used by

Jasmine’s husband for making investments in share. Even though it is likely that assessable

income is generated from shares especially from dividend but still the employer is not benefitted

in the form of tax deduction since as per FBTAA 1986, deduction is limited for the use by

employer only and not by associate (Reuters, 2017).

Electric Heater - Third benefit

Employers may also reduce the personal expenses for employees by meeting some of their

personal expenses. In this regards, a special case arises when the employer tends to pay for an

internally produced product which would culminate in the form of internal expense fringe

benefits (Deutsch, et.al., 2015). As per the information provided, the heater manufactured by the

company (Rapid Heat) tends to sold to any customer at a retail price of $ 1,300. Hence, in the

lack of any fringe benefits, the same amount would have to be spent by Jasmine. But the

employer only takes half of this amount from Jasmine and pays the remaining half on its own.

This benefit in regards to personal expense of Jasmine does give rise to internal expense fringe

benefit.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Unlike previous scenario where the $ 50,000 was being used by Jasmine’s husband for

making an investment in Telstra shares, in this case the same is being done by Jasmine and

hence $ 50,000 would be invested by her and hence the shares would be in her name

(Deutsch, et.al., 2015). As a result, now the employer would be able to claim additional tax

deduction on $ 50,000 which is as highlighted below.

Based on the above computation, it can be inferred that additional deduction of $ 500 in fringe

benefit can be realised on account of this utilisation change by Jasmine.

10

making an investment in Telstra shares, in this case the same is being done by Jasmine and

hence $ 50,000 would be invested by her and hence the shares would be in her name

(Deutsch, et.al., 2015). As a result, now the employer would be able to claim additional tax

deduction on $ 50,000 which is as highlighted below.

Based on the above computation, it can be inferred that additional deduction of $ 500 in fringe

benefit can be realised on account of this utilisation change by Jasmine.

10

References

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 26 September 2018)

ATO, (2018) Fringe Benefits Tax- A Guide For Employers.

http://law.ato.gov.au/atolaw/view.htm?DocID=SAV%2FFBTGEMP%2F00010 (Accessed: 26

September 2018)

Austlii, (2018) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 26

September 2018)

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2015) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

11

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 26 September 2018)

ATO, (2018) Fringe Benefits Tax- A Guide For Employers.

http://law.ato.gov.au/atolaw/view.htm?DocID=SAV%2FFBTGEMP%2F00010 (Accessed: 26

September 2018)

Austlii, (2018) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 26

September 2018)

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2015) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.