Taxation Theory, Pactice and Law

21 Pages3480 Words181 Views

Added on 2020-10-22

Taxation Theory, Pactice and Law

Added on 2020-10-22

ShareRelated Documents

TAXATION THEORY,PRACTICE & LAW

TABLE OF CONTENTSINTRODUCTION...........................................................................................................................1QUESTION 1...................................................................................................................................1Determining the net capital gain of client as on 30 June 2018 ..............................................1QUESTION 2...................................................................................................................................2(a) Advising Jasmine in analysing FBT on various assets.....................................................2(b) Analysing the tax consequences as per loan amount will be used by Jasmine in purchasingsecurities.................................................................................................................................7CONCLUSION................................................................................................................................8REFERENCES................................................................................................................................9

INTRODUCTIONThe report is about the taxation theory and practice law. Theory of taxation includes lotsof taxes which are payable and not to be payable by clients in the organisation. Taxation theoryand practise law, the tax are automatically identified because the tax payers have to pay someproportion to the government benefits they receive. This assignment will present the clients netcapital gain or loss according to the information given. the report will provide the deep insight ofmeaning of fringe benefits tax with the steps of calculation. Present assignment will calculate thefringe benefit liability in tax credit relation. Later, the report will also identify the non-fringebenefit amount according to the given information. QUESTION 1Determining the net capital gain of client as on 30 June 2018 The rise in the value of a capital assets that provides the higher worth than the price ofpurchase is known as capital assets. Until the assets are sold gain is not realized. There are twotypes of capital gain that are short term which are less than one year and others are long termwhich are considered to be more than one year (Paolella and Durand, 2016). It is a profit or earnings that comes from the sale of the capital assets is known as capitalgain. This profit is counted as an income of the payee and therefore, charged to tax for the year atwhich transfer of the capital tax place. If there is no sale of asset, only the transfer of propertytakes place, here the capital gain does not apply (Weber, 2014). However, if this capital asset issell by the individual who owned it, the capital gain will be applicable. The Income Tax Act hasgenerally exempted possession acceptable as gifts by way of an acquisition or will.Below the various information with calculation and interpretation has been discussed.Block of Vacant LandIn this scenario, the client has done legal agreement to sell block of vacant land for$320000. in 2001, she has purchased this land for $100,000 and makes $20000 other expenseslike local council, water sewerage rates and land taxes. The below listed the calculation of hercapital gains. 1

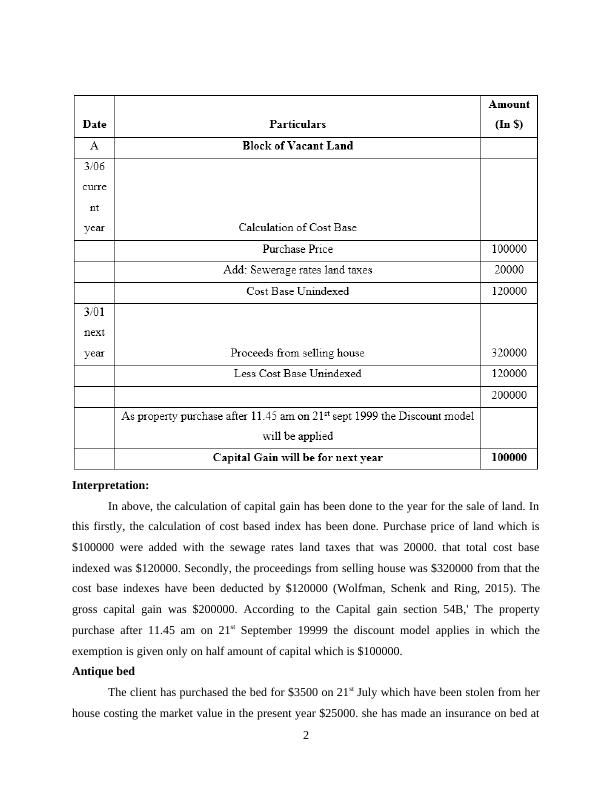

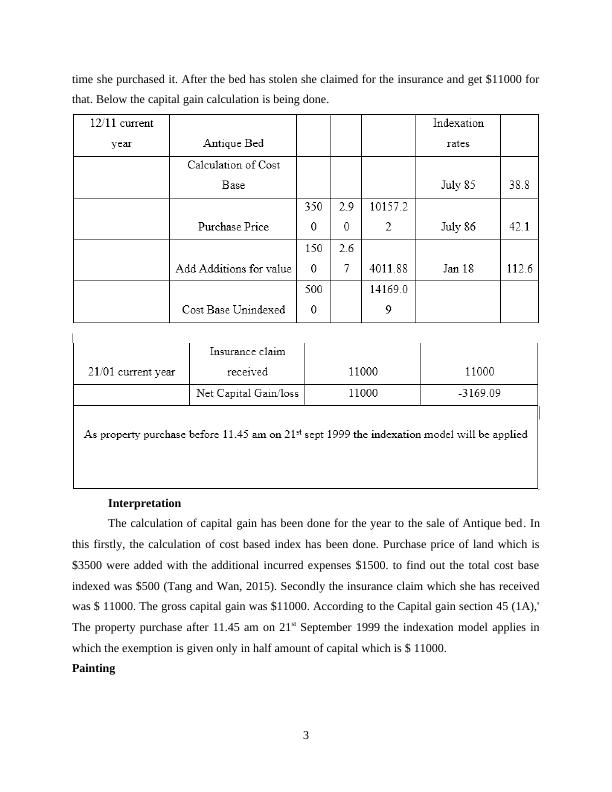

Interpretation: In above, the calculation of capital gain has been done to the year for the sale of land. Inthis firstly, the calculation of cost based index has been done. Purchase price of land which is$100000 were added with the sewage rates land taxes that was 20000. that total cost baseindexed was $120000. Secondly, the proceedings from selling house was $320000 from that thecost base indexes have been deducted by $120000 (Wolfman, Schenk and Ring, 2015). Thegross capital gain was $200000. According to the Capital gain section 54B,' The propertypurchase after 11.45 am on 21st September 19999 the discount model applies in which theexemption is given only on half amount of capital which is $100000. Antique bedThe client has purchased the bed for $3500 on 21st July which have been stolen from herhouse costing the market value in the present year $25000. she has made an insurance on bed at2

time she purchased it. After the bed has stolen she claimed for the insurance and get $11000 forthat. Below the capital gain calculation is being done. InterpretationThe calculation of capital gain has been done for the year to the sale of Antique bed. Inthis firstly, the calculation of cost based index has been done. Purchase price of land which is$3500 were added with the additional incurred expenses $1500. to find out the total cost baseindexed was $500 (Tang and Wan, 2015). Secondly the insurance claim which she has receivedwas $ 11000. The gross capital gain was $11000. According to the Capital gain section 45 (1A),'The property purchase after 11.45 am on 21st September 1999 the indexation model applies inwhich the exemption is given only in half amount of capital which is $ 11000. Painting3

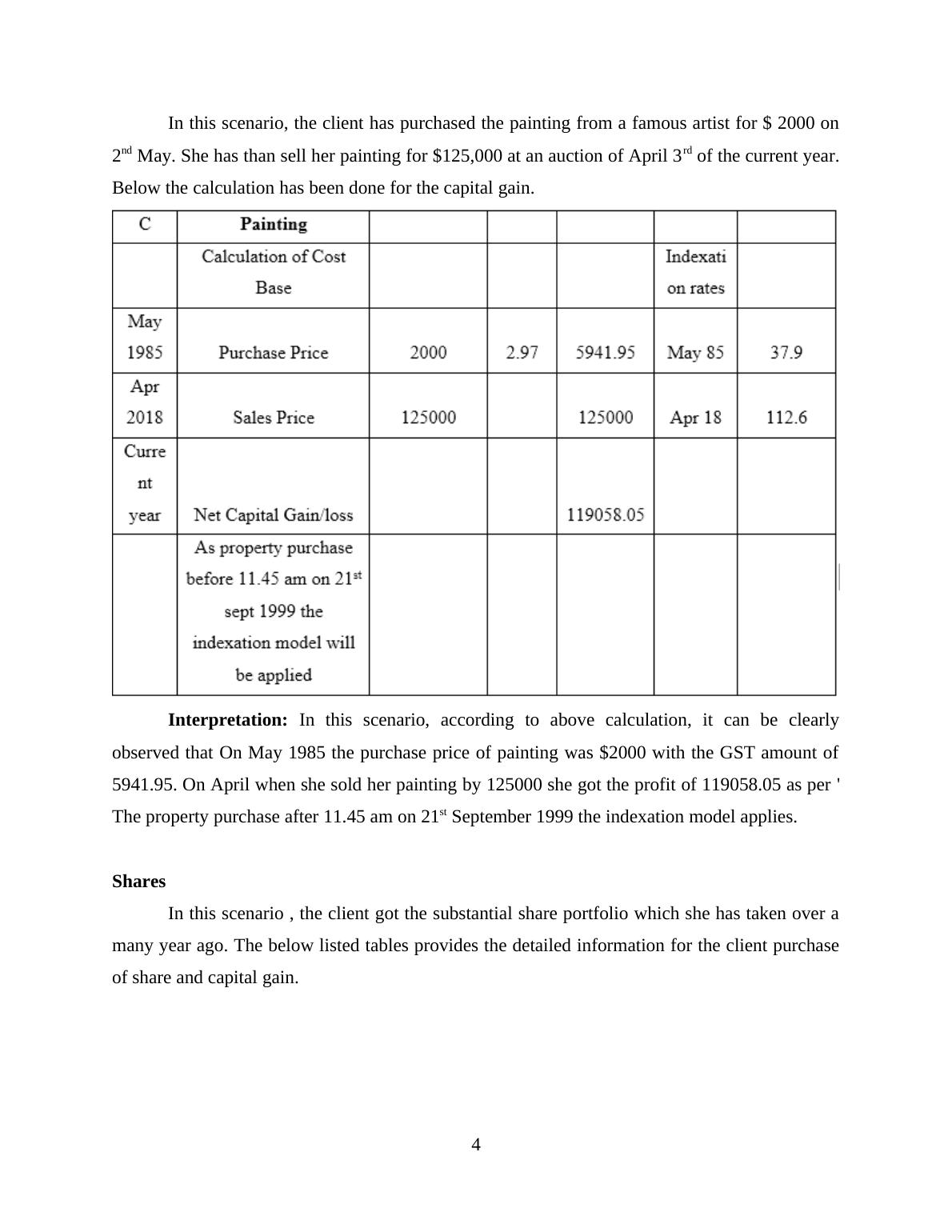

In this scenario, the client has purchased the painting from a famous artist for $ 2000 on2nd May. She has than sell her painting for $125,000 at an auction of April 3rd of the current year.Below the calculation has been done for the capital gain. Interpretation: In this scenario, according to above calculation, it can be clearlyobserved that On May 1985 the purchase price of painting was $2000 with the GST amount of5941.95. On April when she sold her painting by 125000 she got the profit of 119058.05 as per'The property purchase after 11.45 am on 21st September 1999 the indexation model applies. Shares In this scenario , the client got the substantial share portfolio which she has taken over amany year ago. The below listed tables provides the detailed information for the client purchaseof share and capital gain. 4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation Theory, Practice and Law | Assignmentlg...

|21

|3285

|273

Taxation theory, practice and law | Assignment Solutionlg...

|13

|3507

|382

Taxation Theory, Prcatice & Law - Assignmentlg...

|14

|3597

|167

Taxation Theory, Practice & Law: Assignmentlg...

|16

|3800

|365

Taxation Theory, Practice & Law - Assignmentlg...

|14

|3697

|56

Taxation Theory, Practicelg...

|13

|2969

|485