University Taxation Theory, Practice & Law Assignment - Finance

VerifiedAdded on 2023/01/06

|7

|1676

|88

Homework Assignment

AI Summary

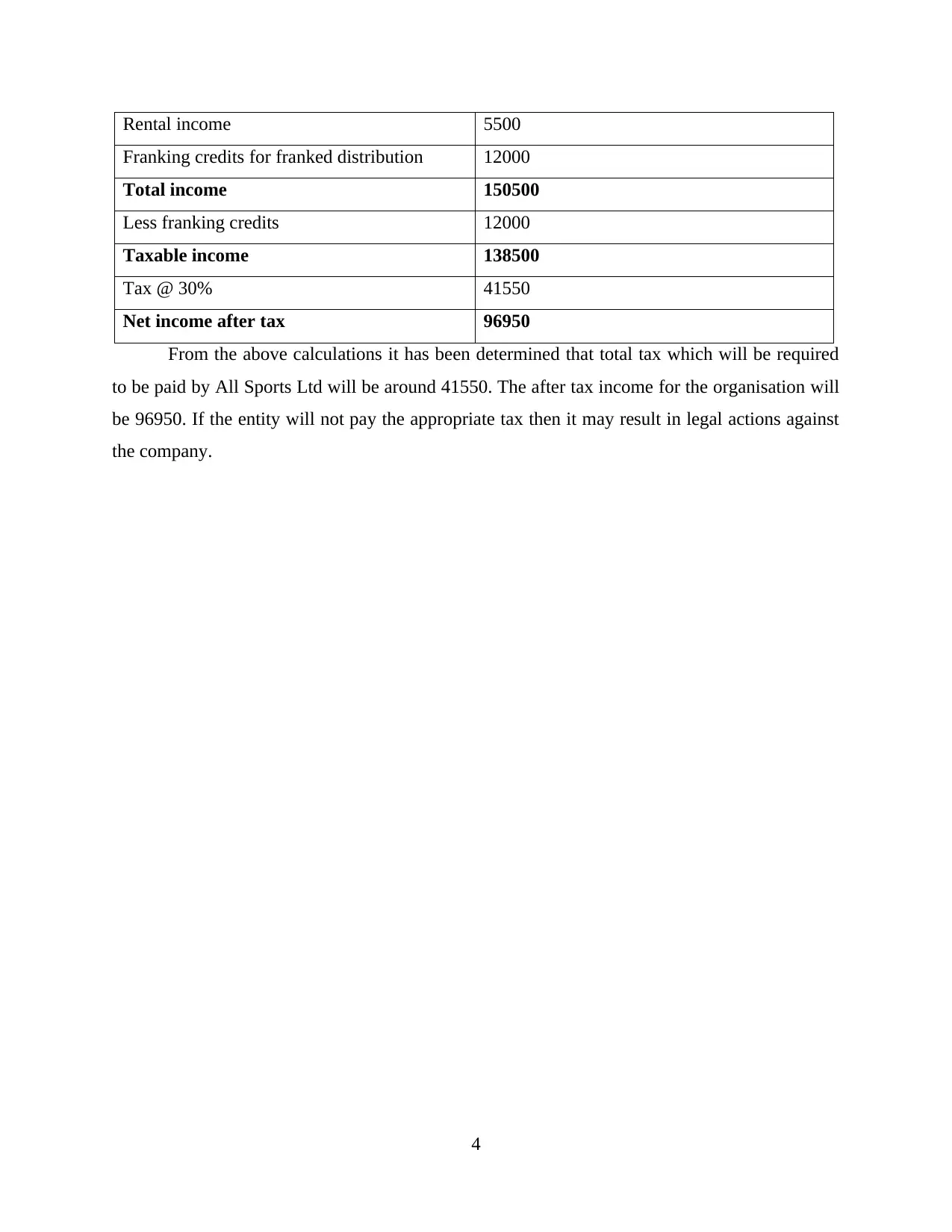

This assignment solution addresses key concepts in taxation theory and law, covering various aspects of Australian taxation. The solution begins with a question on whether an individual, Pablo, is liable to pay Australian tax on their salary, detailing the tax rate for non-residents and the calculation of tax payable. The solution then explores the Californian Copper Syndicate Ltd v Harris case, explaining the court's outcomes and Lord Young's reasoning regarding the taxation of profits. Furthermore, the assignment addresses the GST consequences for two companies, Surfs Up P/L and Billapong P/L, detailing how GST is applied to sales and returns of goods. Finally, the assignment provides a calculation of the net payable tax for All Sports Ltd, including income from trading, distributions, and rental income, along with the application of franking credits and the final tax liability. The document concludes with a list of relevant references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.