Taxation Theory, Practice & Law: A Detailed Assignment

VerifiedAdded on 2020/07/22

|8

|2396

|494

Homework Assignment

AI Summary

This assignment provides a detailed analysis of taxation law, encompassing five key questions. The first question examines capital gains and losses, differentiating between short and long-term gains and their tax implications. The second question focuses on fringe benefits, specifically the taxation of employer-provided loans and the calculation of taxable amounts based on statutory interest rates. Question three delves into tax avoidance strategies, analyzing a case involving a husband and wife and their property investment. The fourth question explores the Duke of Westminster's case and tax avoidance, differentiating between deeds and contracts. Finally, the fifth question addresses the taxation of income from timber sales, clarifying whether such income is classified as agricultural or forest operations. The assignment incorporates supporting evidence from various academic sources and relevant tax laws to support its conclusions.

Taxation Theory, Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................1

Introduction.................................................................................................................................1

Critical analysis:..........................................................................................................................1

Supporting Evidence:..................................................................................................................1

Conclusion:.................................................................................................................................2

Question 2........................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis:..........................................................................................................................2

Supportive evidence:...................................................................................................................3

Conclusion:.................................................................................................................................3

Question 3........................................................................................................................................3

Introduction.................................................................................................................................3

Critical analysis...........................................................................................................................4

Supporting evidence:...................................................................................................................4

Conclusion...................................................................................................................................4

Question 4........................................................................................................................................4

Introduction:................................................................................................................................4

Critical analysis:..........................................................................................................................4

Supporting evidence:...................................................................................................................5

Conclusion...................................................................................................................................5

Question 5........................................................................................................................................5

Introduction.................................................................................................................................5

Critical analyses..........................................................................................................................5

Supporting evidence....................................................................................................................5

Conclusion...................................................................................................................................5

Question 1........................................................................................................................................1

Introduction.................................................................................................................................1

Critical analysis:..........................................................................................................................1

Supporting Evidence:..................................................................................................................1

Conclusion:.................................................................................................................................2

Question 2........................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis:..........................................................................................................................2

Supportive evidence:...................................................................................................................3

Conclusion:.................................................................................................................................3

Question 3........................................................................................................................................3

Introduction.................................................................................................................................3

Critical analysis...........................................................................................................................4

Supporting evidence:...................................................................................................................4

Conclusion...................................................................................................................................4

Question 4........................................................................................................................................4

Introduction:................................................................................................................................4

Critical analysis:..........................................................................................................................4

Supporting evidence:...................................................................................................................5

Conclusion...................................................................................................................................5

Question 5........................................................................................................................................5

Introduction.................................................................................................................................5

Critical analyses..........................................................................................................................5

Supporting evidence....................................................................................................................5

Conclusion...................................................................................................................................5

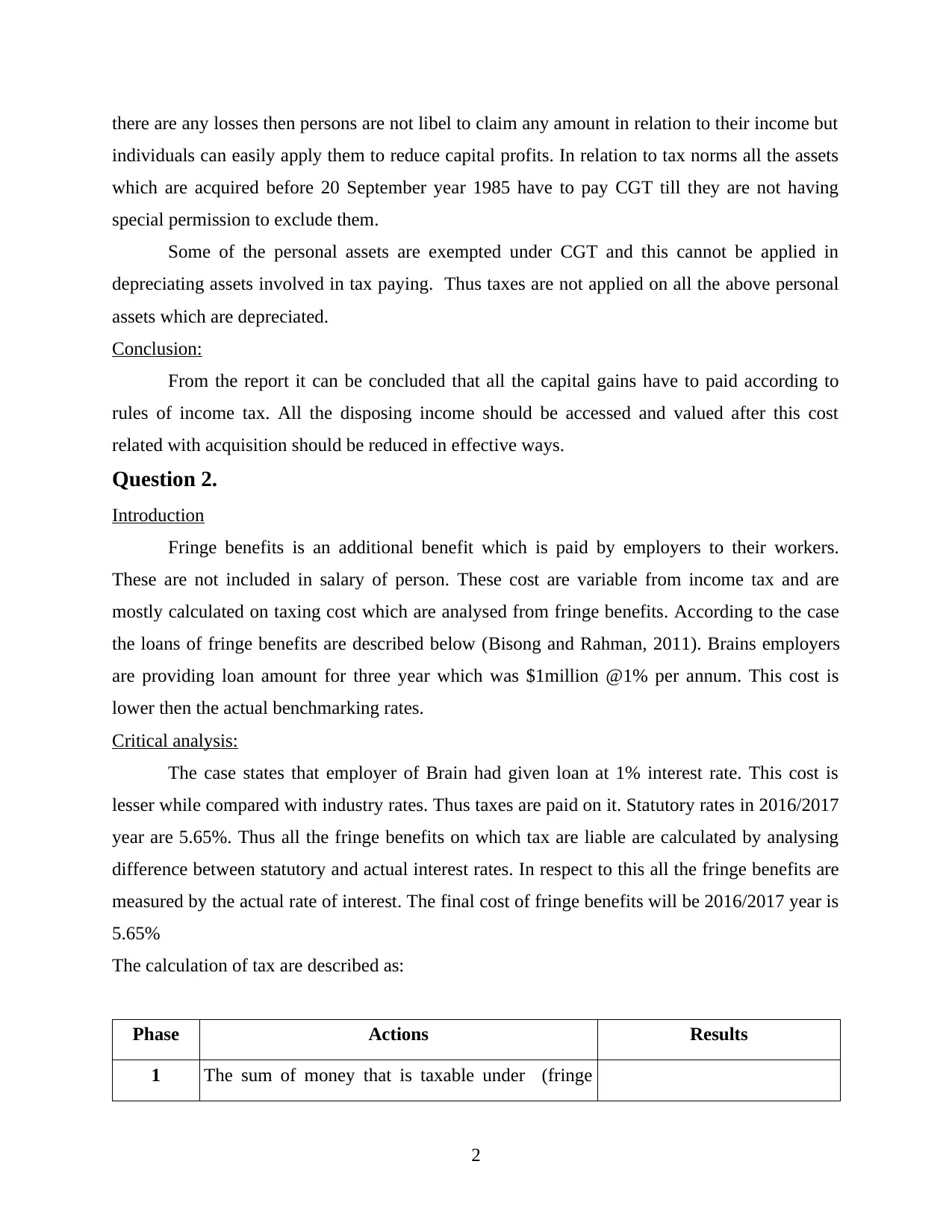

Question 1

Introduction

Capital gains or losses are calculated on the basis of scales which are analysed after

selling all assets. It can arise for long or short terms. If the property are kept with owner more

more than 2 years than it results in achievement of long term gains. Thus all tax are applicable

after analysing cost used in acquisition and then it is paid (Antwi-Agyei and et. al., 2012). If

assets are used for less then 2 years thus taxes are paid directly.

Critical analysis:

According to given case Eric had acquired assets before 12 months. This implies that

person have to pay tax for short time duration. The assets which are acquired by Eric are

evaluated in the below table as:

Particulars Acquired Sale Profit/ loss

Antique base 2000 3000 1000

Antique chair 3000 1000 -2000

Painting 9000 1000 -8000

Home sound system 12000 11000 -1000

Shares 5000 20000 15000

Total (Profits) 5000

From the above table it can be said that Eric had gained profits of $5000 by disposing

their overall assets. All the assets which are used personally and are depreciated will not be libel

to pay any kind of taxes for them. Eric have to pay tax only on their new profits.

Supporting Evidence:

In relation to guides which are used as personal investors and capital profits on taxes of

2016. The capital gains can only be received by selling their shares (Baldwin, Cave and Lodge,

2012). According to norms if any persons are disposing their capital assets and using it to

achieve capital profits, in this situation persons have to prepare reports of their capital loss or

profits under his returning and he have the liability to pay taxes over their profit ratios. But if

1

Introduction

Capital gains or losses are calculated on the basis of scales which are analysed after

selling all assets. It can arise for long or short terms. If the property are kept with owner more

more than 2 years than it results in achievement of long term gains. Thus all tax are applicable

after analysing cost used in acquisition and then it is paid (Antwi-Agyei and et. al., 2012). If

assets are used for less then 2 years thus taxes are paid directly.

Critical analysis:

According to given case Eric had acquired assets before 12 months. This implies that

person have to pay tax for short time duration. The assets which are acquired by Eric are

evaluated in the below table as:

Particulars Acquired Sale Profit/ loss

Antique base 2000 3000 1000

Antique chair 3000 1000 -2000

Painting 9000 1000 -8000

Home sound system 12000 11000 -1000

Shares 5000 20000 15000

Total (Profits) 5000

From the above table it can be said that Eric had gained profits of $5000 by disposing

their overall assets. All the assets which are used personally and are depreciated will not be libel

to pay any kind of taxes for them. Eric have to pay tax only on their new profits.

Supporting Evidence:

In relation to guides which are used as personal investors and capital profits on taxes of

2016. The capital gains can only be received by selling their shares (Baldwin, Cave and Lodge,

2012). According to norms if any persons are disposing their capital assets and using it to

achieve capital profits, in this situation persons have to prepare reports of their capital loss or

profits under his returning and he have the liability to pay taxes over their profit ratios. But if

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

there are any losses then persons are not libel to claim any amount in relation to their income but

individuals can easily apply them to reduce capital profits. In relation to tax norms all the assets

which are acquired before 20 September year 1985 have to pay CGT till they are not having

special permission to exclude them.

Some of the personal assets are exempted under CGT and this cannot be applied in

depreciating assets involved in tax paying. Thus taxes are not applied on all the above personal

assets which are depreciated.

Conclusion:

From the report it can be concluded that all the capital gains have to paid according to

rules of income tax. All the disposing income should be accessed and valued after this cost

related with acquisition should be reduced in effective ways.

Question 2.

Introduction

Fringe benefits is an additional benefit which is paid by employers to their workers.

These are not included in salary of person. These cost are variable from income tax and are

mostly calculated on taxing cost which are analysed from fringe benefits. According to the case

the loans of fringe benefits are described below (Bisong and Rahman, 2011). Brains employers

are providing loan amount for three year which was $1million @1% per annum. This cost is

lower then the actual benchmarking rates.

Critical analysis:

The case states that employer of Brain had given loan at 1% interest rate. This cost is

lesser while compared with industry rates. Thus taxes are paid on it. Statutory rates in 2016/2017

year are 5.65%. Thus all the fringe benefits on which tax are liable are calculated by analysing

difference between statutory and actual interest rates. In respect to this all the fringe benefits are

measured by the actual rate of interest. The final cost of fringe benefits will be 2016/2017 year is

5.65%

The calculation of tax are described as:

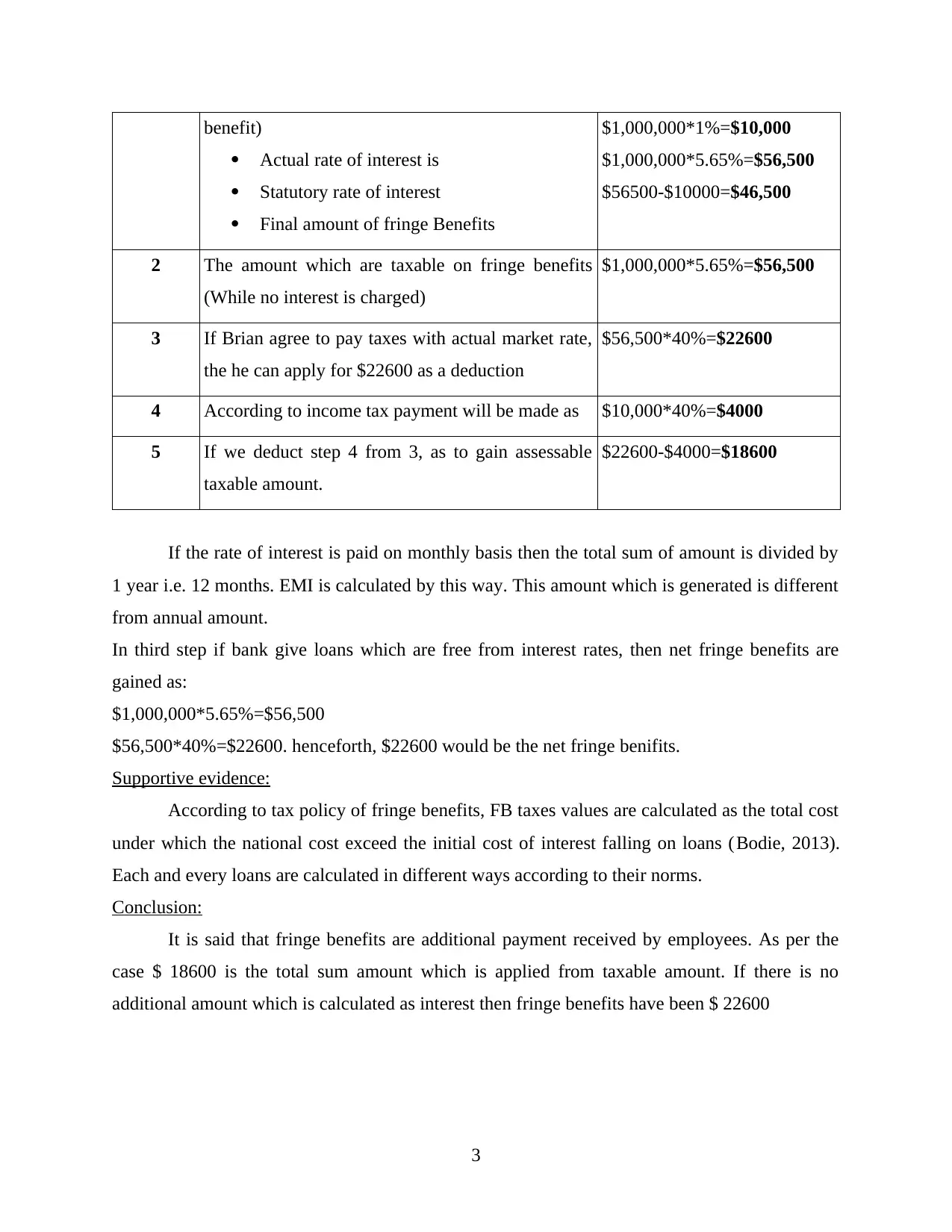

Phase Actions Results

1 The sum of money that is taxable under (fringe

2

individuals can easily apply them to reduce capital profits. In relation to tax norms all the assets

which are acquired before 20 September year 1985 have to pay CGT till they are not having

special permission to exclude them.

Some of the personal assets are exempted under CGT and this cannot be applied in

depreciating assets involved in tax paying. Thus taxes are not applied on all the above personal

assets which are depreciated.

Conclusion:

From the report it can be concluded that all the capital gains have to paid according to

rules of income tax. All the disposing income should be accessed and valued after this cost

related with acquisition should be reduced in effective ways.

Question 2.

Introduction

Fringe benefits is an additional benefit which is paid by employers to their workers.

These are not included in salary of person. These cost are variable from income tax and are

mostly calculated on taxing cost which are analysed from fringe benefits. According to the case

the loans of fringe benefits are described below (Bisong and Rahman, 2011). Brains employers

are providing loan amount for three year which was $1million @1% per annum. This cost is

lower then the actual benchmarking rates.

Critical analysis:

The case states that employer of Brain had given loan at 1% interest rate. This cost is

lesser while compared with industry rates. Thus taxes are paid on it. Statutory rates in 2016/2017

year are 5.65%. Thus all the fringe benefits on which tax are liable are calculated by analysing

difference between statutory and actual interest rates. In respect to this all the fringe benefits are

measured by the actual rate of interest. The final cost of fringe benefits will be 2016/2017 year is

5.65%

The calculation of tax are described as:

Phase Actions Results

1 The sum of money that is taxable under (fringe

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

benefit)

Actual rate of interest is

Statutory rate of interest

Final amount of fringe Benefits

$1,000,000*1%=$10,000

$1,000,000*5.65%=$56,500

$56500-$10000=$46,500

2 The amount which are taxable on fringe benefits

(While no interest is charged)

$1,000,000*5.65%=$56,500

3 If Brian agree to pay taxes with actual market rate,

the he can apply for $22600 as a deduction

$56,500*40%=$22600

4 According to income tax payment will be made as $10,000*40%=$4000

5 If we deduct step 4 from 3, as to gain assessable

taxable amount.

$22600-$4000=$18600

If the rate of interest is paid on monthly basis then the total sum of amount is divided by

1 year i.e. 12 months. EMI is calculated by this way. This amount which is generated is different

from annual amount.

In third step if bank give loans which are free from interest rates, then net fringe benefits are

gained as:

$1,000,000*5.65%=$56,500

$56,500*40%=$22600. henceforth, $22600 would be the net fringe benifits.

Supportive evidence:

According to tax policy of fringe benefits, FB taxes values are calculated as the total cost

under which the national cost exceed the initial cost of interest falling on loans (Bodie, 2013).

Each and every loans are calculated in different ways according to their norms.

Conclusion:

It is said that fringe benefits are additional payment received by employees. As per the

case $ 18600 is the total sum amount which is applied from taxable amount. If there is no

additional amount which is calculated as interest then fringe benefits have been $ 22600

3

Actual rate of interest is

Statutory rate of interest

Final amount of fringe Benefits

$1,000,000*1%=$10,000

$1,000,000*5.65%=$56,500

$56500-$10000=$46,500

2 The amount which are taxable on fringe benefits

(While no interest is charged)

$1,000,000*5.65%=$56,500

3 If Brian agree to pay taxes with actual market rate,

the he can apply for $22600 as a deduction

$56,500*40%=$22600

4 According to income tax payment will be made as $10,000*40%=$4000

5 If we deduct step 4 from 3, as to gain assessable

taxable amount.

$22600-$4000=$18600

If the rate of interest is paid on monthly basis then the total sum of amount is divided by

1 year i.e. 12 months. EMI is calculated by this way. This amount which is generated is different

from annual amount.

In third step if bank give loans which are free from interest rates, then net fringe benefits are

gained as:

$1,000,000*5.65%=$56,500

$56,500*40%=$22600. henceforth, $22600 would be the net fringe benifits.

Supportive evidence:

According to tax policy of fringe benefits, FB taxes values are calculated as the total cost

under which the national cost exceed the initial cost of interest falling on loans (Bodie, 2013).

Each and every loans are calculated in different ways according to their norms.

Conclusion:

It is said that fringe benefits are additional payment received by employees. As per the

case $ 18600 is the total sum amount which is applied from taxable amount. If there is no

additional amount which is calculated as interest then fringe benefits have been $ 22600

3

Question 3

Introduction

The case is about a husband and his wife named as Jack and Jill they have borrowed a

sum of money to buy property on rent. These persons have agree to sign a contract in which the

profit ratios will be divided among ratios of 90:10 and if there is any losses these had to be beard

by only one person jack. The contract was helpful in avoiding factors which were linked with

paying tax liabilities. Last year, they have faced loss as property arose $10000 loss.

Critical analysis

According to case both persons have made contract in order to remove tax liabilities. Jill

is housewife and she is not earning thus dependent and her income is clubbed under assessment

of Jack. The covenant is assigned in order to reduce tax liabilities and income which is earned is

covered under Jack. If there is any losses then it had to be forwarded in coming year. If they wish

to sell the property then they can have capital gains or losses and this will include under Jack

capital income (Brink, 2017). Jill is not libel to pay taxes over her capital profits but Jack had to

pay the tax.

Supporting evidence:

According to law of nation, a person is not liable to take benefits for which she is not

accountant to pay any amount. Thus no form of tax are paid on capital profits which they are

entitled to get. Thus all taxes are to be paid by Jack only (Capital gain tax on property, 2017).

Conclusion

From the above case it is analysed that Jack is having capital loss as he decide to sell his

initial property.

Question 4

Introduction:

According to case of Duke of Westminster's case which was supported by tax avoidance. There

was a deed based on legal document of valence which had list of servants who were gardeners,

national helpers etc. Under thus Duke decided to gave some amount to hid worker who was

having responsibility to taker care of garden. There was an agreement made so as to give

payment to employee on monthly basis but he failed to do so. This was done in order to save

taxes (Evers, Miller and Spengel, 2015).

4

Introduction

The case is about a husband and his wife named as Jack and Jill they have borrowed a

sum of money to buy property on rent. These persons have agree to sign a contract in which the

profit ratios will be divided among ratios of 90:10 and if there is any losses these had to be beard

by only one person jack. The contract was helpful in avoiding factors which were linked with

paying tax liabilities. Last year, they have faced loss as property arose $10000 loss.

Critical analysis

According to case both persons have made contract in order to remove tax liabilities. Jill

is housewife and she is not earning thus dependent and her income is clubbed under assessment

of Jack. The covenant is assigned in order to reduce tax liabilities and income which is earned is

covered under Jack. If there is any losses then it had to be forwarded in coming year. If they wish

to sell the property then they can have capital gains or losses and this will include under Jack

capital income (Brink, 2017). Jill is not libel to pay taxes over her capital profits but Jack had to

pay the tax.

Supporting evidence:

According to law of nation, a person is not liable to take benefits for which she is not

accountant to pay any amount. Thus no form of tax are paid on capital profits which they are

entitled to get. Thus all taxes are to be paid by Jack only (Capital gain tax on property, 2017).

Conclusion

From the above case it is analysed that Jack is having capital loss as he decide to sell his

initial property.

Question 4

Introduction:

According to case of Duke of Westminster's case which was supported by tax avoidance. There

was a deed based on legal document of valence which had list of servants who were gardeners,

national helpers etc. Under thus Duke decided to gave some amount to hid worker who was

having responsibility to taker care of garden. There was an agreement made so as to give

payment to employee on monthly basis but he failed to do so. This was done in order to save

taxes (Evers, Miller and Spengel, 2015).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Critical analysis:

Deed is described as legal documents which are signed with the wish of 2 to 3 persons with their

mutual consent. It is used in order to transfer properties. The relation among deed and contract is

that deed is agreement in written formats which have to be signed by both persons and it had to

be standing in front of third party. Agreements re in written formats and deed are unenforceable

by laws.

Supporting evidence:

The laws implies the valuable legal proceeding while persons are avoiding taxes. There was an

opinion given by Lord Tomlin who says that person have right to reduce taxes and it is not

against the law (Jiang and Shao, 2014). According to Ramsay if persons are finding illegal ways

to save tax then it has to face liability by paying the whole amount.

Conclusion

From the above report it is analysed that if effective ways are adopted to reduce taxes

than it is not illegal.

Question 5

Introduction

It is very crucial to determine amount which will be paid as tax while selling trees. It can

be classifies as money which is received from agriculture sector or it can be act of generating

higher revenues. Bills was the owner of land which was full of palm trees. The areas has to

cleared so that animals can graze there. For this he gave responsibility to a firm who will charge

$ 1000 for clearing each area of 100 square.

Critical analyses

The amount received by selling timber was counted as income which had to be paid in

taxes. The owner was paying money to Logging company in return of land clearing. This

situation is valuable for Bill as his land will be used for animals (Guenther, 2014). He was

involved in a business because company was cutting and taking timber along with them. This is

termed as loyalty as he is not involved in selling trees top another person. He was liable to pay

taxes thus achieving capital profits.

Supporting evidence

According to TR 95/6 if persons are involved to cut trees and selling them in return of

money then it is included under income of individuals. The main aim of Bill is to clear land and

5

Deed is described as legal documents which are signed with the wish of 2 to 3 persons with their

mutual consent. It is used in order to transfer properties. The relation among deed and contract is

that deed is agreement in written formats which have to be signed by both persons and it had to

be standing in front of third party. Agreements re in written formats and deed are unenforceable

by laws.

Supporting evidence:

The laws implies the valuable legal proceeding while persons are avoiding taxes. There was an

opinion given by Lord Tomlin who says that person have right to reduce taxes and it is not

against the law (Jiang and Shao, 2014). According to Ramsay if persons are finding illegal ways

to save tax then it has to face liability by paying the whole amount.

Conclusion

From the above report it is analysed that if effective ways are adopted to reduce taxes

than it is not illegal.

Question 5

Introduction

It is very crucial to determine amount which will be paid as tax while selling trees. It can

be classifies as money which is received from agriculture sector or it can be act of generating

higher revenues. Bills was the owner of land which was full of palm trees. The areas has to

cleared so that animals can graze there. For this he gave responsibility to a firm who will charge

$ 1000 for clearing each area of 100 square.

Critical analyses

The amount received by selling timber was counted as income which had to be paid in

taxes. The owner was paying money to Logging company in return of land clearing. This

situation is valuable for Bill as his land will be used for animals (Guenther, 2014). He was

involved in a business because company was cutting and taking timber along with them. This is

termed as loyalty as he is not involved in selling trees top another person. He was liable to pay

taxes thus achieving capital profits.

Supporting evidence

According to TR 95/6 if persons are involved to cut trees and selling them in return of

money then it is included under income of individuals. The main aim of Bill is to clear land and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

he was not focused on earning profits or monetary value, thus it is not included under forest

operation.

Conclusion

The above report states that if individuals appoint person to cutting trees then income

gained from selling palm trees are calculated under forest operations.

REFERENCES

Books and Journals:

Antwi-Agyei, P. and et. al., 2012. Mapping the vulnerability of crop production to drought in

Ghana using rainfall, yield and socioeconomic data. Applied Geography. 32(2). pp.324-

334.

Baldwin, R., Cave, M. and Lodge, M., 2012. Understanding regulation: theory, strategy, and

practice. Oxford University Press on Demand

Bisong, A. and Rahman, M., 2011. An overview of the security concerns in enterprise cloud

computing. arXiv preprint arXiv:1101.5613.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brink, J., 2017. Taxable benefits provided to expatriate employees seconded in South Africa:

fringe benefits. Tax Breaks Newsletter. 2017(373). pp.5-8.

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax rates

and tax policy considerations. International Tax and Public Finance. 22(3), pp.502-530.

Guenther, D.A., 2014. Measuring corporate tax avoidance: Effective tax rates and book-tax

differences.Browser Download This Paper.

Jiang, Z. and Shao, S., 2014. Distributional effects of a carbon tax on Chinese households: A

case of Shanghai. Energy Policy. 73. pp.269-277.

Kholdy, S. and Sohrabian, A., 2011. Capital gain expectations and efficiency in the real estate

markets. Journal of Business & Economics Research (JBER). 6(4).

McGuire, S.T., Wang, D. and Wilson, R.J., 2014. Dual class ownership and tax avoidance. The

Accounting Review. 89(4). pp.1487-1516.

Mullins, C., 2015. Tax considerations of debit loans: business income tax. TAXtalk. 2015(55).

pp.58-59.

Saez, E. and Zucman, G., 2016. Wealth inequality in the United States since 1913: Evidence

from capitalized income tax data. The Quarterly Journal of Economics. 131(2). pp.519-

578.

Online

6

operation.

Conclusion

The above report states that if individuals appoint person to cutting trees then income

gained from selling palm trees are calculated under forest operations.

REFERENCES

Books and Journals:

Antwi-Agyei, P. and et. al., 2012. Mapping the vulnerability of crop production to drought in

Ghana using rainfall, yield and socioeconomic data. Applied Geography. 32(2). pp.324-

334.

Baldwin, R., Cave, M. and Lodge, M., 2012. Understanding regulation: theory, strategy, and

practice. Oxford University Press on Demand

Bisong, A. and Rahman, M., 2011. An overview of the security concerns in enterprise cloud

computing. arXiv preprint arXiv:1101.5613.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brink, J., 2017. Taxable benefits provided to expatriate employees seconded in South Africa:

fringe benefits. Tax Breaks Newsletter. 2017(373). pp.5-8.

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax rates

and tax policy considerations. International Tax and Public Finance. 22(3), pp.502-530.

Guenther, D.A., 2014. Measuring corporate tax avoidance: Effective tax rates and book-tax

differences.Browser Download This Paper.

Jiang, Z. and Shao, S., 2014. Distributional effects of a carbon tax on Chinese households: A

case of Shanghai. Energy Policy. 73. pp.269-277.

Kholdy, S. and Sohrabian, A., 2011. Capital gain expectations and efficiency in the real estate

markets. Journal of Business & Economics Research (JBER). 6(4).

McGuire, S.T., Wang, D. and Wilson, R.J., 2014. Dual class ownership and tax avoidance. The

Accounting Review. 89(4). pp.1487-1516.

Mullins, C., 2015. Tax considerations of debit loans: business income tax. TAXtalk. 2015(55).

pp.58-59.

Saez, E. and Zucman, G., 2016. Wealth inequality in the United States since 1913: Evidence

from capitalized income tax data. The Quarterly Journal of Economics. 131(2). pp.519-

578.

Online

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.