Taxation Theory, Practice & Law: Case Studies and Solutions Report

VerifiedAdded on 2020/12/18

|12

|3278

|377

Report

AI Summary

This report provides a detailed analysis of taxation laws in Australia, focusing on capital gains and their tax implications. The report presents solutions to two case scenarios. The first scenario analyzes various assets sold by a client, including vacant land, an antique bed, a painting, shares, and a violin, calculating their capital gains and associated tax liabilities. The second scenario offers advice to a company regarding Fringe Benefits Tax (FBT) consequences. The report applies relevant Australian taxation regulations, including the Income Tax Assessment Act 1997 and the Insurance Act 1984, to determine taxable amounts and applicable tax rates. It differentiates between capital gains and capital losses, considering factors such as the acquisition date of assets and insurance claims. The report also addresses the implications of pre-CGT assets and provides a comprehensive understanding of taxation concepts and practices.

Taxation Theory, Practice

& Law

& Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a. Block of vacant land...........................................................................................................1

b. Antique bed........................................................................................................................2

c. Painting...............................................................................................................................3

d. Shares.................................................................................................................................4

e. Violin..................................................................................................................................6

TASK 2............................................................................................................................................7

a Advise Rapid-Heat about FBT consequences....................................................................7

b. Variation to answer if the Jasmine used 500000 as share investment................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a. Block of vacant land...........................................................................................................1

b. Antique bed........................................................................................................................2

c. Painting...............................................................................................................................3

d. Shares.................................................................................................................................4

e. Violin..................................................................................................................................6

TASK 2............................................................................................................................................7

a Advise Rapid-Heat about FBT consequences....................................................................7

b. Variation to answer if the Jasmine used 500000 as share investment................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Taxation theory is the tax system which is concerned with tax brackets and slabs in order

to ascertain tax liabilities for every individual, company or any other institution. As a tax

consultant in Mayfield, New South Wales Australia, various assets which are sold by the client

are analysed in order to ascertain their net taxable amount. In this project report, solutions for

two case scenarios are provided which are concerned with taxation laws. Various assets along

with their capital gains are calculated in first scenario. In second scenario advices to a company

is provided in order to assisting them in taxation. The main aim of this report is build a

understanding about the concept of taxation law and its practices

TASK 1

Mayfield, New South Wales is an Australian Suburb in which Australian laws are

applicable. As an tax consultant of this region, all the suggestion and advices provided to client

are related with laws of this region. In Australia, there are different taxation laws for variety of

income such as Income tax law, GST law and others. In order to provide solution for below

transactions , Income tax law is used in which various tax regulations such as Capital gain tax

(CGT) and Insurance claim tax are used. As a tax consultant, it has been ascertained that the

client is an investor and antique collector and despite of various investments she is not carrying

any business due to which all taxation rates of an individual will be applicable on her. Total and

net taxation amount of this client is determined by ascertaining solutions for below queries.

a. Block of vacant land

Case Scenario: Client is an investor and antique collector, who has signed a contract to

sell a block of vacant land for 320000 which was acquired for the value of 100000 and additional

20000 which were paid by her for water and land taxes. Selling of a land is kind of capital gain

due to which tax rate of CGT will be applicable to the client.

Related Tax and regulations: From the above case scenario it has been ascertained that

CGT will be applicable on the client. According to these regulations, vacant land is a block of

immovable property which is owned as an investment and was acquired after 20 September

1985. According to Australian Taxation Office, Vacant land that is help as a capital asset is

1

Taxation theory is the tax system which is concerned with tax brackets and slabs in order

to ascertain tax liabilities for every individual, company or any other institution. As a tax

consultant in Mayfield, New South Wales Australia, various assets which are sold by the client

are analysed in order to ascertain their net taxable amount. In this project report, solutions for

two case scenarios are provided which are concerned with taxation laws. Various assets along

with their capital gains are calculated in first scenario. In second scenario advices to a company

is provided in order to assisting them in taxation. The main aim of this report is build a

understanding about the concept of taxation law and its practices

TASK 1

Mayfield, New South Wales is an Australian Suburb in which Australian laws are

applicable. As an tax consultant of this region, all the suggestion and advices provided to client

are related with laws of this region. In Australia, there are different taxation laws for variety of

income such as Income tax law, GST law and others. In order to provide solution for below

transactions , Income tax law is used in which various tax regulations such as Capital gain tax

(CGT) and Insurance claim tax are used. As a tax consultant, it has been ascertained that the

client is an investor and antique collector and despite of various investments she is not carrying

any business due to which all taxation rates of an individual will be applicable on her. Total and

net taxation amount of this client is determined by ascertaining solutions for below queries.

a. Block of vacant land

Case Scenario: Client is an investor and antique collector, who has signed a contract to

sell a block of vacant land for 320000 which was acquired for the value of 100000 and additional

20000 which were paid by her for water and land taxes. Selling of a land is kind of capital gain

due to which tax rate of CGT will be applicable to the client.

Related Tax and regulations: From the above case scenario it has been ascertained that

CGT will be applicable on the client. According to these regulations, vacant land is a block of

immovable property which is owned as an investment and was acquired after 20 September

1985. According to Australian Taxation Office, Vacant land that is help as a capital asset is

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

subject to the same capital gains tax rules as per other properties. Expenses paid by the client for

acquisition and sale of land can not be claimed as an income tax deduction.

Net capital gain which is earned by the client along with its taxable value is determined

below:

Date Particulars Amount

Jan 2001 Purchase of block of vacant land 100000

Expenses of water, sewage and land taxes on land 20000

Total cost of land 120000

3 June 2017 Contract price of sale of block of vacant land 320000

3 June 2017 Deposit of contract price 20000

3 Jan 2018 Balance payment 300000

Capital gain 200000

Taxable capital gain 20000

Tax rate

19cents per dollars

exceeding 18201

Net tax payable amount 342

Capital gain is the rise in the value of a capital assets which is usually higher than the

value of purchased cost. In this case, in order to determine the value of capital gain Total cost of

land is deducted from total value of sold asset so that difference can be ascertained. Taxable

capital amount is recorded as 20000 and not 200000 as the client has only received 20000 as a

token amount in this taxation year and rest 180000 will be received in next taxation year.

According to the current tax rates any capital amount which is lower than 18201 is non taxable.

Thus, the value of tax amount which 342 is determined using tax rate of 19% or 19 cents per

dollar exceeding 18201.

b. Antique bed

Case Scenario: In this case, client has claimed for insurance for her antique bed acquired

in 1986 amounting 5000 including all expenses. This capital asset was stolen from her house and

at that time value of that asset was 25000. As provided, on 13 November, 2017 client claimed for

the insurance which was rejected commenting that this particular asset was not mentioned in the

2

acquisition and sale of land can not be claimed as an income tax deduction.

Net capital gain which is earned by the client along with its taxable value is determined

below:

Date Particulars Amount

Jan 2001 Purchase of block of vacant land 100000

Expenses of water, sewage and land taxes on land 20000

Total cost of land 120000

3 June 2017 Contract price of sale of block of vacant land 320000

3 June 2017 Deposit of contract price 20000

3 Jan 2018 Balance payment 300000

Capital gain 200000

Taxable capital gain 20000

Tax rate

19cents per dollars

exceeding 18201

Net tax payable amount 342

Capital gain is the rise in the value of a capital assets which is usually higher than the

value of purchased cost. In this case, in order to determine the value of capital gain Total cost of

land is deducted from total value of sold asset so that difference can be ascertained. Taxable

capital amount is recorded as 20000 and not 200000 as the client has only received 20000 as a

token amount in this taxation year and rest 180000 will be received in next taxation year.

According to the current tax rates any capital amount which is lower than 18201 is non taxable.

Thus, the value of tax amount which 342 is determined using tax rate of 19% or 19 cents per

dollar exceeding 18201.

b. Antique bed

Case Scenario: In this case, client has claimed for insurance for her antique bed acquired

in 1986 amounting 5000 including all expenses. This capital asset was stolen from her house and

at that time value of that asset was 25000. As provided, on 13 November, 2017 client claimed for

the insurance which was rejected commenting that this particular asset was not mentioned in the

2

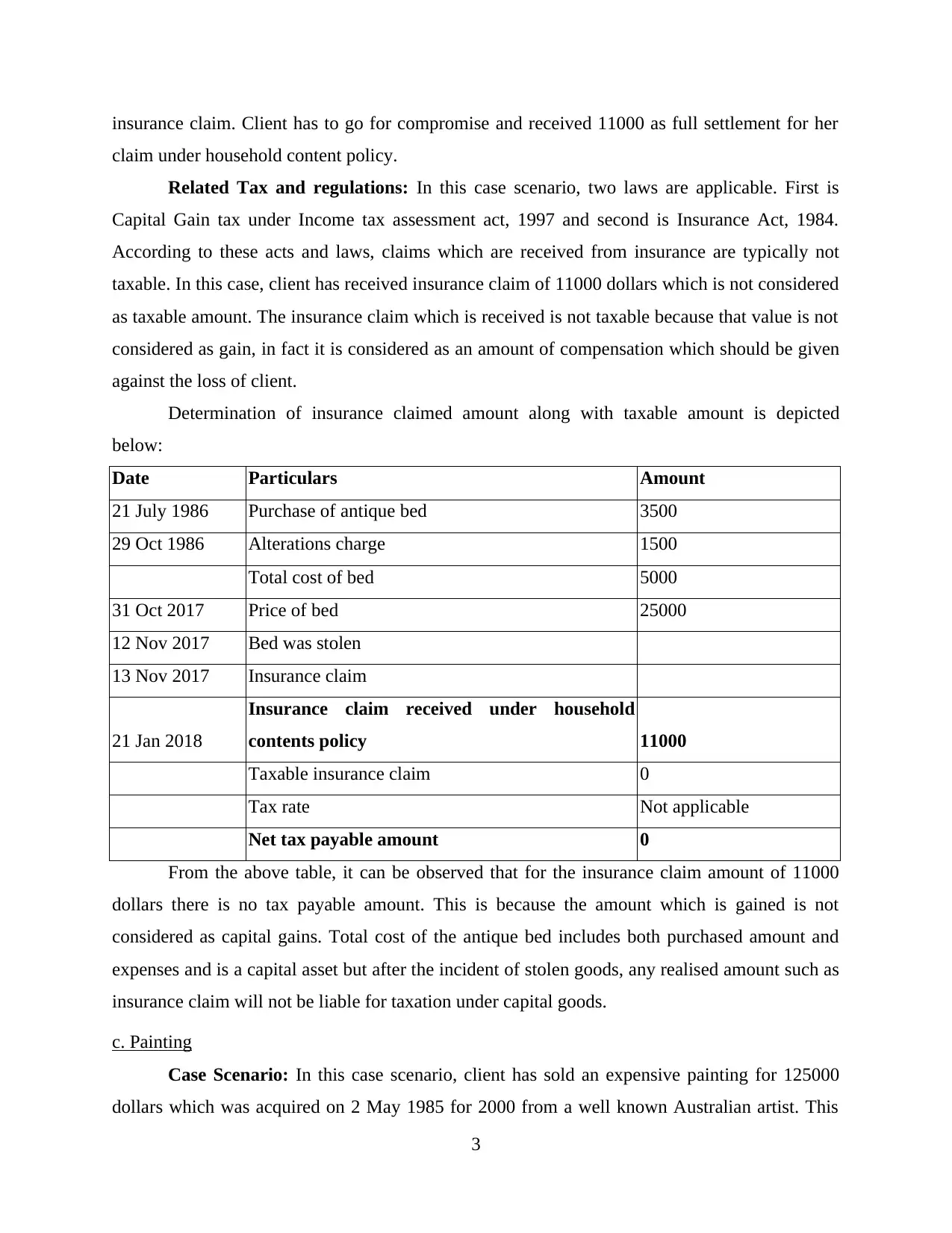

insurance claim. Client has to go for compromise and received 11000 as full settlement for her

claim under household content policy.

Related Tax and regulations: In this case scenario, two laws are applicable. First is

Capital Gain tax under Income tax assessment act, 1997 and second is Insurance Act, 1984.

According to these acts and laws, claims which are received from insurance are typically not

taxable. In this case, client has received insurance claim of 11000 dollars which is not considered

as taxable amount. The insurance claim which is received is not taxable because that value is not

considered as gain, in fact it is considered as an amount of compensation which should be given

against the loss of client.

Determination of insurance claimed amount along with taxable amount is depicted

below:

Date Particulars Amount

21 July 1986 Purchase of antique bed 3500

29 Oct 1986 Alterations charge 1500

Total cost of bed 5000

31 Oct 2017 Price of bed 25000

12 Nov 2017 Bed was stolen

13 Nov 2017 Insurance claim

21 Jan 2018

Insurance claim received under household

contents policy 11000

Taxable insurance claim 0

Tax rate Not applicable

Net tax payable amount 0

From the above table, it can be observed that for the insurance claim amount of 11000

dollars there is no tax payable amount. This is because the amount which is gained is not

considered as capital gains. Total cost of the antique bed includes both purchased amount and

expenses and is a capital asset but after the incident of stolen goods, any realised amount such as

insurance claim will not be liable for taxation under capital goods.

c. Painting

Case Scenario: In this case scenario, client has sold an expensive painting for 125000

dollars which was acquired on 2 May 1985 for 2000 from a well known Australian artist. This

3

claim under household content policy.

Related Tax and regulations: In this case scenario, two laws are applicable. First is

Capital Gain tax under Income tax assessment act, 1997 and second is Insurance Act, 1984.

According to these acts and laws, claims which are received from insurance are typically not

taxable. In this case, client has received insurance claim of 11000 dollars which is not considered

as taxable amount. The insurance claim which is received is not taxable because that value is not

considered as gain, in fact it is considered as an amount of compensation which should be given

against the loss of client.

Determination of insurance claimed amount along with taxable amount is depicted

below:

Date Particulars Amount

21 July 1986 Purchase of antique bed 3500

29 Oct 1986 Alterations charge 1500

Total cost of bed 5000

31 Oct 2017 Price of bed 25000

12 Nov 2017 Bed was stolen

13 Nov 2017 Insurance claim

21 Jan 2018

Insurance claim received under household

contents policy 11000

Taxable insurance claim 0

Tax rate Not applicable

Net tax payable amount 0

From the above table, it can be observed that for the insurance claim amount of 11000

dollars there is no tax payable amount. This is because the amount which is gained is not

considered as capital gains. Total cost of the antique bed includes both purchased amount and

expenses and is a capital asset but after the incident of stolen goods, any realised amount such as

insurance claim will not be liable for taxation under capital goods.

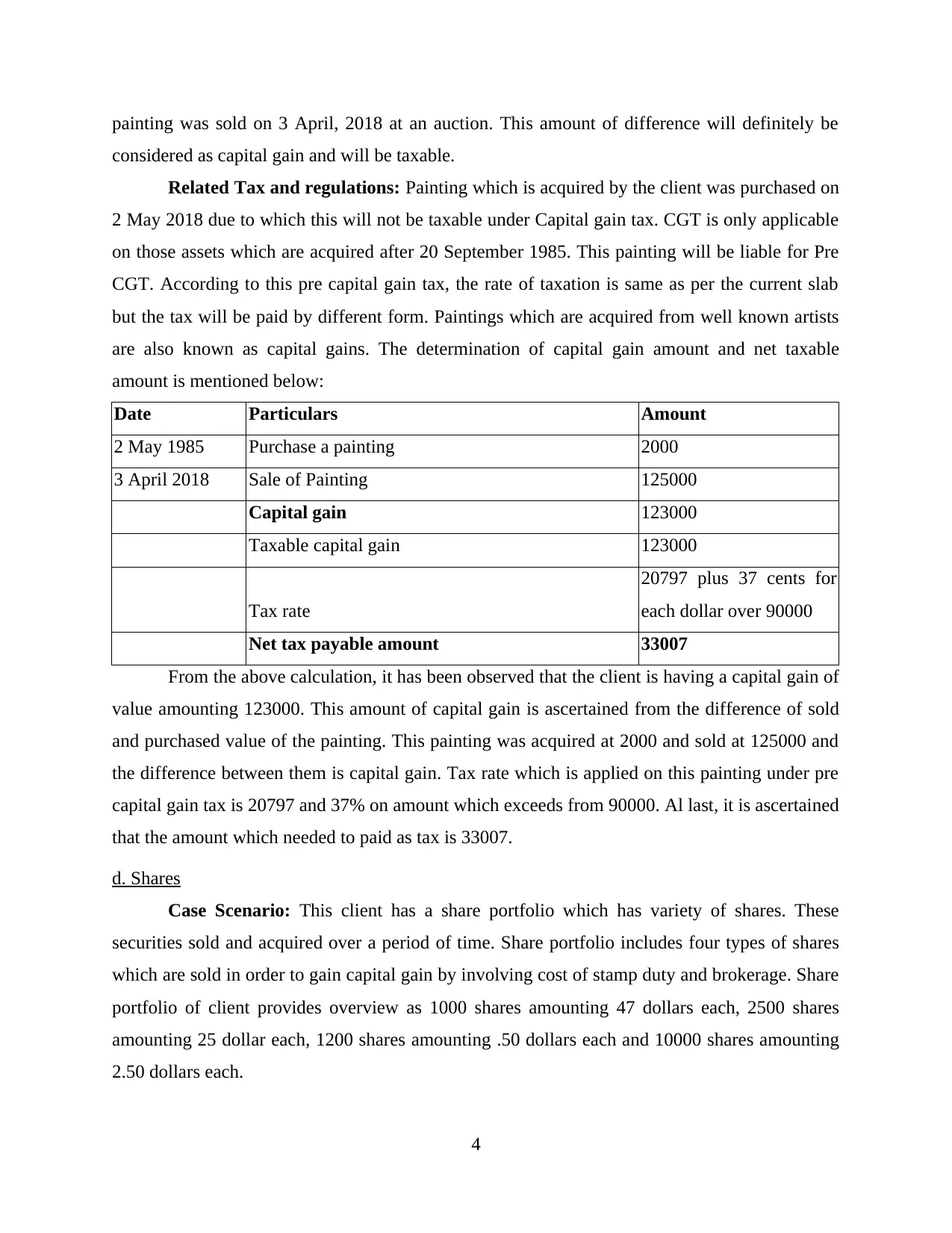

c. Painting

Case Scenario: In this case scenario, client has sold an expensive painting for 125000

dollars which was acquired on 2 May 1985 for 2000 from a well known Australian artist. This

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

painting was sold on 3 April, 2018 at an auction. This amount of difference will definitely be

considered as capital gain and will be taxable.

Related Tax and regulations: Painting which is acquired by the client was purchased on

2 May 2018 due to which this will not be taxable under Capital gain tax. CGT is only applicable

on those assets which are acquired after 20 September 1985. This painting will be liable for Pre

CGT. According to this pre capital gain tax, the rate of taxation is same as per the current slab

but the tax will be paid by different form. Paintings which are acquired from well known artists

are also known as capital gains. The determination of capital gain amount and net taxable

amount is mentioned below:

Date Particulars Amount

2 May 1985 Purchase a painting 2000

3 April 2018 Sale of Painting 125000

Capital gain 123000

Taxable capital gain 123000

Tax rate

20797 plus 37 cents for

each dollar over 90000

Net tax payable amount 33007

From the above calculation, it has been observed that the client is having a capital gain of

value amounting 123000. This amount of capital gain is ascertained from the difference of sold

and purchased value of the painting. This painting was acquired at 2000 and sold at 125000 and

the difference between them is capital gain. Tax rate which is applied on this painting under pre

capital gain tax is 20797 and 37% on amount which exceeds from 90000. Al last, it is ascertained

that the amount which needed to paid as tax is 33007.

d. Shares

Case Scenario: This client has a share portfolio which has variety of shares. These

securities sold and acquired over a period of time. Share portfolio includes four types of shares

which are sold in order to gain capital gain by involving cost of stamp duty and brokerage. Share

portfolio of client provides overview as 1000 shares amounting 47 dollars each, 2500 shares

amounting 25 dollar each, 1200 shares amounting .50 dollars each and 10000 shares amounting

2.50 dollars each.

4

considered as capital gain and will be taxable.

Related Tax and regulations: Painting which is acquired by the client was purchased on

2 May 2018 due to which this will not be taxable under Capital gain tax. CGT is only applicable

on those assets which are acquired after 20 September 1985. This painting will be liable for Pre

CGT. According to this pre capital gain tax, the rate of taxation is same as per the current slab

but the tax will be paid by different form. Paintings which are acquired from well known artists

are also known as capital gains. The determination of capital gain amount and net taxable

amount is mentioned below:

Date Particulars Amount

2 May 1985 Purchase a painting 2000

3 April 2018 Sale of Painting 125000

Capital gain 123000

Taxable capital gain 123000

Tax rate

20797 plus 37 cents for

each dollar over 90000

Net tax payable amount 33007

From the above calculation, it has been observed that the client is having a capital gain of

value amounting 123000. This amount of capital gain is ascertained from the difference of sold

and purchased value of the painting. This painting was acquired at 2000 and sold at 125000 and

the difference between them is capital gain. Tax rate which is applied on this painting under pre

capital gain tax is 20797 and 37% on amount which exceeds from 90000. Al last, it is ascertained

that the amount which needed to paid as tax is 33007.

d. Shares

Case Scenario: This client has a share portfolio which has variety of shares. These

securities sold and acquired over a period of time. Share portfolio includes four types of shares

which are sold in order to gain capital gain by involving cost of stamp duty and brokerage. Share

portfolio of client provides overview as 1000 shares amounting 47 dollars each, 2500 shares

amounting 25 dollar each, 1200 shares amounting .50 dollars each and 10000 shares amounting

2.50 dollars each.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

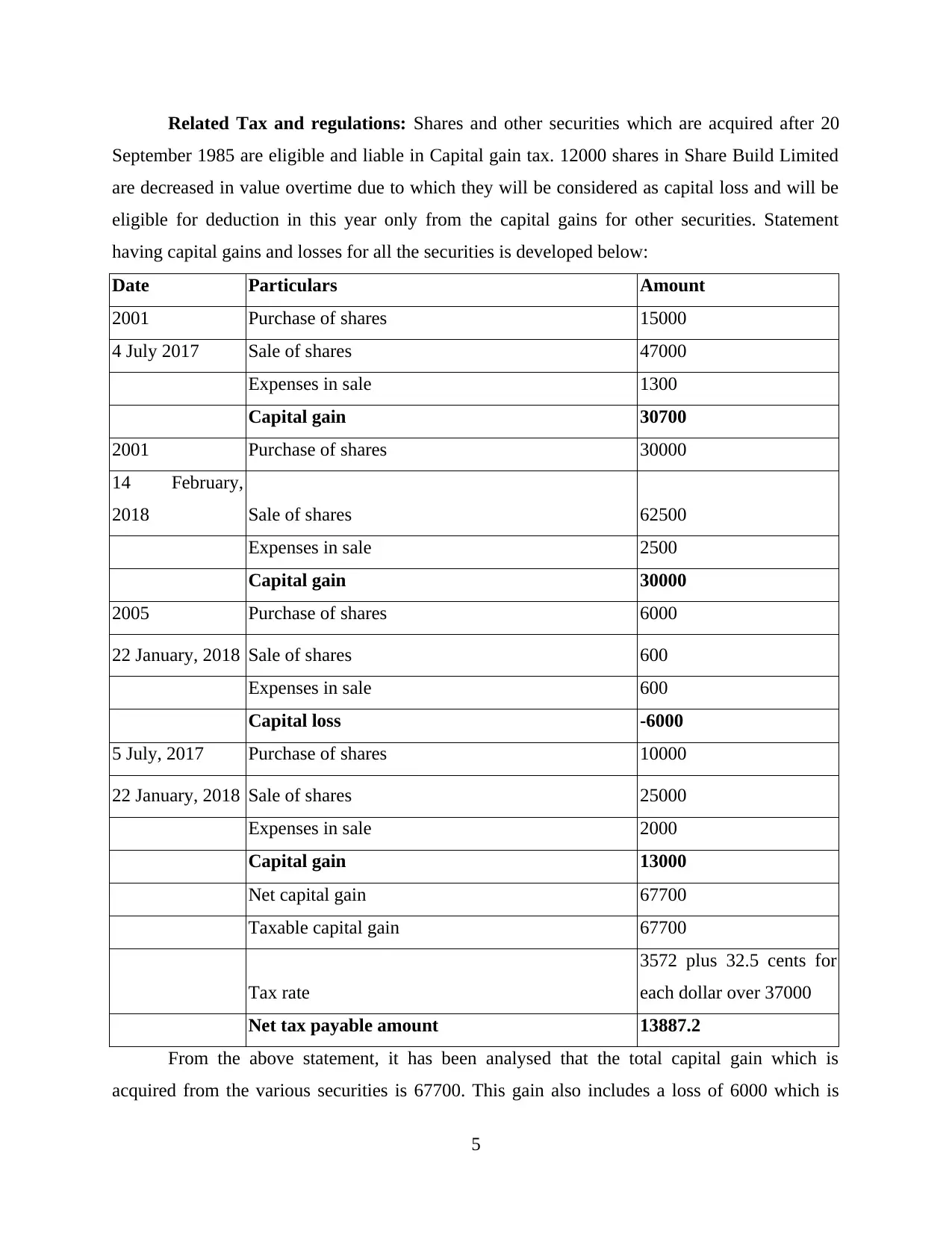

Related Tax and regulations: Shares and other securities which are acquired after 20

September 1985 are eligible and liable in Capital gain tax. 12000 shares in Share Build Limited

are decreased in value overtime due to which they will be considered as capital loss and will be

eligible for deduction in this year only from the capital gains for other securities. Statement

having capital gains and losses for all the securities is developed below:

Date Particulars Amount

2001 Purchase of shares 15000

4 July 2017 Sale of shares 47000

Expenses in sale 1300

Capital gain 30700

2001 Purchase of shares 30000

14 February,

2018 Sale of shares 62500

Expenses in sale 2500

Capital gain 30000

2005 Purchase of shares 6000

22 January, 2018 Sale of shares 600

Expenses in sale 600

Capital loss -6000

5 July, 2017 Purchase of shares 10000

22 January, 2018 Sale of shares 25000

Expenses in sale 2000

Capital gain 13000

Net capital gain 67700

Taxable capital gain 67700

Tax rate

3572 plus 32.5 cents for

each dollar over 37000

Net tax payable amount 13887.2

From the above statement, it has been analysed that the total capital gain which is

acquired from the various securities is 67700. This gain also includes a loss of 6000 which is

5

September 1985 are eligible and liable in Capital gain tax. 12000 shares in Share Build Limited

are decreased in value overtime due to which they will be considered as capital loss and will be

eligible for deduction in this year only from the capital gains for other securities. Statement

having capital gains and losses for all the securities is developed below:

Date Particulars Amount

2001 Purchase of shares 15000

4 July 2017 Sale of shares 47000

Expenses in sale 1300

Capital gain 30700

2001 Purchase of shares 30000

14 February,

2018 Sale of shares 62500

Expenses in sale 2500

Capital gain 30000

2005 Purchase of shares 6000

22 January, 2018 Sale of shares 600

Expenses in sale 600

Capital loss -6000

5 July, 2017 Purchase of shares 10000

22 January, 2018 Sale of shares 25000

Expenses in sale 2000

Capital gain 13000

Net capital gain 67700

Taxable capital gain 67700

Tax rate

3572 plus 32.5 cents for

each dollar over 37000

Net tax payable amount 13887.2

From the above statement, it has been analysed that the total capital gain which is

acquired from the various securities is 67700. This gain also includes a loss of 6000 which is

5

deducted capital gain. Capital gain amounting 67700 is liable for taxation which is charged at the

rate of 32.5% after 37000. Standard charge of tax which is charged is 3572. After calculating

capital gains and losses of all the securities, it has been evaluated that the net taxable amount if

13887.2 dollars.

e. Violin

Case Scenario: In this case scenario, client is a collector of musical instruments and is

owner of several violins. On 1 May, 2018 client has sold one of her violins for 12000 dollars to

her neighbour which was acquired in 1 June 1999 amount 5500 dollars.

Related Tax and regulations: Capita1536237580l gain tax under Income tax law will be

applicable in this case and according to which tax slab of income tax will be applicable on the

capital gain. Despite of the fact that the violin is used by the client on regular basis and is sold to

her neighbour there will be no effect on the taxation rate and tax amount. Calculation of net tax

payable amount and capital gain is depicted below:

Date Particulars Amount

1 June 1999 Purchase of Violin 5500

1 May 2018 Sale of Violin 12000

Capital gain 6500

Taxable capital gain 0

Tax rate Not applicable

Net tax payable amount 0

From the above calculation, it has been ascertained that there is no tax payable amount

against the capital gain of 6500. The amount of tax payable amount is zero due to the tax rates

under CGT according to which any capital gain under 18001 dollars is exempted from tax.

Above there are various determinations of capital gains which are gained by the client.

As an tax consultant of the client, total capital gain and the taxable amount against those gains is

calculated below:

Particulars Amount

Capital gain from block of land 200000

Capital gain of painting 123000

Capital gain of violin 6500

Net capital gain of shares 67700

6

rate of 32.5% after 37000. Standard charge of tax which is charged is 3572. After calculating

capital gains and losses of all the securities, it has been evaluated that the net taxable amount if

13887.2 dollars.

e. Violin

Case Scenario: In this case scenario, client is a collector of musical instruments and is

owner of several violins. On 1 May, 2018 client has sold one of her violins for 12000 dollars to

her neighbour which was acquired in 1 June 1999 amount 5500 dollars.

Related Tax and regulations: Capita1536237580l gain tax under Income tax law will be

applicable in this case and according to which tax slab of income tax will be applicable on the

capital gain. Despite of the fact that the violin is used by the client on regular basis and is sold to

her neighbour there will be no effect on the taxation rate and tax amount. Calculation of net tax

payable amount and capital gain is depicted below:

Date Particulars Amount

1 June 1999 Purchase of Violin 5500

1 May 2018 Sale of Violin 12000

Capital gain 6500

Taxable capital gain 0

Tax rate Not applicable

Net tax payable amount 0

From the above calculation, it has been ascertained that there is no tax payable amount

against the capital gain of 6500. The amount of tax payable amount is zero due to the tax rates

under CGT according to which any capital gain under 18001 dollars is exempted from tax.

Above there are various determinations of capital gains which are gained by the client.

As an tax consultant of the client, total capital gain and the taxable amount against those gains is

calculated below:

Particulars Amount

Capital gain from block of land 200000

Capital gain of painting 123000

Capital gain of violin 6500

Net capital gain of shares 67700

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total capital gain 397200

Less: Capital loss of previous year 8500

Net capital gain 388700

Others:

Insurance claim received under household contents policy 11000

Particulars Amount

Net tax payable amount of block of land 342

Net tax payable amount of painting 33007

Net tax payable amount of violin 0

Net tax payable amount of shares 13887.2

Net tax payable amount on insurance claim of antique bed 0

Total taxable amount for the current assessment year 47236.2

After determining tax liability of the an individual client, it has been seen that total

capital gains acquired by the client after deducting capital loss of precious year is 388700 dollars

on which tax for the 217-2018 is payable as 47236.2 dollars.

TASK 2

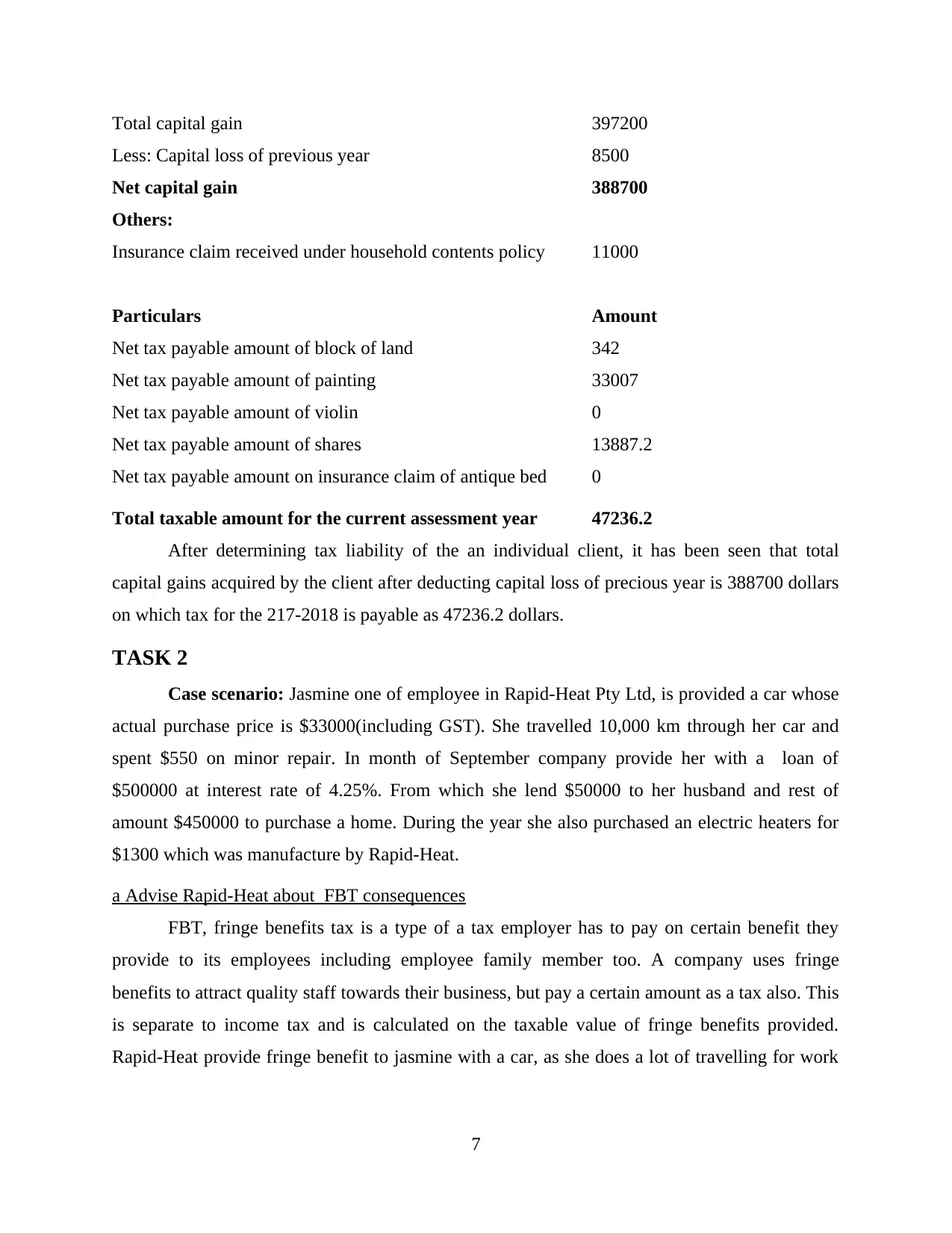

Case scenario: Jasmine one of employee in Rapid-Heat Pty Ltd, is provided a car whose

actual purchase price is $33000(including GST). She travelled 10,000 km through her car and

spent $550 on minor repair. In month of September company provide her with a loan of

$500000 at interest rate of 4.25%. From which she lend $50000 to her husband and rest of

amount $450000 to purchase a home. During the year she also purchased an electric heaters for

$1300 which was manufacture by Rapid-Heat.

a Advise Rapid-Heat about FBT consequences

FBT, fringe benefits tax is a type of a tax employer has to pay on certain benefit they

provide to its employees including employee family member too. A company uses fringe

benefits to attract quality staff towards their business, but pay a certain amount as a tax also. This

is separate to income tax and is calculated on the taxable value of fringe benefits provided.

Rapid-Heat provide fringe benefit to jasmine with a car, as she does a lot of travelling for work

7

Less: Capital loss of previous year 8500

Net capital gain 388700

Others:

Insurance claim received under household contents policy 11000

Particulars Amount

Net tax payable amount of block of land 342

Net tax payable amount of painting 33007

Net tax payable amount of violin 0

Net tax payable amount of shares 13887.2

Net tax payable amount on insurance claim of antique bed 0

Total taxable amount for the current assessment year 47236.2

After determining tax liability of the an individual client, it has been seen that total

capital gains acquired by the client after deducting capital loss of precious year is 388700 dollars

on which tax for the 217-2018 is payable as 47236.2 dollars.

TASK 2

Case scenario: Jasmine one of employee in Rapid-Heat Pty Ltd, is provided a car whose

actual purchase price is $33000(including GST). She travelled 10,000 km through her car and

spent $550 on minor repair. In month of September company provide her with a loan of

$500000 at interest rate of 4.25%. From which she lend $50000 to her husband and rest of

amount $450000 to purchase a home. During the year she also purchased an electric heaters for

$1300 which was manufacture by Rapid-Heat.

a Advise Rapid-Heat about FBT consequences

FBT, fringe benefits tax is a type of a tax employer has to pay on certain benefit they

provide to its employees including employee family member too. A company uses fringe

benefits to attract quality staff towards their business, but pay a certain amount as a tax also. This

is separate to income tax and is calculated on the taxable value of fringe benefits provided.

Rapid-Heat provide fringe benefit to jasmine with a car, as she does a lot of travelling for work

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

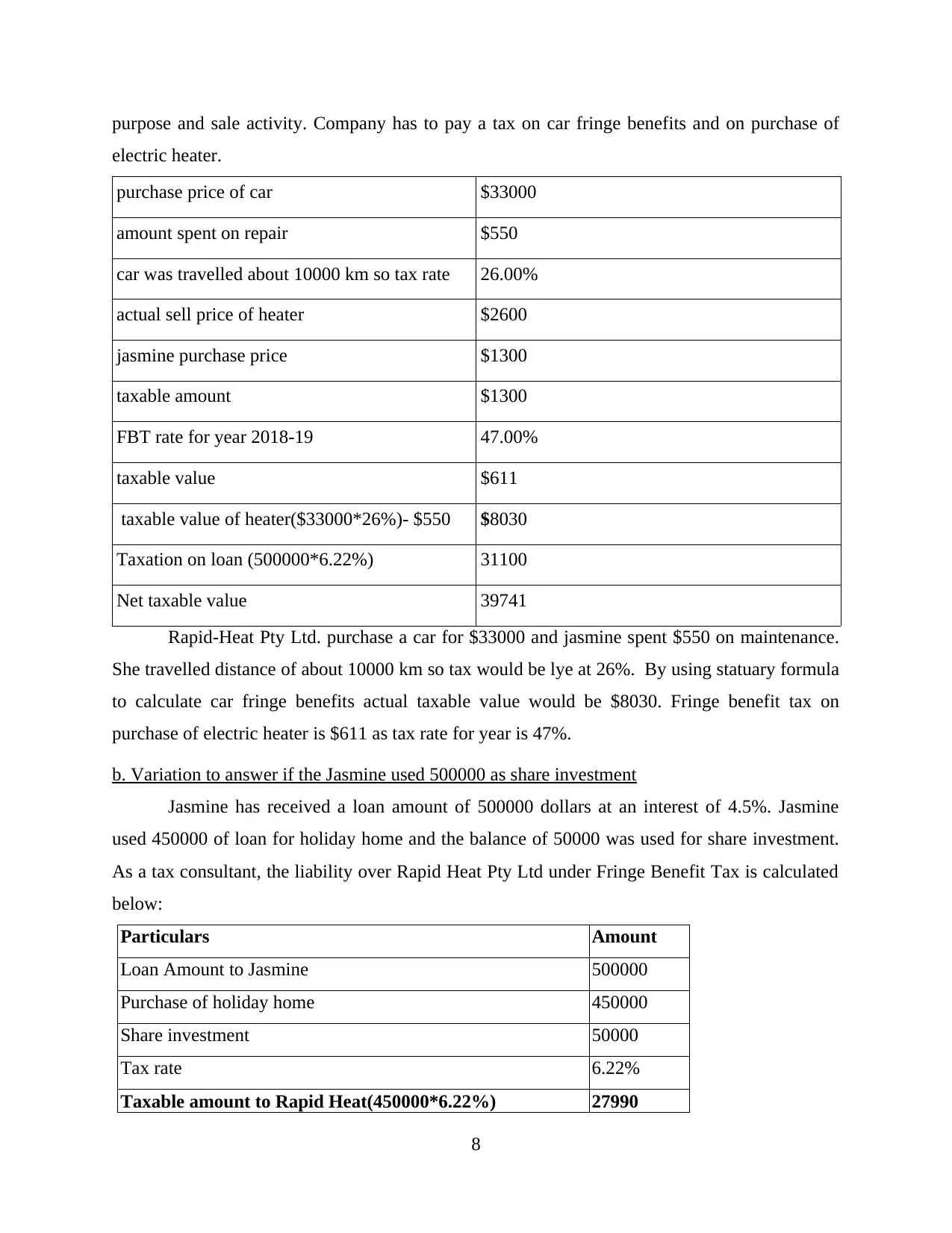

purpose and sale activity. Company has to pay a tax on car fringe benefits and on purchase of

electric heater.

purchase price of car $33000

amount spent on repair $550

car was travelled about 10000 km so tax rate 26.00%

actual sell price of heater $2600

jasmine purchase price $1300

taxable amount $1300

FBT rate for year 2018-19 47.00%

taxable value $611

taxable value of heater($33000*26%)- $550 $8030

Taxation on loan (500000*6.22%) 31100

Net taxable value 39741

Rapid-Heat Pty Ltd. purchase a car for $33000 and jasmine spent $550 on maintenance.

She travelled distance of about 10000 km so tax would be lye at 26%. By using statuary formula

to calculate car fringe benefits actual taxable value would be $8030. Fringe benefit tax on

purchase of electric heater is $611 as tax rate for year is 47%.

b. Variation to answer if the Jasmine used 500000 as share investment

Jasmine has received a loan amount of 500000 dollars at an interest of 4.5%. Jasmine

used 450000 of loan for holiday home and the balance of 50000 was used for share investment.

As a tax consultant, the liability over Rapid Heat Pty Ltd under Fringe Benefit Tax is calculated

below:

Particulars Amount

Loan Amount to Jasmine 500000

Purchase of holiday home 450000

Share investment 50000

Tax rate 6.22%

Taxable amount to Rapid Heat(450000*6.22%) 27990

8

electric heater.

purchase price of car $33000

amount spent on repair $550

car was travelled about 10000 km so tax rate 26.00%

actual sell price of heater $2600

jasmine purchase price $1300

taxable amount $1300

FBT rate for year 2018-19 47.00%

taxable value $611

taxable value of heater($33000*26%)- $550 $8030

Taxation on loan (500000*6.22%) 31100

Net taxable value 39741

Rapid-Heat Pty Ltd. purchase a car for $33000 and jasmine spent $550 on maintenance.

She travelled distance of about 10000 km so tax would be lye at 26%. By using statuary formula

to calculate car fringe benefits actual taxable value would be $8030. Fringe benefit tax on

purchase of electric heater is $611 as tax rate for year is 47%.

b. Variation to answer if the Jasmine used 500000 as share investment

Jasmine has received a loan amount of 500000 dollars at an interest of 4.5%. Jasmine

used 450000 of loan for holiday home and the balance of 50000 was used for share investment.

As a tax consultant, the liability over Rapid Heat Pty Ltd under Fringe Benefit Tax is calculated

below:

Particulars Amount

Loan Amount to Jasmine 500000

Purchase of holiday home 450000

Share investment 50000

Tax rate 6.22%

Taxable amount to Rapid Heat(450000*6.22%) 27990

8

From the above calculation, it has been seen that due to purchase of shares the net taxable

amount on loan is reduced because the amount used to purchase shares are considered as

investments which are not taxable. Hence, the net taxable amount on loan is 27990.

CONCLUSION

From the above project report, it has been observed that taxation law and is practices are

plays a significant role in investments. From analysing the first case scenario, it has been

analysed that the client is an antique collector and does not runs any business and by selling her

capital assets, she has received a huge amount of capital gains which are taxable under taxation

law. By analysing second case scenario, it has been analysed that Rapid Heat company has faced

various consequences of FBT.

9

amount on loan is reduced because the amount used to purchase shares are considered as

investments which are not taxable. Hence, the net taxable amount on loan is 27990.

CONCLUSION

From the above project report, it has been observed that taxation law and is practices are

plays a significant role in investments. From analysing the first case scenario, it has been

analysed that the client is an antique collector and does not runs any business and by selling her

capital assets, she has received a huge amount of capital gains which are taxable under taxation

law. By analysing second case scenario, it has been analysed that Rapid Heat company has faced

various consequences of FBT.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.