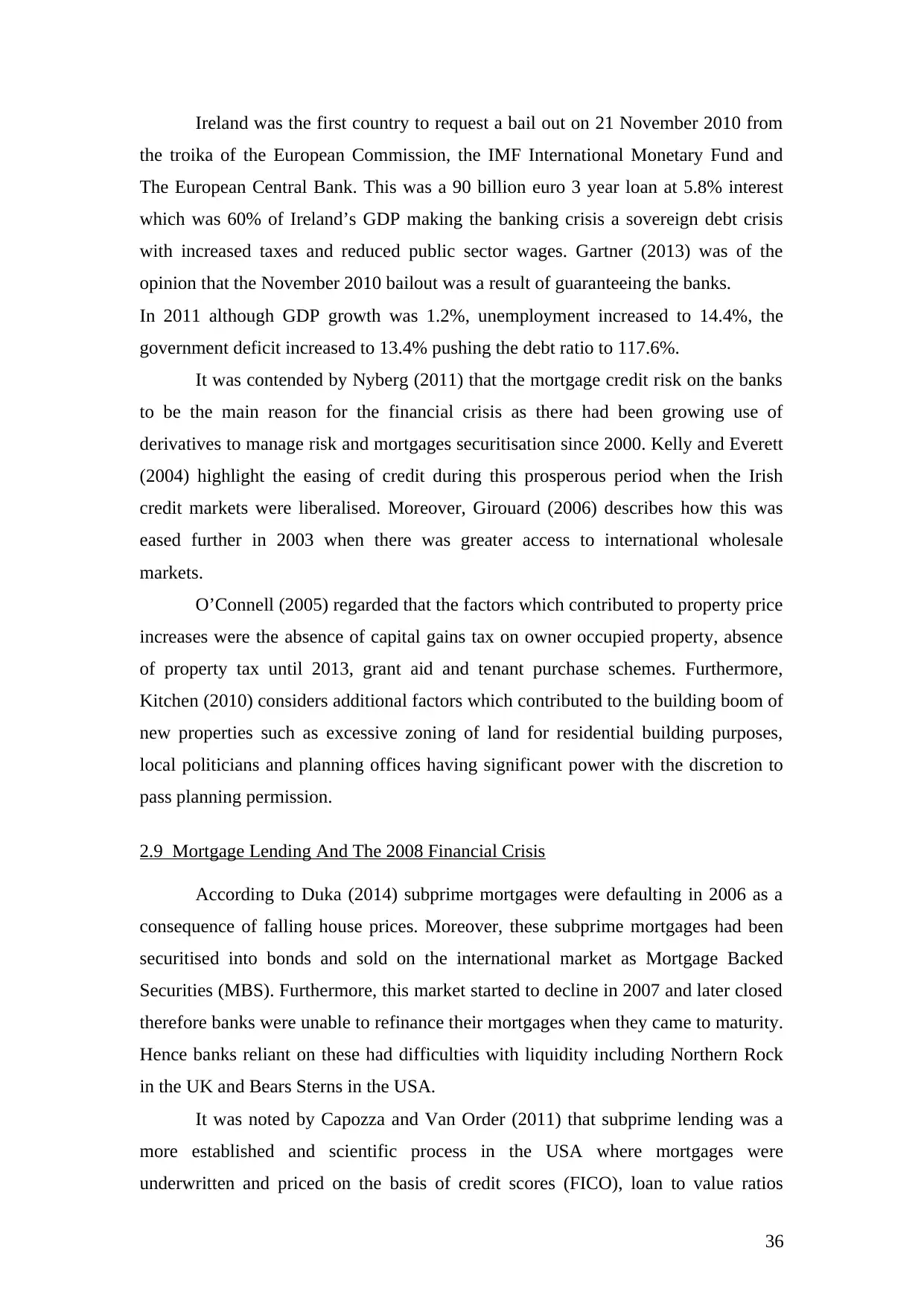

This assignment requires an in-depth examination of recession and crisis management. It involves analyzing the causes, effects, and responses to economic downturns in various countries, including the United States and the United Kingdom. The assignment also delves into specific events such as the Great Depression, the Irish Sovereign Debt Crisis, and the 2007-2008 Global Financial Crisis. Additionally, it explores policies and interventions implemented by governments to mitigate these crises, including fiscal measures, monetary policy, and social housing initiatives. The assignment aims to provide a nuanced understanding of recession and crisis management, highlighting key lessons for policymakers and researchers.

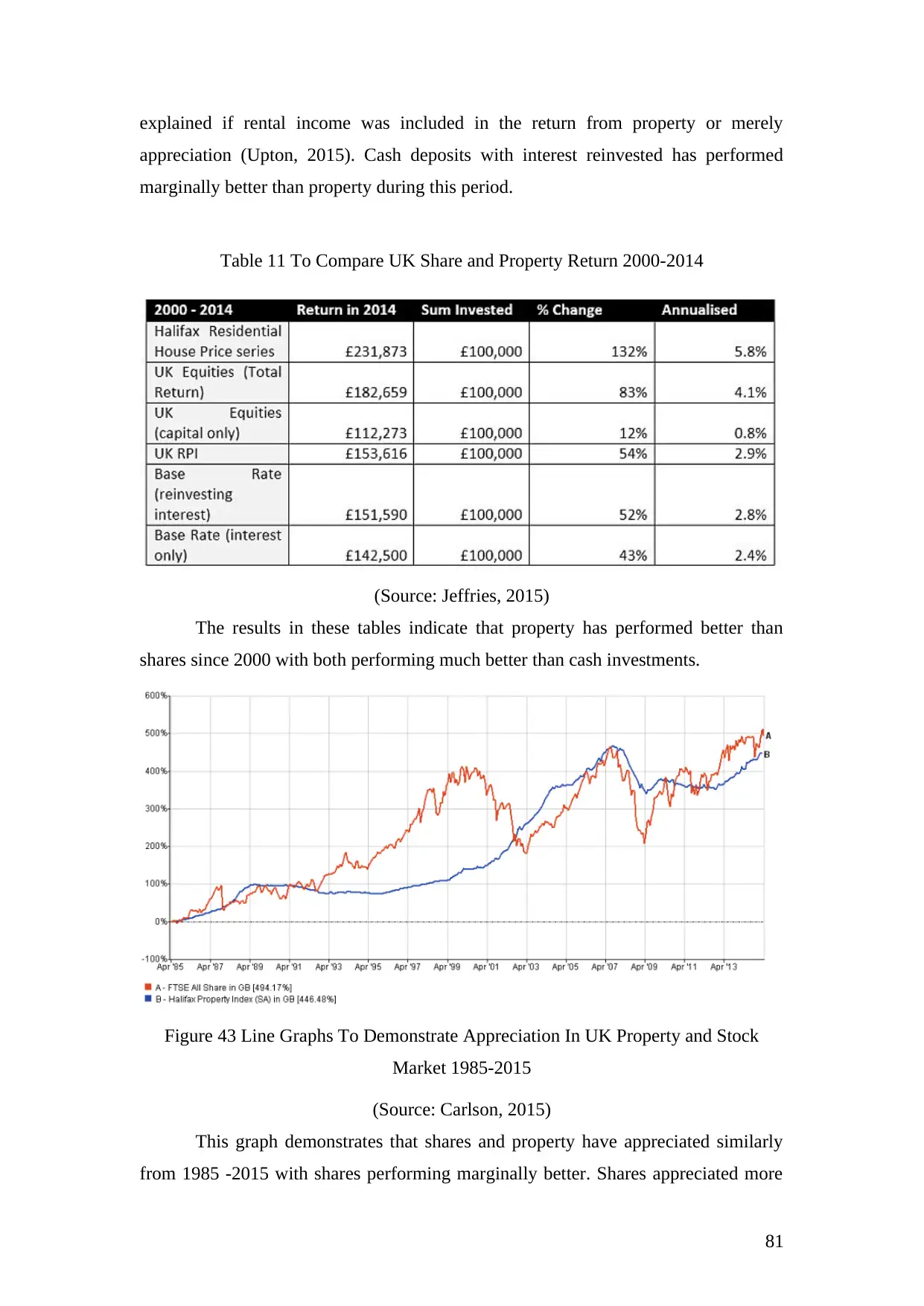

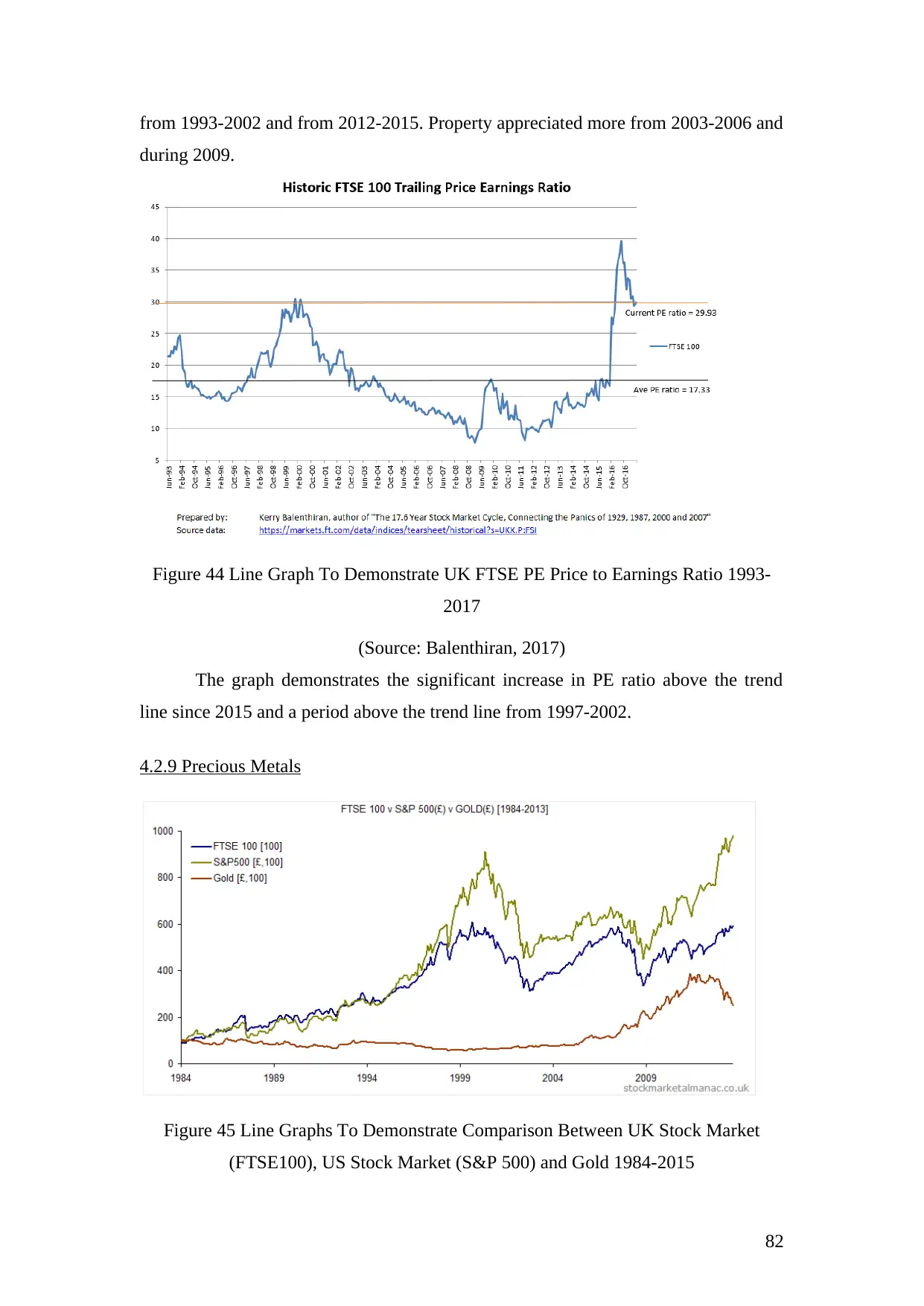

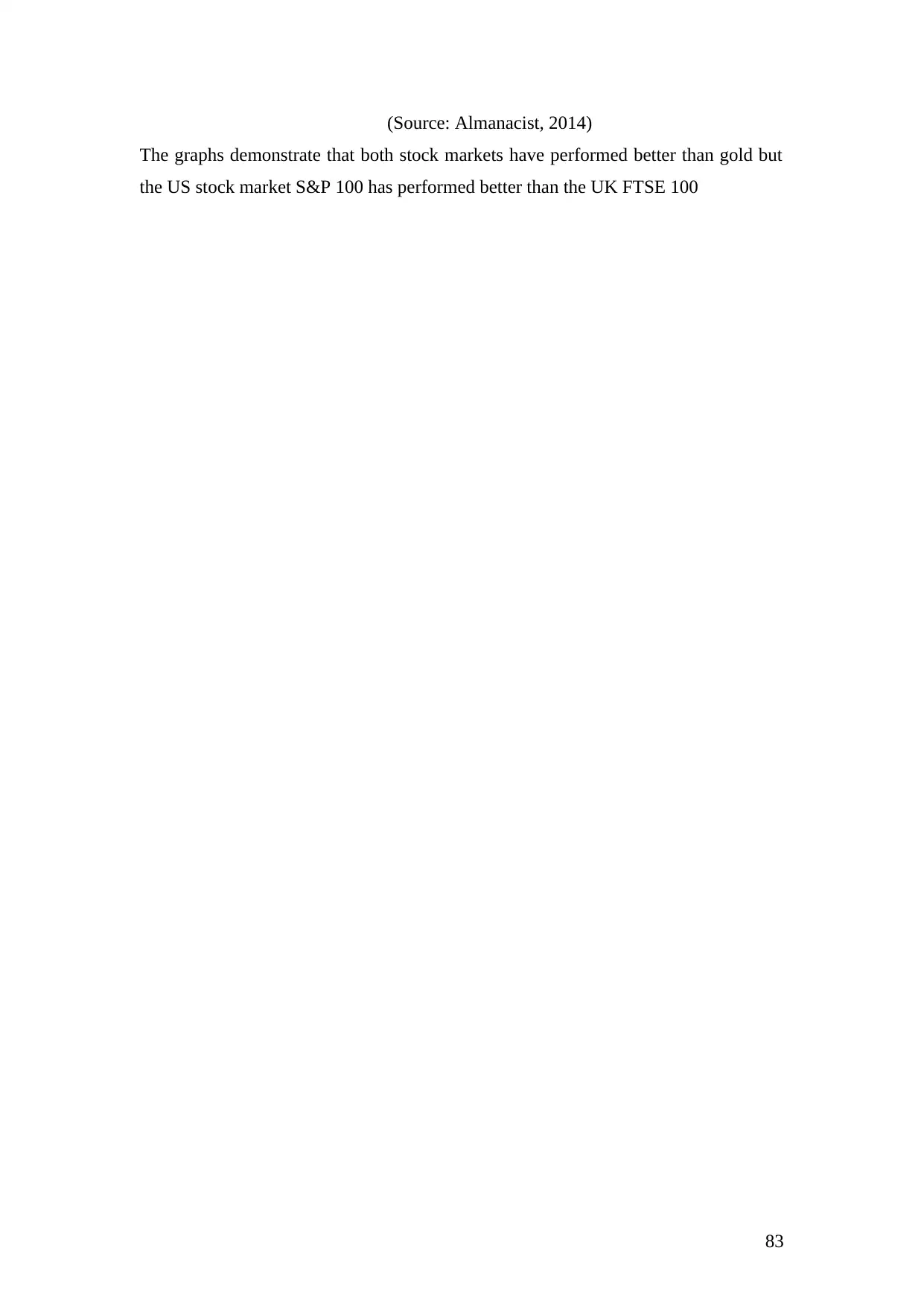

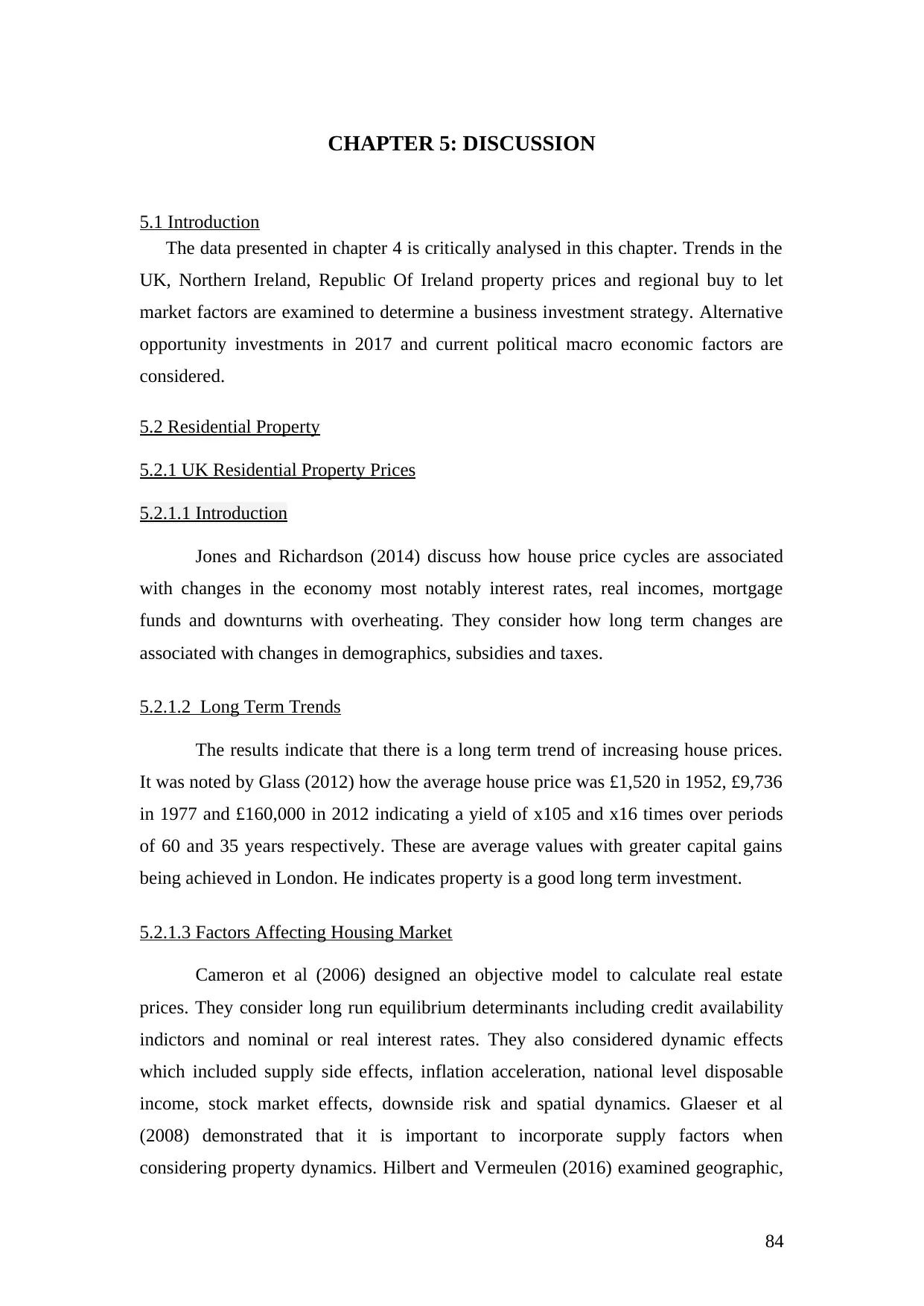

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)