The Institute of Management Accountants

VerifiedAdded on 2022/09/02

|15

|2016

|13

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student

Name of the University

Author Note

Management Accounting

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question 1...................................................................................................................2

Answer to Question 2...................................................................................................................2

Answer to Question 3...................................................................................................................6

Answer to Question 4...................................................................................................................9

Answer to Question 5.................................................................................................................10

Answer to Question 6.................................................................................................................12

Bibliography...............................................................................................................................14

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question 1...................................................................................................................2

Answer to Question 2...................................................................................................................2

Answer to Question 3...................................................................................................................6

Answer to Question 4...................................................................................................................9

Answer to Question 5.................................................................................................................10

Answer to Question 6.................................................................................................................12

Bibliography...............................................................................................................................14

2

MANAGEMENT ACCOUNTING

Answer to Question 1

The main standard which is being jeopardised, as provided by the Institute of

Management Accountants (IMA) is that of competence. It states that the members of IMA

should maintain an appropriate level of professional leadership by enhancing their knowledge

and skills. They should also perform their professional duties in accordance with the relevant

laws, regulations and technical standards. However, in the given situation Bjorn does not have

any necessary skills or qualifications required for performing the role of a management

accountant. As the person being hired by Anni-Frid and Benny does not have the required

professional knowledge, it cannot be expected that they will be able to expand their knowledge

or skills. Similarly, they will also not be able to perform their professional duties with relevant

laws, regulations or technical standards. It also cannot be expected that they would be able to

identify any risk or manage it appropriately. Hence, as the person lacks any of the professional

competencies required to become a Management Accountant, it can be said that the ethical

standard of competence is being violated in this regard.

Answer to Question 2

a) Fixed costs are the ones which remain the same irrespective of the level of production

undertaken by the entity. They continue to remain the same for every year and are to be

paid irrespective of whether a business undertakes any activity. In this case, the fixed

costs incurred by Stylish Chairs are as follows:

Rent of Administrative Offices in CBD and Dandenong

Cost of handling bureaucracy

Miscellaneous costs of administrative office

Salary of supervisor in Dandenong

MANAGEMENT ACCOUNTING

Answer to Question 1

The main standard which is being jeopardised, as provided by the Institute of

Management Accountants (IMA) is that of competence. It states that the members of IMA

should maintain an appropriate level of professional leadership by enhancing their knowledge

and skills. They should also perform their professional duties in accordance with the relevant

laws, regulations and technical standards. However, in the given situation Bjorn does not have

any necessary skills or qualifications required for performing the role of a management

accountant. As the person being hired by Anni-Frid and Benny does not have the required

professional knowledge, it cannot be expected that they will be able to expand their knowledge

or skills. Similarly, they will also not be able to perform their professional duties with relevant

laws, regulations or technical standards. It also cannot be expected that they would be able to

identify any risk or manage it appropriately. Hence, as the person lacks any of the professional

competencies required to become a Management Accountant, it can be said that the ethical

standard of competence is being violated in this regard.

Answer to Question 2

a) Fixed costs are the ones which remain the same irrespective of the level of production

undertaken by the entity. They continue to remain the same for every year and are to be

paid irrespective of whether a business undertakes any activity. In this case, the fixed

costs incurred by Stylish Chairs are as follows:

Rent of Administrative Offices in CBD and Dandenong

Cost of handling bureaucracy

Miscellaneous costs of administrative office

Salary of supervisor in Dandenong

3

MANAGEMENT ACCOUNTING

Administrative costs of warehouse

The variable costs incurred by an entity are the ones which are incurred by an entity on

the basis of the change in the level of production incurred by it. Some of the variable

costs are as follows:

Sales Commission

Invoicing Costs

Material Costs

Costs of labour including carpenter and

assembler

Mixed Costs are the ones which are neither completely fixed nor completely

variable in nature and vary between the two. In this case, the quarterly delivery costs of

the products can be classified as being mixed in nature.

Direct Costs are the ones which are identifiable directly with the costs incurred by the

business whereas indirect costs are the ones which may not be directly identified with the

cost of the goods manufactured by the entity. In this case, the direct and indirect costs are

identified as follows:

Direct Costs Indirect Costs

Sales Commission CBD Bureaucracy

Invoicing costs Administrative office rent

Supervisor salary Miscellaneous costs of administrative

MANAGEMENT ACCOUNTING

Administrative costs of warehouse

The variable costs incurred by an entity are the ones which are incurred by an entity on

the basis of the change in the level of production incurred by it. Some of the variable

costs are as follows:

Sales Commission

Invoicing Costs

Material Costs

Costs of labour including carpenter and

assembler

Mixed Costs are the ones which are neither completely fixed nor completely

variable in nature and vary between the two. In this case, the quarterly delivery costs of

the products can be classified as being mixed in nature.

Direct Costs are the ones which are identifiable directly with the costs incurred by the

business whereas indirect costs are the ones which may not be directly identified with the

cost of the goods manufactured by the entity. In this case, the direct and indirect costs are

identified as follows:

Direct Costs Indirect Costs

Sales Commission CBD Bureaucracy

Invoicing costs Administrative office rent

Supervisor salary Miscellaneous costs of administrative

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING

office

Delivery Costs

Material costs

Labour costs

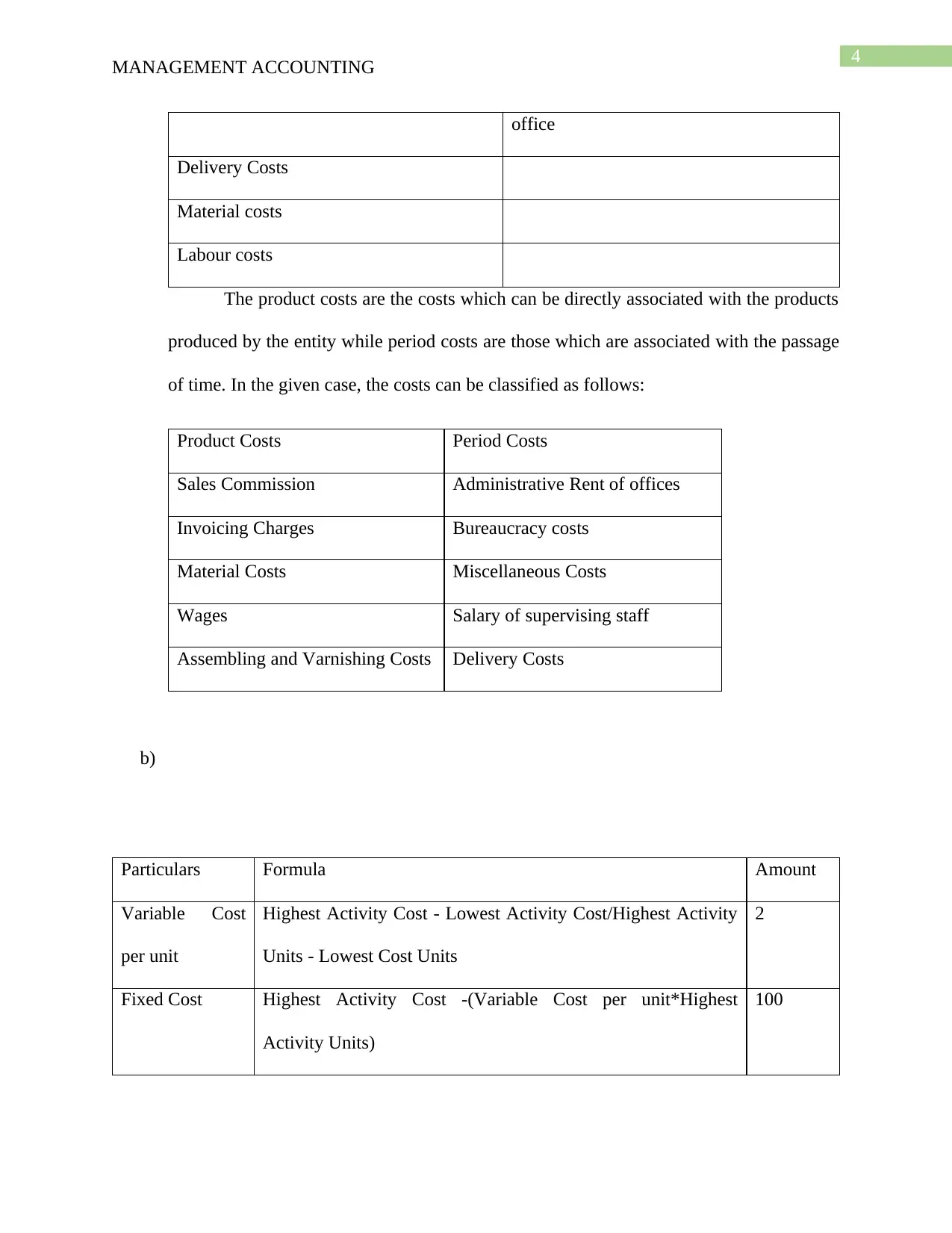

The product costs are the costs which can be directly associated with the products

produced by the entity while period costs are those which are associated with the passage

of time. In the given case, the costs can be classified as follows:

Product Costs Period Costs

Sales Commission Administrative Rent of offices

Invoicing Charges Bureaucracy costs

Material Costs Miscellaneous Costs

Wages Salary of supervising staff

Assembling and Varnishing Costs Delivery Costs

b)

Particulars Formula Amount

Variable Cost

per unit

Highest Activity Cost - Lowest Activity Cost/Highest Activity

Units - Lowest Cost Units

2

Fixed Cost Highest Activity Cost -(Variable Cost per unit*Highest

Activity Units)

100

MANAGEMENT ACCOUNTING

office

Delivery Costs

Material costs

Labour costs

The product costs are the costs which can be directly associated with the products

produced by the entity while period costs are those which are associated with the passage

of time. In the given case, the costs can be classified as follows:

Product Costs Period Costs

Sales Commission Administrative Rent of offices

Invoicing Charges Bureaucracy costs

Material Costs Miscellaneous Costs

Wages Salary of supervising staff

Assembling and Varnishing Costs Delivery Costs

b)

Particulars Formula Amount

Variable Cost

per unit

Highest Activity Cost - Lowest Activity Cost/Highest Activity

Units - Lowest Cost Units

2

Fixed Cost Highest Activity Cost -(Variable Cost per unit*Highest

Activity Units)

100

5

MANAGEMENT ACCOUNTING

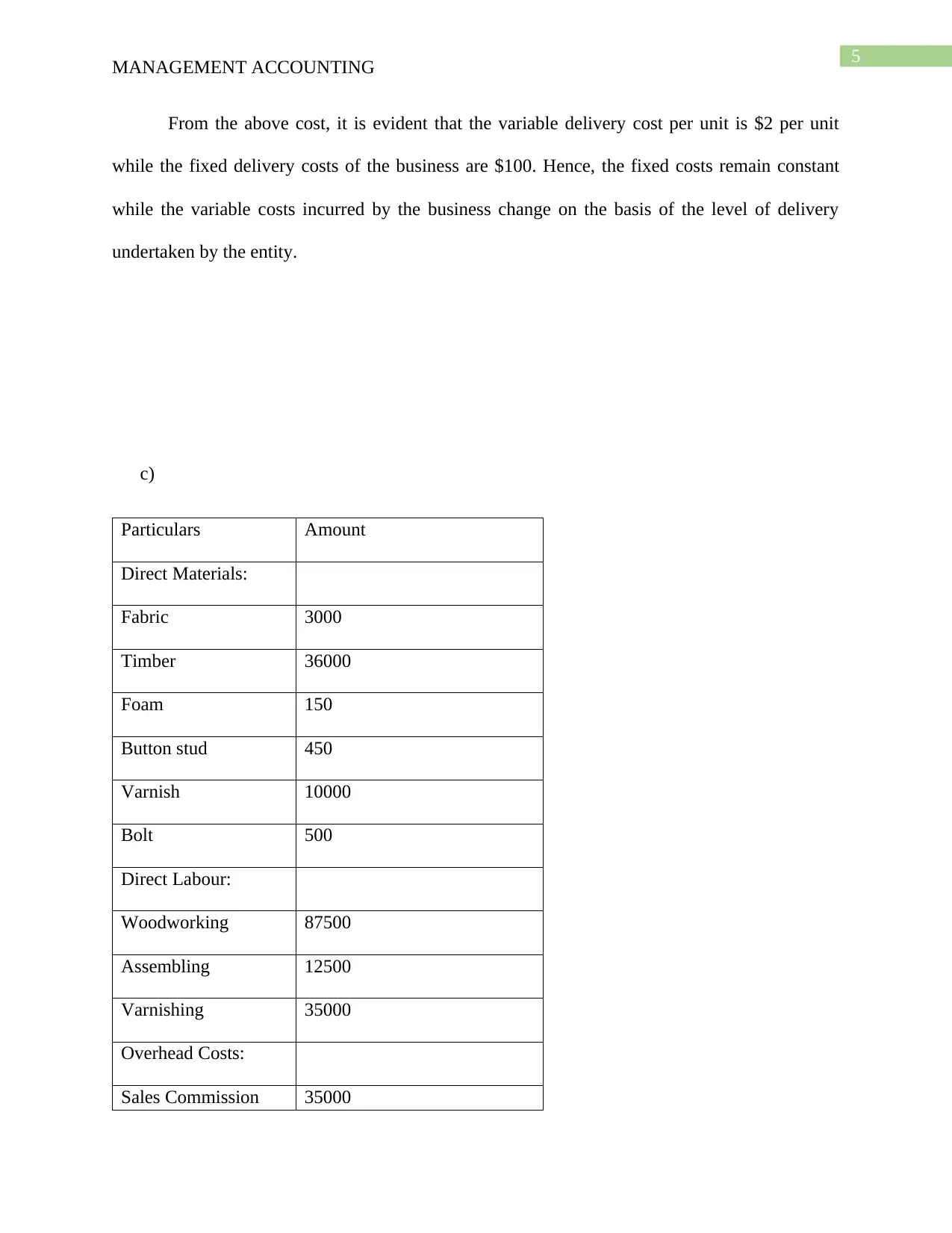

From the above cost, it is evident that the variable delivery cost per unit is $2 per unit

while the fixed delivery costs of the business are $100. Hence, the fixed costs remain constant

while the variable costs incurred by the business change on the basis of the level of delivery

undertaken by the entity.

c)

Particulars Amount

Direct Materials:

Fabric 3000

Timber 36000

Foam 150

Button stud 450

Varnish 10000

Bolt 500

Direct Labour:

Woodworking 87500

Assembling 12500

Varnishing 35000

Overhead Costs:

Sales Commission 35000

MANAGEMENT ACCOUNTING

From the above cost, it is evident that the variable delivery cost per unit is $2 per unit

while the fixed delivery costs of the business are $100. Hence, the fixed costs remain constant

while the variable costs incurred by the business change on the basis of the level of delivery

undertaken by the entity.

c)

Particulars Amount

Direct Materials:

Fabric 3000

Timber 36000

Foam 150

Button stud 450

Varnish 10000

Bolt 500

Direct Labour:

Woodworking 87500

Assembling 12500

Varnishing 35000

Overhead Costs:

Sales Commission 35000

6

MANAGEMENT ACCOUNTING

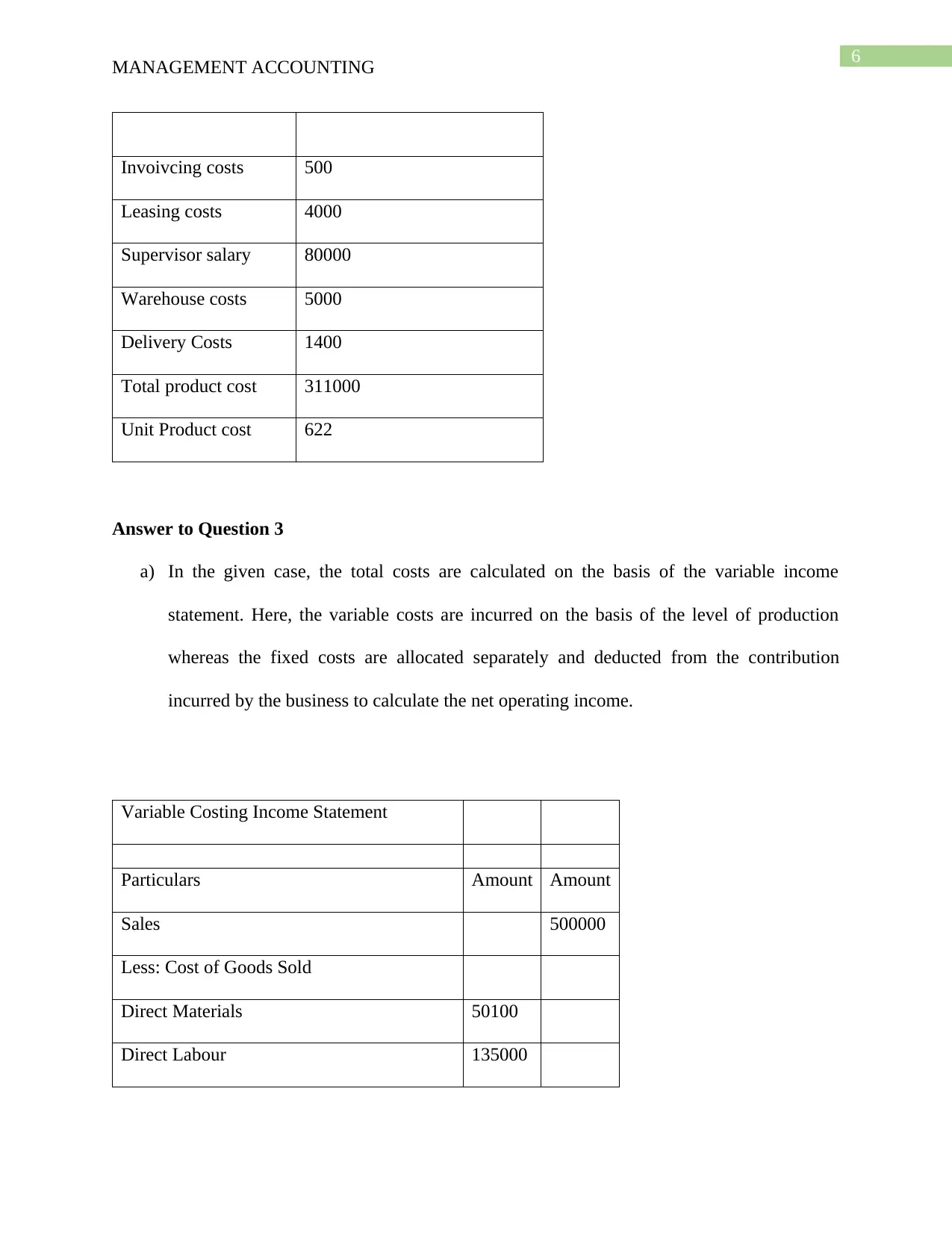

Invoivcing costs 500

Leasing costs 4000

Supervisor salary 80000

Warehouse costs 5000

Delivery Costs 1400

Total product cost 311000

Unit Product cost 622

Answer to Question 3

a) In the given case, the total costs are calculated on the basis of the variable income

statement. Here, the variable costs are incurred on the basis of the level of production

whereas the fixed costs are allocated separately and deducted from the contribution

incurred by the business to calculate the net operating income.

Variable Costing Income Statement

Particulars Amount Amount

Sales 500000

Less: Cost of Goods Sold

Direct Materials 50100

Direct Labour 135000

MANAGEMENT ACCOUNTING

Invoivcing costs 500

Leasing costs 4000

Supervisor salary 80000

Warehouse costs 5000

Delivery Costs 1400

Total product cost 311000

Unit Product cost 622

Answer to Question 3

a) In the given case, the total costs are calculated on the basis of the variable income

statement. Here, the variable costs are incurred on the basis of the level of production

whereas the fixed costs are allocated separately and deducted from the contribution

incurred by the business to calculate the net operating income.

Variable Costing Income Statement

Particulars Amount Amount

Sales 500000

Less: Cost of Goods Sold

Direct Materials 50100

Direct Labour 135000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

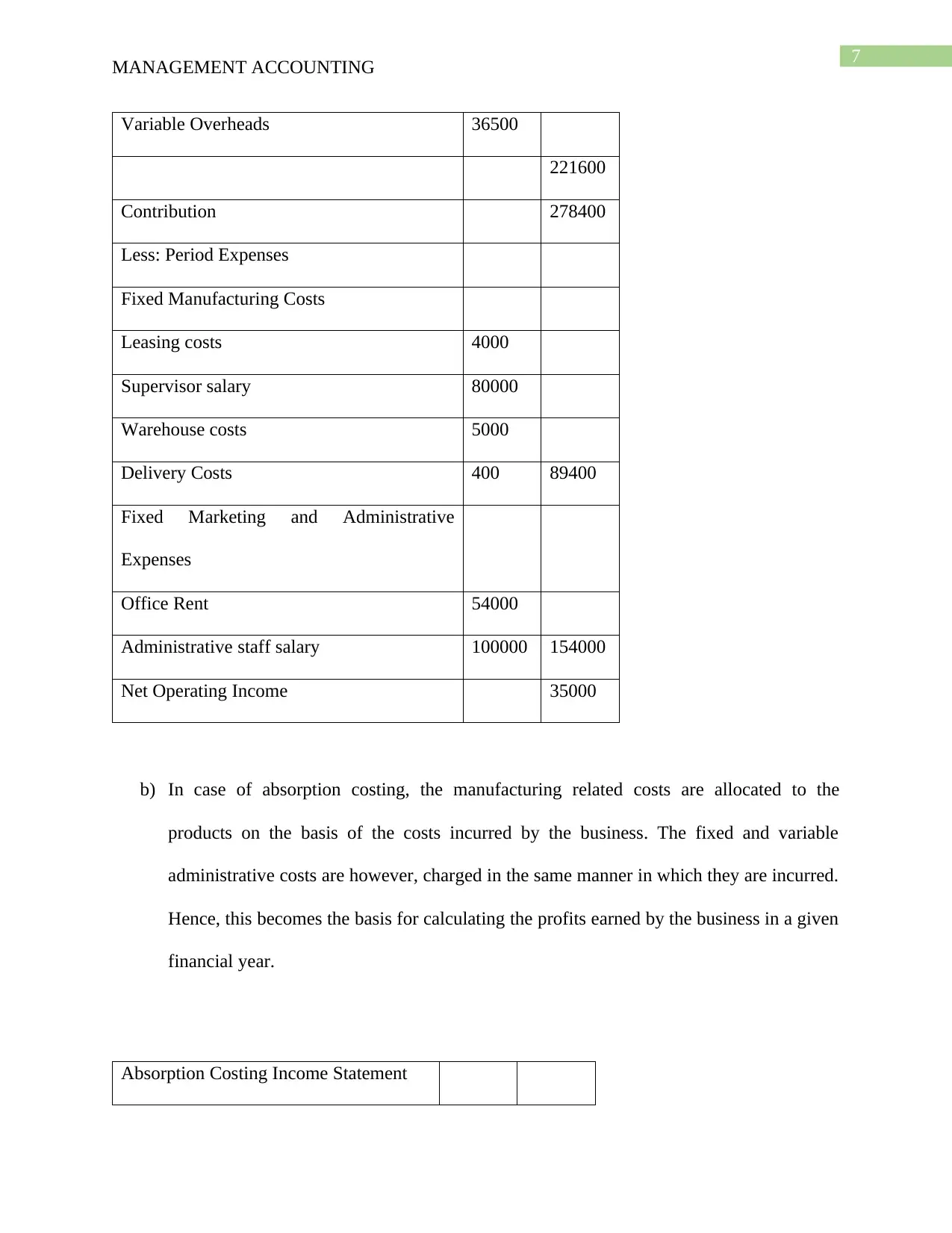

Variable Overheads 36500

221600

Contribution 278400

Less: Period Expenses

Fixed Manufacturing Costs

Leasing costs 4000

Supervisor salary 80000

Warehouse costs 5000

Delivery Costs 400 89400

Fixed Marketing and Administrative

Expenses

Office Rent 54000

Administrative staff salary 100000 154000

Net Operating Income 35000

b) In case of absorption costing, the manufacturing related costs are allocated to the

products on the basis of the costs incurred by the business. The fixed and variable

administrative costs are however, charged in the same manner in which they are incurred.

Hence, this becomes the basis for calculating the profits earned by the business in a given

financial year.

Absorption Costing Income Statement

MANAGEMENT ACCOUNTING

Variable Overheads 36500

221600

Contribution 278400

Less: Period Expenses

Fixed Manufacturing Costs

Leasing costs 4000

Supervisor salary 80000

Warehouse costs 5000

Delivery Costs 400 89400

Fixed Marketing and Administrative

Expenses

Office Rent 54000

Administrative staff salary 100000 154000

Net Operating Income 35000

b) In case of absorption costing, the manufacturing related costs are allocated to the

products on the basis of the costs incurred by the business. The fixed and variable

administrative costs are however, charged in the same manner in which they are incurred.

Hence, this becomes the basis for calculating the profits earned by the business in a given

financial year.

Absorption Costing Income Statement

8

MANAGEMENT ACCOUNTING

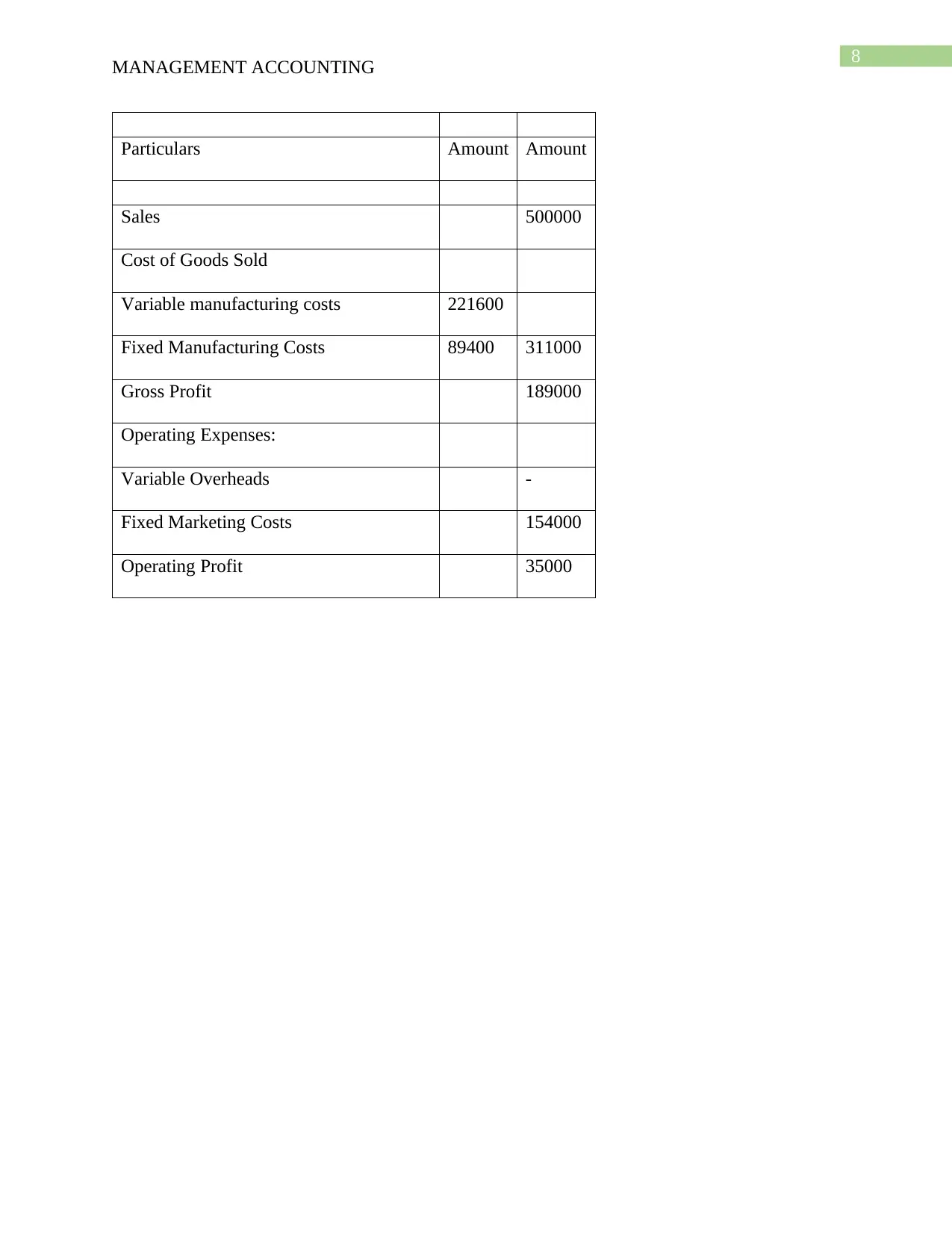

Particulars Amount Amount

Sales 500000

Cost of Goods Sold

Variable manufacturing costs 221600

Fixed Manufacturing Costs 89400 311000

Gross Profit 189000

Operating Expenses:

Variable Overheads -

Fixed Marketing Costs 154000

Operating Profit 35000

MANAGEMENT ACCOUNTING

Particulars Amount Amount

Sales 500000

Cost of Goods Sold

Variable manufacturing costs 221600

Fixed Manufacturing Costs 89400 311000

Gross Profit 189000

Operating Expenses:

Variable Overheads -

Fixed Marketing Costs 154000

Operating Profit 35000

9

MANAGEMENT ACCOUNTING

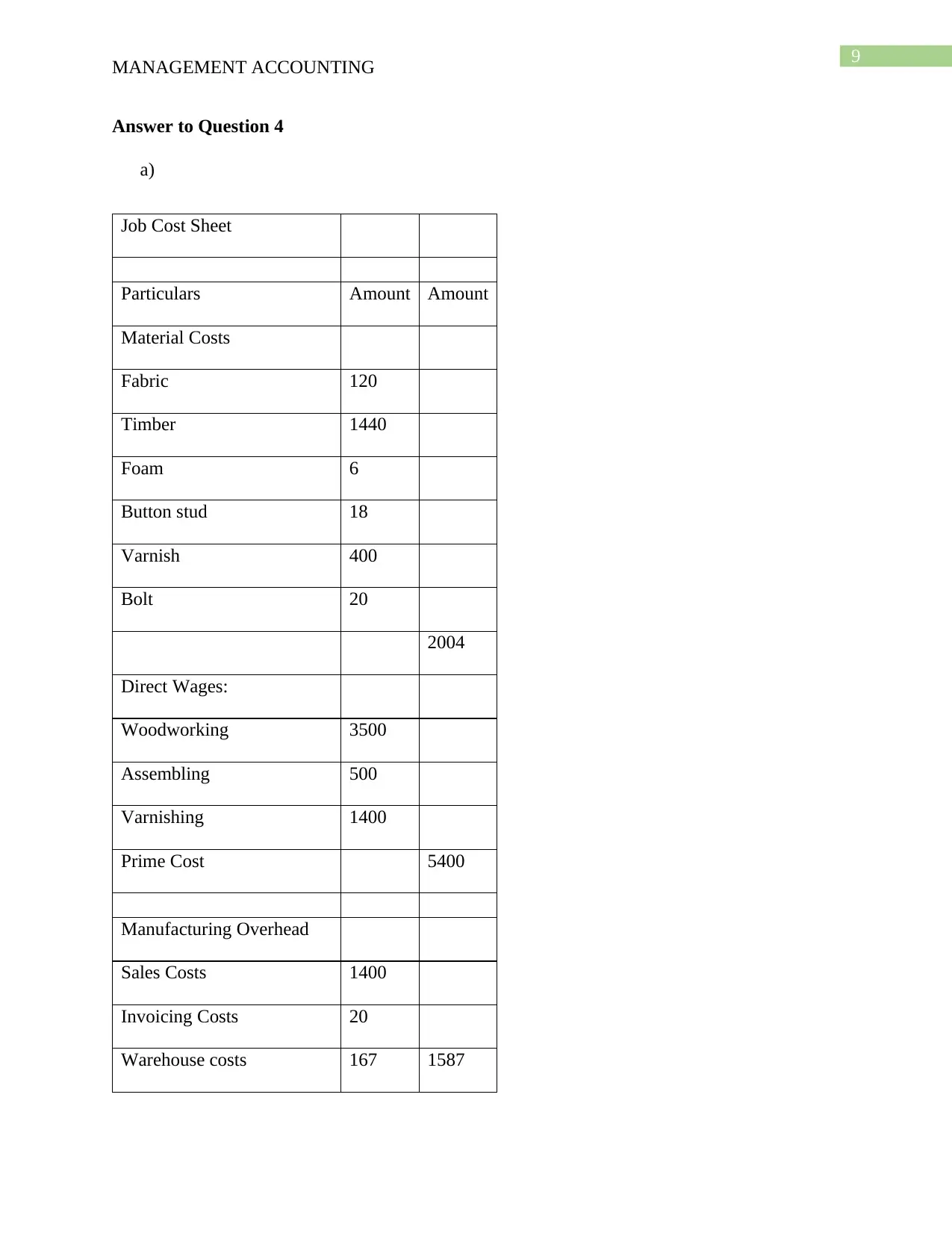

Answer to Question 4

a)

Job Cost Sheet

Particulars Amount Amount

Material Costs

Fabric 120

Timber 1440

Foam 6

Button stud 18

Varnish 400

Bolt 20

2004

Direct Wages:

Woodworking 3500

Assembling 500

Varnishing 1400

Prime Cost 5400

Manufacturing Overhead

Sales Costs 1400

Invoicing Costs 20

Warehouse costs 167 1587

MANAGEMENT ACCOUNTING

Answer to Question 4

a)

Job Cost Sheet

Particulars Amount Amount

Material Costs

Fabric 120

Timber 1440

Foam 6

Button stud 18

Varnish 400

Bolt 20

2004

Direct Wages:

Woodworking 3500

Assembling 500

Varnishing 1400

Prime Cost 5400

Manufacturing Overhead

Sales Costs 1400

Invoicing Costs 20

Warehouse costs 167 1587

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MANAGEMENT ACCOUNTING

Total Costs under Job

Costing

8991

b) In a direct allocation method, the overhead costs are allocated on the basis of all the

services provided to a production department. Any services which are provided by a

service department to another service department are disregarded and thus this method of

allocation becomes an extremely simple manner of allocating the overheads. In the given

situation, the costs incurred in producing the standard quantity of goods is highest in case

of woodworking. This is higher for woodworking when compared to assembling and

vanishing. Hence, any overheads which are allocated on the basis of the direct labour

hours will be allocated at the highest for the activity which consumes most of the

expenditure. This is also because the allocation is done on a proportionate basis. Hence,

any manufacturing overheads which are allocated by the business are highest in case of

woodworking.

Answer to Question 5

In this case, the decision to sell or further develop a product depends on the level of

profits earned from it in the current situation. If the operating profits exceed the previously

existing profits, then the product should be sold. If they do not exceed the profits, then the

decision should be made to further refine the product and make it increasingly cheaper to

produce. The calculation below suggests the variable costing operating income that can be

earned with the help of the product.

MANAGEMENT ACCOUNTING

Total Costs under Job

Costing

8991

b) In a direct allocation method, the overhead costs are allocated on the basis of all the

services provided to a production department. Any services which are provided by a

service department to another service department are disregarded and thus this method of

allocation becomes an extremely simple manner of allocating the overheads. In the given

situation, the costs incurred in producing the standard quantity of goods is highest in case

of woodworking. This is higher for woodworking when compared to assembling and

vanishing. Hence, any overheads which are allocated on the basis of the direct labour

hours will be allocated at the highest for the activity which consumes most of the

expenditure. This is also because the allocation is done on a proportionate basis. Hence,

any manufacturing overheads which are allocated by the business are highest in case of

woodworking.

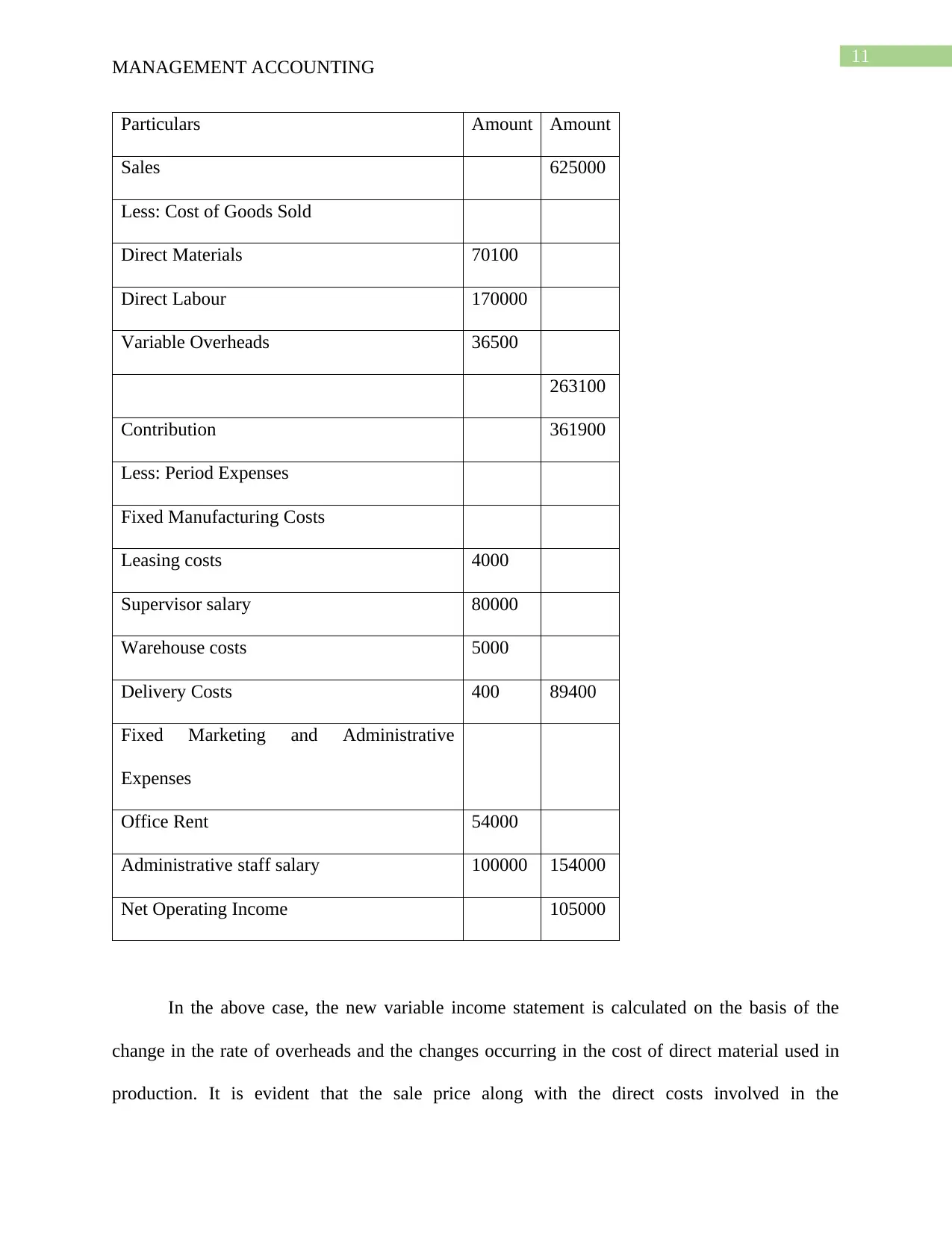

Answer to Question 5

In this case, the decision to sell or further develop a product depends on the level of

profits earned from it in the current situation. If the operating profits exceed the previously

existing profits, then the product should be sold. If they do not exceed the profits, then the

decision should be made to further refine the product and make it increasingly cheaper to

produce. The calculation below suggests the variable costing operating income that can be

earned with the help of the product.

11

MANAGEMENT ACCOUNTING

Particulars Amount Amount

Sales 625000

Less: Cost of Goods Sold

Direct Materials 70100

Direct Labour 170000

Variable Overheads 36500

263100

Contribution 361900

Less: Period Expenses

Fixed Manufacturing Costs

Leasing costs 4000

Supervisor salary 80000

Warehouse costs 5000

Delivery Costs 400 89400

Fixed Marketing and Administrative

Expenses

Office Rent 54000

Administrative staff salary 100000 154000

Net Operating Income 105000

In the above case, the new variable income statement is calculated on the basis of the

change in the rate of overheads and the changes occurring in the cost of direct material used in

production. It is evident that the sale price along with the direct costs involved in the

MANAGEMENT ACCOUNTING

Particulars Amount Amount

Sales 625000

Less: Cost of Goods Sold

Direct Materials 70100

Direct Labour 170000

Variable Overheads 36500

263100

Contribution 361900

Less: Period Expenses

Fixed Manufacturing Costs

Leasing costs 4000

Supervisor salary 80000

Warehouse costs 5000

Delivery Costs 400 89400

Fixed Marketing and Administrative

Expenses

Office Rent 54000

Administrative staff salary 100000 154000

Net Operating Income 105000

In the above case, the new variable income statement is calculated on the basis of the

change in the rate of overheads and the changes occurring in the cost of direct material used in

production. It is evident that the sale price along with the direct costs involved in the

12

MANAGEMENT ACCOUNTING

manufacture of products have increased significantly. However, in order to understand the

viability of the new product, the new income statement is prepared in accordance with the

changed costs and income. An analysis of the available information along these lines suggests

that the net operating income of the business has gone up to $105000. Hence, as producing the

new product is generating more returns for the business, the business will be better off by

producing the new product. The production of this particular product should be undertaken at a

large scale as long as the fixed costs remain under control.

Answer to Question 6

a) This statement of Bjorn is correct. This is because the unit cost of a product is calculated

by dividing the total cost of production with the total number of units manufactured by

the business. Hence, as the denominator continues to increase, the overall calculated

value will decrease. This is when the fixed costs which were incurred in the last year also

continue to remain the same in the current year. Even though the basis of apportionment

of the fixed overheads may change, the costs incurred tend to remain the same. When the

overall costs are calculated on the basis of traditional cost of manufacturing, then the

fixed costs remains the same. When calculated, this would bring down the cost incurred

per unit. Even when the absorption costing method is used, the costs incurred per unit

would come down by a significant amount. This is because the fixed costs also change

with the level of production. An increased level of production would reduce the total

costs. Hence, it can be said that the overall unit cost of production would decrease

because the fixed costs remain the same and there are no significant changes in the direct

costs incurred by the business.

MANAGEMENT ACCOUNTING

manufacture of products have increased significantly. However, in order to understand the

viability of the new product, the new income statement is prepared in accordance with the

changed costs and income. An analysis of the available information along these lines suggests

that the net operating income of the business has gone up to $105000. Hence, as producing the

new product is generating more returns for the business, the business will be better off by

producing the new product. The production of this particular product should be undertaken at a

large scale as long as the fixed costs remain under control.

Answer to Question 6

a) This statement of Bjorn is correct. This is because the unit cost of a product is calculated

by dividing the total cost of production with the total number of units manufactured by

the business. Hence, as the denominator continues to increase, the overall calculated

value will decrease. This is when the fixed costs which were incurred in the last year also

continue to remain the same in the current year. Even though the basis of apportionment

of the fixed overheads may change, the costs incurred tend to remain the same. When the

overall costs are calculated on the basis of traditional cost of manufacturing, then the

fixed costs remains the same. When calculated, this would bring down the cost incurred

per unit. Even when the absorption costing method is used, the costs incurred per unit

would come down by a significant amount. This is because the fixed costs also change

with the level of production. An increased level of production would reduce the total

costs. Hence, it can be said that the overall unit cost of production would decrease

because the fixed costs remain the same and there are no significant changes in the direct

costs incurred by the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

MANAGEMENT ACCOUNTING

b) In this situation, the statement of Bjorn is wrong. This is because there arise situations

when the new businesses established by an entity find it difficult to allocate the indirect

costs incurred by them. This is particularly in case of the indirect or overhead costs

incurred by an entity. In the absorption costing method, allocation of overheads happens

on the basis of the different drivers determining the overhead costs incurred by the entity.

Hence, if the company is able to achieve more production than the budgeted production,

it can be said that there is an over allocation of overhead costs. However, if the company

is producing below the budgeted level of production, it can be said that the business is not

producing sufficient level of output for the amount of indirect costs available with it. This

would result in an under allocation of the overheads. In the given case, the company is

producing only 500 units whereas the budgeted production was 600 units. Hence, the

entity is clearly not able to use the overheads available with it in an efficient manner and

there is an under allocation of the indirect costs available with it.

MANAGEMENT ACCOUNTING

b) In this situation, the statement of Bjorn is wrong. This is because there arise situations

when the new businesses established by an entity find it difficult to allocate the indirect

costs incurred by them. This is particularly in case of the indirect or overhead costs

incurred by an entity. In the absorption costing method, allocation of overheads happens

on the basis of the different drivers determining the overhead costs incurred by the entity.

Hence, if the company is able to achieve more production than the budgeted production,

it can be said that there is an over allocation of overhead costs. However, if the company

is producing below the budgeted level of production, it can be said that the business is not

producing sufficient level of output for the amount of indirect costs available with it. This

would result in an under allocation of the overheads. In the given case, the company is

producing only 500 units whereas the budgeted production was 600 units. Hence, the

entity is clearly not able to use the overheads available with it in an efficient manner and

there is an under allocation of the indirect costs available with it.

14

MANAGEMENT ACCOUNTING

Bibliography

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Imanet.org. (2020). [online] Available at: https://www.imanet.org/career-resources/ethics-center?

ssopc=1 [Accessed 4 Apr. 2020].

Mueller, D., 2018. The usability and suitability of allocation schemes for corporate cost

accounting. In Game Theory in Management Accounting (pp. 401-427). Springer, Cham.

MANAGEMENT ACCOUNTING

Bibliography

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Imanet.org. (2020). [online] Available at: https://www.imanet.org/career-resources/ethics-center?

ssopc=1 [Accessed 4 Apr. 2020].

Mueller, D., 2018. The usability and suitability of allocation schemes for corporate cost

accounting. In Game Theory in Management Accounting (pp. 401-427). Springer, Cham.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.