The Australian Dollar and the Exchange Rates Assignment

VerifiedAdded on 2021/05/31

|33

|5865

|40

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES

Name of the student

Instructor

Institution

Course

Date

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES

Name of the student

Instructor

Institution

Course

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 2

Factors that affect movements in the Australian Dollar include;

QUESTION 1A

Farming; this is because close to 12% of the value of the AUD comes from farming activities

and the related agricultural processes. If any unfortunate events such as drought or restriction

that prevents the export of these agricultural products occur, then the AUD will be affected.

Reserve bank policies; the AUD is quite popular for the bilateral trade between Australia

and Japanese Yen, for which an interest rate of close to 4% spreads between these two countries.

The Australian bank reserve policies will determine the direction of the interest rate and the

profitability of the AUD as far as investment is concerned. (Blundell-Wignall, 2015)

Mining; the price of the Australian dollar is largely impacted by resources such as oil,

gold and coal. This means that depletion of such resources or putting a restriction to their

exploitation and also a fall in demand of these resources in the export markets will have an

impact on the performance of the AUD.

QUESTION 1B

This movement affects the profitability of Australian businesses in several ways depending on

whether it is a depreciation or appreciation;

When AUD appreciates, the profits from imports would increase because it makes the

imports cheap and hence their demands increases. On the other hand, appreciation decreases the

profits from exports because it makes the exports to be expensive and hence reduces their

demands abroad

Factors that affect movements in the Australian Dollar include;

QUESTION 1A

Farming; this is because close to 12% of the value of the AUD comes from farming activities

and the related agricultural processes. If any unfortunate events such as drought or restriction

that prevents the export of these agricultural products occur, then the AUD will be affected.

Reserve bank policies; the AUD is quite popular for the bilateral trade between Australia

and Japanese Yen, for which an interest rate of close to 4% spreads between these two countries.

The Australian bank reserve policies will determine the direction of the interest rate and the

profitability of the AUD as far as investment is concerned. (Blundell-Wignall, 2015)

Mining; the price of the Australian dollar is largely impacted by resources such as oil,

gold and coal. This means that depletion of such resources or putting a restriction to their

exploitation and also a fall in demand of these resources in the export markets will have an

impact on the performance of the AUD.

QUESTION 1B

This movement affects the profitability of Australian businesses in several ways depending on

whether it is a depreciation or appreciation;

When AUD appreciates, the profits from imports would increase because it makes the

imports cheap and hence their demands increases. On the other hand, appreciation decreases the

profits from exports because it makes the exports to be expensive and hence reduces their

demands abroad

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 3

When the AUD depreciates, profitability from the imports decreases because it makes the

imports to be expensive thus a reduction in demand. Consequently, it increases profitability from

the exports because it makes the exports cheap and thus increases their demand.

QUESTION 1C

Foreign exchange hedging is a type of a transaction that is carried out by a forex business

people or investors to protect their businesses from foreign exchange risks that arises from

transactions in foreign currencies. Hedging would assist Australian businesses to diversify

globally and take advantage of these global markets without having to incur the risks of currency

losses. (Dash, 2013). https://www.rba.gov.au/publications/bulletin/2017/dec/8.html.

Question 2a

Roles of Interest Rates in the Economy

An increase in the interest rates encourages saving and this leaves them with less

disposable income, thereby decreasing the price levels. In contrast, a decrease in the interest rates

encourages borrowing and this leaves consumers with more disposable incomes which increases

the price levels.

Price levels are measured using the consumer price index(CPI). It measures the

percentage change in the price of basket of goods and services purchased by households.

When the AUD depreciates, profitability from the imports decreases because it makes the

imports to be expensive thus a reduction in demand. Consequently, it increases profitability from

the exports because it makes the exports cheap and thus increases their demand.

QUESTION 1C

Foreign exchange hedging is a type of a transaction that is carried out by a forex business

people or investors to protect their businesses from foreign exchange risks that arises from

transactions in foreign currencies. Hedging would assist Australian businesses to diversify

globally and take advantage of these global markets without having to incur the risks of currency

losses. (Dash, 2013). https://www.rba.gov.au/publications/bulletin/2017/dec/8.html.

Question 2a

Roles of Interest Rates in the Economy

An increase in the interest rates encourages saving and this leaves them with less

disposable income, thereby decreasing the price levels. In contrast, a decrease in the interest rates

encourages borrowing and this leaves consumers with more disposable incomes which increases

the price levels.

Price levels are measured using the consumer price index(CPI). It measures the

percentage change in the price of basket of goods and services purchased by households.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 4

Interest rates plays a role in the economic growth in that raising it increases the cost of

borrowing, which in turns reduces the disposable income and hence limiting consumer

expenditures which in turn thwarts economic growth (John, 2014).

The GDP is the measure of economic growth. It is arrived at by summing the total value

of goods and services produced within the country.

Interest rates can also control unemployment in that lower interest rates would encourage

borrowing which would leave the consumers with higher disposable incomes, this increases their

expenditure on goods and services and increases demand. It also enables them invest in the

economy thereby creation of jobs through these investments and high demands.

Unemployment rate is the proportion of the labor force that is unemployed. To get to this

statistic we need to calculate the total number of people who are unemployed, we then take this

total as a percentage of the total labor force. Labor force is the total individuals over the age of

15 who are eligible to work, and it includes those in employment and those unemployed.. (John,

2014).

Question 2b

Expansionary and Contractionary Monetary Policies

Expansionary monetary policies lead to a decrease in the interest rates. to increase money

supply in the economy, the interest rates are lowered so as to encourage borrowing and stimulate

economic growth through high expenditures in the economy.

Interest rates plays a role in the economic growth in that raising it increases the cost of

borrowing, which in turns reduces the disposable income and hence limiting consumer

expenditures which in turn thwarts economic growth (John, 2014).

The GDP is the measure of economic growth. It is arrived at by summing the total value

of goods and services produced within the country.

Interest rates can also control unemployment in that lower interest rates would encourage

borrowing which would leave the consumers with higher disposable incomes, this increases their

expenditure on goods and services and increases demand. It also enables them invest in the

economy thereby creation of jobs through these investments and high demands.

Unemployment rate is the proportion of the labor force that is unemployed. To get to this

statistic we need to calculate the total number of people who are unemployed, we then take this

total as a percentage of the total labor force. Labor force is the total individuals over the age of

15 who are eligible to work, and it includes those in employment and those unemployed.. (John,

2014).

Question 2b

Expansionary and Contractionary Monetary Policies

Expansionary monetary policies lead to a decrease in the interest rates. to increase money

supply in the economy, the interest rates are lowered so as to encourage borrowing and stimulate

economic growth through high expenditures in the economy.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 5

Contractionary monetary policies decrease the interest rates. This is because it is aimed at

slowing down inflation rates and therefore there is a need to discourage borrowing. (Blanchard,

2017) .

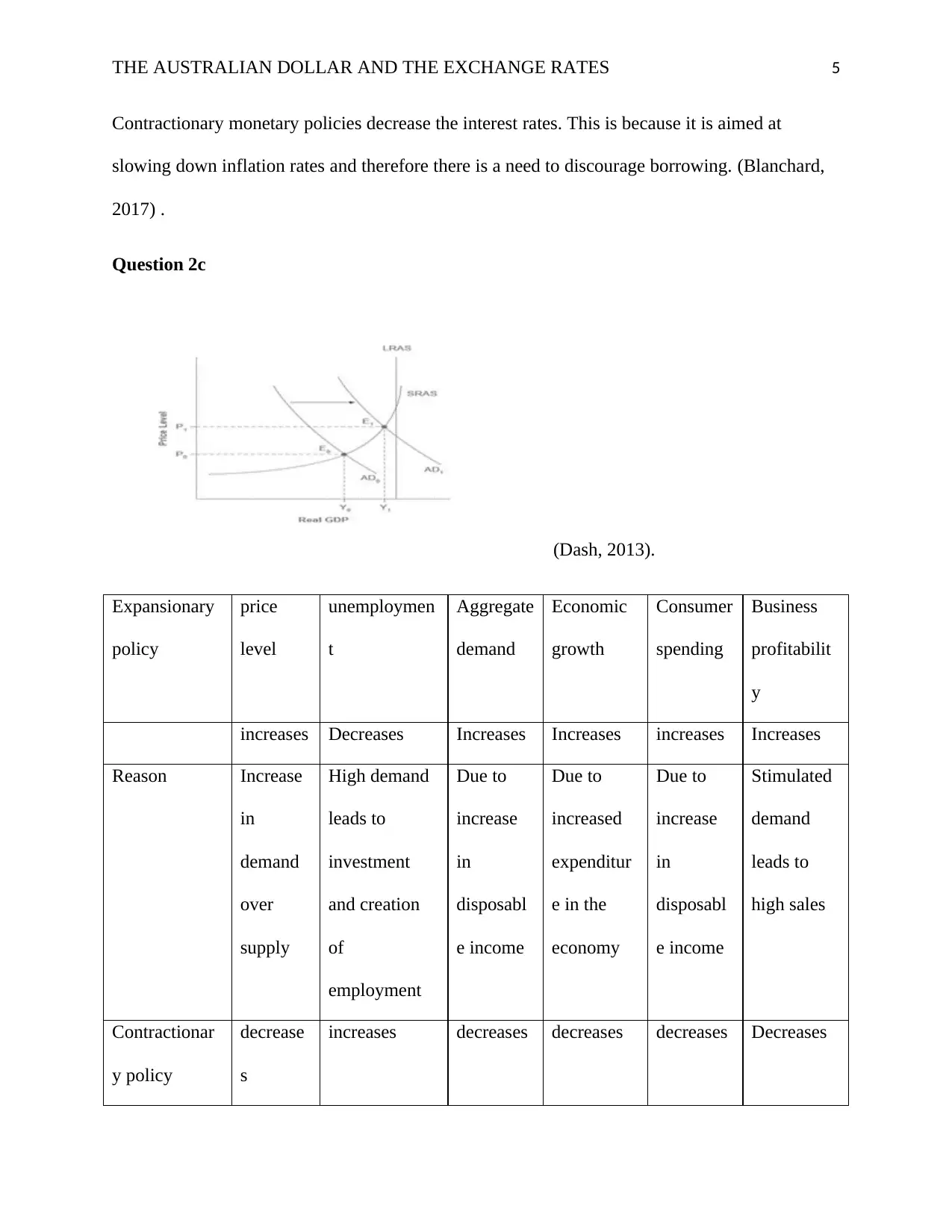

Question 2c

(Dash, 2013).

Expansionary

policy

price

level

unemploymen

t

Aggregate

demand

Economic

growth

Consumer

spending

Business

profitabilit

y

increases Decreases Increases Increases increases Increases

Reason Increase

in

demand

over

supply

High demand

leads to

investment

and creation

of

employment

Due to

increase

in

disposabl

e income

Due to

increased

expenditur

e in the

economy

Due to

increase

in

disposabl

e income

Stimulated

demand

leads to

high sales

Contractionar

y policy

decrease

s

increases decreases decreases decreases Decreases

Contractionary monetary policies decrease the interest rates. This is because it is aimed at

slowing down inflation rates and therefore there is a need to discourage borrowing. (Blanchard,

2017) .

Question 2c

(Dash, 2013).

Expansionary

policy

price

level

unemploymen

t

Aggregate

demand

Economic

growth

Consumer

spending

Business

profitabilit

y

increases Decreases Increases Increases increases Increases

Reason Increase

in

demand

over

supply

High demand

leads to

investment

and creation

of

employment

Due to

increase

in

disposabl

e income

Due to

increased

expenditur

e in the

economy

Due to

increase

in

disposabl

e income

Stimulated

demand

leads to

high sales

Contractionar

y policy

decrease

s

increases decreases decreases decreases Decreases

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 6

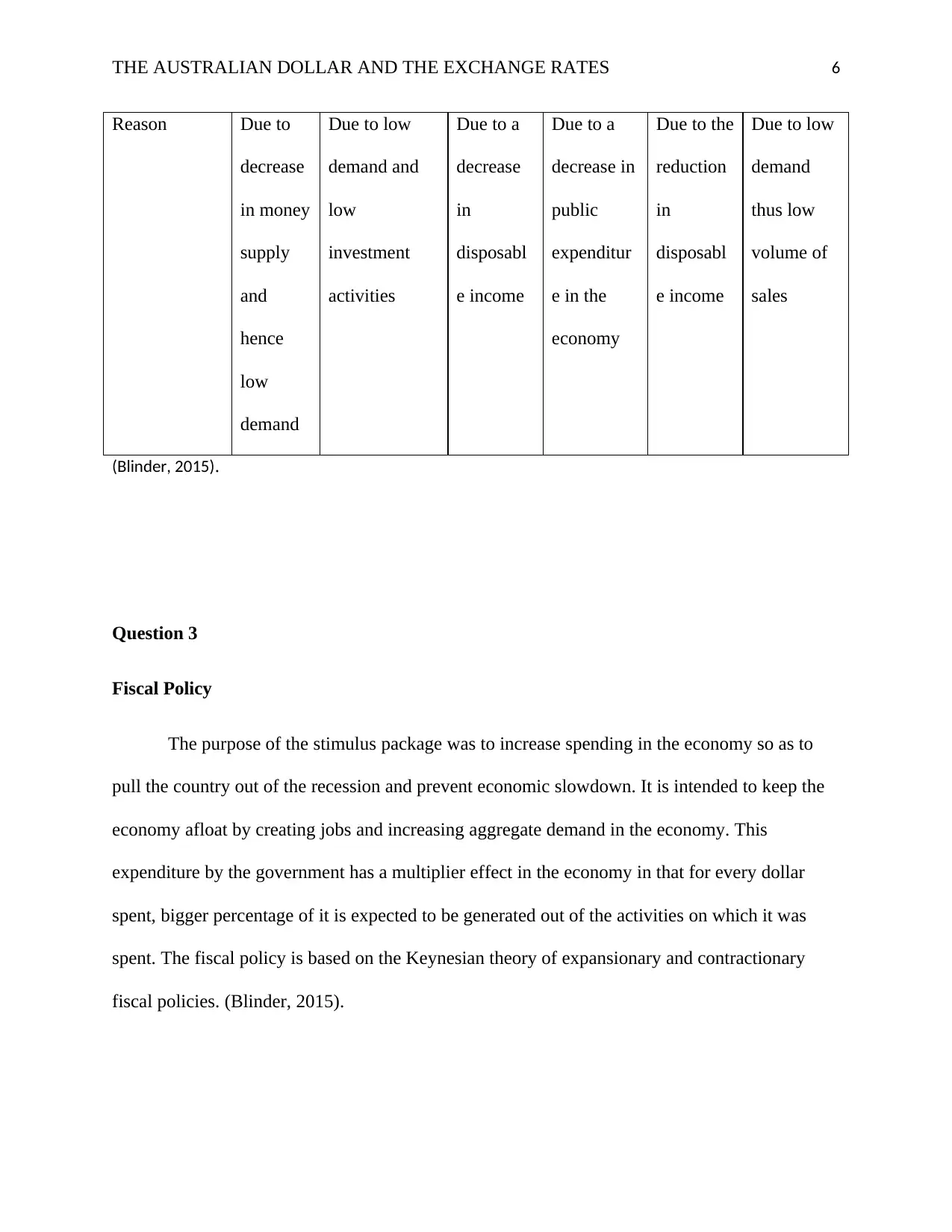

Reason Due to

decrease

in money

supply

and

hence

low

demand

Due to low

demand and

low

investment

activities

Due to a

decrease

in

disposabl

e income

Due to a

decrease in

public

expenditur

e in the

economy

Due to the

reduction

in

disposabl

e income

Due to low

demand

thus low

volume of

sales

(Blinder, 2015).

Question 3

Fiscal Policy

The purpose of the stimulus package was to increase spending in the economy so as to

pull the country out of the recession and prevent economic slowdown. It is intended to keep the

economy afloat by creating jobs and increasing aggregate demand in the economy. This

expenditure by the government has a multiplier effect in the economy in that for every dollar

spent, bigger percentage of it is expected to be generated out of the activities on which it was

spent. The fiscal policy is based on the Keynesian theory of expansionary and contractionary

fiscal policies. (Blinder, 2015).

Reason Due to

decrease

in money

supply

and

hence

low

demand

Due to low

demand and

low

investment

activities

Due to a

decrease

in

disposabl

e income

Due to a

decrease in

public

expenditur

e in the

economy

Due to the

reduction

in

disposabl

e income

Due to low

demand

thus low

volume of

sales

(Blinder, 2015).

Question 3

Fiscal Policy

The purpose of the stimulus package was to increase spending in the economy so as to

pull the country out of the recession and prevent economic slowdown. It is intended to keep the

economy afloat by creating jobs and increasing aggregate demand in the economy. This

expenditure by the government has a multiplier effect in the economy in that for every dollar

spent, bigger percentage of it is expected to be generated out of the activities on which it was

spent. The fiscal policy is based on the Keynesian theory of expansionary and contractionary

fiscal policies. (Blinder, 2015).

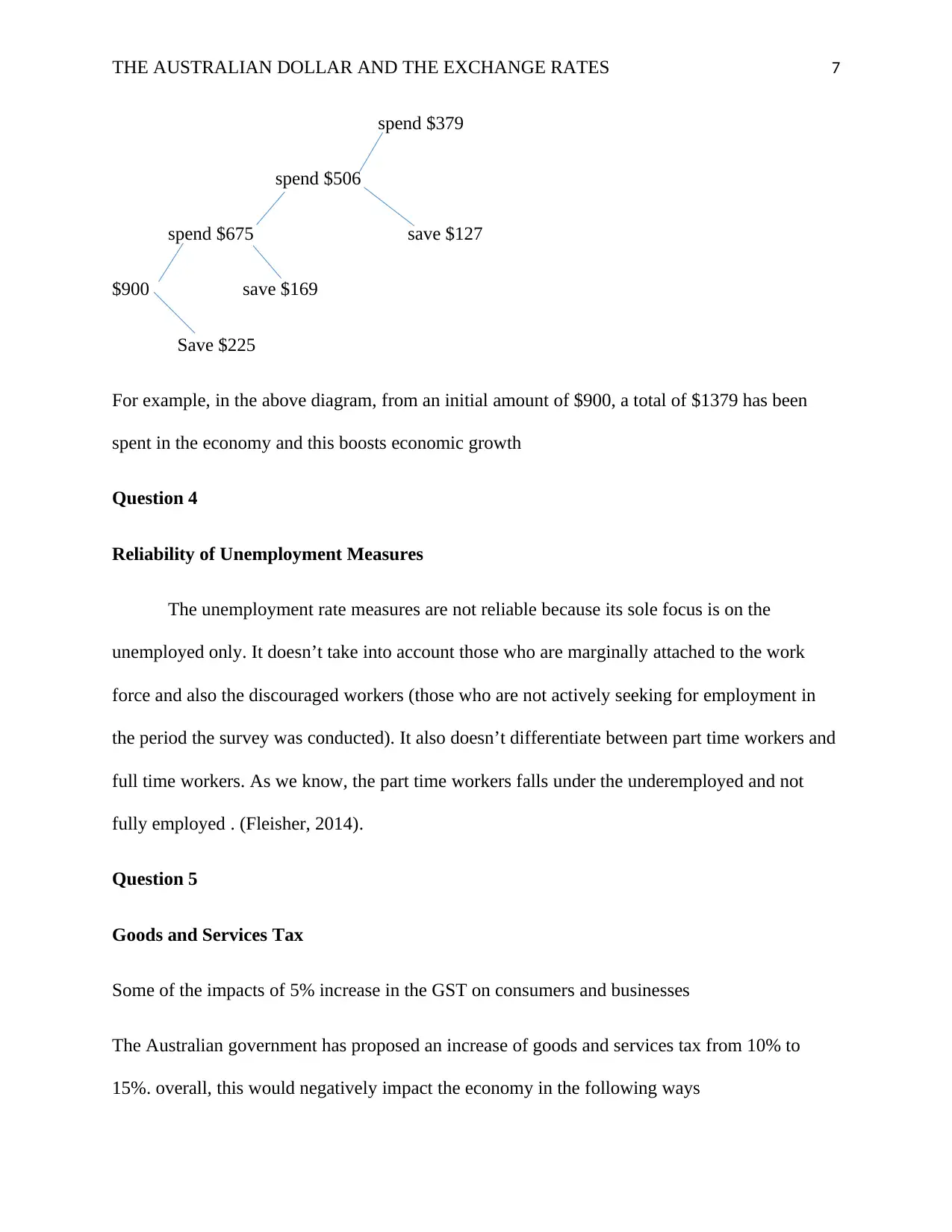

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 7

spend $379

spend $506

spend $675 save $127

$900 save $169

Save $225

For example, in the above diagram, from an initial amount of $900, a total of $1379 has been

spent in the economy and this boosts economic growth

Question 4

Reliability of Unemployment Measures

The unemployment rate measures are not reliable because its sole focus is on the

unemployed only. It doesn’t take into account those who are marginally attached to the work

force and also the discouraged workers (those who are not actively seeking for employment in

the period the survey was conducted). It also doesn’t differentiate between part time workers and

full time workers. As we know, the part time workers falls under the underemployed and not

fully employed . (Fleisher, 2014).

Question 5

Goods and Services Tax

Some of the impacts of 5% increase in the GST on consumers and businesses

The Australian government has proposed an increase of goods and services tax from 10% to

15%. overall, this would negatively impact the economy in the following ways

spend $379

spend $506

spend $675 save $127

$900 save $169

Save $225

For example, in the above diagram, from an initial amount of $900, a total of $1379 has been

spent in the economy and this boosts economic growth

Question 4

Reliability of Unemployment Measures

The unemployment rate measures are not reliable because its sole focus is on the

unemployed only. It doesn’t take into account those who are marginally attached to the work

force and also the discouraged workers (those who are not actively seeking for employment in

the period the survey was conducted). It also doesn’t differentiate between part time workers and

full time workers. As we know, the part time workers falls under the underemployed and not

fully employed . (Fleisher, 2014).

Question 5

Goods and Services Tax

Some of the impacts of 5% increase in the GST on consumers and businesses

The Australian government has proposed an increase of goods and services tax from 10% to

15%. overall, this would negatively impact the economy in the following ways

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 8

There would be a reduction in the consumers spending ability as the increase in prices of these

commodities would discourage spending. Non-essential goods and luxuries would suffer most as

consumers will greatly check their expenditures on these goods.

The costs of production would increase and this would prompt necessary measures by businesses

to counter this. Most likely, they would do this by laying off workers and this would lead to an

increase in the number of those unemployed.

Economic growth would be affected because of the decline in demand of goods and services.

Investments would also decline because the lack of demand. This might force businesses to close

down because it is very unprofitable to do transact in an economy that is doing badly. (Nayak,

2016).

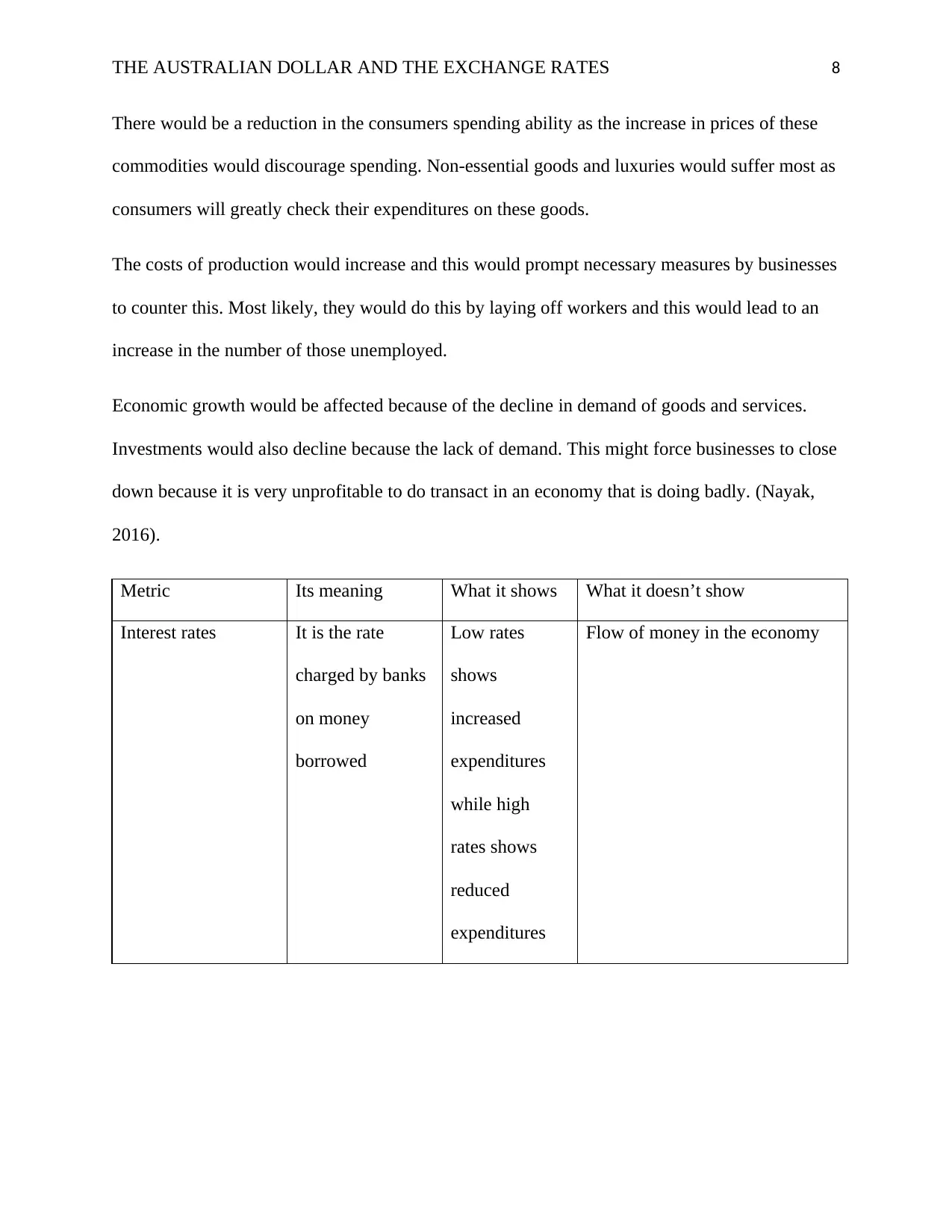

Metric Its meaning What it shows What it doesn’t show

Interest rates It is the rate

charged by banks

on money

borrowed

Low rates

shows

increased

expenditures

while high

rates shows

reduced

expenditures

Flow of money in the economy

There would be a reduction in the consumers spending ability as the increase in prices of these

commodities would discourage spending. Non-essential goods and luxuries would suffer most as

consumers will greatly check their expenditures on these goods.

The costs of production would increase and this would prompt necessary measures by businesses

to counter this. Most likely, they would do this by laying off workers and this would lead to an

increase in the number of those unemployed.

Economic growth would be affected because of the decline in demand of goods and services.

Investments would also decline because the lack of demand. This might force businesses to close

down because it is very unprofitable to do transact in an economy that is doing badly. (Nayak,

2016).

Metric Its meaning What it shows What it doesn’t show

Interest rates It is the rate

charged by banks

on money

borrowed

Low rates

shows

increased

expenditures

while high

rates shows

reduced

expenditures

Flow of money in the economy

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 9

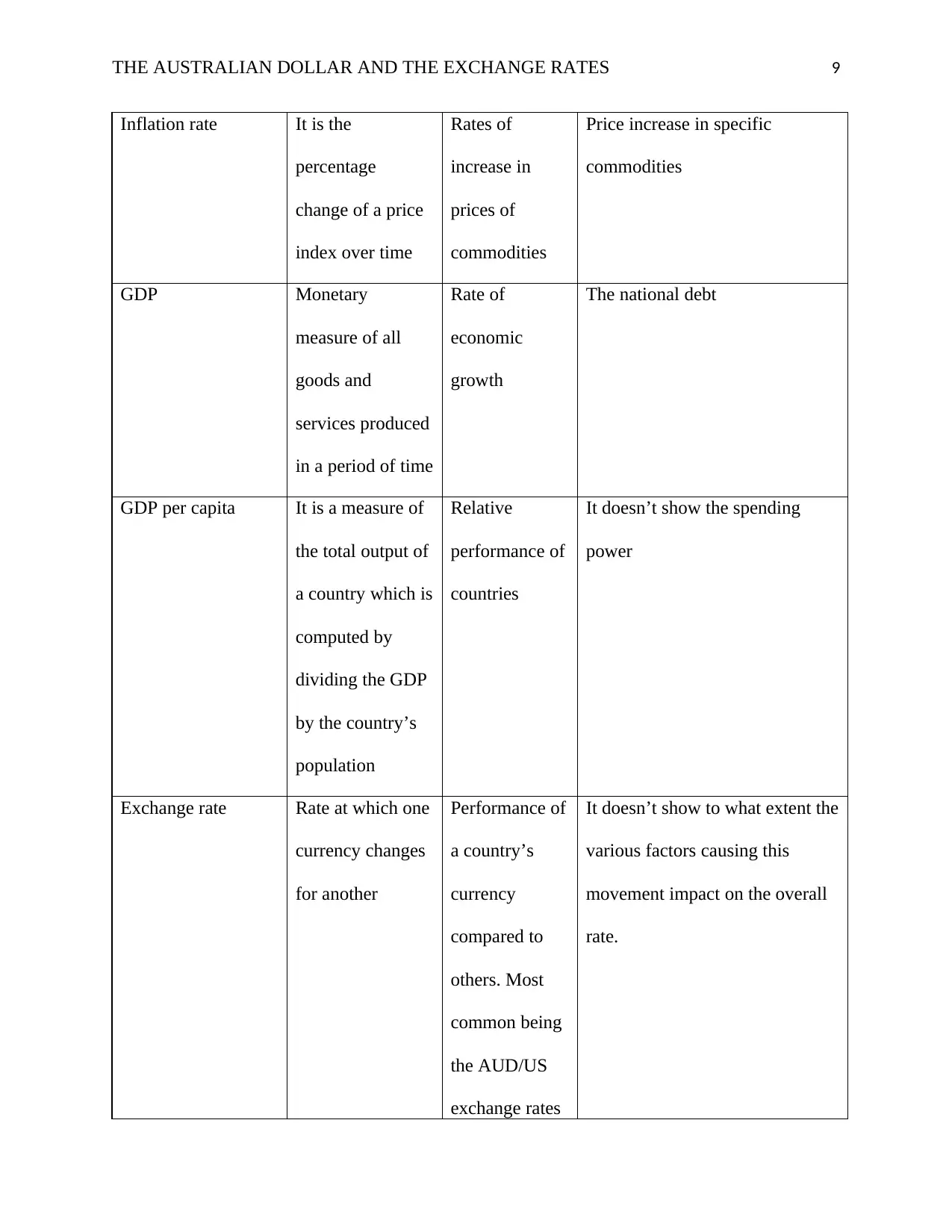

Inflation rate It is the

percentage

change of a price

index over time

Rates of

increase in

prices of

commodities

Price increase in specific

commodities

GDP Monetary

measure of all

goods and

services produced

in a period of time

Rate of

economic

growth

The national debt

GDP per capita It is a measure of

the total output of

a country which is

computed by

dividing the GDP

by the country’s

population

Relative

performance of

countries

It doesn’t show the spending

power

Exchange rate Rate at which one

currency changes

for another

Performance of

a country’s

currency

compared to

others. Most

common being

the AUD/US

exchange rates

It doesn’t show to what extent the

various factors causing this

movement impact on the overall

rate.

Inflation rate It is the

percentage

change of a price

index over time

Rates of

increase in

prices of

commodities

Price increase in specific

commodities

GDP Monetary

measure of all

goods and

services produced

in a period of time

Rate of

economic

growth

The national debt

GDP per capita It is a measure of

the total output of

a country which is

computed by

dividing the GDP

by the country’s

population

Relative

performance of

countries

It doesn’t show the spending

power

Exchange rate Rate at which one

currency changes

for another

Performance of

a country’s

currency

compared to

others. Most

common being

the AUD/US

exchange rates

It doesn’t show to what extent the

various factors causing this

movement impact on the overall

rate.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 10

in Australia

Unemployment rate It is a measure of

the prevalence of

unemployment

Number of the

idle workforce

Underemployment

(Blinder, 2015).

Question 6a

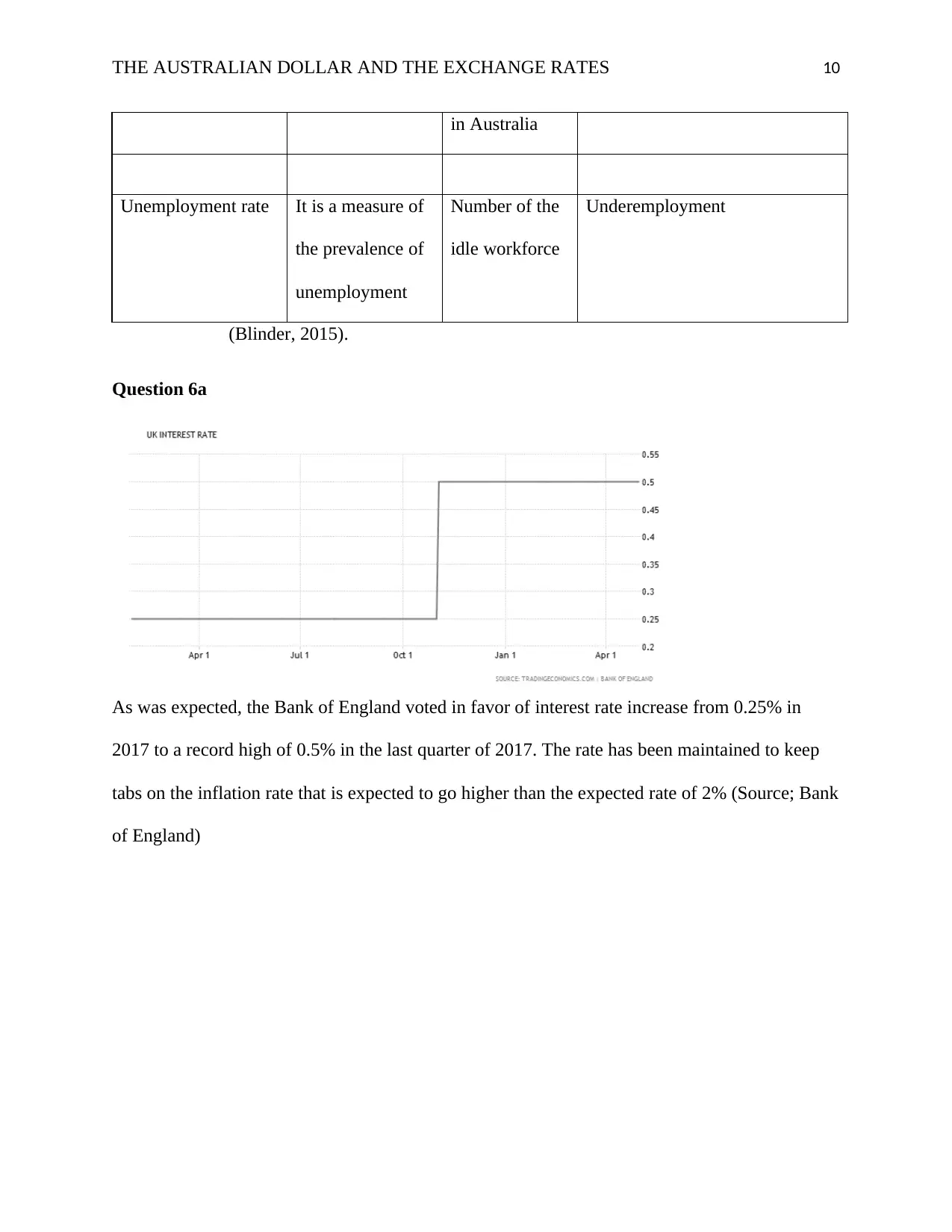

As was expected, the Bank of England voted in favor of interest rate increase from 0.25% in

2017 to a record high of 0.5% in the last quarter of 2017. The rate has been maintained to keep

tabs on the inflation rate that is expected to go higher than the expected rate of 2% (Source; Bank

of England)

in Australia

Unemployment rate It is a measure of

the prevalence of

unemployment

Number of the

idle workforce

Underemployment

(Blinder, 2015).

Question 6a

As was expected, the Bank of England voted in favor of interest rate increase from 0.25% in

2017 to a record high of 0.5% in the last quarter of 2017. The rate has been maintained to keep

tabs on the inflation rate that is expected to go higher than the expected rate of 2% (Source; Bank

of England)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 11

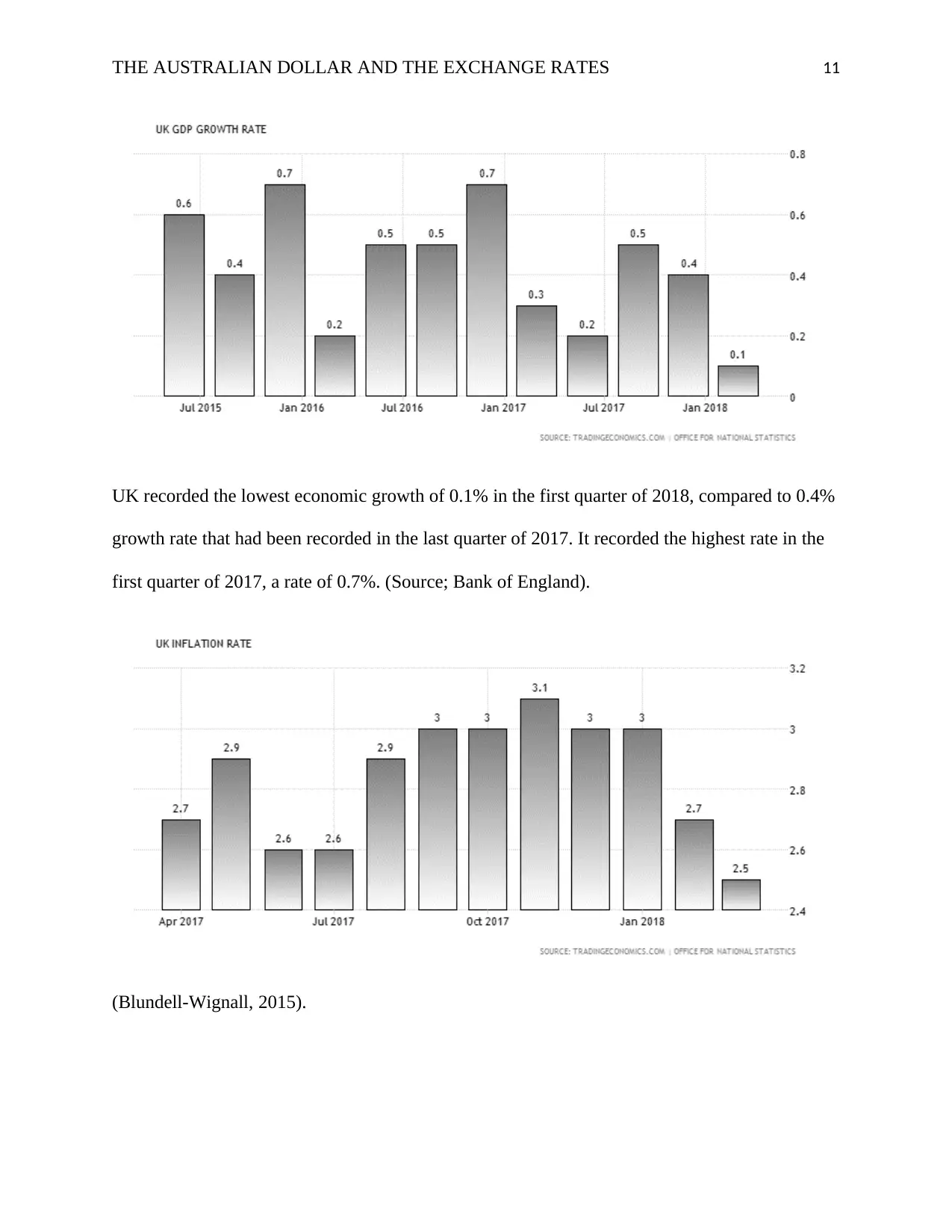

UK recorded the lowest economic growth of 0.1% in the first quarter of 2018, compared to 0.4%

growth rate that had been recorded in the last quarter of 2017. It recorded the highest rate in the

first quarter of 2017, a rate of 0.7%. (Source; Bank of England).

(Blundell-Wignall, 2015).

UK recorded the lowest economic growth of 0.1% in the first quarter of 2018, compared to 0.4%

growth rate that had been recorded in the last quarter of 2017. It recorded the highest rate in the

first quarter of 2017, a rate of 0.7%. (Source; Bank of England).

(Blundell-Wignall, 2015).

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 12

The UK’s inflation rate had been rising steadily from July 2017 when an inflation rate of 2.6%

was recorded, to November 2017 where an inflation rate of 3.1 was recorded. From there, there

has been a steady decline to 2.5% in March. (Source; Office for national statistics).

Question 6b

The use of graphs makes it possible to explain the relationships between the variables under

study. It enables us to study the trends in the movements of the variable overtime and gives

visual illustrations of the relationships of variables under study. Graphs are also easy to read and

interpret.

Question 6c

Inflation rate- this is important because the inflation rate determines the aggregate demand in the

economy. Inflation rate in the UK has been falling steadily and as at April 2017, it stood at

2.5%. this means that the economy is doing well and that the prices of goods are stable. For

Australian businesses, this means that exportation will yield high profits because the sterling

pound is higher than the AUD.

Exchange rate-this is important because it will determine the profitability of the exported goods.

If the AUD is weaker than the sterling pound, it is the best time to export goods to the UK

because it will yield more profit when the currency is exchanged back in Australia. On the other

The UK’s inflation rate had been rising steadily from July 2017 when an inflation rate of 2.6%

was recorded, to November 2017 where an inflation rate of 3.1 was recorded. From there, there

has been a steady decline to 2.5% in March. (Source; Office for national statistics).

Question 6b

The use of graphs makes it possible to explain the relationships between the variables under

study. It enables us to study the trends in the movements of the variable overtime and gives

visual illustrations of the relationships of variables under study. Graphs are also easy to read and

interpret.

Question 6c

Inflation rate- this is important because the inflation rate determines the aggregate demand in the

economy. Inflation rate in the UK has been falling steadily and as at April 2017, it stood at

2.5%. this means that the economy is doing well and that the prices of goods are stable. For

Australian businesses, this means that exportation will yield high profits because the sterling

pound is higher than the AUD.

Exchange rate-this is important because it will determine the profitability of the exported goods.

If the AUD is weaker than the sterling pound, it is the best time to export goods to the UK

because it will yield more profit when the currency is exchanged back in Australia. On the other

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 13

hand, when AUD becomes stronger than the sterling pound, it will not be profitable to do

business in the UK because it will lower profitability of the exports. (Kedia, 2016).

References

Blanchard, O. O. (2017). Policy implications. IMF economic review, 2(22), 563-586.

hand, when AUD becomes stronger than the sterling pound, it will not be profitable to do

business in the UK because it will lower profitability of the exports. (Kedia, 2016).

References

Blanchard, O. O. (2017). Policy implications. IMF economic review, 2(22), 563-586.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 14

Blinder, A. S. (2015). Does fiscal policy matter? New York: Macmillan.

Blundell-Wignall, A. (2015). Major influences on the Australian dollar exchange rate. The

exchange rates,international trade, balance of payments and the reserve bank of Australia, 2(7),

30-79.

Dash, M. (2013). Exchange rate dynamics and forex hedging strategies.

Fleisher, B. M. (2014). Effects of unemployment. New York: Mc Graw Hill.

John, S. R. (2014). The measurement of unemployment. Econometrica, 4(15), 140-180.

Kedia, B. L. (2016). Factors inhibiting export perfomance of firms. Management international

review, 7(34), 30-56.

Nayak, C. R. (2016). Goods and services tax. Boston.

Blinder, A. S. (2015). Does fiscal policy matter? New York: Macmillan.

Blundell-Wignall, A. (2015). Major influences on the Australian dollar exchange rate. The

exchange rates,international trade, balance of payments and the reserve bank of Australia, 2(7),

30-79.

Dash, M. (2013). Exchange rate dynamics and forex hedging strategies.

Fleisher, B. M. (2014). Effects of unemployment. New York: Mc Graw Hill.

John, S. R. (2014). The measurement of unemployment. Econometrica, 4(15), 140-180.

Kedia, B. L. (2016). Factors inhibiting export perfomance of firms. Management international

review, 7(34), 30-56.

Nayak, C. R. (2016). Goods and services tax. Boston.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 15

Bulletin – December Quarter 2017 Foreign Currency Exposure and Hedging in Australia

Laura Berger-Thomson and Blair Chapman[*]

Download 1.38MB

Abstract

The latest Survey of Foreign Currency Exposure confirms that Australian entities' financial

positions are well protected against a depreciation of the Australian dollar. Consistent with

previous surveys, the net foreign currency exposures of the banking sector are fully hedged. This

means that the sector's overall foreign currency liability position would not in itself be a source

of vulnerability in the event of a sudden depreciation of the Australian dollar.

Introduction

Bulletin – December Quarter 2017 Foreign Currency Exposure and Hedging in Australia

Laura Berger-Thomson and Blair Chapman[*]

Download 1.38MB

Abstract

The latest Survey of Foreign Currency Exposure confirms that Australian entities' financial

positions are well protected against a depreciation of the Australian dollar. Consistent with

previous surveys, the net foreign currency exposures of the banking sector are fully hedged. This

means that the sector's overall foreign currency liability position would not in itself be a source

of vulnerability in the event of a sudden depreciation of the Australian dollar.

Introduction

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 16

Since the float of the Australian dollar more than 30 years ago, Australia's flexible exchange rate

has contributed to macroeconomic stability by cushioning the economy from external shocks and

allowing monetary policy to more effectively smooth the business cycle.[1] The benefits of a

flexible exchange rate, however, depend on how exposed individual entities are to currency

movements. If individual entities hold large foreign currency liabilities or have trade payment

obligations denominated in foreign currency, a sharp depreciation of the exchange rate could

adversely affect their balance sheets or cash flows. In turn, this could have implications for

financial stability and macroeconomic performance. It is therefore important to understand the

size and distribution of foreign currency exposures and the extent to which firms protect

themselves against the exchange rate risk arising from these exposures.

Given the importance of hedging behaviour for reducing the vulnerability of particular sectors in

the Australian economy to exchange rate movements, the Reserve Bank initiated, and has

provided funding for, the Australian Bureau of Statistics (ABS) to regularly survey firms' foreign

currency exposures and the extent to which they are hedged. The first Survey of Foreign

Currency Exposure (SFCE) was conducted in 2001 and subsequent surveys have been conducted

every four years.[2]

Broadly speaking, there are two ways in which firms can hedge, both of which are captured by

the survey. First, firms can use derivatives – financial instruments that insure against movements

in the exchange rate. Alternatively, firms can have ‘natural’ hedges. Natural hedges occur when

foreign currency payment obligations or receipts are offset by other payment obligations or

receipts. An example of a natural hedge would be a bank using US dollar deposits to purchase

US Treasury securities. The 2017 SFCE asked firms about their natural hedges for the first time,

allowing for a more complete assessment of hedging behaviour. The 2017 SFCE results also

Since the float of the Australian dollar more than 30 years ago, Australia's flexible exchange rate

has contributed to macroeconomic stability by cushioning the economy from external shocks and

allowing monetary policy to more effectively smooth the business cycle.[1] The benefits of a

flexible exchange rate, however, depend on how exposed individual entities are to currency

movements. If individual entities hold large foreign currency liabilities or have trade payment

obligations denominated in foreign currency, a sharp depreciation of the exchange rate could

adversely affect their balance sheets or cash flows. In turn, this could have implications for

financial stability and macroeconomic performance. It is therefore important to understand the

size and distribution of foreign currency exposures and the extent to which firms protect

themselves against the exchange rate risk arising from these exposures.

Given the importance of hedging behaviour for reducing the vulnerability of particular sectors in

the Australian economy to exchange rate movements, the Reserve Bank initiated, and has

provided funding for, the Australian Bureau of Statistics (ABS) to regularly survey firms' foreign

currency exposures and the extent to which they are hedged. The first Survey of Foreign

Currency Exposure (SFCE) was conducted in 2001 and subsequent surveys have been conducted

every four years.[2]

Broadly speaking, there are two ways in which firms can hedge, both of which are captured by

the survey. First, firms can use derivatives – financial instruments that insure against movements

in the exchange rate. Alternatively, firms can have ‘natural’ hedges. Natural hedges occur when

foreign currency payment obligations or receipts are offset by other payment obligations or

receipts. An example of a natural hedge would be a bank using US dollar deposits to purchase

US Treasury securities. The 2017 SFCE asked firms about their natural hedges for the first time,

allowing for a more complete assessment of hedging behaviour. The 2017 SFCE results also

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 17

include more information on the hedging of expected trade payments and receipts than the results

of the previous survey.

Australia's Net Foreign Currency Position

Australia has historically had a net liability position with the rest of the world, which is the result

of domestic investment exceeding domestic saving over a long period.[3] This position has

averaged between 55 and 60 per cent of GDP for the past decade or so. However, Australia's

foreign liabilities are largely denominated in Australian dollars, but Australia's foreign assets are

largely denominated in foreign currency. As a result, Australia has consistently had a net foreign

currency asset position with the rest of the world. This means that a significant depreciation of

the Australian dollar increases the Australian dollar value of foreign currency assets relative to

foreign currency liabilities. This is true even before hedging of exchange rate risk is taken into

account.

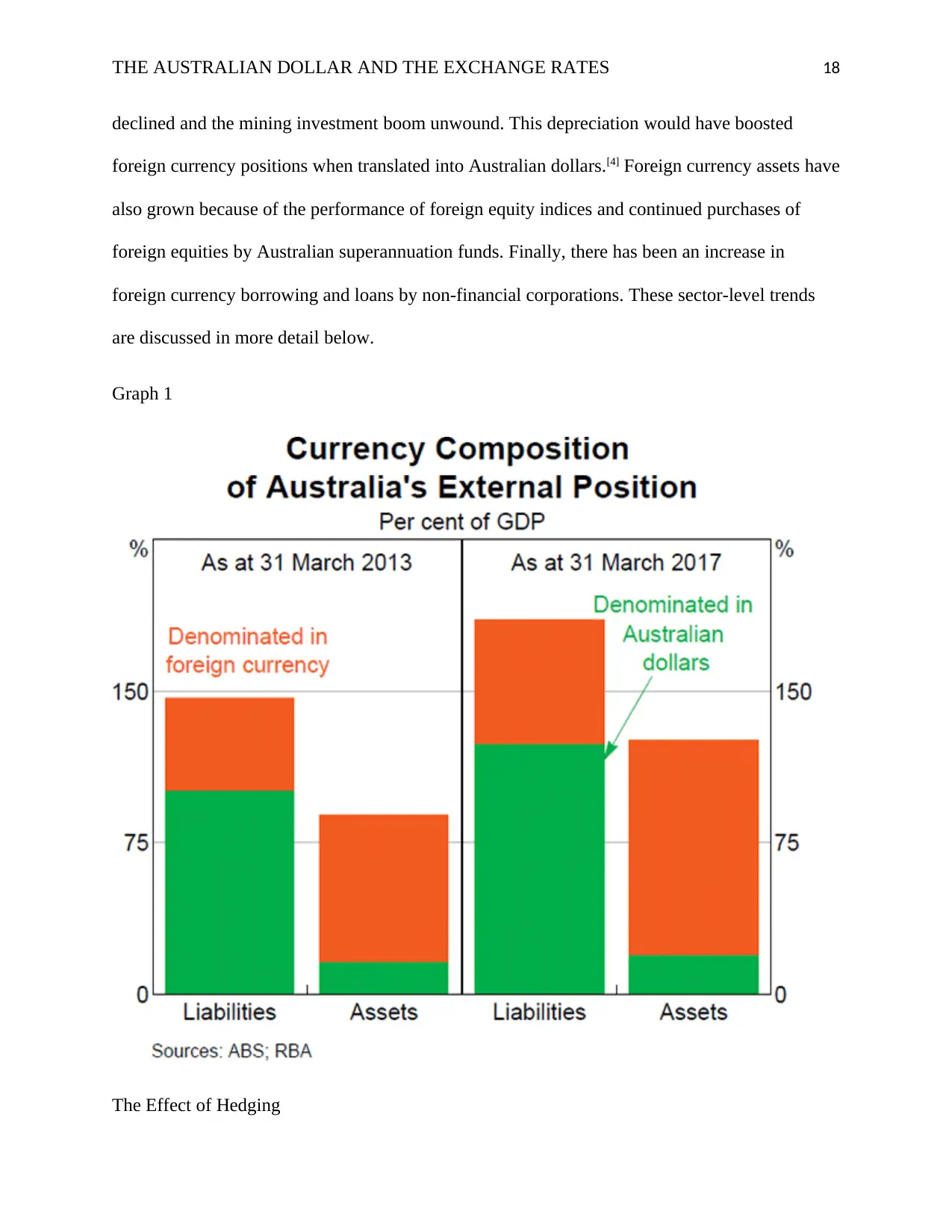

In 2017, Australia's net foreign currency asset position amounted to 45 per cent of GDP (ABS

2017b). Around two-thirds of Australia's foreign liabilities were denominated in Australian

dollars, compared with around 15 per cent of Australia's foreign assets (Graph 1). Since 2013,

foreign currency assets and liabilities have both increased as a share of GDP. Since the dollar

increase in assets has been greater than that in liabilities, there has been an increase in Australia's

net foreign currency asset position of around 15 percentage points of GDP.

Foreign currency assets and liabilities have risen by more than Australian dollar-denominated

foreign assets and liabilities since 2013. That is, the shares of both assets and liabilities that are

in foreign currency have increased. Several factors have contributed to this change. The

Australian dollar has depreciated by around one-quarter since 2013, as the terms of trade

include more information on the hedging of expected trade payments and receipts than the results

of the previous survey.

Australia's Net Foreign Currency Position

Australia has historically had a net liability position with the rest of the world, which is the result

of domestic investment exceeding domestic saving over a long period.[3] This position has

averaged between 55 and 60 per cent of GDP for the past decade or so. However, Australia's

foreign liabilities are largely denominated in Australian dollars, but Australia's foreign assets are

largely denominated in foreign currency. As a result, Australia has consistently had a net foreign

currency asset position with the rest of the world. This means that a significant depreciation of

the Australian dollar increases the Australian dollar value of foreign currency assets relative to

foreign currency liabilities. This is true even before hedging of exchange rate risk is taken into

account.

In 2017, Australia's net foreign currency asset position amounted to 45 per cent of GDP (ABS

2017b). Around two-thirds of Australia's foreign liabilities were denominated in Australian

dollars, compared with around 15 per cent of Australia's foreign assets (Graph 1). Since 2013,

foreign currency assets and liabilities have both increased as a share of GDP. Since the dollar

increase in assets has been greater than that in liabilities, there has been an increase in Australia's

net foreign currency asset position of around 15 percentage points of GDP.

Foreign currency assets and liabilities have risen by more than Australian dollar-denominated

foreign assets and liabilities since 2013. That is, the shares of both assets and liabilities that are

in foreign currency have increased. Several factors have contributed to this change. The

Australian dollar has depreciated by around one-quarter since 2013, as the terms of trade

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 18

declined and the mining investment boom unwound. This depreciation would have boosted

foreign currency positions when translated into Australian dollars.[4] Foreign currency assets have

also grown because of the performance of foreign equity indices and continued purchases of

foreign equities by Australian superannuation funds. Finally, there has been an increase in

foreign currency borrowing and loans by non-financial corporations. These sector-level trends

are discussed in more detail below.

Graph 1

The Effect of Hedging

declined and the mining investment boom unwound. This depreciation would have boosted

foreign currency positions when translated into Australian dollars.[4] Foreign currency assets have

also grown because of the performance of foreign equity indices and continued purchases of

foreign equities by Australian superannuation funds. Finally, there has been an increase in

foreign currency borrowing and loans by non-financial corporations. These sector-level trends

are discussed in more detail below.

Graph 1

The Effect of Hedging

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 19

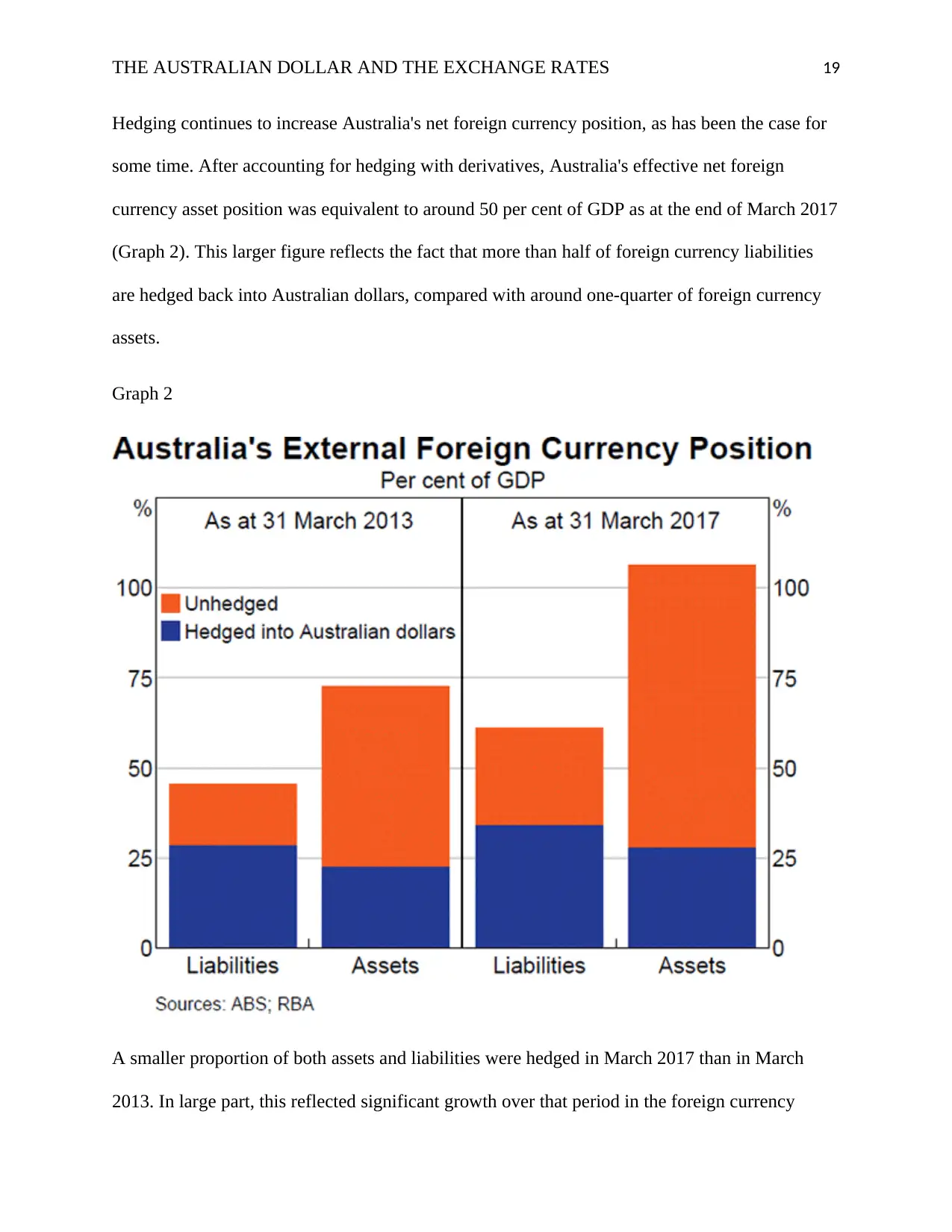

Hedging continues to increase Australia's net foreign currency position, as has been the case for

some time. After accounting for hedging with derivatives, Australia's effective net foreign

currency asset position was equivalent to around 50 per cent of GDP as at the end of March 2017

(Graph 2). This larger figure reflects the fact that more than half of foreign currency liabilities

are hedged back into Australian dollars, compared with around one-quarter of foreign currency

assets.

Graph 2

A smaller proportion of both assets and liabilities were hedged in March 2017 than in March

2013. In large part, this reflected significant growth over that period in the foreign currency

Hedging continues to increase Australia's net foreign currency position, as has been the case for

some time. After accounting for hedging with derivatives, Australia's effective net foreign

currency asset position was equivalent to around 50 per cent of GDP as at the end of March 2017

(Graph 2). This larger figure reflects the fact that more than half of foreign currency liabilities

are hedged back into Australian dollars, compared with around one-quarter of foreign currency

assets.

Graph 2

A smaller proportion of both assets and liabilities were hedged in March 2017 than in March

2013. In large part, this reflected significant growth over that period in the foreign currency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 20

assets and liabilities of non-financial corporations, which tend to use derivatives for hedging

much less than firms in other sectors. Assets of non-financial corporations accounted for 31 per

cent of foreign currency assets in 2017, up from 28 per cent in 2013, while the share of foreign

currency liabilities accounted for by the sector increased from 26 per cent to 36 per cent.

Hedging of liabilities also declined a little within most sectors, possibly reflecting some change

in hedging behaviour.

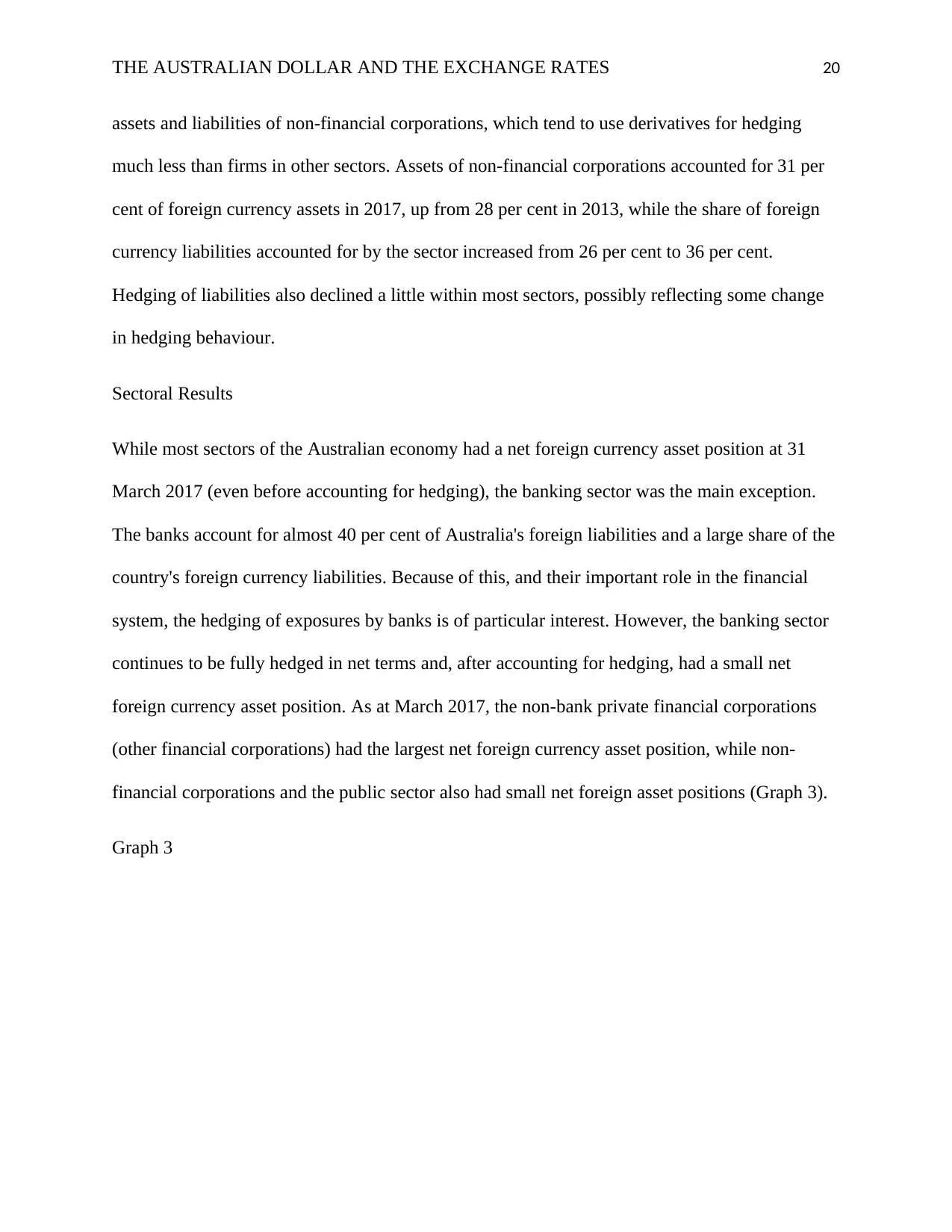

Sectoral Results

While most sectors of the Australian economy had a net foreign currency asset position at 31

March 2017 (even before accounting for hedging), the banking sector was the main exception.

The banks account for almost 40 per cent of Australia's foreign liabilities and a large share of the

country's foreign currency liabilities. Because of this, and their important role in the financial

system, the hedging of exposures by banks is of particular interest. However, the banking sector

continues to be fully hedged in net terms and, after accounting for hedging, had a small net

foreign currency asset position. As at March 2017, the non-bank private financial corporations

(other financial corporations) had the largest net foreign currency asset position, while non-

financial corporations and the public sector also had small net foreign asset positions (Graph 3).

Graph 3

assets and liabilities of non-financial corporations, which tend to use derivatives for hedging

much less than firms in other sectors. Assets of non-financial corporations accounted for 31 per

cent of foreign currency assets in 2017, up from 28 per cent in 2013, while the share of foreign

currency liabilities accounted for by the sector increased from 26 per cent to 36 per cent.

Hedging of liabilities also declined a little within most sectors, possibly reflecting some change

in hedging behaviour.

Sectoral Results

While most sectors of the Australian economy had a net foreign currency asset position at 31

March 2017 (even before accounting for hedging), the banking sector was the main exception.

The banks account for almost 40 per cent of Australia's foreign liabilities and a large share of the

country's foreign currency liabilities. Because of this, and their important role in the financial

system, the hedging of exposures by banks is of particular interest. However, the banking sector

continues to be fully hedged in net terms and, after accounting for hedging, had a small net

foreign currency asset position. As at March 2017, the non-bank private financial corporations

(other financial corporations) had the largest net foreign currency asset position, while non-

financial corporations and the public sector also had small net foreign asset positions (Graph 3).

Graph 3

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 21

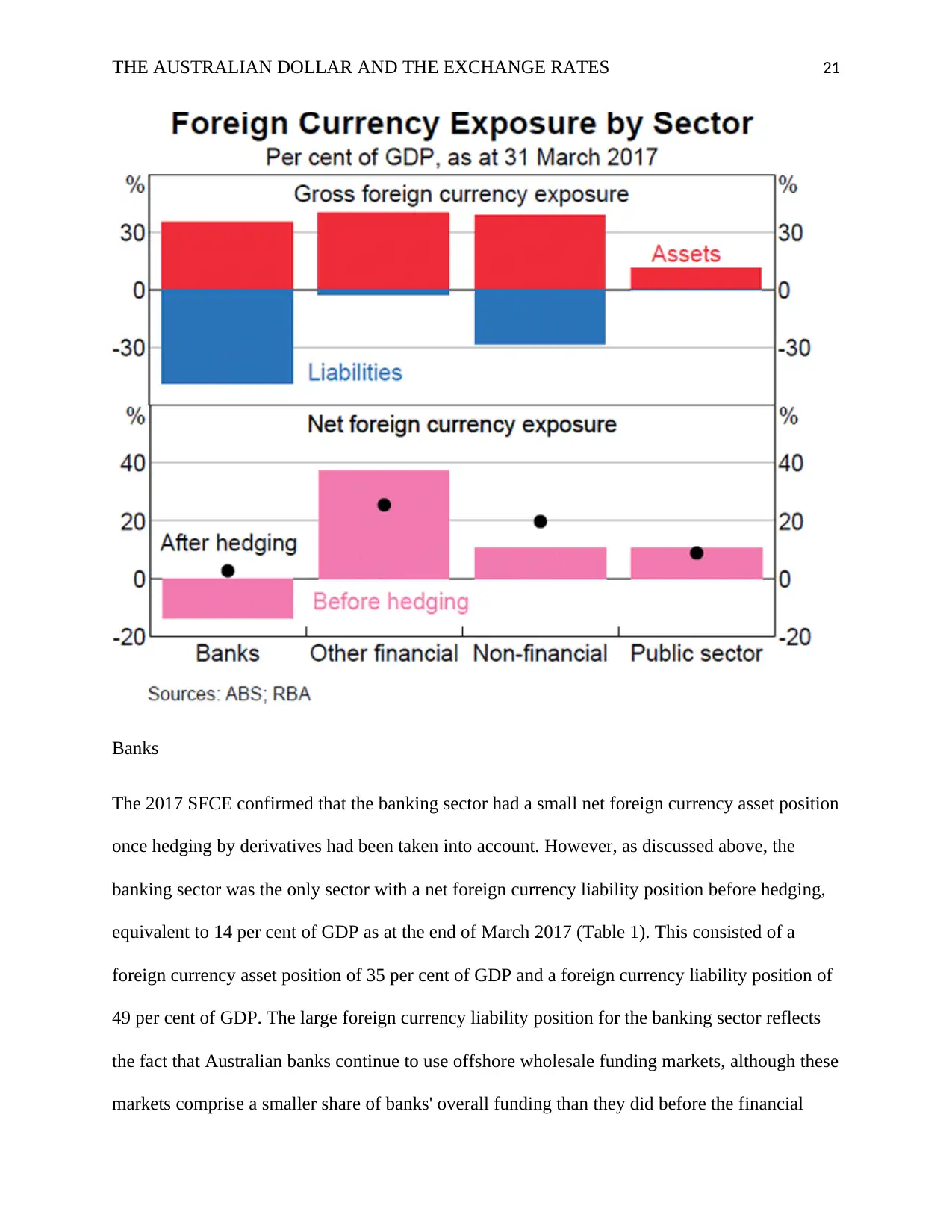

Banks

The 2017 SFCE confirmed that the banking sector had a small net foreign currency asset position

once hedging by derivatives had been taken into account. However, as discussed above, the

banking sector was the only sector with a net foreign currency liability position before hedging,

equivalent to 14 per cent of GDP as at the end of March 2017 (Table 1). This consisted of a

foreign currency asset position of 35 per cent of GDP and a foreign currency liability position of

49 per cent of GDP. The large foreign currency liability position for the banking sector reflects

the fact that Australian banks continue to use offshore wholesale funding markets, although these

markets comprise a smaller share of banks' overall funding than they did before the financial

Banks

The 2017 SFCE confirmed that the banking sector had a small net foreign currency asset position

once hedging by derivatives had been taken into account. However, as discussed above, the

banking sector was the only sector with a net foreign currency liability position before hedging,

equivalent to 14 per cent of GDP as at the end of March 2017 (Table 1). This consisted of a

foreign currency asset position of 35 per cent of GDP and a foreign currency liability position of

49 per cent of GDP. The large foreign currency liability position for the banking sector reflects

the fact that Australian banks continue to use offshore wholesale funding markets, although these

markets comprise a smaller share of banks' overall funding than they did before the financial

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 22

crisis.[5] In 2017, these markets accounted for a little under 20 per cent of total bank funding,

almost all of which was denominated in foreign currency. The share of banking sector funding

sourced from offshore has been roughly constant since March 2013; however, the value of

foreign currency exposures has increased, reflecting the growth in the banking system over this

time. As foreign currency liabilities and assets have increased by similar dollar amounts, the

sector's net foreign currency exposure has remained roughly constant as a share of GDP.

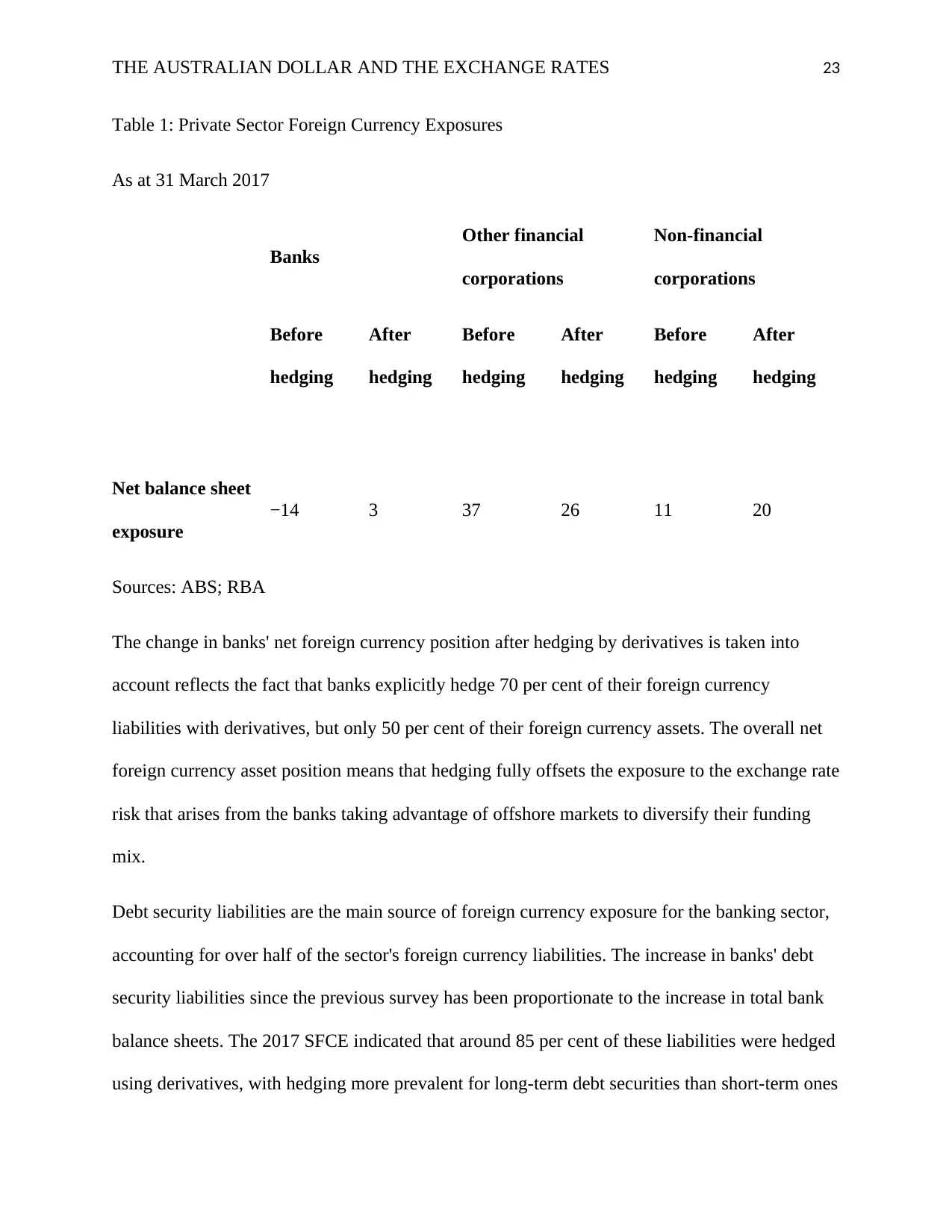

Table 1: Private Sector Foreign Currency Exposures

As at 31 March 2017

Banks

Other financial

corporations

Non-financial

corporations

Before

hedging

After

hedging

Before

hedging

After

hedging

Before

hedging

After

hedging

A$ billion

Assets 603 305 687 463 674 664

Liabilities 841 259 40 23 490 323

Net balance sheet

exposure

−238 45 647 441 184 341

Per cent of GDP

Assets 35 18 40 27 39 38

Liabilities 49 15 2 1 28 19

crisis.[5] In 2017, these markets accounted for a little under 20 per cent of total bank funding,

almost all of which was denominated in foreign currency. The share of banking sector funding

sourced from offshore has been roughly constant since March 2013; however, the value of

foreign currency exposures has increased, reflecting the growth in the banking system over this

time. As foreign currency liabilities and assets have increased by similar dollar amounts, the

sector's net foreign currency exposure has remained roughly constant as a share of GDP.

Table 1: Private Sector Foreign Currency Exposures

As at 31 March 2017

Banks

Other financial

corporations

Non-financial

corporations

Before

hedging

After

hedging

Before

hedging

After

hedging

Before

hedging

After

hedging

A$ billion

Assets 603 305 687 463 674 664

Liabilities 841 259 40 23 490 323

Net balance sheet

exposure

−238 45 647 441 184 341

Per cent of GDP

Assets 35 18 40 27 39 38

Liabilities 49 15 2 1 28 19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 23

Table 1: Private Sector Foreign Currency Exposures

As at 31 March 2017

Banks

Other financial

corporations

Non-financial

corporations

Before

hedging

After

hedging

Before

hedging

After

hedging

Before

hedging

After

hedging

Net balance sheet

exposure

−14 3 37 26 11 20

Sources: ABS; RBA

The change in banks' net foreign currency position after hedging by derivatives is taken into

account reflects the fact that banks explicitly hedge 70 per cent of their foreign currency

liabilities with derivatives, but only 50 per cent of their foreign currency assets. The overall net

foreign currency asset position means that hedging fully offsets the exposure to the exchange rate

risk that arises from the banks taking advantage of offshore markets to diversify their funding

mix.

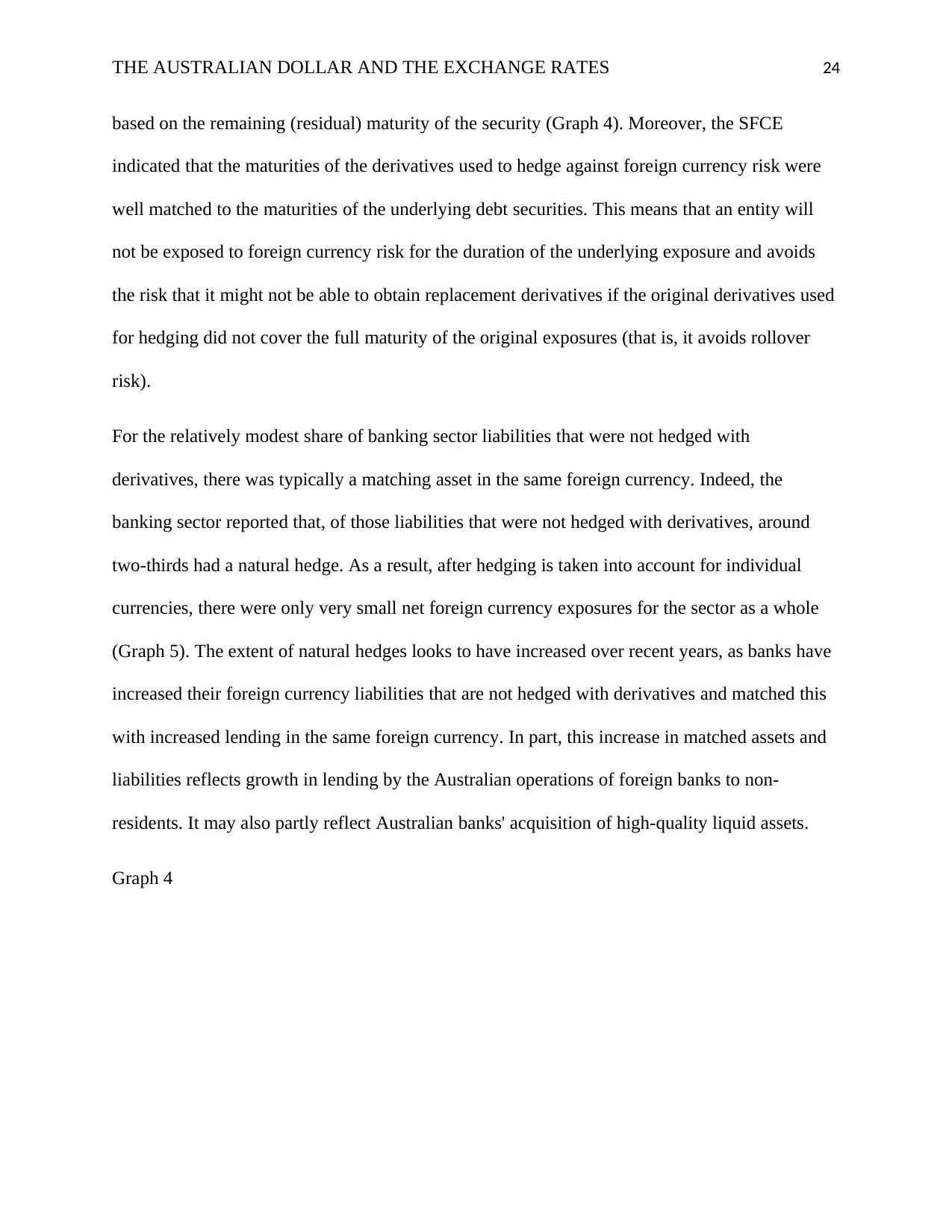

Debt security liabilities are the main source of foreign currency exposure for the banking sector,

accounting for over half of the sector's foreign currency liabilities. The increase in banks' debt

security liabilities since the previous survey has been proportionate to the increase in total bank

balance sheets. The 2017 SFCE indicated that around 85 per cent of these liabilities were hedged

using derivatives, with hedging more prevalent for long-term debt securities than short-term ones

Table 1: Private Sector Foreign Currency Exposures

As at 31 March 2017

Banks

Other financial

corporations

Non-financial

corporations

Before

hedging

After

hedging

Before

hedging

After

hedging

Before

hedging

After

hedging

Net balance sheet

exposure

−14 3 37 26 11 20

Sources: ABS; RBA

The change in banks' net foreign currency position after hedging by derivatives is taken into

account reflects the fact that banks explicitly hedge 70 per cent of their foreign currency

liabilities with derivatives, but only 50 per cent of their foreign currency assets. The overall net

foreign currency asset position means that hedging fully offsets the exposure to the exchange rate

risk that arises from the banks taking advantage of offshore markets to diversify their funding

mix.

Debt security liabilities are the main source of foreign currency exposure for the banking sector,

accounting for over half of the sector's foreign currency liabilities. The increase in banks' debt

security liabilities since the previous survey has been proportionate to the increase in total bank

balance sheets. The 2017 SFCE indicated that around 85 per cent of these liabilities were hedged

using derivatives, with hedging more prevalent for long-term debt securities than short-term ones

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 24

based on the remaining (residual) maturity of the security (Graph 4). Moreover, the SFCE

indicated that the maturities of the derivatives used to hedge against foreign currency risk were

well matched to the maturities of the underlying debt securities. This means that an entity will

not be exposed to foreign currency risk for the duration of the underlying exposure and avoids

the risk that it might not be able to obtain replacement derivatives if the original derivatives used

for hedging did not cover the full maturity of the original exposures (that is, it avoids rollover

risk).

For the relatively modest share of banking sector liabilities that were not hedged with

derivatives, there was typically a matching asset in the same foreign currency. Indeed, the

banking sector reported that, of those liabilities that were not hedged with derivatives, around

two-thirds had a natural hedge. As a result, after hedging is taken into account for individual

currencies, there were only very small net foreign currency exposures for the sector as a whole

(Graph 5). The extent of natural hedges looks to have increased over recent years, as banks have

increased their foreign currency liabilities that are not hedged with derivatives and matched this

with increased lending in the same foreign currency. In part, this increase in matched assets and

liabilities reflects growth in lending by the Australian operations of foreign banks to non-

residents. It may also partly reflect Australian banks' acquisition of high-quality liquid assets.

Graph 4

based on the remaining (residual) maturity of the security (Graph 4). Moreover, the SFCE

indicated that the maturities of the derivatives used to hedge against foreign currency risk were

well matched to the maturities of the underlying debt securities. This means that an entity will

not be exposed to foreign currency risk for the duration of the underlying exposure and avoids

the risk that it might not be able to obtain replacement derivatives if the original derivatives used

for hedging did not cover the full maturity of the original exposures (that is, it avoids rollover

risk).

For the relatively modest share of banking sector liabilities that were not hedged with

derivatives, there was typically a matching asset in the same foreign currency. Indeed, the

banking sector reported that, of those liabilities that were not hedged with derivatives, around

two-thirds had a natural hedge. As a result, after hedging is taken into account for individual

currencies, there were only very small net foreign currency exposures for the sector as a whole

(Graph 5). The extent of natural hedges looks to have increased over recent years, as banks have

increased their foreign currency liabilities that are not hedged with derivatives and matched this

with increased lending in the same foreign currency. In part, this increase in matched assets and

liabilities reflects growth in lending by the Australian operations of foreign banks to non-

residents. It may also partly reflect Australian banks' acquisition of high-quality liquid assets.

Graph 4

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 25

Graph 5

Graph 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 26

Other financial corporations

The other financial corporations sector includes non-bank financial corporations, including

superannuation funds, fund managers and insurance corporations.[6] These entities generally

invest on behalf of households and other firms with the aim of providing high risk-adjusted

returns. These firms seek to diversify their investment portfolios by holding a variety of assets

including foreign equities and assets that pay a fixed income, such as government and corporate

bonds. For example, foreign equities represented 45 per cent of superannuation funds' equity

Other financial corporations

The other financial corporations sector includes non-bank financial corporations, including

superannuation funds, fund managers and insurance corporations.[6] These entities generally

invest on behalf of households and other firms with the aim of providing high risk-adjusted

returns. These firms seek to diversify their investment portfolios by holding a variety of assets

including foreign equities and assets that pay a fixed income, such as government and corporate

bonds. For example, foreign equities represented 45 per cent of superannuation funds' equity

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 27

holdings and foreign fixed income assets represented around one-third of their fixed income

holdings as at 31 March 2017 (APRA 2017).

Since the previous survey, foreign currency assets of the other financial sector have increased

notably, while the sector's foreign currency liabilities have decreased slightly. The increase in

foreign currency assets is consistent with continued purchases of foreign equity assets,

particularly by superannuation funds, as well as the increased Australian dollar value of the

existing stock of assets arising from the depreciation of the Australian dollar since the previous

survey (Black, Chapman and Windsor 2017). Superannuation funds have also increased their

holdings of international fixed income and international infrastructure funds since the previous

survey.

At the end of March 2017, other financial corporations had a net foreign currency asset position

equivalent to 37 per cent of GDP. Foreign equity assets accounted for most of the sector's total

foreign currency assets. These financial corporations used derivatives to hedge around one-third

of their foreign currency assets. After accounting for the use of derivatives for hedging, the net

foreign currency asset position of other financial corporations decreases to be equivalent to

26 per cent of GDP. The SFCE does not split the hedging of foreign currency assets by type, but

Australian Prudential Regulation Authority data (APRA 2017) indicate that superannuation

funds hedge around 65 per cent of their international debt holdings and listed infrastructure funds

but only hedge 30 per cent of their international equity holdings.

Non-financial corporations

Non-financial corporations had a net foreign currency asset position equivalent to 11 per cent of

GDP as at the end of March 2017 (Table 1).[7] This net position consisted of a significant amount

holdings and foreign fixed income assets represented around one-third of their fixed income

holdings as at 31 March 2017 (APRA 2017).

Since the previous survey, foreign currency assets of the other financial sector have increased

notably, while the sector's foreign currency liabilities have decreased slightly. The increase in

foreign currency assets is consistent with continued purchases of foreign equity assets,

particularly by superannuation funds, as well as the increased Australian dollar value of the

existing stock of assets arising from the depreciation of the Australian dollar since the previous

survey (Black, Chapman and Windsor 2017). Superannuation funds have also increased their

holdings of international fixed income and international infrastructure funds since the previous

survey.

At the end of March 2017, other financial corporations had a net foreign currency asset position

equivalent to 37 per cent of GDP. Foreign equity assets accounted for most of the sector's total

foreign currency assets. These financial corporations used derivatives to hedge around one-third

of their foreign currency assets. After accounting for the use of derivatives for hedging, the net

foreign currency asset position of other financial corporations decreases to be equivalent to

26 per cent of GDP. The SFCE does not split the hedging of foreign currency assets by type, but

Australian Prudential Regulation Authority data (APRA 2017) indicate that superannuation

funds hedge around 65 per cent of their international debt holdings and listed infrastructure funds

but only hedge 30 per cent of their international equity holdings.

Non-financial corporations

Non-financial corporations had a net foreign currency asset position equivalent to 11 per cent of

GDP as at the end of March 2017 (Table 1).[7] This net position consisted of a significant amount

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 28

of foreign currency assets, around two-thirds of which were equity assets.[8] However, the sector

also had a significant amount of foreign currency liabilities, almost all of which were either long-

term debt securities or loans. The sector's asset and liability positions were noticeably larger in

2017 than in the previous survey. This growth partly reflects valuation effects from the

Australian dollar depreciation and, for assets, the performance of foreign equities. After

accounting for the use of derivatives to hedge, non-financial corporations had a net foreign

currency asset position of 20 per cent of GDP at the end of March 2017.

Non-financial corporations do not use derivatives for hedging as much as other sectors. The 2017

SFCE indicated that derivatives were used to hedge only around one-third of their foreign

currency liabilities and a negligible amount of the foreign currency assets. This difference is

related to the composition of the sectors' assets and liabilities. The foreign currency equity assets

of the sector include the foreign operations (subsidiaries and branches) of multinational

corporations, which are offset by foreign currency borrowing in the form of loans and debt

securities. In addition, some non-financial corporations conduct much of their trade in foreign

currency, so foreign currency borrowing is matched to trade payments. For example, a large

share of Australia's resource exports is invoiced in US dollars (ABS 2016). Mining firms

generally borrow in US dollars to match the currency of their debt payment obligations to these

trade receipts.

Changes to cash flows arising from exchange rate movements affect trade payment and receipts,

and are a potential source of vulnerability for non-financial corporates. This is important because

a large share of Australia's exports is invoiced in foreign currency. Non-financial corporations

represent almost all of Australia's expected foreign currency trade receipts and a vast majority of

Australia's expected foreign currency trade payments.[9] Hedging of these flows by derivatives is

of foreign currency assets, around two-thirds of which were equity assets.[8] However, the sector

also had a significant amount of foreign currency liabilities, almost all of which were either long-

term debt securities or loans. The sector's asset and liability positions were noticeably larger in

2017 than in the previous survey. This growth partly reflects valuation effects from the

Australian dollar depreciation and, for assets, the performance of foreign equities. After

accounting for the use of derivatives to hedge, non-financial corporations had a net foreign

currency asset position of 20 per cent of GDP at the end of March 2017.

Non-financial corporations do not use derivatives for hedging as much as other sectors. The 2017

SFCE indicated that derivatives were used to hedge only around one-third of their foreign

currency liabilities and a negligible amount of the foreign currency assets. This difference is

related to the composition of the sectors' assets and liabilities. The foreign currency equity assets

of the sector include the foreign operations (subsidiaries and branches) of multinational

corporations, which are offset by foreign currency borrowing in the form of loans and debt

securities. In addition, some non-financial corporations conduct much of their trade in foreign

currency, so foreign currency borrowing is matched to trade payments. For example, a large

share of Australia's resource exports is invoiced in US dollars (ABS 2016). Mining firms

generally borrow in US dollars to match the currency of their debt payment obligations to these

trade receipts.

Changes to cash flows arising from exchange rate movements affect trade payment and receipts,

and are a potential source of vulnerability for non-financial corporates. This is important because

a large share of Australia's exports is invoiced in foreign currency. Non-financial corporations

represent almost all of Australia's expected foreign currency trade receipts and a vast majority of

Australia's expected foreign currency trade payments.[9] Hedging of these flows by derivatives is

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 29

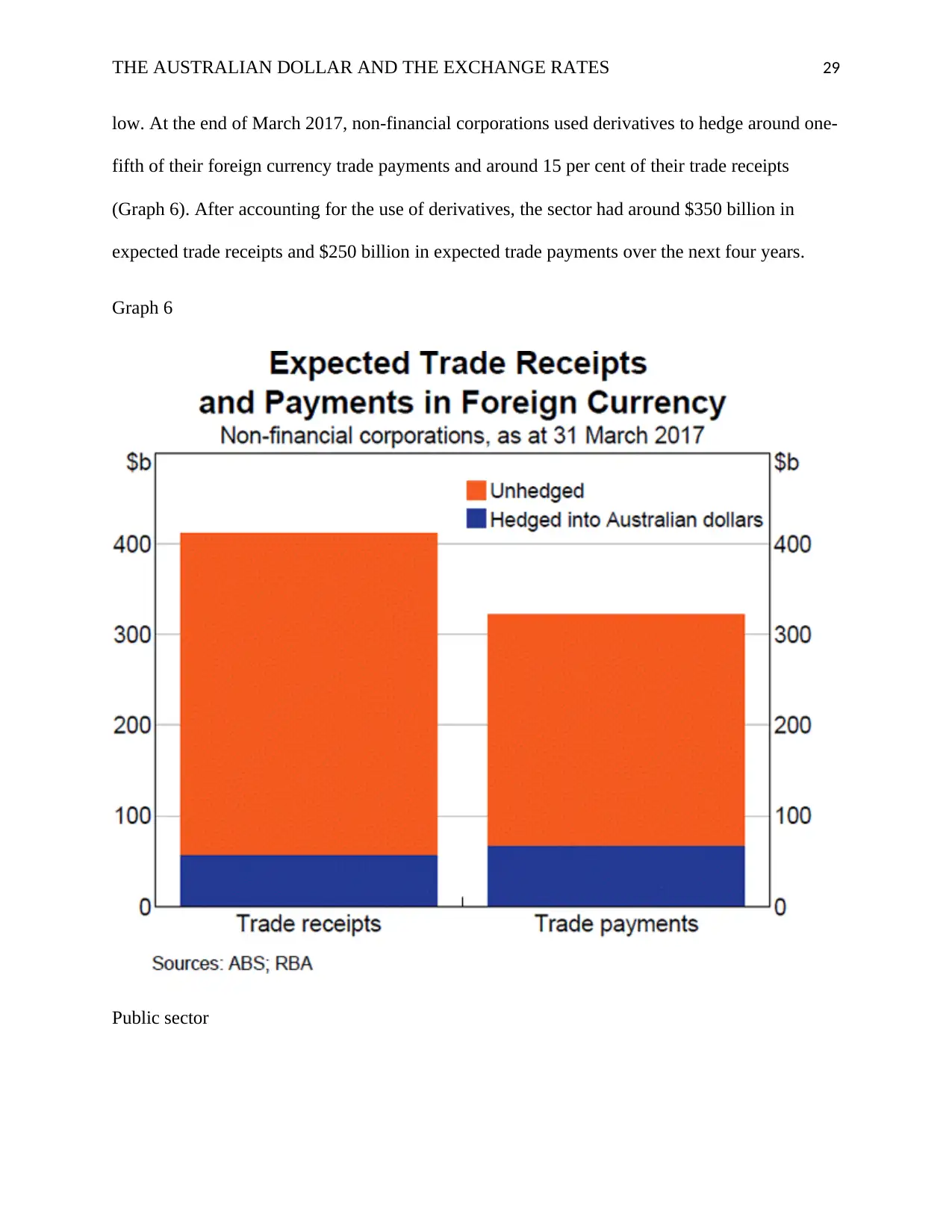

low. At the end of March 2017, non-financial corporations used derivatives to hedge around one-

fifth of their foreign currency trade payments and around 15 per cent of their trade receipts

(Graph 6). After accounting for the use of derivatives, the sector had around $350 billion in

expected trade receipts and $250 billion in expected trade payments over the next four years.

Graph 6

Public sector

low. At the end of March 2017, non-financial corporations used derivatives to hedge around one-

fifth of their foreign currency trade payments and around 15 per cent of their trade receipts

(Graph 6). After accounting for the use of derivatives, the sector had around $350 billion in

expected trade receipts and $250 billion in expected trade payments over the next four years.

Graph 6

Public sector

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 30

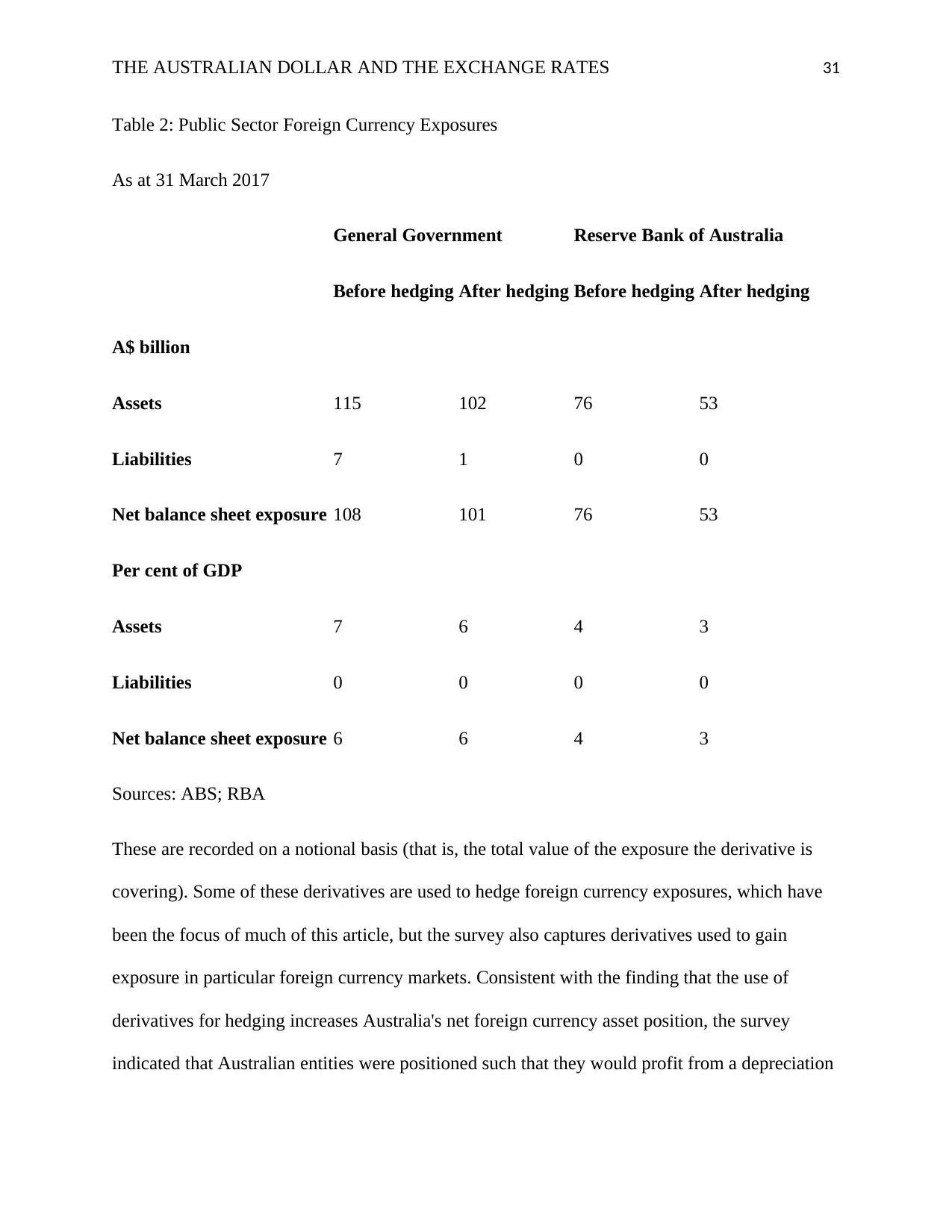

The public sector's foreign currency assets and liabilities are relatively small (Table 2). The

general government sector, which includes federal, state and local governments, had a net

foreign currency asset position of $108 billion before accounting for the use of derivatives for

hedging purposes. The net foreign currency asset position has roughly doubled in its proportion

relative to GDP since the previous survey to 6 per cent. This increase has been mainly driven by

an increase in foreign currency assets. Foreign currency equity assets account for around two-

thirds of the general government's total foreign currency assets. The Australian Government's

Future Fund continues to hold a significant proportion of the foreign currency assets of the

general government sector. The Future Fund had a net foreign currency asset position of around

$85 billion at the end of the 2017 financial year (Future Fund 2017).

The Reserve Bank had a foreign currency asset position equivalent to 4 per cent of GDP as at 31

March 2017. This position represents the net foreign reserve holdings of the Reserve Bank.

Before hedging is taken into account, these reserves reflect the use of foreign exchange swaps to

manage domestic liquidity.[10]

Derivative Holdings

As well as providing information about Australian entities' foreign currency exposures and

hedging, the SFCE also contained detailed information on derivative holdings as at the end of

March 2017.

The public sector's foreign currency assets and liabilities are relatively small (Table 2). The

general government sector, which includes federal, state and local governments, had a net

foreign currency asset position of $108 billion before accounting for the use of derivatives for

hedging purposes. The net foreign currency asset position has roughly doubled in its proportion

relative to GDP since the previous survey to 6 per cent. This increase has been mainly driven by

an increase in foreign currency assets. Foreign currency equity assets account for around two-

thirds of the general government's total foreign currency assets. The Australian Government's

Future Fund continues to hold a significant proportion of the foreign currency assets of the

general government sector. The Future Fund had a net foreign currency asset position of around

$85 billion at the end of the 2017 financial year (Future Fund 2017).

The Reserve Bank had a foreign currency asset position equivalent to 4 per cent of GDP as at 31

March 2017. This position represents the net foreign reserve holdings of the Reserve Bank.

Before hedging is taken into account, these reserves reflect the use of foreign exchange swaps to

manage domestic liquidity.[10]

Derivative Holdings

As well as providing information about Australian entities' foreign currency exposures and

hedging, the SFCE also contained detailed information on derivative holdings as at the end of

March 2017.

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 31

Table 2: Public Sector Foreign Currency Exposures

As at 31 March 2017

General Government Reserve Bank of Australia

Before hedging After hedging Before hedging After hedging

A$ billion

Assets 115 102 76 53

Liabilities 7 1 0 0

Net balance sheet exposure 108 101 76 53

Per cent of GDP

Assets 7 6 4 3

Liabilities 0 0 0 0

Net balance sheet exposure 6 6 4 3

Sources: ABS; RBA

These are recorded on a notional basis (that is, the total value of the exposure the derivative is

covering). Some of these derivatives are used to hedge foreign currency exposures, which have

been the focus of much of this article, but the survey also captures derivatives used to gain

exposure in particular foreign currency markets. Consistent with the finding that the use of

derivatives for hedging increases Australia's net foreign currency asset position, the survey

indicated that Australian entities were positioned such that they would profit from a depreciation

Table 2: Public Sector Foreign Currency Exposures

As at 31 March 2017

General Government Reserve Bank of Australia

Before hedging After hedging Before hedging After hedging

A$ billion

Assets 115 102 76 53

Liabilities 7 1 0 0

Net balance sheet exposure 108 101 76 53

Per cent of GDP

Assets 7 6 4 3

Liabilities 0 0 0 0

Net balance sheet exposure 6 6 4 3

Sources: ABS; RBA

These are recorded on a notional basis (that is, the total value of the exposure the derivative is

covering). Some of these derivatives are used to hedge foreign currency exposures, which have

been the focus of much of this article, but the survey also captures derivatives used to gain

exposure in particular foreign currency markets. Consistent with the finding that the use of

derivatives for hedging increases Australia's net foreign currency asset position, the survey

indicated that Australian entities were positioned such that they would profit from a depreciation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 32

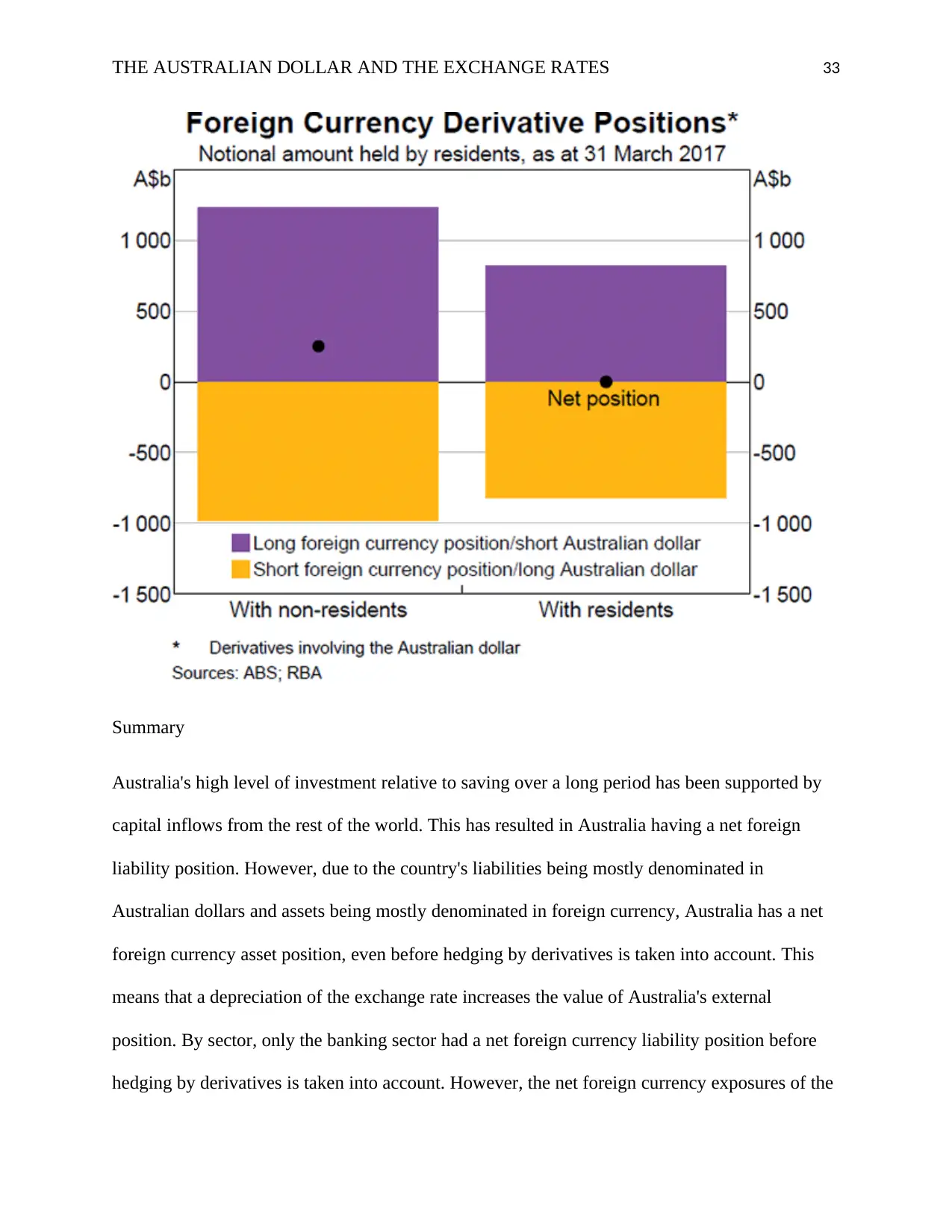

of the Australian dollar (that is, they had a net short Australian dollar position or a net long

foreign currency position against non-residents) (Graph 7).

Cross-currency swaps continue to be the main instrument used to hedge foreign currency

exposures; holdings of these instruments are concentrated in the banking sector.[11] Cross-

currency swaps, which are generally used to hedge longer-term foreign currency risk, accounted

for slightly more than two-thirds of total notional long foreign currency positions (or short

Australian dollar positions) and around half of short foreign currency derivative positions (or

long Australian dollar positions). Forwards, which are generally used to hedge shorter-term

foreign currency risk, accounted for most of the remainder of the positions. These shares were

relatively unchanged from the previous survey, in line with relative stability in the maturity of

banks' new offshore wholesale funding over this period. The shares had increased noticeably in

the four years before the previous survey (Arsov et al 2013).

Graph 7

of the Australian dollar (that is, they had a net short Australian dollar position or a net long

foreign currency position against non-residents) (Graph 7).

Cross-currency swaps continue to be the main instrument used to hedge foreign currency

exposures; holdings of these instruments are concentrated in the banking sector.[11] Cross-

currency swaps, which are generally used to hedge longer-term foreign currency risk, accounted

for slightly more than two-thirds of total notional long foreign currency positions (or short

Australian dollar positions) and around half of short foreign currency derivative positions (or

long Australian dollar positions). Forwards, which are generally used to hedge shorter-term

foreign currency risk, accounted for most of the remainder of the positions. These shares were

relatively unchanged from the previous survey, in line with relative stability in the maturity of

banks' new offshore wholesale funding over this period. The shares had increased noticeably in

the four years before the previous survey (Arsov et al 2013).

Graph 7

THE AUSTRALIAN DOLLAR AND THE EXCHANGE RATES 33

Summary

Australia's high level of investment relative to saving over a long period has been supported by

capital inflows from the rest of the world. This has resulted in Australia having a net foreign

liability position. However, due to the country's liabilities being mostly denominated in

Australian dollars and assets being mostly denominated in foreign currency, Australia has a net

foreign currency asset position, even before hedging by derivatives is taken into account. This

means that a depreciation of the exchange rate increases the value of Australia's external

position. By sector, only the banking sector had a net foreign currency liability position before

hedging by derivatives is taken into account. However, the net foreign currency exposures of the

Summary

Australia's high level of investment relative to saving over a long period has been supported by

capital inflows from the rest of the world. This has resulted in Australia having a net foreign

liability position. However, due to the country's liabilities being mostly denominated in

Australian dollars and assets being mostly denominated in foreign currency, Australia has a net

foreign currency asset position, even before hedging by derivatives is taken into account. This

means that a depreciation of the exchange rate increases the value of Australia's external

position. By sector, only the banking sector had a net foreign currency liability position before

hedging by derivatives is taken into account. However, the net foreign currency exposures of the

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.