Taxation of Individuals and Corporations in Australia Report

VerifiedAdded on 2020/10/05

|12

|2779

|145

Report

AI Summary

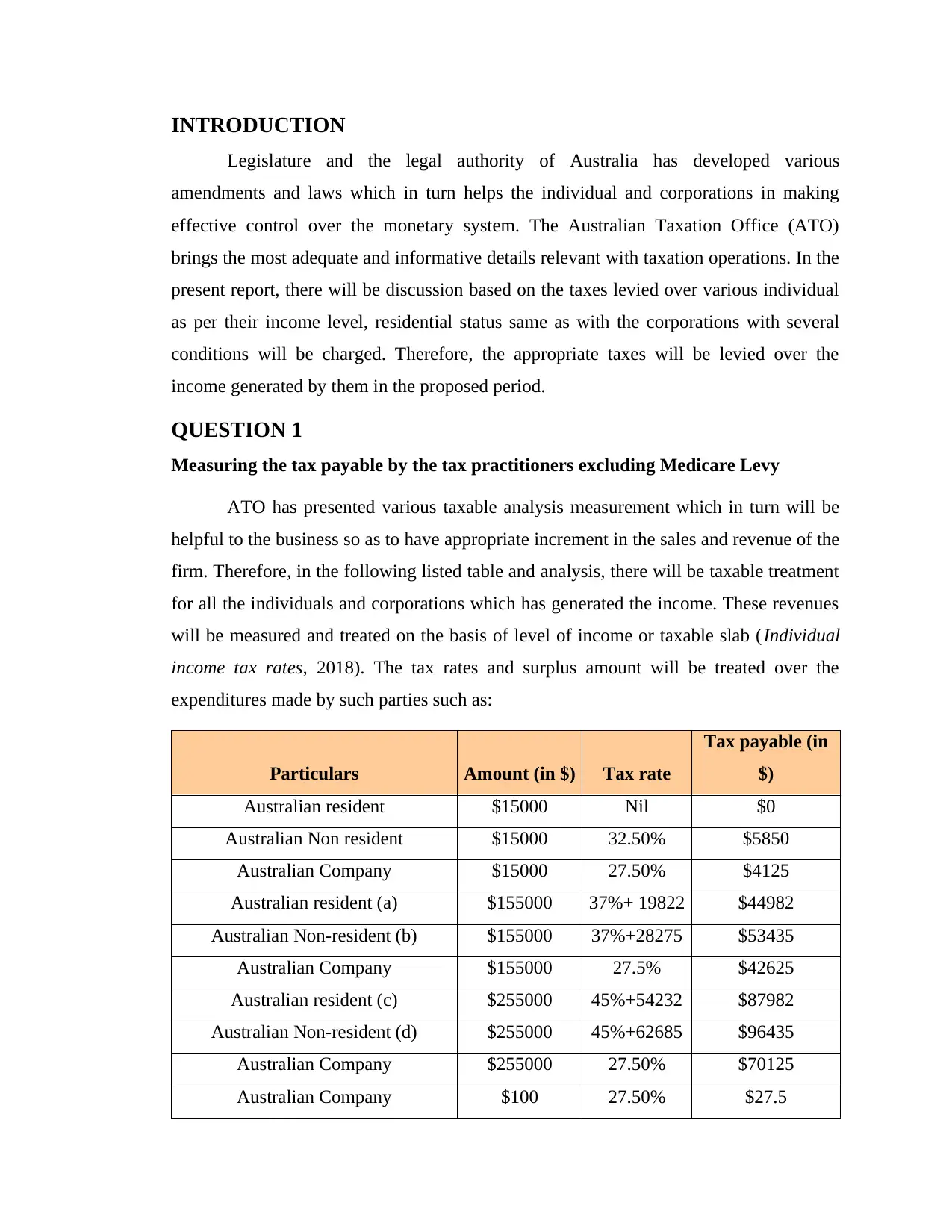

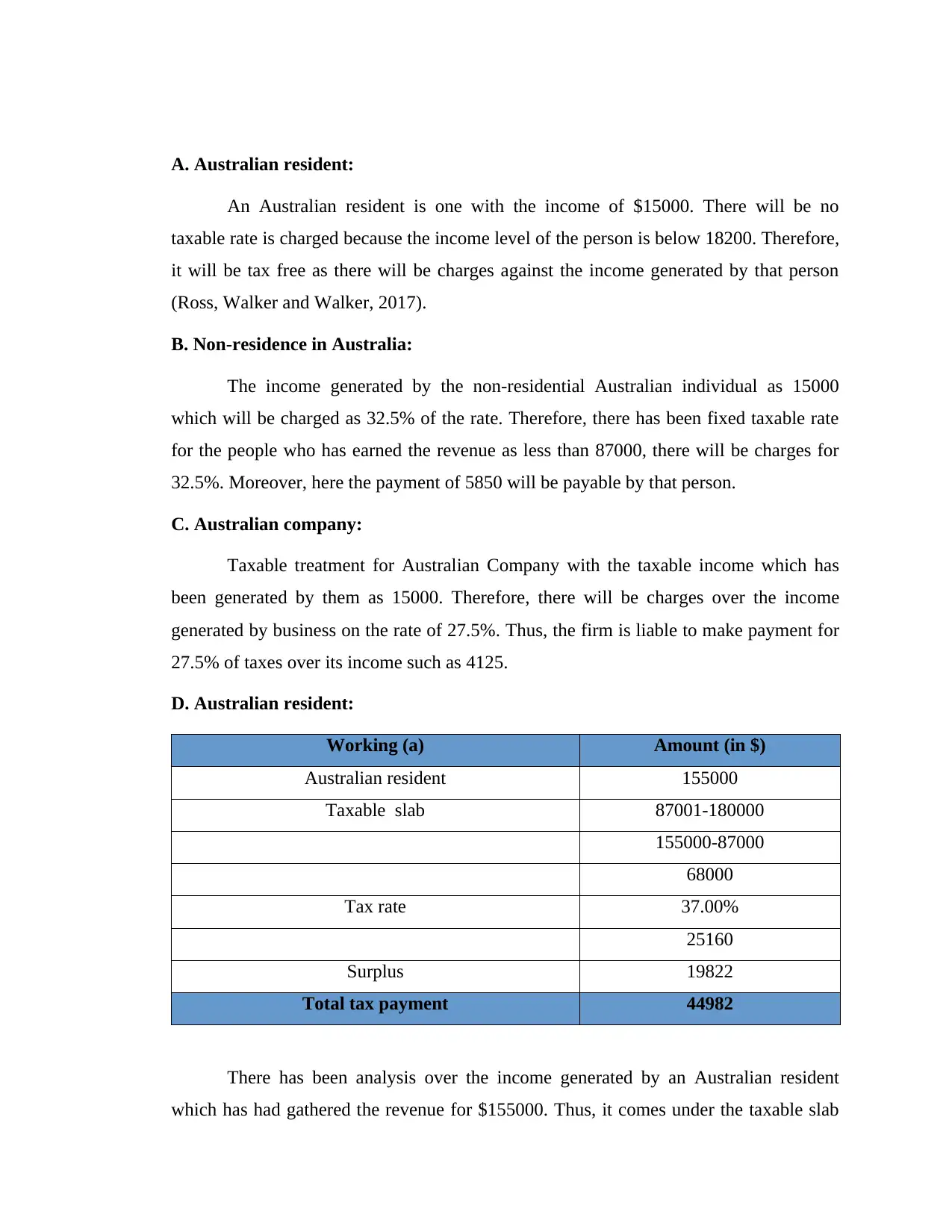

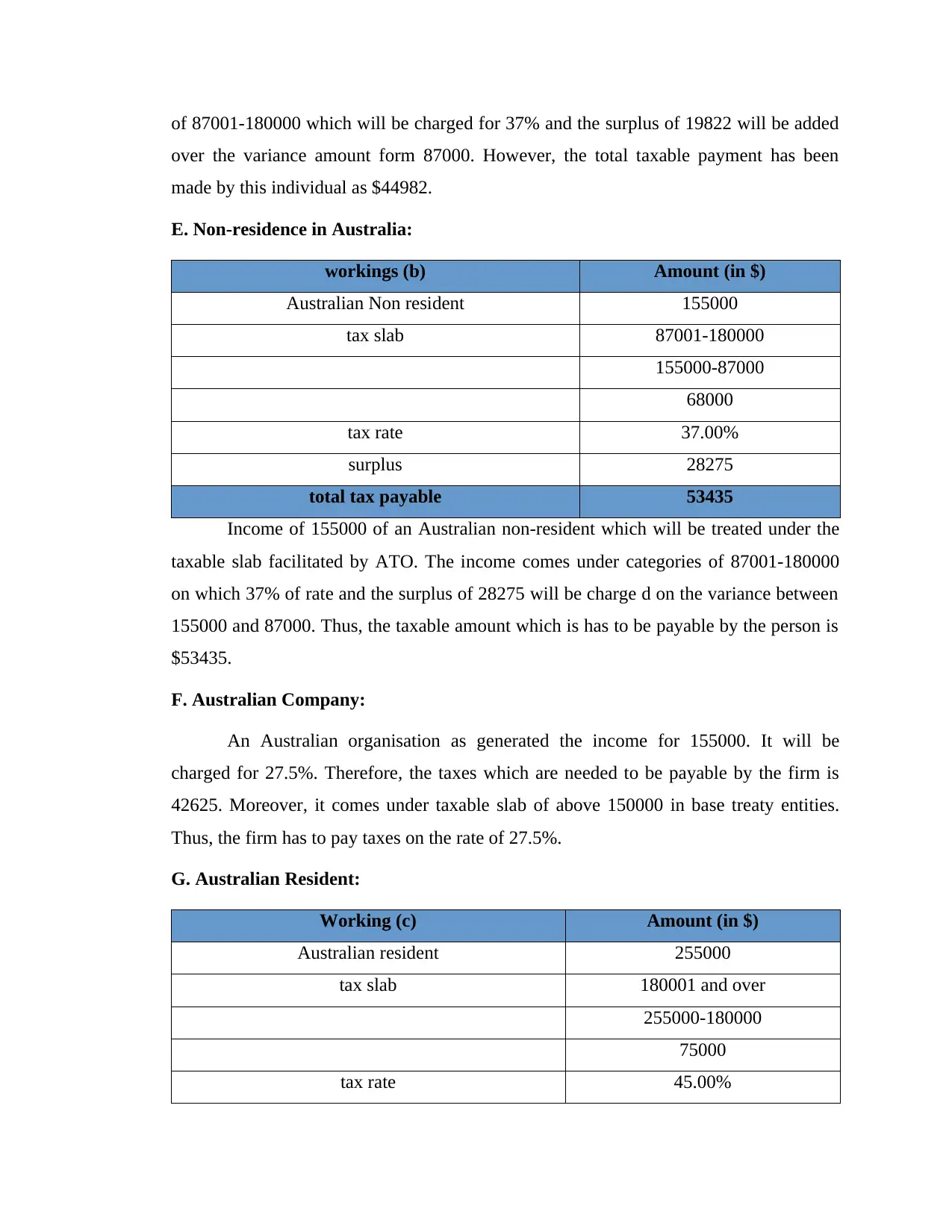

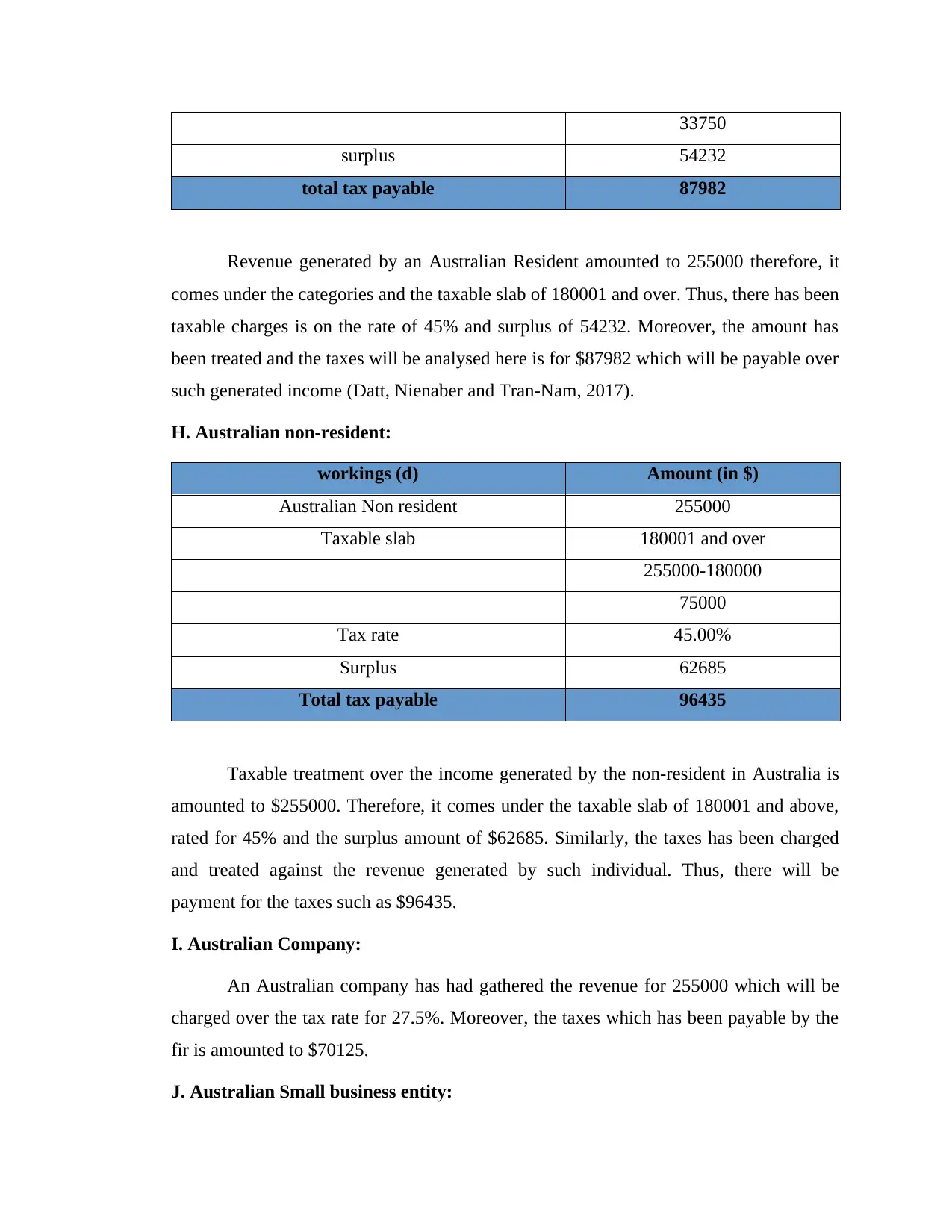

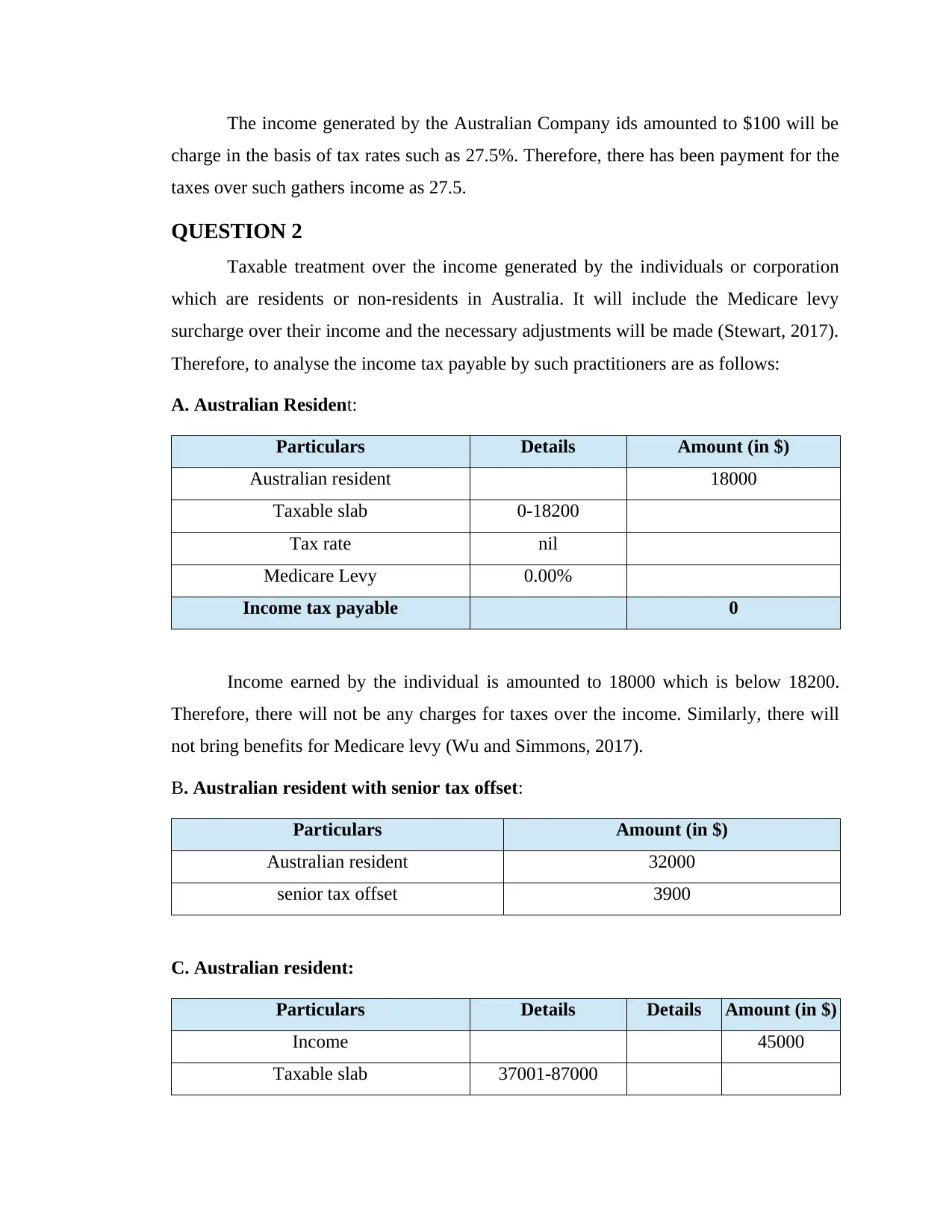

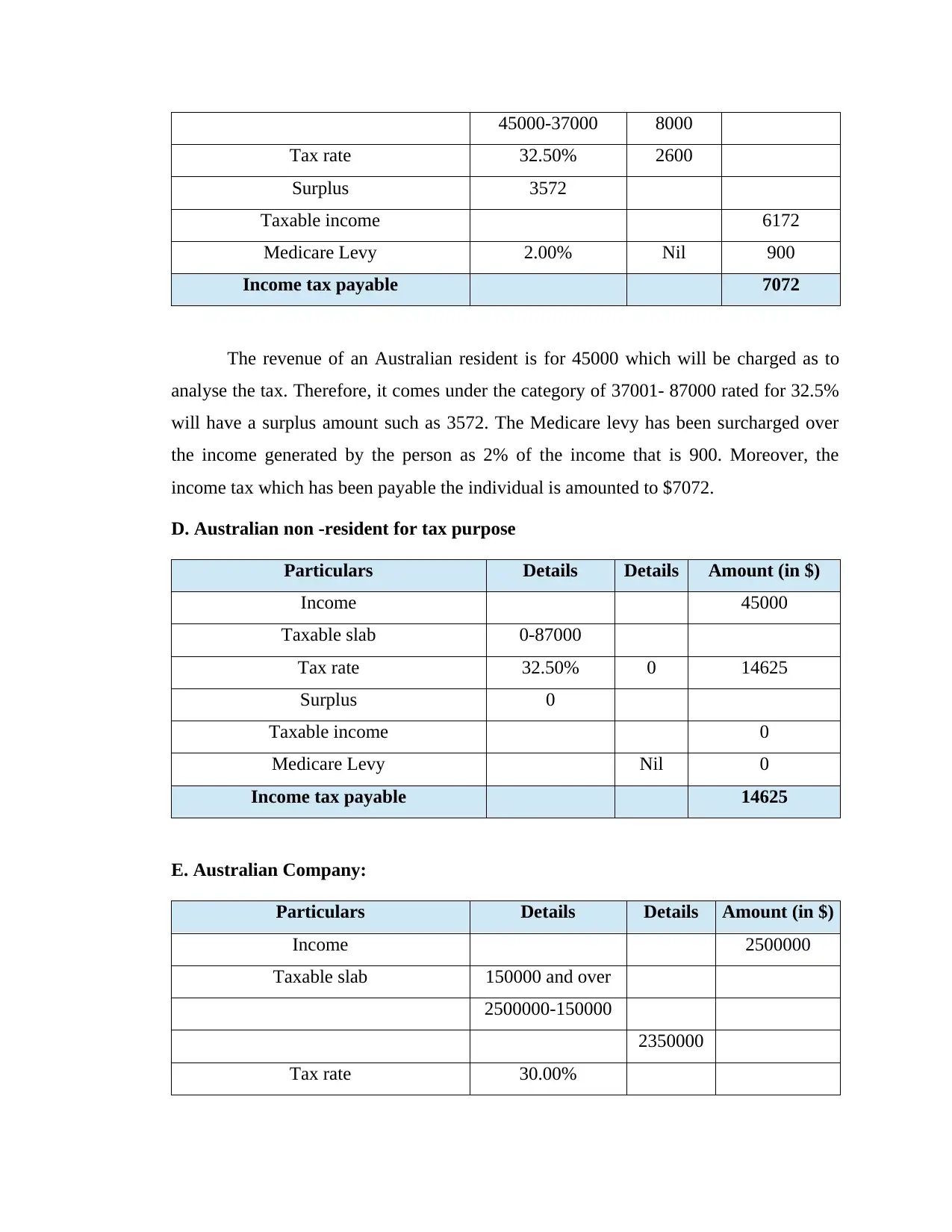

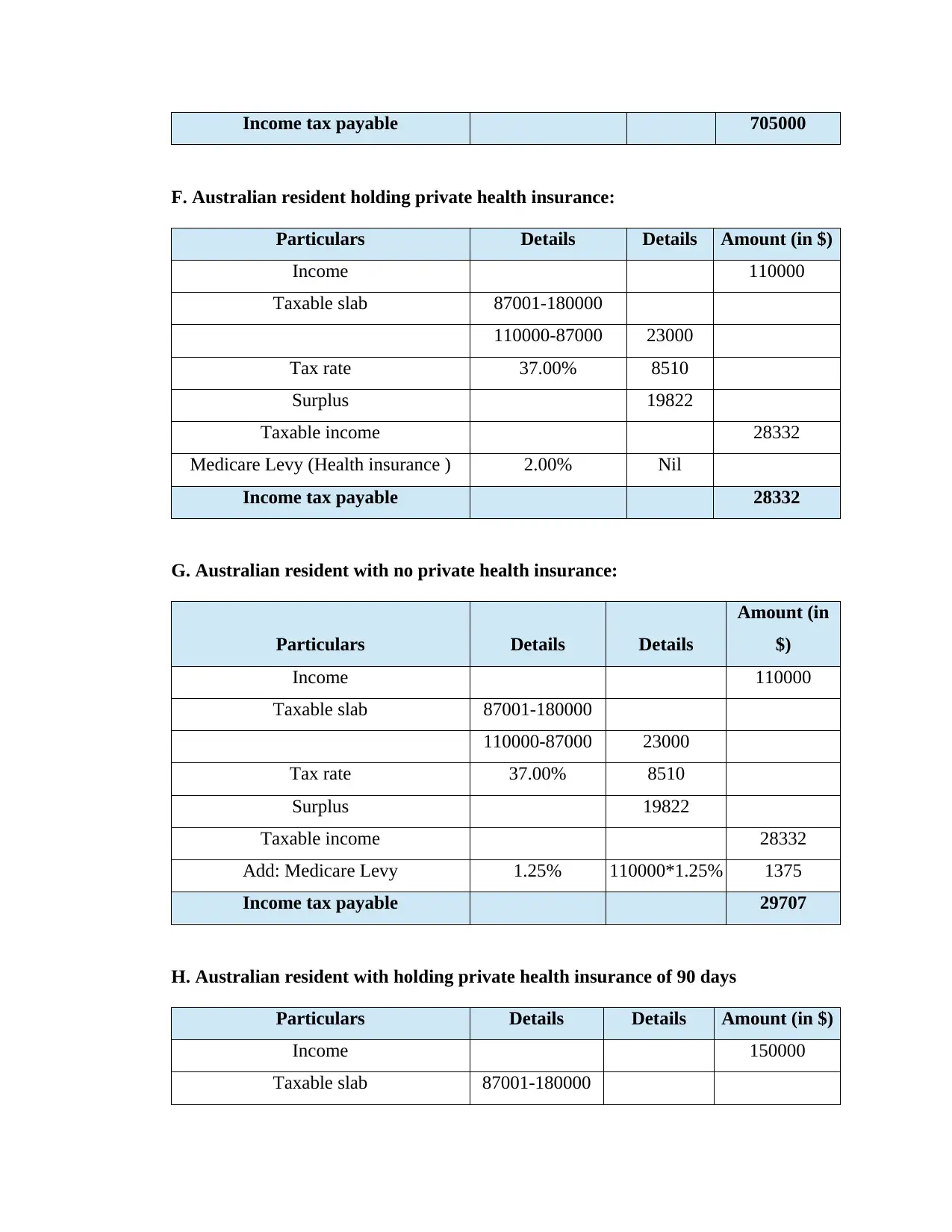

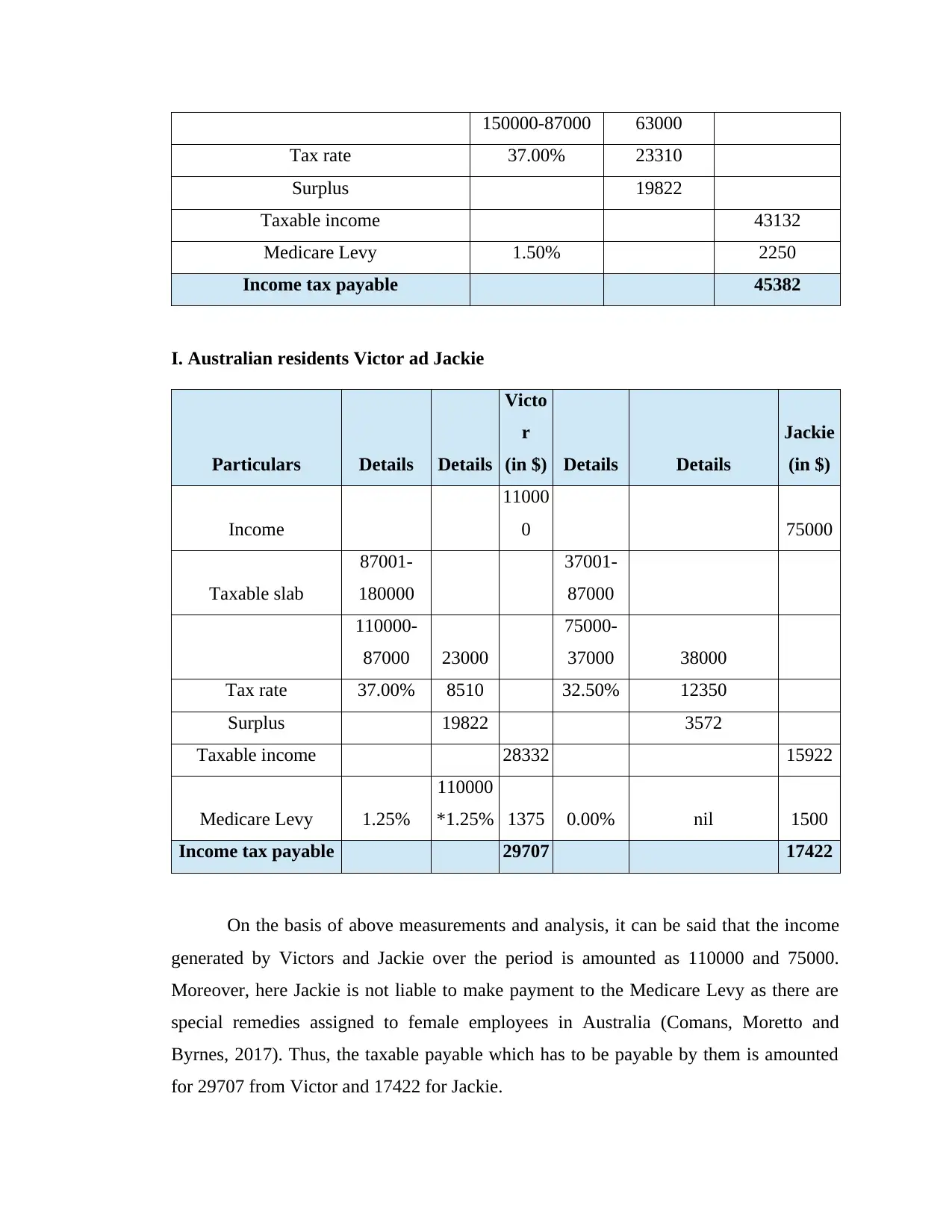

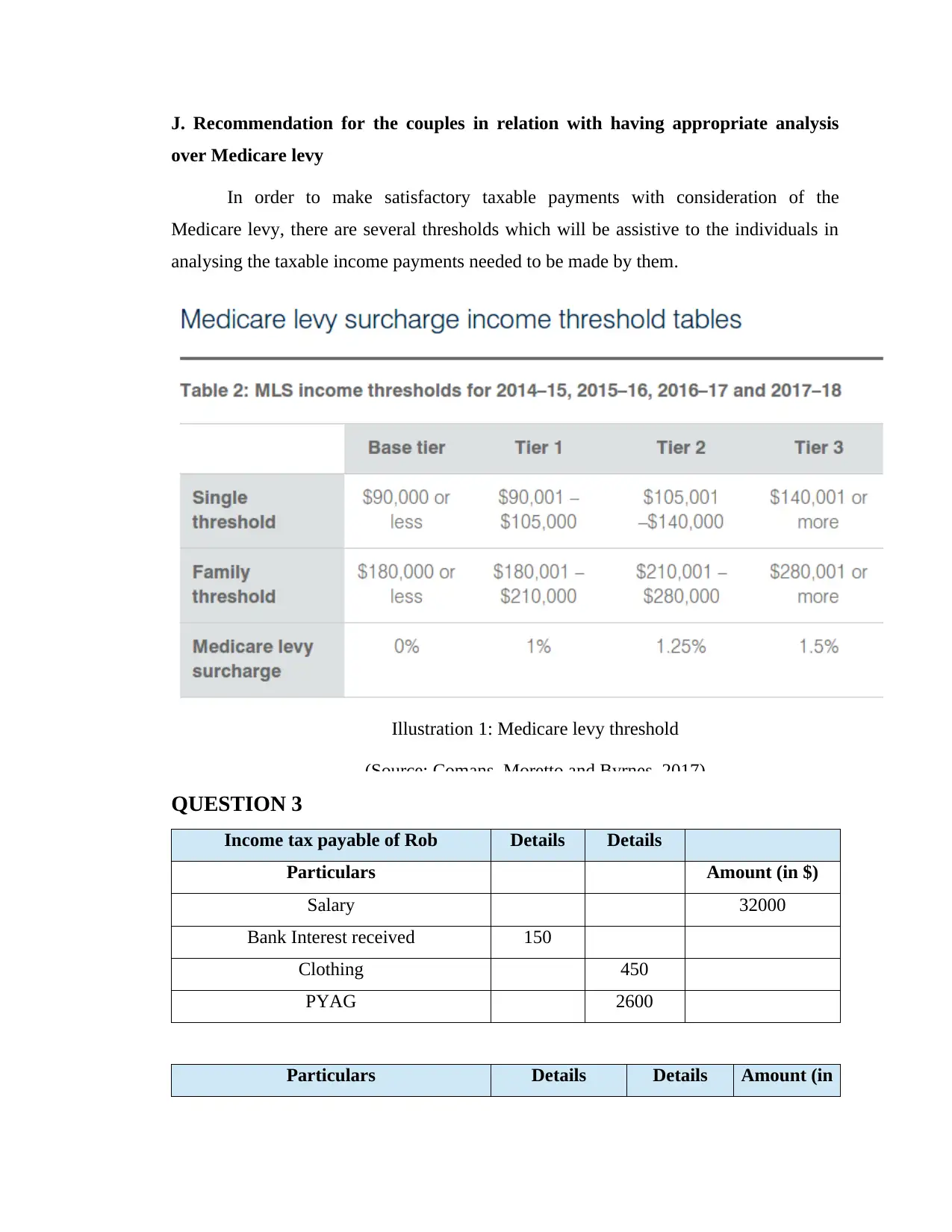

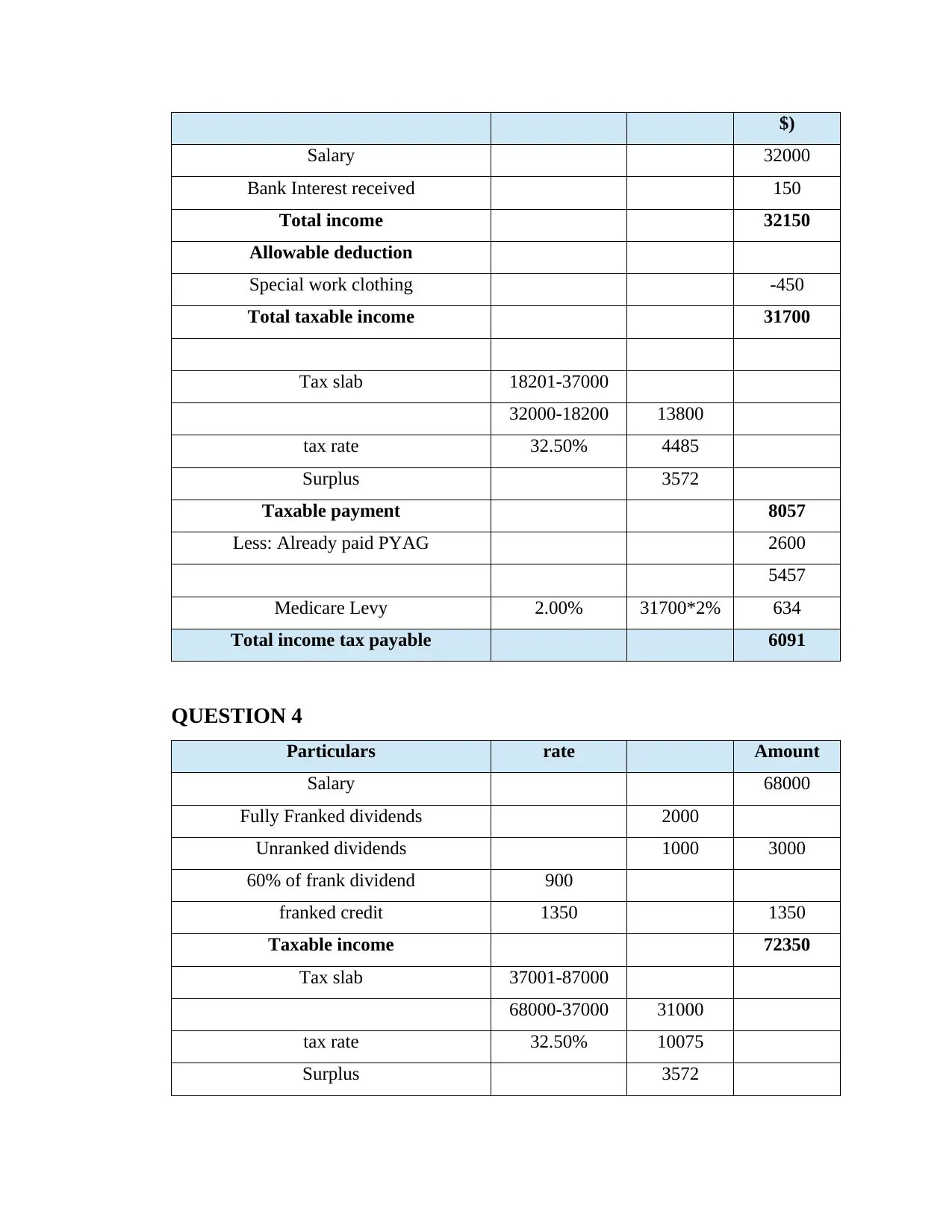

This report provides a comprehensive analysis of the Australian taxation system, focusing on income tax, Medicare levy, and company tax. It examines the tax implications for both Australian residents and non-residents, as well as for companies, across various income levels. The report includes detailed calculations and examples to illustrate how tax payable is determined, considering different tax brackets and thresholds. It also addresses the Medicare levy surcharge and its impact on individuals with and without private health insurance. Furthermore, the report explores specific scenarios, such as tax calculations for individuals with senior tax offsets and those with various income sources, including salary and bank interest. The analysis extends to small business entities and provides recommendations for couples regarding Medicare levy considerations, offering a thorough overview of the Australian tax landscape.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.