The City Sky Question Answer 2022

VerifiedAdded on 2022/10/11

|6

|2287

|12

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Question 1:

The City Sky Co is a property investment and development company.

Recently the company purchased a vacant piece of land south of Brisbane

on which it is planning to build 15 apartments to sell. The City Sky Co has

engaged the services of the local lawyer, Maurice Blackburn, to provide

the legal services required for the development for $33,000. Maurice

Blackburn runs an established sole trader business and turns over

revenue of $300,000 per year. Advise the City Sky Co of the input tax

credit entitlements that they may be entitled to. Assume that The City Sky

Co is registered for GST purposes.

Answer:

The City Sky Company is an investment company dealing in property and

engaged in development work. The company is also registered for goods

and service tax purpose, so it will be entitled for the benefit of input tax

credit as applicable.

The City Sky Co also has a plan to purchase a vacant piece of land south

of Brisbane on which the company is planning to build 15 apartments to

sell. Goods as defined “any kind of movable property other than money

and securities but it includes actionable claims ,growing crops ,grass and

things attached to or forming part of the land which are agreed to be

severed before supply or under a contract of supply ‘’.So under the

particular definition immovable property is not considered to be a part of

Goods.

Land is an immovable property so it is neither goods nor services so it

does not belong or fall under the category of Goods and Service Tax.

Therefore, no GST will be levied on any purchase of vacant land

purchased south of Brisbane on which it is planning to build 15

apartments to sell. The company is also planning to build 15 apartments

on the vacant land which comes beneath the provision of black credit

under GST act. Black Credit means any value or amount of goods received

by a person who is register under GST act for the purpose of construction

of the said immovable property whether in his own account or in the

normal process of business are not entitled to reap the benefit of Income

Tax credit. Therefore, the company is not entitled to take any benefit of

income tax credit for the purpose of building an apartment on the vacant

land.

The City Sky Co has engaged the services of the local lawyer, Maurice

Blackburn, to provide the legal services required for the development for

$33,000.Any form of services availed from lawyer will fall under the

category of reverse charge mechanism. Under the concept of reverse

charge mechanism, the goods and service tax will be borne by the person

who is availing such services rather the provider of services. If the person

The City Sky Co is a property investment and development company.

Recently the company purchased a vacant piece of land south of Brisbane

on which it is planning to build 15 apartments to sell. The City Sky Co has

engaged the services of the local lawyer, Maurice Blackburn, to provide

the legal services required for the development for $33,000. Maurice

Blackburn runs an established sole trader business and turns over

revenue of $300,000 per year. Advise the City Sky Co of the input tax

credit entitlements that they may be entitled to. Assume that The City Sky

Co is registered for GST purposes.

Answer:

The City Sky Company is an investment company dealing in property and

engaged in development work. The company is also registered for goods

and service tax purpose, so it will be entitled for the benefit of input tax

credit as applicable.

The City Sky Co also has a plan to purchase a vacant piece of land south

of Brisbane on which the company is planning to build 15 apartments to

sell. Goods as defined “any kind of movable property other than money

and securities but it includes actionable claims ,growing crops ,grass and

things attached to or forming part of the land which are agreed to be

severed before supply or under a contract of supply ‘’.So under the

particular definition immovable property is not considered to be a part of

Goods.

Land is an immovable property so it is neither goods nor services so it

does not belong or fall under the category of Goods and Service Tax.

Therefore, no GST will be levied on any purchase of vacant land

purchased south of Brisbane on which it is planning to build 15

apartments to sell. The company is also planning to build 15 apartments

on the vacant land which comes beneath the provision of black credit

under GST act. Black Credit means any value or amount of goods received

by a person who is register under GST act for the purpose of construction

of the said immovable property whether in his own account or in the

normal process of business are not entitled to reap the benefit of Income

Tax credit. Therefore, the company is not entitled to take any benefit of

income tax credit for the purpose of building an apartment on the vacant

land.

The City Sky Co has engaged the services of the local lawyer, Maurice

Blackburn, to provide the legal services required for the development for

$33,000.Any form of services availed from lawyer will fall under the

category of reverse charge mechanism. Under the concept of reverse

charge mechanism, the goods and service tax will be borne by the person

who is availing such services rather the provider of services. If the person

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

who has availed such services uses such in its own business than he is

entitled to take benefit for such income tax credit .

The company is a development company who is engaged in the business

of investment and construction of property on the vacant land than the

services of lawyer availed must be used for the purpose o f

business ,therefore the company is entitled for the income tax credit

benefit of the total amount paid as GST.

Maurice Blackburn runs an established sole trader business and turns

over revenue of $300,000 per year. The revenue of the advocate has got

no relevance with the company GST paid nor can claim any amount of

GST on the revenue of the lawyer Maurice Blackburn.

The City Sky Company can avail the benefit of income tax credit on GST

paid on the services mentioned above.

Question 2:

Emma has provided to you a listing of the transactions she has

undertaken throughout the financial year to assist you in completing her

2015 income tax return. Sale of a block of land for $1,000,000: Emma

purchased the land as an investment in 1991. The purchase price was

$250,000, plus $5,000 in stamp duty, $10,000 in legal fees. To fund the

purchase, she took out a loan on which she paid interest totalling

$32,000. During the period of ownership her council rates, water rates

and insurance totalled $22,000. In January 2005 a dispute occurred with a

neighbour over the use of the land and legal fees incurred amounted to

$5,000 in resolving this dispute. Before putting the property on the

market $27,500 was spent to remove a number of large dangerous pine

trees that were on the land. Advertising, legal fees and agent’s fees on

the sale of the land were $25,000. Sale of Emma’s 1000 shares in Rio

Tinto for $50.85 per share: Emma paid brokerage fee of 2% on the sale.

Emma initially purchased the shares for $3.5 per share in 1982. Sale of a

stamp collection Emma had purchased, from a private collector, in January

2015 for $60,000: Emma sold the collection at auction for $50,000.

Auction fees totalled $5,000 for the sale. Sale of a grand piano for

$30,000: It was initially bought for $80,000 in 2000. HI6028 Taxation

Theory, Practice and Law Individual Assignment T2.2019 5 Advise Emma

of the capital gain tax (CGT) consequences of her transitions. Ignore

indexation. Your answer must include references to relevant tax law and

or cases.

entitled to take benefit for such income tax credit .

The company is a development company who is engaged in the business

of investment and construction of property on the vacant land than the

services of lawyer availed must be used for the purpose o f

business ,therefore the company is entitled for the income tax credit

benefit of the total amount paid as GST.

Maurice Blackburn runs an established sole trader business and turns

over revenue of $300,000 per year. The revenue of the advocate has got

no relevance with the company GST paid nor can claim any amount of

GST on the revenue of the lawyer Maurice Blackburn.

The City Sky Company can avail the benefit of income tax credit on GST

paid on the services mentioned above.

Question 2:

Emma has provided to you a listing of the transactions she has

undertaken throughout the financial year to assist you in completing her

2015 income tax return. Sale of a block of land for $1,000,000: Emma

purchased the land as an investment in 1991. The purchase price was

$250,000, plus $5,000 in stamp duty, $10,000 in legal fees. To fund the

purchase, she took out a loan on which she paid interest totalling

$32,000. During the period of ownership her council rates, water rates

and insurance totalled $22,000. In January 2005 a dispute occurred with a

neighbour over the use of the land and legal fees incurred amounted to

$5,000 in resolving this dispute. Before putting the property on the

market $27,500 was spent to remove a number of large dangerous pine

trees that were on the land. Advertising, legal fees and agent’s fees on

the sale of the land were $25,000. Sale of Emma’s 1000 shares in Rio

Tinto for $50.85 per share: Emma paid brokerage fee of 2% on the sale.

Emma initially purchased the shares for $3.5 per share in 1982. Sale of a

stamp collection Emma had purchased, from a private collector, in January

2015 for $60,000: Emma sold the collection at auction for $50,000.

Auction fees totalled $5,000 for the sale. Sale of a grand piano for

$30,000: It was initially bought for $80,000 in 2000. HI6028 Taxation

Theory, Practice and Law Individual Assignment T2.2019 5 Advise Emma

of the capital gain tax (CGT) consequences of her transitions. Ignore

indexation. Your answer must include references to relevant tax law and

or cases.

Answer:

Part 1

Facts of case

Emma has purchased a plot of land as investment with an intention to

resale the same in future, the land was never purchased for constructing

house or self-usage. Post purchase of property, various expenses were

incurred to obtain legal title of the property encompassing stamp duty and

legal fees. Also, for purchasing the said property Emma took look loan and

paid interest on the same to the tune of $ 22,000. There were also legal

dispute on the property and necessary legal fees were paid to safeguard

the asset. The land was finally put to sale for $ 27,500 in 2015.

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from

investment of Emma may be classified as one off transaction, it shall fall

in the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset. Further, there are two types of cost

that are incurred for holding the property (a) Purchase cost and (b)

Ownership Cost and one is incurred while selling the same.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method. The computation shall be

made using discount method as it shall be beneficial to Emma. Further,

the holding period is greater than 12 months. (Finconnect (Australia) Pty

Ltd, 2018)

Based on above analysis, the computation of capital gain/ loss for the

current transaction has been provided as under:

Sl. No Particulars Amount

1 Sale Price of Land 275000

2 Selling Cost 27500

3 Ownership Cost 27000

- Legal fees

-Water & insurance

4 Purchase cost 265000

-Land Price

-Legal fees

-Stamp duty

Part 1

Facts of case

Emma has purchased a plot of land as investment with an intention to

resale the same in future, the land was never purchased for constructing

house or self-usage. Post purchase of property, various expenses were

incurred to obtain legal title of the property encompassing stamp duty and

legal fees. Also, for purchasing the said property Emma took look loan and

paid interest on the same to the tune of $ 22,000. There were also legal

dispute on the property and necessary legal fees were paid to safeguard

the asset. The land was finally put to sale for $ 27,500 in 2015.

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from

investment of Emma may be classified as one off transaction, it shall fall

in the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset. Further, there are two types of cost

that are incurred for holding the property (a) Purchase cost and (b)

Ownership Cost and one is incurred while selling the same.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method. The computation shall be

made using discount method as it shall be beneficial to Emma. Further,

the holding period is greater than 12 months. (Finconnect (Australia) Pty

Ltd, 2018)

Based on above analysis, the computation of capital gain/ loss for the

current transaction has been provided as under:

Sl. No Particulars Amount

1 Sale Price of Land 275000

2 Selling Cost 27500

3 Ownership Cost 27000

- Legal fees

-Water & insurance

4 Purchase cost 265000

-Land Price

-Legal fees

-Stamp duty

5 Capital Loss -44500

Part 2

Facts of case

In the given case, Emma has sold shares which she has purchased way

back in 1982. The cost price of purchase of share was $3.5 and she has

sold the same at $ 50.85. Further, the shares were sold after a brokerage

payment of 2%

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from sale

of shares of Emma may be classified as one off transaction, it shall fall in

the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method. The computation shall be

made using discount method as it shall be beneficial to Emma. Further,

the holding period is greater than 12 months.

However, in the current case since the asset was purchased before

September 20, 1985 the laws of capital gain tax shall not be applicable

and the receipt may be treated as capital receipt and no tax shall be paid

on such receipt. (Finconnect Austraalia Pty Ltd, 2018)

Part 3

Facts of case

Under the third part, Emma has purchased stamps from a private collector

in January 2015 for $ 60,000 and has disposed off the same in the current

year in 2015 for $ 50,000. The auction fees incurred in connection with

the sale has been $ 5,000.

Part 2

Facts of case

In the given case, Emma has sold shares which she has purchased way

back in 1982. The cost price of purchase of share was $3.5 and she has

sold the same at $ 50.85. Further, the shares were sold after a brokerage

payment of 2%

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from sale

of shares of Emma may be classified as one off transaction, it shall fall in

the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method. The computation shall be

made using discount method as it shall be beneficial to Emma. Further,

the holding period is greater than 12 months.

However, in the current case since the asset was purchased before

September 20, 1985 the laws of capital gain tax shall not be applicable

and the receipt may be treated as capital receipt and no tax shall be paid

on such receipt. (Finconnect Austraalia Pty Ltd, 2018)

Part 3

Facts of case

Under the third part, Emma has purchased stamps from a private collector

in January 2015 for $ 60,000 and has disposed off the same in the current

year in 2015 for $ 50,000. The auction fees incurred in connection with

the sale has been $ 5,000.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from sale

of shares of Emma may be classified as one off transaction, it shall fall in

the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method.

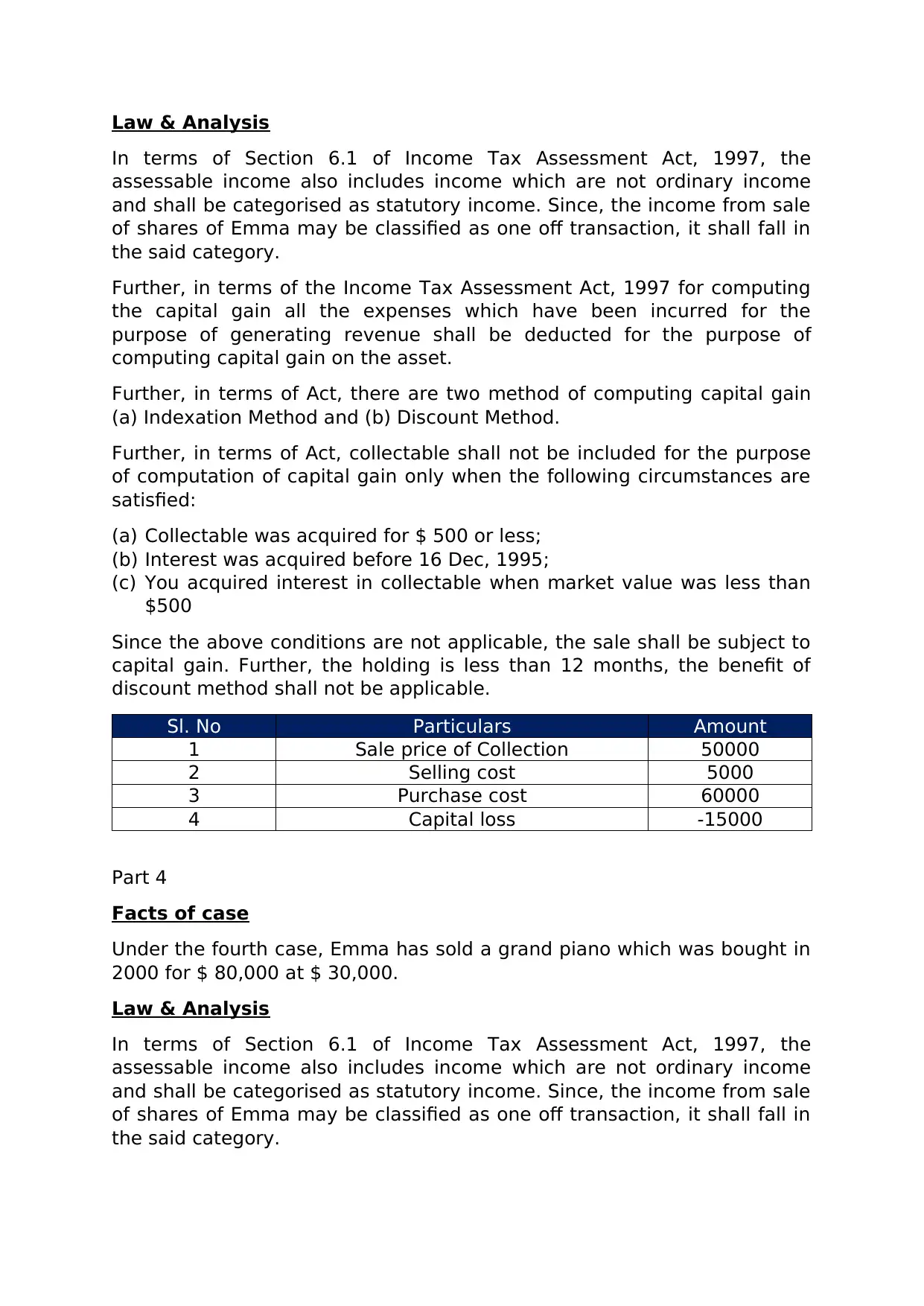

Further, in terms of Act, collectable shall not be included for the purpose

of computation of capital gain only when the following circumstances are

satisfied:

(a) Collectable was acquired for $ 500 or less;

(b) Interest was acquired before 16 Dec, 1995;

(c) You acquired interest in collectable when market value was less than

$500

Since the above conditions are not applicable, the sale shall be subject to

capital gain. Further, the holding is less than 12 months, the benefit of

discount method shall not be applicable.

Sl. No Particulars Amount

1 Sale price of Collection 50000

2 Selling cost 5000

3 Purchase cost 60000

4 Capital loss -15000

Part 4

Facts of case

Under the fourth case, Emma has sold a grand piano which was bought in

2000 for $ 80,000 at $ 30,000.

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from sale

of shares of Emma may be classified as one off transaction, it shall fall in

the said category.

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from sale

of shares of Emma may be classified as one off transaction, it shall fall in

the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method.

Further, in terms of Act, collectable shall not be included for the purpose

of computation of capital gain only when the following circumstances are

satisfied:

(a) Collectable was acquired for $ 500 or less;

(b) Interest was acquired before 16 Dec, 1995;

(c) You acquired interest in collectable when market value was less than

$500

Since the above conditions are not applicable, the sale shall be subject to

capital gain. Further, the holding is less than 12 months, the benefit of

discount method shall not be applicable.

Sl. No Particulars Amount

1 Sale price of Collection 50000

2 Selling cost 5000

3 Purchase cost 60000

4 Capital loss -15000

Part 4

Facts of case

Under the fourth case, Emma has sold a grand piano which was bought in

2000 for $ 80,000 at $ 30,000.

Law & Analysis

In terms of Section 6.1 of Income Tax Assessment Act, 1997, the

assessable income also includes income which are not ordinary income

and shall be categorised as statutory income. Since, the income from sale

of shares of Emma may be classified as one off transaction, it shall fall in

the said category.

Further, in terms of the Income Tax Assessment Act, 1997 for computing

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset.

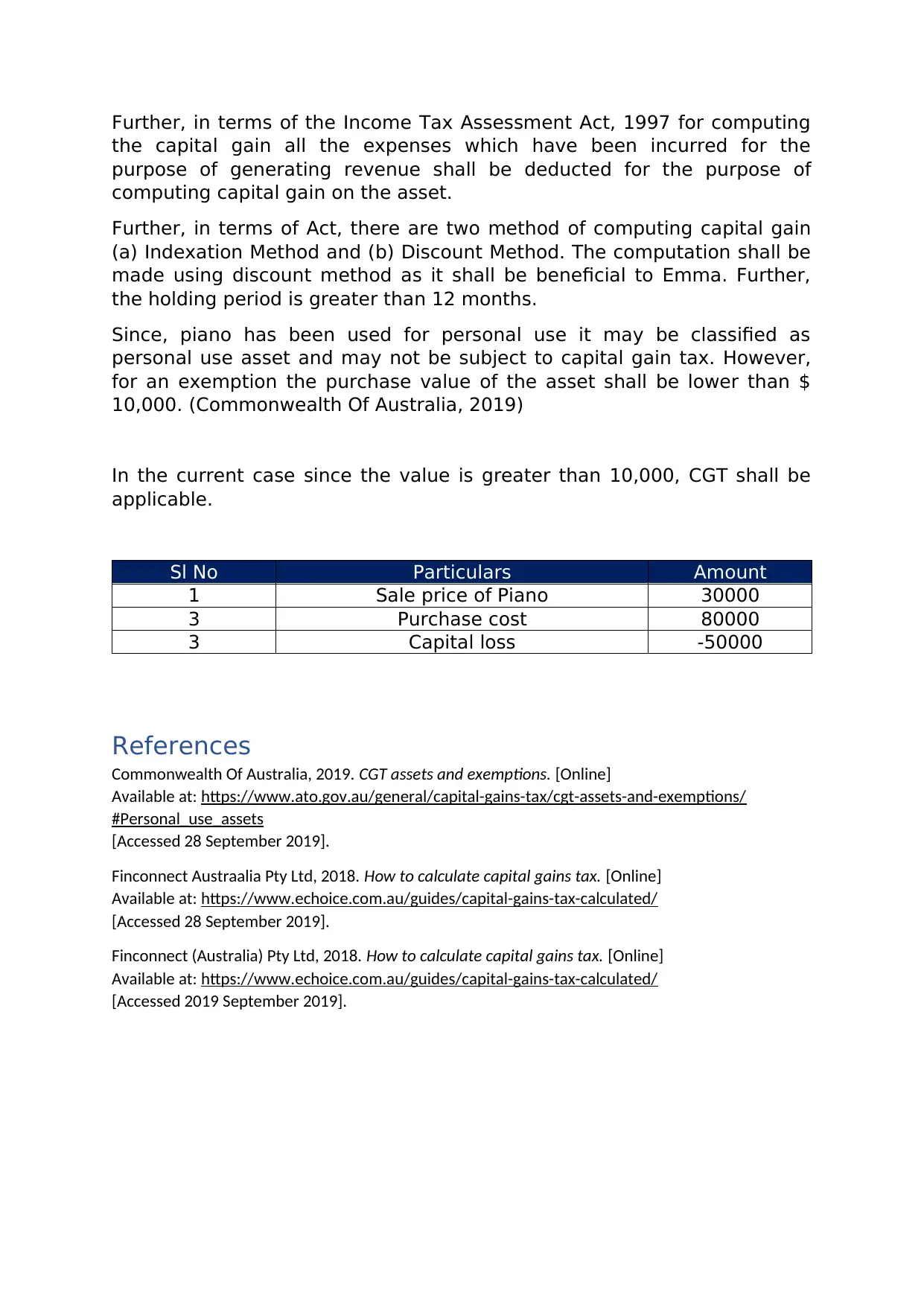

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method. The computation shall be

made using discount method as it shall be beneficial to Emma. Further,

the holding period is greater than 12 months.

Since, piano has been used for personal use it may be classified as

personal use asset and may not be subject to capital gain tax. However,

for an exemption the purchase value of the asset shall be lower than $

10,000. (Commonwealth Of Australia, 2019)

In the current case since the value is greater than 10,000, CGT shall be

applicable.

Sl No Particulars Amount

1 Sale price of Piano 30000

3 Purchase cost 80000

3 Capital loss -50000

References

Commonwealth Of Australia, 2019. CGT assets and exemptions. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#Personal_use_assets

[Accessed 28 September 2019].

Finconnect Austraalia Pty Ltd, 2018. How to calculate capital gains tax. [Online]

Available at: https://www.echoice.com.au/guides/capital-gains-tax-calculated/

[Accessed 28 September 2019].

Finconnect (Australia) Pty Ltd, 2018. How to calculate capital gains tax. [Online]

Available at: https://www.echoice.com.au/guides/capital-gains-tax-calculated/

[Accessed 2019 September 2019].

the capital gain all the expenses which have been incurred for the

purpose of generating revenue shall be deducted for the purpose of

computing capital gain on the asset.

Further, in terms of Act, there are two method of computing capital gain

(a) Indexation Method and (b) Discount Method. The computation shall be

made using discount method as it shall be beneficial to Emma. Further,

the holding period is greater than 12 months.

Since, piano has been used for personal use it may be classified as

personal use asset and may not be subject to capital gain tax. However,

for an exemption the purchase value of the asset shall be lower than $

10,000. (Commonwealth Of Australia, 2019)

In the current case since the value is greater than 10,000, CGT shall be

applicable.

Sl No Particulars Amount

1 Sale price of Piano 30000

3 Purchase cost 80000

3 Capital loss -50000

References

Commonwealth Of Australia, 2019. CGT assets and exemptions. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#Personal_use_assets

[Accessed 28 September 2019].

Finconnect Austraalia Pty Ltd, 2018. How to calculate capital gains tax. [Online]

Available at: https://www.echoice.com.au/guides/capital-gains-tax-calculated/

[Accessed 28 September 2019].

Finconnect (Australia) Pty Ltd, 2018. How to calculate capital gains tax. [Online]

Available at: https://www.echoice.com.au/guides/capital-gains-tax-calculated/

[Accessed 2019 September 2019].

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.