ASSIGNMENT ABOUT THE CORPORATE ACCOUNTING.

VerifiedAdded on 2022/10/04

|11

|1776

|16

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CORPORATE ACCOUNTING 1

CORPORATE

ACCOUNTING

CORPORATE

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 2

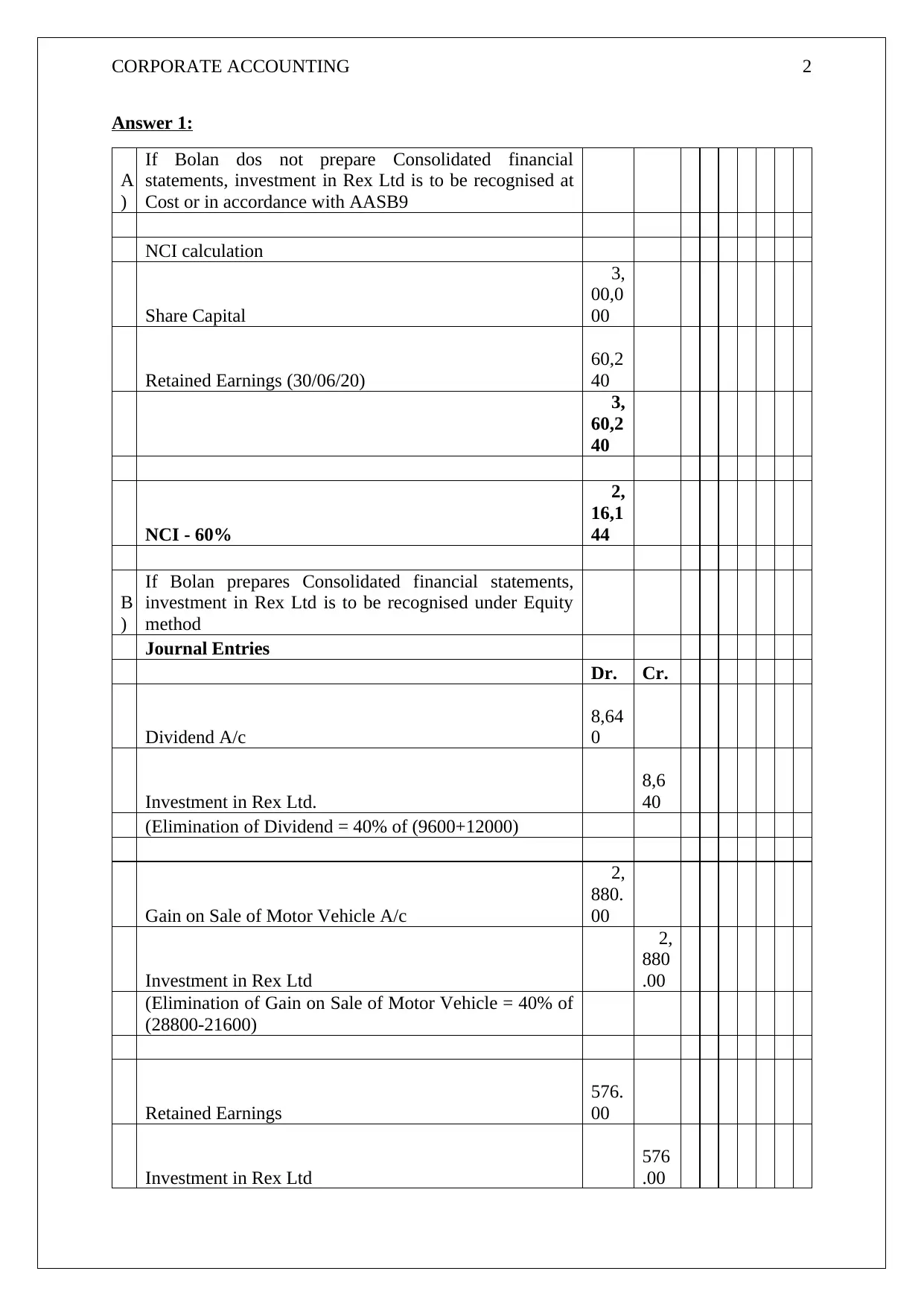

Answer 1:

A

)

If Bolan dos not prepare Consolidated financial

statements, investment in Rex Ltd is to be recognised at

Cost or in accordance with AASB9

NCI calculation

Share Capital

3,

00,0

00

Retained Earnings (30/06/20)

60,2

40

3,

60,2

40

NCI - 60%

2,

16,1

44

B

)

If Bolan prepares Consolidated financial statements,

investment in Rex Ltd is to be recognised under Equity

method

Journal Entries

Dr. Cr.

Dividend A/c

8,64

0

Investment in Rex Ltd.

8,6

40

(Elimination of Dividend = 40% of (9600+12000)

Gain on Sale of Motor Vehicle A/c

2,

880.

00

Investment in Rex Ltd

2,

880

.00

(Elimination of Gain on Sale of Motor Vehicle = 40% of

(28800-21600)

Retained Earnings

576.

00

Investment in Rex Ltd

576

.00

Answer 1:

A

)

If Bolan dos not prepare Consolidated financial

statements, investment in Rex Ltd is to be recognised at

Cost or in accordance with AASB9

NCI calculation

Share Capital

3,

00,0

00

Retained Earnings (30/06/20)

60,2

40

3,

60,2

40

NCI - 60%

2,

16,1

44

B

)

If Bolan prepares Consolidated financial statements,

investment in Rex Ltd is to be recognised under Equity

method

Journal Entries

Dr. Cr.

Dividend A/c

8,64

0

Investment in Rex Ltd.

8,6

40

(Elimination of Dividend = 40% of (9600+12000)

Gain on Sale of Motor Vehicle A/c

2,

880.

00

Investment in Rex Ltd

2,

880

.00

(Elimination of Gain on Sale of Motor Vehicle = 40% of

(28800-21600)

Retained Earnings

576.

00

Investment in Rex Ltd

576

.00

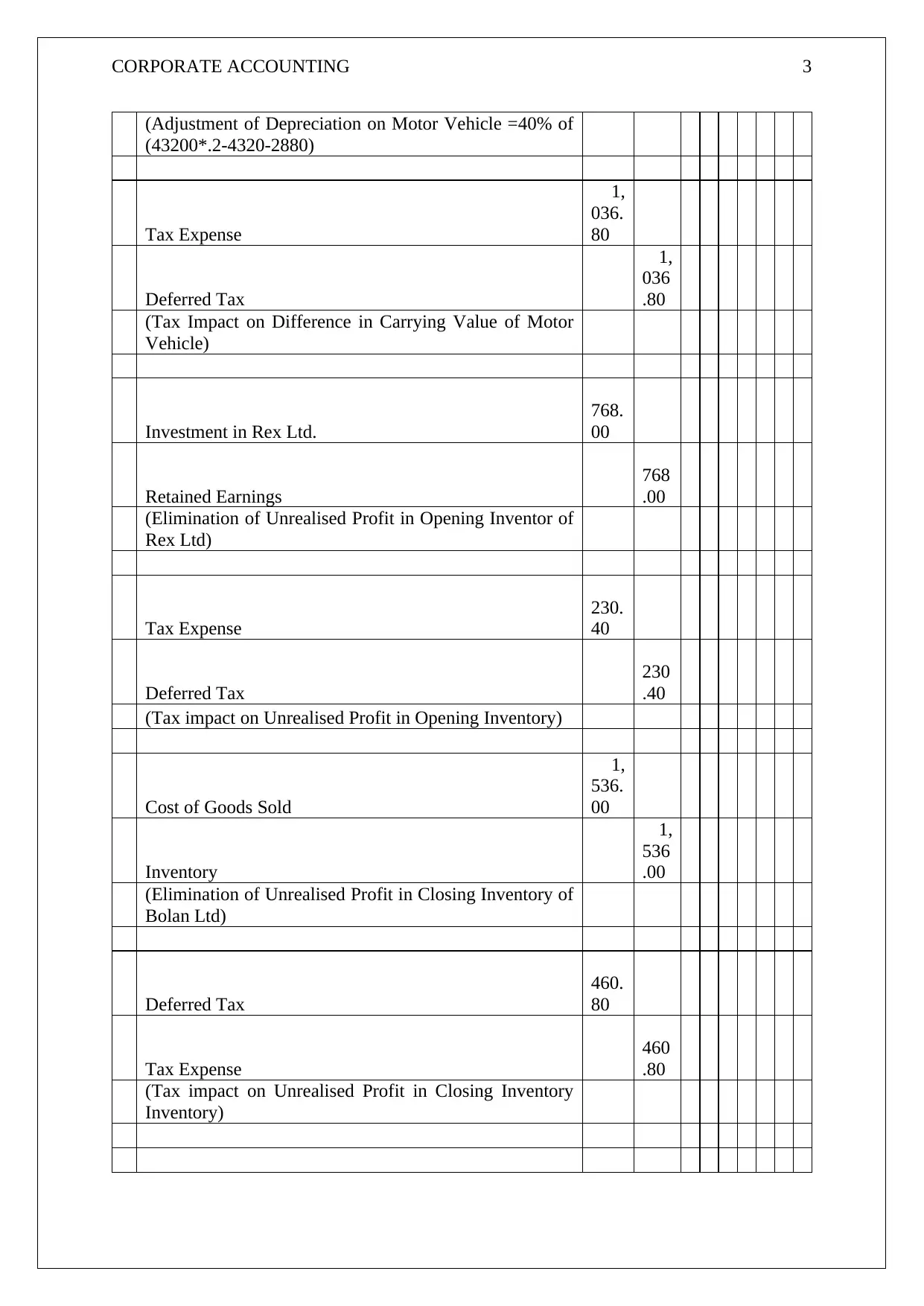

CORPORATE ACCOUNTING 3

(Adjustment of Depreciation on Motor Vehicle =40% of

(43200*.2-4320-2880)

Tax Expense

1,

036.

80

Deferred Tax

1,

036

.80

(Tax Impact on Difference in Carrying Value of Motor

Vehicle)

Investment in Rex Ltd.

768.

00

Retained Earnings

768

.00

(Elimination of Unrealised Profit in Opening Inventor of

Rex Ltd)

Tax Expense

230.

40

Deferred Tax

230

.40

(Tax impact on Unrealised Profit in Opening Inventory)

Cost of Goods Sold

1,

536.

00

Inventory

1,

536

.00

(Elimination of Unrealised Profit in Closing Inventory of

Bolan Ltd)

Deferred Tax

460.

80

Tax Expense

460

.80

(Tax impact on Unrealised Profit in Closing Inventory

Inventory)

(Adjustment of Depreciation on Motor Vehicle =40% of

(43200*.2-4320-2880)

Tax Expense

1,

036.

80

Deferred Tax

1,

036

.80

(Tax Impact on Difference in Carrying Value of Motor

Vehicle)

Investment in Rex Ltd.

768.

00

Retained Earnings

768

.00

(Elimination of Unrealised Profit in Opening Inventor of

Rex Ltd)

Tax Expense

230.

40

Deferred Tax

230

.40

(Tax impact on Unrealised Profit in Opening Inventory)

Cost of Goods Sold

1,

536.

00

Inventory

1,

536

.00

(Elimination of Unrealised Profit in Closing Inventory of

Bolan Ltd)

Deferred Tax

460.

80

Tax Expense

460

.80

(Tax impact on Unrealised Profit in Closing Inventory

Inventory)

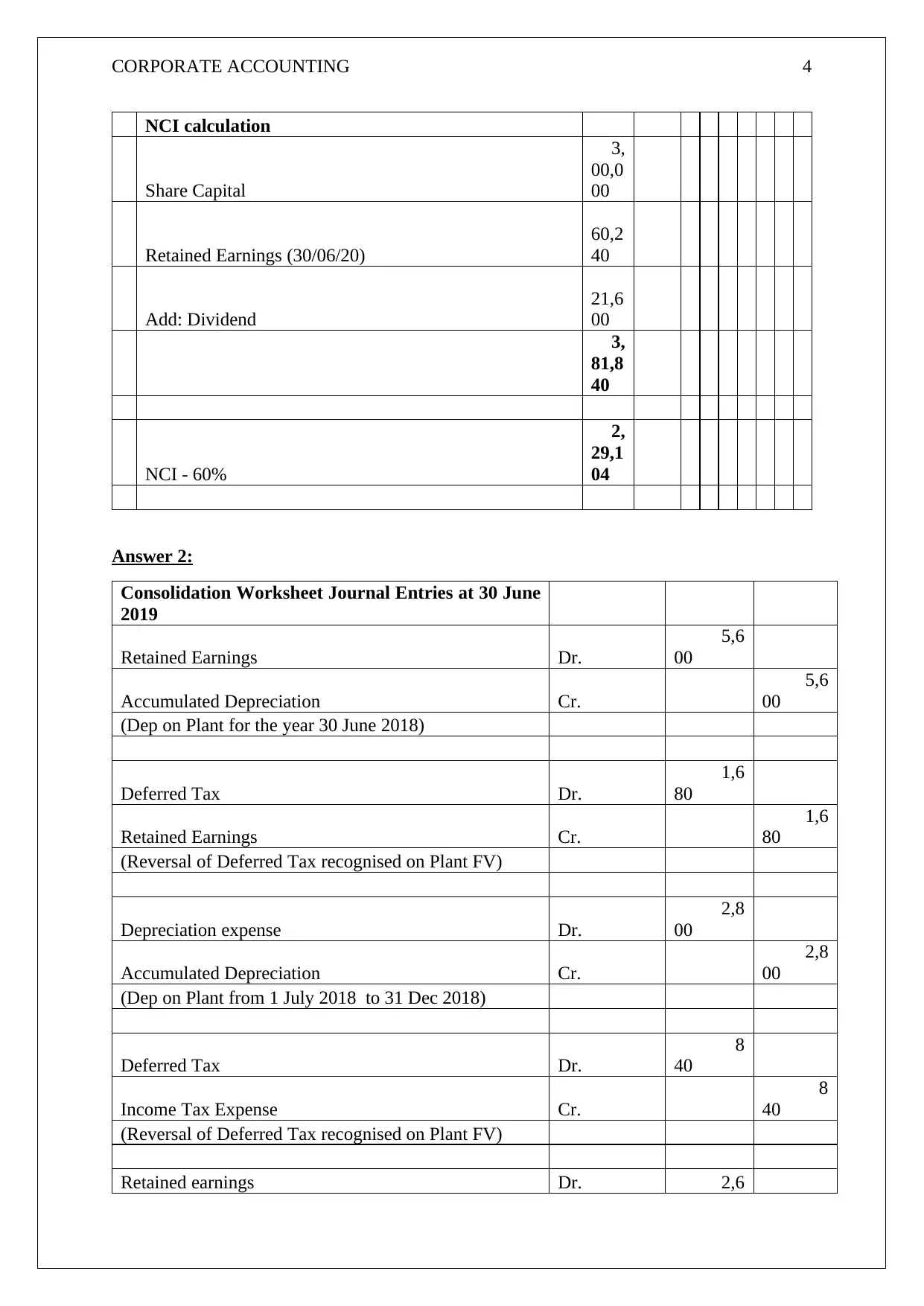

CORPORATE ACCOUNTING 4

NCI calculation

Share Capital

3,

00,0

00

Retained Earnings (30/06/20)

60,2

40

Add: Dividend

21,6

00

3,

81,8

40

NCI - 60%

2,

29,1

04

Answer 2:

Consolidation Worksheet Journal Entries at 30 June

2019

Retained Earnings Dr.

5,6

00

Accumulated Depreciation Cr.

5,6

00

(Dep on Plant for the year 30 June 2018)

Deferred Tax Dr.

1,6

80

Retained Earnings Cr.

1,6

80

(Reversal of Deferred Tax recognised on Plant FV)

Depreciation expense Dr.

2,8

00

Accumulated Depreciation Cr.

2,8

00

(Dep on Plant from 1 July 2018 to 31 Dec 2018)

Deferred Tax Dr.

8

40

Income Tax Expense Cr.

8

40

(Reversal of Deferred Tax recognised on Plant FV)

Retained earnings Dr. 2,6

NCI calculation

Share Capital

3,

00,0

00

Retained Earnings (30/06/20)

60,2

40

Add: Dividend

21,6

00

3,

81,8

40

NCI - 60%

2,

29,1

04

Answer 2:

Consolidation Worksheet Journal Entries at 30 June

2019

Retained Earnings Dr.

5,6

00

Accumulated Depreciation Cr.

5,6

00

(Dep on Plant for the year 30 June 2018)

Deferred Tax Dr.

1,6

80

Retained Earnings Cr.

1,6

80

(Reversal of Deferred Tax recognised on Plant FV)

Depreciation expense Dr.

2,8

00

Accumulated Depreciation Cr.

2,8

00

(Dep on Plant from 1 July 2018 to 31 Dec 2018)

Deferred Tax Dr.

8

40

Income Tax Expense Cr.

8

40

(Reversal of Deferred Tax recognised on Plant FV)

Retained earnings Dr. 2,6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 5

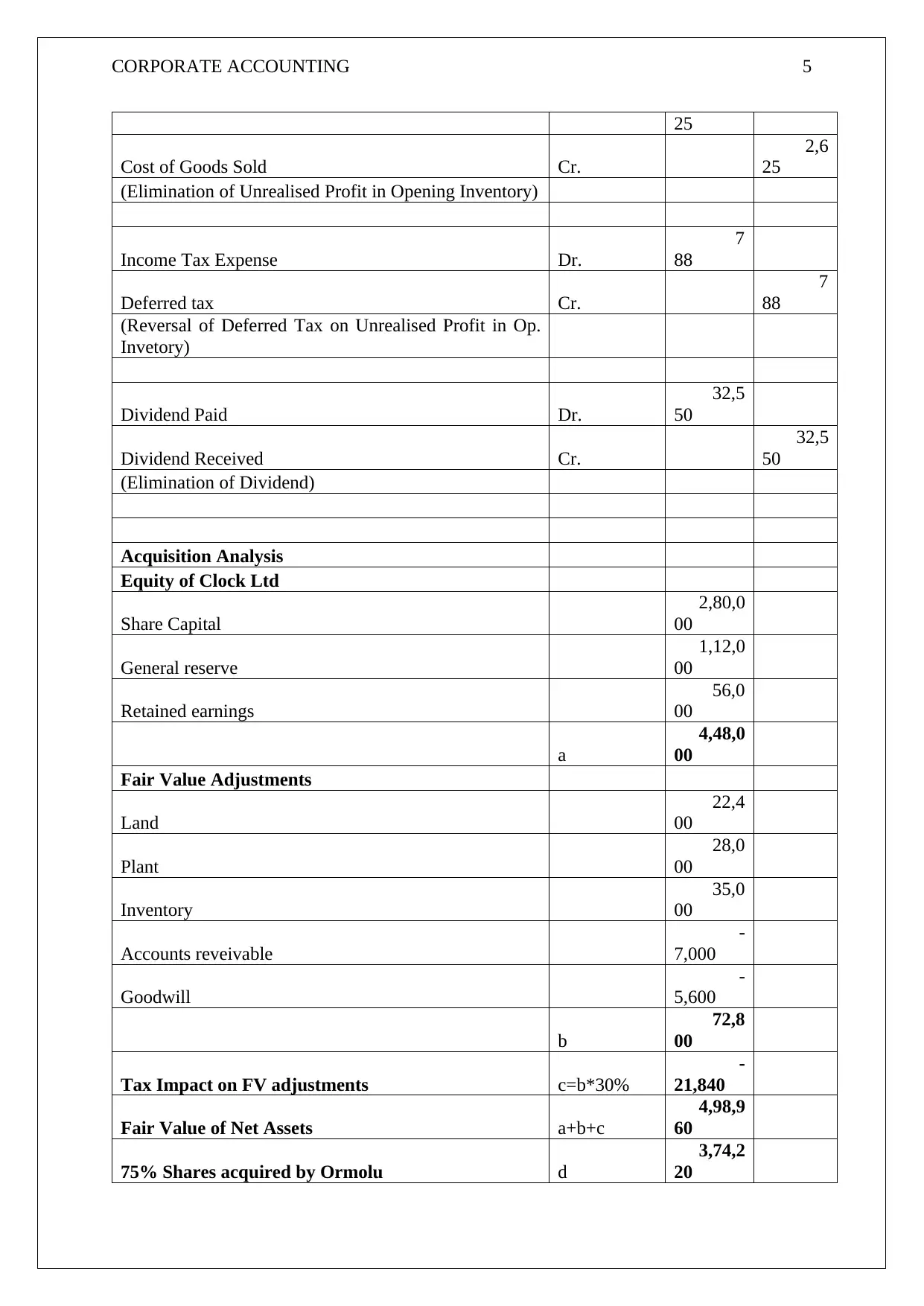

25

Cost of Goods Sold Cr.

2,6

25

(Elimination of Unrealised Profit in Opening Inventory)

Income Tax Expense Dr.

7

88

Deferred tax Cr.

7

88

(Reversal of Deferred Tax on Unrealised Profit in Op.

Invetory)

Dividend Paid Dr.

32,5

50

Dividend Received Cr.

32,5

50

(Elimination of Dividend)

Acquisition Analysis

Equity of Clock Ltd

Share Capital

2,80,0

00

General reserve

1,12,0

00

Retained earnings

56,0

00

a

4,48,0

00

Fair Value Adjustments

Land

22,4

00

Plant

28,0

00

Inventory

35,0

00

Accounts reveivable

-

7,000

Goodwill

-

5,600

b

72,8

00

Tax Impact on FV adjustments c=b*30%

-

21,840

Fair Value of Net Assets a+b+c

4,98,9

60

75% Shares acquired by Ormolu d

3,74,2

20

25

Cost of Goods Sold Cr.

2,6

25

(Elimination of Unrealised Profit in Opening Inventory)

Income Tax Expense Dr.

7

88

Deferred tax Cr.

7

88

(Reversal of Deferred Tax on Unrealised Profit in Op.

Invetory)

Dividend Paid Dr.

32,5

50

Dividend Received Cr.

32,5

50

(Elimination of Dividend)

Acquisition Analysis

Equity of Clock Ltd

Share Capital

2,80,0

00

General reserve

1,12,0

00

Retained earnings

56,0

00

a

4,48,0

00

Fair Value Adjustments

Land

22,4

00

Plant

28,0

00

Inventory

35,0

00

Accounts reveivable

-

7,000

Goodwill

-

5,600

b

72,8

00

Tax Impact on FV adjustments c=b*30%

-

21,840

Fair Value of Net Assets a+b+c

4,98,9

60

75% Shares acquired by Ormolu d

3,74,2

20

CORPORATE ACCOUNTING 6

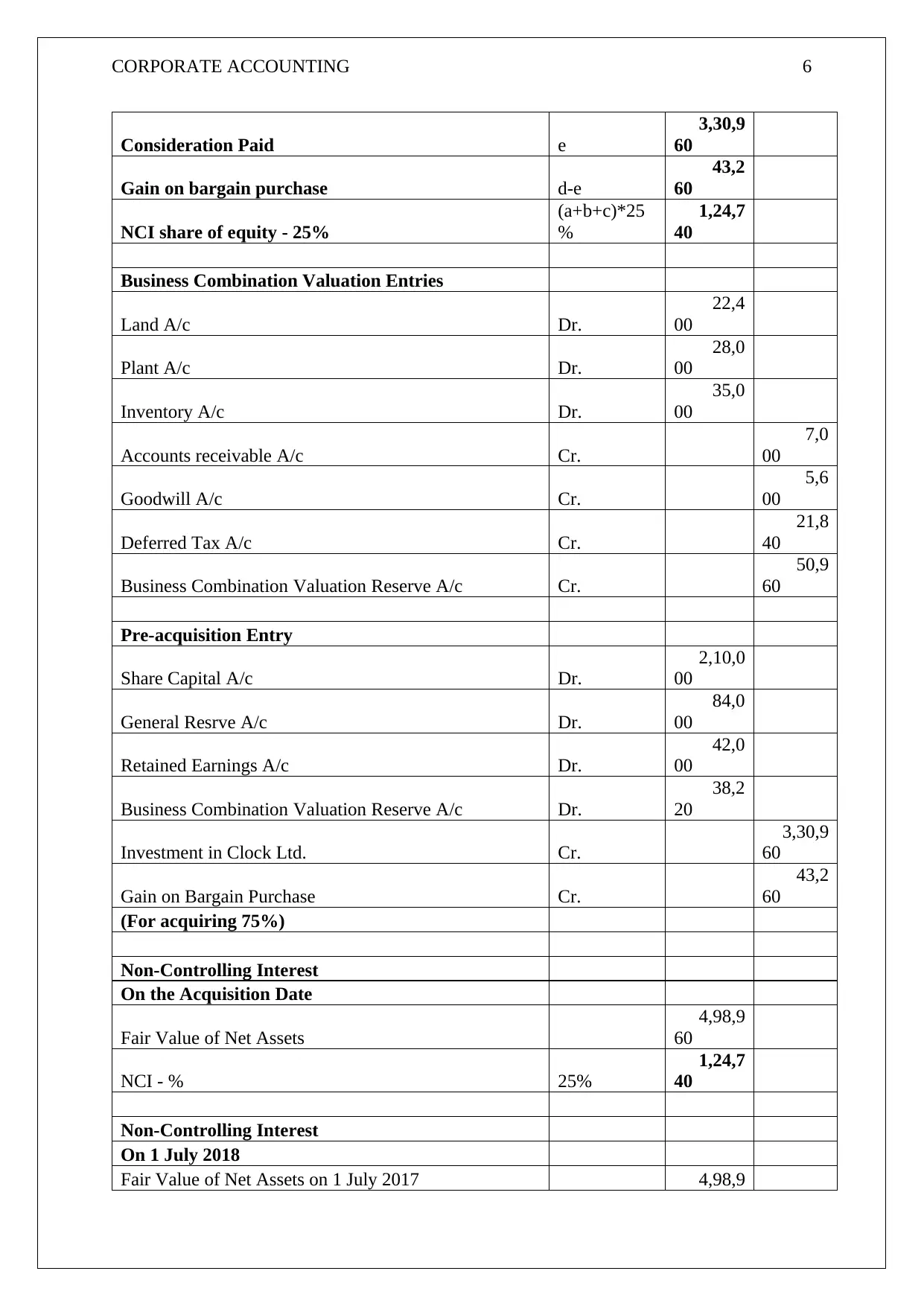

Consideration Paid e

3,30,9

60

Gain on bargain purchase d-e

43,2

60

NCI share of equity - 25%

(a+b+c)*25

%

1,24,7

40

Business Combination Valuation Entries

Land A/c Dr.

22,4

00

Plant A/c Dr.

28,0

00

Inventory A/c Dr.

35,0

00

Accounts receivable A/c Cr.

7,0

00

Goodwill A/c Cr.

5,6

00

Deferred Tax A/c Cr.

21,8

40

Business Combination Valuation Reserve A/c Cr.

50,9

60

Pre-acquisition Entry

Share Capital A/c Dr.

2,10,0

00

General Resrve A/c Dr.

84,0

00

Retained Earnings A/c Dr.

42,0

00

Business Combination Valuation Reserve A/c Dr.

38,2

20

Investment in Clock Ltd. Cr.

3,30,9

60

Gain on Bargain Purchase Cr.

43,2

60

(For acquiring 75%)

Non-Controlling Interest

On the Acquisition Date

Fair Value of Net Assets

4,98,9

60

NCI - % 25%

1,24,7

40

Non-Controlling Interest

On 1 July 2018

Fair Value of Net Assets on 1 July 2017 4,98,9

Consideration Paid e

3,30,9

60

Gain on bargain purchase d-e

43,2

60

NCI share of equity - 25%

(a+b+c)*25

%

1,24,7

40

Business Combination Valuation Entries

Land A/c Dr.

22,4

00

Plant A/c Dr.

28,0

00

Inventory A/c Dr.

35,0

00

Accounts receivable A/c Cr.

7,0

00

Goodwill A/c Cr.

5,6

00

Deferred Tax A/c Cr.

21,8

40

Business Combination Valuation Reserve A/c Cr.

50,9

60

Pre-acquisition Entry

Share Capital A/c Dr.

2,10,0

00

General Resrve A/c Dr.

84,0

00

Retained Earnings A/c Dr.

42,0

00

Business Combination Valuation Reserve A/c Dr.

38,2

20

Investment in Clock Ltd. Cr.

3,30,9

60

Gain on Bargain Purchase Cr.

43,2

60

(For acquiring 75%)

Non-Controlling Interest

On the Acquisition Date

Fair Value of Net Assets

4,98,9

60

NCI - % 25%

1,24,7

40

Non-Controlling Interest

On 1 July 2018

Fair Value of Net Assets on 1 July 2017 4,98,9

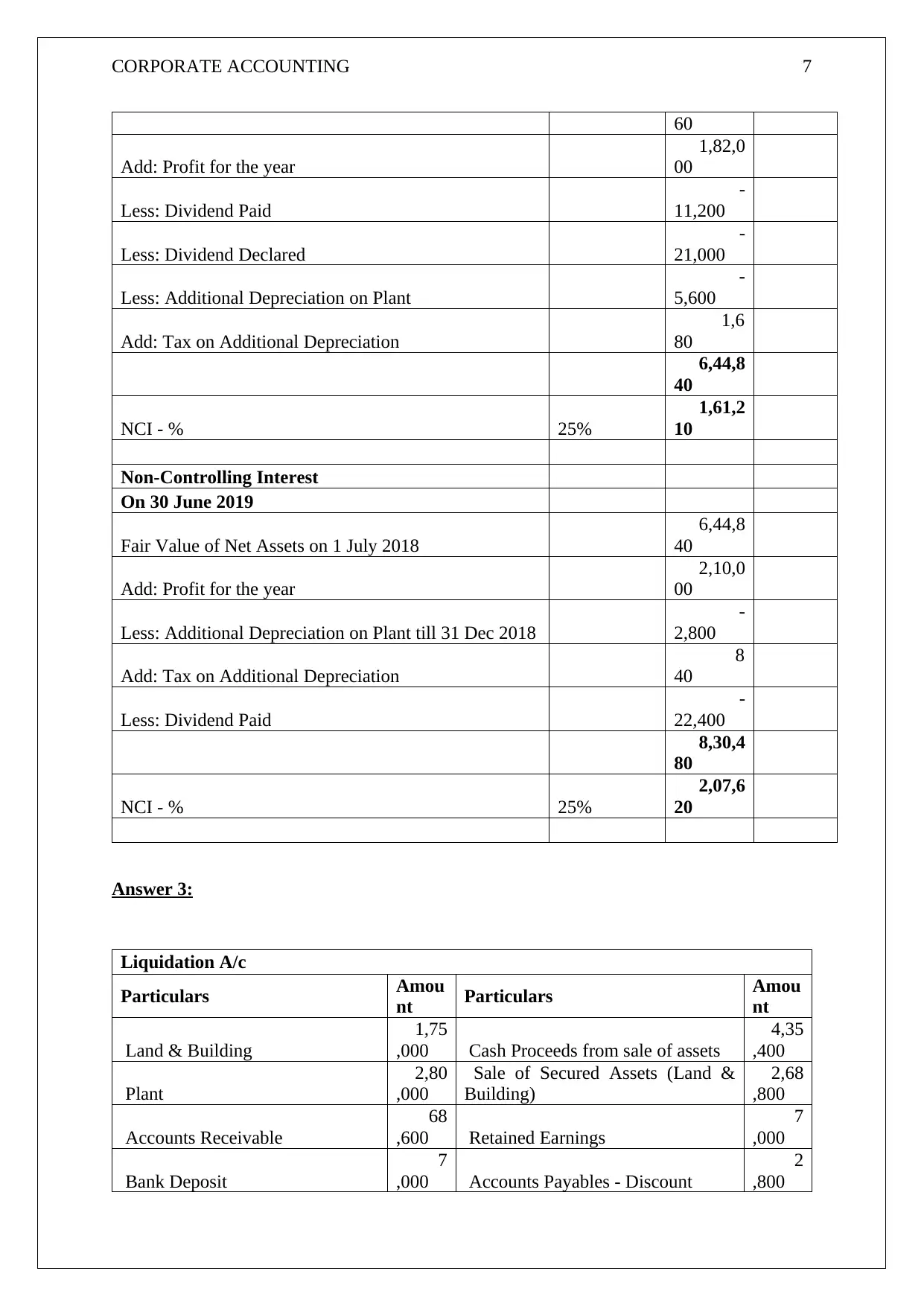

CORPORATE ACCOUNTING 7

60

Add: Profit for the year

1,82,0

00

Less: Dividend Paid

-

11,200

Less: Dividend Declared

-

21,000

Less: Additional Depreciation on Plant

-

5,600

Add: Tax on Additional Depreciation

1,6

80

6,44,8

40

NCI - % 25%

1,61,2

10

Non-Controlling Interest

On 30 June 2019

Fair Value of Net Assets on 1 July 2018

6,44,8

40

Add: Profit for the year

2,10,0

00

Less: Additional Depreciation on Plant till 31 Dec 2018

-

2,800

Add: Tax on Additional Depreciation

8

40

Less: Dividend Paid

-

22,400

8,30,4

80

NCI - % 25%

2,07,6

20

Answer 3:

Liquidation A/c

Particulars Amou

nt Particulars Amou

nt

Land & Building

1,75

,000 Cash Proceeds from sale of assets

4,35

,400

Plant

2,80

,000

Sale of Secured Assets (Land &

Building)

2,68

,800

Accounts Receivable

68

,600 Retained Earnings

7

,000

Bank Deposit

7

,000 Accounts Payables - Discount

2

,800

60

Add: Profit for the year

1,82,0

00

Less: Dividend Paid

-

11,200

Less: Dividend Declared

-

21,000

Less: Additional Depreciation on Plant

-

5,600

Add: Tax on Additional Depreciation

1,6

80

6,44,8

40

NCI - % 25%

1,61,2

10

Non-Controlling Interest

On 30 June 2019

Fair Value of Net Assets on 1 July 2018

6,44,8

40

Add: Profit for the year

2,10,0

00

Less: Additional Depreciation on Plant till 31 Dec 2018

-

2,800

Add: Tax on Additional Depreciation

8

40

Less: Dividend Paid

-

22,400

8,30,4

80

NCI - % 25%

2,07,6

20

Answer 3:

Liquidation A/c

Particulars Amou

nt Particulars Amou

nt

Land & Building

1,75

,000 Cash Proceeds from sale of assets

4,35

,400

Plant

2,80

,000

Sale of Secured Assets (Land &

Building)

2,68

,800

Accounts Receivable

68

,600 Retained Earnings

7

,000

Bank Deposit

7

,000 Accounts Payables - Discount

2

,800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

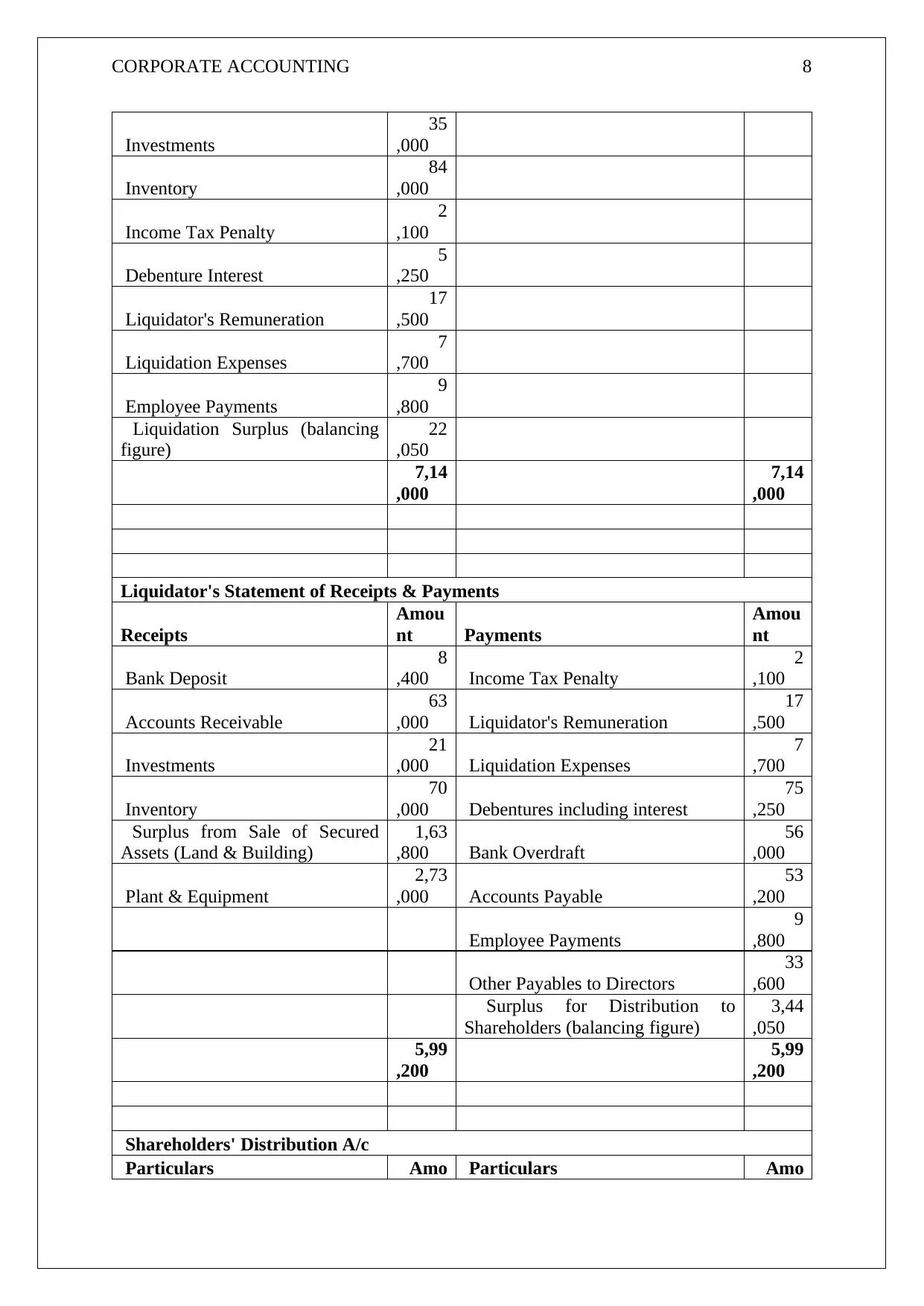

CORPORATE ACCOUNTING 8

Investments

35

,000

Inventory

84

,000

Income Tax Penalty

2

,100

Debenture Interest

5

,250

Liquidator's Remuneration

17

,500

Liquidation Expenses

7

,700

Employee Payments

9

,800

Liquidation Surplus (balancing

figure)

22

,050

7,14

,000

7,14

,000

Liquidator's Statement of Receipts & Payments

Receipts

Amou

nt Payments

Amou

nt

Bank Deposit

8

,400 Income Tax Penalty

2

,100

Accounts Receivable

63

,000 Liquidator's Remuneration

17

,500

Investments

21

,000 Liquidation Expenses

7

,700

Inventory

70

,000 Debentures including interest

75

,250

Surplus from Sale of Secured

Assets (Land & Building)

1,63

,800 Bank Overdraft

56

,000

Plant & Equipment

2,73

,000 Accounts Payable

53

,200

Employee Payments

9

,800

Other Payables to Directors

33

,600

Surplus for Distribution to

Shareholders (balancing figure)

3,44

,050

5,99

,200

5,99

,200

Shareholders' Distribution A/c

Particulars Amo Particulars Amo

Investments

35

,000

Inventory

84

,000

Income Tax Penalty

2

,100

Debenture Interest

5

,250

Liquidator's Remuneration

17

,500

Liquidation Expenses

7

,700

Employee Payments

9

,800

Liquidation Surplus (balancing

figure)

22

,050

7,14

,000

7,14

,000

Liquidator's Statement of Receipts & Payments

Receipts

Amou

nt Payments

Amou

nt

Bank Deposit

8

,400 Income Tax Penalty

2

,100

Accounts Receivable

63

,000 Liquidator's Remuneration

17

,500

Investments

21

,000 Liquidation Expenses

7

,700

Inventory

70

,000 Debentures including interest

75

,250

Surplus from Sale of Secured

Assets (Land & Building)

1,63

,800 Bank Overdraft

56

,000

Plant & Equipment

2,73

,000 Accounts Payable

53

,200

Employee Payments

9

,800

Other Payables to Directors

33

,600

Surplus for Distribution to

Shareholders (balancing figure)

3,44

,050

5,99

,200

5,99

,200

Shareholders' Distribution A/c

Particulars Amo Particulars Amo

CORPORATE ACCOUNTING 9

unt unt

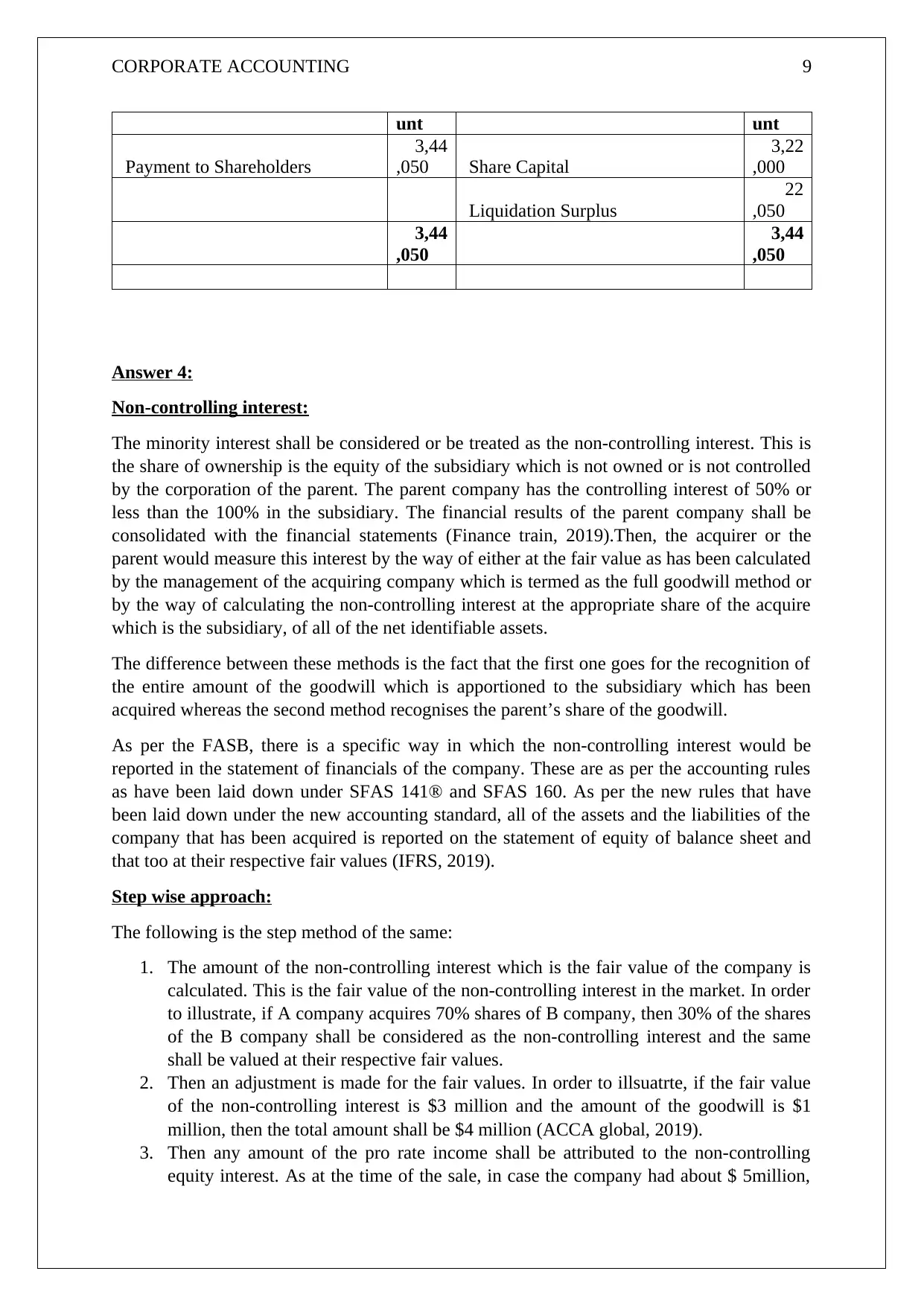

Payment to Shareholders

3,44

,050 Share Capital

3,22

,000

Liquidation Surplus

22

,050

3,44

,050

3,44

,050

Answer 4:

Non-controlling interest:

The minority interest shall be considered or be treated as the non-controlling interest. This is

the share of ownership is the equity of the subsidiary which is not owned or is not controlled

by the corporation of the parent. The parent company has the controlling interest of 50% or

less than the 100% in the subsidiary. The financial results of the parent company shall be

consolidated with the financial statements (Finance train, 2019).Then, the acquirer or the

parent would measure this interest by the way of either at the fair value as has been calculated

by the management of the acquiring company which is termed as the full goodwill method or

by the way of calculating the non-controlling interest at the appropriate share of the acquire

which is the subsidiary, of all of the net identifiable assets.

The difference between these methods is the fact that the first one goes for the recognition of

the entire amount of the goodwill which is apportioned to the subsidiary which has been

acquired whereas the second method recognises the parent’s share of the goodwill.

As per the FASB, there is a specific way in which the non-controlling interest would be

reported in the statement of financials of the company. These are as per the accounting rules

as have been laid down under SFAS 141® and SFAS 160. As per the new rules that have

been laid down under the new accounting standard, all of the assets and the liabilities of the

company that has been acquired is reported on the statement of equity of balance sheet and

that too at their respective fair values (IFRS, 2019).

Step wise approach:

The following is the step method of the same:

1. The amount of the non-controlling interest which is the fair value of the company is

calculated. This is the fair value of the non-controlling interest in the market. In order

to illustrate, if A company acquires 70% shares of B company, then 30% of the shares

of the B company shall be considered as the non-controlling interest and the same

shall be valued at their respective fair values.

2. Then an adjustment is made for the fair values. In order to illsuatrte, if the fair value

of the non-controlling interest is $3 million and the amount of the goodwill is $1

million, then the total amount shall be $4 million (ACCA global, 2019).

3. Then any amount of the pro rate income shall be attributed to the non-controlling

equity interest. As at the time of the sale, in case the company had about $ 5million,

unt unt

Payment to Shareholders

3,44

,050 Share Capital

3,22

,000

Liquidation Surplus

22

,050

3,44

,050

3,44

,050

Answer 4:

Non-controlling interest:

The minority interest shall be considered or be treated as the non-controlling interest. This is

the share of ownership is the equity of the subsidiary which is not owned or is not controlled

by the corporation of the parent. The parent company has the controlling interest of 50% or

less than the 100% in the subsidiary. The financial results of the parent company shall be

consolidated with the financial statements (Finance train, 2019).Then, the acquirer or the

parent would measure this interest by the way of either at the fair value as has been calculated

by the management of the acquiring company which is termed as the full goodwill method or

by the way of calculating the non-controlling interest at the appropriate share of the acquire

which is the subsidiary, of all of the net identifiable assets.

The difference between these methods is the fact that the first one goes for the recognition of

the entire amount of the goodwill which is apportioned to the subsidiary which has been

acquired whereas the second method recognises the parent’s share of the goodwill.

As per the FASB, there is a specific way in which the non-controlling interest would be

reported in the statement of financials of the company. These are as per the accounting rules

as have been laid down under SFAS 141® and SFAS 160. As per the new rules that have

been laid down under the new accounting standard, all of the assets and the liabilities of the

company that has been acquired is reported on the statement of equity of balance sheet and

that too at their respective fair values (IFRS, 2019).

Step wise approach:

The following is the step method of the same:

1. The amount of the non-controlling interest which is the fair value of the company is

calculated. This is the fair value of the non-controlling interest in the market. In order

to illustrate, if A company acquires 70% shares of B company, then 30% of the shares

of the B company shall be considered as the non-controlling interest and the same

shall be valued at their respective fair values.

2. Then an adjustment is made for the fair values. In order to illsuatrte, if the fair value

of the non-controlling interest is $3 million and the amount of the goodwill is $1

million, then the total amount shall be $4 million (ACCA global, 2019).

3. Then any amount of the pro rate income shall be attributed to the non-controlling

equity interest. As at the time of the sale, in case the company had about $ 5million,

CORPORATE ACCOUNTING 10

then any amount of the pro rate share of income for the non- controlling interest shall

be 20% of $ million which is $1 million. This amount shall be added to the above

calculated amount which comes to the total of $12 million.

4. Then any amount of the pro rate or the proportionate shares shall be deducted from

the above calculated amount. For example, if the dividends are $1 million, then the

same would be subtracted from the above fair value which is $12 million less $1

million that comes to be $ 11 million.

5. The above amounts of non-controlling interest of $11 million shall be recorded in the

statement of equity in the consolidated balance sheet of the parent company (Studocu,

2019).

Future years:

For the future years, any amount of profit earned by the company shall be apportioned in the

relevant percentages to the subsidiary company. Suppose, if the non-controlling interest is

20%, and the company after the year of acquisition earns a profit of $100 million, then the

non-controlling share in profit shall be $20 million. The same rule would be followed when

the company pays any amount of dividend to the shareholders. Suppose, if the non-

controlling interest is 20%, and the company after the year of acquisition pays a dividend of

$20 million, then the non-controlling share in profit shall be $4 million. This shall be added

to the non-controlling interest and hence, this amount will keep on increasing.

then any amount of the pro rate share of income for the non- controlling interest shall

be 20% of $ million which is $1 million. This amount shall be added to the above

calculated amount which comes to the total of $12 million.

4. Then any amount of the pro rate or the proportionate shares shall be deducted from

the above calculated amount. For example, if the dividends are $1 million, then the

same would be subtracted from the above fair value which is $12 million less $1

million that comes to be $ 11 million.

5. The above amounts of non-controlling interest of $11 million shall be recorded in the

statement of equity in the consolidated balance sheet of the parent company (Studocu,

2019).

Future years:

For the future years, any amount of profit earned by the company shall be apportioned in the

relevant percentages to the subsidiary company. Suppose, if the non-controlling interest is

20%, and the company after the year of acquisition earns a profit of $100 million, then the

non-controlling share in profit shall be $20 million. The same rule would be followed when

the company pays any amount of dividend to the shareholders. Suppose, if the non-

controlling interest is 20%, and the company after the year of acquisition pays a dividend of

$20 million, then the non-controlling share in profit shall be $4 million. This shall be added

to the non-controlling interest and hence, this amount will keep on increasing.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE ACCOUNTING 11

References:

Accaglobal.com. (2019). IFRS 3 | F7 Financial Reporting | ACCA Qualification | Students |

ACCA Global. [online] Available at: https://www.accaglobal.com/in/en/student/exam-

support-resources/fundamentals-exams-study-resources/f7/technical-articles/

combinations.html [Accessed 4 Oct. 2019].

Finance Train. (2019). Calculation of Non-controlling Interest in Consolidated Financials -

Finance Train. [online] Available at: https://financetrain.com/calculation-of-non-controlling-

interest-in-consolidated-financials/ [Accessed 4 Oct. 2019].

IFRSbox - Making IFRS Easy. (2019). Example: How to Consolidate - IFRSbox - Making

IFRS Easy. [online] Available at: https://www.ifrsbox.com/consolidation-example/ [Accessed

4 Oct. 2019].

www.studocu.com. (2019). Lecture notes, lecture 7 - consolidation: non-controlling interest.

[online] Available at: https://www.studocu.com/en/document/university-of-new-south-

wales/corporate-financial-reporting-and-analysis/lecture-notes/lecture-notes-lecture-7-

consolidation-non-controlling-interest/312784/view [Accessed 4 Oct. 2019].

References:

Accaglobal.com. (2019). IFRS 3 | F7 Financial Reporting | ACCA Qualification | Students |

ACCA Global. [online] Available at: https://www.accaglobal.com/in/en/student/exam-

support-resources/fundamentals-exams-study-resources/f7/technical-articles/

combinations.html [Accessed 4 Oct. 2019].

Finance Train. (2019). Calculation of Non-controlling Interest in Consolidated Financials -

Finance Train. [online] Available at: https://financetrain.com/calculation-of-non-controlling-

interest-in-consolidated-financials/ [Accessed 4 Oct. 2019].

IFRSbox - Making IFRS Easy. (2019). Example: How to Consolidate - IFRSbox - Making

IFRS Easy. [online] Available at: https://www.ifrsbox.com/consolidation-example/ [Accessed

4 Oct. 2019].

www.studocu.com. (2019). Lecture notes, lecture 7 - consolidation: non-controlling interest.

[online] Available at: https://www.studocu.com/en/document/university-of-new-south-

wales/corporate-financial-reporting-and-analysis/lecture-notes/lecture-notes-lecture-7-

consolidation-non-controlling-interest/312784/view [Accessed 4 Oct. 2019].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.