Corporate Finance Report: Valuation Techniques and Financial Analysis

VerifiedAdded on 2022/09/07

|8

|1479

|19

Report

AI Summary

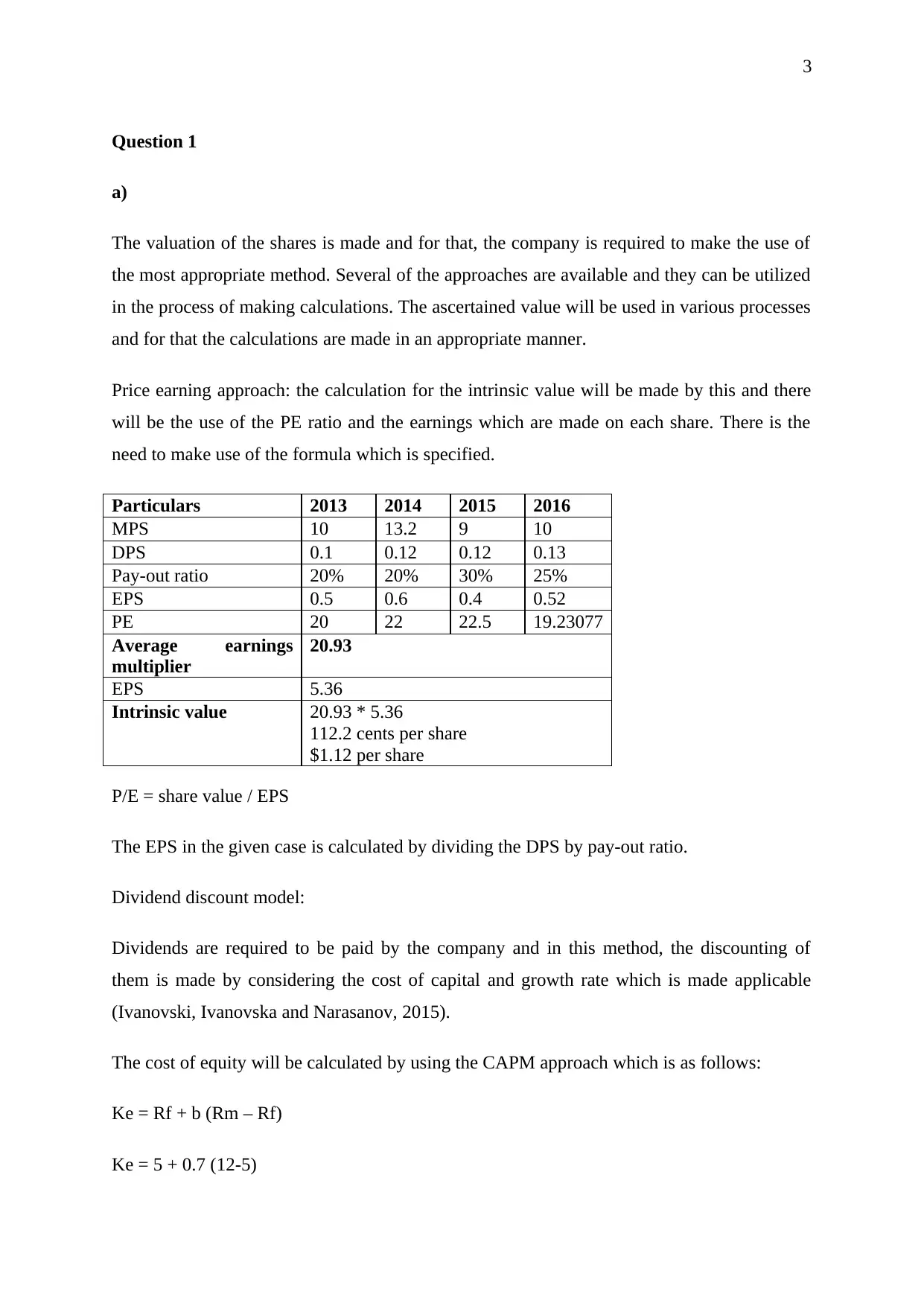

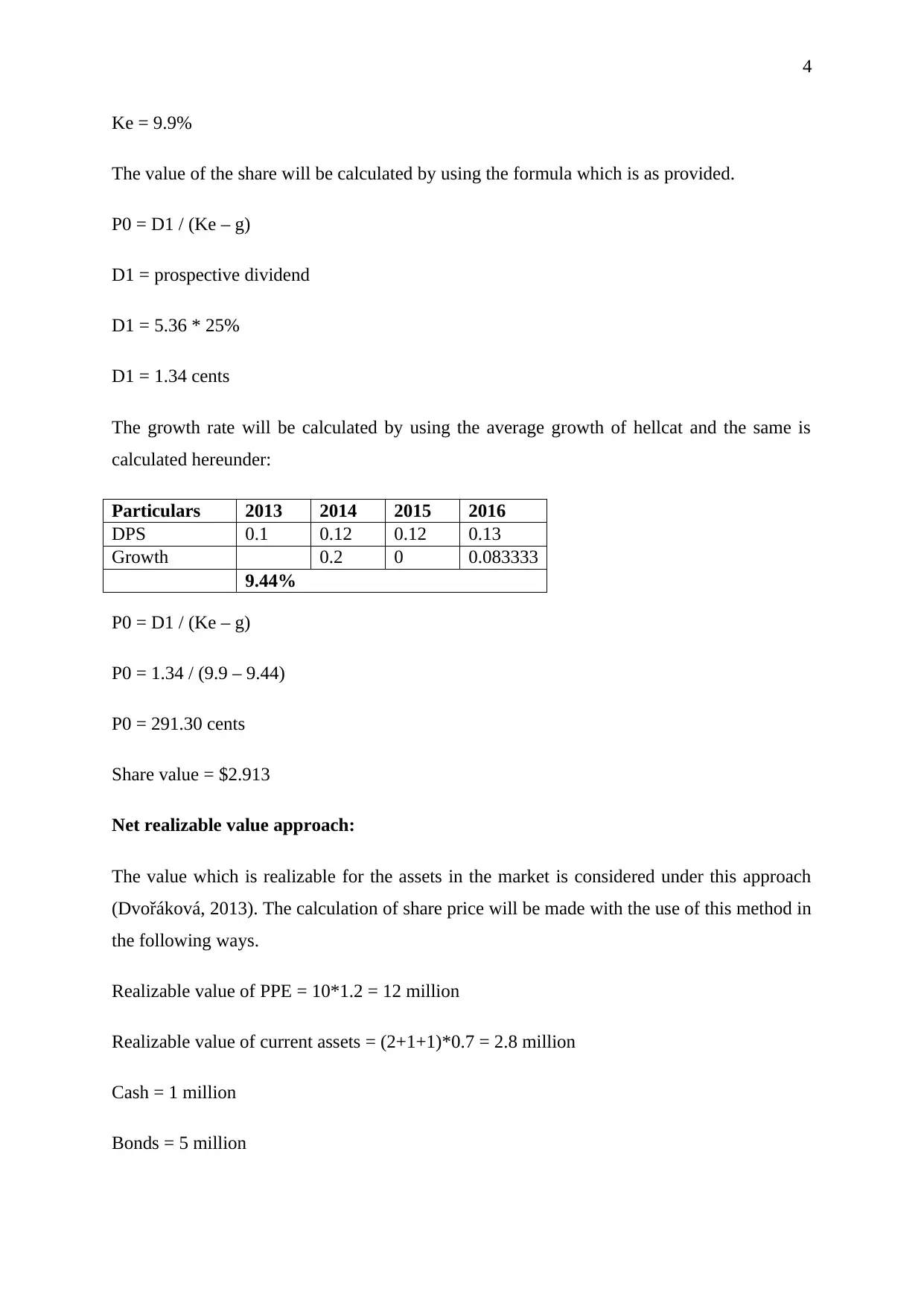

This report provides a detailed analysis of corporate finance, focusing on share valuation techniques. It explores three main approaches: the price earning approach, the dividend discount model, and the net realizable value method. The report calculates intrinsic values using provided financial data, including earnings per share (EPS), dividends per share (DPS), and payout ratios. It also examines the advantages of each valuation method, such as discounted cash flow and equity methods, and evaluates the best approach for decision-making in mergers and acquisitions. The report further analyzes project evaluation using the net present value (NPV) method, considering cash inflows, outflows, tax savings, and salvage values. The analysis includes calculations for capital allowances, tax savings, and net cash flows to determine the project's financial viability. The report references several academic sources to support its findings and conclusions.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.