Taxation System Analysis and Liabilities for Ford Motor PLC Report

VerifiedAdded on 2021/01/01

|13

|3549

|137

Report

AI Summary

This report provides a comprehensive analysis of taxation systems and liabilities, using Ford Motor PLC as a case study. It begins with an introduction to taxation and its significance, followed by an examination of the taxation systems in the UK, US, and Hungary, with a focus on direct and indirect taxes. The report then delves into the taxation liabilities of both unincorporated and incorporated organizations, providing examples and calculations to illustrate the concepts. It explores the advantages and disadvantages of each organizational structure in relation to taxation. The report also covers the personal income tax of Henry Ford, and concludes with an analysis of key legal and ethical constraints on different organizations. The report includes calculations, comparisons, and real-world examples to provide a thorough understanding of the subject matter.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Demonstrating the taxation system which would be effective in governing economic

operations of country in context with Ford Motor PLC..............................................................1

Comparing the taxation system stated in different countries......................................................3

TASK 2............................................................................................................................................4

Exploring the taxation liabilities for unincorporated organisations............................................4

Application of models and formula for interpreting data and determining the taxation

liabilities for unincorporated organisation..................................................................................6

TASK 3............................................................................................................................................7

Exploring the taxation liabilities for incorporated organisation.................................................7

Determining the taxable liabilities for Ford Motor PLC.............................................................8

TASK 4............................................................................................................................................8

Analysing the key legal and ethical constraints on different organisations................................8

Application of Key legal and ethical constraints......................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Demonstrating the taxation system which would be effective in governing economic

operations of country in context with Ford Motor PLC..............................................................1

Comparing the taxation system stated in different countries......................................................3

TASK 2............................................................................................................................................4

Exploring the taxation liabilities for unincorporated organisations............................................4

Application of models and formula for interpreting data and determining the taxation

liabilities for unincorporated organisation..................................................................................6

TASK 3............................................................................................................................................7

Exploring the taxation liabilities for incorporated organisation.................................................7

Determining the taxable liabilities for Ford Motor PLC.............................................................8

TASK 4............................................................................................................................................8

Analysing the key legal and ethical constraints on different organisations................................8

Application of Key legal and ethical constraints......................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Taxation is a method through which a legislative authority in any economy levy taxes on

the income generated by a person or a corporation. It helps in bringing stability in the economy

as per generating appropriate amount for reserves and revenue through taxable collection. In the

present report, there will be discussion based on taxation system and policies which have been

adopted and governed by various countries such as UK, US and Hungary. In context with the

case scenario of Ford Motor PLC (an automotive industry) on which there has been

ascertainment of taxable income of Henry ford as per income tax as well as corporate tax of the

organisation. This assignment will achieve information regarding the taxation liabilities for the

unincorporated and incorporate organisations as well as demonstrate the legal and ethical

environment of various countries as per considering the taxation.

TASK 1 - Demonstrating the taxation system which would be effective in governing

economic operations of country in context with Ford Motor PLC

Introduction to Ford Motor PLC:

Ford is a multinational Automotive industry and have been headquartered in Dearborn,

Michigan. The company is being engaged in producing the large number of automotive designs

which includes luxury cars, SUV, Hatchback etc. It has been operating in many nations and have

employees more than 213,000. Moreover, in the present report, there will be analysis over the

taxation system adopted by the branches of Ford in Hungry, UK and US.

Taxation and taxation system (direct and indirect):

Taxation is the compulsory levy of charges on the income and profits generated by

corporation which have been collected by the government. However, the motive behind such tax

collection is basically for generating the revenue, reserves and funds for utilising in developing

the economy as well as directing the operational growth of the economy.

On the other side, in relation with considering the taxation system in any nation there

have been influences of various charges which were being levied on the purchase and sales of

products and services as well as revenue generated by the professionals for making adequate

ascertainment of profitable gains (von Ehrlich and Radulescu, 2017). These are being classified

1

Taxation is a method through which a legislative authority in any economy levy taxes on

the income generated by a person or a corporation. It helps in bringing stability in the economy

as per generating appropriate amount for reserves and revenue through taxable collection. In the

present report, there will be discussion based on taxation system and policies which have been

adopted and governed by various countries such as UK, US and Hungary. In context with the

case scenario of Ford Motor PLC (an automotive industry) on which there has been

ascertainment of taxable income of Henry ford as per income tax as well as corporate tax of the

organisation. This assignment will achieve information regarding the taxation liabilities for the

unincorporated and incorporate organisations as well as demonstrate the legal and ethical

environment of various countries as per considering the taxation.

TASK 1 - Demonstrating the taxation system which would be effective in governing

economic operations of country in context with Ford Motor PLC

Introduction to Ford Motor PLC:

Ford is a multinational Automotive industry and have been headquartered in Dearborn,

Michigan. The company is being engaged in producing the large number of automotive designs

which includes luxury cars, SUV, Hatchback etc. It has been operating in many nations and have

employees more than 213,000. Moreover, in the present report, there will be analysis over the

taxation system adopted by the branches of Ford in Hungry, UK and US.

Taxation and taxation system (direct and indirect):

Taxation is the compulsory levy of charges on the income and profits generated by

corporation which have been collected by the government. However, the motive behind such tax

collection is basically for generating the revenue, reserves and funds for utilising in developing

the economy as well as directing the operational growth of the economy.

On the other side, in relation with considering the taxation system in any nation there

have been influences of various charges which were being levied on the purchase and sales of

products and services as well as revenue generated by the professionals for making adequate

ascertainment of profitable gains (von Ehrlich and Radulescu, 2017). These are being classified

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in direct and indirect charges levied on the income such as Sales tax, value added tax, inheritance

tax, income tax, corporate tax, national insurance cover etc.

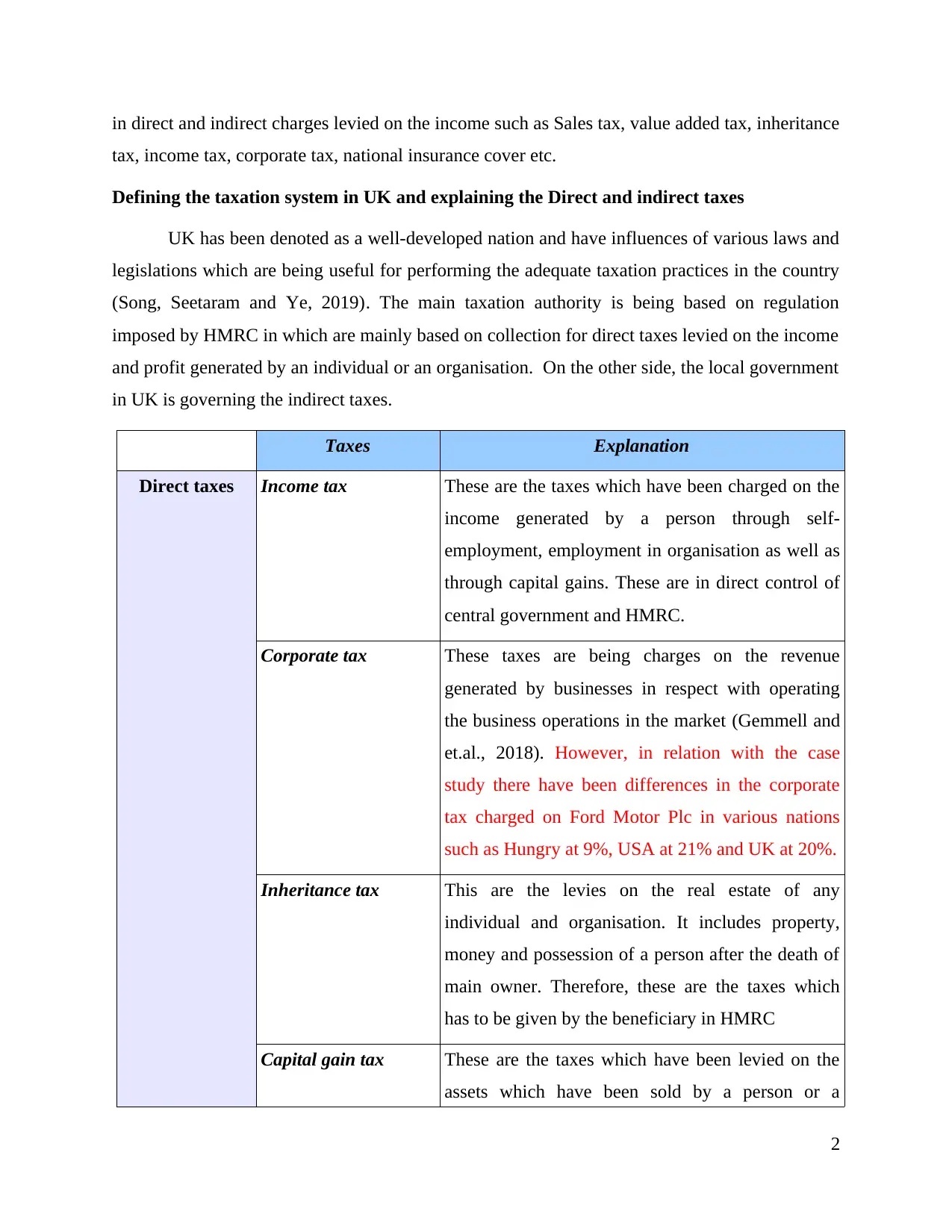

Defining the taxation system in UK and explaining the Direct and indirect taxes

UK has been denoted as a well-developed nation and have influences of various laws and

legislations which are being useful for performing the adequate taxation practices in the country

(Song, Seetaram and Ye, 2019). The main taxation authority is being based on regulation

imposed by HMRC in which are mainly based on collection for direct taxes levied on the income

and profit generated by an individual or an organisation. On the other side, the local government

in UK is governing the indirect taxes.

Taxes Explanation

Direct taxes Income tax These are the taxes which have been charged on the

income generated by a person through self-

employment, employment in organisation as well as

through capital gains. These are in direct control of

central government and HMRC.

Corporate tax These taxes are being charges on the revenue

generated by businesses in respect with operating

the business operations in the market (Gemmell and

et.al., 2018). However, in relation with the case

study there have been differences in the corporate

tax charged on Ford Motor Plc in various nations

such as Hungry at 9%, USA at 21% and UK at 20%.

Inheritance tax This are the levies on the real estate of any

individual and organisation. It includes property,

money and possession of a person after the death of

main owner. Therefore, these are the taxes which

has to be given by the beneficiary in HMRC

Capital gain tax These are the taxes which have been levied on the

assets which have been sold by a person or a

2

tax, income tax, corporate tax, national insurance cover etc.

Defining the taxation system in UK and explaining the Direct and indirect taxes

UK has been denoted as a well-developed nation and have influences of various laws and

legislations which are being useful for performing the adequate taxation practices in the country

(Song, Seetaram and Ye, 2019). The main taxation authority is being based on regulation

imposed by HMRC in which are mainly based on collection for direct taxes levied on the income

and profit generated by an individual or an organisation. On the other side, the local government

in UK is governing the indirect taxes.

Taxes Explanation

Direct taxes Income tax These are the taxes which have been charged on the

income generated by a person through self-

employment, employment in organisation as well as

through capital gains. These are in direct control of

central government and HMRC.

Corporate tax These taxes are being charges on the revenue

generated by businesses in respect with operating

the business operations in the market (Gemmell and

et.al., 2018). However, in relation with the case

study there have been differences in the corporate

tax charged on Ford Motor Plc in various nations

such as Hungry at 9%, USA at 21% and UK at 20%.

Inheritance tax This are the levies on the real estate of any

individual and organisation. It includes property,

money and possession of a person after the death of

main owner. Therefore, these are the taxes which

has to be given by the beneficiary in HMRC

Capital gain tax These are the taxes which have been levied on the

assets which have been sold by a person or a

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

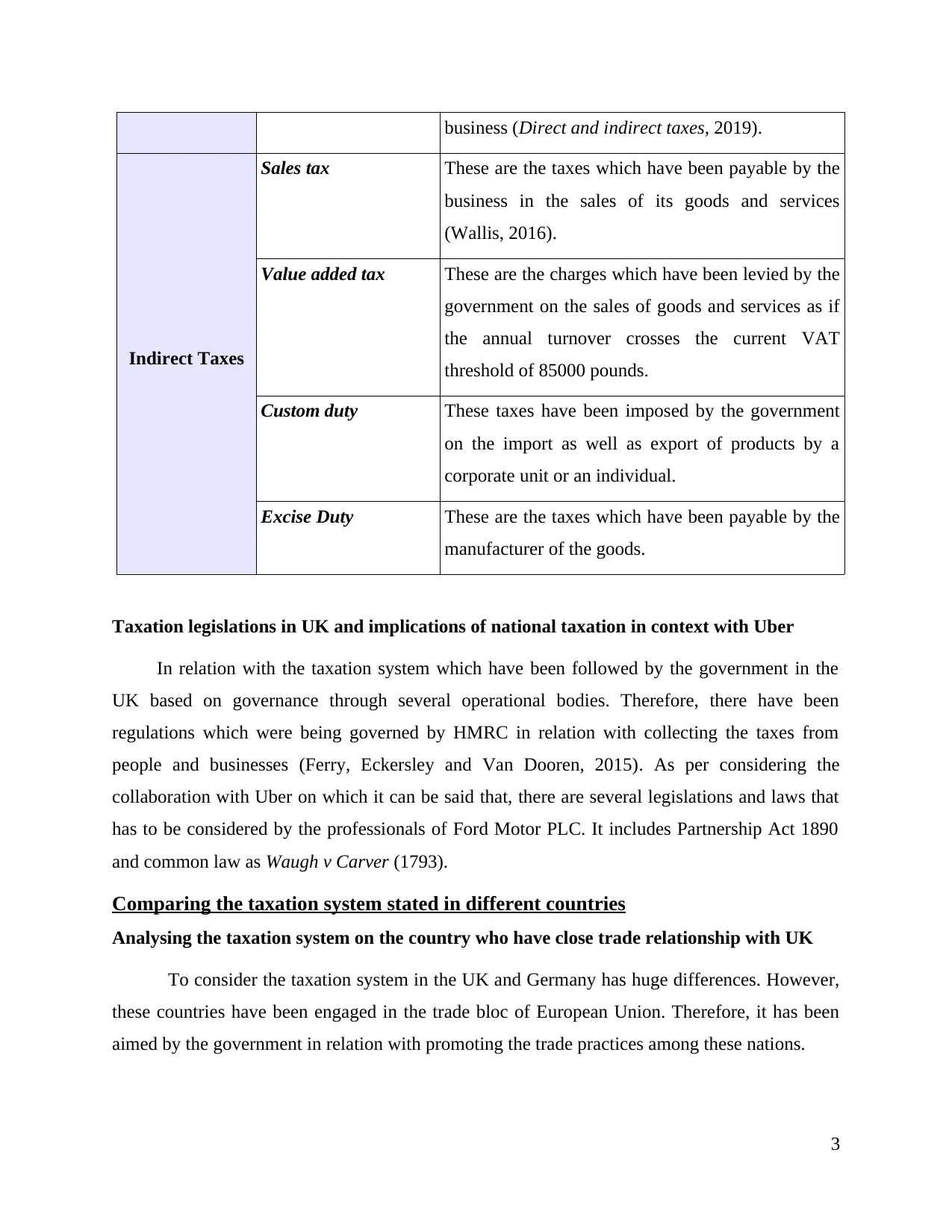

business (Direct and indirect taxes, 2019).

Indirect Taxes

Sales tax These are the taxes which have been payable by the

business in the sales of its goods and services

(Wallis, 2016).

Value added tax These are the charges which have been levied by the

government on the sales of goods and services as if

the annual turnover crosses the current VAT

threshold of 85000 pounds.

Custom duty These taxes have been imposed by the government

on the import as well as export of products by a

corporate unit or an individual.

Excise Duty These are the taxes which have been payable by the

manufacturer of the goods.

Taxation legislations in UK and implications of national taxation in context with Uber

In relation with the taxation system which have been followed by the government in the

UK based on governance through several operational bodies. Therefore, there have been

regulations which were being governed by HMRC in relation with collecting the taxes from

people and businesses (Ferry, Eckersley and Van Dooren, 2015). As per considering the

collaboration with Uber on which it can be said that, there are several legislations and laws that

has to be considered by the professionals of Ford Motor PLC. It includes Partnership Act 1890

and common law as Waugh v Carver (1793).

Comparing the taxation system stated in different countries

Analysing the taxation system on the country who have close trade relationship with UK

To consider the taxation system in the UK and Germany has huge differences. However,

these countries have been engaged in the trade bloc of European Union. Therefore, it has been

aimed by the government in relation with promoting the trade practices among these nations.

3

Indirect Taxes

Sales tax These are the taxes which have been payable by the

business in the sales of its goods and services

(Wallis, 2016).

Value added tax These are the charges which have been levied by the

government on the sales of goods and services as if

the annual turnover crosses the current VAT

threshold of 85000 pounds.

Custom duty These taxes have been imposed by the government

on the import as well as export of products by a

corporate unit or an individual.

Excise Duty These are the taxes which have been payable by the

manufacturer of the goods.

Taxation legislations in UK and implications of national taxation in context with Uber

In relation with the taxation system which have been followed by the government in the

UK based on governance through several operational bodies. Therefore, there have been

regulations which were being governed by HMRC in relation with collecting the taxes from

people and businesses (Ferry, Eckersley and Van Dooren, 2015). As per considering the

collaboration with Uber on which it can be said that, there are several legislations and laws that

has to be considered by the professionals of Ford Motor PLC. It includes Partnership Act 1890

and common law as Waugh v Carver (1793).

Comparing the taxation system stated in different countries

Analysing the taxation system on the country who have close trade relationship with UK

To consider the taxation system in the UK and Germany has huge differences. However,

these countries have been engaged in the trade bloc of European Union. Therefore, it has been

aimed by the government in relation with promoting the trade practices among these nations.

3

Taxation in Germany have been levied by the federal, state and municipal government

which are in context with managing the taxation legislations and operational determination

(McKee, Muir and Moore, 2017). In accordance with the trade bloc and other consequences on

which it can be said that Germany has been denoted as the safest tax heaven as ranked 8th in

world.

Defining the interrelationship between two taxation system which are operating in the two

countries in context of Ford Motor PLC

However, Ford have been operating in UK has the main automotive manufacturer.

Therefore, as if it has its business operated in Germany that there will be various benefits to the

company (Egger and et.al., 2015). As per considering the European union group on which it can

be said that there are various benefits such as less taxes will be payable by the parties which are

being engaged in the trade practices such as excise duty, custom duty etc.

TASK 2 - Exploring the taxation liabilities for unincorporated organisations

Unincorporated organisation: These are the industries which have been set-up by the

group of individuals on the basis of a contractual agreement (Thiel and Wenner, 2018).

However, they are not being registered as a corporate unit as people are operating the activities

on the basis of voluntary group such as Sports club, charity etc. For example: Oxfam have been

operating activities such as Committee for Famine Relief as a charity business in UK.

Characteristics and background

Oxfam has been working as the independent charitable organisation focusing on

alleviation in global poverty which was being founded in 1942. Therefore, it has been denoted as

the major non-profit group which is basically based on bringing the famine relief (Gujarathi and

Comerford, 2016). However, as per considering the characteristics of Oxfam UK which can be

analysed such as:

The right to a sustainable livelihood

4

which are in context with managing the taxation legislations and operational determination

(McKee, Muir and Moore, 2017). In accordance with the trade bloc and other consequences on

which it can be said that Germany has been denoted as the safest tax heaven as ranked 8th in

world.

Defining the interrelationship between two taxation system which are operating in the two

countries in context of Ford Motor PLC

However, Ford have been operating in UK has the main automotive manufacturer.

Therefore, as if it has its business operated in Germany that there will be various benefits to the

company (Egger and et.al., 2015). As per considering the European union group on which it can

be said that there are various benefits such as less taxes will be payable by the parties which are

being engaged in the trade practices such as excise duty, custom duty etc.

TASK 2 - Exploring the taxation liabilities for unincorporated organisations

Unincorporated organisation: These are the industries which have been set-up by the

group of individuals on the basis of a contractual agreement (Thiel and Wenner, 2018).

However, they are not being registered as a corporate unit as people are operating the activities

on the basis of voluntary group such as Sports club, charity etc. For example: Oxfam have been

operating activities such as Committee for Famine Relief as a charity business in UK.

Characteristics and background

Oxfam has been working as the independent charitable organisation focusing on

alleviation in global poverty which was being founded in 1942. Therefore, it has been denoted as

the major non-profit group which is basically based on bringing the famine relief (Gujarathi and

Comerford, 2016). However, as per considering the characteristics of Oxfam UK which can be

analysed such as:

The right to a sustainable livelihood

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The right to basic social services

The right to life and security

The right to be heard

The right to an identity.

Advantages and disadvantages of unincorporated

Advantages:

These are simple, cheap and no restrictions on setting up the business.

There will not be any influences of the politics and campaigning activities.

As the company is not being registered as the corporation that there are less liabilities to

such businesses.

Disadvantages:

They cannot own any property on its own right in the business operations.

There has been equal responsibility for the group’s obligations, liable and debts.

Personal taxation and taxation relating to sole trader and partnership:

Personal taxation has been payable on the income and revenue generated through the

personal sources (Vijver, 2015). However, revenue have been gathered by an individual which

would be effective and adequate in relation with making the adequate operational changes.

Sole trader: Is the person who governs business on the basis of own efforts, planning and

financial implications (von Ehrlich and Radulescu, 2017). Thus, these are the owners who

usually owns a small business enterprise. In accordance with the taxation consequences on which

it can be said that, they are exempted to make taxable payments.

Partnership: the ownership has been divided among the two or more individual which are

operating business activities (Song, Seetaram and Ye, 2019). Thus, the taxes have been charges

over their personal income which is relevant with the share of their investment in the business.

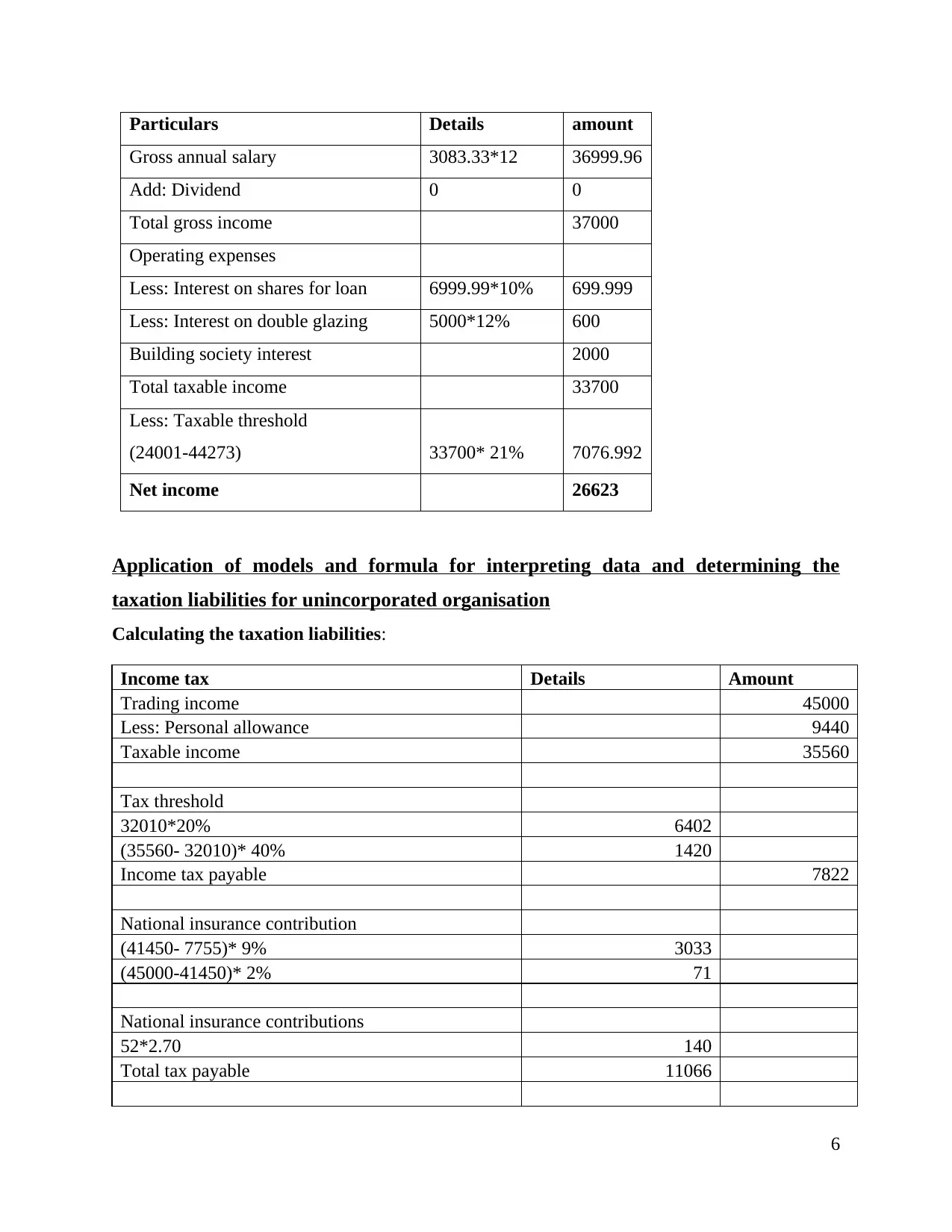

Personal income of Henry Ford:

5

The right to life and security

The right to be heard

The right to an identity.

Advantages and disadvantages of unincorporated

Advantages:

These are simple, cheap and no restrictions on setting up the business.

There will not be any influences of the politics and campaigning activities.

As the company is not being registered as the corporation that there are less liabilities to

such businesses.

Disadvantages:

They cannot own any property on its own right in the business operations.

There has been equal responsibility for the group’s obligations, liable and debts.

Personal taxation and taxation relating to sole trader and partnership:

Personal taxation has been payable on the income and revenue generated through the

personal sources (Vijver, 2015). However, revenue have been gathered by an individual which

would be effective and adequate in relation with making the adequate operational changes.

Sole trader: Is the person who governs business on the basis of own efforts, planning and

financial implications (von Ehrlich and Radulescu, 2017). Thus, these are the owners who

usually owns a small business enterprise. In accordance with the taxation consequences on which

it can be said that, they are exempted to make taxable payments.

Partnership: the ownership has been divided among the two or more individual which are

operating business activities (Song, Seetaram and Ye, 2019). Thus, the taxes have been charges

over their personal income which is relevant with the share of their investment in the business.

Personal income of Henry Ford:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Details amount

Gross annual salary 3083.33*12 36999.96

Add: Dividend 0 0

Total gross income 37000

Operating expenses

Less: Interest on shares for loan 6999.99*10% 699.999

Less: Interest on double glazing 5000*12% 600

Building society interest 2000

Total taxable income 33700

Less: Taxable threshold

(24001-44273) 33700* 21% 7076.992

Net income 26623

Application of models and formula for interpreting data and determining the

taxation liabilities for unincorporated organisation

Calculating the taxation liabilities:

Income tax Details Amount

Trading income 45000

Less: Personal allowance 9440

Taxable income 35560

Tax threshold

32010*20% 6402

(35560- 32010)* 40% 1420

Income tax payable 7822

National insurance contribution

(41450- 7755)* 9% 3033

(45000-41450)* 2% 71

National insurance contributions

52*2.70 140

Total tax payable 11066

6

Gross annual salary 3083.33*12 36999.96

Add: Dividend 0 0

Total gross income 37000

Operating expenses

Less: Interest on shares for loan 6999.99*10% 699.999

Less: Interest on double glazing 5000*12% 600

Building society interest 2000

Total taxable income 33700

Less: Taxable threshold

(24001-44273) 33700* 21% 7076.992

Net income 26623

Application of models and formula for interpreting data and determining the

taxation liabilities for unincorporated organisation

Calculating the taxation liabilities:

Income tax Details Amount

Trading income 45000

Less: Personal allowance 9440

Taxable income 35560

Tax threshold

32010*20% 6402

(35560- 32010)* 40% 1420

Income tax payable 7822

National insurance contribution

(41450- 7755)* 9% 3033

(45000-41450)* 2% 71

National insurance contributions

52*2.70 140

Total tax payable 11066

6

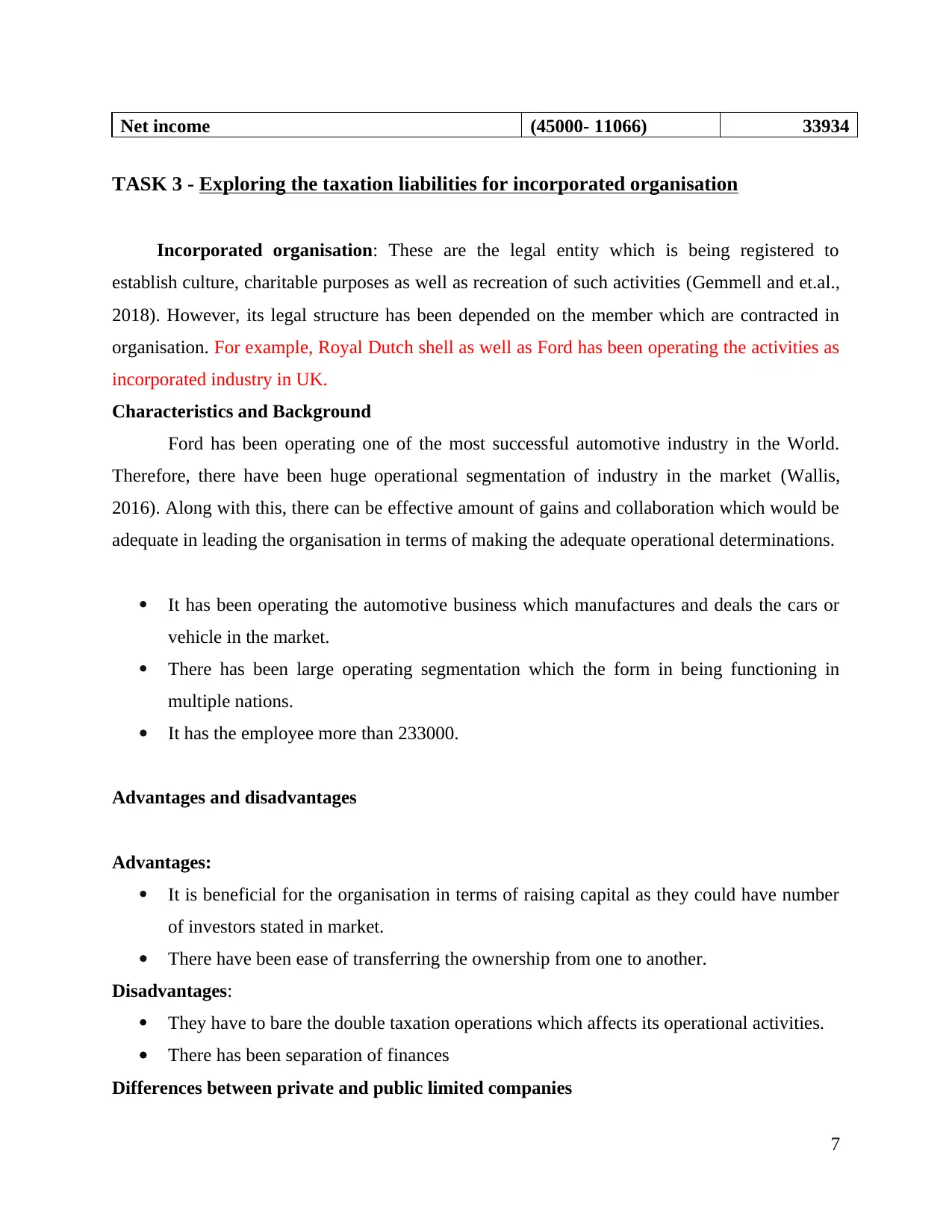

Net income (45000- 11066) 33934

TASK 3 - Exploring the taxation liabilities for incorporated organisation

Incorporated organisation: These are the legal entity which is being registered to

establish culture, charitable purposes as well as recreation of such activities (Gemmell and et.al.,

2018). However, its legal structure has been depended on the member which are contracted in

organisation. For example, Royal Dutch shell as well as Ford has been operating the activities as

incorporated industry in UK.

Characteristics and Background

Ford has been operating one of the most successful automotive industry in the World.

Therefore, there have been huge operational segmentation of industry in the market (Wallis,

2016). Along with this, there can be effective amount of gains and collaboration which would be

adequate in leading the organisation in terms of making the adequate operational determinations.

It has been operating the automotive business which manufactures and deals the cars or

vehicle in the market.

There has been large operating segmentation which the form in being functioning in

multiple nations.

It has the employee more than 233000.

Advantages and disadvantages

Advantages:

It is beneficial for the organisation in terms of raising capital as they could have number

of investors stated in market.

There have been ease of transferring the ownership from one to another.

Disadvantages:

They have to bare the double taxation operations which affects its operational activities.

There has been separation of finances

Differences between private and public limited companies

7

TASK 3 - Exploring the taxation liabilities for incorporated organisation

Incorporated organisation: These are the legal entity which is being registered to

establish culture, charitable purposes as well as recreation of such activities (Gemmell and et.al.,

2018). However, its legal structure has been depended on the member which are contracted in

organisation. For example, Royal Dutch shell as well as Ford has been operating the activities as

incorporated industry in UK.

Characteristics and Background

Ford has been operating one of the most successful automotive industry in the World.

Therefore, there have been huge operational segmentation of industry in the market (Wallis,

2016). Along with this, there can be effective amount of gains and collaboration which would be

adequate in leading the organisation in terms of making the adequate operational determinations.

It has been operating the automotive business which manufactures and deals the cars or

vehicle in the market.

There has been large operating segmentation which the form in being functioning in

multiple nations.

It has the employee more than 233000.

Advantages and disadvantages

Advantages:

It is beneficial for the organisation in terms of raising capital as they could have number

of investors stated in market.

There have been ease of transferring the ownership from one to another.

Disadvantages:

They have to bare the double taxation operations which affects its operational activities.

There has been separation of finances

Differences between private and public limited companies

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

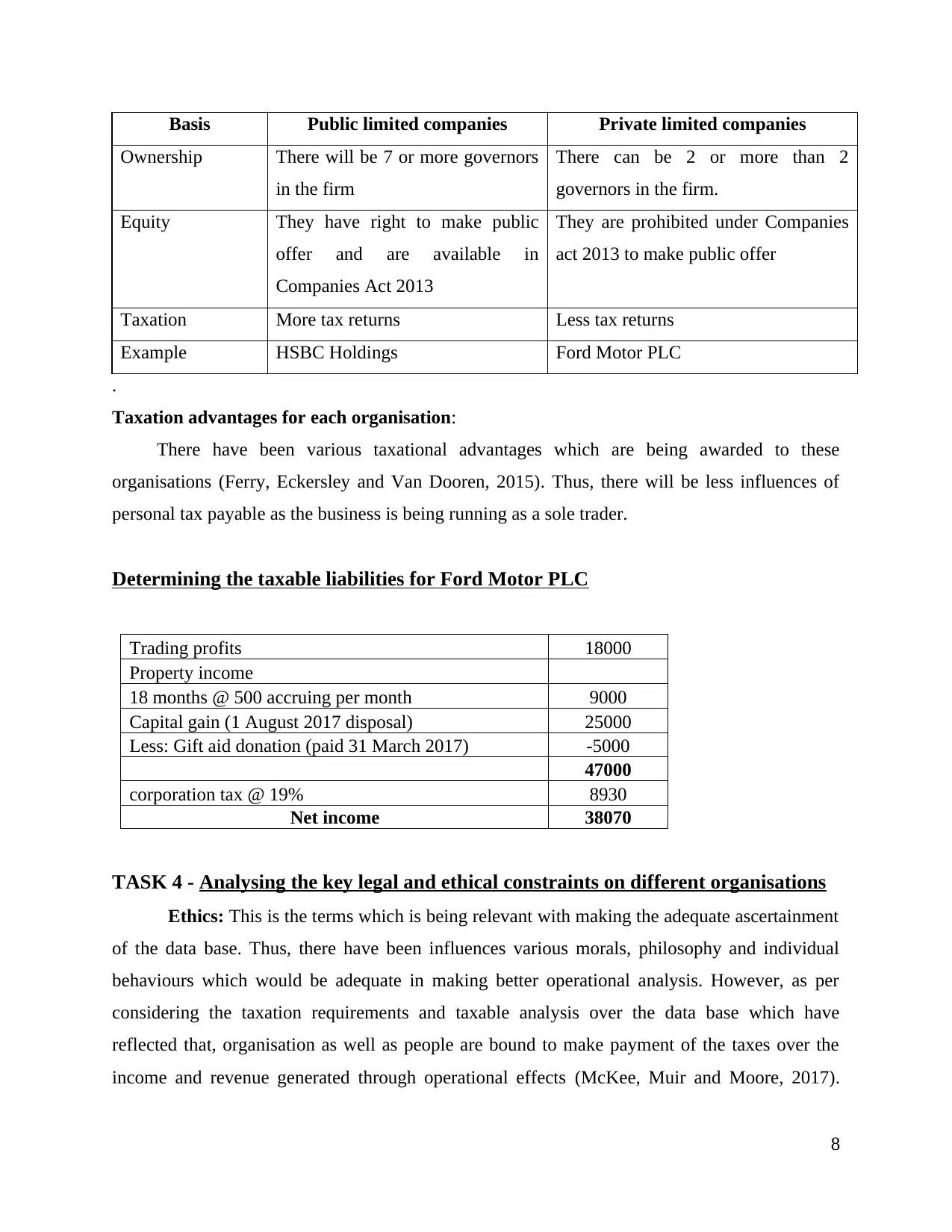

Basis Public limited companies Private limited companies

Ownership There will be 7 or more governors

in the firm

There can be 2 or more than 2

governors in the firm.

Equity They have right to make public

offer and are available in

Companies Act 2013

They are prohibited under Companies

act 2013 to make public offer

Taxation More tax returns Less tax returns

Example HSBC Holdings Ford Motor PLC

.

Taxation advantages for each organisation:

There have been various taxational advantages which are being awarded to these

organisations (Ferry, Eckersley and Van Dooren, 2015). Thus, there will be less influences of

personal tax payable as the business is being running as a sole trader.

Determining the taxable liabilities for Ford Motor PLC

Trading profits 18000

Property income

18 months @ 500 accruing per month 9000

Capital gain (1 August 2017 disposal) 25000

Less: Gift aid donation (paid 31 March 2017) -5000

47000

corporation tax @ 19% 8930

Net income 38070

TASK 4 - Analysing the key legal and ethical constraints on different organisations

Ethics: This is the terms which is being relevant with making the adequate ascertainment

of the data base. Thus, there have been influences various morals, philosophy and individual

behaviours which would be adequate in making better operational analysis. However, as per

considering the taxation requirements and taxable analysis over the data base which have

reflected that, organisation as well as people are bound to make payment of the taxes over the

income and revenue generated through operational effects (McKee, Muir and Moore, 2017).

8

Ownership There will be 7 or more governors

in the firm

There can be 2 or more than 2

governors in the firm.

Equity They have right to make public

offer and are available in

Companies Act 2013

They are prohibited under Companies

act 2013 to make public offer

Taxation More tax returns Less tax returns

Example HSBC Holdings Ford Motor PLC

.

Taxation advantages for each organisation:

There have been various taxational advantages which are being awarded to these

organisations (Ferry, Eckersley and Van Dooren, 2015). Thus, there will be less influences of

personal tax payable as the business is being running as a sole trader.

Determining the taxable liabilities for Ford Motor PLC

Trading profits 18000

Property income

18 months @ 500 accruing per month 9000

Capital gain (1 August 2017 disposal) 25000

Less: Gift aid donation (paid 31 March 2017) -5000

47000

corporation tax @ 19% 8930

Net income 38070

TASK 4 - Analysing the key legal and ethical constraints on different organisations

Ethics: This is the terms which is being relevant with making the adequate ascertainment

of the data base. Thus, there have been influences various morals, philosophy and individual

behaviours which would be adequate in making better operational analysis. However, as per

considering the taxation requirements and taxable analysis over the data base which have

reflected that, organisation as well as people are bound to make payment of the taxes over the

income and revenue generated through operational effects (McKee, Muir and Moore, 2017).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Thus, timely paying income tax return would be adequate in making appropriate operational

ascertainment.

Nation to nation differences: As per considering the differences in the culture, environment as

well as governmental policies there have been changes in the operational techniques to operate

the business activities.

Taxation in Germany have been governed by Federal, state and municipalities

government. Thus, the motive is for developing the country in retaining the adequate operational

success (Egger and et.al., 2015). In UK there are collection of taxes based on the guidelines

presented under the HMRC customs.

Ethical constraints applied across different culture

There have been differences in the culture, social, economy and environment in each

nation which incurred changes and variation in the policies and performance of nation. Thus,

ethical constraint is based on bounding society to follow a norm to follow or behave accordingly

(Thiel and Wenner, 2018). Therefore, there have been various rules and regulation which are

being stated by the government revenant with taxation, fees, charges, rules for traffic, businesses

etc. that governs the society in following the right direction.

Impact of key legal and ethical constraints on different organisation:

Incorporated: As per considering the ethics which are required to be implicated in the

incorporate business regrading taxation and business policies (Gujarathi and Comerford, 2016).

It includes Honesty, integrity, loyalty, fairness, law abiding etc. For example, Ford Motor PLC

have been bound to represent the clear and accurate information regarding the income and

taxable consequences of the business.

Unincorporated: Ethical constraints for the unincorporated business is for making

adequate operational determination which would be effective in leading the firm in operating

various activities (Vijver, 2015). Oxfam have been liable to represent the data base such as

revenue generated by them, expenses incurred during operations etc.

Application of Key legal and ethical constraints

Legal and ethical constraints: A company is legally bound to disclose the income and

revenue generated by them through operational practices (von Ehrlich and Radulescu, 2017).

9

ascertainment.

Nation to nation differences: As per considering the differences in the culture, environment as

well as governmental policies there have been changes in the operational techniques to operate

the business activities.

Taxation in Germany have been governed by Federal, state and municipalities

government. Thus, the motive is for developing the country in retaining the adequate operational

success (Egger and et.al., 2015). In UK there are collection of taxes based on the guidelines

presented under the HMRC customs.

Ethical constraints applied across different culture

There have been differences in the culture, social, economy and environment in each

nation which incurred changes and variation in the policies and performance of nation. Thus,

ethical constraint is based on bounding society to follow a norm to follow or behave accordingly

(Thiel and Wenner, 2018). Therefore, there have been various rules and regulation which are

being stated by the government revenant with taxation, fees, charges, rules for traffic, businesses

etc. that governs the society in following the right direction.

Impact of key legal and ethical constraints on different organisation:

Incorporated: As per considering the ethics which are required to be implicated in the

incorporate business regrading taxation and business policies (Gujarathi and Comerford, 2016).

It includes Honesty, integrity, loyalty, fairness, law abiding etc. For example, Ford Motor PLC

have been bound to represent the clear and accurate information regarding the income and

taxable consequences of the business.

Unincorporated: Ethical constraints for the unincorporated business is for making

adequate operational determination which would be effective in leading the firm in operating

various activities (Vijver, 2015). Oxfam have been liable to represent the data base such as

revenue generated by them, expenses incurred during operations etc.

Application of Key legal and ethical constraints

Legal and ethical constraints: A company is legally bound to disclose the income and

revenue generated by them through operational practices (von Ehrlich and Radulescu, 2017).

9

However, these are the rems which would be effective and adequate in relation with following all

the laws, rules and regulations imposed at regional, national as well as international level. Along

with this, as per considering the taxable liabilities of an organisation. This is an ethical

requirement in an entity which defines the roles of business towards the society. Paying taxes on

the generated revenue to the government would have positive impact of economic development.

Application of different business formatted to individual: There have been application of

various ethic such as recoding the transaction, disclosing the income generated over a period as

well as expenses incurred (Song, Seetaram and Ye, 2019). It funnels the government as well as

investors in terms of analysing the profitability of the organisation as well as duty of following

the legal requirement at the right time.

Compliance requirements: An organisation is being liable to make the adequate taxable

consequences ion which they would have made operational analysis over recording of

transaction, reporting the information regarding the income as well as determining the role of

organisation in relation with collecting the taxes (Gemmell and et.al., 2018).

CONCLUSION

On the basis of above report, on which it can be said that there have been various methods

through which organisation makes taxable payments. It has been counted in the ethics for the

organisations as well as for the individual living in different countries. Thus, making taxable

payment will be adequate in terms of bringing the better gains to the organisation. Report have

covered all the required analysis based on taxation consequences, fair taxation policies, as well

as ethical constraints to be followed by companies in an economy were discussed.

10

the laws, rules and regulations imposed at regional, national as well as international level. Along

with this, as per considering the taxable liabilities of an organisation. This is an ethical

requirement in an entity which defines the roles of business towards the society. Paying taxes on

the generated revenue to the government would have positive impact of economic development.

Application of different business formatted to individual: There have been application of

various ethic such as recoding the transaction, disclosing the income generated over a period as

well as expenses incurred (Song, Seetaram and Ye, 2019). It funnels the government as well as

investors in terms of analysing the profitability of the organisation as well as duty of following

the legal requirement at the right time.

Compliance requirements: An organisation is being liable to make the adequate taxable

consequences ion which they would have made operational analysis over recording of

transaction, reporting the information regarding the income as well as determining the role of

organisation in relation with collecting the taxes (Gemmell and et.al., 2018).

CONCLUSION

On the basis of above report, on which it can be said that there have been various methods

through which organisation makes taxable payments. It has been counted in the ethics for the

organisations as well as for the individual living in different countries. Thus, making taxable

payment will be adequate in terms of bringing the better gains to the organisation. Report have

covered all the required analysis based on taxation consequences, fair taxation policies, as well

as ethical constraints to be followed by companies in an economy were discussed.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.