The European Debt Crisis: Causes and Consequences

VerifiedAdded on 2020/11/12

|11

|2577

|288

AI Summary

This assignment provides an in-depth analysis of the European debt crisis, including its causes, such as budget deficits, corruption, and economic imbalances. It also explores the consequences of the crisis, such as economic growth slowdown and long-term yield spread over German government bonds. The assignment discusses measures to avoid future crises, including bailout programs and trade and capital imbalances in the European economy. It is a useful resource for students looking to understand the complexities of the European debt crisis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

THE EUROPEAN

DEBT CRISIS

DEBT CRISIS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Main forces of European debt crisis............................................................................................1

Consequences of crisis................................................................................................................2

Solutions for crisis......................................................................................................................3

Losers and winners of crisis........................................................................................................4

Measures for preventing from similar crisis...............................................................................5

Future of Euro.............................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Main forces of European debt crisis............................................................................................1

Consequences of crisis................................................................................................................2

Solutions for crisis......................................................................................................................3

Losers and winners of crisis........................................................................................................4

Measures for preventing from similar crisis...............................................................................5

Future of Euro.............................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

European debt crisis is referred as the most serious financial crisis since 1930 by head of

Bank of England. This term reflects the struggle of Europe in context of paying debts which was

built in recent decades. The countries which were involved in this crisis are Italy, Portugal,

Spain, Greece and Ireland as they were failed to generate economic growth which should be able

to pay liabilities to bondholders which was guaranteed. These five countries were in very

immediate danger for creating default in the era of 2010 – 2011.

MAIN BODY

Main forces of European debt crisis

Increasing household and debt level of government is the main cause of crisis. In this,

members of European Union signed a treaty where deficit spending and debt level was set to a

limit known as Maastricht treaty. Excessive social welfare spending was known as the major

reason of debt crisis (Broto and Perez-Quiros, 2015). The debt level was increased because of

package of large bailouts given to financial sector and after that, global economic was slowdown.

In the same series, there was rise in government debt in context of GDP. So, all fiscal deficits

were stressed in euro area which were shrinking or stable from early 1990. There was presence

of excessive lending via banks not spending created this crisis. There are different complicated

derivatives which turned this crisis very worse which is termed as credit default swaps which is

an insurance like derivative instrument is labelled once as market was distressed by small CDS

market and drive rate of bond interest rate of various sovereign nations.

Trade imbalances created variation in labour cost which had framedall southern nations

very less competitive and raised imbalance in trade. The nations of EU have enhanced the labour

cost more than Germany. Competitiveness was lost as those nations increased wages but not

productivity. As labour cost was restrained by Germany as it was and debatable factor in this and

it is cause for low employment rate which is considered as very important factor. It is indicated

by economic evidence that it has major role in trade deficits in t level of public debt. The interest

spread and current account deficit has a strong relationship as it is not a debt crisis; in real, it is

balance of payment crisis.

There was structural contradiction in Euro system which was the major cause of this

crisis. There was presence of monetary union with absence of fiscal union which includes

1

European debt crisis is referred as the most serious financial crisis since 1930 by head of

Bank of England. This term reflects the struggle of Europe in context of paying debts which was

built in recent decades. The countries which were involved in this crisis are Italy, Portugal,

Spain, Greece and Ireland as they were failed to generate economic growth which should be able

to pay liabilities to bondholders which was guaranteed. These five countries were in very

immediate danger for creating default in the era of 2010 – 2011.

MAIN BODY

Main forces of European debt crisis

Increasing household and debt level of government is the main cause of crisis. In this,

members of European Union signed a treaty where deficit spending and debt level was set to a

limit known as Maastricht treaty. Excessive social welfare spending was known as the major

reason of debt crisis (Broto and Perez-Quiros, 2015). The debt level was increased because of

package of large bailouts given to financial sector and after that, global economic was slowdown.

In the same series, there was rise in government debt in context of GDP. So, all fiscal deficits

were stressed in euro area which were shrinking or stable from early 1990. There was presence

of excessive lending via banks not spending created this crisis. There are different complicated

derivatives which turned this crisis very worse which is termed as credit default swaps which is

an insurance like derivative instrument is labelled once as market was distressed by small CDS

market and drive rate of bond interest rate of various sovereign nations.

Trade imbalances created variation in labour cost which had framedall southern nations

very less competitive and raised imbalance in trade. The nations of EU have enhanced the labour

cost more than Germany. Competitiveness was lost as those nations increased wages but not

productivity. As labour cost was restrained by Germany as it was and debatable factor in this and

it is cause for low employment rate which is considered as very important factor. It is indicated

by economic evidence that it has major role in trade deficits in t level of public debt. The interest

spread and current account deficit has a strong relationship as it is not a debt crisis; in real, it is

balance of payment crisis.

There was structural contradiction in Euro system which was the major cause of this

crisis. There was presence of monetary union with absence of fiscal union which includes

1

pension, taxation or any functions of treasury. They have to follow same fiscal path but for

enforcing, they do not have common treasury. They did not have banking union as there was not

any wide approach for bank deposit insurance, bank oversight, etc. There was fear of increasing

default in bond yields but this is very expensive for paying interest on debt (Hallett and Oliva,

2015). As high debt tends to increase high interest rate costs which is very difficult to pay. They

can even apply Treasure Euro Dollar spread which is difference between interest rate on short

term US government debt and on interbank loans for paying its debt.

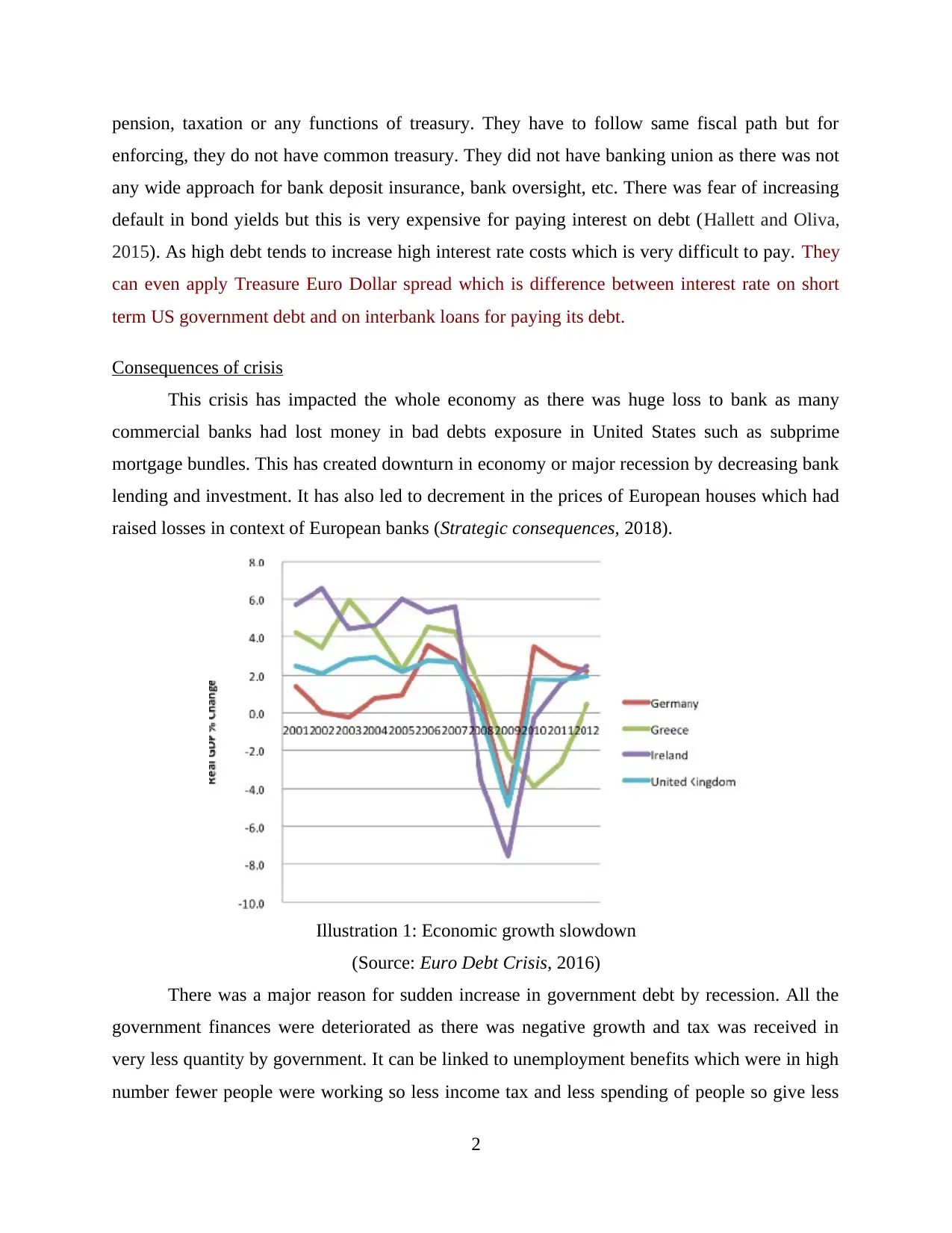

Consequences of crisis

This crisis has impacted the whole economy as there was huge loss to bank as many

commercial banks had lost money in bad debts exposure in United States such as subprime

mortgage bundles. This has created downturn in economy or major recession by decreasing bank

lending and investment. It has also led to decrement in the prices of European houses which had

raised losses in context of European banks (Strategic consequences, 2018).

Illustration 1: Economic growth slowdown

(Source: Euro Debt Crisis, 2016)

There was a major reason for sudden increase in government debt by recession. All the

government finances were deteriorated as there was negative growth and tax was received in

very less quantity by government. It can be linked to unemployment benefits which were in high

number fewer people were working so less income tax and less spending of people so give less

2

enforcing, they do not have common treasury. They did not have banking union as there was not

any wide approach for bank deposit insurance, bank oversight, etc. There was fear of increasing

default in bond yields but this is very expensive for paying interest on debt (Hallett and Oliva,

2015). As high debt tends to increase high interest rate costs which is very difficult to pay. They

can even apply Treasure Euro Dollar spread which is difference between interest rate on short

term US government debt and on interbank loans for paying its debt.

Consequences of crisis

This crisis has impacted the whole economy as there was huge loss to bank as many

commercial banks had lost money in bad debts exposure in United States such as subprime

mortgage bundles. This has created downturn in economy or major recession by decreasing bank

lending and investment. It has also led to decrement in the prices of European houses which had

raised losses in context of European banks (Strategic consequences, 2018).

Illustration 1: Economic growth slowdown

(Source: Euro Debt Crisis, 2016)

There was a major reason for sudden increase in government debt by recession. All the

government finances were deteriorated as there was negative growth and tax was received in

very less quantity by government. It can be linked to unemployment benefits which were in high

number fewer people were working so less income tax and less spending of people so give less

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

VAT and less company profits will give less corporation tax. Debt rose to ratio of GDP as it is

considered as the most useful guide to different level of debt which is a manageable debt. If there

is decrement in GDP and rise in debt, then it will rise in a rapid manner. Due to this crisis, bond

market of nations which were affected performed in worse manner as yield rise reflects fall in

price. On the same side, US treasuries yield fell at very low level historically and it gave very

low level for reflecting investors. This crisis has made worse to Brussels commission and

Germany was criticised for not stimulating more demand in Eurozone as it had given help to

Southern Europeans for increasing their level when public spending has been slashed.

Solutions for crisis

EU faces many problems during crisis such as high unemployment, huge current account

deficit because of less competitiveness, stagnant economic growth and very high government

borrowing. The first measure for overcoming on this crisis is to devalue currency as it will lead

to gain competitiveness and decrease budget deficit with unemployment and it will help

economy for recovering (European debt, 2018.). For decreasing the budget deficit, economic

recovery is termed as an important ingredient. So, option for devaluation must not be considered.

If Euro will be left by countries then it will directly damage and it will tend to give rapid flow of

capital outside country because of these mentioned consequence. Internal devaluation is faced by

Greece and Portugal for restoring competitiveness by decreasing inflation, cost and wages but

this is not considered to be appropriate due to causation of high unemployment and lowering

growth.

In the same series of solution, debt has been consolidated of countries like Greece and

Italy. EU has requirement of partial debt default as there is no chance of repayment for Greece so

it should allow Greece for default and gives full concentration on Italy as it has capability to pay

debt with various constraints such as shortage of money and all. The importance of economic

growth has been determined by EU and ECB, so they are recommended for spending cuts and

austerity but this will lead to occur negative spiral of less growth, lower tax revenues and high

unemployment. Monetary easing is referred as best solution as its main target for high inflation

and quantitative easing. Monetary stimulus should be provided to peripheral countries when they

face deflationary pressures. Only worse thing is wrong attitude about inflation with ECB. There

should be implementation of supply side policies as they will improve efficiency and

competitiveness especially for Greece and Portugal.

3

considered as the most useful guide to different level of debt which is a manageable debt. If there

is decrement in GDP and rise in debt, then it will rise in a rapid manner. Due to this crisis, bond

market of nations which were affected performed in worse manner as yield rise reflects fall in

price. On the same side, US treasuries yield fell at very low level historically and it gave very

low level for reflecting investors. This crisis has made worse to Brussels commission and

Germany was criticised for not stimulating more demand in Eurozone as it had given help to

Southern Europeans for increasing their level when public spending has been slashed.

Solutions for crisis

EU faces many problems during crisis such as high unemployment, huge current account

deficit because of less competitiveness, stagnant economic growth and very high government

borrowing. The first measure for overcoming on this crisis is to devalue currency as it will lead

to gain competitiveness and decrease budget deficit with unemployment and it will help

economy for recovering (European debt, 2018.). For decreasing the budget deficit, economic

recovery is termed as an important ingredient. So, option for devaluation must not be considered.

If Euro will be left by countries then it will directly damage and it will tend to give rapid flow of

capital outside country because of these mentioned consequence. Internal devaluation is faced by

Greece and Portugal for restoring competitiveness by decreasing inflation, cost and wages but

this is not considered to be appropriate due to causation of high unemployment and lowering

growth.

In the same series of solution, debt has been consolidated of countries like Greece and

Italy. EU has requirement of partial debt default as there is no chance of repayment for Greece so

it should allow Greece for default and gives full concentration on Italy as it has capability to pay

debt with various constraints such as shortage of money and all. The importance of economic

growth has been determined by EU and ECB, so they are recommended for spending cuts and

austerity but this will lead to occur negative spiral of less growth, lower tax revenues and high

unemployment. Monetary easing is referred as best solution as its main target for high inflation

and quantitative easing. Monetary stimulus should be provided to peripheral countries when they

face deflationary pressures. Only worse thing is wrong attitude about inflation with ECB. There

should be implementation of supply side policies as they will improve efficiency and

competitiveness especially for Greece and Portugal.

3

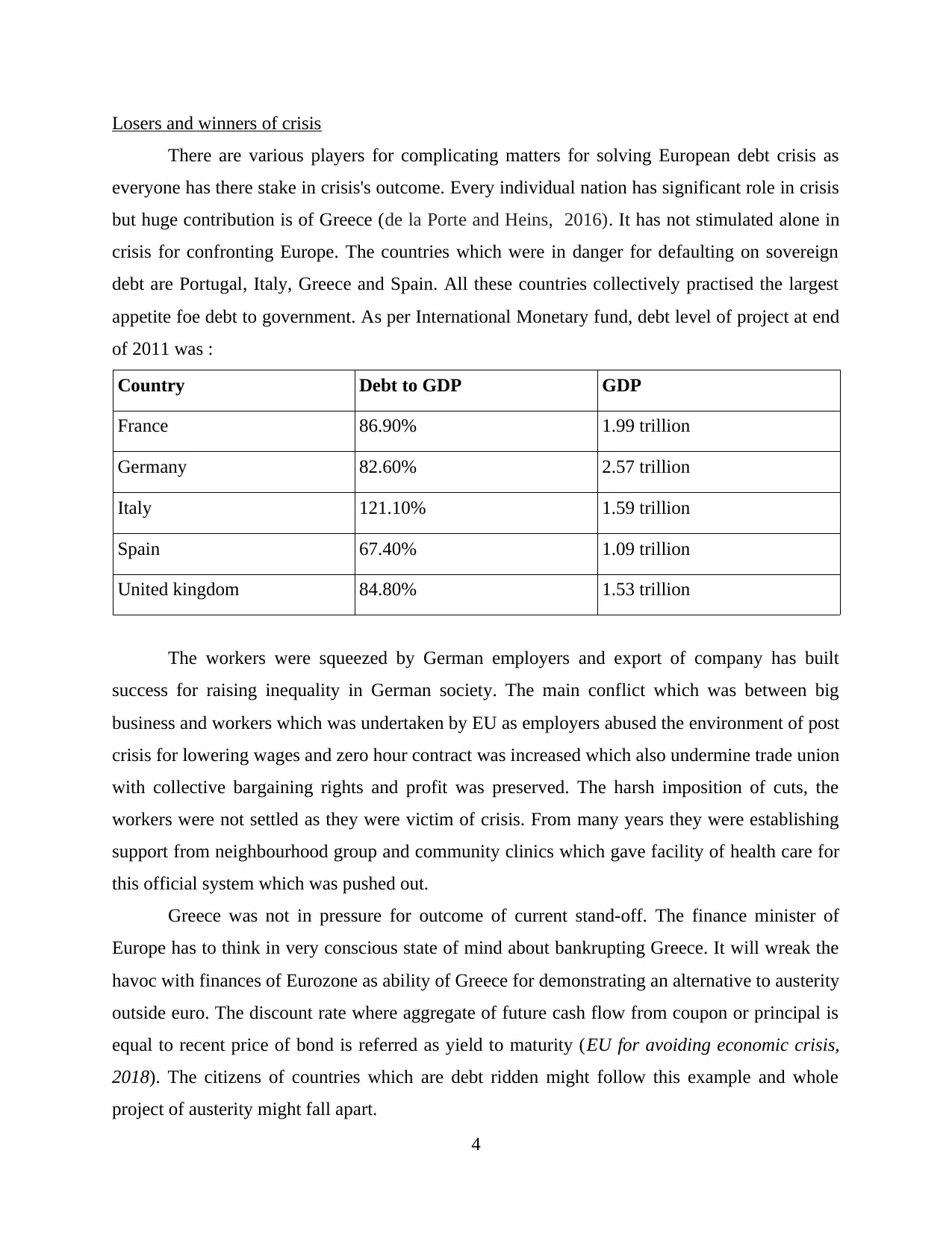

Losers and winners of crisis

There are various players for complicating matters for solving European debt crisis as

everyone has there stake in crisis's outcome. Every individual nation has significant role in crisis

but huge contribution is of Greece (de la Porte and Heins, 2016). It has not stimulated alone in

crisis for confronting Europe. The countries which were in danger for defaulting on sovereign

debt are Portugal, Italy, Greece and Spain. All these countries collectively practised the largest

appetite foe debt to government. As per International Monetary fund, debt level of project at end

of 2011 was :

Country Debt to GDP GDP

France 86.90% 1.99 trillion

Germany 82.60% 2.57 trillion

Italy 121.10% 1.59 trillion

Spain 67.40% 1.09 trillion

United kingdom 84.80% 1.53 trillion

The workers were squeezed by German employers and export of company has built

success for raising inequality in German society. The main conflict which was between big

business and workers which was undertaken by EU as employers abused the environment of post

crisis for lowering wages and zero hour contract was increased which also undermine trade union

with collective bargaining rights and profit was preserved. The harsh imposition of cuts, the

workers were not settled as they were victim of crisis. From many years they were establishing

support from neighbourhood group and community clinics which gave facility of health care for

this official system which was pushed out.

Greece was not in pressure for outcome of current stand-off. The finance minister of

Europe has to think in very conscious state of mind about bankrupting Greece. It will wreak the

havoc with finances of Eurozone as ability of Greece for demonstrating an alternative to austerity

outside euro. The discount rate where aggregate of future cash flow from coupon or principal is

equal to recent price of bond is referred as yield to maturity (EU for avoiding economic crisis,

2018). The citizens of countries which are debt ridden might follow this example and whole

project of austerity might fall apart.

4

There are various players for complicating matters for solving European debt crisis as

everyone has there stake in crisis's outcome. Every individual nation has significant role in crisis

but huge contribution is of Greece (de la Porte and Heins, 2016). It has not stimulated alone in

crisis for confronting Europe. The countries which were in danger for defaulting on sovereign

debt are Portugal, Italy, Greece and Spain. All these countries collectively practised the largest

appetite foe debt to government. As per International Monetary fund, debt level of project at end

of 2011 was :

Country Debt to GDP GDP

France 86.90% 1.99 trillion

Germany 82.60% 2.57 trillion

Italy 121.10% 1.59 trillion

Spain 67.40% 1.09 trillion

United kingdom 84.80% 1.53 trillion

The workers were squeezed by German employers and export of company has built

success for raising inequality in German society. The main conflict which was between big

business and workers which was undertaken by EU as employers abused the environment of post

crisis for lowering wages and zero hour contract was increased which also undermine trade union

with collective bargaining rights and profit was preserved. The harsh imposition of cuts, the

workers were not settled as they were victim of crisis. From many years they were establishing

support from neighbourhood group and community clinics which gave facility of health care for

this official system which was pushed out.

Greece was not in pressure for outcome of current stand-off. The finance minister of

Europe has to think in very conscious state of mind about bankrupting Greece. It will wreak the

havoc with finances of Eurozone as ability of Greece for demonstrating an alternative to austerity

outside euro. The discount rate where aggregate of future cash flow from coupon or principal is

equal to recent price of bond is referred as yield to maturity (EU for avoiding economic crisis,

2018). The citizens of countries which are debt ridden might follow this example and whole

project of austerity might fall apart.

4

Measures for preventing from similar crisis

Government should collectively issue bond instead of issuing their own national bond.

This will lead to addressing problem of liquidity many small financial markets. It will decrease

borrowing costs. There should be inherent contradiction between monetary and economic union

with absence of political union. The strategy of pre-emption should be imposed where in goods

or shares should be purchased by one party before that specific opportunity is gone to others. The

crisis of sovereign must lead to others in certain manner such as investors suddenly pass their

attention to next link which is weakest (Credit default swaps, 2018.). It will be creating no

shortage in economy which is experiencing severe fiscal pressures. As this was conquerable in

case of Greece or Ireland but on contrary side it will be imposing huge challenge with large

member states like Italy or Spain.

The indirect cost must be imposed for fiscal crisis in neighbourhood which is demanding

more exports. The repercussions must be dramatic and it will lead to breakup if default of

sovereign debt. In case of inflexible economy default within currency union is considered as

plausible instead of leaving it. The member state must decide that they are having default and

must cut themselves for temporary basis from various sources of capital and it will be devalued.

It will lead to ensuring and restoring competitiveness and economy will grow as soon as possible

in import of long term inflation perspective. If any one country will boycott itself then whole

efforts and pressure will be on other in intense form. If cost will be hold down then

competitiveness will be improved nut it will lead to expense of very low domestic demand. The

yield spread replicates variation between quoted rate of return of various investments but has

similar maturity with risk premium for single product of investment for other. Different bailout

programs were stated by European zone which were provided by jointly IMF for lowering yield

of monetary transactions (Key players in European debt crisis, 2018).

5

Government should collectively issue bond instead of issuing their own national bond.

This will lead to addressing problem of liquidity many small financial markets. It will decrease

borrowing costs. There should be inherent contradiction between monetary and economic union

with absence of political union. The strategy of pre-emption should be imposed where in goods

or shares should be purchased by one party before that specific opportunity is gone to others. The

crisis of sovereign must lead to others in certain manner such as investors suddenly pass their

attention to next link which is weakest (Credit default swaps, 2018.). It will be creating no

shortage in economy which is experiencing severe fiscal pressures. As this was conquerable in

case of Greece or Ireland but on contrary side it will be imposing huge challenge with large

member states like Italy or Spain.

The indirect cost must be imposed for fiscal crisis in neighbourhood which is demanding

more exports. The repercussions must be dramatic and it will lead to breakup if default of

sovereign debt. In case of inflexible economy default within currency union is considered as

plausible instead of leaving it. The member state must decide that they are having default and

must cut themselves for temporary basis from various sources of capital and it will be devalued.

It will lead to ensuring and restoring competitiveness and economy will grow as soon as possible

in import of long term inflation perspective. If any one country will boycott itself then whole

efforts and pressure will be on other in intense form. If cost will be hold down then

competitiveness will be improved nut it will lead to expense of very low domestic demand. The

yield spread replicates variation between quoted rate of return of various investments but has

similar maturity with risk premium for single product of investment for other. Different bailout

programs were stated by European zone which were provided by jointly IMF for lowering yield

of monetary transactions (Key players in European debt crisis, 2018).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

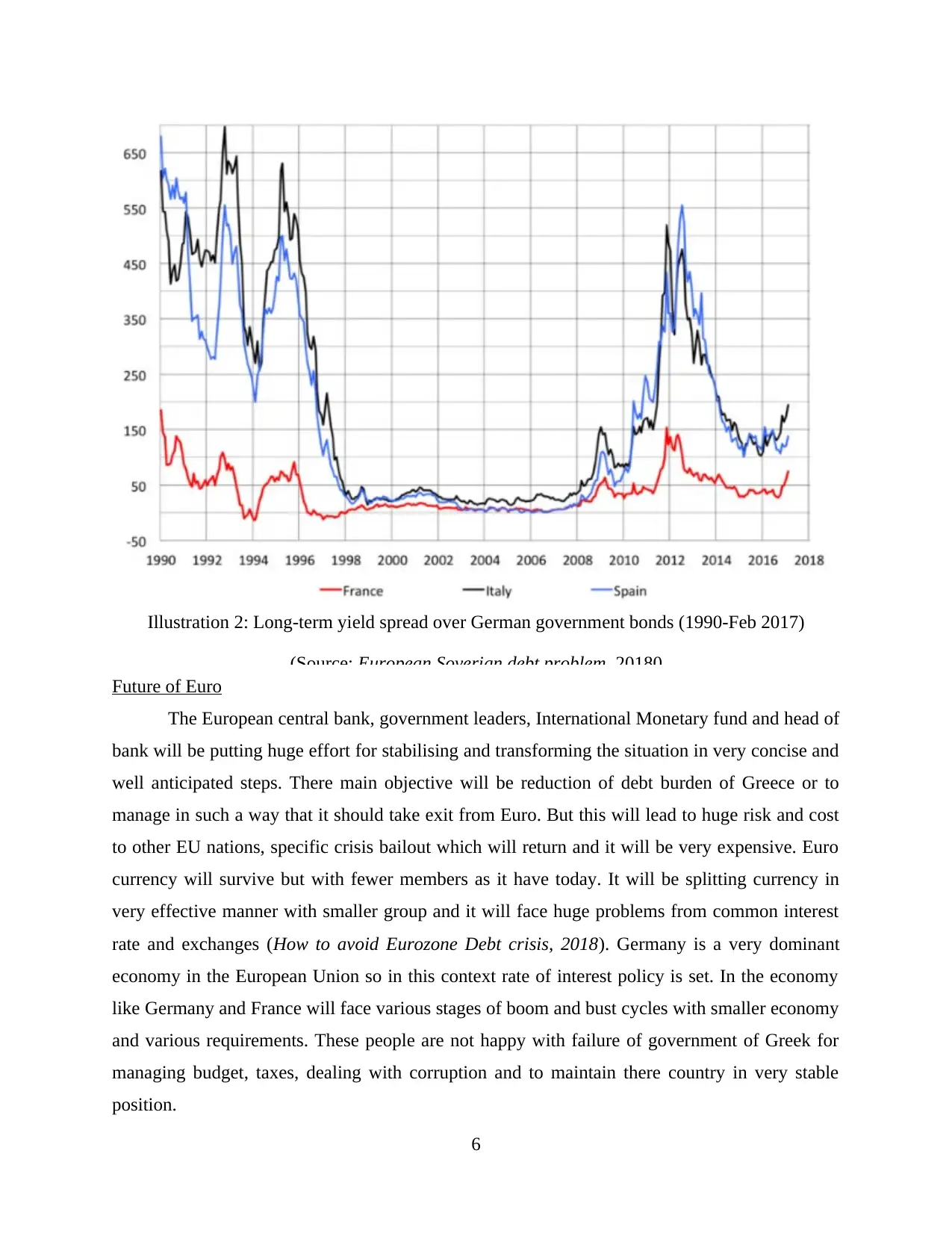

Illustration 2: Long-term yield spread over German government bonds (1990-Feb 2017)

(Source: European Soverign debt problem, 20180

Future of Euro

The European central bank, government leaders, International Monetary fund and head of

bank will be putting huge effort for stabilising and transforming the situation in very concise and

well anticipated steps. There main objective will be reduction of debt burden of Greece or to

manage in such a way that it should take exit from Euro. But this will lead to huge risk and cost

to other EU nations, specific crisis bailout which will return and it will be very expensive. Euro

currency will survive but with fewer members as it have today. It will be splitting currency in

very effective manner with smaller group and it will face huge problems from common interest

rate and exchanges (How to avoid Eurozone Debt crisis, 2018). Germany is a very dominant

economy in the European Union so in this context rate of interest policy is set. In the economy

like Germany and France will face various stages of boom and bust cycles with smaller economy

and various requirements. These people are not happy with failure of government of Greek for

managing budget, taxes, dealing with corruption and to maintain there country in very stable

position.

6

(Source: European Soverign debt problem, 20180

Future of Euro

The European central bank, government leaders, International Monetary fund and head of

bank will be putting huge effort for stabilising and transforming the situation in very concise and

well anticipated steps. There main objective will be reduction of debt burden of Greece or to

manage in such a way that it should take exit from Euro. But this will lead to huge risk and cost

to other EU nations, specific crisis bailout which will return and it will be very expensive. Euro

currency will survive but with fewer members as it have today. It will be splitting currency in

very effective manner with smaller group and it will face huge problems from common interest

rate and exchanges (How to avoid Eurozone Debt crisis, 2018). Germany is a very dominant

economy in the European Union so in this context rate of interest policy is set. In the economy

like Germany and France will face various stages of boom and bust cycles with smaller economy

and various requirements. These people are not happy with failure of government of Greek for

managing budget, taxes, dealing with corruption and to maintain there country in very stable

position.

6

From the above report it has been concluded that various measure like bailout programs

are efficient for conquering with such type of similar crisis. And future of Euro is secure

according to this brief analysis.

7

are efficient for conquering with such type of similar crisis. And future of Euro is secure

according to this brief analysis.

7

REFERENCES

Books and Journals

Broto, C. and Perez-Quiros, G., 2015. Disentangling contagion among Sovereign CDS spreads

during the European debt crisis. Journal of Empirical Finance. 32. pp.165-179.

de la Porte, C. and Heins, E., 2016. A new era of European integration? Governance of labour

market and social policy since the sovereign debt crisis. In The sovereign debt crisis, the

EU and welfare state reform (pp. 15-41). Palgrave Macmillan, London.

Hallett, A. H. and Oliva, J. C. M., 2015. The importance of trade and capital imbalances in the

European debt crisis. Journal of Policy Modeling. 37(2). pp.229-252.

ONLINE

Credit default swaps. 2018. [Online]. Available through

:<https://www.huffingtonpost.in/entry/credit-default-swaps-europe_n_1458842>.

EU for avoiding economic crisis. 2018. [Online]. Available through

:<https://www.weforum.org/agenda/2015/09/what-can-the-eu-do-to-avoid-future-

economic-crises/>.

Euro Debt Crisis. 2016. [Online]. Available through

:<https://www.economicshelp.org/blog/3806/economics/euro-debt-crisis-explained/>.

European debt. 2018. [Online]. Available through

:<https://piie.com/commentary/testimonies/european-debt-and-financial-crisis-origins-

options>.

European Soverign debt problem. 2018. [Online]. Available through

:<https://www.cbsnews.com/news/europes-sovereign-debt-problem-causes-and-solutions/>.

How to avoid Eurozone Debt crisis. 2018. [Online]. Available through :<http://www.cer.eu/in-

the-press/how-avoid-eurozone-debt-crisis>.

Key players in European debt crisis. 2018. [Online]. Available through

:<https://blogs.cfainstitute.org/investor/2011/12/01/key-players-in-the-european-

sovereign-debt-crisis/#Key-Players>.

Strategic consequences. 2018. [Online]. Available through

:<http://www.cer.eu/in-the-press/strategic-consequences-euro-crisis>.

8

Books and Journals

Broto, C. and Perez-Quiros, G., 2015. Disentangling contagion among Sovereign CDS spreads

during the European debt crisis. Journal of Empirical Finance. 32. pp.165-179.

de la Porte, C. and Heins, E., 2016. A new era of European integration? Governance of labour

market and social policy since the sovereign debt crisis. In The sovereign debt crisis, the

EU and welfare state reform (pp. 15-41). Palgrave Macmillan, London.

Hallett, A. H. and Oliva, J. C. M., 2015. The importance of trade and capital imbalances in the

European debt crisis. Journal of Policy Modeling. 37(2). pp.229-252.

ONLINE

Credit default swaps. 2018. [Online]. Available through

:<https://www.huffingtonpost.in/entry/credit-default-swaps-europe_n_1458842>.

EU for avoiding economic crisis. 2018. [Online]. Available through

:<https://www.weforum.org/agenda/2015/09/what-can-the-eu-do-to-avoid-future-

economic-crises/>.

Euro Debt Crisis. 2016. [Online]. Available through

:<https://www.economicshelp.org/blog/3806/economics/euro-debt-crisis-explained/>.

European debt. 2018. [Online]. Available through

:<https://piie.com/commentary/testimonies/european-debt-and-financial-crisis-origins-

options>.

European Soverign debt problem. 2018. [Online]. Available through

:<https://www.cbsnews.com/news/europes-sovereign-debt-problem-causes-and-solutions/>.

How to avoid Eurozone Debt crisis. 2018. [Online]. Available through :<http://www.cer.eu/in-

the-press/how-avoid-eurozone-debt-crisis>.

Key players in European debt crisis. 2018. [Online]. Available through

:<https://blogs.cfainstitute.org/investor/2011/12/01/key-players-in-the-european-

sovereign-debt-crisis/#Key-Players>.

Strategic consequences. 2018. [Online]. Available through

:<http://www.cer.eu/in-the-press/strategic-consequences-euro-crisis>.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.