The Evolution of Marks and Spencer: A Case Study in Retail Growth Strategies

VerifiedAdded on 2024/04/29

|16

|5592

|69

AI Summary

This case study delves into the five phases of growth at Marks and Spencer, analyzing their strategies from store expansion to diversification. It challenges traditional retail evolution theories and emphasizes the importance of adaptive long-term vision in sustaining success.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/233171370

The Evolution of Marks and Spencer

Article in The Service Industries Journal · July 1999

DOI: 10.1080/02642069900000030

CITATIONS

32

READS

4,527

1 author:

Gary Davies

The University of Manchester

113PUBLICATIONS5,078CITATIONS

SEE PROFILE

The Evolution of Marks and Spencer

Article in The Service Industries Journal · July 1999

DOI: 10.1080/02642069900000030

CITATIONS

32

READS

4,527

1 author:

Gary Davies

The University of Manchester

113PUBLICATIONS5,078CITATIONS

SEE PROFILE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The Service Industries Journal

ISSN: 0264-2069 (Print) 1743-9507 (Online) Journal homepag

The Evolution of Marks and Sp

Gary Davies

To cite this article: Gary Davies (1999) The Evolution of Ma

Industries Journal, 19:3, 60-73, DOI: 10.1080/0264206990000

To link to this article: http://dx.doi.org/10.1080/02642069

Published online: 28 Jul 2006.

Submit your article to this journal

Article views: 726

View related articles

Citing articles: 7 View citing articles

ISSN: 0264-2069 (Print) 1743-9507 (Online) Journal homepag

The Evolution of Marks and Sp

Gary Davies

To cite this article: Gary Davies (1999) The Evolution of Ma

Industries Journal, 19:3, 60-73, DOI: 10.1080/0264206990000

To link to this article: http://dx.doi.org/10.1080/02642069

Published online: 28 Jul 2006.

Submit your article to this journal

Article views: 726

View related articles

Citing articles: 7 View citing articles

The Evolution of Marks and Spencer

GARY DAVIES

Financial data drawr~f,-om Marks awd Spencer S arc-hives and

annual reports is used to idenlvyfive phases in the Company S

sales growth. Early, rather erratic, growth, often through

acquisition, gave way to a second phase of store development

funded by the Company S.floatation in the 1920s. Sales growth

in the third phase came substanriveljl through an increase in

store size. A fourth phase involved irnprovernerzts in labour

and space productivity. The final and current phase of

evolution emphasises divers(fication. The pattern of evolution

is compared with two theories of retail change, the Wheel of

Retailing and the Retail Accordion. Neither is compatible with

the sustained growth exhibited, indeed both theories could be

said to predict the failure of the Company 's overall strategy.

INTRODUCTION

Marks and Spencer is widely regarded as one of Britain's leading retail

businesses. They are unusual in having remained substantially in the same

style of retailing for over 100 years (the variety chain store) and in trading

as a single entity.

Their sales growth has been sustained over most of this period without

substantial diversification or the acquisition of different businesses. Their

success has been largely through organic growth and the managed evolution

of a retail format that has changed remarkably slowly over their existence.

The purpose of this study is to identify what Marks and Spencer have done

in the operation of their business to maintain their sales growth and to

compare these findings with two theories of retail change and evolution.

Gary Davies is at Manchestcr Business School, Booth Street West, Manchester MI5 6PB.

The Service Industries Journal, Vo1.19, No.3 (July 1999). pp.60-73

P U B L I S H E DB Y F R A N K C A S S , L O N D O N

GARY DAVIES

Financial data drawr~f,-om Marks awd Spencer S arc-hives and

annual reports is used to idenlvyfive phases in the Company S

sales growth. Early, rather erratic, growth, often through

acquisition, gave way to a second phase of store development

funded by the Company S.floatation in the 1920s. Sales growth

in the third phase came substanriveljl through an increase in

store size. A fourth phase involved irnprovernerzts in labour

and space productivity. The final and current phase of

evolution emphasises divers(fication. The pattern of evolution

is compared with two theories of retail change, the Wheel of

Retailing and the Retail Accordion. Neither is compatible with

the sustained growth exhibited, indeed both theories could be

said to predict the failure of the Company 's overall strategy.

INTRODUCTION

Marks and Spencer is widely regarded as one of Britain's leading retail

businesses. They are unusual in having remained substantially in the same

style of retailing for over 100 years (the variety chain store) and in trading

as a single entity.

Their sales growth has been sustained over most of this period without

substantial diversification or the acquisition of different businesses. Their

success has been largely through organic growth and the managed evolution

of a retail format that has changed remarkably slowly over their existence.

The purpose of this study is to identify what Marks and Spencer have done

in the operation of their business to maintain their sales growth and to

compare these findings with two theories of retail change and evolution.

Gary Davies is at Manchestcr Business School, Booth Street West, Manchester MI5 6PB.

The Service Industries Journal, Vo1.19, No.3 (July 1999). pp.60-73

P U B L I S H E DB Y F R A N K C A S S , L O N D O N

EVOLUTION OF MARKS A N D SPENCER

THEORIES O F RETAIL C H A N G E

There exist a number of theories to explain major change in the retail sector

[Roth and Klein, 19931. The most prominent is the 'Wheel of Retailing',

based on the observation that new retail businesses tend to enter the market

as low cost/low price businesses [McNair, 19581. Over time the retailer

'trades up' by enhancing its service levels and ambience and by raising its

selling prices. This makes the retailer vulnerable to a newer form of

retailing, operating with a lower cost structure and able to offer shoppers

lower prices. The Wheel theory has been much discussed since its inception

[Hollander, 1960; Davidson et al., 1976; Brown, 1988; Valentin, 19911 and

criticised as having no real grounding in economic theory. Nevertheless the

idea of such a cyclical process can be used to explain the long-term

evolution of certain retail sectors, such as that for groceries, where self-

service superstores replaced counter service retailers to be replaced by

lower cost supermarkets, which were attacked in turn by other lower cost

formats such as hypermarkets [Knee and Walters, 19851.

A second model of retail evolution relevant to any study of Marks and

Spencer is that of the 'retail accordion', [Hollander, 19661. Again

observation of actual process was used to suggest a general rule. According

to Hollander a retail sector is dominated in turn by wide assortment retailers

and, more focused, specialist retailers. Department stores developed from

more focused mercers in the mid-nineteenth century [Ferry, 1960;

Adburgham, 1964; 19811 by expanding the different types of product they

sold from textiles to finished clothing, food, furniture and general

household goods. The department store became the one stop shop for the

middle class in Europe, Japan and North America. While the format has

continued to hold a high share of retail sales in North America, it has

declined in Europe, particularly in Britain. More specialist retailers with

narrower ranges concentrating for example on the sale of clothing for one

sex and age group, specialist furniture stores, and, recently, even more

highly focused retailers such as Sock Shop and Tie Rack have all eroded the

market of the generalist department store. The same effect in reverse can be

seen in the decline of specialist food retailers such as butchers, fishmongers,

and greengrocers in favour of grocery superstores, where the wide range

and choice appeals to time pressed shoppers who may prefer not to have to

visit a number of stores for their regular and routine purchases.

There is, therefore, considerable anecdotal evidence to support both

theories. Interestingly both propose a cyclicality in the process of retail

evolution, an inevitability that one type of retailing will be overtaken by

another [Davies, 19921. The expectations would be that a retailer who both

trades up and expands its range places itself at risk to both the Wheel and

Accordion effects. As will become apparent, Marks and Spencer have done

THEORIES O F RETAIL C H A N G E

There exist a number of theories to explain major change in the retail sector

[Roth and Klein, 19931. The most prominent is the 'Wheel of Retailing',

based on the observation that new retail businesses tend to enter the market

as low cost/low price businesses [McNair, 19581. Over time the retailer

'trades up' by enhancing its service levels and ambience and by raising its

selling prices. This makes the retailer vulnerable to a newer form of

retailing, operating with a lower cost structure and able to offer shoppers

lower prices. The Wheel theory has been much discussed since its inception

[Hollander, 1960; Davidson et al., 1976; Brown, 1988; Valentin, 19911 and

criticised as having no real grounding in economic theory. Nevertheless the

idea of such a cyclical process can be used to explain the long-term

evolution of certain retail sectors, such as that for groceries, where self-

service superstores replaced counter service retailers to be replaced by

lower cost supermarkets, which were attacked in turn by other lower cost

formats such as hypermarkets [Knee and Walters, 19851.

A second model of retail evolution relevant to any study of Marks and

Spencer is that of the 'retail accordion', [Hollander, 19661. Again

observation of actual process was used to suggest a general rule. According

to Hollander a retail sector is dominated in turn by wide assortment retailers

and, more focused, specialist retailers. Department stores developed from

more focused mercers in the mid-nineteenth century [Ferry, 1960;

Adburgham, 1964; 19811 by expanding the different types of product they

sold from textiles to finished clothing, food, furniture and general

household goods. The department store became the one stop shop for the

middle class in Europe, Japan and North America. While the format has

continued to hold a high share of retail sales in North America, it has

declined in Europe, particularly in Britain. More specialist retailers with

narrower ranges concentrating for example on the sale of clothing for one

sex and age group, specialist furniture stores, and, recently, even more

highly focused retailers such as Sock Shop and Tie Rack have all eroded the

market of the generalist department store. The same effect in reverse can be

seen in the decline of specialist food retailers such as butchers, fishmongers,

and greengrocers in favour of grocery superstores, where the wide range

and choice appeals to time pressed shoppers who may prefer not to have to

visit a number of stores for their regular and routine purchases.

There is, therefore, considerable anecdotal evidence to support both

theories. Interestingly both propose a cyclicality in the process of retail

evolution, an inevitability that one type of retailing will be overtaken by

another [Davies, 19921. The expectations would be that a retailer who both

trades up and expands its range places itself at risk to both the Wheel and

Accordion effects. As will become apparent, Marks and Spencer have done

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

62 THE SERVICE INDUSTRIES JOURNAL

both over 100 years and have not only survived but have prospered. Some

other explanation is needed to explain successful retail evolution.

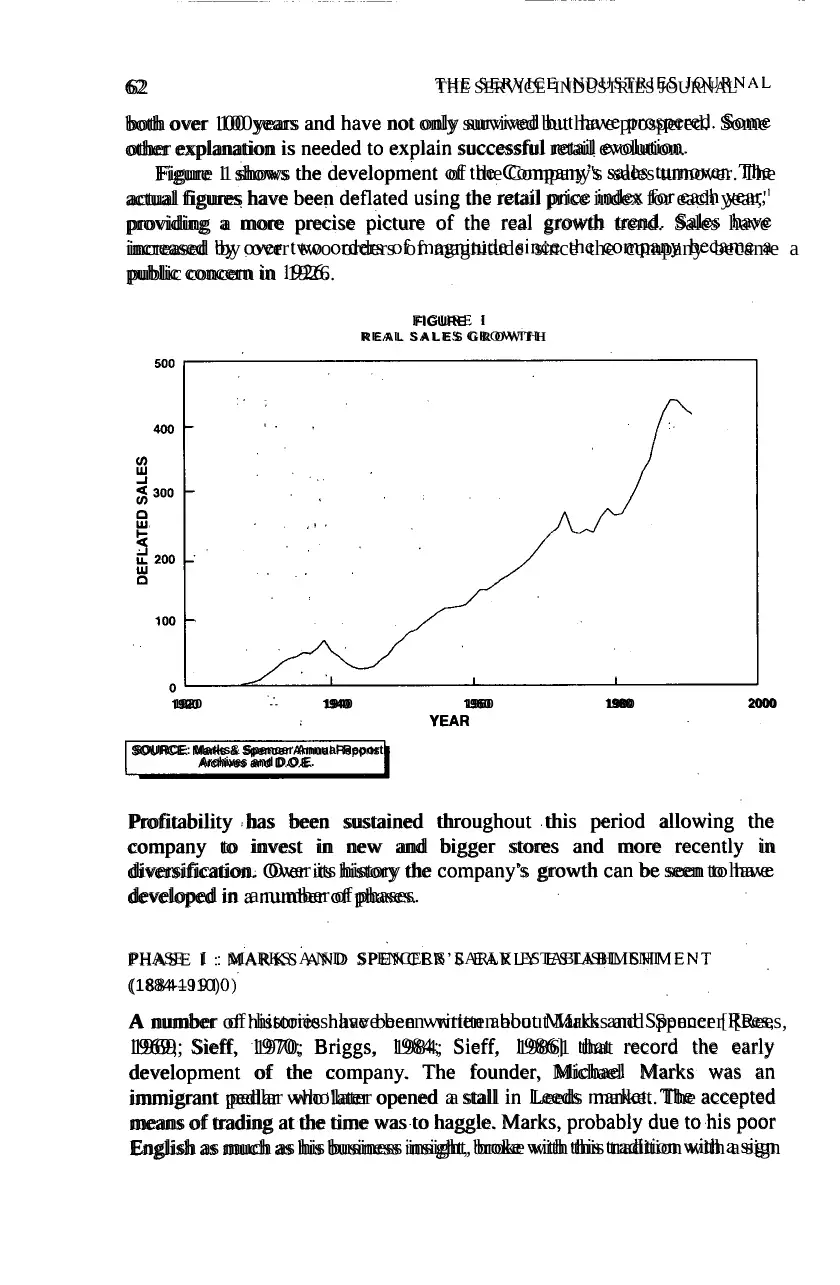

Figure 1 shows the development of the Company's sales turnover. The

actual figures have been deflated using the retail price index for each year,'

providing a more precise picture of the real growth trend. Sales have

increased by over two orders of magnitude since the company became a

public concern in 1926.

FIGURE I

R E A L S A L E S G R O W T H

1920 " 1940 1960 1980 2000

YEAR

SOURCE: Marks & Spencer Annual Reports

Archives and D.O.E.

Profitability has been sustained throughout this period allowing the

company to invest in new and bigger stores and more recently in

diversification. Over its history the company's growth can be seen to have

developed in a number of phases.

PHASE I : MARKS A N D SPENCER'S EARLY ESTABLISHMENT

(1884-1910)

A number of histories have been written about Marks and Spencer [Rees,

1969; Sieff, 1970; Briggs, 1984; Sieff, 19861 that record the early

development of the company. The founder, Michael Marks was an

immigrant pedlar who'later opened a stall in Leeds market. The accepted

means of trading at the time was to haggle. Marks, probably due to his poor

English as much as his business insight, broke with this tradition with a sign

both over 100 years and have not only survived but have prospered. Some

other explanation is needed to explain successful retail evolution.

Figure 1 shows the development of the Company's sales turnover. The

actual figures have been deflated using the retail price index for each year,'

providing a more precise picture of the real growth trend. Sales have

increased by over two orders of magnitude since the company became a

public concern in 1926.

FIGURE I

R E A L S A L E S G R O W T H

1920 " 1940 1960 1980 2000

YEAR

SOURCE: Marks & Spencer Annual Reports

Archives and D.O.E.

Profitability has been sustained throughout this period allowing the

company to invest in new and bigger stores and more recently in

diversification. Over its history the company's growth can be seen to have

developed in a number of phases.

PHASE I : MARKS A N D SPENCER'S EARLY ESTABLISHMENT

(1884-1910)

A number of histories have been written about Marks and Spencer [Rees,

1969; Sieff, 1970; Briggs, 1984; Sieff, 19861 that record the early

development of the company. The founder, Michael Marks was an

immigrant pedlar who'later opened a stall in Leeds market. The accepted

means of trading at the time was to haggle. Marks, probably due to his poor

English as much as his business insight, broke with this tradition with a sign

EVOLUTION OF M A R K S A N D SPENCER 63

which read 'Don't Ask the Price, It's a Penny.'. Marks endeavoured to find

goods he could sell for the fixed price of one penny. The-formula succeeded.

By 1890 he had five.:penny, bazaziis'n.and a..warehouse. In 41894 .Thomas

Spencer joined a busine~s~whichsold haberdashery, earthenware, hardware,

household~goodsand stationery, [Rees, ..1969:1,10].,Their.partnership,became

a ,private . limited. company- in 1903. (.By..1900 .ithere were. 36 .branches,

including 12 shops (as opposed to market stalls or bazaars) .

a After the death of the,partners .whose names (identify the retailer to this

day, ,control. over the, business came. under. Marks'.: son, Simon and his

brother-in-law.Israe1 Sieff:;In 1926;the business became.a public company.

A new. phase .in thecompany:s.history had begun.. . . : i..,

. , . , ' . t . ; I... . ,. . , / ! . a > . ;. - ,,:,,:,

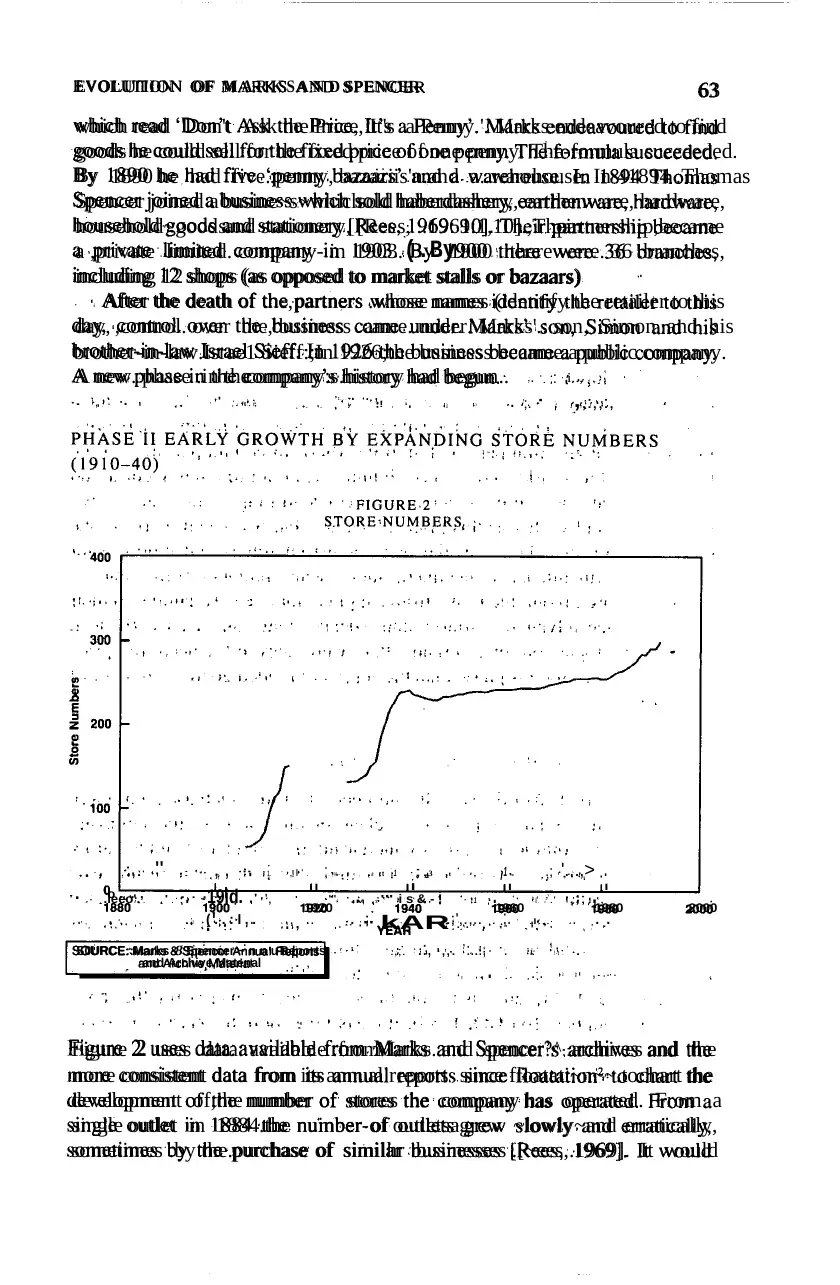

Figure 2 uses data: available .from.Marks. and spencer?^ :archives and the

.

more consistent data from its annual reports since floatati~n~~.to chart the

:,. ' " : " , , ". 1. , I ' , % ~ $ < , 8 t 1 ;,3 t , 1 . .; '...,> .

development of,the number of stores the company has operated. From a

. o . . , . . , . l I I I I

M $ ' i s & - ! '- .leeo'. ' . 19id. ' ', "' . , "' 1 . ' 8 . .' ,;; , ,

1920 , ' 1960 1980 2000

. , . , . I ( . . : I , .. , . . .;',.,.. ;. .I:,. . . ..' . . , . ' " kAR . .

S0URCE::Marks 8 Spencer ~ n n u a lReports. .,;. .:, ,,. :..:, . i: ! t . .

and Archive,Matenal , . , I . I . . . 2 ! . . .

single outlet in 1884.the nuinber-of outletsagrew ~lowly~and erratically,

sometimes .by the.purchase of similhr :businesses .[~ees,.1969]. It would

which read 'Don't Ask the Price, It's a Penny.'. Marks endeavoured to find

goods he could sell for the fixed price of one penny. The-formula succeeded.

By 1890 he had five.:penny, bazaziis'n.and a..warehouse. In 41894 .Thomas

Spencer joined a busine~s~whichsold haberdashery, earthenware, hardware,

household~goodsand stationery, [Rees, ..1969:1,10].,Their.partnership,became

a ,private . limited. company- in 1903. (.By..1900 .ithere were. 36 .branches,

including 12 shops (as opposed to market stalls or bazaars) .

a After the death of the,partners .whose names (identify the retailer to this

day, ,control. over the, business came. under. Marks'.: son, Simon and his

brother-in-law.Israe1 Sieff:;In 1926;the business became.a public company.

A new. phase .in thecompany:s.history had begun.. . . : i..,

. , . , ' . t . ; I... . ,. . , / ! . a > . ;. - ,,:,,:,

Figure 2 uses data: available .from.Marks. and spencer?^ :archives and the

.

more consistent data from its annual reports since floatati~n~~.to chart the

:,. ' " : " , , ". 1. , I ' , % ~ $ < , 8 t 1 ;,3 t , 1 . .; '...,> .

development of,the number of stores the company has operated. From a

. o . . , . . , . l I I I I

M $ ' i s & - ! '- .leeo'. ' . 19id. ' ', "' . , "' 1 . ' 8 . .' ,;; , ,

1920 , ' 1960 1980 2000

. , . , . I ( . . : I , .. , . . .;',.,.. ;. .I:,. . . ..' . . , . ' " kAR . .

S0URCE::Marks 8 Spencer ~ n n u a lReports. .,;. .:, ,,. :..:, . i: ! t . .

and Archive,Matenal , . , I . I . . . 2 ! . . .

single outlet in 1884.the nuinber-of outletsagrew ~lowly~and erratically,

sometimes .by the.purchase of similhr :businesses .[~ees,.1969]. It would

64 T H E S E R V I C EINDUSTRIES J O U R N A L

appear that some consolidation occurred in the early 1920s. From 1926 to

1939 the number of stores grew but in a more sustained manner. In 1900

most shops were small bazaars, typically 30 to 70 feet long by 6 to 13 feet

wide [Briggs, 19841. The capital raised from floatation in 1926 was used to

fund a rapid building and rebuilding programme. Between 1931 and 1935

alone 129 stores were built or rebuilt. By 1940 the company traded from

almost the same number of locations as it has today. This phase of

expansion was typical of a number of multiple retail businesses in the early

part of the twentieth century [Jeffreys, 19541. The separation of the

activities of making and selling goods dated from the industrial revolution

but the development of such large retail businesses did not occur until the

twentieth century [Davies and Hanis, 19901, largely due to the constraints

of legislation designed to aid the small scale retailer. Although resale price

maintenance legislation persisted until the 1960s in Britain [Corina, 197 I],

retailers such as Marks and Spencer found ways both to circumvent it and

to compete on price, in the latter case by concentrating on the sale of own

brand merchandise. It was this price advantage that was so attractive to the

emerging working classes in the new, industrial towns and cities. After

resale price maintenance declined, large scale retailers were able to

negotiate more favourable terms from suppliers more easily, adding to their

cost and price advantage. Marks and Spencer had gained an early lead

through its focus on own brands that were less influenced by price

maintenance during this phase than the supplier branded goods sold by most

of their rivals.

P H A S E 111 G R O W T HI N S T O R E S I Z E(1945-95)

After the Second World War, the number of stores increased far more

slowly. Figures 3 and 4 provide a clear picture of how the company

increased sales volume, not now by increasing the number of stores but by

increasing the average size of each store and with it the range of products

that could be sold. Most stores shared an architectural feature that facilitated

such a strategy, a structural cube, stores being built in multiples of such. As

a result they could be added to in any dimension with relative ease. The

benefits to the retailer from operating larger stores include economies of

scale [NEDO, 19881, and also economies of scope by increasing the range

offered to shoppers [NEDO, 19881. It costs little more to serve a customer

spending £40 than if they spend £4. Expanding the product range increases

the likelihood of multiple purchases.

The total sales areas expanded from 1928 to 1995 by almost exactly 30

times, and this expansion was due substantially to increases in the size of

stores rather than in their number, as had been the case in the second phase

appear that some consolidation occurred in the early 1920s. From 1926 to

1939 the number of stores grew but in a more sustained manner. In 1900

most shops were small bazaars, typically 30 to 70 feet long by 6 to 13 feet

wide [Briggs, 19841. The capital raised from floatation in 1926 was used to

fund a rapid building and rebuilding programme. Between 1931 and 1935

alone 129 stores were built or rebuilt. By 1940 the company traded from

almost the same number of locations as it has today. This phase of

expansion was typical of a number of multiple retail businesses in the early

part of the twentieth century [Jeffreys, 19541. The separation of the

activities of making and selling goods dated from the industrial revolution

but the development of such large retail businesses did not occur until the

twentieth century [Davies and Hanis, 19901, largely due to the constraints

of legislation designed to aid the small scale retailer. Although resale price

maintenance legislation persisted until the 1960s in Britain [Corina, 197 I],

retailers such as Marks and Spencer found ways both to circumvent it and

to compete on price, in the latter case by concentrating on the sale of own

brand merchandise. It was this price advantage that was so attractive to the

emerging working classes in the new, industrial towns and cities. After

resale price maintenance declined, large scale retailers were able to

negotiate more favourable terms from suppliers more easily, adding to their

cost and price advantage. Marks and Spencer had gained an early lead

through its focus on own brands that were less influenced by price

maintenance during this phase than the supplier branded goods sold by most

of their rivals.

P H A S E 111 G R O W T HI N S T O R E S I Z E(1945-95)

After the Second World War, the number of stores increased far more

slowly. Figures 3 and 4 provide a clear picture of how the company

increased sales volume, not now by increasing the number of stores but by

increasing the average size of each store and with it the range of products

that could be sold. Most stores shared an architectural feature that facilitated

such a strategy, a structural cube, stores being built in multiples of such. As

a result they could be added to in any dimension with relative ease. The

benefits to the retailer from operating larger stores include economies of

scale [NEDO, 19881, and also economies of scope by increasing the range

offered to shoppers [NEDO, 19881. It costs little more to serve a customer

spending £40 than if they spend £4. Expanding the product range increases

the likelihood of multiple purchases.

The total sales areas expanded from 1928 to 1995 by almost exactly 30

times, and this expansion was due substantially to increases in the size of

stores rather than in their number, as had been the case in the second phase

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EVOLUTION OF MARKS A N D SPENCER 65

FIGURE 3

AVERAGE S T O R E S I Z E

1940 1960

YEAR

SOURCE: Marks 8 Spencer Annual Reports

and Archives

FIGURE 4

S A L E S AREA

1900 1920 1940 1960 1980 2000

YEAR

SOURCE: Marks 8 Spencer Annual Repom

FIGURE 3

AVERAGE S T O R E S I Z E

1940 1960

YEAR

SOURCE: Marks 8 Spencer Annual Reports

and Archives

FIGURE 4

S A L E S AREA

1900 1920 1940 1960 1980 2000

YEAR

SOURCE: Marks 8 Spencer Annual Repom

66 T H E SERVICE I N D U S T R I E SJ O U R N A L

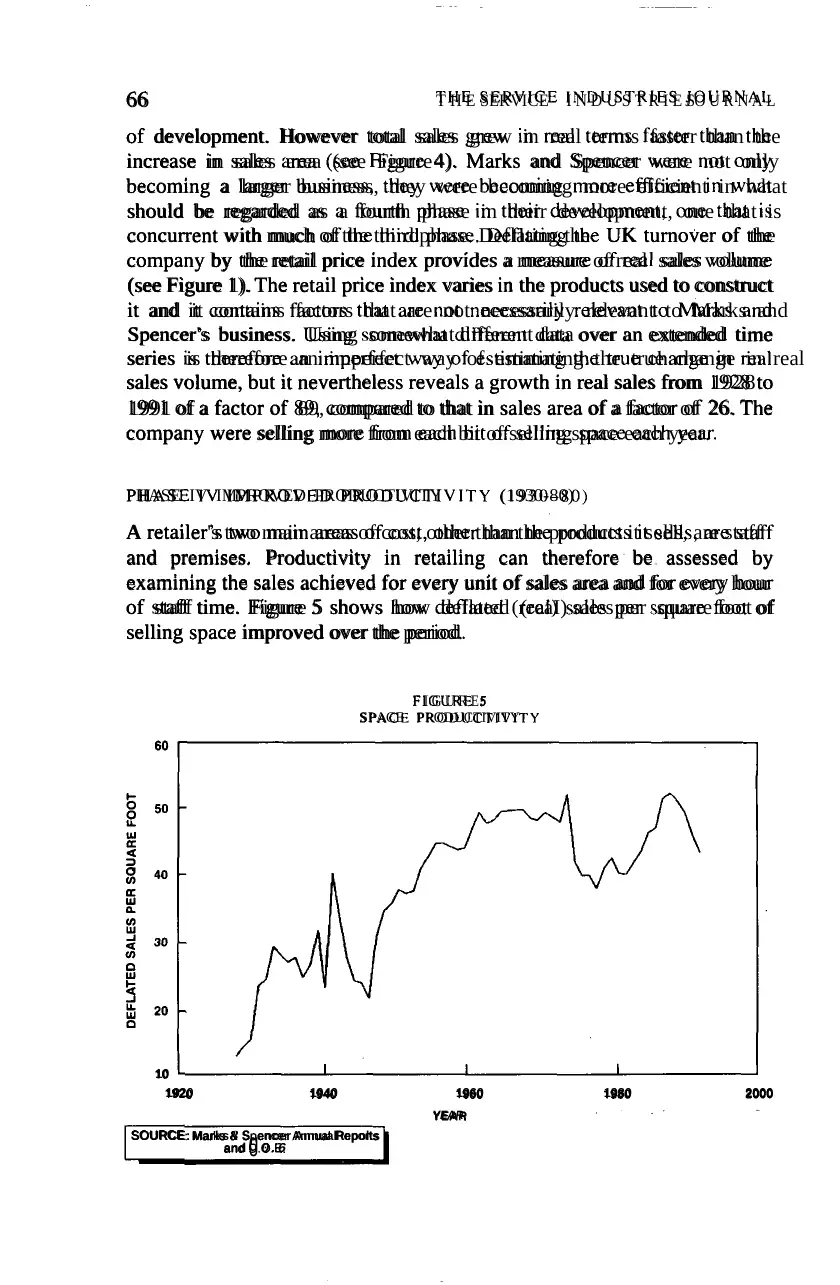

of development. However total sales grew in real terms faster than the

increase in sales area (see Figure 4). Marks and Spencer were not only

becoming a larger business, they were becoming more efficient in what

should be regarded as a fourth phase in their development, one that is

concurrent with much of the third phase. Deflating the UK turnover of the

company by the retail price index provides a measure of real sales volume

(see Figure 1). The retail price index varies in the products used to construct

it and it contains factors that are not necessarily relevant to Marks and

Spencer's business. Using somewhat different data over an extended time

series is therefore an imperfect way of estimating the true change in real

sales volume, but it nevertheless reveals a growth in real sales from 1928 to

1991 of a factor of 89, compared to that in sales area of a factor of 26. The

company were selling more from each bit of selling space each year.

PHASE IV IMPROVED PRODUCTIVITY (1930-80)

A retailer's two main areas of cost, other than the products it sells, are staff

and premises. Productivity in retailing can therefore be assessed by

examining the sales achieved for every unit of sales area and for every hour

of staff time. Figure 5 shows how deflated (reaI) sales per square foot of

selling space improved over the period.

F I G U R E 5

SPACE PRODUCTIVITY

10

1920 1940 1960 1980 2000

YEAR

SOURCE: Marks 8 S encer AnnualRepolts

and g 0.6

of development. However total sales grew in real terms faster than the

increase in sales area (see Figure 4). Marks and Spencer were not only

becoming a larger business, they were becoming more efficient in what

should be regarded as a fourth phase in their development, one that is

concurrent with much of the third phase. Deflating the UK turnover of the

company by the retail price index provides a measure of real sales volume

(see Figure 1). The retail price index varies in the products used to construct

it and it contains factors that are not necessarily relevant to Marks and

Spencer's business. Using somewhat different data over an extended time

series is therefore an imperfect way of estimating the true change in real

sales volume, but it nevertheless reveals a growth in real sales from 1928 to

1991 of a factor of 89, compared to that in sales area of a factor of 26. The

company were selling more from each bit of selling space each year.

PHASE IV IMPROVED PRODUCTIVITY (1930-80)

A retailer's two main areas of cost, other than the products it sells, are staff

and premises. Productivity in retailing can therefore be assessed by

examining the sales achieved for every unit of sales area and for every hour

of staff time. Figure 5 shows how deflated (reaI) sales per square foot of

selling space improved over the period.

F I G U R E 5

SPACE PRODUCTIVITY

10

1920 1940 1960 1980 2000

YEAR

SOURCE: Marks 8 S encer AnnualRepolts

and g 0.6

EVOLUTION O F M A R K S A N D , S P E N C E R 67

The data in some of the war years are somewhat unreliable leading to an

erratic change from year to year. Nevertheless the improvement in space

productivity from 1930 to 1960 is impressive . From then on, no significant

increases have been achieved.

FIGURE 6

EMPLOYEE PRODUCTIVITY

4

& .',? , ., . 1950, : : . , , ' 1 9 6 ( 1 ; , .1?'0 i . 1980 . , , . 1 9 9 0 . . 2000

. . . . . . . . . . . . .L , . ,. , , 1

YEAR

. . 1 , : . . .

SOURCE: Marks.& Spencer Annual Reports , . . . . . . .,. . . . . and Archives. D.O.E. .,,: :..... : ' . . I ~ . . . .

. . . . .. . ..', .:- .<' . . ., . , .. ? i, ./ , . I . , , . '

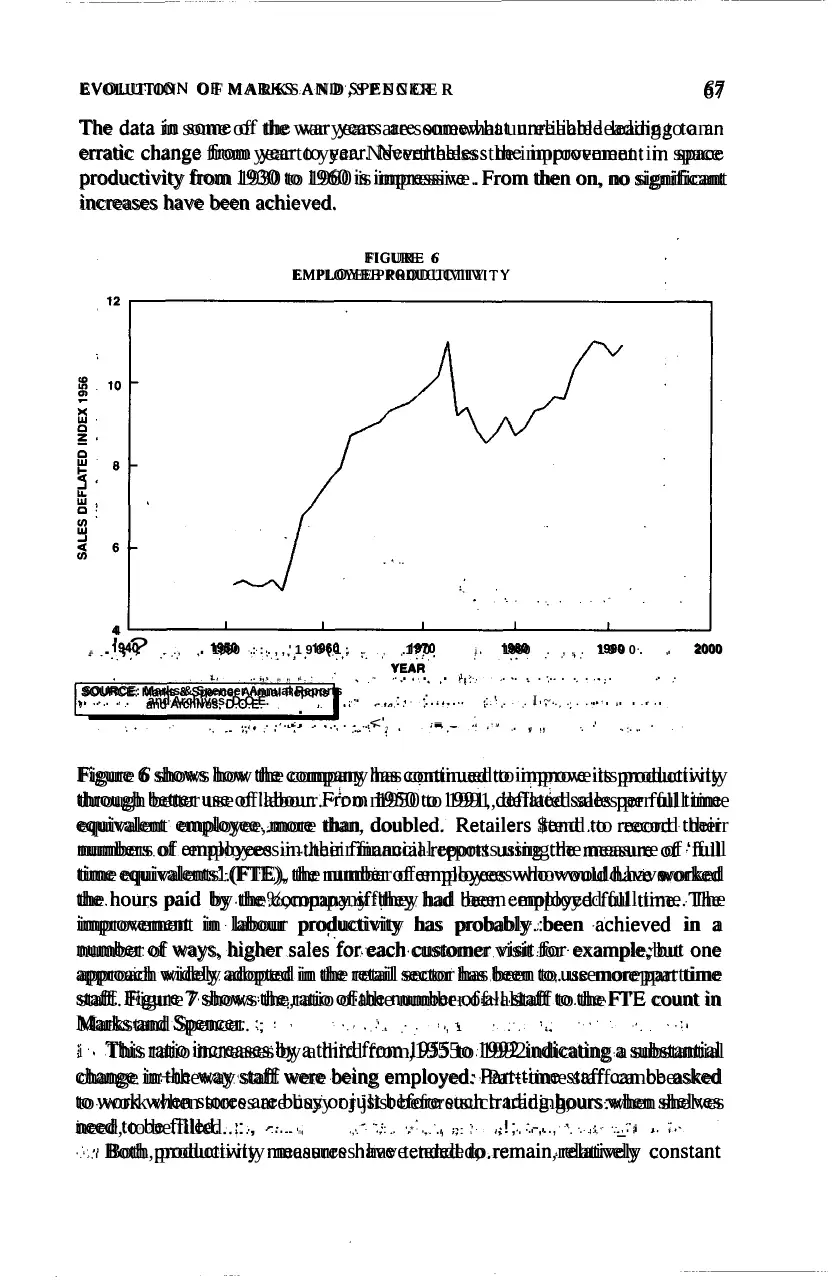

Figure 6 shows how the company has continued to improve its productivity

through better use of labour.~ r o m1950 to 1991, deflated sales per full time

equivalent employee,.more than, doubled. Retailers $tend .to record their

numbers of employees in .their financial reports using the measure of 'full

time equivalentsl.(FTE), the number of employees who~would.haveworked

the hours paid by the%,companysif'they had been employed full time. The

improvement in labour productivity has probably.:been achieved in a

number of ways, higher sales for each customer visit for example;but one

approach widely adopted in the retail sector has been to. usemorepparttime

staff. Figure 7 shows the,ratio ofathe number.of~al1staff to the FI'E count in

Markstand Spencer. ; , 1

i This ratio increases by a third from,1955to 1992indicating a substantial

change in+theway staff were being employed: Part-time staff cancbeasked

to .work when stores are busy or jlist beforetsuch trading,hours:when shelves

. . .

need, to be.filled.. : , -.. . m e ,. ,: . .* ,. ., ;: .s ,!; . .-,.., '. . ,:, .. , .

_. i 1. 5 . -

.'.,I Both, productivity measures have .tended,to.remain,relatively constant

The data in some of the war years are somewhat unreliable leading to an

erratic change from year to year. Nevertheless the improvement in space

productivity from 1930 to 1960 is impressive . From then on, no significant

increases have been achieved.

FIGURE 6

EMPLOYEE PRODUCTIVITY

4

& .',? , ., . 1950, : : . , , ' 1 9 6 ( 1 ; , .1?'0 i . 1980 . , , . 1 9 9 0 . . 2000

. . . . . . . . . . . . .L , . ,. , , 1

YEAR

. . 1 , : . . .

SOURCE: Marks.& Spencer Annual Reports , . . . . . . .,. . . . . and Archives. D.O.E. .,,: :..... : ' . . I ~ . . . .

. . . . .. . ..', .:- .<' . . ., . , .. ? i, ./ , . I . , , . '

Figure 6 shows how the company has continued to improve its productivity

through better use of labour.~ r o m1950 to 1991, deflated sales per full time

equivalent employee,.more than, doubled. Retailers $tend .to record their

numbers of employees in .their financial reports using the measure of 'full

time equivalentsl.(FTE), the number of employees who~would.haveworked

the hours paid by the%,companysif'they had been employed full time. The

improvement in labour productivity has probably.:been achieved in a

number of ways, higher sales for each customer visit for example;but one

approach widely adopted in the retail sector has been to. usemorepparttime

staff. Figure 7 shows the,ratio ofathe number.of~al1staff to the FI'E count in

Markstand Spencer. ; , 1

i This ratio increases by a third from,1955to 1992indicating a substantial

change in+theway staff were being employed: Part-time staff cancbeasked

to .work when stores are busy or jlist beforetsuch trading,hours:when shelves

. . .

need, to be.filled.. : , -.. . m e ,. ,: . .* ,. ., ;: .s ,!; . .-,.., '. . ,:, .. , .

_. i 1. 5 . -

.'.,I Both, productivity measures have .tended,to.remain,relatively constant

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T H E SERVICE INDUSTRIES J O U R N A L

F I G U R E 7

USE OF PART T I M E STAFF

1940 1950 1960 1970 1980 1990 2000

YEAR

I SOURCE: Marks B Spencer Annual Repofts

over the last two decades, indicating that the company is finding it more

difficult to achieve better results in this way. A fifth phase in their search for

sales growth and profitability was needed and a very different approach can

be discovered from the 1980s onwards, that of substantial diversification.

P H A S E V D I V E R S I F I C A T I O N(1980 - C U R R E N T : ,

Retailers can diversify by entering new types of retailing or other types of

activity or they can enter new geographical markets with existing retail

activities. Marks and Spencer have done all three. Early moves into

internationalisation followed a fear of nationalisation by an incoming

Labour administration in the immediate post-war years. Links with

Woolworth (no relation to other companies of the same name) in South

Africa and the acquisition of businesses in Canada began a process that

failed to contribute significantly to sales or profit until other retail

businesses were purchased, Brooks Brothers and Kings Supermarkets,

relatively recently. Exports of St Michael merchandise have made a small

but significant contribution for some years but the growth first of franchised

stores and thereafter of a company owned chain in other European markets

hinted at the development of a truly global business, one where the retail

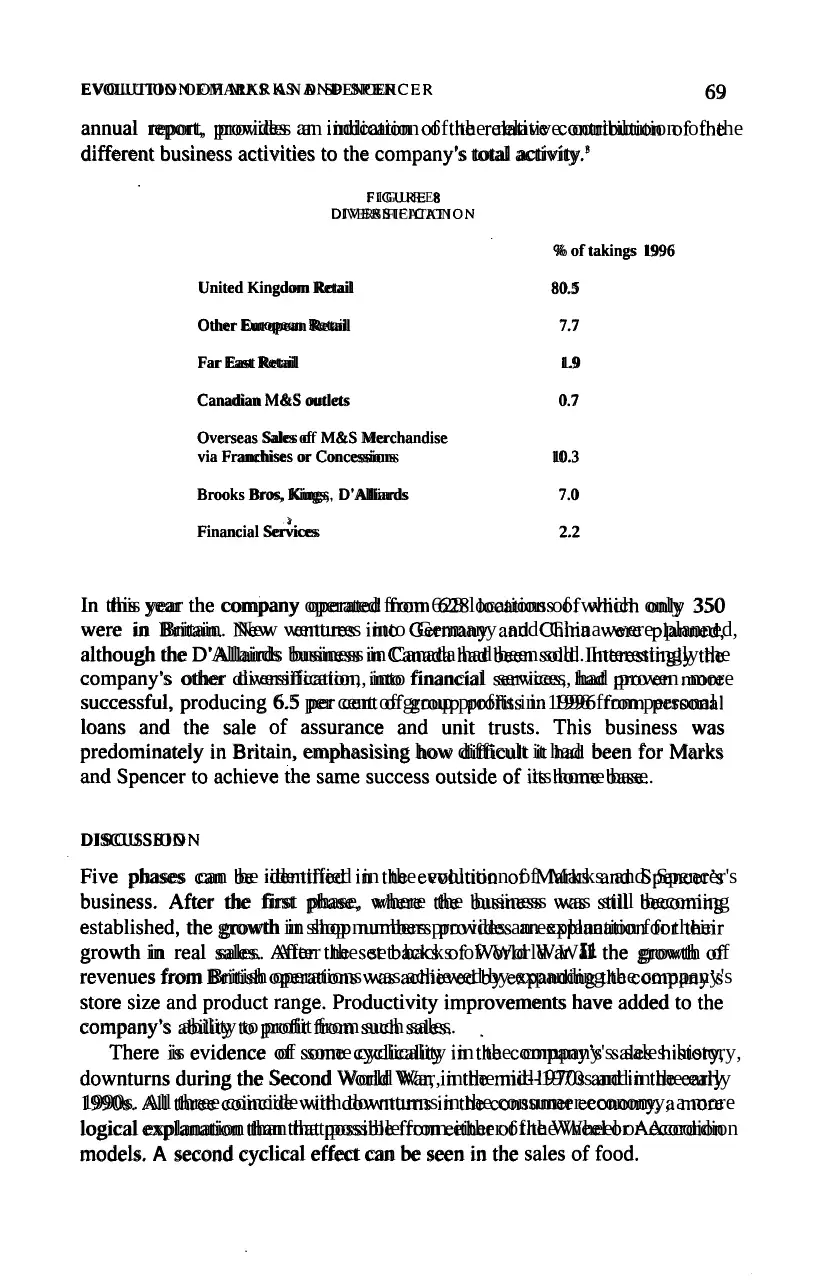

format is similar around the world after 1980. Figure 8, taken from the 1996

F I G U R E 7

USE OF PART T I M E STAFF

1940 1950 1960 1970 1980 1990 2000

YEAR

I SOURCE: Marks B Spencer Annual Repofts

over the last two decades, indicating that the company is finding it more

difficult to achieve better results in this way. A fifth phase in their search for

sales growth and profitability was needed and a very different approach can

be discovered from the 1980s onwards, that of substantial diversification.

P H A S E V D I V E R S I F I C A T I O N(1980 - C U R R E N T : ,

Retailers can diversify by entering new types of retailing or other types of

activity or they can enter new geographical markets with existing retail

activities. Marks and Spencer have done all three. Early moves into

internationalisation followed a fear of nationalisation by an incoming

Labour administration in the immediate post-war years. Links with

Woolworth (no relation to other companies of the same name) in South

Africa and the acquisition of businesses in Canada began a process that

failed to contribute significantly to sales or profit until other retail

businesses were purchased, Brooks Brothers and Kings Supermarkets,

relatively recently. Exports of St Michael merchandise have made a small

but significant contribution for some years but the growth first of franchised

stores and thereafter of a company owned chain in other European markets

hinted at the development of a truly global business, one where the retail

format is similar around the world after 1980. Figure 8, taken from the 1996

EVOLUTION OF MARKS A N D SPENCER 69

annual report, provides an indication of the relative contribution of the

different business activities to the company's total activity.'

F I G U R E 8

DIVERSIFICATION

United Kingdom Retail

% of takings 1996

80.5

Other European Retail 7.7

Far East Retail 1.9

Canadian M&S outlets 0.7

Overseas Sales of M&S Merchandise

via Franchises or Concessions 10.3

Brooks Bros, Kings, D'Alliards 7.0

>

Financial Services 2.2

In this year the company operated from 628 locations of which only 350

were in Britain. New ventures into Germany and China were planned,

although the D'Allairds business in Canada had been sold. Interestingly the

company's other diversification, into financial services, had proven more

successful, producing 6.5 per cent of group profits in 1996 from personal

loans and the sale of assurance and unit trusts. This business was

predominately in Britain, emphasising how difficult it had been for Marks

and Spencer to achieve the same success outside of its home base.

DISCUSSION

Five phases can be identified in the evolution of Marks and Spencer's

business. After the first phase, where the business was still becoming

established, the growth in shop numbers provides an explanation for their

growth in real sales. After the set backs of World WarI1 the growth of

revenues from British operations was achieved by expanding the company's

store size and product range. Productivity improvements have added to the

company's ability to profit from such sales. ,

There is evidence of some cyclicality in the company's sales history,

downturns during the Second World War, in the mid-1970s and in the early

1990s. All three coincide with downturns in the consumer economy, a more

logical explanation than that possible from either of the Wheel or Accordion

models. A second cyclical effect can be seen in the sales of food.

annual report, provides an indication of the relative contribution of the

different business activities to the company's total activity.'

F I G U R E 8

DIVERSIFICATION

United Kingdom Retail

% of takings 1996

80.5

Other European Retail 7.7

Far East Retail 1.9

Canadian M&S outlets 0.7

Overseas Sales of M&S Merchandise

via Franchises or Concessions 10.3

Brooks Bros, Kings, D'Alliards 7.0

>

Financial Services 2.2

In this year the company operated from 628 locations of which only 350

were in Britain. New ventures into Germany and China were planned,

although the D'Allairds business in Canada had been sold. Interestingly the

company's other diversification, into financial services, had proven more

successful, producing 6.5 per cent of group profits in 1996 from personal

loans and the sale of assurance and unit trusts. This business was

predominately in Britain, emphasising how difficult it had been for Marks

and Spencer to achieve the same success outside of its home base.

DISCUSSION

Five phases can be identified in the evolution of Marks and Spencer's

business. After the first phase, where the business was still becoming

established, the growth in shop numbers provides an explanation for their

growth in real sales. After the set backs of World WarI1 the growth of

revenues from British operations was achieved by expanding the company's

store size and product range. Productivity improvements have added to the

company's ability to profit from such sales. ,

There is evidence of some cyclicality in the company's sales history,

downturns during the Second World War, in the mid-1970s and in the early

1990s. All three coincide with downturns in the consumer economy, a more

logical explanation than that possible from either of the Wheel or Accordion

models. A second cyclical effect can be seen in the sales of food.

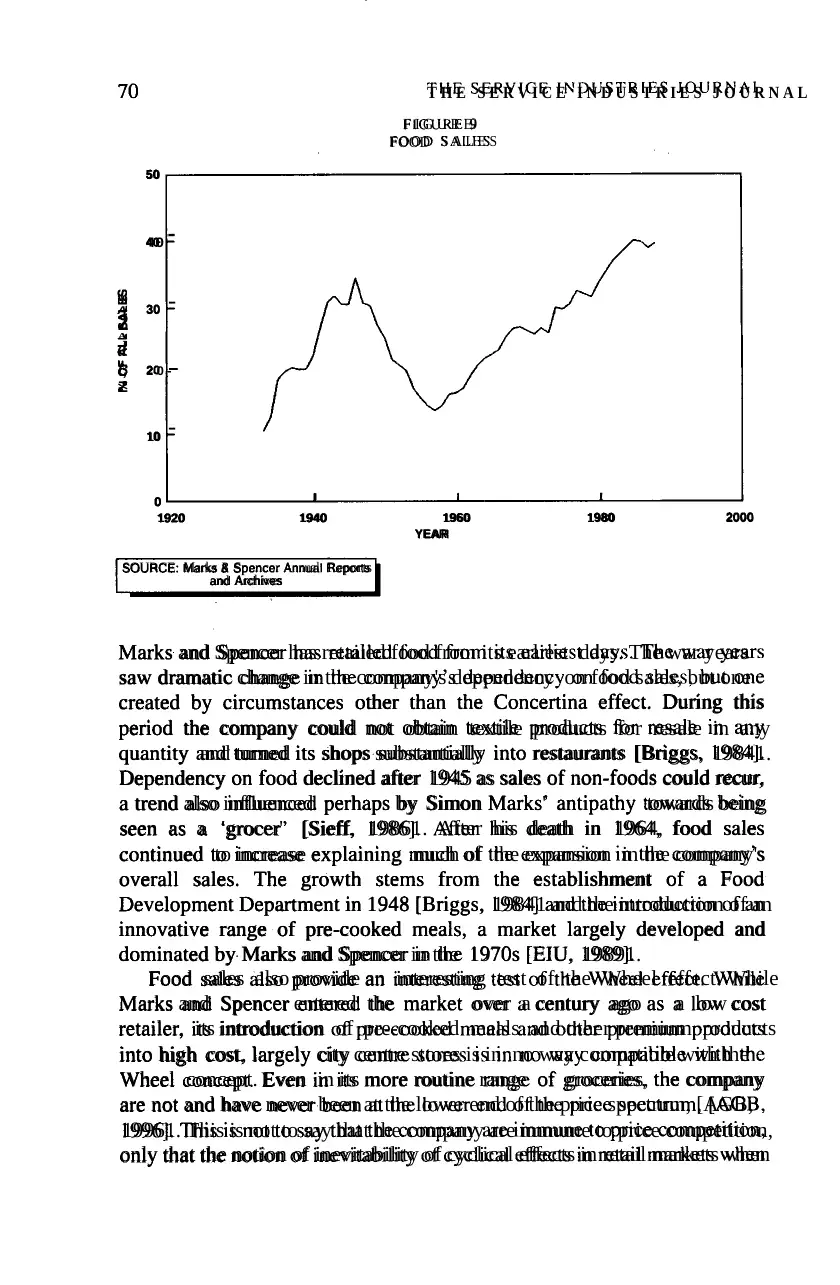

70 T H E S E R V I C E I N D U S T R I E S J O U R N A L

F I G U R E9

FOOD S A L E S

Marks and Spencer has retailed food from its earliest days. The war years

saw dramatic change in the company's dependency on food sales, but one

created by circumstances other than the Concertina effect. During this

period the company could not obtain textile products for resale in any

quantity and turned its shops substantially into restaurants [Briggs, 19841.

Dependency on food declined after 1945 as sales of non-foods could recur,

a trend also influenced perhaps by Simon Marks' antipathy towards being

seen as a 'grocer' [Sieff, 19861. After his death in 1964, food sales

continued to increase explaining much of the expansion in the company's

overall sales. The growth stems from the establishment of a Food

Development Department in 1948 [Briggs, 19841 and the introduction of an

innovative range of pre-cooked meals, a market largely developed and

dominated by Marks and Spencer in the 1970s [EIU, 19891.

Food sales also provide an interesting test of the Wheel effect. While

Marks and Spencer entered the market over a century ago as a low cost

retailer, its introduction of pre-cooked meals and other premium products

into high cost, largely city centre stores is in no way compatible with the

Wheel concept. Even in its more routine range of groceries, the company

are not and have never been at the lower end of the price spectrum, [AGB,

19961. This is not to say that the company are immune to price competition,

only that the notion of inevitability of cyclical effects in retail markets when

50

40

V)W

A 30

2A

d

t; 2 0 -

Z

10

0

-

-

-

I I 1

1920 1940 1960 1980 2000

YEAR

SOURCE: Marks B Spencer Annual Reports

and Archives

F I G U R E9

FOOD S A L E S

Marks and Spencer has retailed food from its earliest days. The war years

saw dramatic change in the company's dependency on food sales, but one

created by circumstances other than the Concertina effect. During this

period the company could not obtain textile products for resale in any

quantity and turned its shops substantially into restaurants [Briggs, 19841.

Dependency on food declined after 1945 as sales of non-foods could recur,

a trend also influenced perhaps by Simon Marks' antipathy towards being

seen as a 'grocer' [Sieff, 19861. After his death in 1964, food sales

continued to increase explaining much of the expansion in the company's

overall sales. The growth stems from the establishment of a Food

Development Department in 1948 [Briggs, 19841 and the introduction of an

innovative range of pre-cooked meals, a market largely developed and

dominated by Marks and Spencer in the 1970s [EIU, 19891.

Food sales also provide an interesting test of the Wheel effect. While

Marks and Spencer entered the market over a century ago as a low cost

retailer, its introduction of pre-cooked meals and other premium products

into high cost, largely city centre stores is in no way compatible with the

Wheel concept. Even in its more routine range of groceries, the company

are not and have never been at the lower end of the price spectrum, [AGB,

19961. This is not to say that the company are immune to price competition,

only that the notion of inevitability of cyclical effects in retail markets when

50

40

V)W

A 30

2A

d

t; 2 0 -

Z

10

0

-

-

-

I I 1

1920 1940 1960 1980 2000

YEAR

SOURCE: Marks B Spencer Annual Reports

and Archives

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EVOLUTION OF MARKS A N D SPENCER 71

retailers trade up or expand their ranges must be challenged. At best it must

be possible for retailers to manage their businesses so as to avoid such

happenings, as illustrated by this analysis.

, A better understanding is needed of how retail businesses can survive

and prosper over the longer=term.-Thisanalysis of Marks and Spencer has

demonstrated the meed for any, business to be adaptive. The,company has

followed a number of complementary, but different strategies. Such

strategies often evolve from one another and overlap in their time frame, but

they are distinct. They are also long-term. The focus on a growth in store

numbers lasted ten years, that on store size over 50 years. The less

successful, approach of internationalisation as part of diversification began

in 1948 and was only paying substantial dividends by the 1990s. What is

noticeable about such observations is the maintenance of a simple, easily

understood directiqn for the business,,one that would have had to be passed

on from one generation of management to another. he influence of the

Marks and Sieff family interests are likely to have been important factors in

the early years. While the last'two chjef executives of Marks and Spencer

have not been members of either family,they,have both been managers with

a lifetime of experience within the bu~iness.~ Such continuity can be

associated with the long-term evolutionary progress of the business. This

must be compared with the approach adopted by sohe of their competitors,

for example House of Fraser, BhS, Debenhams and NEXT (once

Hepworths), where management and strategies have changed frequently and

often radically. Such businesses have at certain times demonstrated faster

rates of growth than Marks and Spencer, but good periods of trading have

been followed or interrupted by more fallow years. Retailing is often

referred to, with the label 'fast changing' and in many ways it is as retailers

react to the ever changing demands of customers and changes in the goods

they are offered by suppliers. Nevertheless the long-term survival and

success of this one company suggests the need to subordinate such

reactivity to a longer term vision of how growth is to be achieved.

Marks and Spencer's experience of international retailing provides a

further example of the relative benefits of thegradua1,versusthe accelerated

approach to development. Three existing businesses have been purchased

since 1946, D' Alliards in Canada, Brooks Brother and Kings' Supermarkets

in America. D'Alliards has been sold,and Brooks,Brothers has not justified

its purchase price. Stores developed out of Marks and Spencer's own

trading format have proven more successful. The benefit of evolution over

revolution is the most important lesson the company has learned over a

century of trading.

In this century of trading,,the company has traded up in price and

expanded its.range of products and services. Both established theories of

retailers trade up or expand their ranges must be challenged. At best it must

be possible for retailers to manage their businesses so as to avoid such

happenings, as illustrated by this analysis.

, A better understanding is needed of how retail businesses can survive

and prosper over the longer=term.-Thisanalysis of Marks and Spencer has

demonstrated the meed for any, business to be adaptive. The,company has

followed a number of complementary, but different strategies. Such

strategies often evolve from one another and overlap in their time frame, but

they are distinct. They are also long-term. The focus on a growth in store

numbers lasted ten years, that on store size over 50 years. The less

successful, approach of internationalisation as part of diversification began

in 1948 and was only paying substantial dividends by the 1990s. What is

noticeable about such observations is the maintenance of a simple, easily

understood directiqn for the business,,one that would have had to be passed

on from one generation of management to another. he influence of the

Marks and Sieff family interests are likely to have been important factors in

the early years. While the last'two chjef executives of Marks and Spencer

have not been members of either family,they,have both been managers with

a lifetime of experience within the bu~iness.~ Such continuity can be

associated with the long-term evolutionary progress of the business. This

must be compared with the approach adopted by sohe of their competitors,

for example House of Fraser, BhS, Debenhams and NEXT (once

Hepworths), where management and strategies have changed frequently and

often radically. Such businesses have at certain times demonstrated faster

rates of growth than Marks and Spencer, but good periods of trading have

been followed or interrupted by more fallow years. Retailing is often

referred to, with the label 'fast changing' and in many ways it is as retailers

react to the ever changing demands of customers and changes in the goods

they are offered by suppliers. Nevertheless the long-term survival and

success of this one company suggests the need to subordinate such

reactivity to a longer term vision of how growth is to be achieved.

Marks and Spencer's experience of international retailing provides a

further example of the relative benefits of thegradua1,versusthe accelerated

approach to development. Three existing businesses have been purchased

since 1946, D' Alliards in Canada, Brooks Brother and Kings' Supermarkets

in America. D'Alliards has been sold,and Brooks,Brothers has not justified

its purchase price. Stores developed out of Marks and Spencer's own

trading format have proven more successful. The benefit of evolution over

revolution is the most important lesson the company has learned over a

century of trading.

In this century of trading,,the company has traded up in price and

expanded its.range of products and services. Both established theories of

72 T H E SERVICE INDUSTRIES JOURNAL

retail evolution suggest that this would make the business vulnerable to

lower cost, lower price retailers on the one hand and more focused retailers

on the other. Neither theory is then satisfactory. Both are empirically

derived rather than theoretically grounded. Theoretical models of strategic

change exist in the mainstream of the strategic literature. It could be time to

bury both of the retail specific approaches in favour of more generalisable

models that could prove more useful in understanding the evolution of any

business.

NOTES

I. The retail price index is recalculated regularly to reflect the prices paid for a range of

commonly purchased items. The selection of items changes to reflect changes in the

purchasing patterns of the British public. The data is available as a number of series. Where

these overlap, the author has scaled earlier series to be compatible with later series. More

recent data are available from the CSO's Annual Abstract of Statistics. Earlier series were

taken from Mitchell [1975].

2. The data series presented here are derived partly from Marks and Spencer's annual report and

accounts and partly from archive material made available to the author by the late Mr Paul

Bookbinder of Marks and Spencer. Prior to 1928 the data are exclusively from archive

material. Some data series began more recently, such as the recording of employee numbers

and this is reflected in the Figures.

3. The data series used in this article represent only the UK retail trading of Marks and Spencer

unless otherwise stated. From the early 1990s the significance of financial services and

international trading increases and the author has estimated UK sales. More recently the

company has reported UK retail sales separately.

4. This paper was written prior to the changes in senior management in 1999.

REFERENCES

AGB, 1996, Retail Audit Figures, Audits of Great Britain, Private Communication.

Adburgham, A., 1964, 1981, Shops and Shopping, first and second editions, London: Banie and

Jenkins.

Briggs, A., 1984,Marks and Spencer 1884-1984, A Centenary History London: Octopus Books.

Brown, S., 1988, 'The Wheel of the Wheel of Retailing'. lnternationtrl Jourrial of Retailing, Vol.

3, No. 1, pp. 16-25.

Corina, M., 1971, Pile it High, Sell it Cheap, London: Weidenfield and Nicholson.

Davidson, W.R., A.D. Bates and S.J. Bass, 1976, 'The Retail Life Cycle', Harvard Business

Review, Nov./Dec., pp. 89-96.

Davies, G., 1992, 'Innovation in Retailing', Crearivirj and Innovcrtir~nMana~ement, Vol. 1, No.

4, pp. 230-39.

Davies, G. and K. Hams, 1990, Small Business, The Independent Remiler; London: Macmillan.

EIU, 1989, Retail Business No. 382, Chilled Foods. Dec., Economist Intelligence Unit.

Ferry, J.W., 1960,A History of the Departnierrt Store, Ncw York: Macmillan.

Hollander S.C., 1966, 'Notes on the Retail Accordion', Journal c~Reroilitig, Vol. 42, No. 2, p.

24.

Hollander, S.C., 1960, 'The Wheel of Retailing', Jourrlal of Marketing, July, pp. 37-42.

Jeffreys, J.B., 1954, Retail Trcrding in Britain 1850-1950, Cambridge: Cambridge University

Press.

Knee, D. and D. Walters, 1985, Strateg)l it1 Retailing,Oxford: Philip Allan, p. 41.

McNair, M.P., 1958, 'Significant Trends and Developments in the Postwar Period', in A.E.

Smith, ed., Competitive Distribution In a Free High Level Econorny, Pittsburgh: University

retail evolution suggest that this would make the business vulnerable to

lower cost, lower price retailers on the one hand and more focused retailers

on the other. Neither theory is then satisfactory. Both are empirically

derived rather than theoretically grounded. Theoretical models of strategic

change exist in the mainstream of the strategic literature. It could be time to

bury both of the retail specific approaches in favour of more generalisable

models that could prove more useful in understanding the evolution of any

business.

NOTES

I. The retail price index is recalculated regularly to reflect the prices paid for a range of

commonly purchased items. The selection of items changes to reflect changes in the

purchasing patterns of the British public. The data is available as a number of series. Where

these overlap, the author has scaled earlier series to be compatible with later series. More

recent data are available from the CSO's Annual Abstract of Statistics. Earlier series were

taken from Mitchell [1975].

2. The data series presented here are derived partly from Marks and Spencer's annual report and

accounts and partly from archive material made available to the author by the late Mr Paul

Bookbinder of Marks and Spencer. Prior to 1928 the data are exclusively from archive

material. Some data series began more recently, such as the recording of employee numbers

and this is reflected in the Figures.

3. The data series used in this article represent only the UK retail trading of Marks and Spencer

unless otherwise stated. From the early 1990s the significance of financial services and

international trading increases and the author has estimated UK sales. More recently the

company has reported UK retail sales separately.

4. This paper was written prior to the changes in senior management in 1999.

REFERENCES

AGB, 1996, Retail Audit Figures, Audits of Great Britain, Private Communication.

Adburgham, A., 1964, 1981, Shops and Shopping, first and second editions, London: Banie and

Jenkins.

Briggs, A., 1984,Marks and Spencer 1884-1984, A Centenary History London: Octopus Books.

Brown, S., 1988, 'The Wheel of the Wheel of Retailing'. lnternationtrl Jourrial of Retailing, Vol.

3, No. 1, pp. 16-25.

Corina, M., 1971, Pile it High, Sell it Cheap, London: Weidenfield and Nicholson.

Davidson, W.R., A.D. Bates and S.J. Bass, 1976, 'The Retail Life Cycle', Harvard Business

Review, Nov./Dec., pp. 89-96.

Davies, G., 1992, 'Innovation in Retailing', Crearivirj and Innovcrtir~nMana~ement, Vol. 1, No.

4, pp. 230-39.

Davies, G. and K. Hams, 1990, Small Business, The Independent Remiler; London: Macmillan.

EIU, 1989, Retail Business No. 382, Chilled Foods. Dec., Economist Intelligence Unit.

Ferry, J.W., 1960,A History of the Departnierrt Store, Ncw York: Macmillan.

Hollander S.C., 1966, 'Notes on the Retail Accordion', Journal c~Reroilitig, Vol. 42, No. 2, p.

24.

Hollander, S.C., 1960, 'The Wheel of Retailing', Jourrlal of Marketing, July, pp. 37-42.

Jeffreys, J.B., 1954, Retail Trcrding in Britain 1850-1950, Cambridge: Cambridge University

Press.

Knee, D. and D. Walters, 1985, Strateg)l it1 Retailing,Oxford: Philip Allan, p. 41.

McNair, M.P., 1958, 'Significant Trends and Developments in the Postwar Period', in A.E.

Smith, ed., Competitive Distribution In a Free High Level Econorny, Pittsburgh: University

EVOLUTION O F MARKS AND SPENCER 73

of Pittsburgh Press.

Mitchell, B.R., 1975, European Historical Statistics 1750-1970, London: Macmillan.

NEDO, 1988, The Future of tlte High Street, Distributive Trades EDC, London: HMSO.

Rees, G., 1969, St Michael a Hisrory of Marks and Spence,: London: Weidenfield and Nicholson

(2nd edition, 1973, London: Pan Books).

Roth, V.F. and S. Klein, 1993, 'A Theory of Retail Change',International Review of Retail

Distribution and Consumer Research. Vol. 3, No. 2, pp. 167-83.

Sieff, I., 1970, The Memoirs of Israel Sieff, London: Weidenfield and Nicholson.

Sieff, M., 1986, Don1 Ask the Price. the Memoirs of the President of Marks and Spencer,

London: Weidenfield and Nicholson.

Valentin. E.K., 1991, 'Retail Market Structure Scenarios and their Strategic Applications',

Internarionul Review of Reruil Distribution and Consumer Research. Vol. I, No. 3, pp.

285-99.

View publication stats

of Pittsburgh Press.

Mitchell, B.R., 1975, European Historical Statistics 1750-1970, London: Macmillan.

NEDO, 1988, The Future of tlte High Street, Distributive Trades EDC, London: HMSO.

Rees, G., 1969, St Michael a Hisrory of Marks and Spence,: London: Weidenfield and Nicholson

(2nd edition, 1973, London: Pan Books).

Roth, V.F. and S. Klein, 1993, 'A Theory of Retail Change',International Review of Retail

Distribution and Consumer Research. Vol. 3, No. 2, pp. 167-83.

Sieff, I., 1970, The Memoirs of Israel Sieff, London: Weidenfield and Nicholson.

Sieff, M., 1986, Don1 Ask the Price. the Memoirs of the President of Marks and Spencer,

London: Weidenfield and Nicholson.

Valentin. E.K., 1991, 'Retail Market Structure Scenarios and their Strategic Applications',

Internarionul Review of Reruil Distribution and Consumer Research. Vol. I, No. 3, pp.

285-99.

View publication stats

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.