Financial Analysis Report: Evaluating Tesco Plc and Benedict Co.

VerifiedAdded on 2023/04/25

|28

|4782

|443

Report

AI Summary

This report provides a financial analysis of Tesco Plc and Benedict Co. The analysis of Tesco Plc's 2016 annual report highlights the company's investment in supplier and employee relationships, contributing to a positive working environment and customer loyalty. The report identifies key stakeholders such as suppliers, customers, and employees, and examines how Tesco's environmental and social review and corporate governance report demonstrate performance to these stakeholders. The analysis of Benedict Co. reveals a decline in financial condition in 20x1 compared to the previous year, raising concerns about its long-term stability. Key financial ratios, including liquidity, gearing, profitability, efficiency, and investor ratios, are calculated and interpreted to assess Benedict Co.'s financial performance. The report concludes that Benedict Co.'s financial instability would likely disqualify it from a contract tender, favoring a more stable competitor. Desklib offers a range of study tools and resources, including solved assignments and past papers, to support students in their academic endeavors.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Executive Summary:

The report is prepared with the intent to analyse the business performance of Tesco Plc and

Benedict Co. After analysing the annual report of Tesco Plc in 2016, it has been found that the

organisation has made a smart move by investing in supplier and employee relationships that

lead to sound working environment for skilled labour. In addition, it manages to earn supplier

trust as well that has assisted the organisation in offering products at reasonable prices for raising

the loyal customer base and attracting the shoppers to shop from its stores. In case of Benedict

Co, it has been found that the organisation has experienced a significant decline in its financial

condition in 20x1 compared to the past year. Due to such negative image, it would not be

selected after adjudication of the tender documents, although they have been at the top of the list.

The second organisation would be selected owing to the concern that Benedict Co. has not been

a stable organisation in the long-term and the image of the purchaser might be affected in the

market in near future.

Executive Summary:

The report is prepared with the intent to analyse the business performance of Tesco Plc and

Benedict Co. After analysing the annual report of Tesco Plc in 2016, it has been found that the

organisation has made a smart move by investing in supplier and employee relationships that

lead to sound working environment for skilled labour. In addition, it manages to earn supplier

trust as well that has assisted the organisation in offering products at reasonable prices for raising

the loyal customer base and attracting the shoppers to shop from its stores. In case of Benedict

Co, it has been found that the organisation has experienced a significant decline in its financial

condition in 20x1 compared to the past year. Due to such negative image, it would not be

selected after adjudication of the tender documents, although they have been at the top of the list.

The second organisation would be selected owing to the concern that Benedict Co. has not been

a stable organisation in the long-term and the image of the purchaser might be affected in the

market in near future.

2FINANCIAL MANAGEMENT

Table of Contents

Introduction:....................................................................................................................................3

1. Tesco Plc:.....................................................................................................................................3

a. Concept of the term ‘stakeholder’ and three types of stakeholders of Tesco:.........................3

b. Role played by Environmental and Social Review and Corporate Governance Report in

demonstrating its performance to two identified stakeholders:...................................................5

2. Benedict Co.:...............................................................................................................................7

a. Purpose and relevance of the chosen ratios:............................................................................7

b and d. Analysis and application of the chosen ratios in the context of Benedict Co.:..............8

c. Aspect of performance of concern for Benedict Co.:............................................................15

Conclusion:....................................................................................................................................15

References:....................................................................................................................................17

Appendices:...................................................................................................................................20

Table of Contents

Introduction:....................................................................................................................................3

1. Tesco Plc:.....................................................................................................................................3

a. Concept of the term ‘stakeholder’ and three types of stakeholders of Tesco:.........................3

b. Role played by Environmental and Social Review and Corporate Governance Report in

demonstrating its performance to two identified stakeholders:...................................................5

2. Benedict Co.:...............................................................................................................................7

a. Purpose and relevance of the chosen ratios:............................................................................7

b and d. Analysis and application of the chosen ratios in the context of Benedict Co.:..............8

c. Aspect of performance of concern for Benedict Co.:............................................................15

Conclusion:....................................................................................................................................15

References:....................................................................................................................................17

Appendices:...................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Introduction:

The objective of the report is to conduct financial analysis of the two organisations,

which include Tesco Plc and Benedict Co. It would look at the key stakeholders of Tesco along

with utilising the 2016 annual report of the organisation for reviewing its performance in terms

of social and corporate responsibilities against its social and environmental review and corporate

governance report. Tesco Plc runs supermarkets in UK, which intends to earn profits by

investing and selling greater quality products (Tesco plc 2019). Like any other global

organisation, Tesco works with a number of stakeholders like suppliers, customers, investors,

employees, shareholders and others. This paper would analyse the contributions of customers,

suppliers and employees to the financial performance of the organisation. Along with this, the

paper would evaluate the financial condition of Benedict Co., which is one of the organisations

that placed tender for the contract. Therefore, a range of financial ratios would be conducted to

gauge the financial performance of the concerned organisation.

1. Tesco Plc:

a. Concept of the term ‘stakeholder’ and three types of stakeholders of Tesco:

Concept of stakeholder:

As stated by Wood, Wrigley and Coe (2016), stakeholders are individuals, groups or

organisations having concern or interest in an organisation. They could be influenced by or

influence the policies, actions and objectives of the organisation. From the broader perspective,

some stakeholders mainly constitute of creditors, employees, customers, shareholders,

government agencies and others. The stakeholders could be categorised into two major groups,

which include internal stakeholders and external stakeholders. In this context, Jenkins and

Introduction:

The objective of the report is to conduct financial analysis of the two organisations,

which include Tesco Plc and Benedict Co. It would look at the key stakeholders of Tesco along

with utilising the 2016 annual report of the organisation for reviewing its performance in terms

of social and corporate responsibilities against its social and environmental review and corporate

governance report. Tesco Plc runs supermarkets in UK, which intends to earn profits by

investing and selling greater quality products (Tesco plc 2019). Like any other global

organisation, Tesco works with a number of stakeholders like suppliers, customers, investors,

employees, shareholders and others. This paper would analyse the contributions of customers,

suppliers and employees to the financial performance of the organisation. Along with this, the

paper would evaluate the financial condition of Benedict Co., which is one of the organisations

that placed tender for the contract. Therefore, a range of financial ratios would be conducted to

gauge the financial performance of the concerned organisation.

1. Tesco Plc:

a. Concept of the term ‘stakeholder’ and three types of stakeholders of Tesco:

Concept of stakeholder:

As stated by Wood, Wrigley and Coe (2016), stakeholders are individuals, groups or

organisations having concern or interest in an organisation. They could be influenced by or

influence the policies, actions and objectives of the organisation. From the broader perspective,

some stakeholders mainly constitute of creditors, employees, customers, shareholders,

government agencies and others. The stakeholders could be categorised into two major groups,

which include internal stakeholders and external stakeholders. In this context, Jenkins and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

Williamson (2015) advocated that internal stakeholders are those groups that are formally parts

of an organisation, while the external stakeholders are individuals or groups that could affect or

affected by an organisation.

Three types of stakeholders of Tesco Plc:

It is possible to group the stakeholders of an organisation into suppliers, employees,

customers and government. From the annual report of Tesco Plc in 2016, there are three main

types of stakeholders, which include suppliers, customers and its colleagues/staffs. The other

stakeholders are identified as the external stakeholders and for Tesco; these stakeholders include

shareholders along with social and environmental stakeholders. Back to the three major

stakeholders, the organisation clearly indicated about them in its annual report as follows:

The customers are denoted as organisations or individuals purchasing the products or

services or make repeat purchases or recommend the organisation to other shoppers. This group

belongs to the external stakeholders of Tesco Plc and the loyalty of the customers is explained by

the shopping frequency and average weekly spends (Tescoplc.com 2019).

Suppliers are categorised as the second major stakeholders belonging to partnerships and

they fall under connected stakeholders.

` Colleagues are referred to by the organisation as its employees where Tesco invests for

providing better services to the customers. This group falls under the internal stakeholders of the

organisation (Hanson et al. 2016). In addition, Tesco has focused on key performance indicators

of its staffs, in which it referred to the measurements regarding recommendation and great place

for work or shop.

Williamson (2015) advocated that internal stakeholders are those groups that are formally parts

of an organisation, while the external stakeholders are individuals or groups that could affect or

affected by an organisation.

Three types of stakeholders of Tesco Plc:

It is possible to group the stakeholders of an organisation into suppliers, employees,

customers and government. From the annual report of Tesco Plc in 2016, there are three main

types of stakeholders, which include suppliers, customers and its colleagues/staffs. The other

stakeholders are identified as the external stakeholders and for Tesco; these stakeholders include

shareholders along with social and environmental stakeholders. Back to the three major

stakeholders, the organisation clearly indicated about them in its annual report as follows:

The customers are denoted as organisations or individuals purchasing the products or

services or make repeat purchases or recommend the organisation to other shoppers. This group

belongs to the external stakeholders of Tesco Plc and the loyalty of the customers is explained by

the shopping frequency and average weekly spends (Tescoplc.com 2019).

Suppliers are categorised as the second major stakeholders belonging to partnerships and

they fall under connected stakeholders.

` Colleagues are referred to by the organisation as its employees where Tesco invests for

providing better services to the customers. This group falls under the internal stakeholders of the

organisation (Hanson et al. 2016). In addition, Tesco has focused on key performance indicators

of its staffs, in which it referred to the measurements regarding recommendation and great place

for work or shop.

5FINANCIAL MANAGEMENT

b. Role played by Environmental and Social Review and Corporate Governance Report in

demonstrating its performance to two identified stakeholders:

From the three identified stakeholders of Tesco, suppliers and employees/colleagues

have been chosen due to two main reasons. Firstly, in order to become a reputed brand in the

retail sector, the employees are the first individuals found to be involved with the customers

(Bamber and Parry 2014). Secondly, the suppliers are the significant components in sustaining

the aim of the organisation to provide promotional products and stable prices. The two

stakeholder groups have not been chosen randomly, the selection has been due to the association

between the changes of the organisation affecting the way the staffs involve with the suppliers.

Tesco has undertaken certain significant changes in 2014 for redeveloping the

relationship with the suppliers. In October 2014, Tesco has drawn a line under the past and it has

started of resetting its working procedure and for this, the support of the managers and

employees are crucial. According to Zentes, Morschett and Schramm-Klein (2017), the changing

environment meeting the resistance of managers has particular thinking pattern in the working

environment exposed in their long-term experience. In case of Tesco, for dealing with the

possible staff resistance, the management has designed new reward schemes along with initiating

training and induction programs. The external factors could influence the staff behaviour as well

that comprise of government or business policies, communities and others. For managing the

effect of the communities, Tesco has realised its unique change for undertaking favourable

environmental change and its communities by enforcing different national and global projects

(Tescoplc.com 2019).

For dealing with economic and social issues in the environment, it is vital for an

organisation to have a wide competent spectrum including its capability for fostering knowledge

b. Role played by Environmental and Social Review and Corporate Governance Report in

demonstrating its performance to two identified stakeholders:

From the three identified stakeholders of Tesco, suppliers and employees/colleagues

have been chosen due to two main reasons. Firstly, in order to become a reputed brand in the

retail sector, the employees are the first individuals found to be involved with the customers

(Bamber and Parry 2014). Secondly, the suppliers are the significant components in sustaining

the aim of the organisation to provide promotional products and stable prices. The two

stakeholder groups have not been chosen randomly, the selection has been due to the association

between the changes of the organisation affecting the way the staffs involve with the suppliers.

Tesco has undertaken certain significant changes in 2014 for redeveloping the

relationship with the suppliers. In October 2014, Tesco has drawn a line under the past and it has

started of resetting its working procedure and for this, the support of the managers and

employees are crucial. According to Zentes, Morschett and Schramm-Klein (2017), the changing

environment meeting the resistance of managers has particular thinking pattern in the working

environment exposed in their long-term experience. In case of Tesco, for dealing with the

possible staff resistance, the management has designed new reward schemes along with initiating

training and induction programs. The external factors could influence the staff behaviour as well

that comprise of government or business policies, communities and others. For managing the

effect of the communities, Tesco has realised its unique change for undertaking favourable

environmental change and its communities by enforcing different national and global projects

(Tescoplc.com 2019).

For dealing with economic and social issues in the environment, it is vital for an

organisation to have a wide competent spectrum including its capability for fostering knowledge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

acquisition. In order to increase the knowledge base of its staffs, Tesco has widened its training

opportunities by intending to resolve the social challenges. Moreover, the organisation has

initiated flexible working hours along with forming a working environment promoting

communication between colleagues. Such initiative has assisted the employees of Tesco in

enhancing their performance and concentrating on customer satisfaction (Petljak and Štulec

2015). This is evident from “Page 21 of the Annual Report of Tesco”, in which it has been

mentioned that the colleagues have stayed the beating heart of the organisation and they have

carried on putting the customers first while providing superior services (Tescoplc.com 2019).

Another social challenge that Tesco has monitored has been the difference between men and

women, which is a crucial aspect in maintaining transparency in the working environment.

After staff behaviour is addressed, Imrie and Dolton (2014) commented that the

organisations are utilising staff behaviour change interventions for addressing different issues

that include minimisation of energy use, minimisation of greenhouse gas (GHG) emissions,

recycling, minimisation of water usage and rise in use of public transport. This could be realised

in the manner that Tesco has approached its environmental initiative for minimising the food

waste within its business operations. This program has been observed to have favourable effect

on the suppliers, as the latter has minimised their waste and the benefits are extended further to

the communities, in which the food surplus could be distributed to the needy individuals

(Haddock-Millar and Rigby 2015). After the environmental program has been implemented,

there has been minimisation in carbon footprint by 8% from the past year and in contrast to 10

years back, carbon intensity per square feet has been minimised with 41.7% (Tescoplc.com

2019).

acquisition. In order to increase the knowledge base of its staffs, Tesco has widened its training

opportunities by intending to resolve the social challenges. Moreover, the organisation has

initiated flexible working hours along with forming a working environment promoting

communication between colleagues. Such initiative has assisted the employees of Tesco in

enhancing their performance and concentrating on customer satisfaction (Petljak and Štulec

2015). This is evident from “Page 21 of the Annual Report of Tesco”, in which it has been

mentioned that the colleagues have stayed the beating heart of the organisation and they have

carried on putting the customers first while providing superior services (Tescoplc.com 2019).

Another social challenge that Tesco has monitored has been the difference between men and

women, which is a crucial aspect in maintaining transparency in the working environment.

After staff behaviour is addressed, Imrie and Dolton (2014) commented that the

organisations are utilising staff behaviour change interventions for addressing different issues

that include minimisation of energy use, minimisation of greenhouse gas (GHG) emissions,

recycling, minimisation of water usage and rise in use of public transport. This could be realised

in the manner that Tesco has approached its environmental initiative for minimising the food

waste within its business operations. This program has been observed to have favourable effect

on the suppliers, as the latter has minimised their waste and the benefits are extended further to

the communities, in which the food surplus could be distributed to the needy individuals

(Haddock-Millar and Rigby 2015). After the environmental program has been implemented,

there has been minimisation in carbon footprint by 8% from the past year and in contrast to 10

years back, carbon intensity per square feet has been minimised with 41.7% (Tescoplc.com

2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

For offering products at reasonable prices and gaining popularity, Tesco has to redevelop

its trust with the suppliers by maintaining transparency in relationship with them mainly when

the customers provide feedbacks on particular products (Mollah 2014). Such changes between

Tesco and its suppliers are witnessed to have positive impact leading to increase in number of

suppliers. As a result, it has assisted the organisation in experiencing a sharp growth each year.

In case, Tesco is assumed to exercise power over the suppliers, the impact would have been rise

in price and minimisation in product ranges, which would chase away the customers (Rodrigue

2014).

Considering all the above-discussed aspects, the systems and programs that Tesco Plc has

formulated in managing the significant changes enforced within the organisation assisted them in

having favourable effect and reaction on its suppliers and employees. Currently, Tesco is a

highly popular business and it is highly proud of the way its colleagues and suppliers provided

responses to the undertaken changes, as evident from “Page 8 of its Annual Report”

(Tescoplc.com 2019).

2. Benedict Co.:

a. Purpose and relevance of the chosen ratios:

For analysing the financial condition of Benedict Co, a number of financial ratios have

been chosen to meet the needs of the stakeholders. The provided financial statements of the

organisation for the years 20x0 and 20x1 and other materials have been utilised for computing

the relevant ratios. Moreover, the use of literature review has been made for assuring relevance

of the selected ratios, which has assisted in computing and interpreting the ratios for gauging the

financial performance and position of Benedict Co. The ratios mainly used for this report include

the following:

For offering products at reasonable prices and gaining popularity, Tesco has to redevelop

its trust with the suppliers by maintaining transparency in relationship with them mainly when

the customers provide feedbacks on particular products (Mollah 2014). Such changes between

Tesco and its suppliers are witnessed to have positive impact leading to increase in number of

suppliers. As a result, it has assisted the organisation in experiencing a sharp growth each year.

In case, Tesco is assumed to exercise power over the suppliers, the impact would have been rise

in price and minimisation in product ranges, which would chase away the customers (Rodrigue

2014).

Considering all the above-discussed aspects, the systems and programs that Tesco Plc has

formulated in managing the significant changes enforced within the organisation assisted them in

having favourable effect and reaction on its suppliers and employees. Currently, Tesco is a

highly popular business and it is highly proud of the way its colleagues and suppliers provided

responses to the undertaken changes, as evident from “Page 8 of its Annual Report”

(Tescoplc.com 2019).

2. Benedict Co.:

a. Purpose and relevance of the chosen ratios:

For analysing the financial condition of Benedict Co, a number of financial ratios have

been chosen to meet the needs of the stakeholders. The provided financial statements of the

organisation for the years 20x0 and 20x1 and other materials have been utilised for computing

the relevant ratios. Moreover, the use of literature review has been made for assuring relevance

of the selected ratios, which has assisted in computing and interpreting the ratios for gauging the

financial performance and position of Benedict Co. The ratios mainly used for this report include

the following:

8FINANCIAL MANAGEMENT

Liquidity ratios like current ratio and quick ratio, since they are associated with suppliers

and customers

Gearing ratios like interest cover and debt/equity ratio, since they are pertinent to lenders

Profitability ratios that are applicable to lenders, suppliers and customers

Efficiency ratios for analysing the use of resources in order to gauge the performance of

the suppliers

Investor ratios for gauging the performance of the investors like return on equity,

earnings yield, dividend yield, earnings per share and others

b and d. Analysis and application of the chosen ratios in the context of Benedict Co.:

The following ratios have been chosen for evaluating the financial condition of Benedict

Co.:

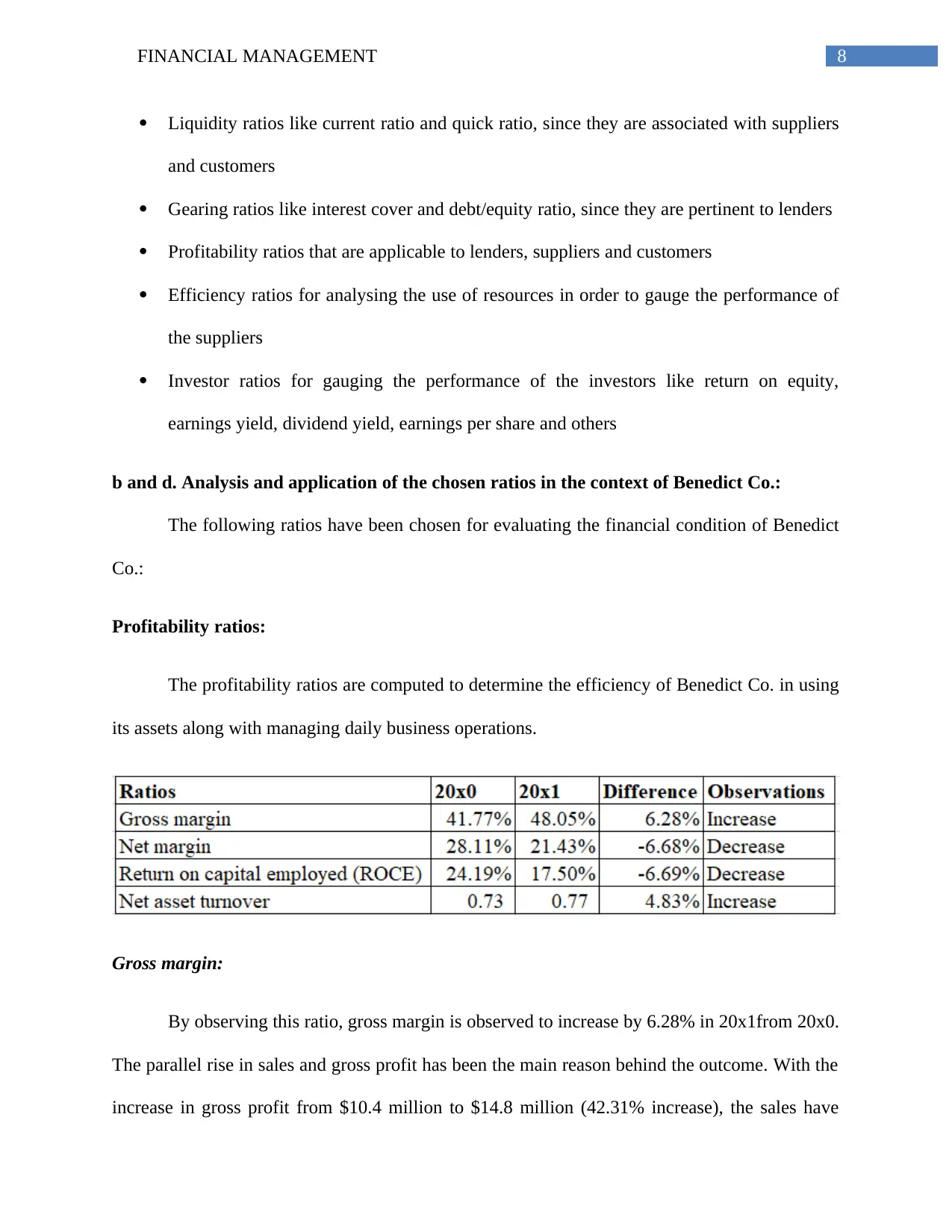

Profitability ratios:

The profitability ratios are computed to determine the efficiency of Benedict Co. in using

its assets along with managing daily business operations.

Gross margin:

By observing this ratio, gross margin is observed to increase by 6.28% in 20x1from 20x0.

The parallel rise in sales and gross profit has been the main reason behind the outcome. With the

increase in gross profit from $10.4 million to $14.8 million (42.31% increase), the sales have

Liquidity ratios like current ratio and quick ratio, since they are associated with suppliers

and customers

Gearing ratios like interest cover and debt/equity ratio, since they are pertinent to lenders

Profitability ratios that are applicable to lenders, suppliers and customers

Efficiency ratios for analysing the use of resources in order to gauge the performance of

the suppliers

Investor ratios for gauging the performance of the investors like return on equity,

earnings yield, dividend yield, earnings per share and others

b and d. Analysis and application of the chosen ratios in the context of Benedict Co.:

The following ratios have been chosen for evaluating the financial condition of Benedict

Co.:

Profitability ratios:

The profitability ratios are computed to determine the efficiency of Benedict Co. in using

its assets along with managing daily business operations.

Gross margin:

By observing this ratio, gross margin is observed to increase by 6.28% in 20x1from 20x0.

The parallel rise in sales and gross profit has been the main reason behind the outcome. With the

increase in gross profit from $10.4 million to $14.8 million (42.31% increase), the sales have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

risen by 23.69% in 20x1 as well. However, the interpretation of this ratio contradicts the past

assumption that the ability of the organisation in generating profits from sales has been

minimised, which could be observed in net margin analysis below. Therefore, it could be stated

that the rise in gross margin is due to rise in sales in comparison to very low cost of sales.

Net margin:

According to the above table, a decline in operating profit has negative impact on net

margin. At the same time, there has been simultaneous rise in sales revenue (23.69% increase)

lowering this ratio from 28.11% in 20x0 to 21.43% in 20x1. A fall in net margin signifies

downfall in the ability of an organisation to utilise revenue effectively for profit generation

(Robinson et al. 2015).

Return on capital employed (ROCE):

The decline in ROCE from 24.19% in 20x0 to 17.50% in 20x1 has been due to a

combination of two factors. The first factor is the decrease in operating profit of the organisation

from $8.7 million in 20x0 to $8.3 million in 20x1 and rise in capital employed from $33 million

in 20x0 to $40 million in 20x1. In this regard, Vogel (2014) indicated that such status reflects the

fall in efficiency of the organisation in utilising capital for profit generation.

Net asset turnover:

For the concerned period, this ratio is observed to increase from 0.73 times to 0.77 times,

which denotes an increase of 4.83% in the ratio due to higher increase in sales compared to

employed capital. As advocated by Williams and Dobelman (2017), such movement signifies

risen by 23.69% in 20x1 as well. However, the interpretation of this ratio contradicts the past

assumption that the ability of the organisation in generating profits from sales has been

minimised, which could be observed in net margin analysis below. Therefore, it could be stated

that the rise in gross margin is due to rise in sales in comparison to very low cost of sales.

Net margin:

According to the above table, a decline in operating profit has negative impact on net

margin. At the same time, there has been simultaneous rise in sales revenue (23.69% increase)

lowering this ratio from 28.11% in 20x0 to 21.43% in 20x1. A fall in net margin signifies

downfall in the ability of an organisation to utilise revenue effectively for profit generation

(Robinson et al. 2015).

Return on capital employed (ROCE):

The decline in ROCE from 24.19% in 20x0 to 17.50% in 20x1 has been due to a

combination of two factors. The first factor is the decrease in operating profit of the organisation

from $8.7 million in 20x0 to $8.3 million in 20x1 and rise in capital employed from $33 million

in 20x0 to $40 million in 20x1. In this regard, Vogel (2014) indicated that such status reflects the

fall in efficiency of the organisation in utilising capital for profit generation.

Net asset turnover:

For the concerned period, this ratio is observed to increase from 0.73 times to 0.77 times,

which denotes an increase of 4.83% in the ratio due to higher increase in sales compared to

employed capital. As advocated by Williams and Dobelman (2017), such movement signifies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

slight improvement in the ability of the organisation in generating revenue effectively from

capital.

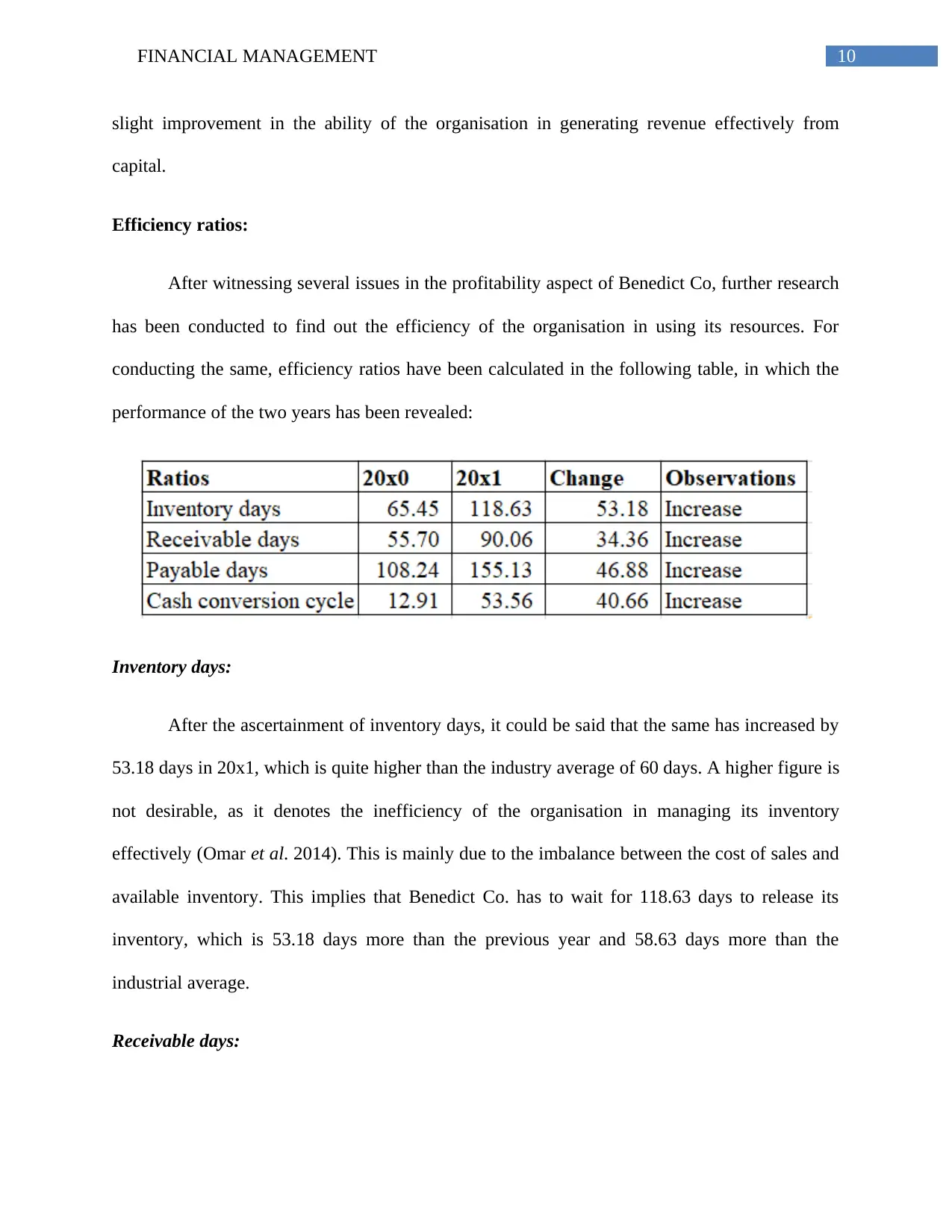

Efficiency ratios:

After witnessing several issues in the profitability aspect of Benedict Co, further research

has been conducted to find out the efficiency of the organisation in using its resources. For

conducting the same, efficiency ratios have been calculated in the following table, in which the

performance of the two years has been revealed:

Inventory days:

After the ascertainment of inventory days, it could be said that the same has increased by

53.18 days in 20x1, which is quite higher than the industry average of 60 days. A higher figure is

not desirable, as it denotes the inefficiency of the organisation in managing its inventory

effectively (Omar et al. 2014). This is mainly due to the imbalance between the cost of sales and

available inventory. This implies that Benedict Co. has to wait for 118.63 days to release its

inventory, which is 53.18 days more than the previous year and 58.63 days more than the

industrial average.

Receivable days:

slight improvement in the ability of the organisation in generating revenue effectively from

capital.

Efficiency ratios:

After witnessing several issues in the profitability aspect of Benedict Co, further research

has been conducted to find out the efficiency of the organisation in using its resources. For

conducting the same, efficiency ratios have been calculated in the following table, in which the

performance of the two years has been revealed:

Inventory days:

After the ascertainment of inventory days, it could be said that the same has increased by

53.18 days in 20x1, which is quite higher than the industry average of 60 days. A higher figure is

not desirable, as it denotes the inefficiency of the organisation in managing its inventory

effectively (Omar et al. 2014). This is mainly due to the imbalance between the cost of sales and

available inventory. This implies that Benedict Co. has to wait for 118.63 days to release its

inventory, which is 53.18 days more than the previous year and 58.63 days more than the

industrial average.

Receivable days:

11FINANCIAL MANAGEMENT

This ratio generally denotes the number of days taken by the debtors to settle their

payments towards an organisation (Wahlen, Baginski and Bradshaw 2014). This number is seen

to rise from 55.70 days in 20x0 to 90.06 days in 20x1, which is 34.36 days more than the

previous year and 35 days more than the industrial average. Thus, the ability of Benedict Co. in

collecting revenue from invoiced or sold stock has declined.

Payable days:

From 20x0 to 20x1, the organisation has raised its time for paying the creditors’ by 43.31

days and 65.31 days more than the industrial average. Despite the fact that Benedict Co. enjoys

trade credits, the rise in payable days is more than that of receivable days. This situation is

deemed to be critical, since the suppliers might not be willing to supply owing to the long credit

period. This denotes the complex financial condition of the organisation as well.

Cash conversion cycle:

According to the above table, an increase in this ratio could be observed from 12.91 days

in 20x0 to 53.56 days in 20x1. This implies that Benedict Co. has to wait for 40.66 days more in

20x1 for converting its stock into cash, which is again another issue for the organisation.

Liquidity ratios:

The reason behind the selection of liquidity ratios is to assure the investors that Benedict

Co. could honour its debts easily in a shorter timeframe. The reason that the financial managers

need to gain an understanding of the short-term ratios is linked with the creditors providing

short-term loans, as they are involved to be working with banks as well as other short-term

lenders.

This ratio generally denotes the number of days taken by the debtors to settle their

payments towards an organisation (Wahlen, Baginski and Bradshaw 2014). This number is seen

to rise from 55.70 days in 20x0 to 90.06 days in 20x1, which is 34.36 days more than the

previous year and 35 days more than the industrial average. Thus, the ability of Benedict Co. in

collecting revenue from invoiced or sold stock has declined.

Payable days:

From 20x0 to 20x1, the organisation has raised its time for paying the creditors’ by 43.31

days and 65.31 days more than the industrial average. Despite the fact that Benedict Co. enjoys

trade credits, the rise in payable days is more than that of receivable days. This situation is

deemed to be critical, since the suppliers might not be willing to supply owing to the long credit

period. This denotes the complex financial condition of the organisation as well.

Cash conversion cycle:

According to the above table, an increase in this ratio could be observed from 12.91 days

in 20x0 to 53.56 days in 20x1. This implies that Benedict Co. has to wait for 40.66 days more in

20x1 for converting its stock into cash, which is again another issue for the organisation.

Liquidity ratios:

The reason behind the selection of liquidity ratios is to assure the investors that Benedict

Co. could honour its debts easily in a shorter timeframe. The reason that the financial managers

need to gain an understanding of the short-term ratios is linked with the creditors providing

short-term loans, as they are involved to be working with banks as well as other short-term

lenders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.