Corporate Financial Management: Causes and Impacts of Global Financial Crisis

VerifiedAdded on 2023/04/23

|12

|2860

|191

AI Summary

The paper discusses the possible causes of financial crisis and impacts of crisis on different economies. The paper would also propose reformations to avoid future crisis as well.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE FINANCIAL MANAGEMENT

Corporate Financial Management

Name of the Student

Name of the University

Authors Note

Course ID

Corporate Financial Management

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE FINANCIAL MANAGEMENT

Table of Contents

Introduction:...............................................................................................................................2

Examples of Financial Crisis.....................................................................................................2

The new Triffin Dilemma:.....................................................................................................2

Lehman Brothers Failure and Balance of Payments:.............................................................3

Collapse of Financial Markets:..............................................................................................3

Possible Causes of Financial Crisis:..........................................................................................4

Would GFC happen again?........................................................................................................5

Impact of GFC in economies of different countries including the home country:....................6

Proposed Reformations:.............................................................................................................7

Conclusions:...............................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Introduction:...............................................................................................................................2

Examples of Financial Crisis.....................................................................................................2

The new Triffin Dilemma:.....................................................................................................2

Lehman Brothers Failure and Balance of Payments:.............................................................3

Collapse of Financial Markets:..............................................................................................3

Possible Causes of Financial Crisis:..........................................................................................4

Would GFC happen again?........................................................................................................5

Impact of GFC in economies of different countries including the home country:....................6

Proposed Reformations:.............................................................................................................7

Conclusions:...............................................................................................................................8

References:.................................................................................................................................9

2CORPORATE FINANCIAL MANAGEMENT

Introduction:

The international financial crisis and the economic crisis of 2008-09 is not well

unspoken among the government, media or in the theoretical discourse. The public hunt for

the guilty without understanding the difficult causes of the disaster (Lane and Milesi-Ferretti

2018). A large part of the people believe that the culprits are the bankers, bonuses, greed,

fraud, speculations and corruptions. While others have hinted that human failures in making

contingent decision such as the failure of Lehman Brothers. Majority of this is neither wrong

neither correct.

The credit crisis directly resulted in the decline of the mortgage market in US. When

the FED (Federal Reserve of America) undertook the decision of reducing the rate of interest

by 1 per cent to cover the negative impact of growth in the economy led to the

commencement of the problem (Balakrishnan, Watts and Zuo 2016). The financial crisis has

resulted in indebtedness and collapse of numerous banks and financial institutions not only in

US but also across the world. The paper would discuss the possible causes of financial crisis

and impacts of crisis on different economies. The paper would also propose reformations to

avoid future crisis as well.

Examples of Financial Crisis

The new Triffin Dilemma:

A system was proposed by Triffin governed by the IMF that would produce special

rights of drawings as the new artificial currency basket which would substitute more for the

dollars and hence transforming the IMF to central bank (Bénétrix, Lane and Shambaugh

2015). The assumption that dollar is not threatened by the hard inflation the federal reserve

can pursue the fully autonomous monetary policy for external valuation of dollar. This

system gave rise to number of adverse incentives. For US it flooded the economy with the

Introduction:

The international financial crisis and the economic crisis of 2008-09 is not well

unspoken among the government, media or in the theoretical discourse. The public hunt for

the guilty without understanding the difficult causes of the disaster (Lane and Milesi-Ferretti

2018). A large part of the people believe that the culprits are the bankers, bonuses, greed,

fraud, speculations and corruptions. While others have hinted that human failures in making

contingent decision such as the failure of Lehman Brothers. Majority of this is neither wrong

neither correct.

The credit crisis directly resulted in the decline of the mortgage market in US. When

the FED (Federal Reserve of America) undertook the decision of reducing the rate of interest

by 1 per cent to cover the negative impact of growth in the economy led to the

commencement of the problem (Balakrishnan, Watts and Zuo 2016). The financial crisis has

resulted in indebtedness and collapse of numerous banks and financial institutions not only in

US but also across the world. The paper would discuss the possible causes of financial crisis

and impacts of crisis on different economies. The paper would also propose reformations to

avoid future crisis as well.

Examples of Financial Crisis

The new Triffin Dilemma:

A system was proposed by Triffin governed by the IMF that would produce special

rights of drawings as the new artificial currency basket which would substitute more for the

dollars and hence transforming the IMF to central bank (Bénétrix, Lane and Shambaugh

2015). The assumption that dollar is not threatened by the hard inflation the federal reserve

can pursue the fully autonomous monetary policy for external valuation of dollar. This

system gave rise to number of adverse incentives. For US it flooded the economy with the

3CORPORATE FINANCIAL MANAGEMENT

inflow of capital and resulted in the overvaluation of the real exchange rate which was

relative to the current account deficit of US.

The Triffin Dilemma resulted in the flooding of the US financial sector where both

the risk seeking and the risk averse external capital flows led to high demand for the financial

products of different types and promoted unsustainable, dangerous macroeconomic regime

based on the asset bubbles (Sui and Sun 2016).

Lehman Brothers Failure and Balance of Payments:

There was not any direct effect of Lehman failure on the domestic and the financial

sector due to the limited exposure of the Indian Banks. The failure of Lehman Brothers

resulted in the sell-off of the domestic markets by the portfolio investors leading to

deleveraging. There was also the large amount of outflow of capital by the portfolio investors

and parallel pressure from the overseas exchange market (Carson, Fargher and Zhang 2017).

Whereas the overseas direct inflows reflected resilience and the access to the trade credits and

commercial borrowings became difficult. The net amount of capital inflow in 2008-09 was

reduced substantially with significant depletion of reserves. There was a reserve loss of US

$38 billion from the US $58 billion in 2008-09 reflecting a loss of valuation.

Collapse of Financial Markets:

The financial crisis led to direct failure in the mortgage market of US as FED’s

decision of reducing the interest rate to 1% led to negative effect on the economy. The excess

amount of lending resulted in the higher demand of new houses among the Americans. This

gave rise to boom in housing market and price of house tripled (Lane and Milesi-Ferretti

2017). The investment banks categorized the loans and selling it as financial derivatives.

However, the defaulters for Sub-prime loan increased and investment banks were unable to

find buyers. This led to higher supply over demand and price of house began falling. This led

inflow of capital and resulted in the overvaluation of the real exchange rate which was

relative to the current account deficit of US.

The Triffin Dilemma resulted in the flooding of the US financial sector where both

the risk seeking and the risk averse external capital flows led to high demand for the financial

products of different types and promoted unsustainable, dangerous macroeconomic regime

based on the asset bubbles (Sui and Sun 2016).

Lehman Brothers Failure and Balance of Payments:

There was not any direct effect of Lehman failure on the domestic and the financial

sector due to the limited exposure of the Indian Banks. The failure of Lehman Brothers

resulted in the sell-off of the domestic markets by the portfolio investors leading to

deleveraging. There was also the large amount of outflow of capital by the portfolio investors

and parallel pressure from the overseas exchange market (Carson, Fargher and Zhang 2017).

Whereas the overseas direct inflows reflected resilience and the access to the trade credits and

commercial borrowings became difficult. The net amount of capital inflow in 2008-09 was

reduced substantially with significant depletion of reserves. There was a reserve loss of US

$38 billion from the US $58 billion in 2008-09 reflecting a loss of valuation.

Collapse of Financial Markets:

The financial crisis led to direct failure in the mortgage market of US as FED’s

decision of reducing the interest rate to 1% led to negative effect on the economy. The excess

amount of lending resulted in the higher demand of new houses among the Americans. This

gave rise to boom in housing market and price of house tripled (Lane and Milesi-Ferretti

2017). The investment banks categorized the loans and selling it as financial derivatives.

However, the defaulters for Sub-prime loan increased and investment banks were unable to

find buyers. This led to higher supply over demand and price of house began falling. This led

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE FINANCIAL MANAGEMENT

the investment banks to huge loss and resulted in bankruptcies as well as closure of financial

firms in US and across the world.

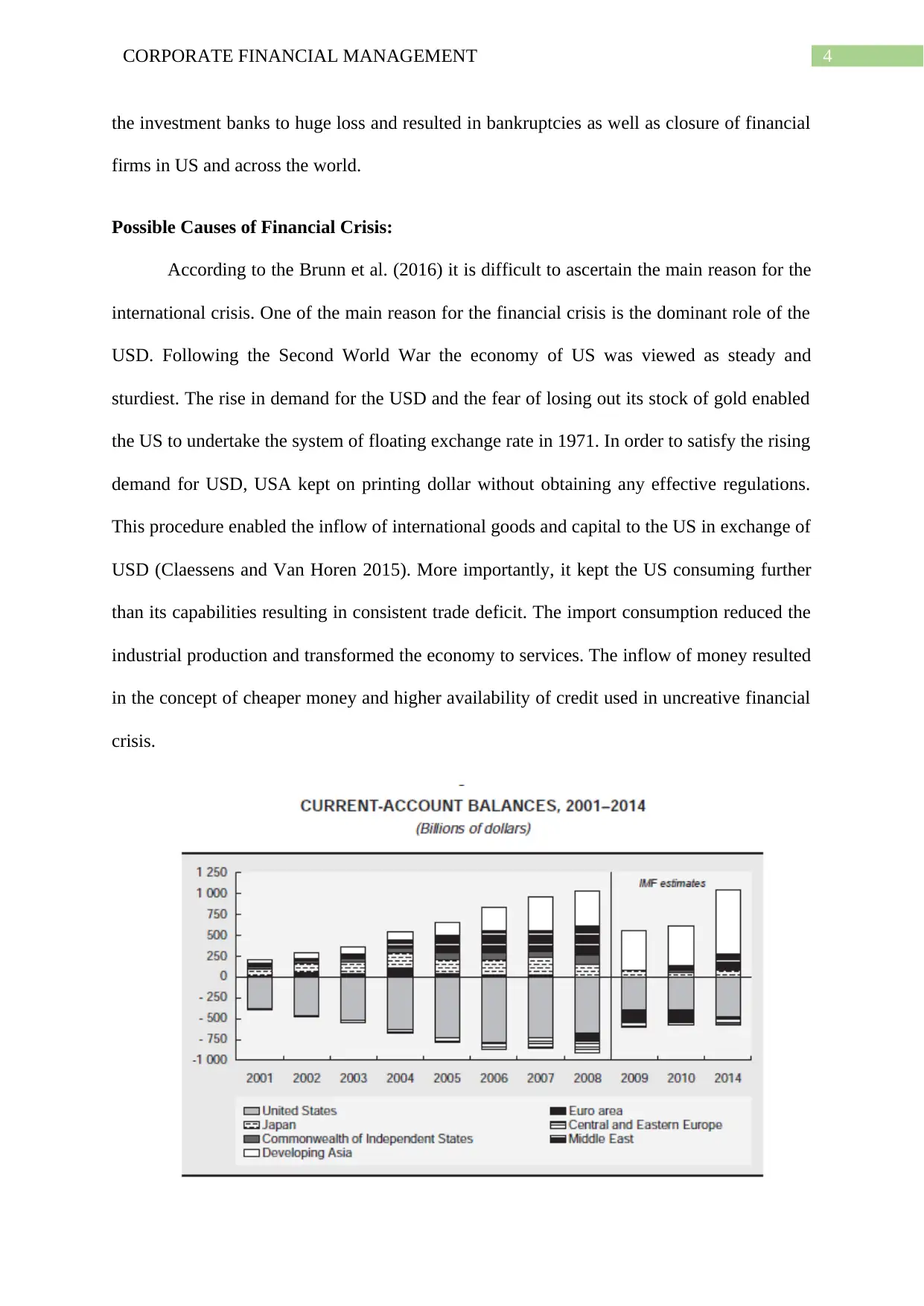

Possible Causes of Financial Crisis:

According to the Brunn et al. (2016) it is difficult to ascertain the main reason for the

international crisis. One of the main reason for the financial crisis is the dominant role of the

USD. Following the Second World War the economy of US was viewed as steady and

sturdiest. The rise in demand for the USD and the fear of losing out its stock of gold enabled

the US to undertake the system of floating exchange rate in 1971. In order to satisfy the rising

demand for USD, USA kept on printing dollar without obtaining any effective regulations.

This procedure enabled the inflow of international goods and capital to the US in exchange of

USD (Claessens and Van Horen 2015). More importantly, it kept the US consuming further

than its capabilities resulting in consistent trade deficit. The import consumption reduced the

industrial production and transformed the economy to services. The inflow of money resulted

in the concept of cheaper money and higher availability of credit used in uncreative financial

crisis.

the investment banks to huge loss and resulted in bankruptcies as well as closure of financial

firms in US and across the world.

Possible Causes of Financial Crisis:

According to the Brunn et al. (2016) it is difficult to ascertain the main reason for the

international crisis. One of the main reason for the financial crisis is the dominant role of the

USD. Following the Second World War the economy of US was viewed as steady and

sturdiest. The rise in demand for the USD and the fear of losing out its stock of gold enabled

the US to undertake the system of floating exchange rate in 1971. In order to satisfy the rising

demand for USD, USA kept on printing dollar without obtaining any effective regulations.

This procedure enabled the inflow of international goods and capital to the US in exchange of

USD (Claessens and Van Horen 2015). More importantly, it kept the US consuming further

than its capabilities resulting in consistent trade deficit. The import consumption reduced the

industrial production and transformed the economy to services. The inflow of money resulted

in the concept of cheaper money and higher availability of credit used in uncreative financial

crisis.

5CORPORATE FINANCIAL MANAGEMENT

Figure 1: Figure showing current account balance

(Source: Rey 2015)

Another possible factor that led to financial crisis is the unnecessary deregulation of

the financial markets. US was the leader in the world of financial market liberalization. To

attain this, the financial markets were excessively deregulated by the government and Federal

Reserve of America relaxed its observation and monitoring procedure (Vazquez and Federico

2015). The idea of market liberalization swept the world with the push from the GATS

contract. This permitted the US to expand its role as the leading player in offering financial

services. Numerous financial products and derivatives was bought leading to rise in

international trade and liberalization. The engagement of some financial and investment

banks in the mortgage market is regarded as the instance that impact the deregulations and

liberalization. This expansion gave rise to bubble which burst and frozen the entire securities

market.

There was also the imbalance in the market of world trade. As noticed China has

gained immensely from the joining with the WTO in 2001. China exploited the advantages of

the new international system of trade and across the world it flooded with the cheaper

products (Li et al. 2016). China kept its exchange rate of Yuan very low and the products of

China were very competitive in the international market. China gained huge amount of

surplus but US increased its trade deficit. Production of industrial and consumer goods fell

down in US and the economy transformed to service economy.

Would GFC happen again?

As stated by DesJardine, Bansal and Yang (2017) the central banks all through the

world have undertaken a quicker succession in reducing their cost of borrowing to a record of

greater than $10 trillion in the negative yielding sovereign debt. This stimulates the monetary

Figure 1: Figure showing current account balance

(Source: Rey 2015)

Another possible factor that led to financial crisis is the unnecessary deregulation of

the financial markets. US was the leader in the world of financial market liberalization. To

attain this, the financial markets were excessively deregulated by the government and Federal

Reserve of America relaxed its observation and monitoring procedure (Vazquez and Federico

2015). The idea of market liberalization swept the world with the push from the GATS

contract. This permitted the US to expand its role as the leading player in offering financial

services. Numerous financial products and derivatives was bought leading to rise in

international trade and liberalization. The engagement of some financial and investment

banks in the mortgage market is regarded as the instance that impact the deregulations and

liberalization. This expansion gave rise to bubble which burst and frozen the entire securities

market.

There was also the imbalance in the market of world trade. As noticed China has

gained immensely from the joining with the WTO in 2001. China exploited the advantages of

the new international system of trade and across the world it flooded with the cheaper

products (Li et al. 2016). China kept its exchange rate of Yuan very low and the products of

China were very competitive in the international market. China gained huge amount of

surplus but US increased its trade deficit. Production of industrial and consumer goods fell

down in US and the economy transformed to service economy.

Would GFC happen again?

As stated by DesJardine, Bansal and Yang (2017) the central banks all through the

world have undertaken a quicker succession in reducing their cost of borrowing to a record of

greater than $10 trillion in the negative yielding sovereign debt. This stimulates the monetary

6CORPORATE FINANCIAL MANAGEMENT

supply as the temporary measure of purchase of time and permitting the economies to recover

the form the shock of 2008. But the politicians do not has the appetite of implementing the

structural financial reformations for sustainable economic growth. They have only used

liquidity injections from the central banks to lend the added amount of cash to meet its deficit

instead of cutting the benefits or reforming it expressively.

The private sector companies have more regularly retreated from the capital

investment which would normally be conducive to the economic expansion (Kerlin et al.

2016). The pullback is largely attributable to the wide range of reasons from restructuring

their own balance sheets to the uncertain economic environment which has culminated in the

capital planning. The net impact of this there is a rise in the international debt to -240% of the

GDP. The corporate debt of US also climbed as earnings have deteriorated.

The corporate level borrowings growth is overtaking the GDP growth rate and has

introduced the debt to GDP ratios in every past three US recessions (Beuselinck et al. 2017).

Therefore, this makes it evident that another global financial crisis is imminent since the lead

time involved among the rising corporate debt which is relative to the GDP and earlier

collapses that has varied.

Impact of GFC in economies of different countries including the home country:

The international financial crisis was notable enough to create an impact on the

majority of the nations across the world. There were some of the developing nations that

escaped from indulging in the recession because of having a negative growth. But the GDP of

the developing nations weakened significantly from pre-crisis to post crisis level (Kenourgios

and Dimitriou 2015). Brazil and Republic of Korea suffered strong devaluations ever since

the outbreak of the crisis and its intensification. They were significantly affected by the crisis

despite its current account surplus in 2007 that turned to deficit in 2008.

supply as the temporary measure of purchase of time and permitting the economies to recover

the form the shock of 2008. But the politicians do not has the appetite of implementing the

structural financial reformations for sustainable economic growth. They have only used

liquidity injections from the central banks to lend the added amount of cash to meet its deficit

instead of cutting the benefits or reforming it expressively.

The private sector companies have more regularly retreated from the capital

investment which would normally be conducive to the economic expansion (Kerlin et al.

2016). The pullback is largely attributable to the wide range of reasons from restructuring

their own balance sheets to the uncertain economic environment which has culminated in the

capital planning. The net impact of this there is a rise in the international debt to -240% of the

GDP. The corporate debt of US also climbed as earnings have deteriorated.

The corporate level borrowings growth is overtaking the GDP growth rate and has

introduced the debt to GDP ratios in every past three US recessions (Beuselinck et al. 2017).

Therefore, this makes it evident that another global financial crisis is imminent since the lead

time involved among the rising corporate debt which is relative to the GDP and earlier

collapses that has varied.

Impact of GFC in economies of different countries including the home country:

The international financial crisis was notable enough to create an impact on the

majority of the nations across the world. There were some of the developing nations that

escaped from indulging in the recession because of having a negative growth. But the GDP of

the developing nations weakened significantly from pre-crisis to post crisis level (Kenourgios

and Dimitriou 2015). Brazil and Republic of Korea suffered strong devaluations ever since

the outbreak of the crisis and its intensification. They were significantly affected by the crisis

despite its current account surplus in 2007 that turned to deficit in 2008.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCIAL MANAGEMENT

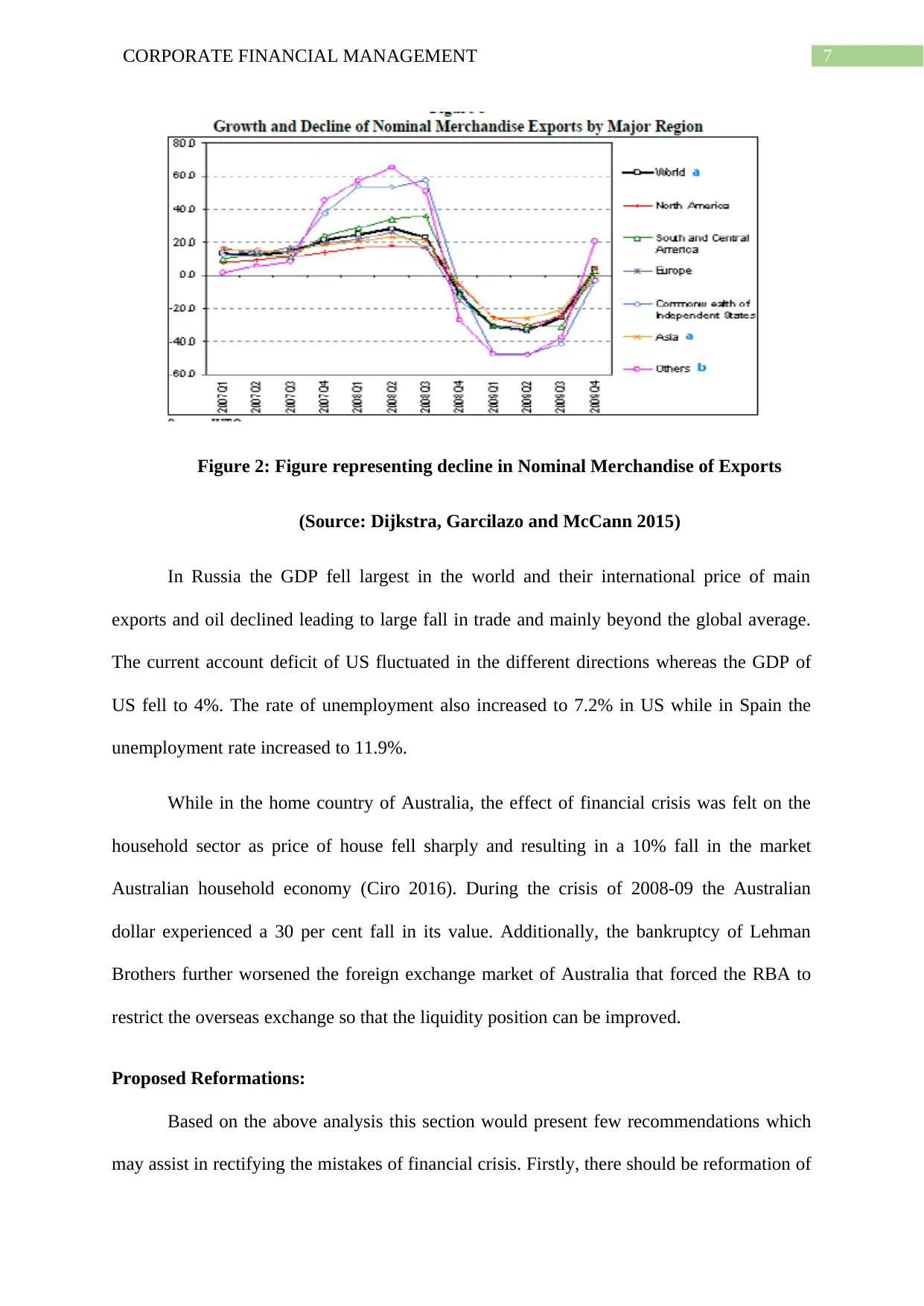

Figure 2: Figure representing decline in Nominal Merchandise of Exports

(Source: Dijkstra, Garcilazo and McCann 2015)

In Russia the GDP fell largest in the world and their international price of main

exports and oil declined leading to large fall in trade and mainly beyond the global average.

The current account deficit of US fluctuated in the different directions whereas the GDP of

US fell to 4%. The rate of unemployment also increased to 7.2% in US while in Spain the

unemployment rate increased to 11.9%.

While in the home country of Australia, the effect of financial crisis was felt on the

household sector as price of house fell sharply and resulting in a 10% fall in the market

Australian household economy (Ciro 2016). During the crisis of 2008-09 the Australian

dollar experienced a 30 per cent fall in its value. Additionally, the bankruptcy of Lehman

Brothers further worsened the foreign exchange market of Australia that forced the RBA to

restrict the overseas exchange so that the liquidity position can be improved.

Proposed Reformations:

Based on the above analysis this section would present few recommendations which

may assist in rectifying the mistakes of financial crisis. Firstly, there should be reformation of

Figure 2: Figure representing decline in Nominal Merchandise of Exports

(Source: Dijkstra, Garcilazo and McCann 2015)

In Russia the GDP fell largest in the world and their international price of main

exports and oil declined leading to large fall in trade and mainly beyond the global average.

The current account deficit of US fluctuated in the different directions whereas the GDP of

US fell to 4%. The rate of unemployment also increased to 7.2% in US while in Spain the

unemployment rate increased to 11.9%.

While in the home country of Australia, the effect of financial crisis was felt on the

household sector as price of house fell sharply and resulting in a 10% fall in the market

Australian household economy (Ciro 2016). During the crisis of 2008-09 the Australian

dollar experienced a 30 per cent fall in its value. Additionally, the bankruptcy of Lehman

Brothers further worsened the foreign exchange market of Australia that forced the RBA to

restrict the overseas exchange so that the liquidity position can be improved.

Proposed Reformations:

Based on the above analysis this section would present few recommendations which

may assist in rectifying the mistakes of financial crisis. Firstly, there should be reformation of

8CORPORATE FINANCIAL MANAGEMENT

the WTO and global trade. The WTO is required to be more active in creating a balance in

the global trade. Nations such as China must not be permitted to dominate the global trade by

using unfair trade activities as there are several countries that suffer from the declining

exports.

Secondly, the role of banks and rating agencies models for internal ratings suggest

that these institutions must be eliminated (Gruber and Kamin 2015). The current specialized

companies must reduce their entry barriers and should improve the competition. The

payments by the issuer must not be allowed and payment by the investors would create a

collective action problem.

Thirdly, it is proposed that the spending of government and incentive packages is

considered very vital in periods of recession. However, it is proposed that the public spending

must place emphasis on the construction and infrastructure activities which might result in

economic growth.

Conclusions:

Opinions regarding the factors that resulted in economic crisis differs widely. The

prime causes of crisis are the rising imbalance in the world trade and the parallel flow of

capital during the past decades distorted the structure of globalization. The new Triffin

dilemma led to flood in the financial sector with both the risk seeking and risk averse outside

capital flows by creating huge demand for the financial products that gave rise to risky

macroeconomic regimes. Conclusively, the international system of currency requires

fundamental reformations which would reduce the international imbalance and promote

orderly adjustment of exchange rate to improve the real economy.

the WTO and global trade. The WTO is required to be more active in creating a balance in

the global trade. Nations such as China must not be permitted to dominate the global trade by

using unfair trade activities as there are several countries that suffer from the declining

exports.

Secondly, the role of banks and rating agencies models for internal ratings suggest

that these institutions must be eliminated (Gruber and Kamin 2015). The current specialized

companies must reduce their entry barriers and should improve the competition. The

payments by the issuer must not be allowed and payment by the investors would create a

collective action problem.

Thirdly, it is proposed that the spending of government and incentive packages is

considered very vital in periods of recession. However, it is proposed that the public spending

must place emphasis on the construction and infrastructure activities which might result in

economic growth.

Conclusions:

Opinions regarding the factors that resulted in economic crisis differs widely. The

prime causes of crisis are the rising imbalance in the world trade and the parallel flow of

capital during the past decades distorted the structure of globalization. The new Triffin

dilemma led to flood in the financial sector with both the risk seeking and risk averse outside

capital flows by creating huge demand for the financial products that gave rise to risky

macroeconomic regimes. Conclusively, the international system of currency requires

fundamental reformations which would reduce the international imbalance and promote

orderly adjustment of exchange rate to improve the real economy.

9CORPORATE FINANCIAL MANAGEMENT

References:

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Bénétrix, A.S., Lane, P.R. and Shambaugh, J.C., 2015. International currency exposures,

valuation effects and the global financial crisis. Journal of International Economics, 96,

pp.S98-S109.

Beuselinck, C., Cao, L., Deloof, M. and Xia, X., 2017. The value of government ownership

during the global financial crisis. Journal of corporate Finance, 42, pp.481-493.

Brunn, S., Devriendt, L., Boulton, A., Derudder, B. and Witlox, F., 2016. Assessing the

impacts of the global financial crisis on major and minor cities in South and Southeast Asia: a

hyperlink analysis. In Spatial Diversity and Dynamics in Resources and Urban

Development (pp. 135-155). Springer, Dordrecht.

Carson, E., Fargher, N. and Zhang, Y., 2017. Explaining auditors’ propensity to issue going-

concern opinions in Australia after the global financial crisis. Accounting and Finance, pp.1-

39.

Ciro, T., 2016. The global financial crisis: Triggers, responses and aftermath. Routledge.

Claessens, S. and Van Horen, N., 2015. The impact of the global financial crisis on banking

globalization. IMF Economic Review, 63(4), pp.868-918.

DesJardine, M., Bansal, P. and Yang, Y., 2017. Bouncing back: Building resilience through

social and environmental practices in the context of the 2008 global financial crisis. Journal

of Management, p.0149206317708854.

References:

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Bénétrix, A.S., Lane, P.R. and Shambaugh, J.C., 2015. International currency exposures,

valuation effects and the global financial crisis. Journal of International Economics, 96,

pp.S98-S109.

Beuselinck, C., Cao, L., Deloof, M. and Xia, X., 2017. The value of government ownership

during the global financial crisis. Journal of corporate Finance, 42, pp.481-493.

Brunn, S., Devriendt, L., Boulton, A., Derudder, B. and Witlox, F., 2016. Assessing the

impacts of the global financial crisis on major and minor cities in South and Southeast Asia: a

hyperlink analysis. In Spatial Diversity and Dynamics in Resources and Urban

Development (pp. 135-155). Springer, Dordrecht.

Carson, E., Fargher, N. and Zhang, Y., 2017. Explaining auditors’ propensity to issue going-

concern opinions in Australia after the global financial crisis. Accounting and Finance, pp.1-

39.

Ciro, T., 2016. The global financial crisis: Triggers, responses and aftermath. Routledge.

Claessens, S. and Van Horen, N., 2015. The impact of the global financial crisis on banking

globalization. IMF Economic Review, 63(4), pp.868-918.

DesJardine, M., Bansal, P. and Yang, Y., 2017. Bouncing back: Building resilience through

social and environmental practices in the context of the 2008 global financial crisis. Journal

of Management, p.0149206317708854.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE FINANCIAL MANAGEMENT

Dijkstra, L., Garcilazo, E. and McCann, P., 2015. The effects of the global financial crisis on

European regions and cities. Journal of Economic Geography, 15(5), pp.935-949.

Gruber, J.W. and Kamin, S.B., 2015. The corporate saving glut in the aftermath of the global

financial crisis.

Kenourgios, D. and Dimitriou, D., 2015. Contagion of the Global Financial Crisis and the

real economy: A regional analysis. Economic Modelling, 44, pp.283-293.

Kerlin, J., Malinowska-Misiąg, E., Smaga, P., Witkowski, B., Nowak, A.K., Kozłowska, A.

and Wiśniewski, P., 2016. European Bank Restructuring During the Global Financial Crisis.

Springer.

Lane, M.P.R. and Milesi-Ferretti, M.G.M., 2017. International financial integration in the

aftermath of the global financial crisis. International Monetary Fund.

Lane, P.R. and Milesi-Ferretti, G.M., 2018. The external wealth of nations revisited:

international financial integration in the aftermath of the global financial crisis. IMF

Economic Review, 66(1), pp.189-222.

Li, W.Y., Chow, P.S., Choi, T.M. and Chan, H.L., 2016. Supplier integration, green

sustainability programs, and financial performance of fashion enterprises under global

financial crisis. Journal of cleaner production, 135, pp.57-70.

Rey, H., 2015. Dilemma not trilemma: the global financial cycle and monetary policy

independence (No. w21162). National Bureau of Economic Research.

Sui, L. and Sun, L., 2016. Spillover effects between exchange rates and stock prices:

Evidence from BRICS around the recent global financial crisis. Research in International

Business and Finance, 36, pp.459-471.

Dijkstra, L., Garcilazo, E. and McCann, P., 2015. The effects of the global financial crisis on

European regions and cities. Journal of Economic Geography, 15(5), pp.935-949.

Gruber, J.W. and Kamin, S.B., 2015. The corporate saving glut in the aftermath of the global

financial crisis.

Kenourgios, D. and Dimitriou, D., 2015. Contagion of the Global Financial Crisis and the

real economy: A regional analysis. Economic Modelling, 44, pp.283-293.

Kerlin, J., Malinowska-Misiąg, E., Smaga, P., Witkowski, B., Nowak, A.K., Kozłowska, A.

and Wiśniewski, P., 2016. European Bank Restructuring During the Global Financial Crisis.

Springer.

Lane, M.P.R. and Milesi-Ferretti, M.G.M., 2017. International financial integration in the

aftermath of the global financial crisis. International Monetary Fund.

Lane, P.R. and Milesi-Ferretti, G.M., 2018. The external wealth of nations revisited:

international financial integration in the aftermath of the global financial crisis. IMF

Economic Review, 66(1), pp.189-222.

Li, W.Y., Chow, P.S., Choi, T.M. and Chan, H.L., 2016. Supplier integration, green

sustainability programs, and financial performance of fashion enterprises under global

financial crisis. Journal of cleaner production, 135, pp.57-70.

Rey, H., 2015. Dilemma not trilemma: the global financial cycle and monetary policy

independence (No. w21162). National Bureau of Economic Research.

Sui, L. and Sun, L., 2016. Spillover effects between exchange rates and stock prices:

Evidence from BRICS around the recent global financial crisis. Research in International

Business and Finance, 36, pp.459-471.

11CORPORATE FINANCIAL MANAGEMENT

Vazquez, F. and Federico, P., 2015. Bank funding structures and risk: Evidence from the

global financial crisis. Journal of banking & finance, 61, pp.1-14.

Vazquez, F. and Federico, P., 2015. Bank funding structures and risk: Evidence from the

global financial crisis. Journal of banking & finance, 61, pp.1-14.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.