Analysis of Financial Statements and IFRS Adjustments for Rocha PLC

VerifiedAdded on 2020/07/22

|9

|1651

|107

Report

AI Summary

This report provides a detailed analysis of the financial statements of Rocha PLC, incorporating adjustments in line with International Financial Reporting Standards (IFRS). The analysis covers various items including investment property valuation, trade receivables, government grants, share capital...

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. ADJUSTMENTS IN LINE WITH THE IFRS AND ACCOUNTING CONCEPTS.................1

Item 1...........................................................................................................................................1

Item 5...........................................................................................................................................1

Item 7...........................................................................................................................................2

Item 8...........................................................................................................................................2

Item 9...........................................................................................................................................3

Item 11.........................................................................................................................................3

2. PREPARATION OF FINANCIAL STATEMENTS FOR THE ROCHA PLC.........................3

1. Statement of income statement................................................................................................3

2. Statement of changes in equity................................................................................................4

3. Statement of financial position................................................................................................5

REFERENCES................................................................................................................................7

1. ADJUSTMENTS IN LINE WITH THE IFRS AND ACCOUNTING CONCEPTS.................1

Item 1...........................................................................................................................................1

Item 5...........................................................................................................................................1

Item 7...........................................................................................................................................2

Item 8...........................................................................................................................................2

Item 9...........................................................................................................................................3

Item 11.........................................................................................................................................3

2. PREPARATION OF FINANCIAL STATEMENTS FOR THE ROCHA PLC.........................3

1. Statement of income statement................................................................................................3

2. Statement of changes in equity................................................................................................4

3. Statement of financial position................................................................................................5

REFERENCES................................................................................................................................7

1. ADJUSTMENTS IN LINE WITH THE IFRS AND ACCOUNTING

CONCEPTS

Item 1

According to the provisions of IAS 40, investment property is recognized at fair value at

the end of every accounting period. It means that every year, property is revaluated at its fair

value and any changes in the fair value are recognized as profit or loss in the statement of

comprehensive income (IAS 40 Investment Property, 2016). IFRS 13 indicates that fair value is

the price, at which, the assets can be exchanged between two knowledgeable and willing parties

in arm’s length transaction without deducting any transaction cost. Thus, applying the rule, on 1st

April, 2016, investment property is valued at £830,000 which at the end of financial year, 2017

valued at £850,000. Thus, increase in value of the investment property by (£850,000-£830,000),

£20,000 will be recognized as profit in P&L account.

Journal entry

Profit on revaluation of investment property A/c Dr. £20,000

To profit and loss a/c £20,000

Item 5

Trade receivables are recognized differently in line with the provisions of IAS 39 and

IFRS 9. It is because, IAS 39 only recognize bad debts as a credit loss if there is sufficient

evidences available to believe in impairment loss. However, in contrast, IFRS 9 allows entity to

recognize expected reasonable impairment loss according to the historical experiences even no

loss event happened yet (Silvia, 2015). Thus, applying the principle of IFRS 9, it becomes clear a

debtors owing £20,000 will be considered as fully credit loss in the financial statement.

However, for the remaining debtors, allowance will be created @ 5% of (£101,800- £4800 -

£20,000 = £77,000) worth £3,850 for the expected future credit loss due to bad & doubtful debts.

Journal entries:

Bad debts a/c Dr. £20,000

To Trade receivables a/c £20,000

Allowances for receivables a/c Dr. £3,850

GTo Trade receivables a/c £3,850

1

CONCEPTS

Item 1

According to the provisions of IAS 40, investment property is recognized at fair value at

the end of every accounting period. It means that every year, property is revaluated at its fair

value and any changes in the fair value are recognized as profit or loss in the statement of

comprehensive income (IAS 40 Investment Property, 2016). IFRS 13 indicates that fair value is

the price, at which, the assets can be exchanged between two knowledgeable and willing parties

in arm’s length transaction without deducting any transaction cost. Thus, applying the rule, on 1st

April, 2016, investment property is valued at £830,000 which at the end of financial year, 2017

valued at £850,000. Thus, increase in value of the investment property by (£850,000-£830,000),

£20,000 will be recognized as profit in P&L account.

Journal entry

Profit on revaluation of investment property A/c Dr. £20,000

To profit and loss a/c £20,000

Item 5

Trade receivables are recognized differently in line with the provisions of IAS 39 and

IFRS 9. It is because, IAS 39 only recognize bad debts as a credit loss if there is sufficient

evidences available to believe in impairment loss. However, in contrast, IFRS 9 allows entity to

recognize expected reasonable impairment loss according to the historical experiences even no

loss event happened yet (Silvia, 2015). Thus, applying the principle of IFRS 9, it becomes clear a

debtors owing £20,000 will be considered as fully credit loss in the financial statement.

However, for the remaining debtors, allowance will be created @ 5% of (£101,800- £4800 -

£20,000 = £77,000) worth £3,850 for the expected future credit loss due to bad & doubtful debts.

Journal entries:

Bad debts a/c Dr. £20,000

To Trade receivables a/c £20,000

Allowances for receivables a/c Dr. £3,850

GTo Trade receivables a/c £3,850

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit & loss a/c Dr. £3,850

To Allowances for receivables a/c £3,850

Item 7

As per the provision of IAS 20, government grant must be recognised either as deferred

income or at the amount less assets’s carrying value in the financial statements. As per the

scenario, Rocha Plc uses deferred income method to record governmental grants in their

financial statements. Thus, following journal entries must be made in such respect, stated here as

under:

Correct entry for the receipts of the grants:

Bank a/c Dr. £40,000

To office equipments a/c £40,000

Wrong entry made for the receipts of the grants

Bank a/c Dr. £40,000

To Suspense a/c £40,000

Rectifying entry

Suspense a/c Dr. £40,000

To Office equipments a/c £40,000

Item 8

According to IFRS provisions, if an entity issue shares above par or nominal value than

amount exceeded over par value will be recognised in an additional contributed capital account,

called share premium account. However, sale proceed at aggregate par needs to be credited in

ordinary share capital account (Stent, Bradbury and Hooks, 2017). In the given case study,

accountant of the company has wrongly entered all the sale proceed in the ordinary share capital

account, thus, following entry must be passed to rectify the errors made, as follows:

Correct entry

Bank a/c Dr. £900,000

To ordinary share capital a/c £500,000

To share premium a/c £400,000

Wrong entry

Bank a/c Dr. £900,000

To ordinary share capital a/c £900,000

2

To Allowances for receivables a/c £3,850

Item 7

As per the provision of IAS 20, government grant must be recognised either as deferred

income or at the amount less assets’s carrying value in the financial statements. As per the

scenario, Rocha Plc uses deferred income method to record governmental grants in their

financial statements. Thus, following journal entries must be made in such respect, stated here as

under:

Correct entry for the receipts of the grants:

Bank a/c Dr. £40,000

To office equipments a/c £40,000

Wrong entry made for the receipts of the grants

Bank a/c Dr. £40,000

To Suspense a/c £40,000

Rectifying entry

Suspense a/c Dr. £40,000

To Office equipments a/c £40,000

Item 8

According to IFRS provisions, if an entity issue shares above par or nominal value than

amount exceeded over par value will be recognised in an additional contributed capital account,

called share premium account. However, sale proceed at aggregate par needs to be credited in

ordinary share capital account (Stent, Bradbury and Hooks, 2017). In the given case study,

accountant of the company has wrongly entered all the sale proceed in the ordinary share capital

account, thus, following entry must be passed to rectify the errors made, as follows:

Correct entry

Bank a/c Dr. £900,000

To ordinary share capital a/c £500,000

To share premium a/c £400,000

Wrong entry

Bank a/c Dr. £900,000

To ordinary share capital a/c £900,000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

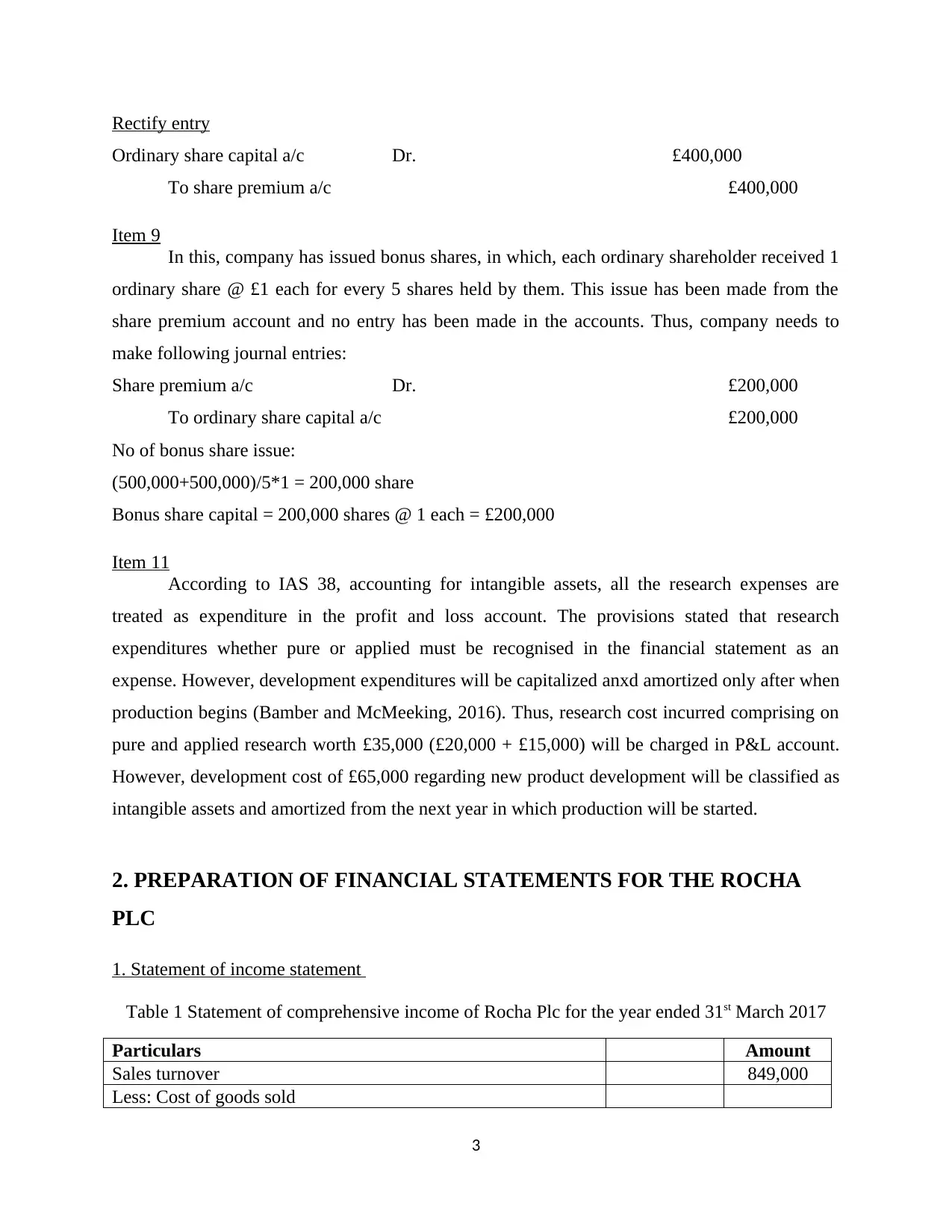

Rectify entry

Ordinary share capital a/c Dr. £400,000

To share premium a/c £400,000

Item 9

In this, company has issued bonus shares, in which, each ordinary shareholder received 1

ordinary share @ £1 each for every 5 shares held by them. This issue has been made from the

share premium account and no entry has been made in the accounts. Thus, company needs to

make following journal entries:

Share premium a/c Dr. £200,000

To ordinary share capital a/c £200,000

No of bonus share issue:

(500,000+500,000)/5*1 = 200,000 share

Bonus share capital = 200,000 shares @ 1 each = £200,000

Item 11

According to IAS 38, accounting for intangible assets, all the research expenses are

treated as expenditure in the profit and loss account. The provisions stated that research

expenditures whether pure or applied must be recognised in the financial statement as an

expense. However, development expenditures will be capitalized anxd amortized only after when

production begins (Bamber and McMeeking, 2016). Thus, research cost incurred comprising on

pure and applied research worth £35,000 (£20,000 + £15,000) will be charged in P&L account.

However, development cost of £65,000 regarding new product development will be classified as

intangible assets and amortized from the next year in which production will be started.

2. PREPARATION OF FINANCIAL STATEMENTS FOR THE ROCHA

PLC

1. Statement of income statement

Table 1 Statement of comprehensive income of Rocha Plc for the year ended 31st March 2017

Particulars Amount

Sales turnover 849,000

Less: Cost of goods sold

3

Ordinary share capital a/c Dr. £400,000

To share premium a/c £400,000

Item 9

In this, company has issued bonus shares, in which, each ordinary shareholder received 1

ordinary share @ £1 each for every 5 shares held by them. This issue has been made from the

share premium account and no entry has been made in the accounts. Thus, company needs to

make following journal entries:

Share premium a/c Dr. £200,000

To ordinary share capital a/c £200,000

No of bonus share issue:

(500,000+500,000)/5*1 = 200,000 share

Bonus share capital = 200,000 shares @ 1 each = £200,000

Item 11

According to IAS 38, accounting for intangible assets, all the research expenses are

treated as expenditure in the profit and loss account. The provisions stated that research

expenditures whether pure or applied must be recognised in the financial statement as an

expense. However, development expenditures will be capitalized anxd amortized only after when

production begins (Bamber and McMeeking, 2016). Thus, research cost incurred comprising on

pure and applied research worth £35,000 (£20,000 + £15,000) will be charged in P&L account.

However, development cost of £65,000 regarding new product development will be classified as

intangible assets and amortized from the next year in which production will be started.

2. PREPARATION OF FINANCIAL STATEMENTS FOR THE ROCHA

PLC

1. Statement of income statement

Table 1 Statement of comprehensive income of Rocha Plc for the year ended 31st March 2017

Particulars Amount

Sales turnover 849,000

Less: Cost of goods sold

3

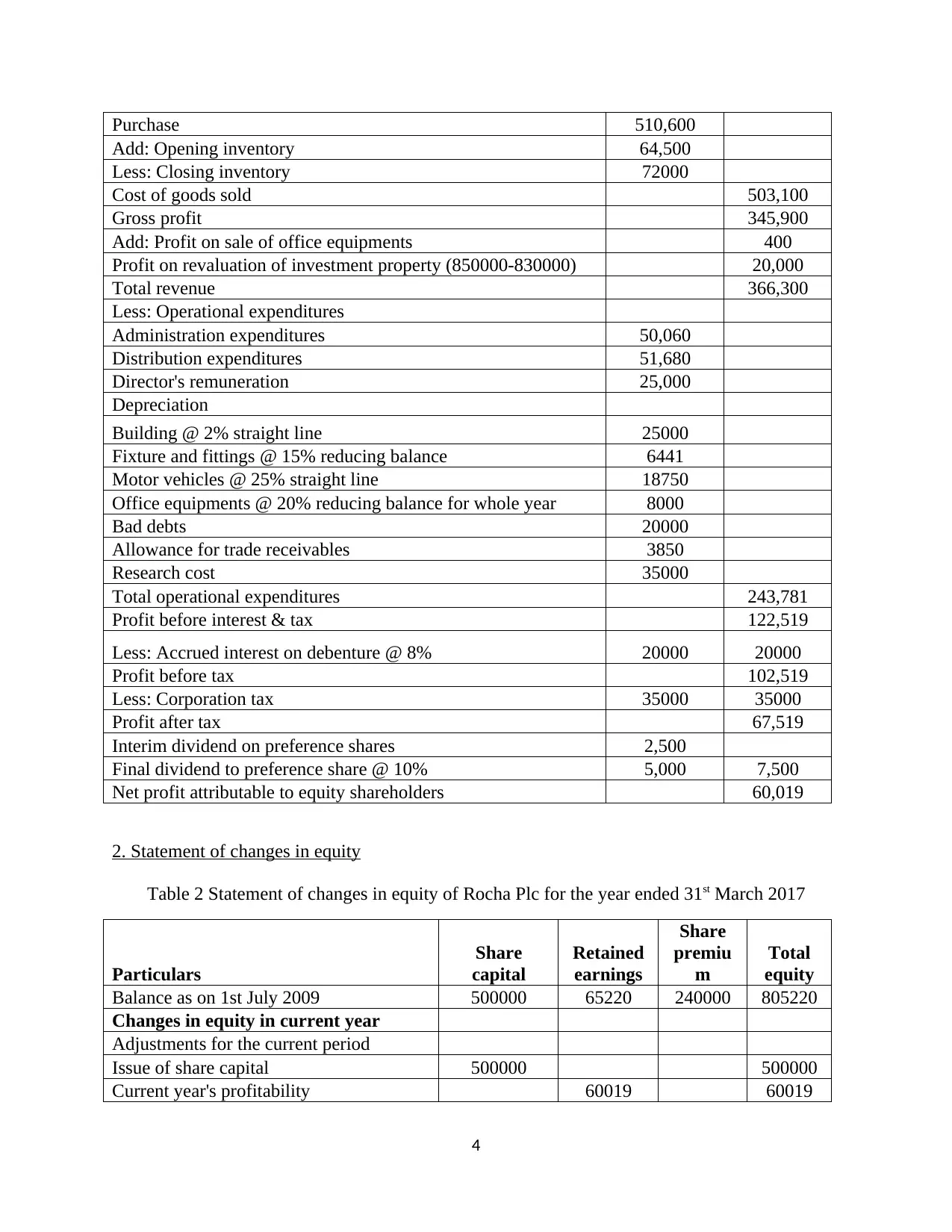

Purchase 510,600

Add: Opening inventory 64,500

Less: Closing inventory 72000

Cost of goods sold 503,100

Gross profit 345,900

Add: Profit on sale of office equipments 400

Profit on revaluation of investment property (850000-830000) 20,000

Total revenue 366,300

Less: Operational expenditures

Administration expenditures 50,060

Distribution expenditures 51,680

Director's remuneration 25,000

Depreciation

Building @ 2% straight line 25000

Fixture and fittings @ 15% reducing balance 6441

Motor vehicles @ 25% straight line 18750

Office equipments @ 20% reducing balance for whole year 8000

Bad debts 20000

Allowance for trade receivables 3850

Research cost 35000

Total operational expenditures 243,781

Profit before interest & tax 122,519

Less: Accrued interest on debenture @ 8% 20000 20000

Profit before tax 102,519

Less: Corporation tax 35000 35000

Profit after tax 67,519

Interim dividend on preference shares 2,500

Final dividend to preference share @ 10% 5,000 7,500

Net profit attributable to equity shareholders 60,019

2. Statement of changes in equity

Table 2 Statement of changes in equity of Rocha Plc for the year ended 31st March 2017

Particulars

Share

capital

Retained

earnings

Share

premiu

m

Total

equity

Balance as on 1st July 2009 500000 65220 240000 805220

Changes in equity in current year

Adjustments for the current period

Issue of share capital 500000 500000

Current year's profitability 60019 60019

4

Add: Opening inventory 64,500

Less: Closing inventory 72000

Cost of goods sold 503,100

Gross profit 345,900

Add: Profit on sale of office equipments 400

Profit on revaluation of investment property (850000-830000) 20,000

Total revenue 366,300

Less: Operational expenditures

Administration expenditures 50,060

Distribution expenditures 51,680

Director's remuneration 25,000

Depreciation

Building @ 2% straight line 25000

Fixture and fittings @ 15% reducing balance 6441

Motor vehicles @ 25% straight line 18750

Office equipments @ 20% reducing balance for whole year 8000

Bad debts 20000

Allowance for trade receivables 3850

Research cost 35000

Total operational expenditures 243,781

Profit before interest & tax 122,519

Less: Accrued interest on debenture @ 8% 20000 20000

Profit before tax 102,519

Less: Corporation tax 35000 35000

Profit after tax 67,519

Interim dividend on preference shares 2,500

Final dividend to preference share @ 10% 5,000 7,500

Net profit attributable to equity shareholders 60,019

2. Statement of changes in equity

Table 2 Statement of changes in equity of Rocha Plc for the year ended 31st March 2017

Particulars

Share

capital

Retained

earnings

Share

premiu

m

Total

equity

Balance as on 1st July 2009 500000 65220 240000 805220

Changes in equity in current year

Adjustments for the current period

Issue of share capital 500000 500000

Current year's profitability 60019 60019

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revaluation gain on investment property 0

Share premium on additional share issue 400000 400000

Bonus share issued 200000 -200000 0

Balance as on 1st July 2010 1200000 125239 440000 1765239

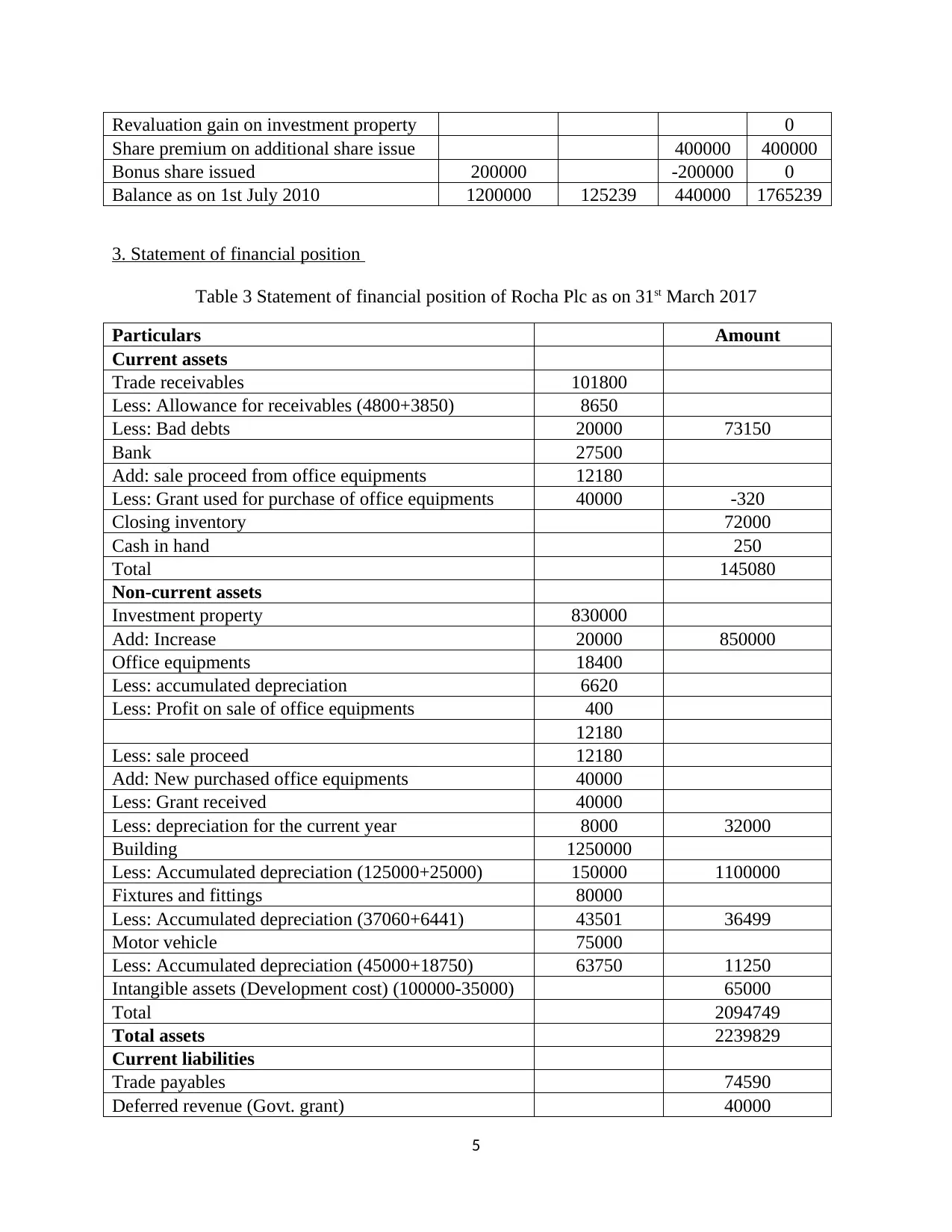

3. Statement of financial position

Table 3 Statement of financial position of Rocha Plc as on 31st March 2017

Particulars Amount

Current assets

Trade receivables 101800

Less: Allowance for receivables (4800+3850) 8650

Less: Bad debts 20000 73150

Bank 27500

Add: sale proceed from office equipments 12180

Less: Grant used for purchase of office equipments 40000 -320

Closing inventory 72000

Cash in hand 250

Total 145080

Non-current assets

Investment property 830000

Add: Increase 20000 850000

Office equipments 18400

Less: accumulated depreciation 6620

Less: Profit on sale of office equipments 400

12180

Less: sale proceed 12180

Add: New purchased office equipments 40000

Less: Grant received 40000

Less: depreciation for the current year 8000 32000

Building 1250000

Less: Accumulated depreciation (125000+25000) 150000 1100000

Fixtures and fittings 80000

Less: Accumulated depreciation (37060+6441) 43501 36499

Motor vehicle 75000

Less: Accumulated depreciation (45000+18750) 63750 11250

Intangible assets (Development cost) (100000-35000) 65000

Total 2094749

Total assets 2239829

Current liabilities

Trade payables 74590

Deferred revenue (Govt. grant) 40000

5

Share premium on additional share issue 400000 400000

Bonus share issued 200000 -200000 0

Balance as on 1st July 2010 1200000 125239 440000 1765239

3. Statement of financial position

Table 3 Statement of financial position of Rocha Plc as on 31st March 2017

Particulars Amount

Current assets

Trade receivables 101800

Less: Allowance for receivables (4800+3850) 8650

Less: Bad debts 20000 73150

Bank 27500

Add: sale proceed from office equipments 12180

Less: Grant used for purchase of office equipments 40000 -320

Closing inventory 72000

Cash in hand 250

Total 145080

Non-current assets

Investment property 830000

Add: Increase 20000 850000

Office equipments 18400

Less: accumulated depreciation 6620

Less: Profit on sale of office equipments 400

12180

Less: sale proceed 12180

Add: New purchased office equipments 40000

Less: Grant received 40000

Less: depreciation for the current year 8000 32000

Building 1250000

Less: Accumulated depreciation (125000+25000) 150000 1100000

Fixtures and fittings 80000

Less: Accumulated depreciation (37060+6441) 43501 36499

Motor vehicle 75000

Less: Accumulated depreciation (45000+18750) 63750 11250

Intangible assets (Development cost) (100000-35000) 65000

Total 2094749

Total assets 2239829

Current liabilities

Trade payables 74590

Deferred revenue (Govt. grant) 40000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

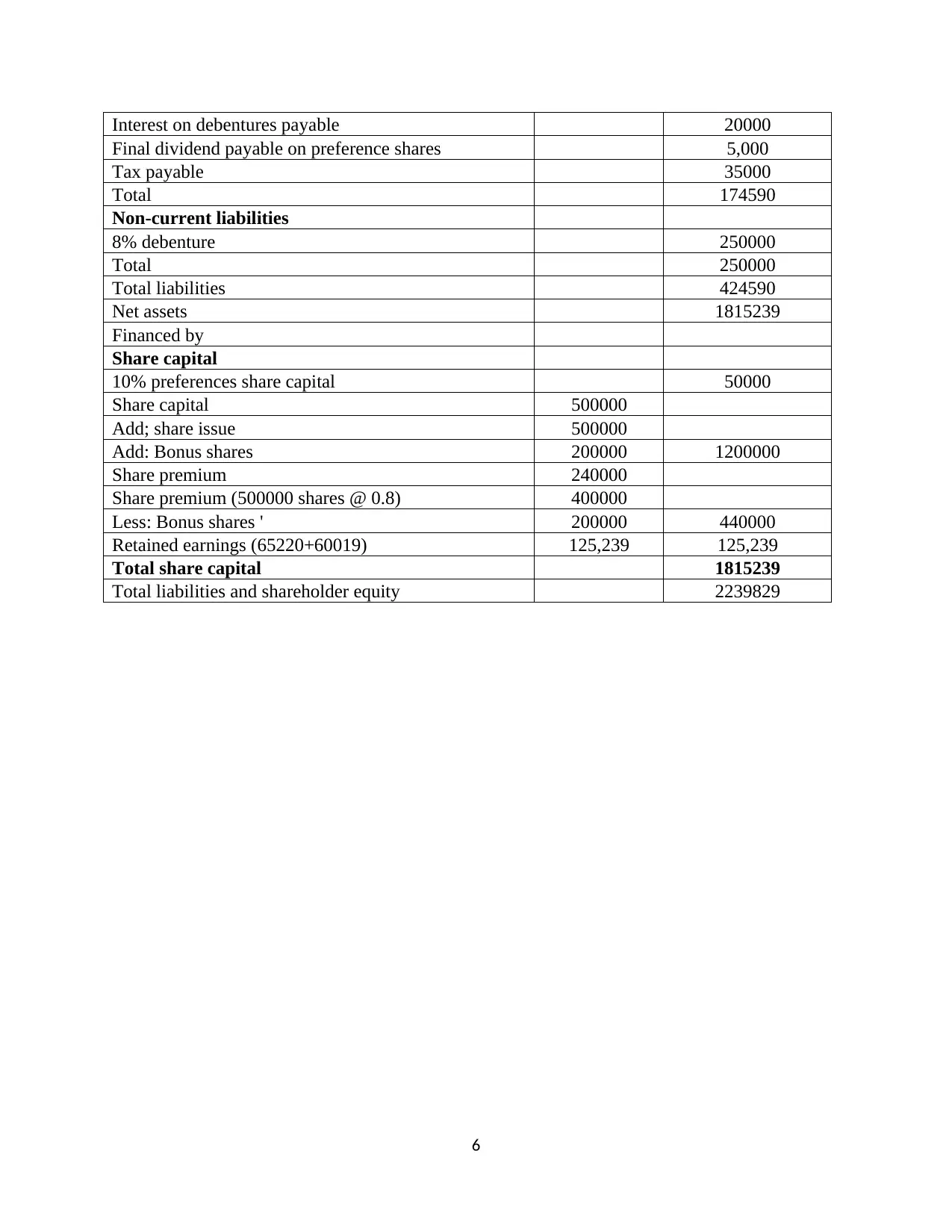

Interest on debentures payable 20000

Final dividend payable on preference shares 5,000

Tax payable 35000

Total 174590

Non-current liabilities

8% debenture 250000

Total 250000

Total liabilities 424590

Net assets 1815239

Financed by

Share capital

10% preferences share capital 50000

Share capital 500000

Add; share issue 500000

Add: Bonus shares 200000 1200000

Share premium 240000

Share premium (500000 shares @ 0.8) 400000

Less: Bonus shares ' 200000 440000

Retained earnings (65220+60019) 125,239 125,239

Total share capital 1815239

Total liabilities and shareholder equity 2239829

6

Final dividend payable on preference shares 5,000

Tax payable 35000

Total 174590

Non-current liabilities

8% debenture 250000

Total 250000

Total liabilities 424590

Net assets 1815239

Financed by

Share capital

10% preferences share capital 50000

Share capital 500000

Add; share issue 500000

Add: Bonus shares 200000 1200000

Share premium 240000

Share premium (500000 shares @ 0.8) 400000

Less: Bonus shares ' 200000 440000

Retained earnings (65220+60019) 125,239 125,239

Total share capital 1815239

Total liabilities and shareholder equity 2239829

6

REFERENCES

Bamber, M. and McMeeking, K., 2016. An examination of international accounting standard-

setting due process and the implications for legitimacy. The British Accounting Review.

48(1). pp.59-73.

Stent, W., Bradbury, M. E. and Hooks, J., 2017. Insights into accounting choice from the

adoption timing of International Financial Reporting Standards. Accounting & Finance.

57(S1). pp.255-276.

Online

IAS 40 Investment Property. 2016. [Online]. Available through:

https://www.google.co.in/search?

q=IFRS+13&oq=IFRS+13+&aqs=chrome..69i57j0l5.2888j0j9&sourceid=chrome&ie=U

TF-8. [Accessed on 3rd July 2017].

Silvia, M., 2015. How New Impairment Rules in IFRS 9 Affects. [Online]. Available through:

http://www.ifrsbox.com/ifrs-9-expected-credit-loss/. [Accessed on 3rd July 2017].

7

Bamber, M. and McMeeking, K., 2016. An examination of international accounting standard-

setting due process and the implications for legitimacy. The British Accounting Review.

48(1). pp.59-73.

Stent, W., Bradbury, M. E. and Hooks, J., 2017. Insights into accounting choice from the

adoption timing of International Financial Reporting Standards. Accounting & Finance.

57(S1). pp.255-276.

Online

IAS 40 Investment Property. 2016. [Online]. Available through:

https://www.google.co.in/search?

q=IFRS+13&oq=IFRS+13+&aqs=chrome..69i57j0l5.2888j0j9&sourceid=chrome&ie=U

TF-8. [Accessed on 3rd July 2017].

Silvia, M., 2015. How New Impairment Rules in IFRS 9 Affects. [Online]. Available through:

http://www.ifrsbox.com/ifrs-9-expected-credit-loss/. [Accessed on 3rd July 2017].

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.