Bankruptcy Prediction Models: Altman Z-Score and Ohlson O-Score

VerifiedAdded on 2023/04/21

|10

|7538

|132

Report

AI Summary

This report presents a research proposal comparing the accuracy of two bankruptcy prediction models: Altman Z-Score and Ohlson O-Score. The study aims to determine which model provides more accurate predictions of company bankruptcy. The research will involve a review of existing literature, including key articles such as Altman (1968) and Ohlson (1980), along with other relevant journals to examine the methodologies and findings of each model. The proposal outlines the research question, hypotheses, and the significance of the study, focusing on the application of financial ratios and statistical techniques like logit analysis. The goal is to contribute to a better understanding of financial distress prediction and provide insights into the comparative strengths and weaknesses of the Altman and Ohlson models.

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2069 The Clute Institute

The Use Of Ohlson's O-Score

For Bankruptcy Prediction In Thailand

Judy Ramage Lawrence, Christian Brothers University, USA

Surapol Pongsatat, Ramkhamhaeng University, Thailand

Howard Lawrence, University of Mississippi, USA

ABSTRACT

Business failure is a major concern to all parties involved and can create high costs and heavy

losses. If bankruptcy can be predicted with reasonable accuracy ahead of time, firms can better

protect their businesses and can take action to minimize risk and loss of business, and perhaps

even prevent the bankruptcy itself. Bankruptcy prediction in thailand is important because

business in thailand has historically operated on a system of trust where one person doing

business trusts the other to perform as agreed upon in written and oral contracts. The threat of

bankruptcy tends to diminish that trust and weakens the country's ability to prosper. While

research in bankruptcy has been extensive, there has been only limited research on bankruptcy

prediction in thailand. This study expands on an earlier study by pongsatat, et al (1994) using

ohlson's o-score to determine if there a significant difference in ohlson’s o-score as measured by

ohlson’s logit analysis model between bankrupt and non-bankrupt firms in thailand. The results

of the independent samples t-test demonstrates that there are significant differences in the

population means for one year, two years and three years prior to bankruptcy at the 0.05 level.

Therefore the null hypothesis that there is no difference in the mean of ohlson’s o-score as

measured by logit analysis between bankrupt and non-bankrupt firms in thailand is rejected.

Keywords: Bankruptcy; Prediction; Ohlson O-Score; Thailand

INTRODUCTION

he failure of a business organization has significant economic effects for its owners, creditors, and to

society overall. Almost every firm has debt and in the majority of cases that debt is the result of good

financial planning, because debt financing is often a lower cost alternative to equity financing.

Unfortunately, with debt there comes risk, and the ultimate risk is that of bankruptcy. To avoid this problem firms

need reliable ways to predict bankruptcy. This is so because with proper warning, businesses can often take the

necessary measures to minimize this risk and possibly prevent the bankruptcy itself.

Thailand is a country that has historically operated on a system of personal trust between parties. Oral

contracts are more common in Thailand than in countries such as the United States. Bankruptcy causes that trust to

be diminished and ultimately hurts the country’s ability to prosper. There have been many studies of bankruptcy in

Asia with the majority finding that the causes of bankruptcy in Asian countries can be quite different from studies in

western countries (Pongsatat, et al, 2004: Evans, et al, 2013; Sirirattanaphonkun & Pattarathammas, 2012;

Treewichayapong, et al 2011; Reynolds, et al, 2002; Urapeepatanapong, et al, 1998). The analysis of financial ratios

has been the primary method used for analysis. (See: Pongsatat, et al, 2004; Clark & Jung, 2002; Brietzke, 2001;

Pugh & Dehesh, 2001; Haley, 2000; & Tirapat & Nittayagasetwat, 1999). Four of these studies addressed

bankruptcy in Thailand (Pongsatat, et al, 2004; Evans, et al, 2013; Reynolds, et al, 2002 & Tirapat &

Nittayagasetwat, 1999). The remaining studies addressed bankruptcy in South Korea (Clark & Jung, 2002; Haley,

2000) Indonesia (Brietzke, 2001), and Taiwan (Clark & Jung, 2002). As in the west, financial strength has been the

primary indicator of the ability to avoid bankruptcy. Other factors have also come into play, with the inability to

adjust to changing environmental factors being the major cause. Such factors as customer preferences, social norms,

new legal requirements and rapidly changing global competitive forces have meant that companies must adjust or

T

Copyright by author(s); CC-BY 2069 The Clute Institute

The Use Of Ohlson's O-Score

For Bankruptcy Prediction In Thailand

Judy Ramage Lawrence, Christian Brothers University, USA

Surapol Pongsatat, Ramkhamhaeng University, Thailand

Howard Lawrence, University of Mississippi, USA

ABSTRACT

Business failure is a major concern to all parties involved and can create high costs and heavy

losses. If bankruptcy can be predicted with reasonable accuracy ahead of time, firms can better

protect their businesses and can take action to minimize risk and loss of business, and perhaps

even prevent the bankruptcy itself. Bankruptcy prediction in thailand is important because

business in thailand has historically operated on a system of trust where one person doing

business trusts the other to perform as agreed upon in written and oral contracts. The threat of

bankruptcy tends to diminish that trust and weakens the country's ability to prosper. While

research in bankruptcy has been extensive, there has been only limited research on bankruptcy

prediction in thailand. This study expands on an earlier study by pongsatat, et al (1994) using

ohlson's o-score to determine if there a significant difference in ohlson’s o-score as measured by

ohlson’s logit analysis model between bankrupt and non-bankrupt firms in thailand. The results

of the independent samples t-test demonstrates that there are significant differences in the

population means for one year, two years and three years prior to bankruptcy at the 0.05 level.

Therefore the null hypothesis that there is no difference in the mean of ohlson’s o-score as

measured by logit analysis between bankrupt and non-bankrupt firms in thailand is rejected.

Keywords: Bankruptcy; Prediction; Ohlson O-Score; Thailand

INTRODUCTION

he failure of a business organization has significant economic effects for its owners, creditors, and to

society overall. Almost every firm has debt and in the majority of cases that debt is the result of good

financial planning, because debt financing is often a lower cost alternative to equity financing.

Unfortunately, with debt there comes risk, and the ultimate risk is that of bankruptcy. To avoid this problem firms

need reliable ways to predict bankruptcy. This is so because with proper warning, businesses can often take the

necessary measures to minimize this risk and possibly prevent the bankruptcy itself.

Thailand is a country that has historically operated on a system of personal trust between parties. Oral

contracts are more common in Thailand than in countries such as the United States. Bankruptcy causes that trust to

be diminished and ultimately hurts the country’s ability to prosper. There have been many studies of bankruptcy in

Asia with the majority finding that the causes of bankruptcy in Asian countries can be quite different from studies in

western countries (Pongsatat, et al, 2004: Evans, et al, 2013; Sirirattanaphonkun & Pattarathammas, 2012;

Treewichayapong, et al 2011; Reynolds, et al, 2002; Urapeepatanapong, et al, 1998). The analysis of financial ratios

has been the primary method used for analysis. (See: Pongsatat, et al, 2004; Clark & Jung, 2002; Brietzke, 2001;

Pugh & Dehesh, 2001; Haley, 2000; & Tirapat & Nittayagasetwat, 1999). Four of these studies addressed

bankruptcy in Thailand (Pongsatat, et al, 2004; Evans, et al, 2013; Reynolds, et al, 2002 & Tirapat &

Nittayagasetwat, 1999). The remaining studies addressed bankruptcy in South Korea (Clark & Jung, 2002; Haley,

2000) Indonesia (Brietzke, 2001), and Taiwan (Clark & Jung, 2002). As in the west, financial strength has been the

primary indicator of the ability to avoid bankruptcy. Other factors have also come into play, with the inability to

adjust to changing environmental factors being the major cause. Such factors as customer preferences, social norms,

new legal requirements and rapidly changing global competitive forces have meant that companies must adjust or

T

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2070 The Clute Institute

die. As these forces continue, companies must find better ways to predict bankruptcy. This is all the more

important in Thailand today given that much of the investment that previously came to Thailand now goes to

countries such as China and Vietnam.

Two of the primary methods used in the west to predict bankruptcy are Altman's Z-score and Ohlson's O-

score. Pongsatat, et al, (2004) examined the comparative ability of Ohlson’s Logit model and Altman’s four-

variance model for predicting bankruptcy in Thailand to determine if there was a difference in their ability to predict

bankruptcy in Thailand. This study expands on Pongsatat’s 2004 study to specifically examine Ohlson’s logit

model’s ability to predict bankruptcy for both financial and non-financial firms.

Pongsatat’s 2004 study found that this analysis is important because evidence suggests that studies

conducted in countries such as the united states and the european union may not have relevance to a country such as

thailand. Pongsatat cited tirapat and nittayagasetwat (1999) who found that the institutional structure of the financial

sector in thailand is characterized as a bank centered financial system, while that of the u.s. is a market based

system. For example, tirapat and nittayagasetwat (1999) point out that in thailand, the credits from financial

institutions such as commercial banks and finance companies can be five or more times larger than the funds raised

from the stock and bond markets. In 1997, at the height of the asian crisis, the amount was 16.7 times higher. These

are significantly larger numbers than what could be found in most western economies. Other differences in thailand

cited by tirapat and nittayagasetwat (1999) included a higher concentration of shares being held by a few individuals

and more shares with large family ownership.

DISCUSSION

The cause of business failures is a matter that has been discussed and researched at length and it has been a

topic of interest for hundreds of years. Throughout these years, ratio analysis has been at the heart of the matter.

According to Horrigan (1968), the evolution of ratio analysis came about in approximately 300 BC, primarily

because of Euclid’s analysis of the properties of ratios in Book V of his Elements. Wall (1919) may have been the

first to recognize that a relative ratio criteria could be used in place of the more popular absolute ratio criteria.

Horrigan (1968) described Wall’s Study of Credit Barometrics, as historic “because it was a widely-read overt

departure from the customary usage of a single ratio with an absolute criterion” (p. 285–286). According to

Horrigan, Wall studied 981 firms and used seven ratios in his analysis. The firms were stratified by industry and

geographical areas with nine different subdivisions in each stratum. In doing this, “Wall…had, in effect,

popularized the ideas of using many ratios and using empirically determined relative ratio criteria” (Horrigan, 1968,

p. 286).

Fitzpatrick (1931) also conducted early research in this area. Fitzpatrick examined 13 ratios to see if they

could indicate failure. He examined each ratio individually using a univariate analysis. Unfortunately, Fitzpatrick

was not able to show a significant relationship with bankruptcy. Thirty-five years later Beaver (1966a and 1966b)

conducted a univariate analysis and was able to show a significant relationship. Beaver’s study is considered one of

the classics in the field.

Altman (1968) moved from using a univariate approach to using multiple discriminant analysis to predict

bankruptcy. Even today, researchers still regard Altman’s Z-Score as a good indicator of a company’s ability to

avoid bankruptcy. Altman later revised his model to incorporate a “four variable Z-Score” prediction model

(Altman, 1993). This revised model, Altman felt, significantly improved the predictive ability of his earlier model.

Later, in 1980, Ohlson published a study using "Logit" or Multiple Logistic Regressions in constructing a

bankruptcy prediction model. Ohlson felt that his study had an important advantage in that they had an important

timing advantage that allowed one to check whether the company entered bankruptcy prior to, or after the date of

release for the financials. Ohlson claimed that previous studies did not explicitly consider the timing issue.

According to Cybinski (2001), another difference between the early and late studies was that early studies were

concerned with explanation rather than prediction.

Copyright by author(s); CC-BY 2070 The Clute Institute

die. As these forces continue, companies must find better ways to predict bankruptcy. This is all the more

important in Thailand today given that much of the investment that previously came to Thailand now goes to

countries such as China and Vietnam.

Two of the primary methods used in the west to predict bankruptcy are Altman's Z-score and Ohlson's O-

score. Pongsatat, et al, (2004) examined the comparative ability of Ohlson’s Logit model and Altman’s four-

variance model for predicting bankruptcy in Thailand to determine if there was a difference in their ability to predict

bankruptcy in Thailand. This study expands on Pongsatat’s 2004 study to specifically examine Ohlson’s logit

model’s ability to predict bankruptcy for both financial and non-financial firms.

Pongsatat’s 2004 study found that this analysis is important because evidence suggests that studies

conducted in countries such as the united states and the european union may not have relevance to a country such as

thailand. Pongsatat cited tirapat and nittayagasetwat (1999) who found that the institutional structure of the financial

sector in thailand is characterized as a bank centered financial system, while that of the u.s. is a market based

system. For example, tirapat and nittayagasetwat (1999) point out that in thailand, the credits from financial

institutions such as commercial banks and finance companies can be five or more times larger than the funds raised

from the stock and bond markets. In 1997, at the height of the asian crisis, the amount was 16.7 times higher. These

are significantly larger numbers than what could be found in most western economies. Other differences in thailand

cited by tirapat and nittayagasetwat (1999) included a higher concentration of shares being held by a few individuals

and more shares with large family ownership.

DISCUSSION

The cause of business failures is a matter that has been discussed and researched at length and it has been a

topic of interest for hundreds of years. Throughout these years, ratio analysis has been at the heart of the matter.

According to Horrigan (1968), the evolution of ratio analysis came about in approximately 300 BC, primarily

because of Euclid’s analysis of the properties of ratios in Book V of his Elements. Wall (1919) may have been the

first to recognize that a relative ratio criteria could be used in place of the more popular absolute ratio criteria.

Horrigan (1968) described Wall’s Study of Credit Barometrics, as historic “because it was a widely-read overt

departure from the customary usage of a single ratio with an absolute criterion” (p. 285–286). According to

Horrigan, Wall studied 981 firms and used seven ratios in his analysis. The firms were stratified by industry and

geographical areas with nine different subdivisions in each stratum. In doing this, “Wall…had, in effect,

popularized the ideas of using many ratios and using empirically determined relative ratio criteria” (Horrigan, 1968,

p. 286).

Fitzpatrick (1931) also conducted early research in this area. Fitzpatrick examined 13 ratios to see if they

could indicate failure. He examined each ratio individually using a univariate analysis. Unfortunately, Fitzpatrick

was not able to show a significant relationship with bankruptcy. Thirty-five years later Beaver (1966a and 1966b)

conducted a univariate analysis and was able to show a significant relationship. Beaver’s study is considered one of

the classics in the field.

Altman (1968) moved from using a univariate approach to using multiple discriminant analysis to predict

bankruptcy. Even today, researchers still regard Altman’s Z-Score as a good indicator of a company’s ability to

avoid bankruptcy. Altman later revised his model to incorporate a “four variable Z-Score” prediction model

(Altman, 1993). This revised model, Altman felt, significantly improved the predictive ability of his earlier model.

Later, in 1980, Ohlson published a study using "Logit" or Multiple Logistic Regressions in constructing a

bankruptcy prediction model. Ohlson felt that his study had an important advantage in that they had an important

timing advantage that allowed one to check whether the company entered bankruptcy prior to, or after the date of

release for the financials. Ohlson claimed that previous studies did not explicitly consider the timing issue.

According to Cybinski (2001), another difference between the early and late studies was that early studies were

concerned with explanation rather than prediction.

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2071 The Clute Institute

In their study of bankruptcy in Thailand, Pongsatat, et al (2004) found that by the end of the 1970s, most

bankruptcy prediction used some form of multivariate analysis with multiple discriminant analysis the preferred

method. They found also that some researchers felt that multiple discriminant analysis had two fundamental

weaknesses. According to Jones (1987) multiple discriminant analysis does not consider prior probabilities and also

assumes an equal probability of group membership based on sample proportions. To eliminate these two

weaknesses, researchers began to use two additional statistical techniques: multiple logistic regression (or logit

analysis) and probit analysis. Kleinbaum & Klein, (2002) describe logit as a technique based on a cumulative

probability function that does not require the independent variables to be normal. Logit puts a weight on each of the

variables so that the formula generates a probability of classification putting the weighted groups into one or more

separate groups. The probit method is similar to logit except that it uses a nearly identical normal cumulative

probability function instead of the logistical cumulative function (Gentry, Newbold and Whitford, 1985). Boritz and

Kennedy (1995) described the differences between the two approaches as simply being that the logit model used the

cumulative logistic function and probit used the cumulative normal distribution.

In their review of the literature, Pongsatat et al concluded that Martin (1977) probably was the first to

conduct a study using logit analysis in bankruptcy prediction. Martin looked at 58 failed Federal Reserve member

banks and compared them to a group of non-failed banks. Using 25 financial ratios classified as asset risk, liquidity,

capital adequacy and earnings, Martin developed a model that correctly classified failed banks 87% to 96% of the

time. Pongsatat et al concluded that this ability to accurately predict failed financial firms was important in any

analysis of bankruptcy in Thailand.

As stated above, James Ohlson (1980) is acknowledged to be the first researcher to conduct a

comprehensive study of bankruptcy using logit analysis. Ohlson felt that the strength of his technique was that it

was simple to apply and could be used in a number of different circumstances (Ohlson, 1980). Ohlson did

acknowledge that the weakness in his model was that it did not consider the firm’s market transaction data.

Ohlson cited three primary problems with prior studies that had been done using the more popular multiple

discriminant analysis technique. First he objected to the statistical requirements imposed on the distributional

properties of the ratio. Among these requirements were that the variance – covariance relationships of the ratios had

to be the same for both groups and that the predictors (ratios) had to be normally distributed. Second, the output to

the multiple discriminant analysis is a score, which has little intuitive interpretation. Third, he did not feel that the

use of the procedure of matching failed and non – failed firms provided any benefit to an analysis. Ohlson felt that

the use of conditional logit analysis essentially avoids all the problems discussed with respect to multiple

discriminant analysis (Ohlson, 1980). Ohlson conducted three sets of computations using his logit model. Model

one predicted bankruptcy within one year; model two predicted bankruptcy within two years, given that the

company did not fail within the subsequent year; and model three predicted bankruptcy within one or two years.

By obtaining data from the Wall Street Journal Index in the Seventies (1970 – 1976), financial information

of 105 bankrupt firms, and 2058 non-bankrupt firms were obtained from the Compustat file. From Ohlson’s study

the results indicate that the four factors derived from financial statements that are statistically significant for

purposes of assessing the probability of bankruptcy are first, size; second, a measure of leverage (total liabilities to

total assets); third, a measure of performance (net income to total assets and fixed assets to total liabilities); and

fourth, some measures of current liquidity (working capital to total assets, current assets to current liabilities).

(Ohlson, 1980)

By the end of his study Ohlson concluded that the predictive power of the model depends upon when the

financial report is made available, and the predictive powers seem to be robust across the estimation procedure.

Finally, Ohlson recommended that further research needed to be conducted to improve the accuracy of the

prediction model. While Ohlson’s results were not as good as Altman’s, he concluded that his methodology was

more sound. He also reached another interesting conclusion from his study in that he found that the size of the firm

was the most important predictor in his model (Patterson, 2001). According to Khunthong (1997), Ohlson’s model

for predicting bankruptcy within one year, using nine accounting ratios and a cutoff point equally weighted with

type I and type II errors, gave a correct classification 96% of the time.

Copyright by author(s); CC-BY 2071 The Clute Institute

In their study of bankruptcy in Thailand, Pongsatat, et al (2004) found that by the end of the 1970s, most

bankruptcy prediction used some form of multivariate analysis with multiple discriminant analysis the preferred

method. They found also that some researchers felt that multiple discriminant analysis had two fundamental

weaknesses. According to Jones (1987) multiple discriminant analysis does not consider prior probabilities and also

assumes an equal probability of group membership based on sample proportions. To eliminate these two

weaknesses, researchers began to use two additional statistical techniques: multiple logistic regression (or logit

analysis) and probit analysis. Kleinbaum & Klein, (2002) describe logit as a technique based on a cumulative

probability function that does not require the independent variables to be normal. Logit puts a weight on each of the

variables so that the formula generates a probability of classification putting the weighted groups into one or more

separate groups. The probit method is similar to logit except that it uses a nearly identical normal cumulative

probability function instead of the logistical cumulative function (Gentry, Newbold and Whitford, 1985). Boritz and

Kennedy (1995) described the differences between the two approaches as simply being that the logit model used the

cumulative logistic function and probit used the cumulative normal distribution.

In their review of the literature, Pongsatat et al concluded that Martin (1977) probably was the first to

conduct a study using logit analysis in bankruptcy prediction. Martin looked at 58 failed Federal Reserve member

banks and compared them to a group of non-failed banks. Using 25 financial ratios classified as asset risk, liquidity,

capital adequacy and earnings, Martin developed a model that correctly classified failed banks 87% to 96% of the

time. Pongsatat et al concluded that this ability to accurately predict failed financial firms was important in any

analysis of bankruptcy in Thailand.

As stated above, James Ohlson (1980) is acknowledged to be the first researcher to conduct a

comprehensive study of bankruptcy using logit analysis. Ohlson felt that the strength of his technique was that it

was simple to apply and could be used in a number of different circumstances (Ohlson, 1980). Ohlson did

acknowledge that the weakness in his model was that it did not consider the firm’s market transaction data.

Ohlson cited three primary problems with prior studies that had been done using the more popular multiple

discriminant analysis technique. First he objected to the statistical requirements imposed on the distributional

properties of the ratio. Among these requirements were that the variance – covariance relationships of the ratios had

to be the same for both groups and that the predictors (ratios) had to be normally distributed. Second, the output to

the multiple discriminant analysis is a score, which has little intuitive interpretation. Third, he did not feel that the

use of the procedure of matching failed and non – failed firms provided any benefit to an analysis. Ohlson felt that

the use of conditional logit analysis essentially avoids all the problems discussed with respect to multiple

discriminant analysis (Ohlson, 1980). Ohlson conducted three sets of computations using his logit model. Model

one predicted bankruptcy within one year; model two predicted bankruptcy within two years, given that the

company did not fail within the subsequent year; and model three predicted bankruptcy within one or two years.

By obtaining data from the Wall Street Journal Index in the Seventies (1970 – 1976), financial information

of 105 bankrupt firms, and 2058 non-bankrupt firms were obtained from the Compustat file. From Ohlson’s study

the results indicate that the four factors derived from financial statements that are statistically significant for

purposes of assessing the probability of bankruptcy are first, size; second, a measure of leverage (total liabilities to

total assets); third, a measure of performance (net income to total assets and fixed assets to total liabilities); and

fourth, some measures of current liquidity (working capital to total assets, current assets to current liabilities).

(Ohlson, 1980)

By the end of his study Ohlson concluded that the predictive power of the model depends upon when the

financial report is made available, and the predictive powers seem to be robust across the estimation procedure.

Finally, Ohlson recommended that further research needed to be conducted to improve the accuracy of the

prediction model. While Ohlson’s results were not as good as Altman’s, he concluded that his methodology was

more sound. He also reached another interesting conclusion from his study in that he found that the size of the firm

was the most important predictor in his model (Patterson, 2001). According to Khunthong (1997), Ohlson’s model

for predicting bankruptcy within one year, using nine accounting ratios and a cutoff point equally weighted with

type I and type II errors, gave a correct classification 96% of the time.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2072 The Clute Institute

A review of the literature indicates that it was the Thai Baht crises and the resultant increase in

bankruptcies that may have caused researchers to begin to investigate the use of bankruptcy prediction models in

Thailand. The financial crisis occurred when banks and financial companies borrowed heavily on a short–term basis

from banks in other countries - primarily Japan and the United States - and made overly risky loans to finance the

construction of commercial and residential units. When the demand for such units was not forthcoming as expected,

a domino effect occurred: the real estate investors who borrowed defaulted, their lenders defaulted, and the banks

were left with foreign currency denominated loans requiring payment. A subsequent foreign exchange crisis

followed the collapse of the real estate market.

Treewichayapong, et al (2011) conducted a study on real estate bankruptcy in Thailand and found that the

results of the bankruptcy prediction using binary logistic regression and Cox proportional hazards model show that

financial ratios, as leading indicators of corporate bankruptcy, play more significant roles than company specific and

corporate variables. Reynolds et al (2002) examined the financial capital structure of major financial companies in

Thailand over the period 1993 – 1998. Their stated purpose was to estimate the probability of a financial company

surviving in 1997 when the Thailand financial crisis began. The prediction model applied both probit and logistic

binomial regression analyses to estimate the probability of financial distress (defined by Reynolds et al as firms

closed down or reorganized) for firms traded on the Stock Exchange of Thailand. The financial data was obtained

from balance sheet and income statements for 91 financial companies over the period 1993 to 1996.

Tirapat and Nittayagasetwat (1999) used a logit regression to develop a macro-related micro-crises

investigation model for the 459 firms listed in the Stock Exchange of Thailand (SET) in 1996. Fifty-five of these

firms were financially distressed under the definition used by the SET. Tirapat and Nittayagasetwat’s sample

included 341 of the 404 non-failed firms and all 55 of the failed firms. Tirapat and Nittayagasetwat used the SET's

definition of a failed firm. This definition says that a firm is distressed when it is either closed down by the Thai

government or required by the stock exchange or the Bank of Thailand to submit a restructuring plans.

In their logit regression, Tirapat and Nittayagasetwat (1999) incorporated a two-step process whereby

“changes in macroeconomic factors and the firm’s sensitivity to those factors affect the firm’s stock return, with a

firm’s stock return in turn having an effect on the firm’s probability of financial distress” (p.106). The total

prediction accuracy of the Tirapat and Nittayagasetwat model equaled 63.89% for the full-sample test, 77.49% for

the in-sample test, and 75.76% for the out-sample test. The results of their study suggest that a firm with a higher

estimated rate of return has a lower probability of financial distress. Their study also indicates the importance of

macroeconomic conditions because they can strongly influence the probability of a firm’s financial distress. The

researchers found that the only significant macro factor was the sensitivity of the firm to inflation. In summary, they

concluded that only the systematic risk of a firm exposed to inflation affects the probability of the firm’s financial

distress. The higher a firm’s sensitivity to inflation, the more likely the firm’s exposure to financial distress.

Ohlson’s model has been used in a variety of scenarios other than bankruptcy. For example, Lee et al. (2014)

evaluated the predictive power of the Ohlson model for future market value assessment. Noga and Schnader, (2013)

expanded on Ohlson’s model by investigating the association between abnormal changes in book-tax differences

(BTDs) and bankruptcy using a hazard model and out-of-sample testing.

RESEARCH METHODOLOGY

This study uses the logit analysis technique as popularized by Ohlson. Ohlson used this method to develop

his “O-score” to be used as a model. There are a variety of reasons for selecting Ohlson’s model for this study.

Some researchers feel that multiple discriminant analysis has two fundamental weaknesses. As stated earlier,

according to Jones (1987) multiple discriminant analysis does not consider prior probabilities and also must assume

an equal probability of group membership based on sample proportions. Ohlson (1980) argues that these statistical

requirements on the distributional properties of the predictors cause significant problems. For example, Ohlson,

states that the requirement of a normally distributed predictor argues against the use of a dummy variable. This

limitation, according to Ohlson, severely limits the model as a discriminating tool. Logit analysis, it is argued,

eliminates these two weaknesses.

Copyright by author(s); CC-BY 2072 The Clute Institute

A review of the literature indicates that it was the Thai Baht crises and the resultant increase in

bankruptcies that may have caused researchers to begin to investigate the use of bankruptcy prediction models in

Thailand. The financial crisis occurred when banks and financial companies borrowed heavily on a short–term basis

from banks in other countries - primarily Japan and the United States - and made overly risky loans to finance the

construction of commercial and residential units. When the demand for such units was not forthcoming as expected,

a domino effect occurred: the real estate investors who borrowed defaulted, their lenders defaulted, and the banks

were left with foreign currency denominated loans requiring payment. A subsequent foreign exchange crisis

followed the collapse of the real estate market.

Treewichayapong, et al (2011) conducted a study on real estate bankruptcy in Thailand and found that the

results of the bankruptcy prediction using binary logistic regression and Cox proportional hazards model show that

financial ratios, as leading indicators of corporate bankruptcy, play more significant roles than company specific and

corporate variables. Reynolds et al (2002) examined the financial capital structure of major financial companies in

Thailand over the period 1993 – 1998. Their stated purpose was to estimate the probability of a financial company

surviving in 1997 when the Thailand financial crisis began. The prediction model applied both probit and logistic

binomial regression analyses to estimate the probability of financial distress (defined by Reynolds et al as firms

closed down or reorganized) for firms traded on the Stock Exchange of Thailand. The financial data was obtained

from balance sheet and income statements for 91 financial companies over the period 1993 to 1996.

Tirapat and Nittayagasetwat (1999) used a logit regression to develop a macro-related micro-crises

investigation model for the 459 firms listed in the Stock Exchange of Thailand (SET) in 1996. Fifty-five of these

firms were financially distressed under the definition used by the SET. Tirapat and Nittayagasetwat’s sample

included 341 of the 404 non-failed firms and all 55 of the failed firms. Tirapat and Nittayagasetwat used the SET's

definition of a failed firm. This definition says that a firm is distressed when it is either closed down by the Thai

government or required by the stock exchange or the Bank of Thailand to submit a restructuring plans.

In their logit regression, Tirapat and Nittayagasetwat (1999) incorporated a two-step process whereby

“changes in macroeconomic factors and the firm’s sensitivity to those factors affect the firm’s stock return, with a

firm’s stock return in turn having an effect on the firm’s probability of financial distress” (p.106). The total

prediction accuracy of the Tirapat and Nittayagasetwat model equaled 63.89% for the full-sample test, 77.49% for

the in-sample test, and 75.76% for the out-sample test. The results of their study suggest that a firm with a higher

estimated rate of return has a lower probability of financial distress. Their study also indicates the importance of

macroeconomic conditions because they can strongly influence the probability of a firm’s financial distress. The

researchers found that the only significant macro factor was the sensitivity of the firm to inflation. In summary, they

concluded that only the systematic risk of a firm exposed to inflation affects the probability of the firm’s financial

distress. The higher a firm’s sensitivity to inflation, the more likely the firm’s exposure to financial distress.

Ohlson’s model has been used in a variety of scenarios other than bankruptcy. For example, Lee et al. (2014)

evaluated the predictive power of the Ohlson model for future market value assessment. Noga and Schnader, (2013)

expanded on Ohlson’s model by investigating the association between abnormal changes in book-tax differences

(BTDs) and bankruptcy using a hazard model and out-of-sample testing.

RESEARCH METHODOLOGY

This study uses the logit analysis technique as popularized by Ohlson. Ohlson used this method to develop

his “O-score” to be used as a model. There are a variety of reasons for selecting Ohlson’s model for this study.

Some researchers feel that multiple discriminant analysis has two fundamental weaknesses. As stated earlier,

according to Jones (1987) multiple discriminant analysis does not consider prior probabilities and also must assume

an equal probability of group membership based on sample proportions. Ohlson (1980) argues that these statistical

requirements on the distributional properties of the predictors cause significant problems. For example, Ohlson,

states that the requirement of a normally distributed predictor argues against the use of a dummy variable. This

limitation, according to Ohlson, severely limits the model as a discriminating tool. Logit analysis, it is argued,

eliminates these two weaknesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2073 The Clute Institute

Other researchers have agreed with Ohlson stating that because logit analysis is based on a cumulative

probability function it does not require the independent variables to be normal. Logit puts a weight on each of the

variables so that the formula generates a probability of classification putting the weighted groups into one or more

separate groups.

Still another argument for logit analysis in this study is that the SET in Thailand has a significant number of

financial firms, some of which have faced financial distress. There is some indication that multiple discriminant

analysis does not provide a good prediction for financial firms. Pastena and Ruland (1986) used multiple

discriminant analysis in their study but stated that they, “restricted the sample to manufacturing firms since the

Altman model was not developed for banks, insurance companies, or other nonmanufacturing businesses” (p. 294).

Other researchers have come to similar conclusions. Dietrich and Kaplan (1982), for example, stated that probit

analysis was theoretically superior to multiple discriminant analysis in their study of bank loans. The elimination of

financial institutions is not a restriction that would be possible in this study.

Still another question to address is whether to use the logit or probit method. The probit method is similar

to logit except that it uses a nearly identical normal cumulative probability function instead of the logistical

cumulative function (Gentry, Newbold and Whitford, 1985). Boritz and Kennedy (1995) described the differences

between the two approaches as simply being that the logit model used the cumulative logistic function and probit

used the cumulative normal distribution. Because the logit method has been more thoroughly tested and because it

is the method used by Ohlson in developing his model, this study uses the logit approach.

Research Question

The following research question investigates the research problem of this study:

Is there a significant difference in ohlson’s o-score as measured by ohlson’s logit analysis model between

bankrupt and non-bankrupt firms in thailand?

The literature discloses only a few studies of bankruptcy in thailand, which were primarily motivated by the

1997 thai baht crisis that caused thailand to experience a number of bankruptcies. The research in thailand on this

subject is so narrow that there is not broad agreement on what factors accurately predict bankruptcy and there is a

divergence of conclusions reached. The answer to this research question may help to reconcile some of the past

disagreements.

Hypothesis Development

The research question stated above gives rise to and forms the basis for the following hypothesis.

H1: There is no difference in the mean of ohlson’s o score as measured by ohlson’s logit analysis between bankrupt

and non-bankrupt firms in Thailand.

The dependent variables in this study are defined as failed or non-failed firms in Thailand as identified by

the Stock Exchange of Thailand or the Bank of Thailand. The dependent variables will be coded as “0” for a non-

failed firm and “1” for a failed firm. This methodology is consistent with the approach used by Ohlson (1980).

Independent variables consist of the financial ratios used by Ohlson. They are:

Size = Log of the total assets / log of GNP price level index

TLTA = Total liabilities / total assets

WCTA = Working capital / total assets

CLCA = Current liabilities / current assets

NITA = Net income / total assets

FUTL = Cash flows from operation / total liabilities (Note that Ohlson used “funds from operations” as

that was the reporting method of the day. Currently, cash flow from operations is the approximately

equivalent figure for funds. Accordingly, this study uses cash flows from operations as a proxy for funds

from operations.)

Copyright by author(s); CC-BY 2073 The Clute Institute

Other researchers have agreed with Ohlson stating that because logit analysis is based on a cumulative

probability function it does not require the independent variables to be normal. Logit puts a weight on each of the

variables so that the formula generates a probability of classification putting the weighted groups into one or more

separate groups.

Still another argument for logit analysis in this study is that the SET in Thailand has a significant number of

financial firms, some of which have faced financial distress. There is some indication that multiple discriminant

analysis does not provide a good prediction for financial firms. Pastena and Ruland (1986) used multiple

discriminant analysis in their study but stated that they, “restricted the sample to manufacturing firms since the

Altman model was not developed for banks, insurance companies, or other nonmanufacturing businesses” (p. 294).

Other researchers have come to similar conclusions. Dietrich and Kaplan (1982), for example, stated that probit

analysis was theoretically superior to multiple discriminant analysis in their study of bank loans. The elimination of

financial institutions is not a restriction that would be possible in this study.

Still another question to address is whether to use the logit or probit method. The probit method is similar

to logit except that it uses a nearly identical normal cumulative probability function instead of the logistical

cumulative function (Gentry, Newbold and Whitford, 1985). Boritz and Kennedy (1995) described the differences

between the two approaches as simply being that the logit model used the cumulative logistic function and probit

used the cumulative normal distribution. Because the logit method has been more thoroughly tested and because it

is the method used by Ohlson in developing his model, this study uses the logit approach.

Research Question

The following research question investigates the research problem of this study:

Is there a significant difference in ohlson’s o-score as measured by ohlson’s logit analysis model between

bankrupt and non-bankrupt firms in thailand?

The literature discloses only a few studies of bankruptcy in thailand, which were primarily motivated by the

1997 thai baht crisis that caused thailand to experience a number of bankruptcies. The research in thailand on this

subject is so narrow that there is not broad agreement on what factors accurately predict bankruptcy and there is a

divergence of conclusions reached. The answer to this research question may help to reconcile some of the past

disagreements.

Hypothesis Development

The research question stated above gives rise to and forms the basis for the following hypothesis.

H1: There is no difference in the mean of ohlson’s o score as measured by ohlson’s logit analysis between bankrupt

and non-bankrupt firms in Thailand.

The dependent variables in this study are defined as failed or non-failed firms in Thailand as identified by

the Stock Exchange of Thailand or the Bank of Thailand. The dependent variables will be coded as “0” for a non-

failed firm and “1” for a failed firm. This methodology is consistent with the approach used by Ohlson (1980).

Independent variables consist of the financial ratios used by Ohlson. They are:

Size = Log of the total assets / log of GNP price level index

TLTA = Total liabilities / total assets

WCTA = Working capital / total assets

CLCA = Current liabilities / current assets

NITA = Net income / total assets

FUTL = Cash flows from operation / total liabilities (Note that Ohlson used “funds from operations” as

that was the reporting method of the day. Currently, cash flow from operations is the approximately

equivalent figure for funds. Accordingly, this study uses cash flows from operations as a proxy for funds

from operations.)

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2074 The Clute Institute

Dummy variables will be used to adjust for certain microeconomic variables. The dummy variables are:

OENEG = 1, if net income was negative for the last two years = 0, otherwise.

INTWO = 1, if total liabilities is greater than total assets = 0, otherwise.

Changes in net income will be accounted for by using the following variable:

CHIN = (NIt - NIt - 1) divided by (|NI t| + |NIt - 1|) where NI t is net income for the most recent period. The (|)

symbol indicates that the absolute value of the variable is to be used.

While other researchers have examined the effect of different variables (see Khodadadi et al. 2013), the

financial statement variables used above are the same as those used by Ohlson (1980) in the development of his O-

score. Ohlson stated that “common sense” suggests that the sign of the coefficients would be as follows:

Positive Negative Indeterminate

TLTA SIZE OENIG

CLCA WCTA

INTWO NITA

FUTL

CHIN

As stated above, this study uses logit analysis to compare the failed and non-failed firms. Logit analysis is

a member of the general class of models called log-linear models and can be used in a variety of circumstances to

deal with any number of outcome variables (Simonoff, 1997). However, in this study, logit is used to perform a

logistic regression in which a two-value (binary) outcome is predicted by a variety of variables. In the literature,

logit is described as a variation of ordinary regression and is used most frequently to model the relationship between

two outcome variables and a set of explanatory variables. While the outcome variables in this study are failed and

non-failed firms, the outcome variable could be any dichotomous variable such as “dead” or “alive” in medicine, or

“sell” or “don’t sell” in investing (Dorak, 2002). The usual goal of logit analysis is to focus on group membership.

As stated earlier, logit analysis makes no assumptions about such things as normality or linear relationships.

Furthermore, equal variances and the distribution of the predictor variables are not issues to be considered. These

advantages are somewhat offset by the fact that the regression is sensitive to extreme variables in the predictor

variables and collinearity (Kleinbaum, & Klein, 2002). Because of this sensitivity, this study takes extreme care in

the pre-screening of the predictor variables.

Logit analysis depends heavily on probability. Because this study uses matched pair samples with an equal

number of failed and non-failed firms, the probability of randomly selecting a failed firm is 50% or 0.5. To illustrate

further, in a similar way, the probability of rolling a “six” on a single roll of a die would be 1/6 or 0.16667.

In a logistic regression, the “odds” of an event is defined as the probability of an event occurring, divided

by the probability of the event not occurring. The probability of not rolling a six on a roll of a die would be 1-p(X)

or 0.8333. The odds, therefore, would be the 0.16667 divided by 0.8333 or 0.2. The odds ratio for a predictor tells

the relative amount by which the odds of the outcome increase or decrease when the value of the predictor is

increased by one unit. One of the fundamental rules in probability analysis is that probabilities cannot exceed one.

Note, however, that while the probabilities cannot exceed one, the odds can be greater than one. It is in the creation

of the odds that the “logit” comes into play. The logit is the natural logarithm of the odds. Accordingly, the logit of

rolling a six would be the natural log of 0.2 or a minus 1.609 (Kleinbaum, & Klein, 2002).

Recall from above that Ohlson’s logistic regression model was given as:

P(B) = 1/1+e-z

This formula is the logistical regression that was run to address the research question in the study. The

three major results from this analysis consist of two primary elements. The first is a classification table that

identifies the correct and incorrect classifications identified by the model. The second measurement seeks to obtain

an indication of how well the data fits the model. Indicators of this fit include the statistical significance for each

variable in the equation as well as a Chi-square statistic for each variable. The overall measure of the fit of the

model considers the log-likelihood statistic along with an appropriate goodness of fit statistic (R 2).

Copyright by author(s); CC-BY 2074 The Clute Institute

Dummy variables will be used to adjust for certain microeconomic variables. The dummy variables are:

OENEG = 1, if net income was negative for the last two years = 0, otherwise.

INTWO = 1, if total liabilities is greater than total assets = 0, otherwise.

Changes in net income will be accounted for by using the following variable:

CHIN = (NIt - NIt - 1) divided by (|NI t| + |NIt - 1|) where NI t is net income for the most recent period. The (|)

symbol indicates that the absolute value of the variable is to be used.

While other researchers have examined the effect of different variables (see Khodadadi et al. 2013), the

financial statement variables used above are the same as those used by Ohlson (1980) in the development of his O-

score. Ohlson stated that “common sense” suggests that the sign of the coefficients would be as follows:

Positive Negative Indeterminate

TLTA SIZE OENIG

CLCA WCTA

INTWO NITA

FUTL

CHIN

As stated above, this study uses logit analysis to compare the failed and non-failed firms. Logit analysis is

a member of the general class of models called log-linear models and can be used in a variety of circumstances to

deal with any number of outcome variables (Simonoff, 1997). However, in this study, logit is used to perform a

logistic regression in which a two-value (binary) outcome is predicted by a variety of variables. In the literature,

logit is described as a variation of ordinary regression and is used most frequently to model the relationship between

two outcome variables and a set of explanatory variables. While the outcome variables in this study are failed and

non-failed firms, the outcome variable could be any dichotomous variable such as “dead” or “alive” in medicine, or

“sell” or “don’t sell” in investing (Dorak, 2002). The usual goal of logit analysis is to focus on group membership.

As stated earlier, logit analysis makes no assumptions about such things as normality or linear relationships.

Furthermore, equal variances and the distribution of the predictor variables are not issues to be considered. These

advantages are somewhat offset by the fact that the regression is sensitive to extreme variables in the predictor

variables and collinearity (Kleinbaum, & Klein, 2002). Because of this sensitivity, this study takes extreme care in

the pre-screening of the predictor variables.

Logit analysis depends heavily on probability. Because this study uses matched pair samples with an equal

number of failed and non-failed firms, the probability of randomly selecting a failed firm is 50% or 0.5. To illustrate

further, in a similar way, the probability of rolling a “six” on a single roll of a die would be 1/6 or 0.16667.

In a logistic regression, the “odds” of an event is defined as the probability of an event occurring, divided

by the probability of the event not occurring. The probability of not rolling a six on a roll of a die would be 1-p(X)

or 0.8333. The odds, therefore, would be the 0.16667 divided by 0.8333 or 0.2. The odds ratio for a predictor tells

the relative amount by which the odds of the outcome increase or decrease when the value of the predictor is

increased by one unit. One of the fundamental rules in probability analysis is that probabilities cannot exceed one.

Note, however, that while the probabilities cannot exceed one, the odds can be greater than one. It is in the creation

of the odds that the “logit” comes into play. The logit is the natural logarithm of the odds. Accordingly, the logit of

rolling a six would be the natural log of 0.2 or a minus 1.609 (Kleinbaum, & Klein, 2002).

Recall from above that Ohlson’s logistic regression model was given as:

P(B) = 1/1+e-z

This formula is the logistical regression that was run to address the research question in the study. The

three major results from this analysis consist of two primary elements. The first is a classification table that

identifies the correct and incorrect classifications identified by the model. The second measurement seeks to obtain

an indication of how well the data fits the model. Indicators of this fit include the statistical significance for each

variable in the equation as well as a Chi-square statistic for each variable. The overall measure of the fit of the

model considers the log-likelihood statistic along with an appropriate goodness of fit statistic (R 2).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2075 The Clute Institute

Description of Population and Sample

Similar to Pongsatat et al. (2004) the population of this study is the firms listed on the Stock Exchange of

Thailand. From this population, a sample was selected of 60 failed or financially distressed firms and 60 non-failed

firms. A failed firm or financially distressed firm is one that either: (1) has been liquidated during the current year,

(2) has received an audit that expresses concern about the going concern capabilities of the firm, (3) has been closed

down by governmental authorities, (4) has been asked to submit restructuring plans by the Bank of Thailand or the

Stock Exchange of Thailand or (5) has filed bankruptcy proceedings in one or more countries or some other

notification indicating bankruptcy proceedings. To be selected for study, all firms must have been in business and

published financial statements for each of the three years prior to failure. Financial information, including all

financial statements was drawn from the e-library of the Stock Exchange of Thailand. Additional information for

specific companies were drawn from the annual reports of those firms. Each of the 60 failed and non-failed firms

were matched using their SIC code and their asset size.

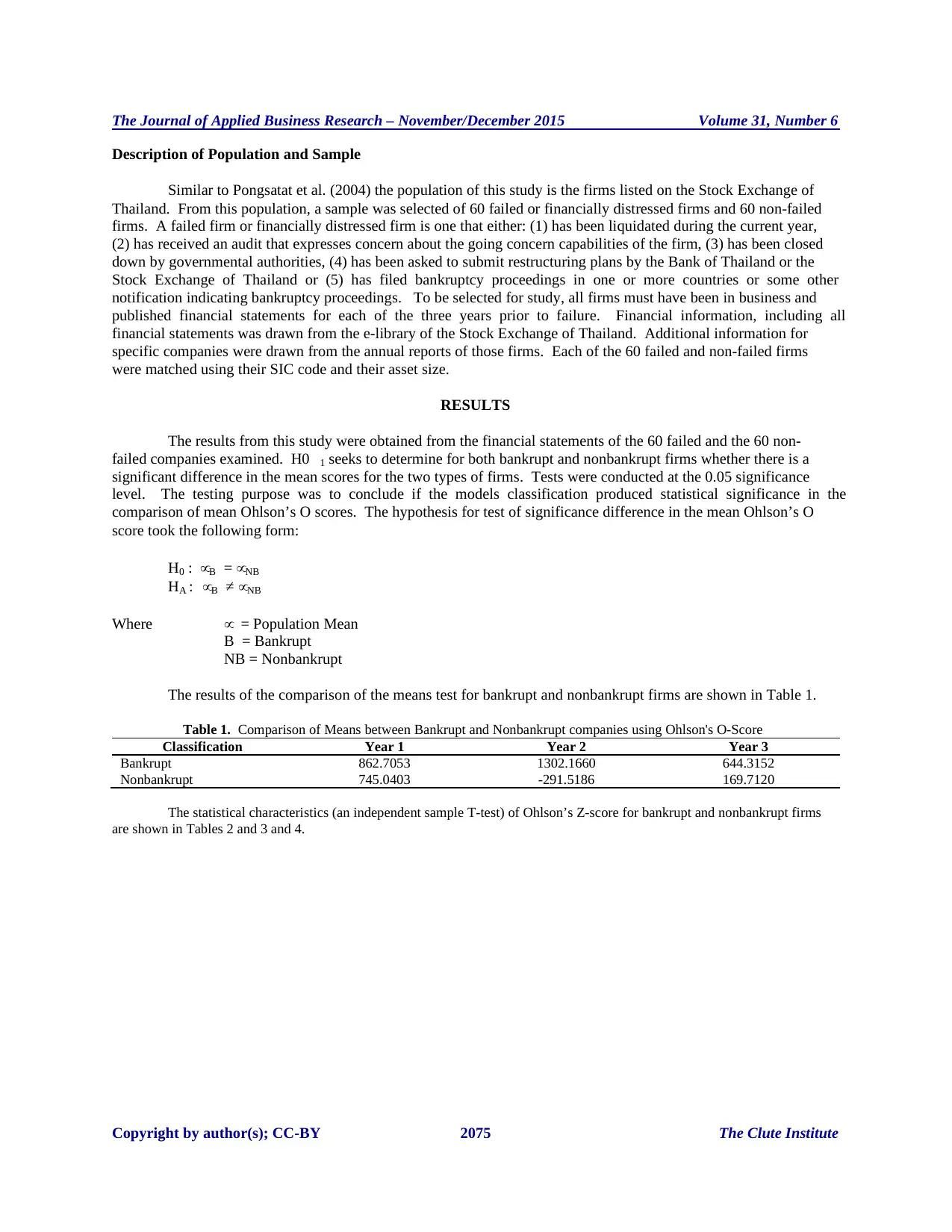

RESULTS

The results from this study were obtained from the financial statements of the 60 failed and the 60 non-

failed companies examined. H0 1 seeks to determine for both bankrupt and nonbankrupt firms whether there is a

significant difference in the mean scores for the two types of firms. Tests were conducted at the 0.05 significance

level. The testing purpose was to conclude if the models classification produced statistical significance in the

comparison of mean Ohlson’s O scores. The hypothesis for test of significance difference in the mean Ohlson’s O

score took the following form:

H0 : μB = μNB

HA : μB ≠ μNB

Where μ = Population Mean

B = Bankrupt

NB = Nonbankrupt

The results of the comparison of the means test for bankrupt and nonbankrupt firms are shown in Table 1.

Table 1. Comparison of Means between Bankrupt and Nonbankrupt companies using Ohlson's O-Score

Classification Year 1 Year 2 Year 3

Bankrupt 862.7053 1302.1660 644.3152

Nonbankrupt 745.0403 -291.5186 169.7120

The statistical characteristics (an independent sample T-test) of Ohlson’s Z-score for bankrupt and nonbankrupt firms

are shown in Tables 2 and 3 and 4.

Copyright by author(s); CC-BY 2075 The Clute Institute

Description of Population and Sample

Similar to Pongsatat et al. (2004) the population of this study is the firms listed on the Stock Exchange of

Thailand. From this population, a sample was selected of 60 failed or financially distressed firms and 60 non-failed

firms. A failed firm or financially distressed firm is one that either: (1) has been liquidated during the current year,

(2) has received an audit that expresses concern about the going concern capabilities of the firm, (3) has been closed

down by governmental authorities, (4) has been asked to submit restructuring plans by the Bank of Thailand or the

Stock Exchange of Thailand or (5) has filed bankruptcy proceedings in one or more countries or some other

notification indicating bankruptcy proceedings. To be selected for study, all firms must have been in business and

published financial statements for each of the three years prior to failure. Financial information, including all

financial statements was drawn from the e-library of the Stock Exchange of Thailand. Additional information for

specific companies were drawn from the annual reports of those firms. Each of the 60 failed and non-failed firms

were matched using their SIC code and their asset size.

RESULTS

The results from this study were obtained from the financial statements of the 60 failed and the 60 non-

failed companies examined. H0 1 seeks to determine for both bankrupt and nonbankrupt firms whether there is a

significant difference in the mean scores for the two types of firms. Tests were conducted at the 0.05 significance

level. The testing purpose was to conclude if the models classification produced statistical significance in the

comparison of mean Ohlson’s O scores. The hypothesis for test of significance difference in the mean Ohlson’s O

score took the following form:

H0 : μB = μNB

HA : μB ≠ μNB

Where μ = Population Mean

B = Bankrupt

NB = Nonbankrupt

The results of the comparison of the means test for bankrupt and nonbankrupt firms are shown in Table 1.

Table 1. Comparison of Means between Bankrupt and Nonbankrupt companies using Ohlson's O-Score

Classification Year 1 Year 2 Year 3

Bankrupt 862.7053 1302.1660 644.3152

Nonbankrupt 745.0403 -291.5186 169.7120

The statistical characteristics (an independent sample T-test) of Ohlson’s Z-score for bankrupt and nonbankrupt firms

are shown in Tables 2 and 3 and 4.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2076 The Clute Institute

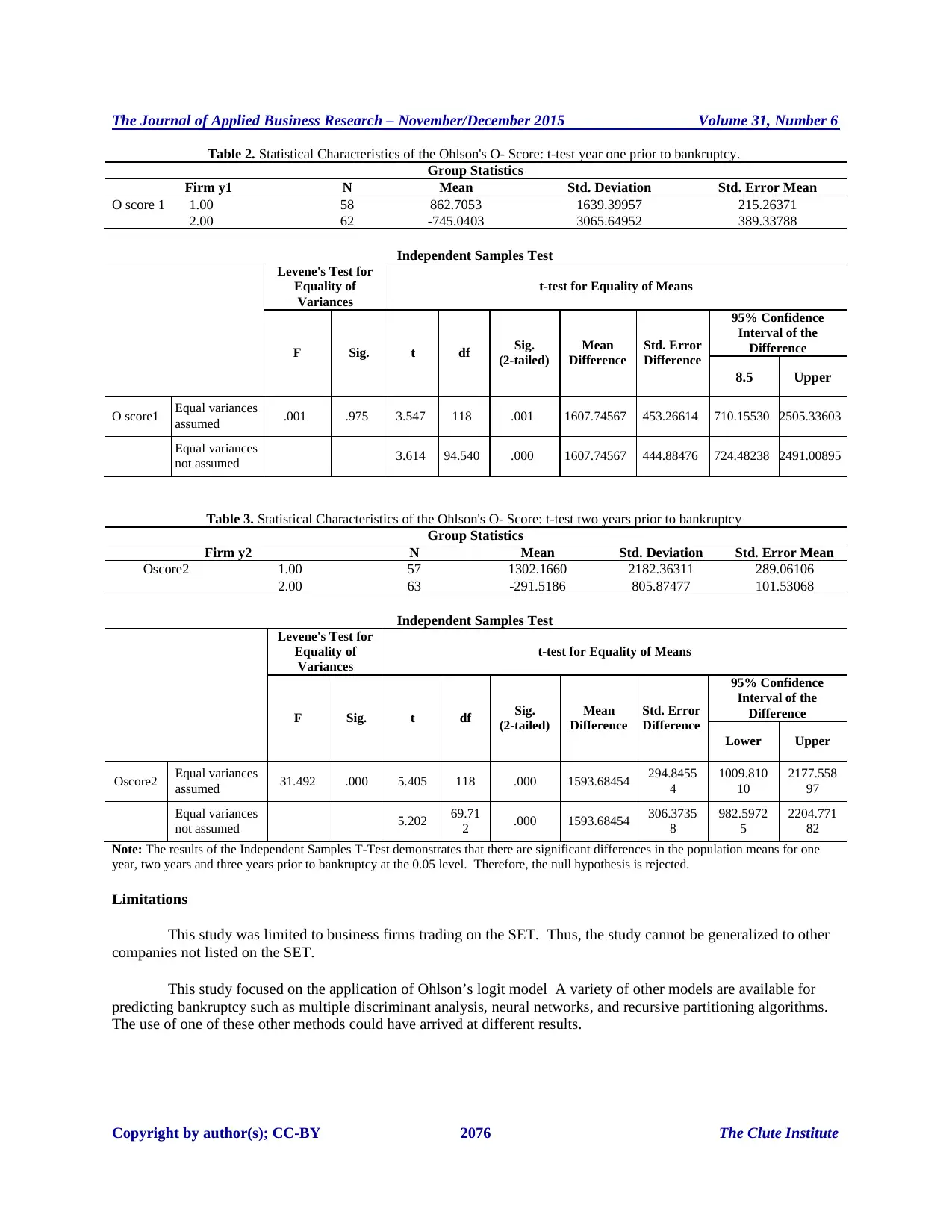

Table 2. Statistical Characteristics of the Ohlson's O- Score: t-test year one prior to bankruptcy.

Group Statistics

Firm y1 N Mean Std. Deviation Std. Error Mean

O score 1 1.00 58 862.7053 1639.39957 215.26371

2.00 62 -745.0403 3065.64952 389.33788

Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig.

(2-tailed)

Mean

Difference

Std. Error

Difference

95% Confidence

Interval of the

Difference

8.5 Upper

O score1 Equal variances

assumed .001 .975 3.547 118 .001 1607.74567 453.26614 710.15530 2505.33603

Equal variances

not assumed 3.614 94.540 .000 1607.74567 444.88476 724.48238 2491.00895

Table 3. Statistical Characteristics of the Ohlson's O- Score: t-test two years prior to bankruptcy

Group Statistics

Firm y2 N Mean Std. Deviation Std. Error Mean

Oscore2 1.00 57 1302.1660 2182.36311 289.06106

2.00 63 -291.5186 805.87477 101.53068

Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig.

(2-tailed)

Mean

Difference

Std. Error

Difference

95% Confidence

Interval of the

Difference

Lower Upper

Oscore2 Equal variances

assumed 31.492 .000 5.405 118 .000 1593.68454 294.8455

4

1009.810

10

2177.558

97

Equal variances

not assumed 5.202 69.71

2 .000 1593.68454 306.3735

8

982.5972

5

2204.771

82

Note: The results of the Independent Samples T-Test demonstrates that there are significant differences in the population means for one

year, two years and three years prior to bankruptcy at the 0.05 level. Therefore, the null hypothesis is rejected.

Limitations

This study was limited to business firms trading on the SET. Thus, the study cannot be generalized to other

companies not listed on the SET.

This study focused on the application of Ohlson’s logit model A variety of other models are available for

predicting bankruptcy such as multiple discriminant analysis, neural networks, and recursive partitioning algorithms.

The use of one of these other methods could have arrived at different results.

Copyright by author(s); CC-BY 2076 The Clute Institute

Table 2. Statistical Characteristics of the Ohlson's O- Score: t-test year one prior to bankruptcy.

Group Statistics

Firm y1 N Mean Std. Deviation Std. Error Mean

O score 1 1.00 58 862.7053 1639.39957 215.26371

2.00 62 -745.0403 3065.64952 389.33788

Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig.

(2-tailed)

Mean

Difference

Std. Error

Difference

95% Confidence

Interval of the

Difference

8.5 Upper

O score1 Equal variances

assumed .001 .975 3.547 118 .001 1607.74567 453.26614 710.15530 2505.33603

Equal variances

not assumed 3.614 94.540 .000 1607.74567 444.88476 724.48238 2491.00895

Table 3. Statistical Characteristics of the Ohlson's O- Score: t-test two years prior to bankruptcy

Group Statistics

Firm y2 N Mean Std. Deviation Std. Error Mean

Oscore2 1.00 57 1302.1660 2182.36311 289.06106

2.00 63 -291.5186 805.87477 101.53068

Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig.

(2-tailed)

Mean

Difference

Std. Error

Difference

95% Confidence

Interval of the

Difference

Lower Upper

Oscore2 Equal variances

assumed 31.492 .000 5.405 118 .000 1593.68454 294.8455

4

1009.810

10

2177.558

97

Equal variances

not assumed 5.202 69.71

2 .000 1593.68454 306.3735

8

982.5972

5

2204.771

82

Note: The results of the Independent Samples T-Test demonstrates that there are significant differences in the population means for one

year, two years and three years prior to bankruptcy at the 0.05 level. Therefore, the null hypothesis is rejected.

Limitations

This study was limited to business firms trading on the SET. Thus, the study cannot be generalized to other

companies not listed on the SET.

This study focused on the application of Ohlson’s logit model A variety of other models are available for

predicting bankruptcy such as multiple discriminant analysis, neural networks, and recursive partitioning algorithms.

The use of one of these other methods could have arrived at different results.

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2077 The Clute Institute

Implications of the Research

Many companies all over the world enter financial distress for a variety of reasons including poor

management, dishonest management, economic recession, changes in globalization, and even war and terrorism.

Major bankruptcies such as Enron, WorldCom, and Waste Management have caused tens of thousands of employees

to lose their jobs, and a greater number of investors to lose their savings. Bankers and creditors lost billions of

dollars; communities lost vital services, and the economy of the country suffered. Much of these losses could have

been avoided with a suitable early warning system that identified weaknesses and allowed the constituents to make

adequate plans and take necessary steps.

Recommendations for Future Research

Because of the limited focus of this study, it would be helpful for future research to apply similar

bankruptcy prediction models to business firms not publicly traded on the Stock Market of Thailand.

Because of the high level of Type α errors in this study, future research should examine other bankruptcy

models to determine if a lower level of Type α errors can be realized.

Given the low incidence of research in the area of civil service and government enterprise areas, it is

suggested that these areas be examined in future research to identify better when these areas are in danger of failure.

AUTHOR INFORMATION

Dr. Judy Ramage Lawrence is Professor of Accounting at Christian Brothers University. She holds a BS from the

University of Memphis, an MS from the University of Arkansas, and a DBA from Nova Southeastern University.

She has over years’ experience in accounting in both local and Big Four accounting firms. Her research interest are

in the areas of fraud examination and international accounting. Dr. Lawrence has over 30 publications in refereed

journals

Dr. Surapol Pongsatat is a lecturer in the Advanced MBA program at Ramkhamhaeng University in Bangkok,

Thailand. Dr. Pongsatat is also an advisor in the DPA program at Phetchabun Rajabhat University in the Mueang

Phetchabun District, Phetchabun, Thailand. Dr. Pongsat’s current research interests are in the field of international

business and bankruptcy.

Dr. Howard Lawrence is Clinical Professor of Accounting at The University of Mississippi. He holds a BS in

Mechanical Engineering from Christian Brothers University, an MBA from the University of Memphis, and a PhD

from the University of Mississippi. Dr. Lawrence has over 20 years’ experience in the paper industry and the steel

industry. His research interest are in the area of international accounting and fraud examination.

REFERENCES

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Papers and

proceedings of the Twenty-Ninth Annual Meeting of the American Finance Association, Detroit, Michigan

December 28-30, The Journal of Finance, 23(4), 589-609.

Altman, E. I. (1993). Corporate Financial Distress and Bankruptcy: A Complete Guide to Predicting and Avoiding

Distress and Profiting from Bankruptcy, 2 nd Ed. New York: John Wiley and Sons.

Beaver, W. H. (1966a). Financial ratios as predictors of failure. Empirical Research in Accounting: Selected Studies,

71-111.

Beaver, W. H. (1966b). Market prices, financial ratios, and the prediction of failure. Journal of Accounting

Research, 6(2), 179-182.

Boritz, J. E, & Kennedy, D. B. (1995). Effectiveness of neural network types for prediction of business failure.

Expert Systems with Applications, 9(4), 503-512.

Brietzke, P. (2001). Securitization and bankruptcy in Indonesia: Theme and variations. Global Jurist Topics, 1(1), 5-

16.

Copyright by author(s); CC-BY 2077 The Clute Institute

Implications of the Research

Many companies all over the world enter financial distress for a variety of reasons including poor

management, dishonest management, economic recession, changes in globalization, and even war and terrorism.

Major bankruptcies such as Enron, WorldCom, and Waste Management have caused tens of thousands of employees

to lose their jobs, and a greater number of investors to lose their savings. Bankers and creditors lost billions of

dollars; communities lost vital services, and the economy of the country suffered. Much of these losses could have

been avoided with a suitable early warning system that identified weaknesses and allowed the constituents to make

adequate plans and take necessary steps.

Recommendations for Future Research

Because of the limited focus of this study, it would be helpful for future research to apply similar

bankruptcy prediction models to business firms not publicly traded on the Stock Market of Thailand.

Because of the high level of Type α errors in this study, future research should examine other bankruptcy

models to determine if a lower level of Type α errors can be realized.

Given the low incidence of research in the area of civil service and government enterprise areas, it is

suggested that these areas be examined in future research to identify better when these areas are in danger of failure.

AUTHOR INFORMATION

Dr. Judy Ramage Lawrence is Professor of Accounting at Christian Brothers University. She holds a BS from the

University of Memphis, an MS from the University of Arkansas, and a DBA from Nova Southeastern University.

She has over years’ experience in accounting in both local and Big Four accounting firms. Her research interest are

in the areas of fraud examination and international accounting. Dr. Lawrence has over 30 publications in refereed

journals

Dr. Surapol Pongsatat is a lecturer in the Advanced MBA program at Ramkhamhaeng University in Bangkok,

Thailand. Dr. Pongsatat is also an advisor in the DPA program at Phetchabun Rajabhat University in the Mueang

Phetchabun District, Phetchabun, Thailand. Dr. Pongsat’s current research interests are in the field of international

business and bankruptcy.

Dr. Howard Lawrence is Clinical Professor of Accounting at The University of Mississippi. He holds a BS in

Mechanical Engineering from Christian Brothers University, an MBA from the University of Memphis, and a PhD

from the University of Mississippi. Dr. Lawrence has over 20 years’ experience in the paper industry and the steel

industry. His research interest are in the area of international accounting and fraud examination.

REFERENCES

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Papers and

proceedings of the Twenty-Ninth Annual Meeting of the American Finance Association, Detroit, Michigan

December 28-30, The Journal of Finance, 23(4), 589-609.

Altman, E. I. (1993). Corporate Financial Distress and Bankruptcy: A Complete Guide to Predicting and Avoiding

Distress and Profiting from Bankruptcy, 2 nd Ed. New York: John Wiley and Sons.

Beaver, W. H. (1966a). Financial ratios as predictors of failure. Empirical Research in Accounting: Selected Studies,

71-111.

Beaver, W. H. (1966b). Market prices, financial ratios, and the prediction of failure. Journal of Accounting

Research, 6(2), 179-182.

Boritz, J. E, & Kennedy, D. B. (1995). Effectiveness of neural network types for prediction of business failure.

Expert Systems with Applications, 9(4), 503-512.

Brietzke, P. (2001). Securitization and bankruptcy in Indonesia: Theme and variations. Global Jurist Topics, 1(1), 5-

16.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Journal of Applied Business Research – November/December 2015 Volume 31, Number 6

Copyright by author(s); CC-BY 2078 The Clute Institute

Clark, C. & Jung, C. (2002). Implications of the Asian flu for developmental state theory: The cases of South Korea

and Taiwan. Asian Affairs, an American Review, 29(1), 16-44.

Cybinski, P. (2001). Description, explanation, prediction – the evolution of bankruptcy. Managerial Finance,

Patrington: 27(4), 29-46.

Dietrich, R., & Kaplan, R. (1982). Empirical analysis of the commercial loan classification decision. The Accounting

Review, 57(1), 18-38.

Dorak, M. T. (2002). Common concepts in statistics. Common Concepts in Statistics, Glasgow: 10(1), pp. 1-21.

Evans, R.T., Thanida, C., & Theo, C. (2013). Successful turnaround strategy, Thailand evidence. Journal of

Accounting in Emerging Economics. 3(2), 115-124.

Fitzpatrick, P. J. (1931). Symptoms of industrial failures. Catholic University of America Press.

Gentry, J. A., Newbold, P. & Whitford, D. T. (1985). Classifying bankrupt firms with funds flow components.

Journal of Accounting Research, Chicago: 23(1), 146-161.

Haley, U. C. V. (2000). Corporate Governance and restructuring in East Asia: An overview. Seoul Journal of

Economics, 13(3), 265-288.

Horrigan, J. O. (1968). A short history of financial ratio analysis. The Accounting Review, 43(2), 284-294.

Jones, F. L. (1987). Current techniques in bankruptcy prediction. Journal of Accounting Literature, 6(1), 131-164.

Khodadadi, V., Farazmand, H., & Sheybeh, S. (2013). Assessing the Valuation Model Based on Abnormal Earnings

(Ohlson) by Notice to the Macroeconomic Variables. Journal of Financial Accounting Research, 5(17), 3-

21.