Activity Based Costing Applications

VerifiedAdded on 2020/02/18

|22

|4750

|36

AI Summary

This assignment explores the concept and application of Activity Based Costing (ABC). It examines how ABC is used in diverse sectors like healthcare and hospitality to accurately allocate costs and improve decision-making. The assignment also discusses the advantages and potential drawbacks of implementing ABC systems within organizations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting practice 1

Name of the student

Title topic-Management accounting practice

University name-

Name of the student

Title topic-Management accounting practice

University name-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management accounting practice 2

Table of Contents

Task 1..........................................................................................................................................................3

INTRODUCTION...................................................................................................................................3

LITERATURE REVIEW:.......................................................................................................................3

Changes in the focus of management accounting practices.....................................................................3

Management Accountant’s role in the contemporary business world..................................................4

Customer’s value and Shareholder’s wealth........................................................................................7

Contemporary techniques of resource management.............................................................................9

Task 2........................................................................................................................................................12

Cost allocation Methods........................................................................................................................12

Report....................................................................................................................................................13

Background.......................................................................................................................................13

Practical analysis of the problem.......................................................................................................13

Implications.......................................................................................................................................15

Conclusion.................................................................................................................................................16

Appendices........................................................................................................................................17

References.................................................................................................................................................21

Table of Contents

Task 1..........................................................................................................................................................3

INTRODUCTION...................................................................................................................................3

LITERATURE REVIEW:.......................................................................................................................3

Changes in the focus of management accounting practices.....................................................................3

Management Accountant’s role in the contemporary business world..................................................4

Customer’s value and Shareholder’s wealth........................................................................................7

Contemporary techniques of resource management.............................................................................9

Task 2........................................................................................................................................................12

Cost allocation Methods........................................................................................................................12

Report....................................................................................................................................................13

Background.......................................................................................................................................13

Practical analysis of the problem.......................................................................................................13

Implications.......................................................................................................................................15

Conclusion.................................................................................................................................................16

Appendices........................................................................................................................................17

References.................................................................................................................................................21

Management accounting practice 3

Task 1

INTRODUCTION

This report reflects the key understanding on the accounting practices and particular

changes arise after implementation of newly adopted accounting practices and rules. In this

report, key area of management accounting is related to the management accounting practice and

benefits arise from the newly introduced accounting practice on the business organizations. With

the increasing ramification of economic changes, management accounting practice has been

changing throughout the time and it is becoming cumbersome process for accountant to comply

with implemented rules and regulations in determined approach. In this report, various newly

introduced accounting rules and adopted management process system have been taken into

consideration. It is considered that management department has to ensure all the changes in

accounting rules and regulation with a view to adopt new process system and process

management in determined approach. These accountants have to evaluate whether company is

complying with all the rules and applicable standard while running its business effectively in

organization (Muckstadt & Sapra, 2010).

LITERATURE REVIEW:

Changes in the focus of management accounting practices

As per the perception of Muckstadt & Sapra, (2010) it is reflected that with the increasing

ramification of economic changes, management accounting practice has been changing and it is

becoming cumbersome process for accountant to comply with implemented rules and regulations

in determined approach. These changing factors are imposing the requirement on business to

change their ways of operating a management of business. There are several big organizations

such as G.E. capital, Wesfarmers, Woolworth and Morrison plc. That has adopted changed

management accounting practice in their accounting and reporting frameworks. These changed

Task 1

INTRODUCTION

This report reflects the key understanding on the accounting practices and particular

changes arise after implementation of newly adopted accounting practices and rules. In this

report, key area of management accounting is related to the management accounting practice and

benefits arise from the newly introduced accounting practice on the business organizations. With

the increasing ramification of economic changes, management accounting practice has been

changing throughout the time and it is becoming cumbersome process for accountant to comply

with implemented rules and regulations in determined approach. In this report, various newly

introduced accounting rules and adopted management process system have been taken into

consideration. It is considered that management department has to ensure all the changes in

accounting rules and regulation with a view to adopt new process system and process

management in determined approach. These accountants have to evaluate whether company is

complying with all the rules and applicable standard while running its business effectively in

organization (Muckstadt & Sapra, 2010).

LITERATURE REVIEW:

Changes in the focus of management accounting practices

As per the perception of Muckstadt & Sapra, (2010) it is reflected that with the increasing

ramification of economic changes, management accounting practice has been changing and it is

becoming cumbersome process for accountant to comply with implemented rules and regulations

in determined approach. These changing factors are imposing the requirement on business to

change their ways of operating a management of business. There are several big organizations

such as G.E. capital, Wesfarmers, Woolworth and Morrison plc. That has adopted changed

management accounting practice in their accounting and reporting frameworks. These changed

Management accounting practice 4

have been adopted with a view to strengthen the accounting and reporting frameworks of

organization and increasing transparency of business functioning to their shareholders.

As per the perception of Christ, & Burritt (2013) it is reflected that there are several management

accounting techniques which have been adopted by organizations such as cost management

technique, ABC accounting technique, LIFO, FIFO methods, overhead absorption and

apportions accounting technique and costing technique. However, accountants have become

aware about these accounting techniques to manage their accounting practice in determined

approach. Nonetheless, Multinational organizations set up different big rules and regulations for

the management accounting practices with a view to strengthen the accounting and reporting

frameworks and increasing transparency of business functioning to their shareholders. Ideally,

when companies adopt different management accounting practice, then they have to evaluate

various factors such as life cycle of business, size of business, regulatory requirements,

modernisations of techniques and inventory management techniques.

Management Accountant’s role in the contemporary business world

As stated by Needle, (2010) it is reflected that with the changes in economic factors and

business conditions, accountant has various responsibilities of management accountant and other

executives of management. Management accountant has covered not only accounting task to

manage the business transactions but also play important role in playing financial tasks in

determined approach. However, there are several reporting and analysis work which are played

by accountant in an organization.

Reporting and analysis work:

As per the views of Hada, Chakravarty & Mukherjee, (2014) it is divulged that Reporting of

financial statement to stakeholders is an important functioning of organizations. The

have been adopted with a view to strengthen the accounting and reporting frameworks of

organization and increasing transparency of business functioning to their shareholders.

As per the perception of Christ, & Burritt (2013) it is reflected that there are several management

accounting techniques which have been adopted by organizations such as cost management

technique, ABC accounting technique, LIFO, FIFO methods, overhead absorption and

apportions accounting technique and costing technique. However, accountants have become

aware about these accounting techniques to manage their accounting practice in determined

approach. Nonetheless, Multinational organizations set up different big rules and regulations for

the management accounting practices with a view to strengthen the accounting and reporting

frameworks and increasing transparency of business functioning to their shareholders. Ideally,

when companies adopt different management accounting practice, then they have to evaluate

various factors such as life cycle of business, size of business, regulatory requirements,

modernisations of techniques and inventory management techniques.

Management Accountant’s role in the contemporary business world

As stated by Needle, (2010) it is reflected that with the changes in economic factors and

business conditions, accountant has various responsibilities of management accountant and other

executives of management. Management accountant has covered not only accounting task to

manage the business transactions but also play important role in playing financial tasks in

determined approach. However, there are several reporting and analysis work which are played

by accountant in an organization.

Reporting and analysis work:

As per the views of Hada, Chakravarty & Mukherjee, (2014) it is divulged that Reporting of

financial statement to stakeholders is an important functioning of organizations. The

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management accounting practice 5

management accountant is responsible for preparation the management accountant is responsible

for preparation of reports on the functioning of various operations and to identify the root causes

of any deficiency in the operations. Also the accountant is required to apply the analytical skills

to the data of the company to compare the actual results with the benchmarks and to report the

deviations, if any with the suitable recommendations.

Formulation of Strategies: The management accountants are responsible to formulate the

strategies for the management and the effective implementation of the same so as to achieve the

targets and the goals effectively.

Decision Making: The decision making function is the most crucial function in any organization

as it require good amount of information to take important decisions for the company. The

management accountant provides material and necessary to the top level management.

Interpretation of Information: Management accountant helps in the interpretation of financial

information provided to the management so that it becomes easy for the managers to understand

the operating results.

Advisor: Cost management is supposed to provide the best advice relation to various crucial

matters on which management has to take firm decisions. The accountant is required to provide

the advice which is best suitable to the company so as to improve the overall performance of the

different functions of the company.

Change Manager: As organization has to adapt to the changes that are rapidly occurring in the

environment in which it is operating, the management accountant will help the firm to cope up

with the changes by identifying and assessing the need and implications of changes through

provision of updated information (Christ, & Burritt 2013)

management accountant is responsible for preparation the management accountant is responsible

for preparation of reports on the functioning of various operations and to identify the root causes

of any deficiency in the operations. Also the accountant is required to apply the analytical skills

to the data of the company to compare the actual results with the benchmarks and to report the

deviations, if any with the suitable recommendations.

Formulation of Strategies: The management accountants are responsible to formulate the

strategies for the management and the effective implementation of the same so as to achieve the

targets and the goals effectively.

Decision Making: The decision making function is the most crucial function in any organization

as it require good amount of information to take important decisions for the company. The

management accountant provides material and necessary to the top level management.

Interpretation of Information: Management accountant helps in the interpretation of financial

information provided to the management so that it becomes easy for the managers to understand

the operating results.

Advisor: Cost management is supposed to provide the best advice relation to various crucial

matters on which management has to take firm decisions. The accountant is required to provide

the advice which is best suitable to the company so as to improve the overall performance of the

different functions of the company.

Change Manager: As organization has to adapt to the changes that are rapidly occurring in the

environment in which it is operating, the management accountant will help the firm to cope up

with the changes by identifying and assessing the need and implications of changes through

provision of updated information (Christ, & Burritt 2013)

Management accounting practice 6

Performance measurement: The management accountant helps the organization in measuring the

performance of overall organization as well as the performance of individuals of the

management such as employees and the managers.

Performance measurement: The management accountant helps the organization in measuring the

performance of overall organization as well as the performance of individuals of the

management such as employees and the managers.

Management accounting practice 7

Customer’s value and Shareholder’s wealth

As per the views of Iyer, et al. (2015) it is divulged that creation of customer’s value is

very important business functioning of organization. It is considered that if amount paid by

customer to buy goods and services from the market is high as compared to the satisfaction they

get from the market then customer’s value would be high. It is further observed that in case if

customers get high satisfaction from the purchased goods and services then in this customer’s

value would be high. It is observed that accountant management could increase the overall client

satisfaction if they implement proper management accounting system to record financial and

non-financial transactions in determined approach. There are several companies such as G.E.

capital, Wesfarmers, Woolworth and Morrison plc. who have created core competency in

creation of customer’s value and shareholders wealth. These companies have developed

organization culture by implementing proper level of policies and frameworks and delivering

best level of services to clients. Customers in the market could evaluate the brand image and

value chain activities of organization by understanding financial statements in determined

approach. Application of different level of accounting practice and developed accounting plans

has helped G.E. capital, Wesfarmers, Woolworth and Morrison plc. to creation customer’s value

in the market. This has not only increased overall clients buying habits but also enhance the

brand image of company in market. This creation of customer’s value is key pillar for the

success of organization and it could be created by increasing the overall quality of client and

production efficiency in determined approach (Iyer, et al. 2015).

Shareholder’s wealth

Shareholders are the key persons of company who make investment and provide capital

to run the business. With the help of effective accounting management practice, company could

Customer’s value and Shareholder’s wealth

As per the views of Iyer, et al. (2015) it is divulged that creation of customer’s value is

very important business functioning of organization. It is considered that if amount paid by

customer to buy goods and services from the market is high as compared to the satisfaction they

get from the market then customer’s value would be high. It is further observed that in case if

customers get high satisfaction from the purchased goods and services then in this customer’s

value would be high. It is observed that accountant management could increase the overall client

satisfaction if they implement proper management accounting system to record financial and

non-financial transactions in determined approach. There are several companies such as G.E.

capital, Wesfarmers, Woolworth and Morrison plc. who have created core competency in

creation of customer’s value and shareholders wealth. These companies have developed

organization culture by implementing proper level of policies and frameworks and delivering

best level of services to clients. Customers in the market could evaluate the brand image and

value chain activities of organization by understanding financial statements in determined

approach. Application of different level of accounting practice and developed accounting plans

has helped G.E. capital, Wesfarmers, Woolworth and Morrison plc. to creation customer’s value

in the market. This has not only increased overall clients buying habits but also enhance the

brand image of company in market. This creation of customer’s value is key pillar for the

success of organization and it could be created by increasing the overall quality of client and

production efficiency in determined approach (Iyer, et al. 2015).

Shareholder’s wealth

Shareholders are the key persons of company who make investment and provide capital

to run the business. With the help of effective accounting management practice, company could

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting practice 8

increase the overall transparency of business and showcase the real earning to its stakeholders. It

is further observed that if company increase the earning per share then it will eventually increase

the overall shareholder’s health. Companies like G.E. capital, Wesfarmers, Woolworth and

Morrison plc. have been offering high amount of earning per share to its shareholders. Morrison

plc. offered 1.23 points average EPS to its shareholders since last five years data. On the other

hand, Woolworth and Wesfarmers shared approximately 1.92 points average EPS to its shares.

Company could increase the shareholders health by offering dividend, bonus shares and other

retained earnings for the betterment of shareholders earning. However, various companies such

as BP Billiton and Rio Tinto instead of offering dividend to its shareholders plug back all the

profit earned in the business functioning of organization. This process will not only increase the

overall value capital of the organizations but also provide high level of value creation to

shareholders who invested their money in organization. It is observed that if company must focus

on maximization of company’s performance and increasing the overall value of capital. If

companies fail to create value of investment then it will decrease the value of company in

shareholders’ mind. However, each and every companies issues dividend, shareholders rights

issues and other right to its shareholders with a view to establish proper level of nexus between

company’s welfare and shareholders wealth in effective manner. This shareholders wealth could

be increased if company have proper level of harmonization in plugging back of profit and

distributing overall earning to its shareholders (Iyer, et al. 2015).

As stated by Muckstadt & Sapra, 2010 it is reflected that after evaluating these two issues

given above, it could be inferred that if organizations are making proper level of efforts then

these two issues could be mitigated in determined approach. It is evaluated that company needs

to identify the best possible efforts method such as issues of stock options, issues of right shares,

increase the overall transparency of business and showcase the real earning to its stakeholders. It

is further observed that if company increase the earning per share then it will eventually increase

the overall shareholder’s health. Companies like G.E. capital, Wesfarmers, Woolworth and

Morrison plc. have been offering high amount of earning per share to its shareholders. Morrison

plc. offered 1.23 points average EPS to its shareholders since last five years data. On the other

hand, Woolworth and Wesfarmers shared approximately 1.92 points average EPS to its shares.

Company could increase the shareholders health by offering dividend, bonus shares and other

retained earnings for the betterment of shareholders earning. However, various companies such

as BP Billiton and Rio Tinto instead of offering dividend to its shareholders plug back all the

profit earned in the business functioning of organization. This process will not only increase the

overall value capital of the organizations but also provide high level of value creation to

shareholders who invested their money in organization. It is observed that if company must focus

on maximization of company’s performance and increasing the overall value of capital. If

companies fail to create value of investment then it will decrease the value of company in

shareholders’ mind. However, each and every companies issues dividend, shareholders rights

issues and other right to its shareholders with a view to establish proper level of nexus between

company’s welfare and shareholders wealth in effective manner. This shareholders wealth could

be increased if company have proper level of harmonization in plugging back of profit and

distributing overall earning to its shareholders (Iyer, et al. 2015).

As stated by Muckstadt & Sapra, 2010 it is reflected that after evaluating these two issues

given above, it could be inferred that if organizations are making proper level of efforts then

these two issues could be mitigated in determined approach. It is evaluated that company needs

to identify the best possible efforts method such as issues of stock options, issues of right shares,

Management accounting practice 9

dividend and other benefits to shareholders to increase the overall shareholders wealth. It is

considered that shareholder’s wealth is completely dependent upon two factors such as

distributions of company’s benefits to shareholders and increase in the invested capital of

company. Another issue is related to providing customer’s satisfaction to clients in the market. If

company re-engineering its value chain activities to increase the effectiveness of overall

efficiency of business then it will also increase the client satisfaction and brand image of

company in the market.

Contemporary techniques of resource management:

It is observed that if company manages its resources such as financial, operating and

other resources in effective manner then it will result to following benefits to organization such

as creation of synergy in market, development of core competency and offering high level of

quality and management of business (Muckstadt & Sapra, 2010).

Resources management is the system of management of resources of company in easy

and determined approach with a view to create value of investment and efficiency of business.

With the help of this resources management of business, company could reduce the wastage and

by products of business. However, there are several techniques and methods which are very

crucial for the management of business resources in company such as ABC costing technique,

cost management method and absorption and appropriation of expenses in different department

and determining the economic batch quantity by establishment of Economic order quantity of

business. However, management of resources is done by using LIFO and FIFO method in

inventory management technique (Hansen, 2011). It is considered that LIFO, FIFO and setting

economic order of quantity is the most common method which company could use with a view

to reduce the wastage and overburden of inventories in warehouse of the business. There are

dividend and other benefits to shareholders to increase the overall shareholders wealth. It is

considered that shareholder’s wealth is completely dependent upon two factors such as

distributions of company’s benefits to shareholders and increase in the invested capital of

company. Another issue is related to providing customer’s satisfaction to clients in the market. If

company re-engineering its value chain activities to increase the effectiveness of overall

efficiency of business then it will also increase the client satisfaction and brand image of

company in the market.

Contemporary techniques of resource management:

It is observed that if company manages its resources such as financial, operating and

other resources in effective manner then it will result to following benefits to organization such

as creation of synergy in market, development of core competency and offering high level of

quality and management of business (Muckstadt & Sapra, 2010).

Resources management is the system of management of resources of company in easy

and determined approach with a view to create value of investment and efficiency of business.

With the help of this resources management of business, company could reduce the wastage and

by products of business. However, there are several techniques and methods which are very

crucial for the management of business resources in company such as ABC costing technique,

cost management method and absorption and appropriation of expenses in different department

and determining the economic batch quantity by establishment of Economic order quantity of

business. However, management of resources is done by using LIFO and FIFO method in

inventory management technique (Hansen, 2011). It is considered that LIFO, FIFO and setting

economic order of quantity is the most common method which company could use with a view

to reduce the wastage and overburden of inventories in warehouse of the business. There are

Management accounting practice 10

several companies such as G.E. capital, Wesfarmers, Woolworth and Morrison plc. who have

been using inventory management business technique to maintain proper level of inventory in

warehouse.

Target costing: This is the technique which is used to determine the margin company needs to

earn after selling products and services. This target costing also helps company to reduce the

complexity of business and reduce the byproducts (Baker & English, 2011).

Activity Based Budgeting- This is the budgeting process which helps organization to prepare

budgeting process to analysis the cost attributable for the different department of organization.

This Activity based budgeting assists company to evaluate the revenue and other associated cost

of particular department and organizations in determined approach. This Activity based

budgeting will help company to evaluate the historical budget information and prepare an

effective inventory management plan. This will not only help in reducing overall cost of

particular process system but will organization to create core competency in the production of

organization This Activity based budgeting provide effective control on the management of

expenses and inventory management of business. Nonetheless, this is very costly process and

may result to increment in overall production cost for the particular time period (Lambert &

Pezet, 2011).

Total quality management: This technique is developed with a view to increase the total quality

of offered goods and service for the better satisfaction of clients. This TQM assists in increasing

the overall efficiency of business and customized overall goods and services in determined

approach. This TQM method is used by organization to set up particular standards and quality

benchmark to increase the overall efficiency of business.

several companies such as G.E. capital, Wesfarmers, Woolworth and Morrison plc. who have

been using inventory management business technique to maintain proper level of inventory in

warehouse.

Target costing: This is the technique which is used to determine the margin company needs to

earn after selling products and services. This target costing also helps company to reduce the

complexity of business and reduce the byproducts (Baker & English, 2011).

Activity Based Budgeting- This is the budgeting process which helps organization to prepare

budgeting process to analysis the cost attributable for the different department of organization.

This Activity based budgeting assists company to evaluate the revenue and other associated cost

of particular department and organizations in determined approach. This Activity based

budgeting will help company to evaluate the historical budget information and prepare an

effective inventory management plan. This will not only help in reducing overall cost of

particular process system but will organization to create core competency in the production of

organization This Activity based budgeting provide effective control on the management of

expenses and inventory management of business. Nonetheless, this is very costly process and

may result to increment in overall production cost for the particular time period (Lambert &

Pezet, 2011).

Total quality management: This technique is developed with a view to increase the total quality

of offered goods and service for the better satisfaction of clients. This TQM assists in increasing

the overall efficiency of business and customized overall goods and services in determined

approach. This TQM method is used by organization to set up particular standards and quality

benchmark to increase the overall efficiency of business.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management accounting practice 11

Resource levelling: This technique is developed with a view to increase the overall efficiency of

company to increase the satisfaction of clients managed in order to handle the constraint

effectively.

Six sigma: This is the set standard which is used by company for the quality check or proof

reading of work. This Six sigma process is highly used by GE capital to evaluate its value chain

activities (Hirst, Thompson & Bromley, 2015).

Logistic management: This process is used to manage the flow of goods and services from one

place to another place. This logistic management implement efficient business functioning and

decrease the complexity of value chain activities.

Resource levelling: This technique is developed with a view to increase the overall efficiency of

company to increase the satisfaction of clients managed in order to handle the constraint

effectively.

Six sigma: This is the set standard which is used by company for the quality check or proof

reading of work. This Six sigma process is highly used by GE capital to evaluate its value chain

activities (Hirst, Thompson & Bromley, 2015).

Logistic management: This process is used to manage the flow of goods and services from one

place to another place. This logistic management implement efficient business functioning and

decrease the complexity of value chain activities.

Management accounting practice 12

Task 2

Cost allocation Methods:

Allocation of cost is different department is very necessary task for determining the cost

of productions and units produced. However, there are several methods such as ABC costing,

traditional costing and other methods to make bifurcation of cost in different department in

determine approach (Dunning, 2014).

Direct Method: This method is most common method in which all the cost is directly bifurcated

into different department of organization.

Step down Method: In this method all the associated department and functions share the

expenses and overhead cost in different particular department.

Reciprocal Method: With the help of this method, proper allocation of expenses in different

department is based on the recognition of corresponding services to the service departments.

However, this method is complicate and result to high level of complexity to determine the

reciprocal allocation of indirect expenses in concerned department (Needle, 2010).

However, it is evaluated that direct cost is allocated directly to the concerned department

but allocation of indirect cost is based on the different cost drivers such as variable cost, number

of hours and labour machinery working (Boxall & Purcell, 2011).

The cost is allocated by using cost actual labour or machinery working in the business process of

organization.

Note- Allocation of same cost could be done on the basis of Machinery hours and working rate.

Task 2

Cost allocation Methods:

Allocation of cost is different department is very necessary task for determining the cost

of productions and units produced. However, there are several methods such as ABC costing,

traditional costing and other methods to make bifurcation of cost in different department in

determine approach (Dunning, 2014).

Direct Method: This method is most common method in which all the cost is directly bifurcated

into different department of organization.

Step down Method: In this method all the associated department and functions share the

expenses and overhead cost in different particular department.

Reciprocal Method: With the help of this method, proper allocation of expenses in different

department is based on the recognition of corresponding services to the service departments.

However, this method is complicate and result to high level of complexity to determine the

reciprocal allocation of indirect expenses in concerned department (Needle, 2010).

However, it is evaluated that direct cost is allocated directly to the concerned department

but allocation of indirect cost is based on the different cost drivers such as variable cost, number

of hours and labour machinery working (Boxall & Purcell, 2011).

The cost is allocated by using cost actual labour or machinery working in the business process of

organization.

Note- Allocation of same cost could be done on the basis of Machinery hours and working rate.

Management accounting practice 13

Report

To

The Managing Director

Teletrix ltd.

Date: 13th September 2017

Sir,

This report reflects the details study on the ABC costing and traditional costing method that

could be used by company.

Background

Namazi, M. (2016). Time-driven activity-based costing: Theory, applications and

limitations. Iranian Journal of Management Studies, 9(3), 457.

Sigüenza Guzmán, L., Van den Abbeele, A., & Cattrysse, D. (2014). Time-driven activity-based

costing systems for cataloguing processes: a case study.

With the increasing ramification of economic changes and increasing

complexity of business, costing technique is used to determine the overall

cost of production of organization. Overheads are the additional amount of

charges which are incurred by organization and bifurcation of same is done

by using two costing technique Traditional costing and activity based

costing. Traditional costing is the costing technique in which overhead cost

and direct labour rate is sued to undertaken to determine the overall cost

(Hada, Chakravarty & Mukherjee, 2014).

However ABC costing is the modern technique in which allocation of

overhead and expense in different department is made on the basis of several

factors such as nature of business, incurred expenses and accounting

Report

To

The Managing Director

Teletrix ltd.

Date: 13th September 2017

Sir,

This report reflects the details study on the ABC costing and traditional costing method that

could be used by company.

Background

Namazi, M. (2016). Time-driven activity-based costing: Theory, applications and

limitations. Iranian Journal of Management Studies, 9(3), 457.

Sigüenza Guzmán, L., Van den Abbeele, A., & Cattrysse, D. (2014). Time-driven activity-based

costing systems for cataloguing processes: a case study.

With the increasing ramification of economic changes and increasing

complexity of business, costing technique is used to determine the overall

cost of production of organization. Overheads are the additional amount of

charges which are incurred by organization and bifurcation of same is done

by using two costing technique Traditional costing and activity based

costing. Traditional costing is the costing technique in which overhead cost

and direct labour rate is sued to undertaken to determine the overall cost

(Hada, Chakravarty & Mukherjee, 2014).

However ABC costing is the modern technique in which allocation of

overhead and expense in different department is made on the basis of several

factors such as nature of business, incurred expenses and accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting practice 14

management practice of organization (Bayati, et al. 2015).

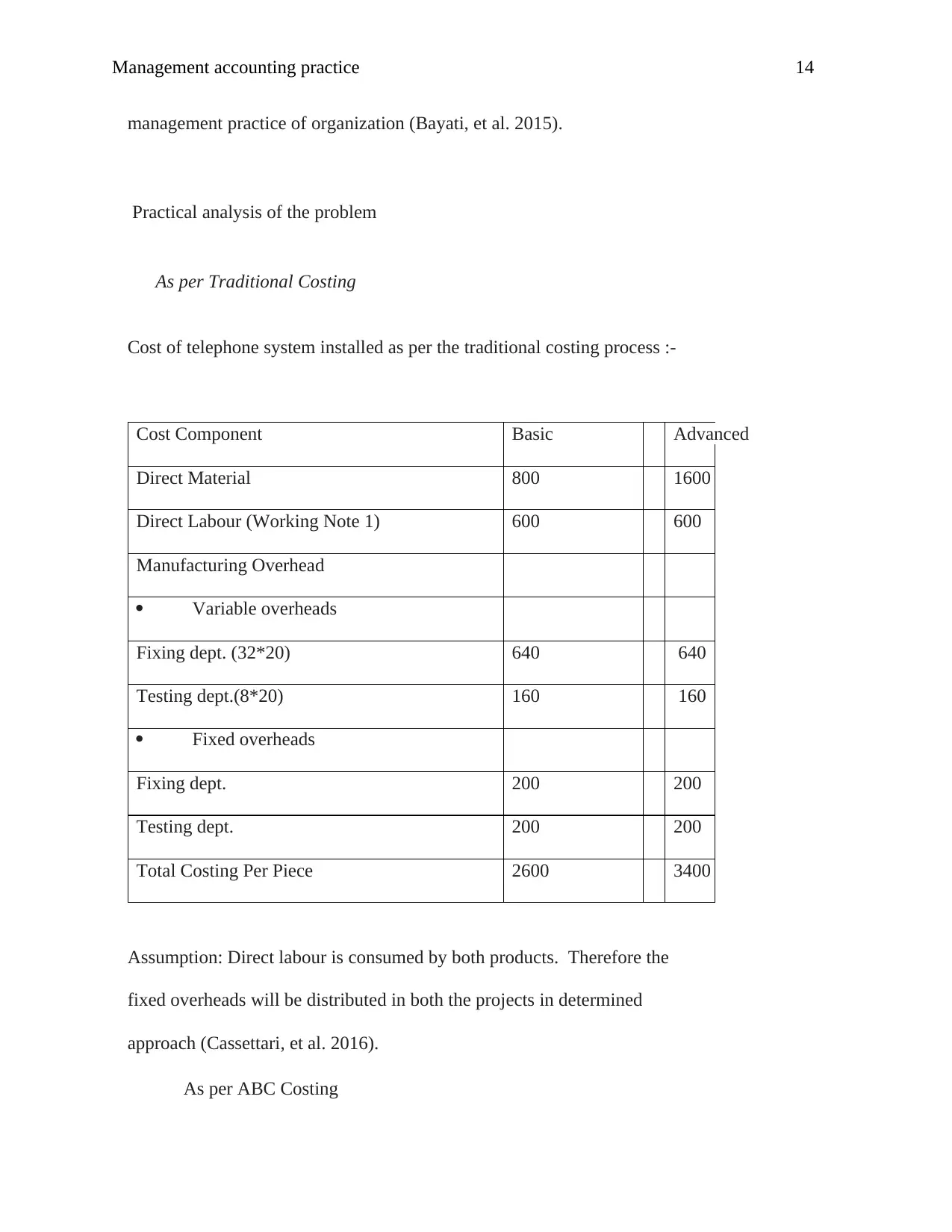

Practical analysis of the problem

As per Traditional Costing

Cost of telephone system installed as per the traditional costing process :-

Cost Component Basic Advanced

Direct Material 800 1600

Direct Labour (Working Note 1) 600 600

Manufacturing Overhead

Variable overheads

Fixing dept. (32*20) 640 640

Testing dept.(8*20) 160 160

Fixed overheads

Fixing dept. 200 200

Testing dept. 200 200

Total Costing Per Piece 2600 3400

Assumption: Direct labour is consumed by both products. Therefore the

fixed overheads will be distributed in both the projects in determined

approach (Cassettari, et al. 2016).

As per ABC Costing

management practice of organization (Bayati, et al. 2015).

Practical analysis of the problem

As per Traditional Costing

Cost of telephone system installed as per the traditional costing process :-

Cost Component Basic Advanced

Direct Material 800 1600

Direct Labour (Working Note 1) 600 600

Manufacturing Overhead

Variable overheads

Fixing dept. (32*20) 640 640

Testing dept.(8*20) 160 160

Fixed overheads

Fixing dept. 200 200

Testing dept. 200 200

Total Costing Per Piece 2600 3400

Assumption: Direct labour is consumed by both products. Therefore the

fixed overheads will be distributed in both the projects in determined

approach (Cassettari, et al. 2016).

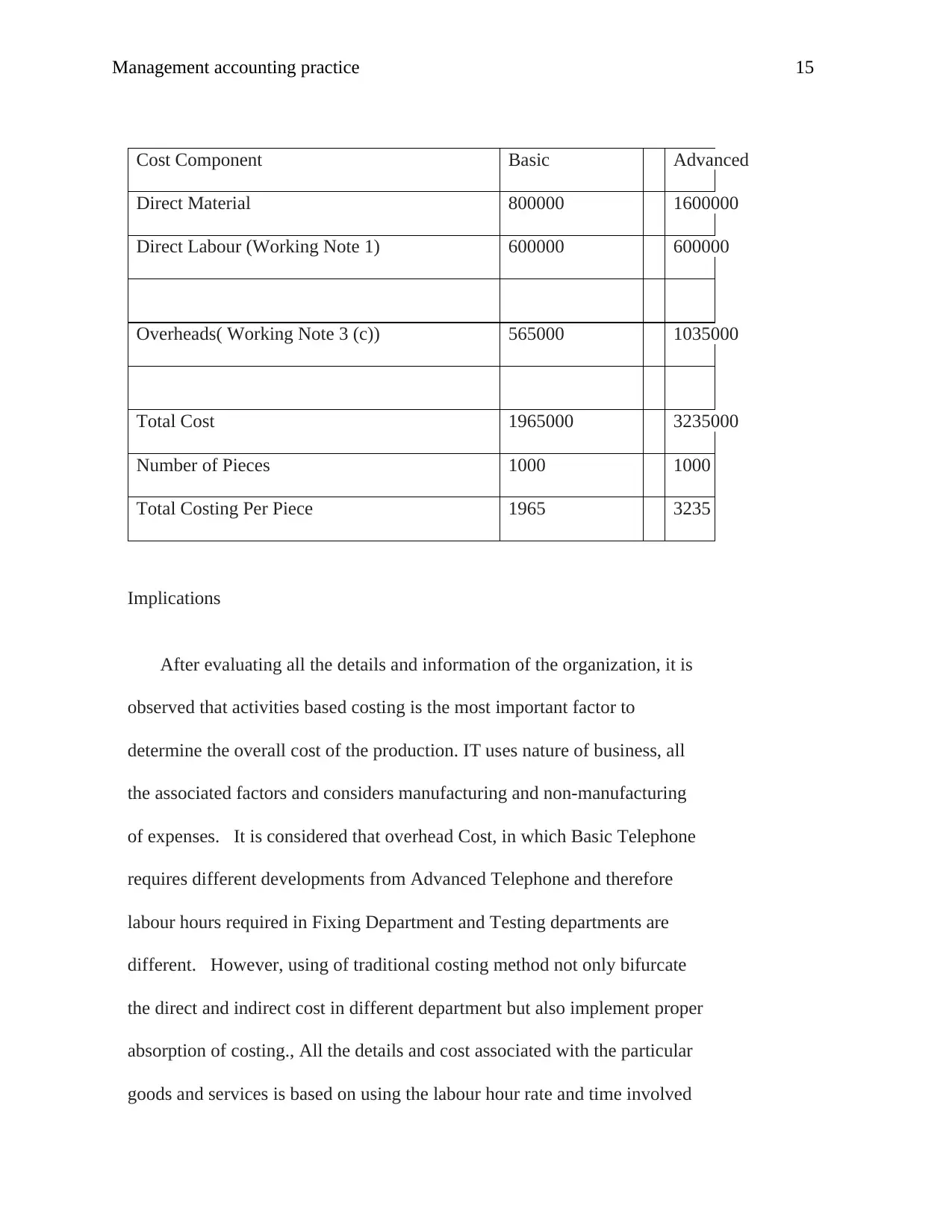

As per ABC Costing

Management accounting practice 15

Cost Component Basic Advanced

Direct Material 800000 1600000

Direct Labour (Working Note 1) 600000 600000

Overheads( Working Note 3 (c)) 565000 1035000

Total Cost 1965000 3235000

Number of Pieces 1000 1000

Total Costing Per Piece 1965 3235

Implications

After evaluating all the details and information of the organization, it is

observed that activities based costing is the most important factor to

determine the overall cost of the production. IT uses nature of business, all

the associated factors and considers manufacturing and non-manufacturing

of expenses. It is considered that overhead Cost, in which Basic Telephone

requires different developments from Advanced Telephone and therefore

labour hours required in Fixing Department and Testing departments are

different. However, using of traditional costing method not only bifurcate

the direct and indirect cost in different department but also implement proper

absorption of costing., All the details and cost associated with the particular

goods and services is based on using the labour hour rate and time involved

Cost Component Basic Advanced

Direct Material 800000 1600000

Direct Labour (Working Note 1) 600000 600000

Overheads( Working Note 3 (c)) 565000 1035000

Total Cost 1965000 3235000

Number of Pieces 1000 1000

Total Costing Per Piece 1965 3235

Implications

After evaluating all the details and information of the organization, it is

observed that activities based costing is the most important factor to

determine the overall cost of the production. IT uses nature of business, all

the associated factors and considers manufacturing and non-manufacturing

of expenses. It is considered that overhead Cost, in which Basic Telephone

requires different developments from Advanced Telephone and therefore

labour hours required in Fixing Department and Testing departments are

different. However, using of traditional costing method not only bifurcate

the direct and indirect cost in different department but also implement proper

absorption of costing., All the details and cost associated with the particular

goods and services is based on using the labour hour rate and time involved

Management accounting practice 16

in production process of organization. Nonetheless, the main common

problem in this traditional method is arising related to accuracy and evaluates

the associated problems in determined approach. Teletrix will have problem

to determine the overhead expenses in different department. It is observed

that setting overhead expense and hourly cost is hard to determine in case of

less availability of information (Cugueró-Escofet & Fito, 2016).

These both costing technique such as ABC costing and traditional costing

technique have different costing methods and implementation of these

costing methods is based on the nature and associated factors of business

(Aminian, et al. 2016).

Activity-based costing is the most common technique which should be used

by organizations to determine the accuracy and proper values of incurred

expense in different organization functioning in determined approach. ABC

costing is mostly affected by nature of business, associated factors and

determining value proposition in effective manner (Abdullah, Jadhav &

Borhade, 2014).

It is determined that by using ABC costing, proper level of

bifurcation could be made in particular department of organization and

determining the overall direct and indirect cost of the organization.

By using this method, calculation of cost associated with the

particular department are evaluated that proper business functioning is done

by bifurcating relevant and irrelevant cost of production (Ebrahimian, Taheri

in production process of organization. Nonetheless, the main common

problem in this traditional method is arising related to accuracy and evaluates

the associated problems in determined approach. Teletrix will have problem

to determine the overhead expenses in different department. It is observed

that setting overhead expense and hourly cost is hard to determine in case of

less availability of information (Cugueró-Escofet & Fito, 2016).

These both costing technique such as ABC costing and traditional costing

technique have different costing methods and implementation of these

costing methods is based on the nature and associated factors of business

(Aminian, et al. 2016).

Activity-based costing is the most common technique which should be used

by organizations to determine the accuracy and proper values of incurred

expense in different organization functioning in determined approach. ABC

costing is mostly affected by nature of business, associated factors and

determining value proposition in effective manner (Abdullah, Jadhav &

Borhade, 2014).

It is determined that by using ABC costing, proper level of

bifurcation could be made in particular department of organization and

determining the overall direct and indirect cost of the organization.

By using this method, calculation of cost associated with the

particular department are evaluated that proper business functioning is done

by bifurcating relevant and irrelevant cost of production (Ebrahimian, Taheri

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management accounting practice 17

& Yousefi, 2015).

Traditional costing method accompanied with the allocation of direct and

indirect cost is the most common costing method which is mostly used by

traditional companies. In this method, evaluation of cost of production is

based on the bifurcation of direct and indirect cost (Mashayekhi & Ara,

2017).

Direct cost is the major part of the cost of the products. With the help

of traditional costing method, company could easily make bifurcation in the

overall cost of production and production level with a view to identify level

of costing in separate department of organization. It also helps in

appropriation of cost in different department (Raab & Zemke, 2016).

Conclusion

In this report, there is various costing technique such as ABC, revenue

management and other pricing techniques have been used to manage the

costing and pricing technique of Teletrix company (Sigüenza Guzmán, Van

den Abbeele & Cattrysse, 2014). These technique helps Teletrix company to

reduce the overall cost and increase the business efficiency in determined

approach. It is considered that if companies could use these techniques then

it will increase the overall efficiency of business (Namazi, 2016).

& Yousefi, 2015).

Traditional costing method accompanied with the allocation of direct and

indirect cost is the most common costing method which is mostly used by

traditional companies. In this method, evaluation of cost of production is

based on the bifurcation of direct and indirect cost (Mashayekhi & Ara,

2017).

Direct cost is the major part of the cost of the products. With the help

of traditional costing method, company could easily make bifurcation in the

overall cost of production and production level with a view to identify level

of costing in separate department of organization. It also helps in

appropriation of cost in different department (Raab & Zemke, 2016).

Conclusion

In this report, there is various costing technique such as ABC, revenue

management and other pricing techniques have been used to manage the

costing and pricing technique of Teletrix company (Sigüenza Guzmán, Van

den Abbeele & Cattrysse, 2014). These technique helps Teletrix company to

reduce the overall cost and increase the business efficiency in determined

approach. It is considered that if companies could use these techniques then

it will increase the overall efficiency of business (Namazi, 2016).

Management accounting practice 18

Appendices

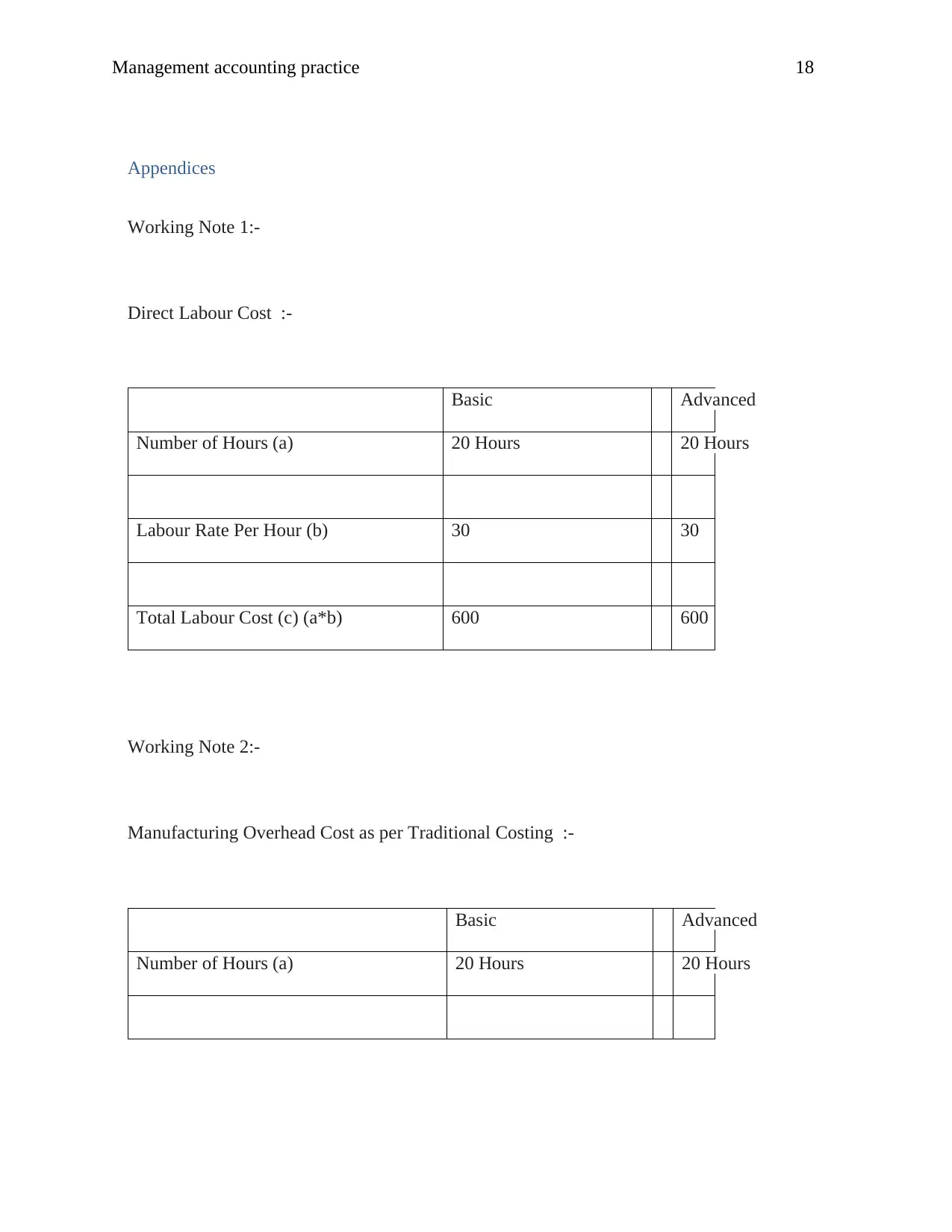

Working Note 1:-

Direct Labour Cost :-

Basic Advanced

Number of Hours (a) 20 Hours 20 Hours

Labour Rate Per Hour (b) 30 30

Total Labour Cost (c) (a*b) 600 600

Working Note 2:-

Manufacturing Overhead Cost as per Traditional Costing :-

Basic Advanced

Number of Hours (a) 20 Hours 20 Hours

Appendices

Working Note 1:-

Direct Labour Cost :-

Basic Advanced

Number of Hours (a) 20 Hours 20 Hours

Labour Rate Per Hour (b) 30 30

Total Labour Cost (c) (a*b) 600 600

Working Note 2:-

Manufacturing Overhead Cost as per Traditional Costing :-

Basic Advanced

Number of Hours (a) 20 Hours 20 Hours

Management accounting practice 19

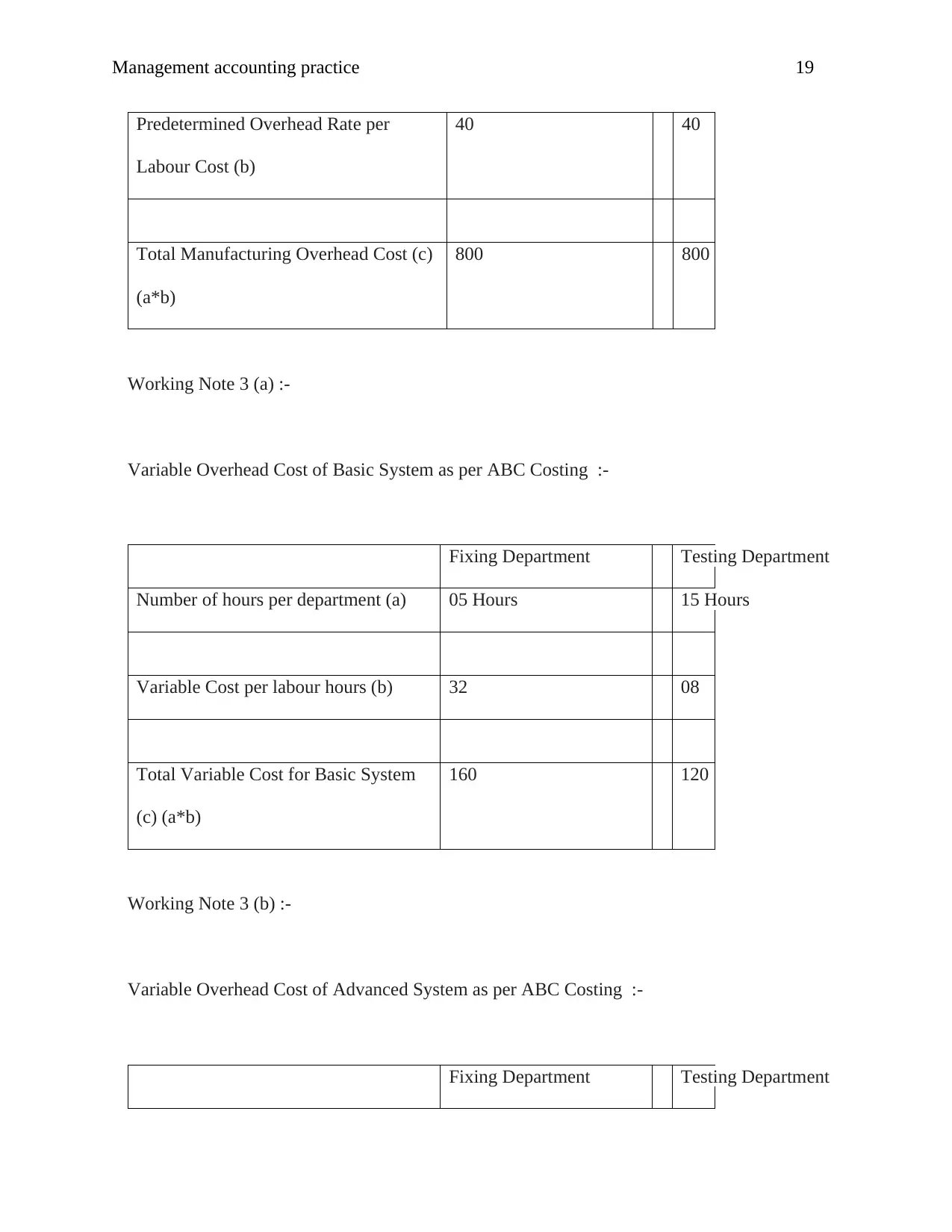

Predetermined Overhead Rate per

Labour Cost (b)

40 40

Total Manufacturing Overhead Cost (c)

(a*b)

800 800

Working Note 3 (a) :-

Variable Overhead Cost of Basic System as per ABC Costing :-

Fixing Department Testing Department

Number of hours per department (a) 05 Hours 15 Hours

Variable Cost per labour hours (b) 32 08

Total Variable Cost for Basic System

(c) (a*b)

160 120

Working Note 3 (b) :-

Variable Overhead Cost of Advanced System as per ABC Costing :-

Fixing Department Testing Department

Predetermined Overhead Rate per

Labour Cost (b)

40 40

Total Manufacturing Overhead Cost (c)

(a*b)

800 800

Working Note 3 (a) :-

Variable Overhead Cost of Basic System as per ABC Costing :-

Fixing Department Testing Department

Number of hours per department (a) 05 Hours 15 Hours

Variable Cost per labour hours (b) 32 08

Total Variable Cost for Basic System

(c) (a*b)

160 120

Working Note 3 (b) :-

Variable Overhead Cost of Advanced System as per ABC Costing :-

Fixing Department Testing Department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting practice 20

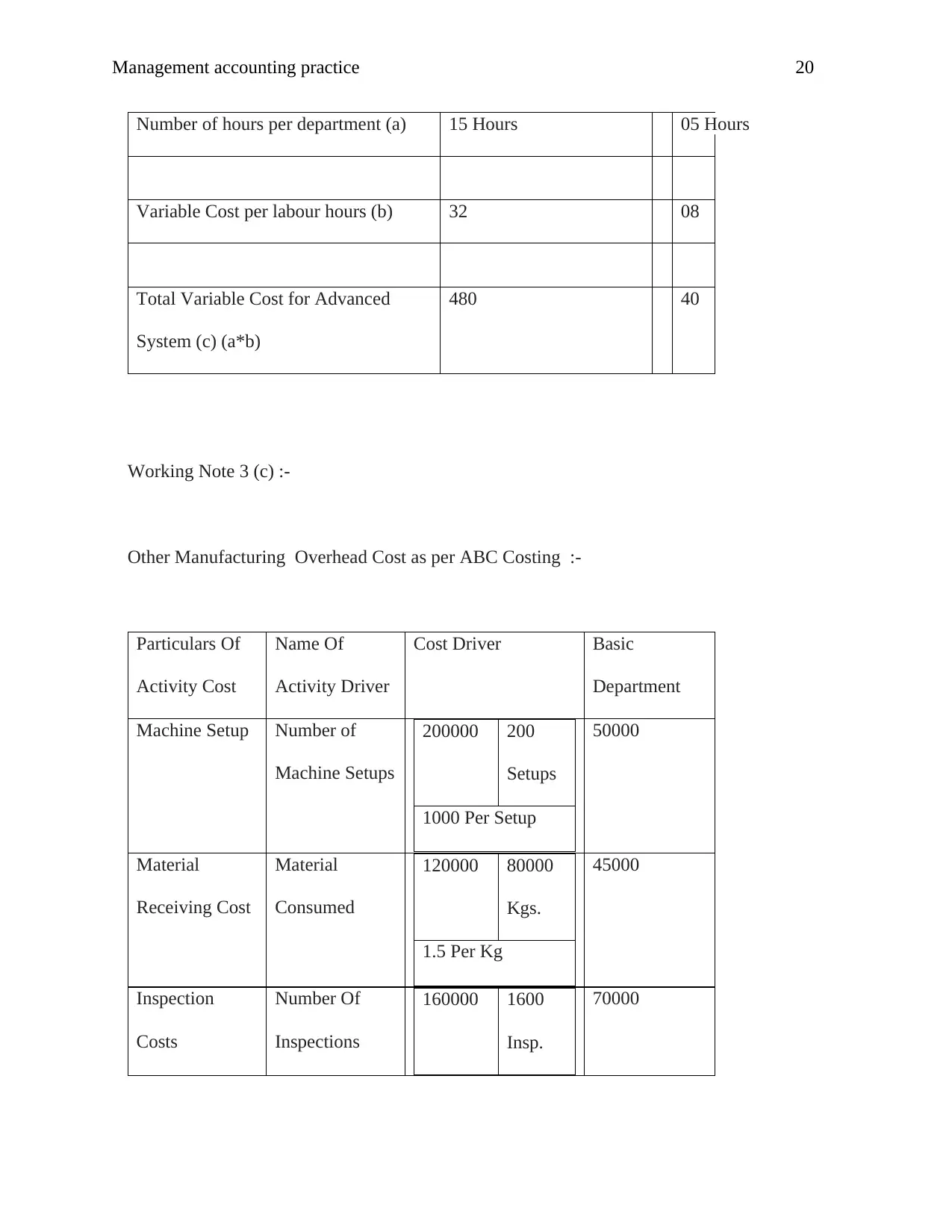

Number of hours per department (a) 15 Hours 05 Hours

Variable Cost per labour hours (b) 32 08

Total Variable Cost for Advanced

System (c) (a*b)

480 40

Working Note 3 (c) :-

Other Manufacturing Overhead Cost as per ABC Costing :-

Particulars Of

Activity Cost

Name Of

Activity Driver

Cost Driver Basic

Department

Machine Setup Number of

Machine Setups

200000 200

Setups

1000 Per Setup

50000

Material

Receiving Cost

Material

Consumed

120000 80000

Kgs.

1.5 Per Kg

45000

Inspection

Costs

Number Of

Inspections

160000 1600

Insp.

70000

Number of hours per department (a) 15 Hours 05 Hours

Variable Cost per labour hours (b) 32 08

Total Variable Cost for Advanced

System (c) (a*b)

480 40

Working Note 3 (c) :-

Other Manufacturing Overhead Cost as per ABC Costing :-

Particulars Of

Activity Cost

Name Of

Activity Driver

Cost Driver Basic

Department

Machine Setup Number of

Machine Setups

200000 200

Setups

1000 Per Setup

50000

Material

Receiving Cost

Material

Consumed

120000 80000

Kgs.

1.5 Per Kg

45000

Inspection

Costs

Number Of

Inspections

160000 1600

Insp.

70000

Management accounting practice 21

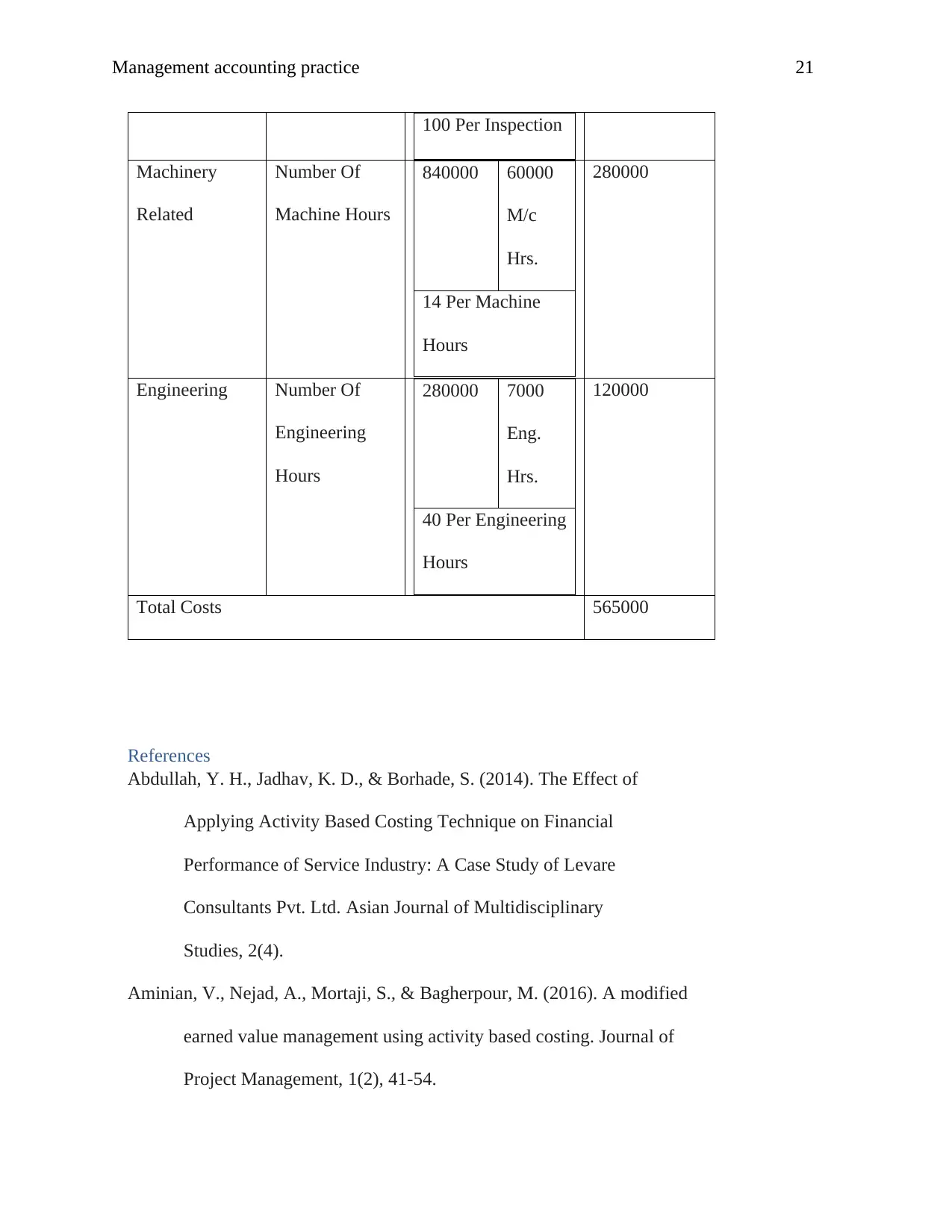

100 Per Inspection

Machinery

Related

Number Of

Machine Hours

840000 60000

M/c

Hrs.

14 Per Machine

Hours

280000

Engineering Number Of

Engineering

Hours

280000 7000

Eng.

Hrs.

40 Per Engineering

Hours

120000

Total Costs 565000

References

Abdullah, Y. H., Jadhav, K. D., & Borhade, S. (2014). The Effect of

Applying Activity Based Costing Technique on Financial

Performance of Service Industry: A Case Study of Levare

Consultants Pvt. Ltd. Asian Journal of Multidisciplinary

Studies, 2(4).

Aminian, V., Nejad, A., Mortaji, S., & Bagherpour, M. (2016). A modified

earned value management using activity based costing. Journal of

Project Management, 1(2), 41-54.

100 Per Inspection

Machinery

Related

Number Of

Machine Hours

840000 60000

M/c

Hrs.

14 Per Machine

Hours

280000

Engineering Number Of

Engineering

Hours

280000 7000

Eng.

Hrs.

40 Per Engineering

Hours

120000

Total Costs 565000

References

Abdullah, Y. H., Jadhav, K. D., & Borhade, S. (2014). The Effect of

Applying Activity Based Costing Technique on Financial

Performance of Service Industry: A Case Study of Levare

Consultants Pvt. Ltd. Asian Journal of Multidisciplinary

Studies, 2(4).

Aminian, V., Nejad, A., Mortaji, S., & Bagherpour, M. (2016). A modified

earned value management using activity based costing. Journal of

Project Management, 1(2), 41-54.

Management accounting practice 22

Baker, H. K., & English, P. (2011). Capital budgeting valuation: Financial

analysis for today's investment projects (Vol. 13). John Wiley &

Sons.

Bayati, M., Ahari, A. M., Badakhshan, A., Gholipour, M., & Joulaei, H.

(2015). Cost Analysis of MRI Services in Iran: An Application of

Activity Based Costing Technique. Iranian Journal of

Radiology, 12(4).

Boxall, P., & Purcell, J. (2011). Strategy and human resource management.

Palgrave Macmillan.

Cassettari, L., Mosca, M., Mosca, R., Rolando, F., Costa, M., & Pisaturo, V.

(2016). IVF cycle cost estimation using Activity Based Costing and

Monte Carlo simulation. Health care management science, 19(1), 20-

30.

Cugueró-Escofet, N., & Fito, M. (2016). The Impact of ABC Costing

Systems to Solve Managerial Cost Problems: A Real Improvement, a

Fad or a Fashion?.

Cugueró-Escofet, N., & Fito, M. (2016). The Impact of ABC Costing

Systems to Solve Managerial Cost Problems: A Real Improvement, a

Fad or a Fashion?.

Dunning, J. H. (2014). The Globalization of Business (Routledge Revivals):

The Challenge of the 1990s. Routledge.

Ebrahimian, H., Taheri, B., & Yousefi, N. (2015). Optimal operation of

energy at hydrothermal power plants by simultaneous minimization

Baker, H. K., & English, P. (2011). Capital budgeting valuation: Financial

analysis for today's investment projects (Vol. 13). John Wiley &

Sons.

Bayati, M., Ahari, A. M., Badakhshan, A., Gholipour, M., & Joulaei, H.

(2015). Cost Analysis of MRI Services in Iran: An Application of

Activity Based Costing Technique. Iranian Journal of

Radiology, 12(4).

Boxall, P., & Purcell, J. (2011). Strategy and human resource management.

Palgrave Macmillan.

Cassettari, L., Mosca, M., Mosca, R., Rolando, F., Costa, M., & Pisaturo, V.

(2016). IVF cycle cost estimation using Activity Based Costing and

Monte Carlo simulation. Health care management science, 19(1), 20-

30.

Cugueró-Escofet, N., & Fito, M. (2016). The Impact of ABC Costing

Systems to Solve Managerial Cost Problems: A Real Improvement, a

Fad or a Fashion?.

Cugueró-Escofet, N., & Fito, M. (2016). The Impact of ABC Costing

Systems to Solve Managerial Cost Problems: A Real Improvement, a

Fad or a Fashion?.

Dunning, J. H. (2014). The Globalization of Business (Routledge Revivals):

The Challenge of the 1990s. Routledge.

Ebrahimian, H., Taheri, B., & Yousefi, N. (2015). Optimal operation of

energy at hydrothermal power plants by simultaneous minimization

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.