Audit, Assurance and Compliance - Assignment

13 Pages3101 Words34 Views

Added on 2020-03-02

Audit, Assurance and Compliance - Assignment

Added on 2020-03-02

ShareRelated Documents

Running head: AUDIT, ASSURANCE AND COMPLIANCEAudit, Assurance and ComplianceName of the Student:Name of the University:Author’s Note:Course ID:

AUDIT, ASSURANCE AND COMPLIANCE 1Table of ContentsAnswer 1..........................................................................................................................................2Answer 2..........................................................................................................................................4Answer 3..........................................................................................................................................6Part A: Answer............................................................................................................................6Part B: Answer...........................................................................................................................10Reference List................................................................................................................................11

AUDIT, ASSURANCE AND COMPLIANCE 2Answer 1In the method for setting up the review design of Double Ink Printers Limited (DIPL), theinvestigative procedure related with money related information gives monstrous regard. As amatter of fact, review design passes on the required orientation and principles to the evaluators inthe midst of the review operations. Precisely, review design engages the evaluators in keeping upthe cost of review in a particular purpose of containment for foreseeing confusion with thereview clients (Alam 2014). The legitimate approach related to the monetary information ofDIPL shows the system for spreading budgetary information from the distinctive money relateddeclarations of the association. The methodology for separating the budgetary information of theassociations could be brought out through a couple of frameworks. With the help of analytic approach for assessing the money related information, theaccounting and monetary examiners of the association s could utilize such information forundertaking particular budgetary and accounting decisions (Baylis et al. 2017). The ordinary sizelogical approach enables in the system for dissecting the money related introduction of theassociations from the normal viewpoints. One of the fundamental favorable circumstances is thatit helps in growing help in separating the money related reports from various monetary coursesof occasions. The accounting and monetary specialists could utilize various lines of things from thebudgetary reports and they could affirm their base of making arrangements for the associations.For instance, the selection philosophy of different money related and accounting things in themonetary reports, for instance, net liabilities, assets, proprietor's esteem and others could be seen

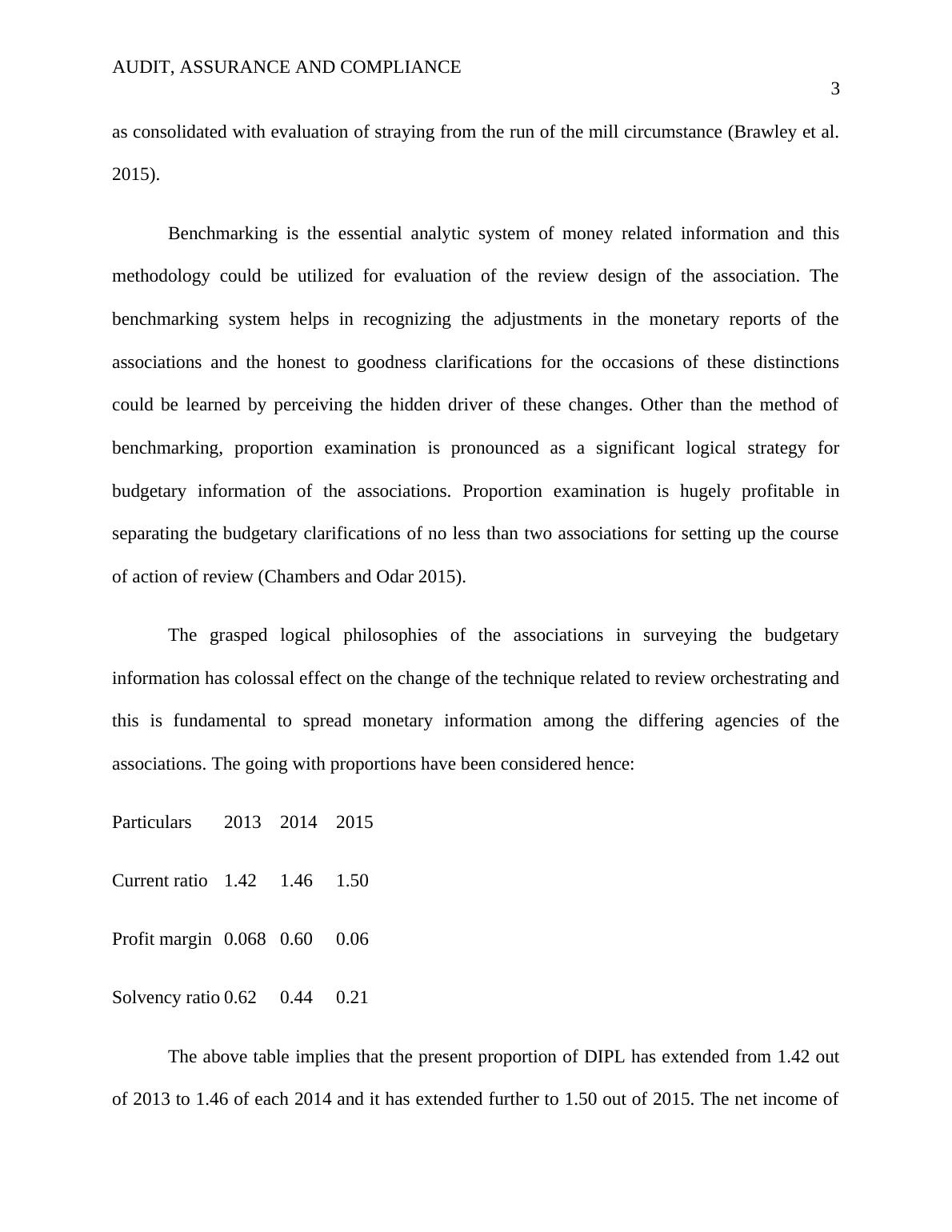

AUDIT, ASSURANCE AND COMPLIANCE 3as consolidated with evaluation of straying from the run of the mill circumstance (Brawley et al.2015). Benchmarking is the essential analytic system of money related information and thismethodology could be utilized for evaluation of the review design of the association. Thebenchmarking system helps in recognizing the adjustments in the monetary reports of theassociations and the honest to goodness clarifications for the occasions of these distinctionscould be learned by perceiving the hidden driver of these changes. Other than the method ofbenchmarking, proportion examination is pronounced as a significant logical strategy forbudgetary information of the associations. Proportion examination is hugely profitable inseparating the budgetary clarifications of no less than two associations for setting up the courseof action of review (Chambers and Odar 2015). The grasped logical philosophies of the associations in surveying the budgetaryinformation has colossal effect on the change of the technique related to review orchestrating andthis is fundamental to spread monetary information among the differing agencies of theassociations. The going with proportions have been considered hence: Particulars201320142015 Current ratio1.421.461.50 Profit margin0.0680.600.06 Solvency ratio0.620.440.21 The above table implies that the present proportion of DIPL has extended from 1.42 outof 2013 to 1.46 of each 2014 and it has extended further to 1.50 out of 2015. The net income of

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Report on Audit, Assurance and Compliancelg...

|8

|1628

|50

HI6026 Auditing & Assurance Serviceslg...

|13

|2929

|75

HI6026 Assignment | Audit, Assurance and Compliancelg...

|14

|3469

|46

HI6026 - Audit, Assurance and Compliance | Assignmentlg...

|12

|2880

|56

HI6026 - Audit, Assurance and Compliance, Question/Answerlg...

|10

|2418

|34

HI6026 - Assignment - Audit, Assurance & Compliancelg...

|12

|2881

|54