Analyzing Impairment of Assets Under IAS 36: A Case Study of Gali Ltd

VerifiedAdded on 2023/04/25

|7

|1239

|96

Report

AI Summary

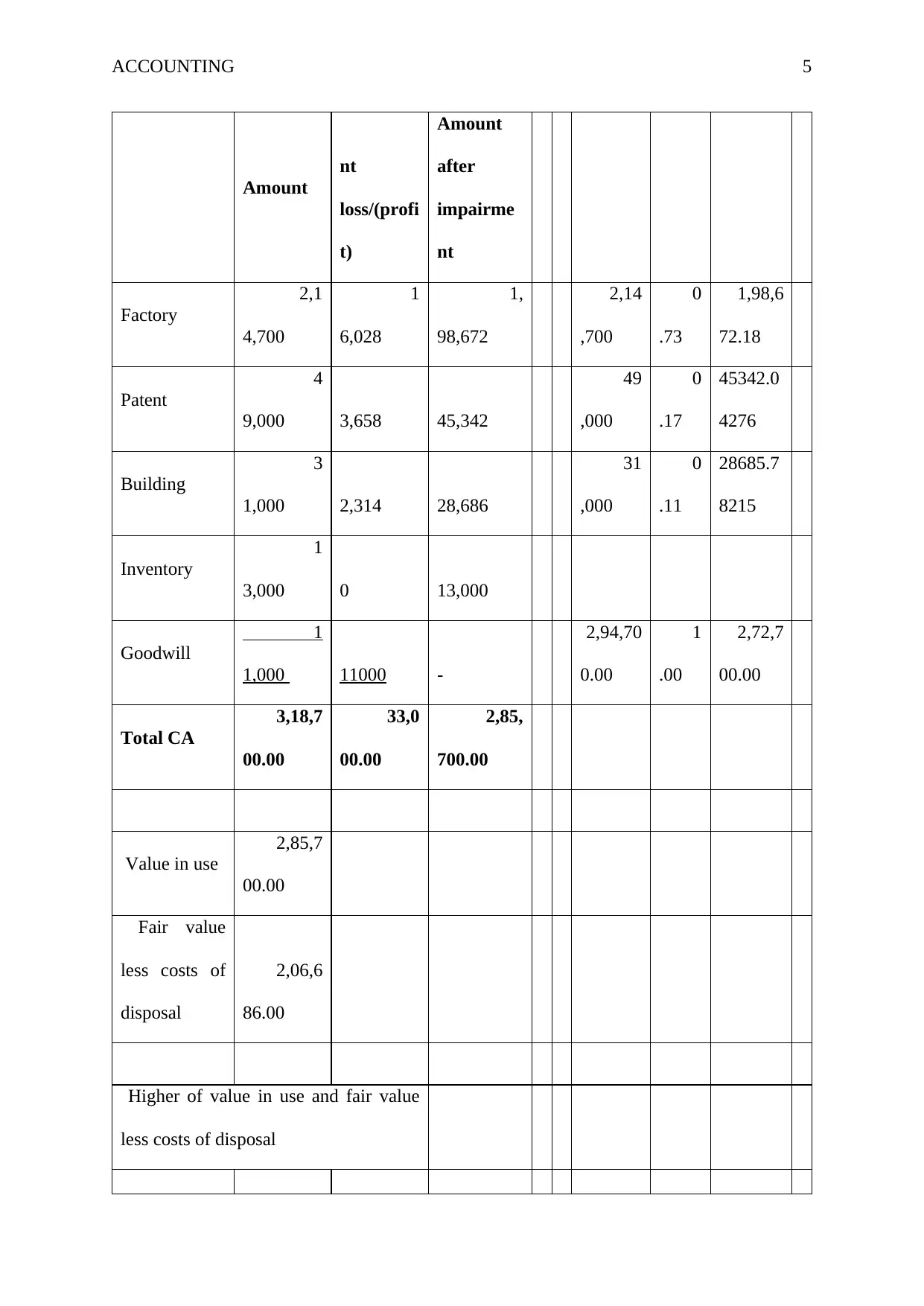

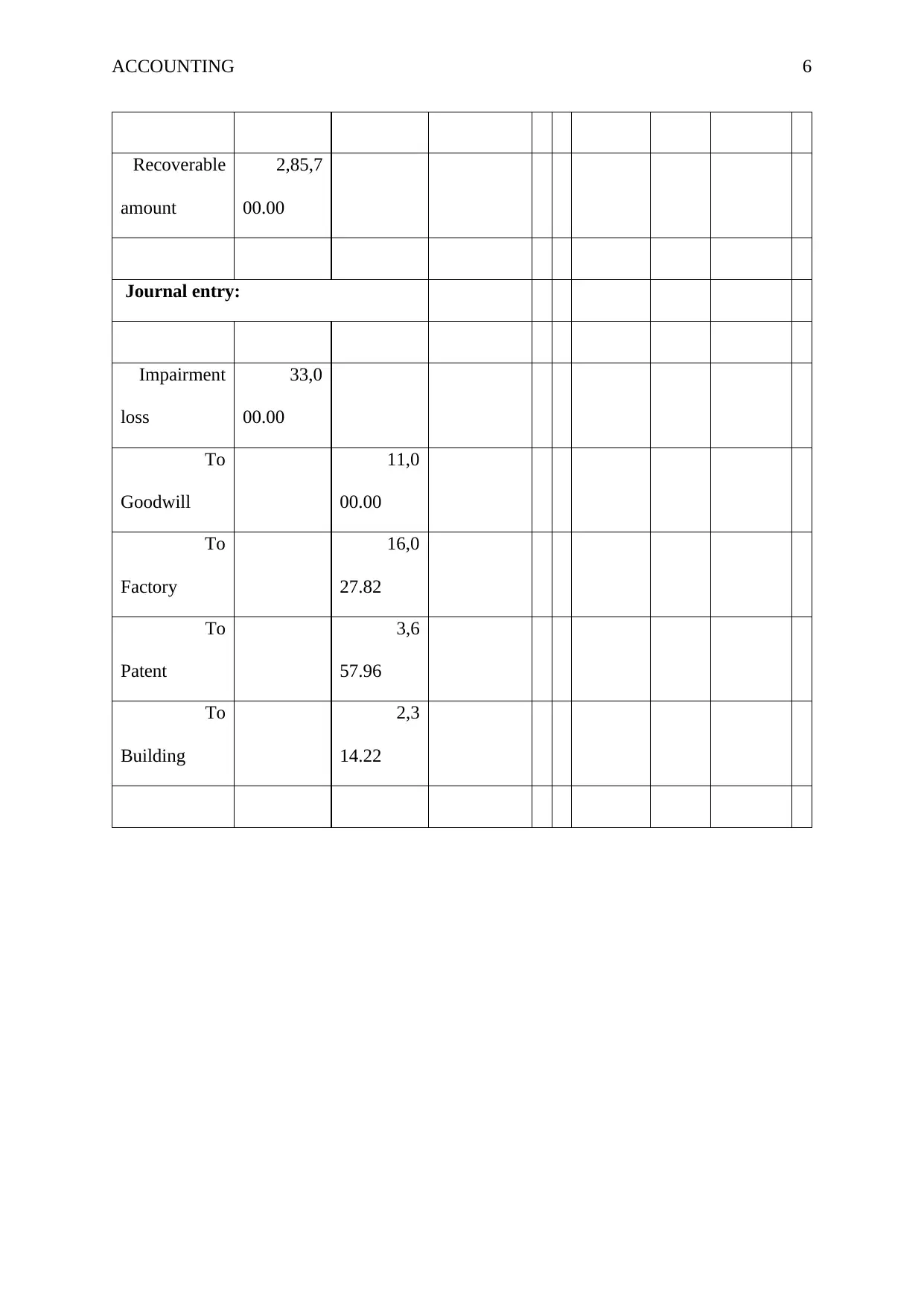

This report provides a detailed analysis of IAS 36, focusing on the impairment of assets. It explains how to calculate the recoverable amount, value in use, and fair value less costs of disposal. The report includes a practical application with calculations and journal entries for Gali Ltd, demonstrating how to account for impairment losses in accordance with IAS 36. The analysis covers external and internal factors affecting impairment and provides illustrative examples. The report also includes the journal entries for the impairment loss calculation. Desklib offers more solved assignments and study resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.