Accounting for Business: Financial Ratio Analysis and Interpretation

VerifiedAdded on 2020/10/22

|8

|1865

|426

Report

AI Summary

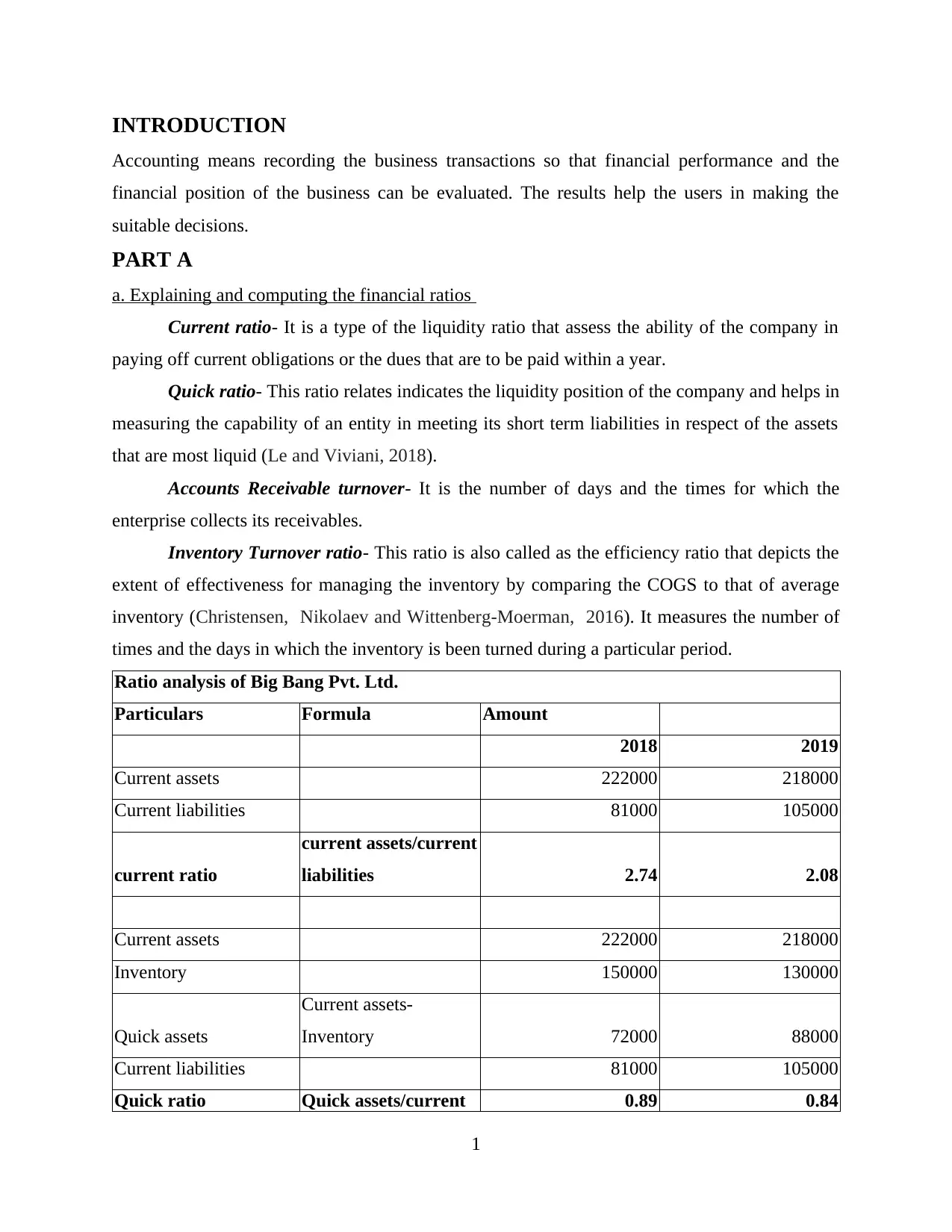

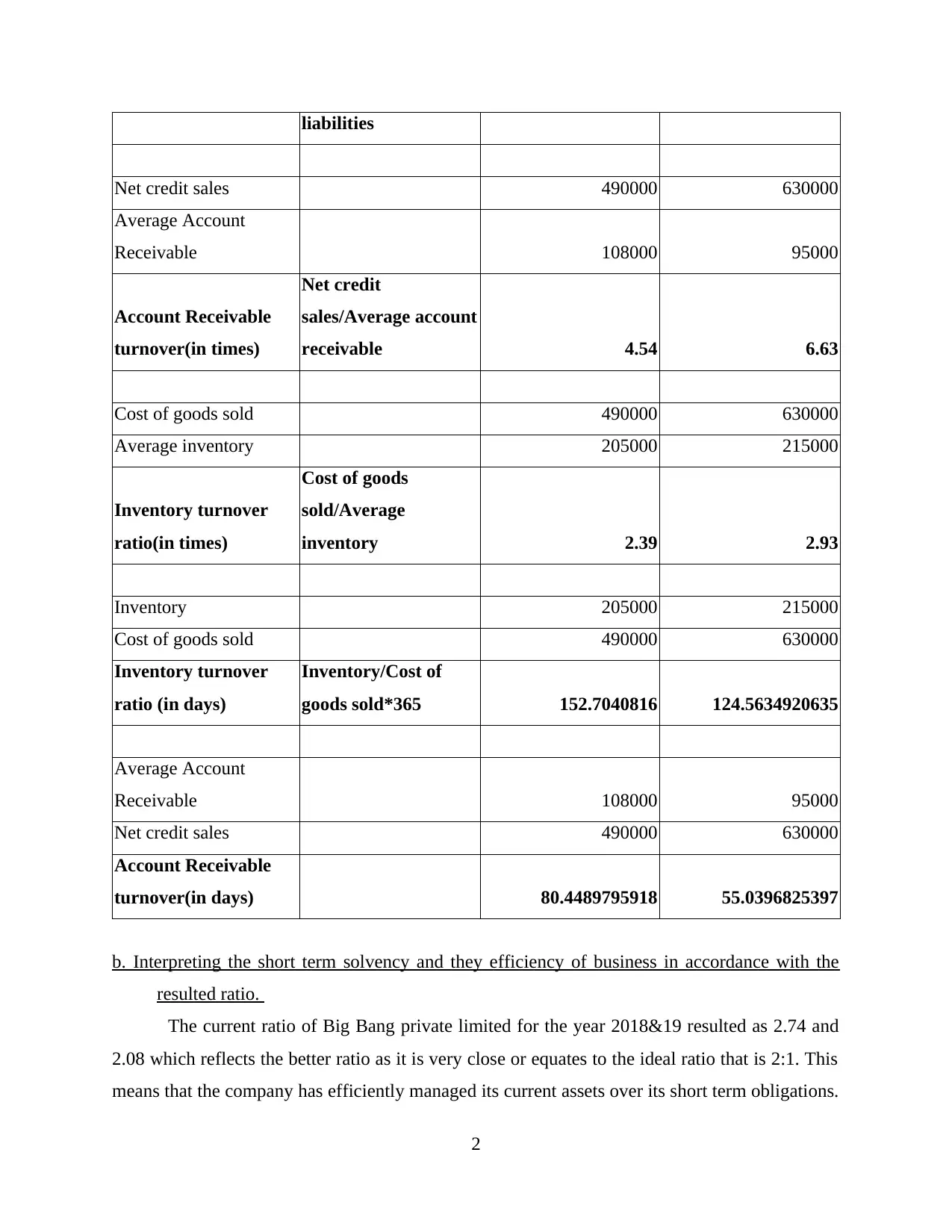

This report provides a comprehensive analysis of financial ratios, focusing on current ratio, quick ratio, accounts receivable turnover, and inventory turnover. The analysis includes the computation of these ratios for Big Bang Pvt. Ltd. over two years, followed by an interpretation of short-term solvency and efficiency. The report further distinguishes between items representing income and revenue, providing examples. Additionally, it offers suggestions from the perspective of a banker and a business person regarding loan approvals and potential acquisitions, respectively. Finally, it considers a scenario where existing owners pay off liabilities, offering a strategic recommendation. The report concludes by emphasizing the importance of accounting in evaluating business financial information.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.