Detailed Analysis of Financial Intermediaries in a Modern Economy

VerifiedAdded on 2023/01/03

|12

|3455

|31

Report

AI Summary

This report provides a comprehensive overview of the role of financial intermediaries in a modern economy. It begins with an introduction to financial intermediaries, defining their function as the link between service providers and customers, and the channels through which savings are invested. The report explores the various roles of financial intermediaries, including channeling funds from surplus to deficit units. It then delves into the specifics of different types of intermediaries, such as deposit-type institutions (banks), contractual savings institutions (insurance, pension funds), commercial banks, thrift institutions, and credit unions. Each type is described in detail, highlighting their specific functions, sources of funds, and impact on the financial system. The report emphasizes the importance of financial intermediaries in promoting economic growth and efficient capital allocation. The report also discusses the role of each financial intermediary and their specific functions. The report also mentions the different roles of commercial banks, thrift institutions, and credit unions. It also discusses the role of the Federal Deposit Insurance Corporation (FDIC) and the impact of the 2008 financial crises.

The role of financial intermediaries

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION.................3

MAIN BODY..................................................................................................................................3

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

2

MAIN BODY..................................................................................................................................3

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

2

Explain in detail the role of financial intermediaries in a modern economy.

INTRODUCTION

Financial terms in a country are the most important factor that regulates the improvement

and growth of economy. In this financial system, the essential role is played by financial

intermediaries. A financial intermediary can be explained as an institution or organization that is

acting as the middle party in two important segments of an economical setup. These segments

are service provider and ultimate customer. In other words, a financial intermediary can be

explained as the tool or route through which savings are channelized into the tunnel of

investment. Financial intermediaries basically exist in the financial market so as to render profits

for all participants in the financial system and sometimes they are acting as the regulating

authority of financial transactions also. Trends suggest that financial intermediaries role in

savings and investment functions can be used for an efficient market system or like the sub-

prime crisis shows, they can be a cause for concern as well. This report is focusing on discussion

of roles of different financial intermediaries in a modern economical setup.

MAIN BODY

This report will start from explaining different roles that a financial intermediary is taking

on in a financial system. The main role is to channelize excess funds from the surplus units to

those units which are facing the deficit. The main reason behind naming these institutions as

intermediaries is that they are acting as the middlemen in whole financial system. They are

taking up the responsibility for moving funds to deficit units from surplus units. They do not take

financial method in consideration and just concentrating on bringing different participants on the

same page and with the benefit of least possible cost and least inconvenience. If the economy

wants to climb the growth chart, than most factor is to ensure that financial system is working in

an efficient manner. This efficiency can be measured through availability of amount of capital in

the economy. Capital formation is an important aspect of growth of economy (Allen and et al.,

2018). Thus, if the financial system works properly, firms with the most promising investment

opportunities receive funds, and those with inferior opportunities receive no funding. In a similar

manner, consumers who can pay the current market rate of interest can purchase cars, boats,

vacations, and homes on credit − and thus have them now rather than waiting until they have the

3

INTRODUCTION

Financial terms in a country are the most important factor that regulates the improvement

and growth of economy. In this financial system, the essential role is played by financial

intermediaries. A financial intermediary can be explained as an institution or organization that is

acting as the middle party in two important segments of an economical setup. These segments

are service provider and ultimate customer. In other words, a financial intermediary can be

explained as the tool or route through which savings are channelized into the tunnel of

investment. Financial intermediaries basically exist in the financial market so as to render profits

for all participants in the financial system and sometimes they are acting as the regulating

authority of financial transactions also. Trends suggest that financial intermediaries role in

savings and investment functions can be used for an efficient market system or like the sub-

prime crisis shows, they can be a cause for concern as well. This report is focusing on discussion

of roles of different financial intermediaries in a modern economical setup.

MAIN BODY

This report will start from explaining different roles that a financial intermediary is taking

on in a financial system. The main role is to channelize excess funds from the surplus units to

those units which are facing the deficit. The main reason behind naming these institutions as

intermediaries is that they are acting as the middlemen in whole financial system. They are

taking up the responsibility for moving funds to deficit units from surplus units. They do not take

financial method in consideration and just concentrating on bringing different participants on the

same page and with the benefit of least possible cost and least inconvenience. If the economy

wants to climb the growth chart, than most factor is to ensure that financial system is working in

an efficient manner. This efficiency can be measured through availability of amount of capital in

the economy. Capital formation is an important aspect of growth of economy (Allen and et al.,

2018). Thus, if the financial system works properly, firms with the most promising investment

opportunities receive funds, and those with inferior opportunities receive no funding. In a similar

manner, consumers who can pay the current market rate of interest can purchase cars, boats,

vacations, and homes on credit − and thus have them now rather than waiting until they have the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

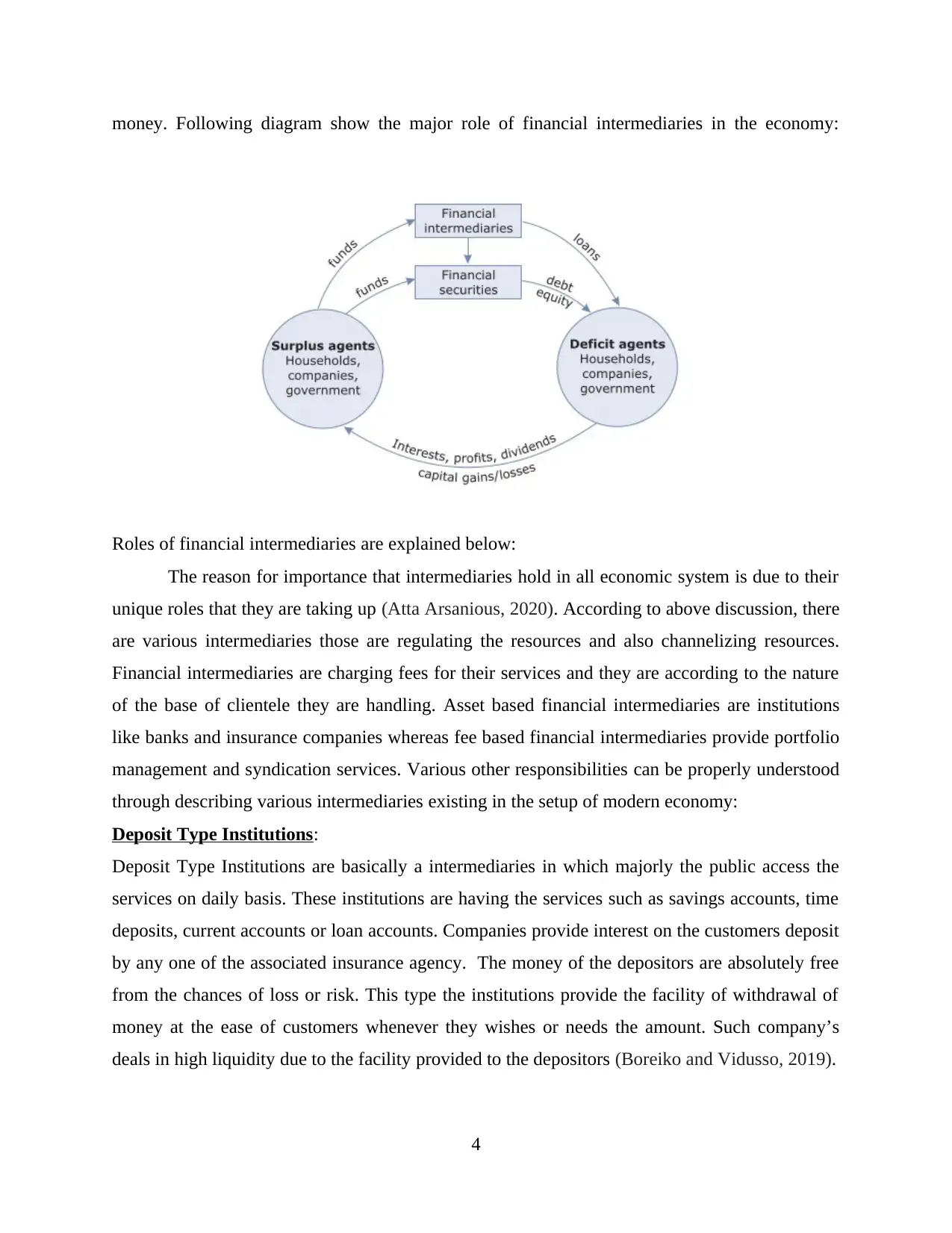

money. Following diagram show the major role of financial intermediaries in the economy:

Roles of financial intermediaries are explained below:

The reason for importance that intermediaries hold in all economic system is due to their

unique roles that they are taking up (Atta Arsanious, 2020). According to above discussion, there

are various intermediaries those are regulating the resources and also channelizing resources.

Financial intermediaries are charging fees for their services and they are according to the nature

of the base of clientele they are handling. Asset based financial intermediaries are institutions

like banks and insurance companies whereas fee based financial intermediaries provide portfolio

management and syndication services. Various other responsibilities can be properly understood

through describing various intermediaries existing in the setup of modern economy:

Deposit Type Institutions:

Deposit Type Institutions are basically a intermediaries in which majorly the public access the

services on daily basis. These institutions are having the services such as savings accounts, time

deposits, current accounts or loan accounts. Companies provide interest on the customers deposit

by any one of the associated insurance agency. The money of the depositors are absolutely free

from the chances of loss or risk. This type the institutions provide the facility of withdrawal of

money at the ease of customers whenever they wishes or needs the amount. Such company’s

deals in high liquidity due to the facility provided to the depositors (Boreiko and Vidusso, 2019).

4

Roles of financial intermediaries are explained below:

The reason for importance that intermediaries hold in all economic system is due to their

unique roles that they are taking up (Atta Arsanious, 2020). According to above discussion, there

are various intermediaries those are regulating the resources and also channelizing resources.

Financial intermediaries are charging fees for their services and they are according to the nature

of the base of clientele they are handling. Asset based financial intermediaries are institutions

like banks and insurance companies whereas fee based financial intermediaries provide portfolio

management and syndication services. Various other responsibilities can be properly understood

through describing various intermediaries existing in the setup of modern economy:

Deposit Type Institutions:

Deposit Type Institutions are basically a intermediaries in which majorly the public access the

services on daily basis. These institutions are having the services such as savings accounts, time

deposits, current accounts or loan accounts. Companies provide interest on the customers deposit

by any one of the associated insurance agency. The money of the depositors are absolutely free

from the chances of loss or risk. This type the institutions provide the facility of withdrawal of

money at the ease of customers whenever they wishes or needs the amount. Such company’s

deals in high liquidity due to the facility provided to the depositors (Boreiko and Vidusso, 2019).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The congress committee has raised the limit of federal deposit insurance from $100,000

to $250,000 due to the financial crises of year 2008. The aim of this action is to gain more trust

and confidence of the customers for the banking sector and to deposit in it. This happened

because multibillion dollar funds were taken out from the money market and liquidated the assets

for the same. In 1980 the limit in insurance agencies has increased (Chan, 2019). In year 1991 in

the banking sector the ratio of insured depositors from 82 per cent to 62 in year ending 2007.

Contractual Savings Institutions:

Contractual Savings Institution is an arrangement and investment of funds for a long

period of time on contractual basis through an institution. Investment such as in Pension Funds,

Insurance, Provident funds, etc. A contract is made for the investment from the customers to

their pension or insurance accounts. Such institutions deals in long term funds such as stocks or

bonds and does not concerns on liquidity as they have a stable cash flow. The main transaction of

these institutions is to obtain funds from long term contractual arrangements and then, further

investing these funds in capital markets. The major examples in this category are insurance

companies and pension funds. The main feature of these institutions is that there is a relatively

slow flow of funds those are coming from contractual commitments along with their

policyholders in insurance category and also in category of participants in pension fund.

Therefore, liquidity can never become a problem in administration of these organisations. Due to

the reason of their efficiency in operations and also because of the organizational structure, the

firm is capable to invest in long term securities, such as bonds and in some cases in common

stock also.

Life Insurance Companies:

Life Insurance Companies are those who provide the insurance policies to those who

want to protect their family from loss such as pre mature death or retirement. The company gets

funds from selling of such policies. In against of paying premium to the company the insured

family gets some monetary benefit from the company to reduce their losses. Some policies

provide only the risk protection whereas some policies provide savings along with risk protection

feature. Companies invest its funds generally in the high yield investments which are for long

term. This is done because the company has predictions on its inflows and outflows. Such

institutions are being governed by states having fewer restrictions (Corrado and Corrado, 2017).

Casualty Insurance Companies:

5

to $250,000 due to the financial crises of year 2008. The aim of this action is to gain more trust

and confidence of the customers for the banking sector and to deposit in it. This happened

because multibillion dollar funds were taken out from the money market and liquidated the assets

for the same. In 1980 the limit in insurance agencies has increased (Chan, 2019). In year 1991 in

the banking sector the ratio of insured depositors from 82 per cent to 62 in year ending 2007.

Contractual Savings Institutions:

Contractual Savings Institution is an arrangement and investment of funds for a long

period of time on contractual basis through an institution. Investment such as in Pension Funds,

Insurance, Provident funds, etc. A contract is made for the investment from the customers to

their pension or insurance accounts. Such institutions deals in long term funds such as stocks or

bonds and does not concerns on liquidity as they have a stable cash flow. The main transaction of

these institutions is to obtain funds from long term contractual arrangements and then, further

investing these funds in capital markets. The major examples in this category are insurance

companies and pension funds. The main feature of these institutions is that there is a relatively

slow flow of funds those are coming from contractual commitments along with their

policyholders in insurance category and also in category of participants in pension fund.

Therefore, liquidity can never become a problem in administration of these organisations. Due to

the reason of their efficiency in operations and also because of the organizational structure, the

firm is capable to invest in long term securities, such as bonds and in some cases in common

stock also.

Life Insurance Companies:

Life Insurance Companies are those who provide the insurance policies to those who

want to protect their family from loss such as pre mature death or retirement. The company gets

funds from selling of such policies. In against of paying premium to the company the insured

family gets some monetary benefit from the company to reduce their losses. Some policies

provide only the risk protection whereas some policies provide savings along with risk protection

feature. Companies invest its funds generally in the high yield investments which are for long

term. This is done because the company has predictions on its inflows and outflows. Such

institutions are being governed by states having fewer restrictions (Corrado and Corrado, 2017).

Casualty Insurance Companies:

5

These companies are opposite to Life Insurance as it provides policies to those who want

protection for incidents such as fire, theft, accidents, for their assets. Such policies do not provide

any liquidity and any surrender value to its customers as it is pure risk protection insurance. The

companies have the predictions on their inflows but do not have any on its outflows. They deal in

highly marketable securities generally short term due to the presence of non projection of cash

outflows. Companies generally take holdings on equity securities in order to offset their lower

returns. To reduce the taxes of the institution they hold their position in some municipal bonds.

Pension Funds:

The fund from the combined contribution of an employer and a employee during the job

in a particular company is termed as pension funds. The employees get this payment back during

his retirement period on monthly basis (Ferrarini, 2017). The aim of this fund is to secure the

employees retirement as after retirement he will not be able to earn regular salary from the

company. The institutions invest these funds in equity obligation funds or in corporate bonds.

The requirement of retirement income and the success of labours has in getting their pension

funds increased has proven a growth factor for the institutions. This growth is to private sector as

well as to the state and local government bodies since world War II. The inflows in such funds

are for a long period and the institutions are having forecasts for the outflow. Therefore the

companies use to invest the funds into long term securities having the feature of high yield.

Commercial banks:

These are considered as most diversified middle firm on the basis of amount of holding in

categories of assets and liabilities. These are also the largest intermediary on the same basis of

numbers. According to different surveys, it is visible that at the end of year 2003, the holding of

commercial banks in figures was $7.8 trillion. This holding was in the category of financial

assets. Banks are creating liabilities in the name of savings account, checking accounts and

various other type of time deposits. The institution which is responsible for issuing insurance for

bank deposits, famously known as Federal Deposit Insurance Corporation has issued a total of

insurance for bank deposits for $250,000 to the maximum limit. In the other side of balance

sheet, which is covering all the assets of the bank, they are issuing a variety of loans that are

covering various categories. These categories can be named as loans rendered to consumers,

businesses and state and local government. Furthermore, various commercial banks are having

some important departments; those are responsible for handling operations like leasing and trust.

6

protection for incidents such as fire, theft, accidents, for their assets. Such policies do not provide

any liquidity and any surrender value to its customers as it is pure risk protection insurance. The

companies have the predictions on their inflows but do not have any on its outflows. They deal in

highly marketable securities generally short term due to the presence of non projection of cash

outflows. Companies generally take holdings on equity securities in order to offset their lower

returns. To reduce the taxes of the institution they hold their position in some municipal bonds.

Pension Funds:

The fund from the combined contribution of an employer and a employee during the job

in a particular company is termed as pension funds. The employees get this payment back during

his retirement period on monthly basis (Ferrarini, 2017). The aim of this fund is to secure the

employees retirement as after retirement he will not be able to earn regular salary from the

company. The institutions invest these funds in equity obligation funds or in corporate bonds.

The requirement of retirement income and the success of labours has in getting their pension

funds increased has proven a growth factor for the institutions. This growth is to private sector as

well as to the state and local government bodies since world War II. The inflows in such funds

are for a long period and the institutions are having forecasts for the outflow. Therefore the

companies use to invest the funds into long term securities having the feature of high yield.

Commercial banks:

These are considered as most diversified middle firm on the basis of amount of holding in

categories of assets and liabilities. These are also the largest intermediary on the same basis of

numbers. According to different surveys, it is visible that at the end of year 2003, the holding of

commercial banks in figures was $7.8 trillion. This holding was in the category of financial

assets. Banks are creating liabilities in the name of savings account, checking accounts and

various other type of time deposits. The institution which is responsible for issuing insurance for

bank deposits, famously known as Federal Deposit Insurance Corporation has issued a total of

insurance for bank deposits for $250,000 to the maximum limit. In the other side of balance

sheet, which is covering all the assets of the bank, they are issuing a variety of loans that are

covering various categories. These categories can be named as loans rendered to consumers,

businesses and state and local government. Furthermore, various commercial banks are having

some important departments; those are responsible for handling operations like leasing and trust.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These departments are known as trust departments and leasing governments. Commercial banks

are holding a high value of importance in modern economic system, due to the reason that they

play a vital role in the monetary system of country and also they are affecting the well being of

economic situations in the country. They are having the most significant role in the area of their

location in which they are situated. In addition to this, they are the highest impacting regulation

in category of whole system of financial institutions in the system (Marini and et al., 2018).

Thrift institution:

Thrift institutions are basically the common name for institutions that are handling the

business of savings and loan businesses, and mutual savings banks are the main organisations

those are coming under this category (McLeod and et al., 2018). The main source of funds for

these organizations is issuance of checking accounts, often called as NOW accounts, savings

accounts and various other types of time deposits that are made in these institutions from general

public. These organizations are further using these funds so as to purchase loans in real estate

area. The major types of these loans come under the category of mortgages in long term time

period. According to different surveys and figures, it is very evident that these organizations are

the biggest providers in the category of mortgage loans. They provide a great help to consumers

and hence, play a vital role in channelizing the movement of fund in the right direction in an

economical setup. At the present time, these organizations are specialised in providing the

intermediation service in the sector of maturity and denomination funds. This is due to the reason

that they are acquiring funds through borrowing process of money for a very short term period.

This borrowing is done through two major forms of accounts and they are checking and savings

account. They are lending money on long term in exchange of collateral of real estate. In the case

of thrift institutions, the FDIC insurance amount comes up the maximum limit of $250,000.

Credit unions

These are institutions which are operating on a small scale. These organisations are non

profit and working on cooperative organisational structure. These firms are consumer oriented

and are owned and operated completely by the members and customers of the firm (Mimir,

2016). The company has two major heads in the liabilities section and they are checking

accounts, often called as share drafts and second is savings account, called as share accounts.

These liabilities are basically devoted to only one thing and it is short term consumer loans.

These share accounts issued by the credit union are insured by the federal institution to the

7

are holding a high value of importance in modern economic system, due to the reason that they

play a vital role in the monetary system of country and also they are affecting the well being of

economic situations in the country. They are having the most significant role in the area of their

location in which they are situated. In addition to this, they are the highest impacting regulation

in category of whole system of financial institutions in the system (Marini and et al., 2018).

Thrift institution:

Thrift institutions are basically the common name for institutions that are handling the

business of savings and loan businesses, and mutual savings banks are the main organisations

those are coming under this category (McLeod and et al., 2018). The main source of funds for

these organizations is issuance of checking accounts, often called as NOW accounts, savings

accounts and various other types of time deposits that are made in these institutions from general

public. These organizations are further using these funds so as to purchase loans in real estate

area. The major types of these loans come under the category of mortgages in long term time

period. According to different surveys and figures, it is very evident that these organizations are

the biggest providers in the category of mortgage loans. They provide a great help to consumers

and hence, play a vital role in channelizing the movement of fund in the right direction in an

economical setup. At the present time, these organizations are specialised in providing the

intermediation service in the sector of maturity and denomination funds. This is due to the reason

that they are acquiring funds through borrowing process of money for a very short term period.

This borrowing is done through two major forms of accounts and they are checking and savings

account. They are lending money on long term in exchange of collateral of real estate. In the case

of thrift institutions, the FDIC insurance amount comes up the maximum limit of $250,000.

Credit unions

These are institutions which are operating on a small scale. These organisations are non

profit and working on cooperative organisational structure. These firms are consumer oriented

and are owned and operated completely by the members and customers of the firm (Mimir,

2016). The company has two major heads in the liabilities section and they are checking

accounts, often called as share drafts and second is savings account, called as share accounts.

These liabilities are basically devoted to only one thing and it is short term consumer loans.

These share accounts issued by the credit union are insured by the federal institution to the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maximum amount of $250,000. Credit unions are the organisations those are formed by

consumers having the value of common bond. To illustrate, common example of credit unions is

employees of a same firm, company or a firm. The main feature of this institution is that, to avail

services offered by them, it is essential to take membership (Santandrea and et al., 2018). The

evident difference between credit unions and every other institution in category of financial

intermediary is that members of credit unions should have common bond requirement, the

restriction that most loans are to consumers, and their exemption from federal income tax

because of their cooperative nature.

Investment funds

The main line of transaction of this intermediary is to sell shares to present investors in

the market and the funds received from the receipt of these sales is further used by the institution

to buy direct financial claims available in the market. The main feature of these institutions is

that they are offering the advantage of both facilities to investors, which are denomination

flexibility and default risk intermediation. Various types of investment funds are explained

below:

Mutual funds: These are the type of funds in which equity shares are sold out to investors

and the received fund is used to further purchase stocks and bonds. The benefit of these

institutions in comparison of direct investments is that they are attempting to provide

access to small investors for investment risk at low level. This benefit is resulted from

diversification, economies of scale in transaction cost and also professional managers.

The evident feature of these mutual funds is that the value of per share is usually not

fixed and it is fluctuating in response to change in price of the stock in the portfolio of

related investment. Mutual funds are specialized in the particular related sector of the

market place. To illustrate, perfect example is that some people are investing in equities

or debt, whereas, on the other hand, some are interested to invest in a particular industry,

example can be energy or electronics, others are seeking in growth or income stocks and

yet there are some who are interested only in foreign investments (Shahbazand et al.,

2018).

Money market mutual funds: It is a simply mutual fund that is taking active role in

investments in money market securities. The main feature of these securities is that they

are for short term and have very low default risk. These securities sell in denominations

8

consumers having the value of common bond. To illustrate, common example of credit unions is

employees of a same firm, company or a firm. The main feature of this institution is that, to avail

services offered by them, it is essential to take membership (Santandrea and et al., 2018). The

evident difference between credit unions and every other institution in category of financial

intermediary is that members of credit unions should have common bond requirement, the

restriction that most loans are to consumers, and their exemption from federal income tax

because of their cooperative nature.

Investment funds

The main line of transaction of this intermediary is to sell shares to present investors in

the market and the funds received from the receipt of these sales is further used by the institution

to buy direct financial claims available in the market. The main feature of these institutions is

that they are offering the advantage of both facilities to investors, which are denomination

flexibility and default risk intermediation. Various types of investment funds are explained

below:

Mutual funds: These are the type of funds in which equity shares are sold out to investors

and the received fund is used to further purchase stocks and bonds. The benefit of these

institutions in comparison of direct investments is that they are attempting to provide

access to small investors for investment risk at low level. This benefit is resulted from

diversification, economies of scale in transaction cost and also professional managers.

The evident feature of these mutual funds is that the value of per share is usually not

fixed and it is fluctuating in response to change in price of the stock in the portfolio of

related investment. Mutual funds are specialized in the particular related sector of the

market place. To illustrate, perfect example is that some people are investing in equities

or debt, whereas, on the other hand, some are interested to invest in a particular industry,

example can be energy or electronics, others are seeking in growth or income stocks and

yet there are some who are interested only in foreign investments (Shahbazand et al.,

2018).

Money market mutual funds: It is a simply mutual fund that is taking active role in

investments in money market securities. The main feature of these securities is that they

are for short term and have very low default risk. These securities sell in denominations

8

of $1 million or more, so most investors are unable to purchase them. Thus, MMMFs

provide investors with small money balances the opportunity to earn the market rate of

interest without incurring a great deal of financial risk (Agrawal and et al., 2016).

Finance corporations

They are defined as to make the loans for the customers and nominal enterprise. They

don’t allow saving amounts from customers, they looking forward for the majority of their

monetary value by selling short term tactics which is called as commercial documents to

shareholders or investors. The amount of their funds which is come from the sales equity and

long term debenture norms. There are various types of finance corporation which are consumer

finance organisation which specialized in instalment, taxes and household, enterprises finance

organisation which willing to acquire loan, property on lease to enterprises and sales finance

organisation that finance goods sold through the retailers. Finance companies are operated by the

states so in this they originate are also inform to many central guidelines. These terms and

conditions are focus on primarily on customer dealings and deal with loan relations, situations,

rates, and assortment practices.

Federal agencies

The government of United States act as a highly financial intermediary by the carrying

and lending activities of its companies, these agencies are highly growing of all financial

institutions. The main work of federal agencies to reduce the cost and it also enhances the

availability of amounts which support the organisation in financial aspects.

CONCLUSION

From the above report, it can be inferred that financial intermediaries are playing the very

important role in modern economy setup. They are acting as Lubricants that will help the

economy to keep going in the growth graph. The main role of financial intermediaries comes in

front when they have to reinvent every possible area so as to cater to every investor according to

their diverse portfolios and in alignment of their needs and wants. These financial institutions

have the responsibility of satisfying the needs of both borrowers and lenders so that there is a

proper balance stroke in the economy. The very term intermediary would suggest that these

institutions are pivotal to the working of the economy and they along with the monetary

authorities have to ensure that credit reaches to the needy without jeopardizing the interests of

the investors. This is one of the main challenges before them.

9

provide investors with small money balances the opportunity to earn the market rate of

interest without incurring a great deal of financial risk (Agrawal and et al., 2016).

Finance corporations

They are defined as to make the loans for the customers and nominal enterprise. They

don’t allow saving amounts from customers, they looking forward for the majority of their

monetary value by selling short term tactics which is called as commercial documents to

shareholders or investors. The amount of their funds which is come from the sales equity and

long term debenture norms. There are various types of finance corporation which are consumer

finance organisation which specialized in instalment, taxes and household, enterprises finance

organisation which willing to acquire loan, property on lease to enterprises and sales finance

organisation that finance goods sold through the retailers. Finance companies are operated by the

states so in this they originate are also inform to many central guidelines. These terms and

conditions are focus on primarily on customer dealings and deal with loan relations, situations,

rates, and assortment practices.

Federal agencies

The government of United States act as a highly financial intermediary by the carrying

and lending activities of its companies, these agencies are highly growing of all financial

institutions. The main work of federal agencies to reduce the cost and it also enhances the

availability of amounts which support the organisation in financial aspects.

CONCLUSION

From the above report, it can be inferred that financial intermediaries are playing the very

important role in modern economy setup. They are acting as Lubricants that will help the

economy to keep going in the growth graph. The main role of financial intermediaries comes in

front when they have to reinvent every possible area so as to cater to every investor according to

their diverse portfolios and in alignment of their needs and wants. These financial institutions

have the responsibility of satisfying the needs of both borrowers and lenders so that there is a

proper balance stroke in the economy. The very term intermediary would suggest that these

institutions are pivotal to the working of the economy and they along with the monetary

authorities have to ensure that credit reaches to the needy without jeopardizing the interests of

the investors. This is one of the main challenges before them.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Agrawal, and et al., 2016. Cost‐reducing innovation and the role of patent intermediaries in

increasing market efficiency. Production and Operations Management. 25(2). pp.173-

191.

Allen, and et al., 2018. Financial structure, economic growth and development. In Handbook of

finance and development. Edward Elgar Publishing.

Atta Arsanious, E., 2020. Investigating the Role of the Financial Intermediaries on Sustainable

Development in Egypt: An Empirical Evidence. Available at SSRN 3636281.

Boreiko, D. and Vidusso, G., 2019. New blockchain intermediaries: do ICO rating websites do

their job well? The Journal of Alternative Investments. 21(4). pp.67-79.

Chan, J.M., 2019. Financial frictions and trade intermediation: Theory and evidence. European

Economic Review. 119, pp.567-593.

Corrado, G. and Corrado, L., 2017. Inclusive finance for inclusive growth and development.

Current opinion in environmental sustainability. 24, pp.19-23.

Ferrarini, G., 2017. Understanding the role of corporate governance in financial institutions: A

research agenda. European Corporate Governance Institute (ECGI)-Law Working

Paper, (347).

Marini, and et al., 2018. Accountability practices in microfinance: cultural translation and the

role of intermediaries. Accounting, Auditing & Accountability Journal.

McLeod, and et al., 2018. Organizational virtue and stakeholder interdependence: An empirical

examination of financial intermediaries and IPO firms. Journal of Business Ethics.

149(4). pp.785-798.

Mimir, Y., 2016. Financial intermediaries, credit shocks and business cycles. Oxford Bulletin of

Economics and Statistics. 78(1). pp.42-74.

Santandrea, M., Agasisti, T., Giorgino, M. and Patrucco, A.S., 2018. Business models in the

search for efficiency: the case of public financial intermediaries. Public Money &

Management. 38(3), pp.234-243.

Shahbaz, and et al., 2018. Financial development, industrialization, the role of institutions and

government: a comparative analysis between India and China. Applied Economics.

50(17). pp.1952-1977.

11

Books and Journals

Agrawal, and et al., 2016. Cost‐reducing innovation and the role of patent intermediaries in

increasing market efficiency. Production and Operations Management. 25(2). pp.173-

191.

Allen, and et al., 2018. Financial structure, economic growth and development. In Handbook of

finance and development. Edward Elgar Publishing.

Atta Arsanious, E., 2020. Investigating the Role of the Financial Intermediaries on Sustainable

Development in Egypt: An Empirical Evidence. Available at SSRN 3636281.

Boreiko, D. and Vidusso, G., 2019. New blockchain intermediaries: do ICO rating websites do

their job well? The Journal of Alternative Investments. 21(4). pp.67-79.

Chan, J.M., 2019. Financial frictions and trade intermediation: Theory and evidence. European

Economic Review. 119, pp.567-593.

Corrado, G. and Corrado, L., 2017. Inclusive finance for inclusive growth and development.

Current opinion in environmental sustainability. 24, pp.19-23.

Ferrarini, G., 2017. Understanding the role of corporate governance in financial institutions: A

research agenda. European Corporate Governance Institute (ECGI)-Law Working

Paper, (347).

Marini, and et al., 2018. Accountability practices in microfinance: cultural translation and the

role of intermediaries. Accounting, Auditing & Accountability Journal.

McLeod, and et al., 2018. Organizational virtue and stakeholder interdependence: An empirical

examination of financial intermediaries and IPO firms. Journal of Business Ethics.

149(4). pp.785-798.

Mimir, Y., 2016. Financial intermediaries, credit shocks and business cycles. Oxford Bulletin of

Economics and Statistics. 78(1). pp.42-74.

Santandrea, M., Agasisti, T., Giorgino, M. and Patrucco, A.S., 2018. Business models in the

search for efficiency: the case of public financial intermediaries. Public Money &

Management. 38(3), pp.234-243.

Shahbaz, and et al., 2018. Financial development, industrialization, the role of institutions and

government: a comparative analysis between India and China. Applied Economics.

50(17). pp.1952-1977.

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.