Financial Markets

VerifiedAdded on 2022/11/25

|21

|3096

|420

AI Summary

This document discusses various topics related to financial markets, including yield rates, coupon rates, loanable funds market, and the impact of interest rates on exchange rates. It also provides calculations and analysis for investment options and risk management strategies. Explore the world of financial markets with Desklib.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL MARKETS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Q1.)

a) Yield rates in Europe have been negative and that of US have been positive. Positive yield

on treasury bonds signify that there has been a positive return on investment. However, it

may not be the case always as the central bank of US Fed does not cut rates below zero as its

policy rate is to stay positive. Yields on Treasury bonds going negative means there is a

supply crunch where cash is needed by companies and as US auction rules prevent rates

going below zero, the treasury bills can generate negative yields if traded in secondary

markets.

b) Coupon rate = central government bond yield + 1.86 p.a.

Central government bond yield rate for four year’s maturity = -0.74

Rate of coupon = -0.74 + 1.86 = 1.12% p.a.

Annual payment = 1000 * 1.12% = 11.2

Current market price of a bond = (2.3 / 1+4.5)1 + (11.2 / 1+4.5%)2 + (11.2 / 1+4.5%)3 +(11.2

/ 1+4.5%)4 + (8.4/1+4.5%)5

=35109.66

c) Change in demand for capital and Loanable funds market

It shows how an increase in demand by companies for capital can influence the market of

loanable funds. An increase in the technical improvement can increase the capital’s marginal

product, changing the capital’s demand curve. Firms are to give money for increase in capital

acquisition by asking for funds which are loanable and leading to rise in rate of interest. Thus, in

market capital’s demand is greater leading to higher interest rates (Guo and et.al.,. 2018).

Change in loanable funds market of loanable funds and capital demand

Second example can be when events in the market affect the capital firms hold. If customer

increase consumption which supplies less of funds at any rate of interest. Consumer preferences’

change affects the loanable funds’ supply.

d) Changes in rate of interest are to affect likely the rate of exchange as rate of interest, inflation

and exchange rates are highly related with each other. On manipulation of rate of interest, central

bank may influence over inflation and rate of exchange and interest rate change can affect

a) Yield rates in Europe have been negative and that of US have been positive. Positive yield

on treasury bonds signify that there has been a positive return on investment. However, it

may not be the case always as the central bank of US Fed does not cut rates below zero as its

policy rate is to stay positive. Yields on Treasury bonds going negative means there is a

supply crunch where cash is needed by companies and as US auction rules prevent rates

going below zero, the treasury bills can generate negative yields if traded in secondary

markets.

b) Coupon rate = central government bond yield + 1.86 p.a.

Central government bond yield rate for four year’s maturity = -0.74

Rate of coupon = -0.74 + 1.86 = 1.12% p.a.

Annual payment = 1000 * 1.12% = 11.2

Current market price of a bond = (2.3 / 1+4.5)1 + (11.2 / 1+4.5%)2 + (11.2 / 1+4.5%)3 +(11.2

/ 1+4.5%)4 + (8.4/1+4.5%)5

=35109.66

c) Change in demand for capital and Loanable funds market

It shows how an increase in demand by companies for capital can influence the market of

loanable funds. An increase in the technical improvement can increase the capital’s marginal

product, changing the capital’s demand curve. Firms are to give money for increase in capital

acquisition by asking for funds which are loanable and leading to rise in rate of interest. Thus, in

market capital’s demand is greater leading to higher interest rates (Guo and et.al.,. 2018).

Change in loanable funds market of loanable funds and capital demand

Second example can be when events in the market affect the capital firms hold. If customer

increase consumption which supplies less of funds at any rate of interest. Consumer preferences’

change affects the loanable funds’ supply.

d) Changes in rate of interest are to affect likely the rate of exchange as rate of interest, inflation

and exchange rates are highly related with each other. On manipulation of rate of interest, central

bank may influence over inflation and rate of exchange and interest rate change can affect

currency values. Higher interest rate give lenders a high return comparing with other countries. If

rate of interest is high, it can bring in foreign capital and increase the exchange rates. Impact of

interest rate being high is slowed if inflation in the country is high, comparing to others.

Opposite relation is existing for decrease in rates of interest which is lower rate of interest

influence to decrease rate of exchange.

Q2.)

i) It can be seen that Australia and New Zealand Banking Group have interest rate as 0.75%

which is on daily compounding basis. Thus, calculating the same, we get

Time period= 4 years= 4*365= 1460

Rate of interest=0.75%

Interest on one day= 0.75% of 15000= 112.5

Interest on whole time period= 112.5*1460= 164250

Total sum earned= 15000+164250=179250.00.

ii) If the interest is earned frequently in each year, it will add up to the investment horizon. This

is true that if interest is earned at a compounding rate of interest then it will add up to the amount

because at simple rate of interest one cannot get the amount as it is done only on the principal

and not the interest. In compounding rate of return, money will be compounded on the interest

earned daily and thus it will help in increasing the yield amount after the time period

(Macapinlac, 2018).

c) In this question, Compound Interest method can be used to calculate which option should be

suitable.

Formula for Amount= Principal*(1+r/100)^n

Here, Principal= Cash flow or earnings

R= compounding rate of interest

N= time period

Amount Calculation

rate of interest is high, it can bring in foreign capital and increase the exchange rates. Impact of

interest rate being high is slowed if inflation in the country is high, comparing to others.

Opposite relation is existing for decrease in rates of interest which is lower rate of interest

influence to decrease rate of exchange.

Q2.)

i) It can be seen that Australia and New Zealand Banking Group have interest rate as 0.75%

which is on daily compounding basis. Thus, calculating the same, we get

Time period= 4 years= 4*365= 1460

Rate of interest=0.75%

Interest on one day= 0.75% of 15000= 112.5

Interest on whole time period= 112.5*1460= 164250

Total sum earned= 15000+164250=179250.00.

ii) If the interest is earned frequently in each year, it will add up to the investment horizon. This

is true that if interest is earned at a compounding rate of interest then it will add up to the amount

because at simple rate of interest one cannot get the amount as it is done only on the principal

and not the interest. In compounding rate of return, money will be compounded on the interest

earned daily and thus it will help in increasing the yield amount after the time period

(Macapinlac, 2018).

c) In this question, Compound Interest method can be used to calculate which option should be

suitable.

Formula for Amount= Principal*(1+r/100)^n

Here, Principal= Cash flow or earnings

R= compounding rate of interest

N= time period

Amount Calculation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

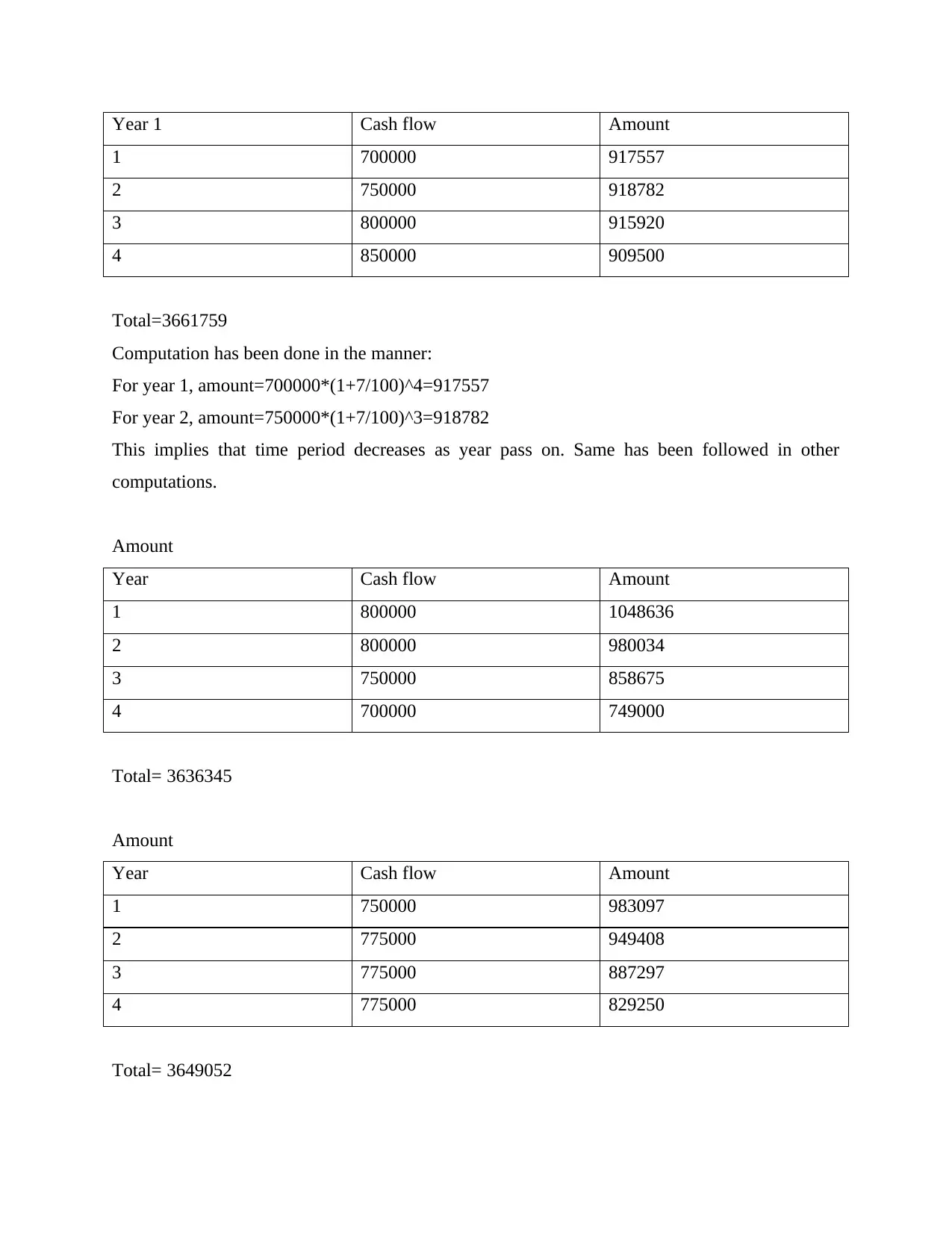

Year 1 Cash flow Amount

1 700000 917557

2 750000 918782

3 800000 915920

4 850000 909500

Total=3661759

Computation has been done in the manner:

For year 1, amount=700000*(1+7/100)^4=917557

For year 2, amount=750000*(1+7/100)^3=918782

This implies that time period decreases as year pass on. Same has been followed in other

computations.

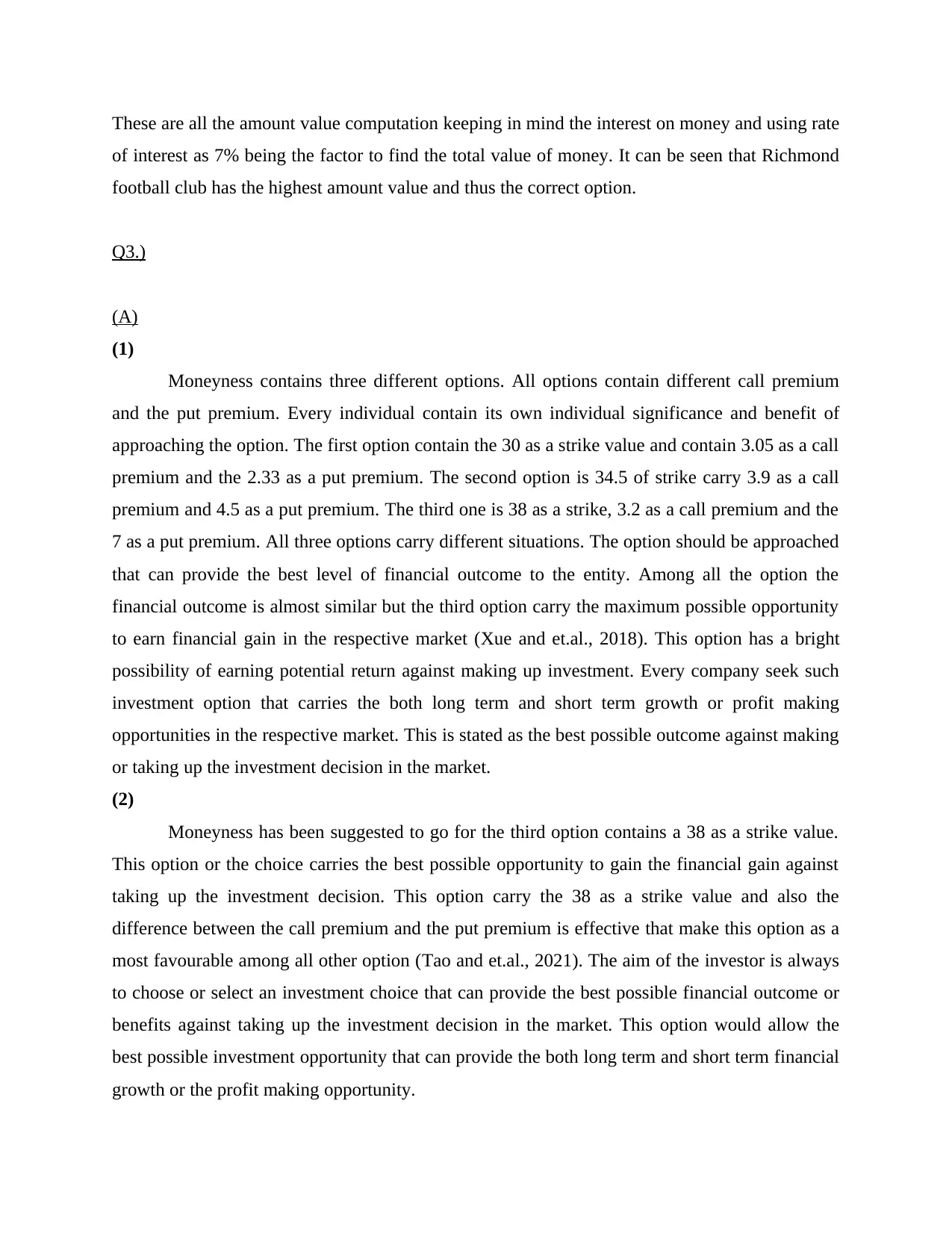

Amount

Year Cash flow Amount

1 800000 1048636

2 800000 980034

3 750000 858675

4 700000 749000

Total= 3636345

Amount

Year Cash flow Amount

1 750000 983097

2 775000 949408

3 775000 887297

4 775000 829250

Total= 3649052

1 700000 917557

2 750000 918782

3 800000 915920

4 850000 909500

Total=3661759

Computation has been done in the manner:

For year 1, amount=700000*(1+7/100)^4=917557

For year 2, amount=750000*(1+7/100)^3=918782

This implies that time period decreases as year pass on. Same has been followed in other

computations.

Amount

Year Cash flow Amount

1 800000 1048636

2 800000 980034

3 750000 858675

4 700000 749000

Total= 3636345

Amount

Year Cash flow Amount

1 750000 983097

2 775000 949408

3 775000 887297

4 775000 829250

Total= 3649052

These are all the amount value computation keeping in mind the interest on money and using rate

of interest as 7% being the factor to find the total value of money. It can be seen that Richmond

football club has the highest amount value and thus the correct option.

Q3.)

(A)

(1)

Moneyness contains three different options. All options contain different call premium

and the put premium. Every individual contain its own individual significance and benefit of

approaching the option. The first option contain the 30 as a strike value and contain 3.05 as a call

premium and the 2.33 as a put premium. The second option is 34.5 of strike carry 3.9 as a call

premium and 4.5 as a put premium. The third one is 38 as a strike, 3.2 as a call premium and the

7 as a put premium. All three options carry different situations. The option should be approached

that can provide the best level of financial outcome to the entity. Among all the option the

financial outcome is almost similar but the third option carry the maximum possible opportunity

to earn financial gain in the respective market (Xue and et.al., 2018). This option has a bright

possibility of earning potential return against making up investment. Every company seek such

investment option that carries the both long term and short term growth or profit making

opportunities in the respective market. This is stated as the best possible outcome against making

or taking up the investment decision in the market.

(2)

Moneyness has been suggested to go for the third option contains a 38 as a strike value.

This option or the choice carries the best possible opportunity to gain the financial gain against

taking up the investment decision. This option carry the 38 as a strike value and also the

difference between the call premium and the put premium is effective that make this option as a

most favourable among all other option (Tao and et.al., 2021). The aim of the investor is always

to choose or select an investment choice that can provide the best possible financial outcome or

benefits against taking up the investment decision in the market. This option would allow the

best possible investment opportunity that can provide the both long term and short term financial

growth or the profit making opportunity.

of interest as 7% being the factor to find the total value of money. It can be seen that Richmond

football club has the highest amount value and thus the correct option.

Q3.)

(A)

(1)

Moneyness contains three different options. All options contain different call premium

and the put premium. Every individual contain its own individual significance and benefit of

approaching the option. The first option contain the 30 as a strike value and contain 3.05 as a call

premium and the 2.33 as a put premium. The second option is 34.5 of strike carry 3.9 as a call

premium and 4.5 as a put premium. The third one is 38 as a strike, 3.2 as a call premium and the

7 as a put premium. All three options carry different situations. The option should be approached

that can provide the best level of financial outcome to the entity. Among all the option the

financial outcome is almost similar but the third option carry the maximum possible opportunity

to earn financial gain in the respective market (Xue and et.al., 2018). This option has a bright

possibility of earning potential return against making up investment. Every company seek such

investment option that carries the both long term and short term growth or profit making

opportunities in the respective market. This is stated as the best possible outcome against making

or taking up the investment decision in the market.

(2)

Moneyness has been suggested to go for the third option contains a 38 as a strike value.

This option or the choice carries the best possible opportunity to gain the financial gain against

taking up the investment decision. This option carry the 38 as a strike value and also the

difference between the call premium and the put premium is effective that make this option as a

most favourable among all other option (Tao and et.al., 2021). The aim of the investor is always

to choose or select an investment choice that can provide the best possible financial outcome or

benefits against taking up the investment decision in the market. This option would allow the

best possible investment opportunity that can provide the both long term and short term financial

growth or the profit making opportunity.

(3)

In case the 100000 shares are purchased than it would cost to 3800000. This is a huge

funds that would allow the company to gain a huge potential return against investing inn the

option. The huge investment always undertakes risk of financial loss. Stock market is totally

based on the financial risk that also contains opportunity to gain the financial profit or the return

against investing in the option.

B

(1)

Both the companies have done a investment choices for 9 months time. Even if the

options are selected for the 6 month time buy the tenure is 9 months. This would certainly cost

the interest based on the 9 months tenure. This involves the interest rate of .9% based on the term

and condition of the investment made. It can certainly demonstrated that the interst would be

allocated as a part of the agreement and would be deal by the both the companies engaged in the

contract.

(2)

Compensatory payment:

50000000 * .15% (.96% - .81%) * 9 / 12

= 56250

This would be allocated between both the parties involved in the contract. This would be

segregated into both the parties involved in the contract in against to undertake the financial risk.

Investment is always require to segregate the risk involve in the investment choice is made. This

can be done with support of strategic alliances or the contract made by the parties involved in the

agreement.

c)Derivatives to hedge risks of various types

Companies use a manoeuvre known as hedge which can lessen the risk which is involved in

interest rate risk. Hedge takes place when risk of interest rate gets decreased because of

implementing the derivative instrument. Derivative is instrument which has value got from other

assets. The assets can be stocks, currencies or bonds (Guo and et.al.,. 2018). If the Australian

mining company wants to remove the interest rate risk, company needs implementation of

perfect hedge with a type of derivative instrument. Example of instruments which can be used by

In case the 100000 shares are purchased than it would cost to 3800000. This is a huge

funds that would allow the company to gain a huge potential return against investing inn the

option. The huge investment always undertakes risk of financial loss. Stock market is totally

based on the financial risk that also contains opportunity to gain the financial profit or the return

against investing in the option.

B

(1)

Both the companies have done a investment choices for 9 months time. Even if the

options are selected for the 6 month time buy the tenure is 9 months. This would certainly cost

the interest based on the 9 months tenure. This involves the interest rate of .9% based on the term

and condition of the investment made. It can certainly demonstrated that the interst would be

allocated as a part of the agreement and would be deal by the both the companies engaged in the

contract.

(2)

Compensatory payment:

50000000 * .15% (.96% - .81%) * 9 / 12

= 56250

This would be allocated between both the parties involved in the contract. This would be

segregated into both the parties involved in the contract in against to undertake the financial risk.

Investment is always require to segregate the risk involve in the investment choice is made. This

can be done with support of strategic alliances or the contract made by the parties involved in the

agreement.

c)Derivatives to hedge risks of various types

Companies use a manoeuvre known as hedge which can lessen the risk which is involved in

interest rate risk. Hedge takes place when risk of interest rate gets decreased because of

implementing the derivative instrument. Derivative is instrument which has value got from other

assets. The assets can be stocks, currencies or bonds (Guo and et.al.,. 2018). If the Australian

mining company wants to remove the interest rate risk, company needs implementation of

perfect hedge with a type of derivative instrument. Example of instruments which can be used by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company for combating interest rate risk are forward rate agreements, futures and option

contracts, interest rate swaps etc.

Forward rate agreements

Company can make use of the forward rate agreement for reducing interest rate risk by coming

in a contract with other party for buying commodity. This contract goes into effect in a future

date with price agreed on making contract. Thus, hedging against the risk can be done by

engaging in this instrument where an investor wants to see on the interest rate while purchasing

the bond simultaneously.

Future contracts

Futures is used when a product is a stock exchange traded contract made between parties. In case

of the Australian company a risk is there that market factors can reduce bond’s value and thus

through this instrument risk can be hedged by getting in a future contract with investor

(Hernández and Benavides, 2019).

To confront the exchange rate risk, currency swap is the financial instrument or derivative which

can be used to mitigate the risk. It has involvement of interest exchange in a currency for same in

another one.

It may be used by the mining company where currency swaps can be used. They consist of two

principals which are exchanged in starting and agreement’s end. The principals are amount

already determined on which the exchange interest payment is based. Principal here is only used

as a base for calculating the interest rate payments.

For dealing with oil rate risk, purchase of current oil contracts helps serve as a derivative for risk

mitigation. Purchase of call option is another derivative which gives buyer right to make

purchase of a commodity on a given price and a given date. If company buys a call option, it

shall mean buying the right for purchasing oil in future at a price agreed on today.

contracts, interest rate swaps etc.

Forward rate agreements

Company can make use of the forward rate agreement for reducing interest rate risk by coming

in a contract with other party for buying commodity. This contract goes into effect in a future

date with price agreed on making contract. Thus, hedging against the risk can be done by

engaging in this instrument where an investor wants to see on the interest rate while purchasing

the bond simultaneously.

Future contracts

Futures is used when a product is a stock exchange traded contract made between parties. In case

of the Australian company a risk is there that market factors can reduce bond’s value and thus

through this instrument risk can be hedged by getting in a future contract with investor

(Hernández and Benavides, 2019).

To confront the exchange rate risk, currency swap is the financial instrument or derivative which

can be used to mitigate the risk. It has involvement of interest exchange in a currency for same in

another one.

It may be used by the mining company where currency swaps can be used. They consist of two

principals which are exchanged in starting and agreement’s end. The principals are amount

already determined on which the exchange interest payment is based. Principal here is only used

as a base for calculating the interest rate payments.

For dealing with oil rate risk, purchase of current oil contracts helps serve as a derivative for risk

mitigation. Purchase of call option is another derivative which gives buyer right to make

purchase of a commodity on a given price and a given date. If company buys a call option, it

shall mean buying the right for purchasing oil in future at a price agreed on today.

Q4.)

A

On 7th April Fitch rating downgrade the Australia is 4 biggest bank credit rating. This

simply means that I'm the credit rating of the banks have decreased and this will affect the

borrower was lenders and the financial institutions to a great extent. This is pertaining to the fact

that if the credit rating will not be good than the borrower was will not borrow the money from

that Bank. Hence this will reduce the operational value of the bank as there will not be more

people taking loan from the bank. The lender that is the bank will also be affected to a great

extent. The reason pertaining to the fact is that when there will not be any borrower then the

lenders will also be not having the people to lend the money (Torre-Torres, Galeana-Figueroa

and Álvarez-García, 2021). Hence the operational cycle of the bank will be affected to a great

extent. in against of this The financial institutions will be affected in the positive manner. The

reason underlying this fact is that when banks credit rating will be lower than the people will go

to other financial institutions to take loans. Hence this will improve the operational capacity of

the financial institutions. The major implication of the downgrade to the health of the financial

system will be that now the people will not prefer to go to those banks in order to take loans.

Hence in case the biggest bank of Australia will be downgraded then this will affect the whole

financial system and its effective working.

B

i

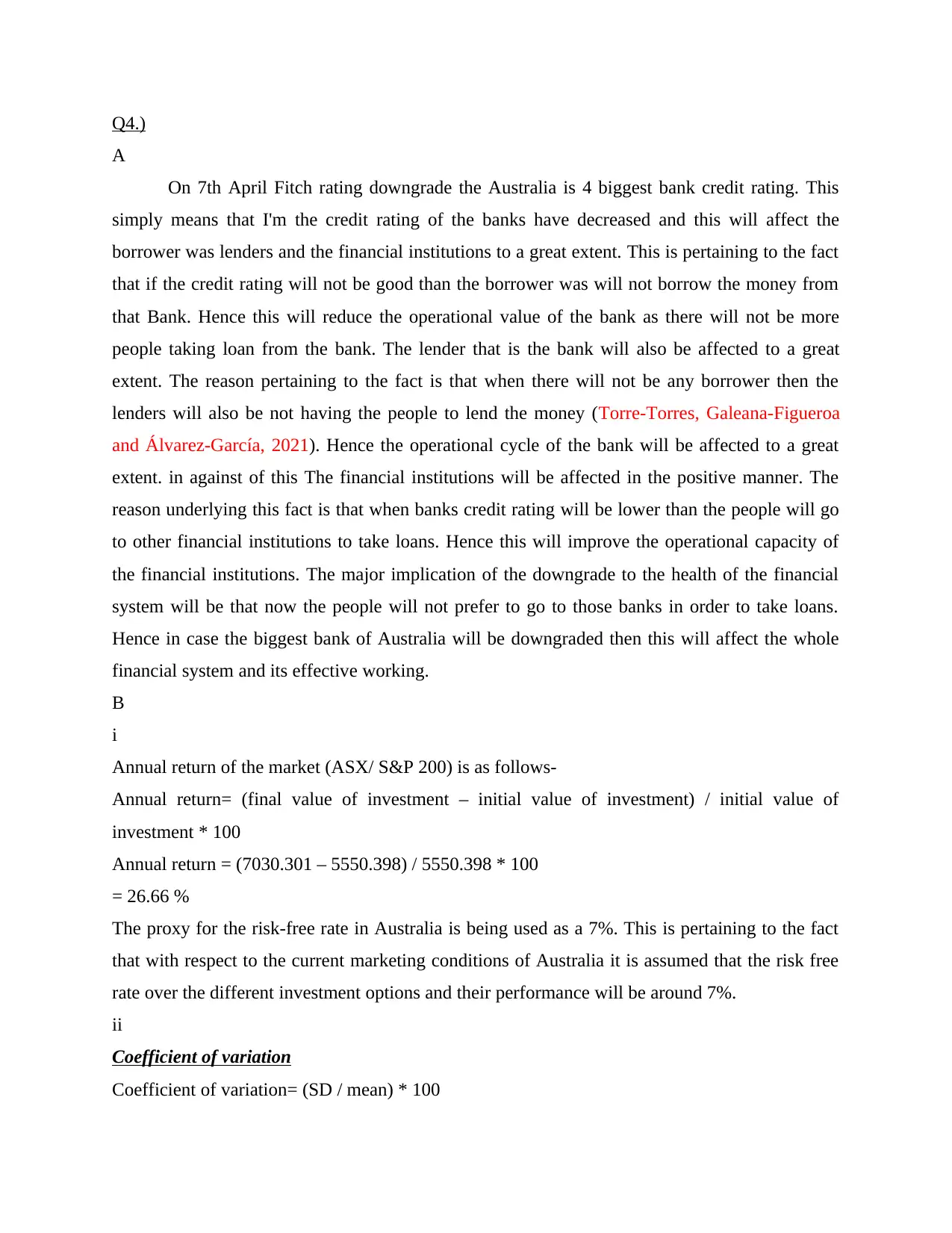

Annual return of the market (ASX/ S&P 200) is as follows-

Annual return= (final value of investment – initial value of investment) / initial value of

investment * 100

Annual return = (7030.301 – 5550.398) / 5550.398 * 100

= 26.66 %

The proxy for the risk-free rate in Australia is being used as a 7%. This is pertaining to the fact

that with respect to the current marketing conditions of Australia it is assumed that the risk free

rate over the different investment options and their performance will be around 7%.

ii

Coefficient of variation

Coefficient of variation= (SD / mean) * 100

A

On 7th April Fitch rating downgrade the Australia is 4 biggest bank credit rating. This

simply means that I'm the credit rating of the banks have decreased and this will affect the

borrower was lenders and the financial institutions to a great extent. This is pertaining to the fact

that if the credit rating will not be good than the borrower was will not borrow the money from

that Bank. Hence this will reduce the operational value of the bank as there will not be more

people taking loan from the bank. The lender that is the bank will also be affected to a great

extent. The reason pertaining to the fact is that when there will not be any borrower then the

lenders will also be not having the people to lend the money (Torre-Torres, Galeana-Figueroa

and Álvarez-García, 2021). Hence the operational cycle of the bank will be affected to a great

extent. in against of this The financial institutions will be affected in the positive manner. The

reason underlying this fact is that when banks credit rating will be lower than the people will go

to other financial institutions to take loans. Hence this will improve the operational capacity of

the financial institutions. The major implication of the downgrade to the health of the financial

system will be that now the people will not prefer to go to those banks in order to take loans.

Hence in case the biggest bank of Australia will be downgraded then this will affect the whole

financial system and its effective working.

B

i

Annual return of the market (ASX/ S&P 200) is as follows-

Annual return= (final value of investment – initial value of investment) / initial value of

investment * 100

Annual return = (7030.301 – 5550.398) / 5550.398 * 100

= 26.66 %

The proxy for the risk-free rate in Australia is being used as a 7%. This is pertaining to the fact

that with respect to the current marketing conditions of Australia it is assumed that the risk free

rate over the different investment options and their performance will be around 7%.

ii

Coefficient of variation

Coefficient of variation= (SD / mean) * 100

Fund SD Mean Coefficient of

variation

Fund A 10.75 24.61 44.22

Fund B 14.82 24.61 60.22

Fund C 12.33 24.61 50.11

Sharpe and Jensen indices of performance

Sharpe ratio= PR – RFR/ SD

Where,

PR = portfolio return

RFR = risk free rate

SD = Standard deviation

Fund PR RFR SD Sharpe ratio

Fund A 19.50 7 10.75 1.16

Fund B 28.65 7 14.82 1.46

Fund C 25.70 7 12.33 1.51

Jensen measure

Jensen alpha= PR – CAPM

Where,

PR = portfolio return

CAPM = risk free rate + β (return of market risk- free rate of return

Fund PR Risk free rate Beta Jensen indices

Fund A 19.50 7 0.873 11.627

Fund B 28.65 7 1.251 20.399

Fund C 25.70 7 1.005 17.695

C

The colonial first state wholesale imputation fund is a type of fund which provides

investors with exposure to Australian equity ISM which are having the possibility of resulting in

capital growth for linger period of time and increase in tax income with help of dividend

variation

Fund A 10.75 24.61 44.22

Fund B 14.82 24.61 60.22

Fund C 12.33 24.61 50.11

Sharpe and Jensen indices of performance

Sharpe ratio= PR – RFR/ SD

Where,

PR = portfolio return

RFR = risk free rate

SD = Standard deviation

Fund PR RFR SD Sharpe ratio

Fund A 19.50 7 10.75 1.16

Fund B 28.65 7 14.82 1.46

Fund C 25.70 7 12.33 1.51

Jensen measure

Jensen alpha= PR – CAPM

Where,

PR = portfolio return

CAPM = risk free rate + β (return of market risk- free rate of return

Fund PR Risk free rate Beta Jensen indices

Fund A 19.50 7 0.873 11.627

Fund B 28.65 7 1.251 20.399

Fund C 25.70 7 1.005 17.695

C

The colonial first state wholesale imputation fund is a type of fund which provides

investors with exposure to Australian equity ISM which are having the possibility of resulting in

capital growth for linger period of time and increase in tax income with help of dividend

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

payment method (Trinks and et.al., 2018). The major objective of this fund is to provide long-

term capital growth including some tax effective income. The main aim of this fund is to perform

better than the ASX 300/ S&P accumulation index..

In against of this the Vanguard emerging market share index fund is a type of fund which

results in tracking up the return relating to the MSCI within the emerging market index. This

type of fund provides a exposure relating to low cost which listed company within the emerging

market. This allows the investor to participate within the long-term potential investment options.

In addition to this type of fund results in different values which frequently fluctuates depending

on the foreign exchange currency.

The risk involved within the colonial first state wholesale imputation fund is high. In

against of this the risk involved within the Vanguard emerging market share index fund is

comparatively low.

In against of this the colonial first state imputation fund is suitable for the investors who

are looking for straight forward returns which are subject to investment risk which can include

the loss of income and capital as well (Mohamadi, Mohamadi and Esmaili Kia, 2021). In contrast

to this the Vanguard emerging market stock index fund is appropriate for different types of

investors which have the objective of returns benefitting for longer term. This also involves high

degree of risk tolerance capability within the person so that they can have high exposure to high

gains.

term capital growth including some tax effective income. The main aim of this fund is to perform

better than the ASX 300/ S&P accumulation index..

In against of this the Vanguard emerging market share index fund is a type of fund which

results in tracking up the return relating to the MSCI within the emerging market index. This

type of fund provides a exposure relating to low cost which listed company within the emerging

market. This allows the investor to participate within the long-term potential investment options.

In addition to this type of fund results in different values which frequently fluctuates depending

on the foreign exchange currency.

The risk involved within the colonial first state wholesale imputation fund is high. In

against of this the risk involved within the Vanguard emerging market share index fund is

comparatively low.

In against of this the colonial first state imputation fund is suitable for the investors who

are looking for straight forward returns which are subject to investment risk which can include

the loss of income and capital as well (Mohamadi, Mohamadi and Esmaili Kia, 2021). In contrast

to this the Vanguard emerging market stock index fund is appropriate for different types of

investors which have the objective of returns benefitting for longer term. This also involves high

degree of risk tolerance capability within the person so that they can have high exposure to high

gains.

REFERENCES

Books and journals

Guo, J., Gang, J., Hu, N. and Utham, V., 2018. The role of derivatives in hedge fund

activism. Quantitative finance, 18(9), pp.1531-1541.

Hernández, W. and Benavides, J.B., 2019. A new perspective for the use of financial derivatives

to hedge foreign exchange rate: L-BFGS perspective to assess the strikes and principals

of plain vanilla options. Revista Activos, 17(2), pp.159-175.

Macapinlac, R., 2018. Analyzing Financial Markets.

Elwood, S.K., 2017. Accounting For Asymmetric Information And Screening In Market Models

Of The Loanable Funds And Labor Markets. Journal for Economic Educators, 17(1),

pp.14-24.

Torre-Torres, O.V., Galeana-Figueroa, E. and Álvarez-García, J., 2021. A Markov-Switching

VSTOXX Trading Algorithm for Enhancing EUR Stock Portfolio Performance.

Mathematics, 9(9), p.1030.

Trinks, A., and et.al., 2018. Fossil fuel divestment and portfolio performance. Ecological

economics, 146, pp.740-748.

Mohamadi, Y., Mohamadi, A. and Esmaili Kia, G., 2021. The Effect of Macroeconomic

Variables on Stock Portfolio Performance Based on Traditional and Modern Network.

Advances in Mathematical Finance and Applications, 6(3), pp.1-25.

Books and journals

Guo, J., Gang, J., Hu, N. and Utham, V., 2018. The role of derivatives in hedge fund

activism. Quantitative finance, 18(9), pp.1531-1541.

Hernández, W. and Benavides, J.B., 2019. A new perspective for the use of financial derivatives

to hedge foreign exchange rate: L-BFGS perspective to assess the strikes and principals

of plain vanilla options. Revista Activos, 17(2), pp.159-175.

Macapinlac, R., 2018. Analyzing Financial Markets.

Elwood, S.K., 2017. Accounting For Asymmetric Information And Screening In Market Models

Of The Loanable Funds And Labor Markets. Journal for Economic Educators, 17(1),

pp.14-24.

Torre-Torres, O.V., Galeana-Figueroa, E. and Álvarez-García, J., 2021. A Markov-Switching

VSTOXX Trading Algorithm for Enhancing EUR Stock Portfolio Performance.

Mathematics, 9(9), p.1030.

Trinks, A., and et.al., 2018. Fossil fuel divestment and portfolio performance. Ecological

economics, 146, pp.740-748.

Mohamadi, Y., Mohamadi, A. and Esmaili Kia, G., 2021. The Effect of Macroeconomic

Variables on Stock Portfolio Performance Based on Traditional and Modern Network.

Advances in Mathematical Finance and Applications, 6(3), pp.1-25.

Tao, Z. and et.al., 2021. Review and analysis of investment decision making algorithms in long-

term agent-based electric power system simulation models. Renewable and Sustainable

Energy Reviews. 136. p.110405.

Xue, W. and et.al., 2018. Pythagorean fuzzy LINMAP method based on the entropy theory for

railway project investment decision making. International Journal of Intelligent

Systems. 33(1). pp.93-125.

term agent-based electric power system simulation models. Renewable and Sustainable

Energy Reviews. 136. p.110405.

Xue, W. and et.al., 2018. Pythagorean fuzzy LINMAP method based on the entropy theory for

railway project investment decision making. International Journal of Intelligent

Systems. 33(1). pp.93-125.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

3

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.