Essay on Time Value of Money and Retirement Planning

VerifiedAdded on 2023/06/12

|17

|3485

|378

AI Summary

This essay explains the concept of time value of money and its importance in financial decisions. It also discusses retirement planning and investment options for accumulating funds. The essay covers topics such as discounting and compounding techniques, valuation of financial instruments, and capital budgeting decisions. The investment options for retirement planning are evaluated and compared. Course code BAO 5534 Business Finance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BAO 5534 BUSINESS FINANCE

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task-1: Essay on Time Value of Money

The concept of time value of money is the basic premise of financial decisions. The

concept of time value of money confers that the value of money reduces with the efflux of time.

This means that the value of one dollar today will not be the same after 1 year from today (Drake

and Fabozzi, 2009). The purchasing power of one dollar today will reduce over the period of

time due to inflation and other economic changes. For example, a man who bought suppose one

KG bananas in one dollar today would not be able to do so after one year. After one year he

might has to pay 1.5 dollar to buy one kg bananas. The consideration of time value of money is

of utmost importance in the financial decisions. If a firm deciding on to invest in a project does

not consider the time value of money, it will end up evaluating the project’s financial viability in

wrong way (Drake and Fabozzi, 2009).

There are four basic factors which lead the consideration of time value of money concept.

These four factors are risk and uncertainty, inflation, consumption, and investment opportunity.

It is important to consider the risk and uncertainty involved in an investment decision (Silver,

2011). As the future is uncertain and hence the receipt of cash flows can not be guaranteed with

certainty, therefore, the firm makes provision for this uncertainty by adjusting the discount rate.

The inflation refers to increase in the price of goods and services over the period of one year.

The increase in the price of goods and services affects the cash flows of a firm and hence it is

important to consider inflation when assessing financial viability of the project. The discount rate

is further adjusted on account of inflation after being adjusted for risk and uncertainty (Silver,

2011).

2

The concept of time value of money is the basic premise of financial decisions. The

concept of time value of money confers that the value of money reduces with the efflux of time.

This means that the value of one dollar today will not be the same after 1 year from today (Drake

and Fabozzi, 2009). The purchasing power of one dollar today will reduce over the period of

time due to inflation and other economic changes. For example, a man who bought suppose one

KG bananas in one dollar today would not be able to do so after one year. After one year he

might has to pay 1.5 dollar to buy one kg bananas. The consideration of time value of money is

of utmost importance in the financial decisions. If a firm deciding on to invest in a project does

not consider the time value of money, it will end up evaluating the project’s financial viability in

wrong way (Drake and Fabozzi, 2009).

There are four basic factors which lead the consideration of time value of money concept.

These four factors are risk and uncertainty, inflation, consumption, and investment opportunity.

It is important to consider the risk and uncertainty involved in an investment decision (Silver,

2011). As the future is uncertain and hence the receipt of cash flows can not be guaranteed with

certainty, therefore, the firm makes provision for this uncertainty by adjusting the discount rate.

The inflation refers to increase in the price of goods and services over the period of one year.

The increase in the price of goods and services affects the cash flows of a firm and hence it is

important to consider inflation when assessing financial viability of the project. The discount rate

is further adjusted on account of inflation after being adjusted for risk and uncertainty (Silver,

2011).

2

Consumption and investment opportunity leads encourages a person to receive money

today rather than tomorrow. The person would always prefer to consume today rather than

consuming tomorrow. Further, the dollar money received today could be invested to earn income

for the future (Halpin and Senior, 2011). Thus, a person receiving money in future would like

have incentive or some extra charge. For example, a person receiving $100 today would not like

to defer this payment for one year if he does not receive anything greater than $100. If the person

defers the payment of $100 for one year, he would be deprived of consumption of goods or

services which he could have availed by utilizing $100 today. He would also loose opportunity to

invest money. So, he would be happy to defer it if say the payment after one year becomes $110.

In such a case, there would be some incentive to the person deferring payment for one year

(Halpin and Senior, 2011).

There are two techniques being emerged from the concept of time value of money

namely discounting and compounding. Discounting refers to bringing the value of money to be

received in future to the present times while compounding means determining the future value of

money (Baker and English, 2011). An example of discounting technique:

Value of $100 receivable after one year at discount rate of 10% would be $90.90. This is

arrived at as under:

PV = FV/(1+r)t

Here, PV = Present value

FV = Future value

R = Rate of discount

3

today rather than tomorrow. The person would always prefer to consume today rather than

consuming tomorrow. Further, the dollar money received today could be invested to earn income

for the future (Halpin and Senior, 2011). Thus, a person receiving money in future would like

have incentive or some extra charge. For example, a person receiving $100 today would not like

to defer this payment for one year if he does not receive anything greater than $100. If the person

defers the payment of $100 for one year, he would be deprived of consumption of goods or

services which he could have availed by utilizing $100 today. He would also loose opportunity to

invest money. So, he would be happy to defer it if say the payment after one year becomes $110.

In such a case, there would be some incentive to the person deferring payment for one year

(Halpin and Senior, 2011).

There are two techniques being emerged from the concept of time value of money

namely discounting and compounding. Discounting refers to bringing the value of money to be

received in future to the present times while compounding means determining the future value of

money (Baker and English, 2011). An example of discounting technique:

Value of $100 receivable after one year at discount rate of 10% would be $90.90. This is

arrived at as under:

PV = FV/(1+r)t

Here, PV = Present value

FV = Future value

R = Rate of discount

3

= 100/(1+.10)1

= 90.90

On the other hand, if we calculate let say value of $100 invested at the rate of 10% after

one year, it would amount to $110, this is called compounded value. This value has been arrived

at as under:

Fv = PV (1+r)n

= 100(1+.10)1

= $110

In capital budgeting decisions, the discounting technique is used instead of compounding.

The discounting technique provides computation of the present value of future cash flows which

is compared with the investment amount to arrive at the decision. The compounding technique in

the capital budgeting decisions can not be applied as it would be difficult to determine the rate of

return that the project would generate over the period of time. However, the future cash inflows

can be estimated with reliability. With the help of discounting technique, the present value of the

future cash flows can be determined (Shapiro, 2008).

It is to be noted that a discount rate is used in computing the present value of future cash

flows. This discount rate is determined having regards to the investor’s desired rate of return

(Shapiro, 2008). The discount rate could also be said to be the approximation to the cost of

capital of the firm. A firm may use its weighted average cost of capital as the discount rate. The

weighted average cost of capital of the firm comprises the cost of different components of the

capital such as equity, debt, and preference shares. In an all equity firm, the CAPM return could

4

= 90.90

On the other hand, if we calculate let say value of $100 invested at the rate of 10% after

one year, it would amount to $110, this is called compounded value. This value has been arrived

at as under:

Fv = PV (1+r)n

= 100(1+.10)1

= $110

In capital budgeting decisions, the discounting technique is used instead of compounding.

The discounting technique provides computation of the present value of future cash flows which

is compared with the investment amount to arrive at the decision. The compounding technique in

the capital budgeting decisions can not be applied as it would be difficult to determine the rate of

return that the project would generate over the period of time. However, the future cash inflows

can be estimated with reliability. With the help of discounting technique, the present value of the

future cash flows can be determined (Shapiro, 2008).

It is to be noted that a discount rate is used in computing the present value of future cash

flows. This discount rate is determined having regards to the investor’s desired rate of return

(Shapiro, 2008). The discount rate could also be said to be the approximation to the cost of

capital of the firm. A firm may use its weighted average cost of capital as the discount rate. The

weighted average cost of capital of the firm comprises the cost of different components of the

capital such as equity, debt, and preference shares. In an all equity firm, the CAPM return could

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

also provide an approximation of the discount rate. However, whatever method is used in

computing the discount rate, a further adjustment for the risk and inflation is required. The

discount rate must incorporate risk and it should be adjusted for inflation. Further, it may be

noted that the discount rate would change from project to project because of change in the risk of

different projects (Shapiro, 2008).

There is immense use of the concept of time value of money in the valuation of the

financial instruments. All the financial instruments such as equity shares, preferences shares,

bonds and debentures are valued by discounting the future income flowing from the investment.

The equity shares are valued with reference to the discounted value of expected dividend

payments over the period (Shim and Siegel, 2008). According to the dividend discount model,

the value of an equity share can be computed by the following formula:

po = D0*(1+g)/(Ke-g)

Where,

Do = Current dividend

Ke = Cost of equity

G = growth rate

Thus, it could be observed that the value of equity shares is computed by discounting the

future dividend with the discount rate which is cost of equity in this case. The current dividend

(D0) is multiplied by the growth rate to compute the future dividend and discounting is applied

on this figure to get the value of share as on today.

5

computing the discount rate, a further adjustment for the risk and inflation is required. The

discount rate must incorporate risk and it should be adjusted for inflation. Further, it may be

noted that the discount rate would change from project to project because of change in the risk of

different projects (Shapiro, 2008).

There is immense use of the concept of time value of money in the valuation of the

financial instruments. All the financial instruments such as equity shares, preferences shares,

bonds and debentures are valued by discounting the future income flowing from the investment.

The equity shares are valued with reference to the discounted value of expected dividend

payments over the period (Shim and Siegel, 2008). According to the dividend discount model,

the value of an equity share can be computed by the following formula:

po = D0*(1+g)/(Ke-g)

Where,

Do = Current dividend

Ke = Cost of equity

G = growth rate

Thus, it could be observed that the value of equity shares is computed by discounting the

future dividend with the discount rate which is cost of equity in this case. The current dividend

(D0) is multiplied by the growth rate to compute the future dividend and discounting is applied

on this figure to get the value of share as on today.

5

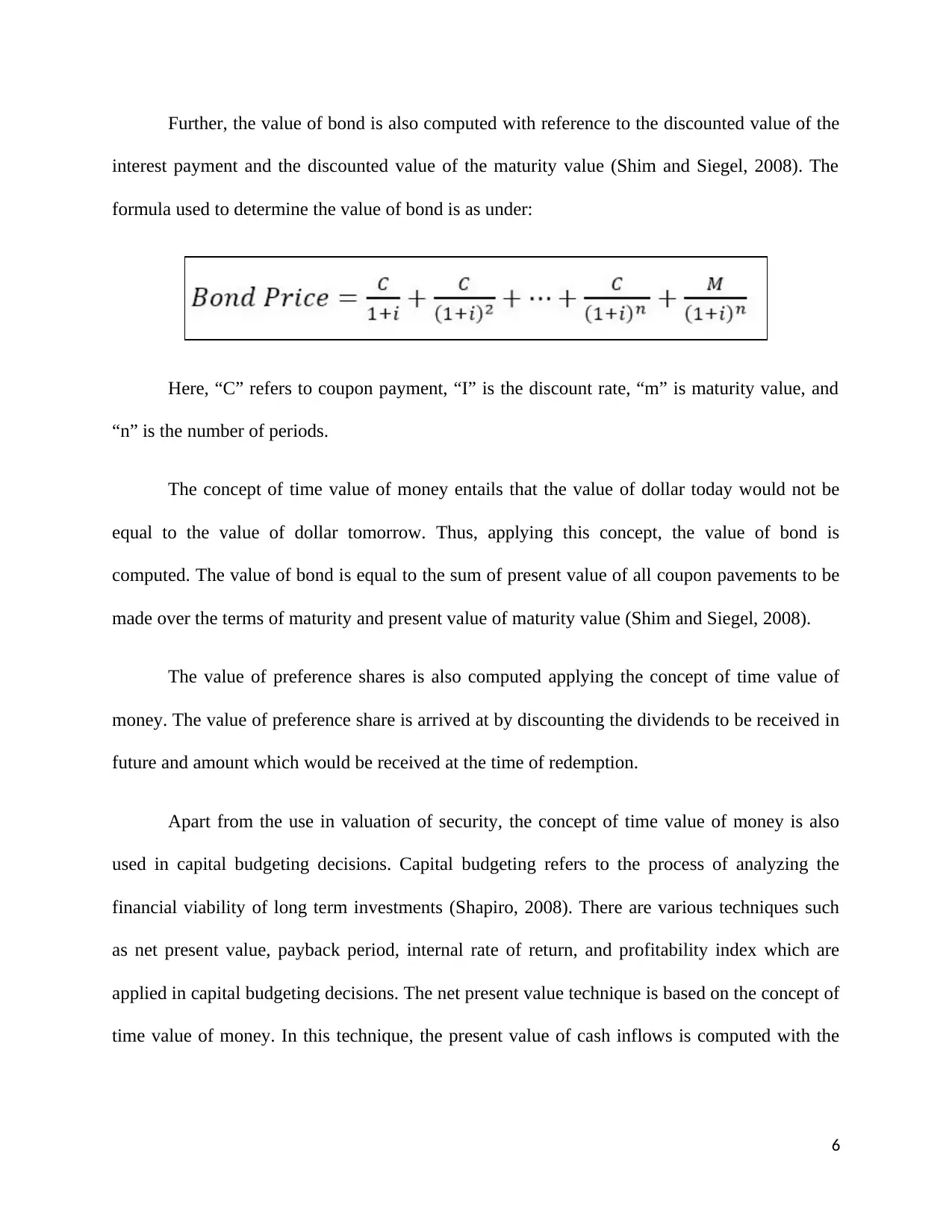

Further, the value of bond is also computed with reference to the discounted value of the

interest payment and the discounted value of the maturity value (Shim and Siegel, 2008). The

formula used to determine the value of bond is as under:

Here, “C” refers to coupon payment, “I” is the discount rate, “m” is maturity value, and

“n” is the number of periods.

The concept of time value of money entails that the value of dollar today would not be

equal to the value of dollar tomorrow. Thus, applying this concept, the value of bond is

computed. The value of bond is equal to the sum of present value of all coupon pavements to be

made over the terms of maturity and present value of maturity value (Shim and Siegel, 2008).

The value of preference shares is also computed applying the concept of time value of

money. The value of preference share is arrived at by discounting the dividends to be received in

future and amount which would be received at the time of redemption.

Apart from the use in valuation of security, the concept of time value of money is also

used in capital budgeting decisions. Capital budgeting refers to the process of analyzing the

financial viability of long term investments (Shapiro, 2008). There are various techniques such

as net present value, payback period, internal rate of return, and profitability index which are

applied in capital budgeting decisions. The net present value technique is based on the concept of

time value of money. In this technique, the present value of cash inflows is computed with the

6

interest payment and the discounted value of the maturity value (Shim and Siegel, 2008). The

formula used to determine the value of bond is as under:

Here, “C” refers to coupon payment, “I” is the discount rate, “m” is maturity value, and

“n” is the number of periods.

The concept of time value of money entails that the value of dollar today would not be

equal to the value of dollar tomorrow. Thus, applying this concept, the value of bond is

computed. The value of bond is equal to the sum of present value of all coupon pavements to be

made over the terms of maturity and present value of maturity value (Shim and Siegel, 2008).

The value of preference shares is also computed applying the concept of time value of

money. The value of preference share is arrived at by discounting the dividends to be received in

future and amount which would be received at the time of redemption.

Apart from the use in valuation of security, the concept of time value of money is also

used in capital budgeting decisions. Capital budgeting refers to the process of analyzing the

financial viability of long term investments (Shapiro, 2008). There are various techniques such

as net present value, payback period, internal rate of return, and profitability index which are

applied in capital budgeting decisions. The net present value technique is based on the concept of

time value of money. In this technique, the present value of cash inflows is computed with the

6

application of discount rate. The value of initial investment is deducted from the total present

value of cash inflows and result is known as net present value (Shapiro, 2008).

The discount rate is determined with reference to different parameters in different

situations. In one case, the discount rate may be determined with reference to the borrowing rate

and another it may be determined with reference to the cost of equity. Further, the discount rate

is adjusted for the risk premium and inflation effect. The higher the risk higher will be the

discount rate and higher the discount rate lower will be the present value. The discounting of

cash flows is done only after adjusting the discount rate with the risk premium and inflation

(Shapiro, 2008).

Therefore, it may be concluded from the overall discussion that the concept of time value

of money forms the basic premise of the financial management. The crucial financial

management decisions involving capital budgeting and investment decisions are based on the

concept of time value of money. The application of time value of money concept is wide spread

from valuation of securities to the investment in plant and machinery.

7

value of cash inflows and result is known as net present value (Shapiro, 2008).

The discount rate is determined with reference to different parameters in different

situations. In one case, the discount rate may be determined with reference to the borrowing rate

and another it may be determined with reference to the cost of equity. Further, the discount rate

is adjusted for the risk premium and inflation effect. The higher the risk higher will be the

discount rate and higher the discount rate lower will be the present value. The discounting of

cash flows is done only after adjusting the discount rate with the risk premium and inflation

(Shapiro, 2008).

Therefore, it may be concluded from the overall discussion that the concept of time value

of money forms the basic premise of the financial management. The crucial financial

management decisions involving capital budgeting and investment decisions are based on the

concept of time value of money. The application of time value of money concept is wide spread

from valuation of securities to the investment in plant and machinery.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part-2

Question-1

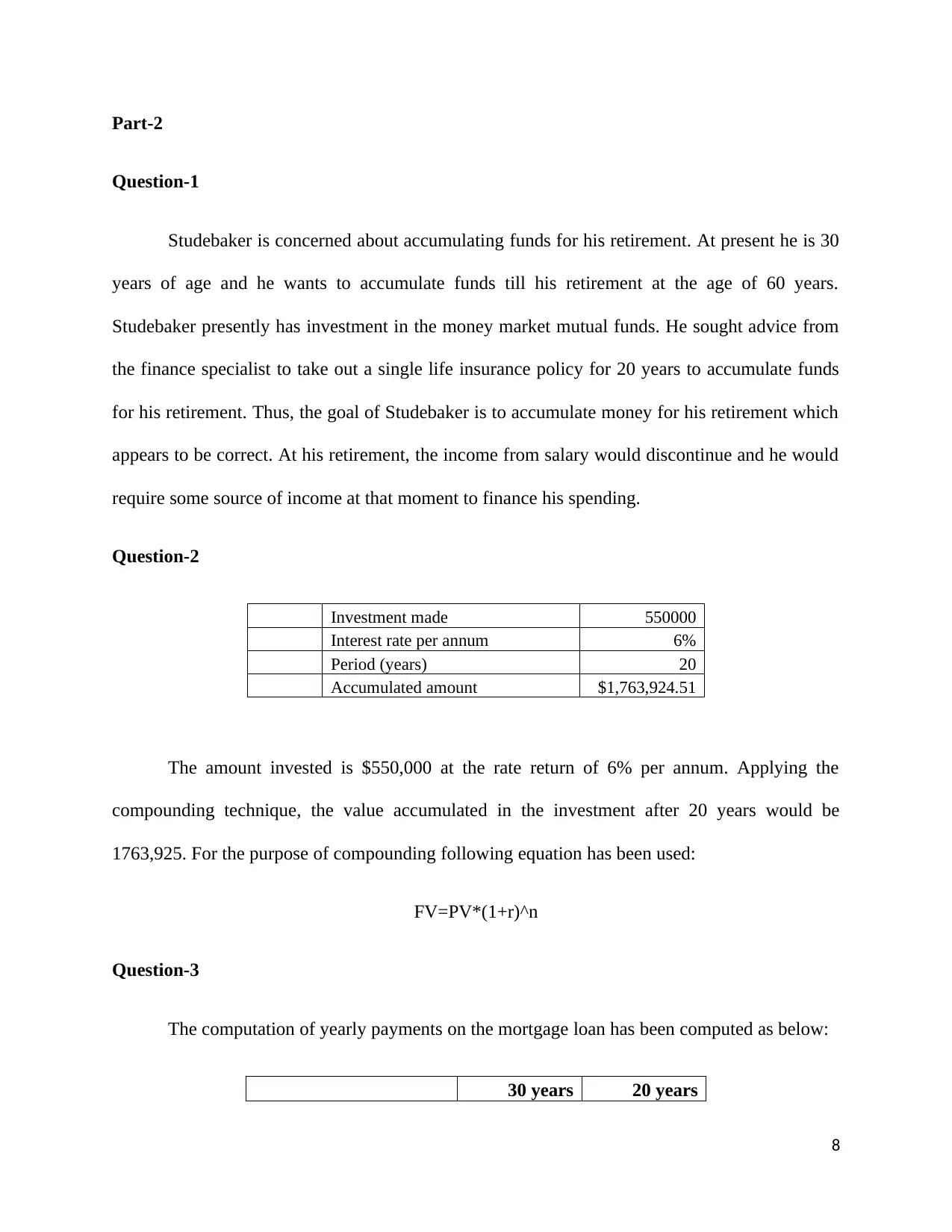

Studebaker is concerned about accumulating funds for his retirement. At present he is 30

years of age and he wants to accumulate funds till his retirement at the age of 60 years.

Studebaker presently has investment in the money market mutual funds. He sought advice from

the finance specialist to take out a single life insurance policy for 20 years to accumulate funds

for his retirement. Thus, the goal of Studebaker is to accumulate money for his retirement which

appears to be correct. At his retirement, the income from salary would discontinue and he would

require some source of income at that moment to finance his spending.

Question-2

Investment made 550000

Interest rate per annum 6%

Period (years) 20

Accumulated amount $1,763,924.51

The amount invested is $550,000 at the rate return of 6% per annum. Applying the

compounding technique, the value accumulated in the investment after 20 years would be

1763,925. For the purpose of compounding following equation has been used:

FV=PV*(1+r)^n

Question-3

The computation of yearly payments on the mortgage loan has been computed as below:

30 years 20 years

8

Question-1

Studebaker is concerned about accumulating funds for his retirement. At present he is 30

years of age and he wants to accumulate funds till his retirement at the age of 60 years.

Studebaker presently has investment in the money market mutual funds. He sought advice from

the finance specialist to take out a single life insurance policy for 20 years to accumulate funds

for his retirement. Thus, the goal of Studebaker is to accumulate money for his retirement which

appears to be correct. At his retirement, the income from salary would discontinue and he would

require some source of income at that moment to finance his spending.

Question-2

Investment made 550000

Interest rate per annum 6%

Period (years) 20

Accumulated amount $1,763,924.51

The amount invested is $550,000 at the rate return of 6% per annum. Applying the

compounding technique, the value accumulated in the investment after 20 years would be

1763,925. For the purpose of compounding following equation has been used:

FV=PV*(1+r)^n

Question-3

The computation of yearly payments on the mortgage loan has been computed as below:

30 years 20 years

8

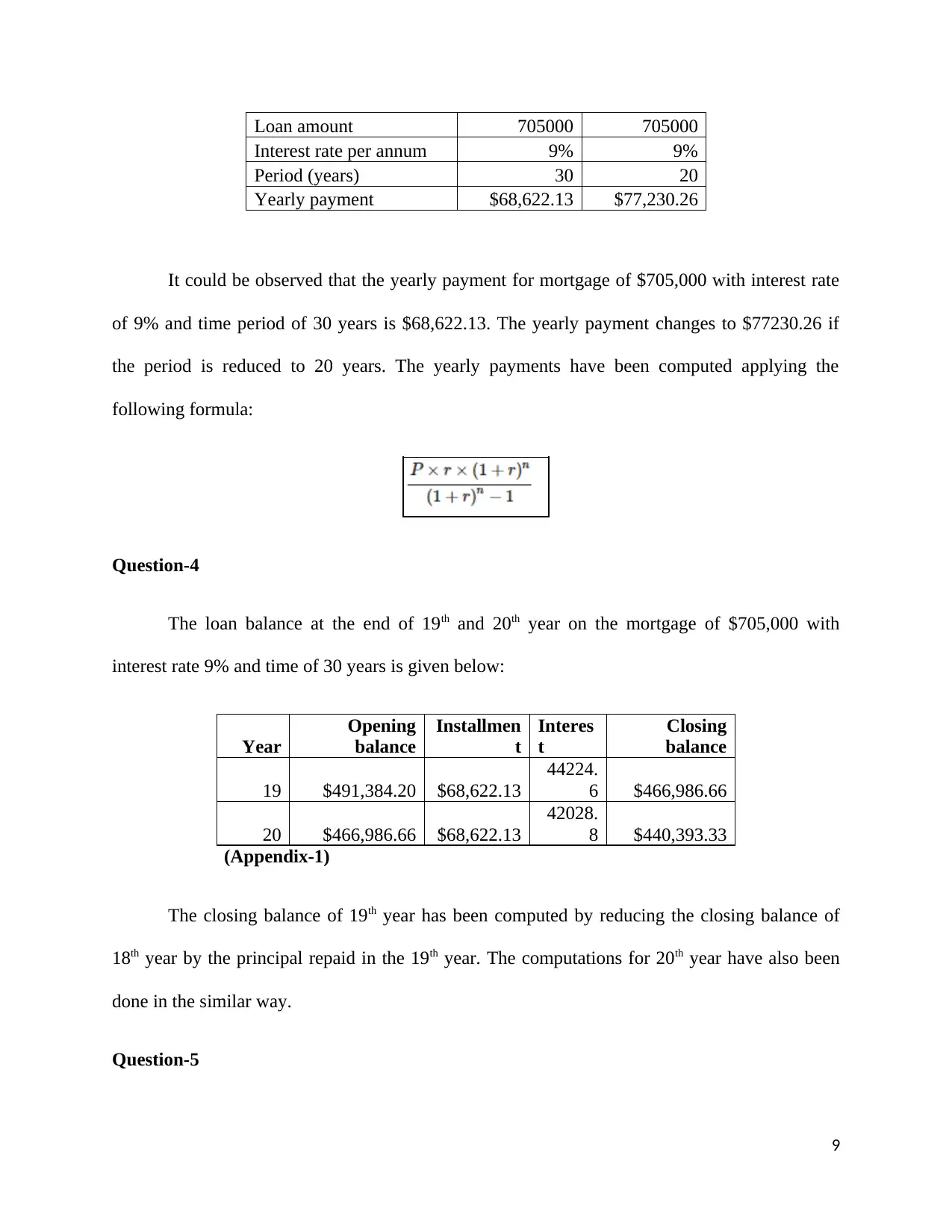

Loan amount 705000 705000

Interest rate per annum 9% 9%

Period (years) 30 20

Yearly payment $68,622.13 $77,230.26

It could be observed that the yearly payment for mortgage of $705,000 with interest rate

of 9% and time period of 30 years is $68,622.13. The yearly payment changes to $77230.26 if

the period is reduced to 20 years. The yearly payments have been computed applying the

following formula:

Question-4

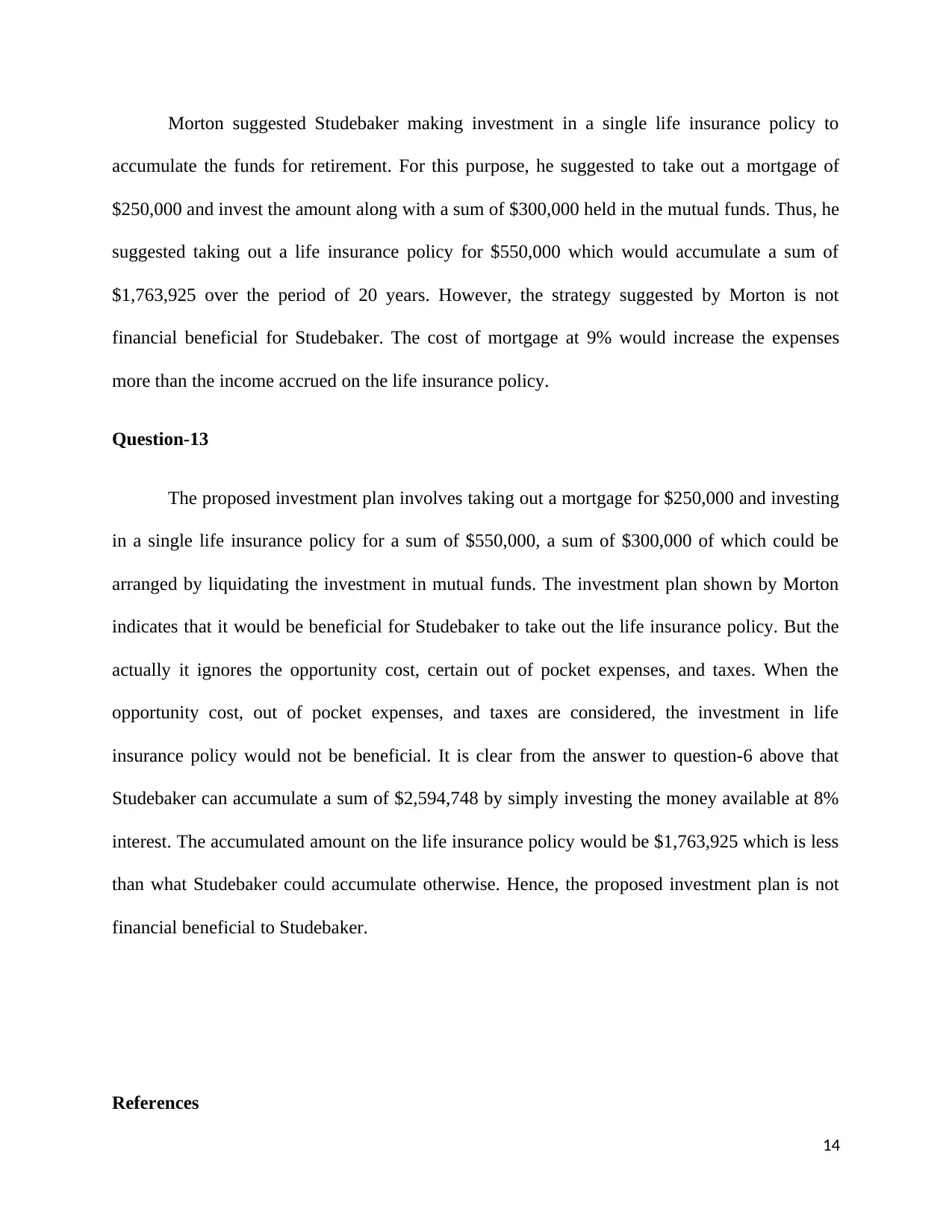

The loan balance at the end of 19th and 20th year on the mortgage of $705,000 with

interest rate 9% and time of 30 years is given below:

Year

Opening

balance

Installmen

t

Interes

t

Closing

balance

19 $491,384.20 $68,622.13

44224.

6 $466,986.66

20 $466,986.66 $68,622.13

42028.

8 $440,393.33

(Appendix-1)

The closing balance of 19th year has been computed by reducing the closing balance of

18th year by the principal repaid in the 19th year. The computations for 20th year have also been

done in the similar way.

Question-5

9

Interest rate per annum 9% 9%

Period (years) 30 20

Yearly payment $68,622.13 $77,230.26

It could be observed that the yearly payment for mortgage of $705,000 with interest rate

of 9% and time period of 30 years is $68,622.13. The yearly payment changes to $77230.26 if

the period is reduced to 20 years. The yearly payments have been computed applying the

following formula:

Question-4

The loan balance at the end of 19th and 20th year on the mortgage of $705,000 with

interest rate 9% and time of 30 years is given below:

Year

Opening

balance

Installmen

t

Interes

t

Closing

balance

19 $491,384.20 $68,622.13

44224.

6 $466,986.66

20 $466,986.66 $68,622.13

42028.

8 $440,393.33

(Appendix-1)

The closing balance of 19th year has been computed by reducing the closing balance of

18th year by the principal repaid in the 19th year. The computations for 20th year have also been

done in the similar way.

Question-5

9

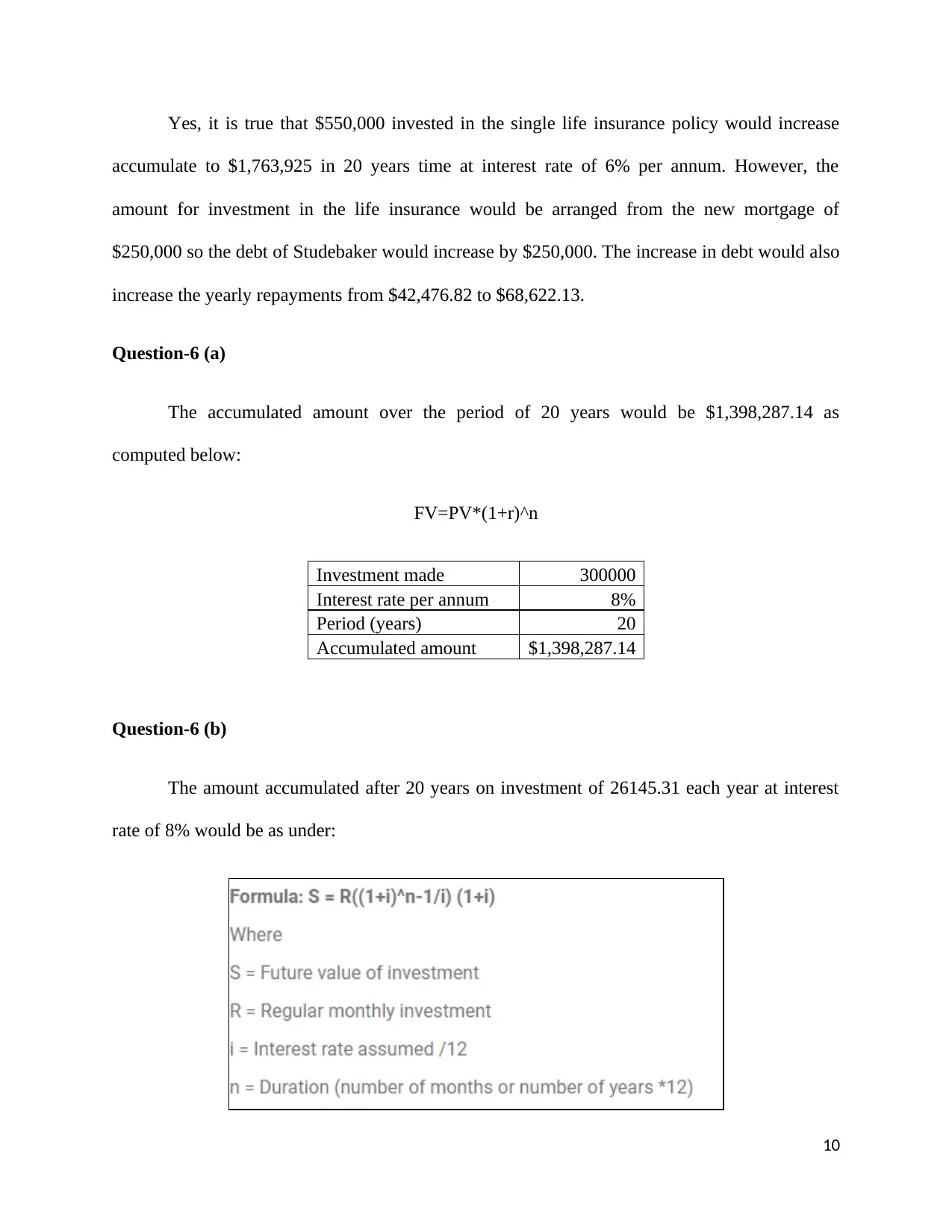

Yes, it is true that $550,000 invested in the single life insurance policy would increase

accumulate to $1,763,925 in 20 years time at interest rate of 6% per annum. However, the

amount for investment in the life insurance would be arranged from the new mortgage of

$250,000 so the debt of Studebaker would increase by $250,000. The increase in debt would also

increase the yearly repayments from $42,476.82 to $68,622.13.

Question-6 (a)

The accumulated amount over the period of 20 years would be $1,398,287.14 as

computed below:

FV=PV*(1+r)^n

Investment made 300000

Interest rate per annum 8%

Period (years) 20

Accumulated amount $1,398,287.14

Question-6 (b)

The amount accumulated after 20 years on investment of 26145.31 each year at interest

rate of 8% would be as under:

10

accumulate to $1,763,925 in 20 years time at interest rate of 6% per annum. However, the

amount for investment in the life insurance would be arranged from the new mortgage of

$250,000 so the debt of Studebaker would increase by $250,000. The increase in debt would also

increase the yearly repayments from $42,476.82 to $68,622.13.

Question-6 (a)

The accumulated amount over the period of 20 years would be $1,398,287.14 as

computed below:

FV=PV*(1+r)^n

Investment made 300000

Interest rate per annum 8%

Period (years) 20

Accumulated amount $1,398,287.14

Question-6 (b)

The amount accumulated after 20 years on investment of 26145.31 each year at interest

rate of 8% would be as under:

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

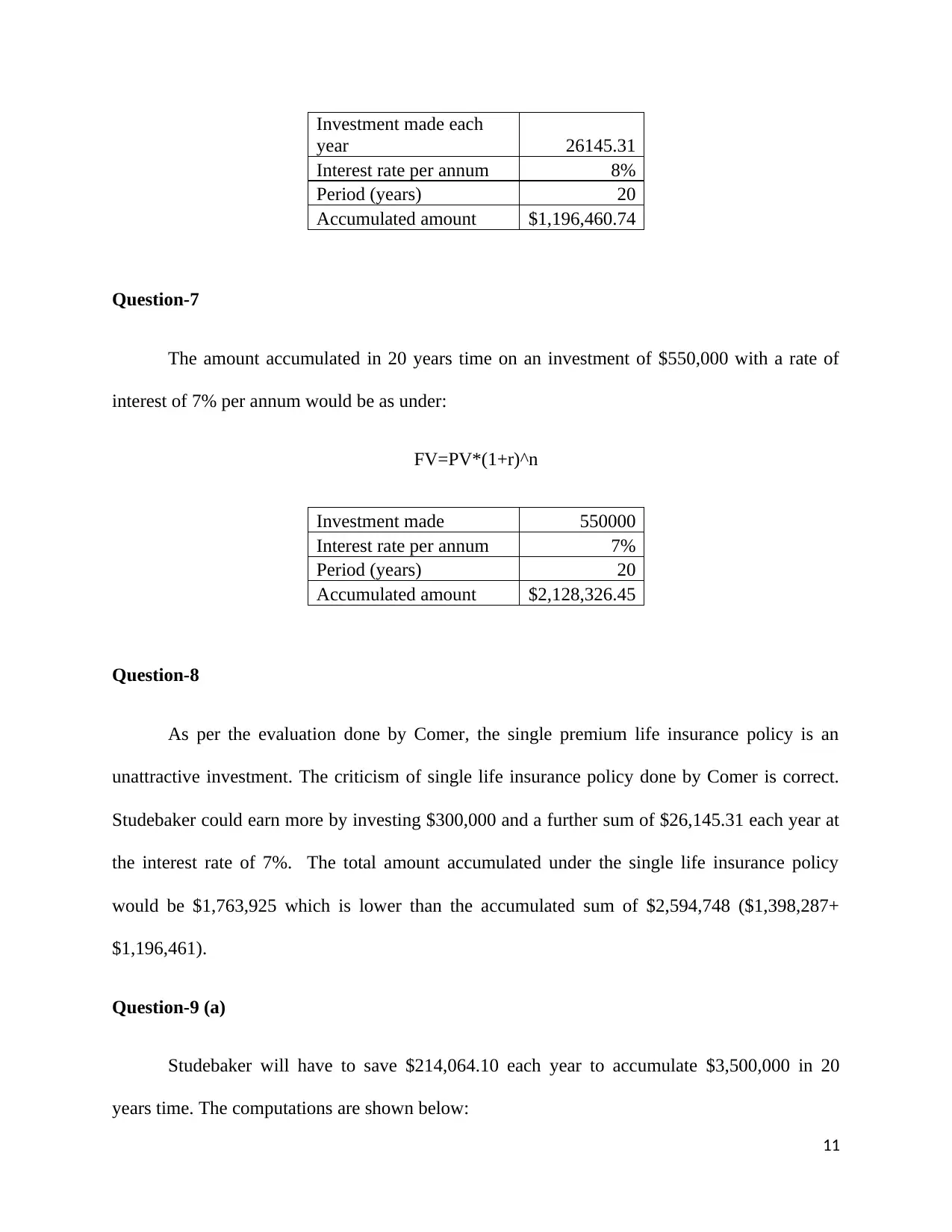

Investment made each

year 26145.31

Interest rate per annum 8%

Period (years) 20

Accumulated amount $1,196,460.74

Question-7

The amount accumulated in 20 years time on an investment of $550,000 with a rate of

interest of 7% per annum would be as under:

FV=PV*(1+r)^n

Investment made 550000

Interest rate per annum 7%

Period (years) 20

Accumulated amount $2,128,326.45

Question-8

As per the evaluation done by Comer, the single premium life insurance policy is an

unattractive investment. The criticism of single life insurance policy done by Comer is correct.

Studebaker could earn more by investing $300,000 and a further sum of $26,145.31 each year at

the interest rate of 7%. The total amount accumulated under the single life insurance policy

would be $1,763,925 which is lower than the accumulated sum of $2,594,748 ($1,398,287+

$1,196,461).

Question-9 (a)

Studebaker will have to save $214,064.10 each year to accumulate $3,500,000 in 20

years time. The computations are shown below:

11

year 26145.31

Interest rate per annum 8%

Period (years) 20

Accumulated amount $1,196,460.74

Question-7

The amount accumulated in 20 years time on an investment of $550,000 with a rate of

interest of 7% per annum would be as under:

FV=PV*(1+r)^n

Investment made 550000

Interest rate per annum 7%

Period (years) 20

Accumulated amount $2,128,326.45

Question-8

As per the evaluation done by Comer, the single premium life insurance policy is an

unattractive investment. The criticism of single life insurance policy done by Comer is correct.

Studebaker could earn more by investing $300,000 and a further sum of $26,145.31 each year at

the interest rate of 7%. The total amount accumulated under the single life insurance policy

would be $1,763,925 which is lower than the accumulated sum of $2,594,748 ($1,398,287+

$1,196,461).

Question-9 (a)

Studebaker will have to save $214,064.10 each year to accumulate $3,500,000 in 20

years time. The computations are shown below:

11

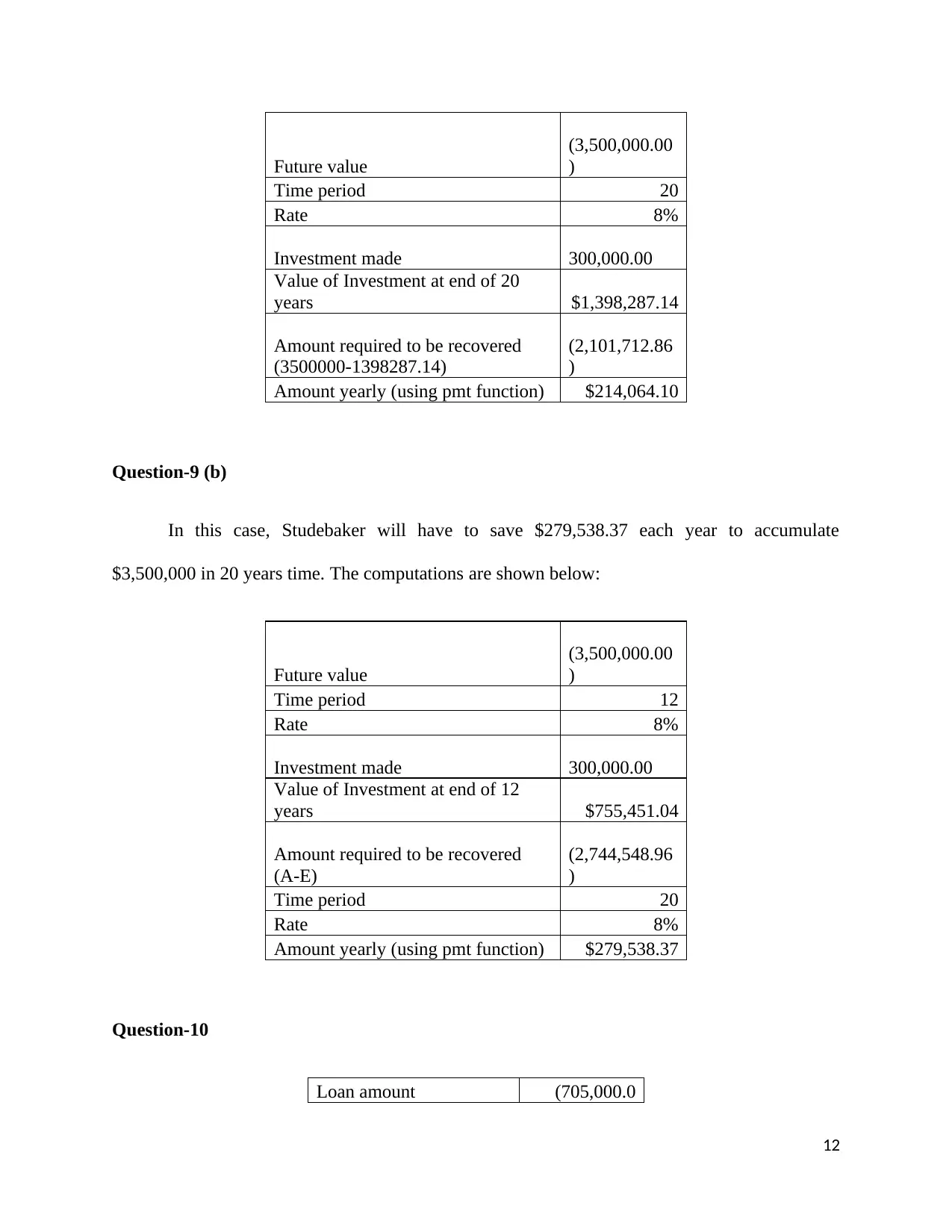

Future value

(3,500,000.00

)

Time period 20

Rate 8%

Investment made 300,000.00

Value of Investment at end of 20

years $1,398,287.14

Amount required to be recovered

(3500000-1398287.14)

(2,101,712.86

)

Amount yearly (using pmt function) $214,064.10

Question-9 (b)

In this case, Studebaker will have to save $279,538.37 each year to accumulate

$3,500,000 in 20 years time. The computations are shown below:

Future value

(3,500,000.00

)

Time period 12

Rate 8%

Investment made 300,000.00

Value of Investment at end of 12

years $755,451.04

Amount required to be recovered

(A-E)

(2,744,548.96

)

Time period 20

Rate 8%

Amount yearly (using pmt function) $279,538.37

Question-10

Loan amount (705,000.0

12

(3,500,000.00

)

Time period 20

Rate 8%

Investment made 300,000.00

Value of Investment at end of 20

years $1,398,287.14

Amount required to be recovered

(3500000-1398287.14)

(2,101,712.86

)

Amount yearly (using pmt function) $214,064.10

Question-9 (b)

In this case, Studebaker will have to save $279,538.37 each year to accumulate

$3,500,000 in 20 years time. The computations are shown below:

Future value

(3,500,000.00

)

Time period 12

Rate 8%

Investment made 300,000.00

Value of Investment at end of 12

years $755,451.04

Amount required to be recovered

(A-E)

(2,744,548.96

)

Time period 20

Rate 8%

Amount yearly (using pmt function) $279,538.37

Question-10

Loan amount (705,000.0

12

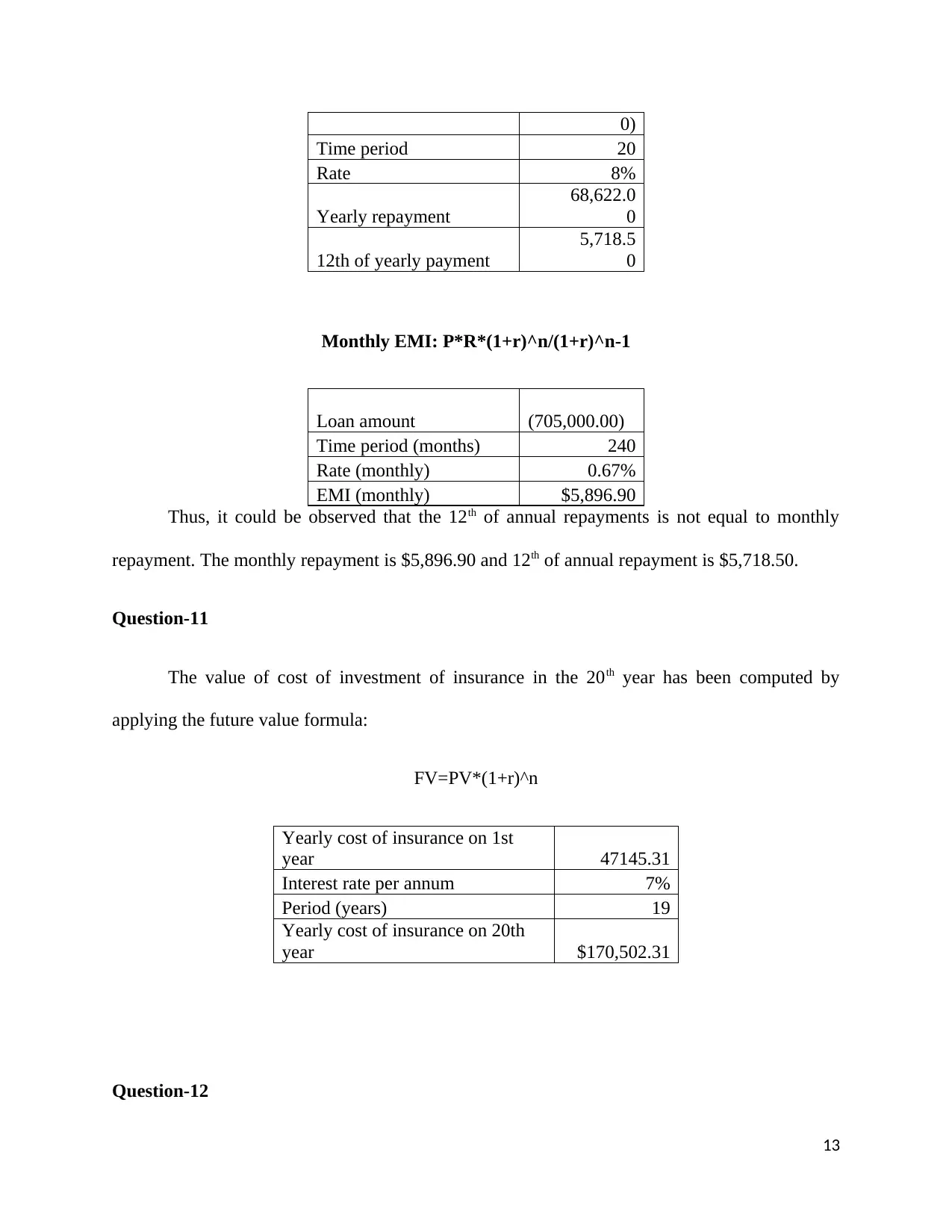

0)

Time period 20

Rate 8%

Yearly repayment

68,622.0

0

12th of yearly payment

5,718.5

0

Monthly EMI: P*R*(1+r)^n/(1+r)^n-1

Loan amount (705,000.00)

Time period (months) 240

Rate (monthly) 0.67%

EMI (monthly) $5,896.90

Thus, it could be observed that the 12th of annual repayments is not equal to monthly

repayment. The monthly repayment is $5,896.90 and 12th of annual repayment is $5,718.50.

Question-11

The value of cost of investment of insurance in the 20th year has been computed by

applying the future value formula:

FV=PV*(1+r)^n

Yearly cost of insurance on 1st

year 47145.31

Interest rate per annum 7%

Period (years) 19

Yearly cost of insurance on 20th

year $170,502.31

Question-12

13

Time period 20

Rate 8%

Yearly repayment

68,622.0

0

12th of yearly payment

5,718.5

0

Monthly EMI: P*R*(1+r)^n/(1+r)^n-1

Loan amount (705,000.00)

Time period (months) 240

Rate (monthly) 0.67%

EMI (monthly) $5,896.90

Thus, it could be observed that the 12th of annual repayments is not equal to monthly

repayment. The monthly repayment is $5,896.90 and 12th of annual repayment is $5,718.50.

Question-11

The value of cost of investment of insurance in the 20th year has been computed by

applying the future value formula:

FV=PV*(1+r)^n

Yearly cost of insurance on 1st

year 47145.31

Interest rate per annum 7%

Period (years) 19

Yearly cost of insurance on 20th

year $170,502.31

Question-12

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Morton suggested Studebaker making investment in a single life insurance policy to

accumulate the funds for retirement. For this purpose, he suggested to take out a mortgage of

$250,000 and invest the amount along with a sum of $300,000 held in the mutual funds. Thus, he

suggested taking out a life insurance policy for $550,000 which would accumulate a sum of

$1,763,925 over the period of 20 years. However, the strategy suggested by Morton is not

financial beneficial for Studebaker. The cost of mortgage at 9% would increase the expenses

more than the income accrued on the life insurance policy.

Question-13

The proposed investment plan involves taking out a mortgage for $250,000 and investing

in a single life insurance policy for a sum of $550,000, a sum of $300,000 of which could be

arranged by liquidating the investment in mutual funds. The investment plan shown by Morton

indicates that it would be beneficial for Studebaker to take out the life insurance policy. But the

actually it ignores the opportunity cost, certain out of pocket expenses, and taxes. When the

opportunity cost, out of pocket expenses, and taxes are considered, the investment in life

insurance policy would not be beneficial. It is clear from the answer to question-6 above that

Studebaker can accumulate a sum of $2,594,748 by simply investing the money available at 8%

interest. The accumulated amount on the life insurance policy would be $1,763,925 which is less

than what Studebaker could accumulate otherwise. Hence, the proposed investment plan is not

financial beneficial to Studebaker.

References

14

accumulate the funds for retirement. For this purpose, he suggested to take out a mortgage of

$250,000 and invest the amount along with a sum of $300,000 held in the mutual funds. Thus, he

suggested taking out a life insurance policy for $550,000 which would accumulate a sum of

$1,763,925 over the period of 20 years. However, the strategy suggested by Morton is not

financial beneficial for Studebaker. The cost of mortgage at 9% would increase the expenses

more than the income accrued on the life insurance policy.

Question-13

The proposed investment plan involves taking out a mortgage for $250,000 and investing

in a single life insurance policy for a sum of $550,000, a sum of $300,000 of which could be

arranged by liquidating the investment in mutual funds. The investment plan shown by Morton

indicates that it would be beneficial for Studebaker to take out the life insurance policy. But the

actually it ignores the opportunity cost, certain out of pocket expenses, and taxes. When the

opportunity cost, out of pocket expenses, and taxes are considered, the investment in life

insurance policy would not be beneficial. It is clear from the answer to question-6 above that

Studebaker can accumulate a sum of $2,594,748 by simply investing the money available at 8%

interest. The accumulated amount on the life insurance policy would be $1,763,925 which is less

than what Studebaker could accumulate otherwise. Hence, the proposed investment plan is not

financial beneficial to Studebaker.

References

14

Baker, H.K. and English, P. 2011. Capital Budgeting Valuation: Financial Analysis for Today's

Investment Projects. John Wiley & Sons.

Drake, P.P. and Fabozzi, F.J. 2009. Foundations and Applications of the Time Value of Money.

John Wiley & Sons.

Halpin, D.W. and Senior, B.A. 2011. Financial Management and Accounting Fundamentals for

Construction. John Wiley & Sons.

Shapiro. 2008. Capital Budgeting And Investment Analysis. Pearson Education India.

Shim, J.K. and Siegel, J.G. 2008. Financial Management. Barron's Educational Series.

Silver, T.L. 2011. The Time Value of Life: Why Time Is More Valuable Than Money. iUniverse.

Appendix-1

15

Investment Projects. John Wiley & Sons.

Drake, P.P. and Fabozzi, F.J. 2009. Foundations and Applications of the Time Value of Money.

John Wiley & Sons.

Halpin, D.W. and Senior, B.A. 2011. Financial Management and Accounting Fundamentals for

Construction. John Wiley & Sons.

Shapiro. 2008. Capital Budgeting And Investment Analysis. Pearson Education India.

Shim, J.K. and Siegel, J.G. 2008. Financial Management. Barron's Educational Series.

Silver, T.L. 2011. The Time Value of Life: Why Time Is More Valuable Than Money. iUniverse.

Appendix-1

15

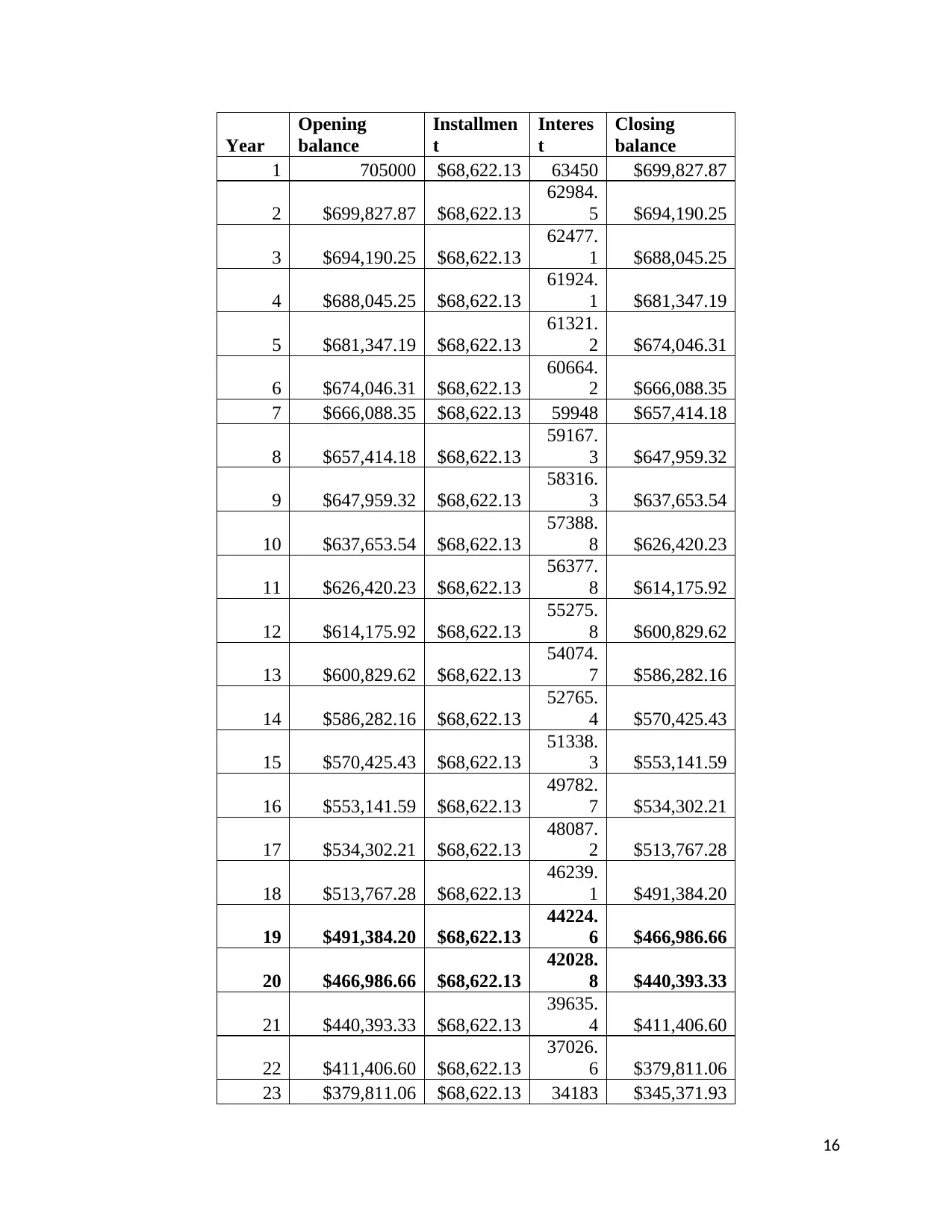

Year

Opening

balance

Installmen

t

Interes

t

Closing

balance

1 705000 $68,622.13 63450 $699,827.87

2 $699,827.87 $68,622.13

62984.

5 $694,190.25

3 $694,190.25 $68,622.13

62477.

1 $688,045.25

4 $688,045.25 $68,622.13

61924.

1 $681,347.19

5 $681,347.19 $68,622.13

61321.

2 $674,046.31

6 $674,046.31 $68,622.13

60664.

2 $666,088.35

7 $666,088.35 $68,622.13 59948 $657,414.18

8 $657,414.18 $68,622.13

59167.

3 $647,959.32

9 $647,959.32 $68,622.13

58316.

3 $637,653.54

10 $637,653.54 $68,622.13

57388.

8 $626,420.23

11 $626,420.23 $68,622.13

56377.

8 $614,175.92

12 $614,175.92 $68,622.13

55275.

8 $600,829.62

13 $600,829.62 $68,622.13

54074.

7 $586,282.16

14 $586,282.16 $68,622.13

52765.

4 $570,425.43

15 $570,425.43 $68,622.13

51338.

3 $553,141.59

16 $553,141.59 $68,622.13

49782.

7 $534,302.21

17 $534,302.21 $68,622.13

48087.

2 $513,767.28

18 $513,767.28 $68,622.13

46239.

1 $491,384.20

19 $491,384.20 $68,622.13

44224.

6 $466,986.66

20 $466,986.66 $68,622.13

42028.

8 $440,393.33

21 $440,393.33 $68,622.13

39635.

4 $411,406.60

22 $411,406.60 $68,622.13

37026.

6 $379,811.06

23 $379,811.06 $68,622.13 34183 $345,371.93

16

Opening

balance

Installmen

t

Interes

t

Closing

balance

1 705000 $68,622.13 63450 $699,827.87

2 $699,827.87 $68,622.13

62984.

5 $694,190.25

3 $694,190.25 $68,622.13

62477.

1 $688,045.25

4 $688,045.25 $68,622.13

61924.

1 $681,347.19

5 $681,347.19 $68,622.13

61321.

2 $674,046.31

6 $674,046.31 $68,622.13

60664.

2 $666,088.35

7 $666,088.35 $68,622.13 59948 $657,414.18

8 $657,414.18 $68,622.13

59167.

3 $647,959.32

9 $647,959.32 $68,622.13

58316.

3 $637,653.54

10 $637,653.54 $68,622.13

57388.

8 $626,420.23

11 $626,420.23 $68,622.13

56377.

8 $614,175.92

12 $614,175.92 $68,622.13

55275.

8 $600,829.62

13 $600,829.62 $68,622.13

54074.

7 $586,282.16

14 $586,282.16 $68,622.13

52765.

4 $570,425.43

15 $570,425.43 $68,622.13

51338.

3 $553,141.59

16 $553,141.59 $68,622.13

49782.

7 $534,302.21

17 $534,302.21 $68,622.13

48087.

2 $513,767.28

18 $513,767.28 $68,622.13

46239.

1 $491,384.20

19 $491,384.20 $68,622.13

44224.

6 $466,986.66

20 $466,986.66 $68,622.13

42028.

8 $440,393.33

21 $440,393.33 $68,622.13

39635.

4 $411,406.60

22 $411,406.60 $68,622.13

37026.

6 $379,811.06

23 $379,811.06 $68,622.13 34183 $345,371.93

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

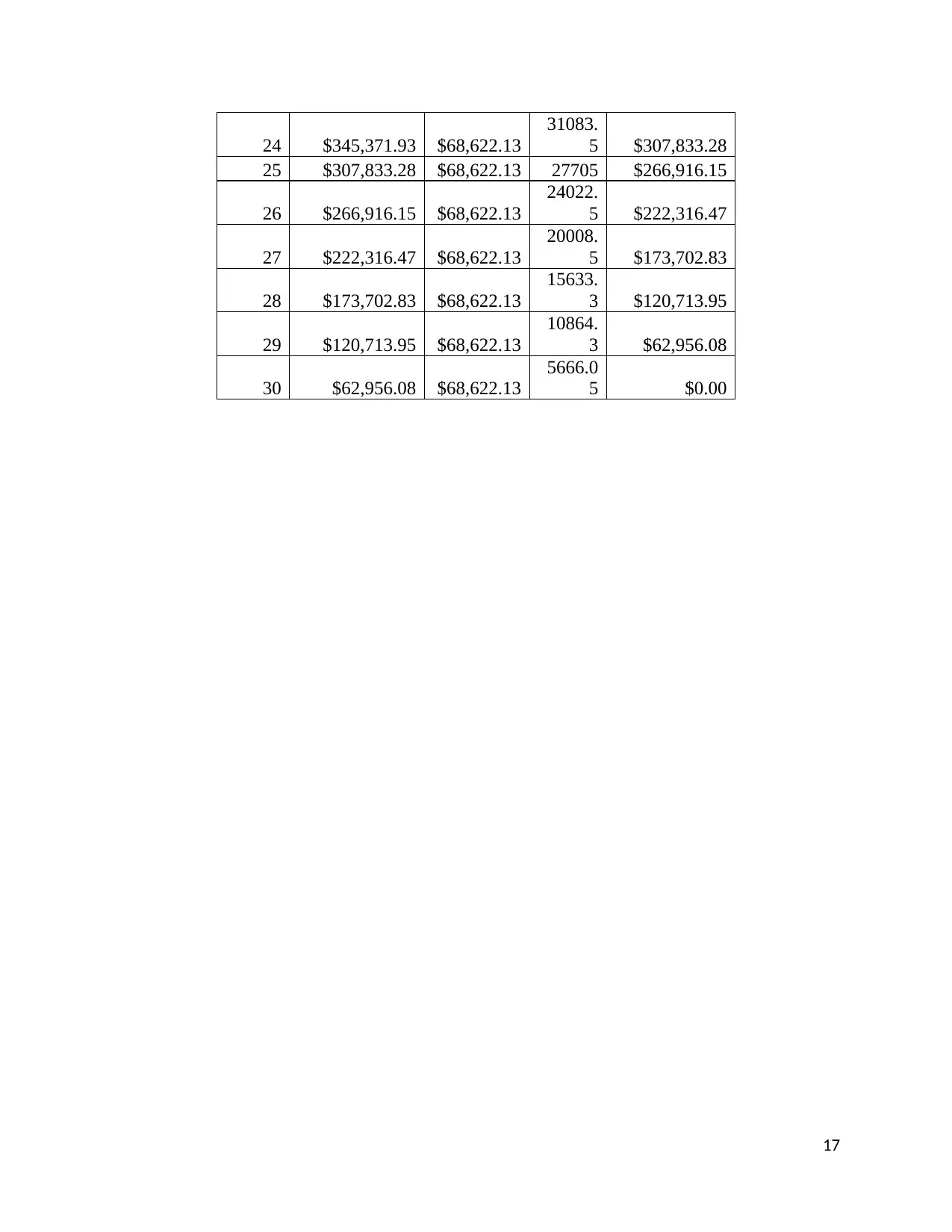

24 $345,371.93 $68,622.13

31083.

5 $307,833.28

25 $307,833.28 $68,622.13 27705 $266,916.15

26 $266,916.15 $68,622.13

24022.

5 $222,316.47

27 $222,316.47 $68,622.13

20008.

5 $173,702.83

28 $173,702.83 $68,622.13

15633.

3 $120,713.95

29 $120,713.95 $68,622.13

10864.

3 $62,956.08

30 $62,956.08 $68,622.13

5666.0

5 $0.00

17

31083.

5 $307,833.28

25 $307,833.28 $68,622.13 27705 $266,916.15

26 $266,916.15 $68,622.13

24022.

5 $222,316.47

27 $222,316.47 $68,622.13

20008.

5 $173,702.83

28 $173,702.83 $68,622.13

15633.

3 $120,713.95

29 $120,713.95 $68,622.13

10864.

3 $62,956.08

30 $62,956.08 $68,622.13

5666.0

5 $0.00

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.