Management Accounting Report: UCK Furniture's Financial Performance

VerifiedAdded on 2020/12/24

|12

|2819

|237

Report

AI Summary

This report provides a detailed analysis of management accounting principles applied to UCK Furniture, a leading furniture company in the U.K. It explores various costing methods, including marginal and absorption costing, to determine the company's net profit. The report also examines a range of management techniques and planning tools, such as forecasting and contingency tools, used for budgeting and financial control. An analysis of the company's income statement and a comparison with UCK Woodwork's financial ratios are included to identify key financial issues and evaluate the effectiveness of the accounting system. Finally, the report offers insights into how UCK Furniture can improve its financial performance through better planning and resource management. Desklib provides students with access to a variety of past papers and solved assignments, making it an invaluable resource for academic success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Calculation of cost by using various methods......................................................................1

1.2 Range of management techniques.........................................................................................2

1.3: Analysis of data collected from income statement...............................................................3

TASK 2............................................................................................................................................3

2.1: Advantage and disadvantage of using planning tools...........................................................3

2.2: Analysis of the expenses for July and August......................................................................4

2.3: Objective and cash budget....................................................................................................5

TASK 3............................................................................................................................................6

3.1: Use of accounting system to determine financial issues.......................................................6

3.2: Evaluating financial issues faced by UCK furniture............................................................6

3.3: Analysis of planning tools that is used in management accounting.....................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Calculation of cost by using various methods......................................................................1

1.2 Range of management techniques.........................................................................................2

1.3: Analysis of data collected from income statement...............................................................3

TASK 2............................................................................................................................................3

2.1: Advantage and disadvantage of using planning tools...........................................................3

2.2: Analysis of the expenses for July and August......................................................................4

2.3: Objective and cash budget....................................................................................................5

TASK 3............................................................................................................................................6

3.1: Use of accounting system to determine financial issues.......................................................6

3.2: Evaluating financial issues faced by UCK furniture............................................................6

3.3: Analysis of planning tools that is used in management accounting.....................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is known as the process of analysing, recording, reporting useful

financial information that help internal manager to make useful decision and improve the

performance and productivity of company (Amoako, 2013). With the help of management

accounting manager of an organisation are able to figure out early problem, that may reduces

their performance and market share. UCK furniture is one of the leading furniture company in

U.K that use to manufacture and supply beautiful interior and exterior furnitures to customer.

In this report uses of different costing method that are useful in determining the actual net

profit for company is discussed. Along with advantages and disadvantage of various planning

tool is shown that aid in controlling budgets. Comparison with other company in regarding to use

of accounting system.

TASK 1

1.1: Calculation of cost by using various methods.

Cost is defined as the value that is use by buyer in order to make purchase of something

offer for sales by seller. It is basically the aspects that is reasoned while the production of

different goods and services within company. Costing is consider to be a reliable procedure of

calculating total cost of UCK furniture in investing in manufacture process with the actual

current present cost of capital. So it is stated that cost id directly or indirectly related to

production of useful goods. There are different types of costing system that are connected with

UKC furniture business operations and are discussed below:

Marginal costing: This system is used to calculate the additional cost involved by

company in order to produce an extra unit of output. It is basically known as incremental cost

that consist of specific variable while calculating total contribution per unit during an accounting

year. In general, marginal cost are based on production expenses that are direct of variable such

as labour material and equipment. It is taken into report for taking useful future decision as

possibilities of mistakes are less in this method.

Absorption costing: This costing system help to calculate cost that is applicable in

producing useful product within an organisation. It consist of both variable and fixed cost as it is

commonly known as full costing system (Absorption costing, 2018.). There are various

importance of using absorption costing system but at the same time it affect the net profitability

1

Management accounting is known as the process of analysing, recording, reporting useful

financial information that help internal manager to make useful decision and improve the

performance and productivity of company (Amoako, 2013). With the help of management

accounting manager of an organisation are able to figure out early problem, that may reduces

their performance and market share. UCK furniture is one of the leading furniture company in

U.K that use to manufacture and supply beautiful interior and exterior furnitures to customer.

In this report uses of different costing method that are useful in determining the actual net

profit for company is discussed. Along with advantages and disadvantage of various planning

tool is shown that aid in controlling budgets. Comparison with other company in regarding to use

of accounting system.

TASK 1

1.1: Calculation of cost by using various methods.

Cost is defined as the value that is use by buyer in order to make purchase of something

offer for sales by seller. It is basically the aspects that is reasoned while the production of

different goods and services within company. Costing is consider to be a reliable procedure of

calculating total cost of UCK furniture in investing in manufacture process with the actual

current present cost of capital. So it is stated that cost id directly or indirectly related to

production of useful goods. There are different types of costing system that are connected with

UKC furniture business operations and are discussed below:

Marginal costing: This system is used to calculate the additional cost involved by

company in order to produce an extra unit of output. It is basically known as incremental cost

that consist of specific variable while calculating total contribution per unit during an accounting

year. In general, marginal cost are based on production expenses that are direct of variable such

as labour material and equipment. It is taken into report for taking useful future decision as

possibilities of mistakes are less in this method.

Absorption costing: This costing system help to calculate cost that is applicable in

producing useful product within an organisation. It consist of both variable and fixed cost as it is

commonly known as full costing system (Absorption costing, 2018.). There are various

importance of using absorption costing system but at the same time it affect the net profitability

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

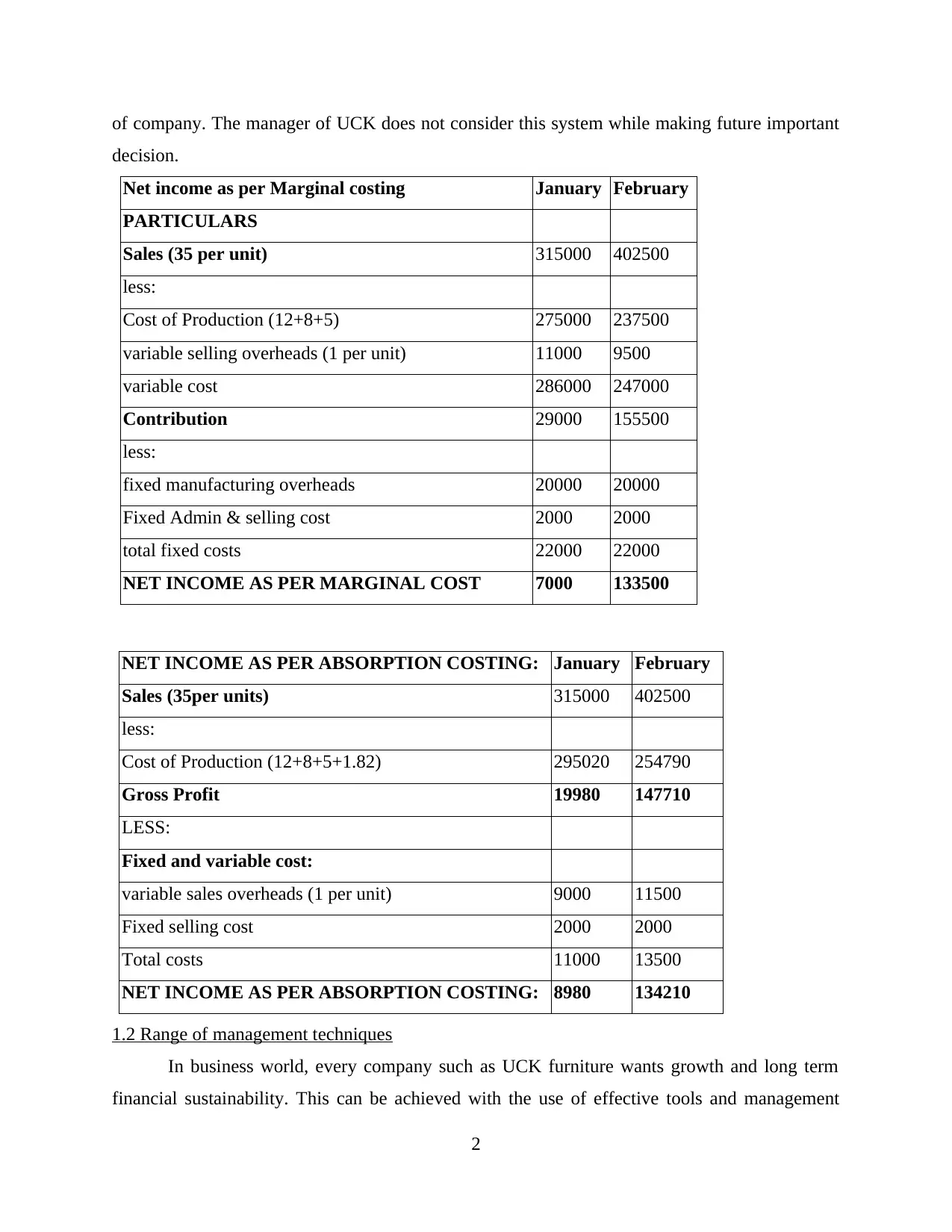

of company. The manager of UCK does not consider this system while making future important

decision.

Net income as per Marginal costing January February

PARTICULARS

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

NET INCOME AS PER ABSORPTION COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2 Range of management techniques

In business world, every company such as UCK furniture wants growth and long term

financial sustainability. This can be achieved with the use of effective tools and management

2

decision.

Net income as per Marginal costing January February

PARTICULARS

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

NET INCOME AS PER ABSORPTION COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2 Range of management techniques

In business world, every company such as UCK furniture wants growth and long term

financial sustainability. This can be achieved with the use of effective tools and management

2

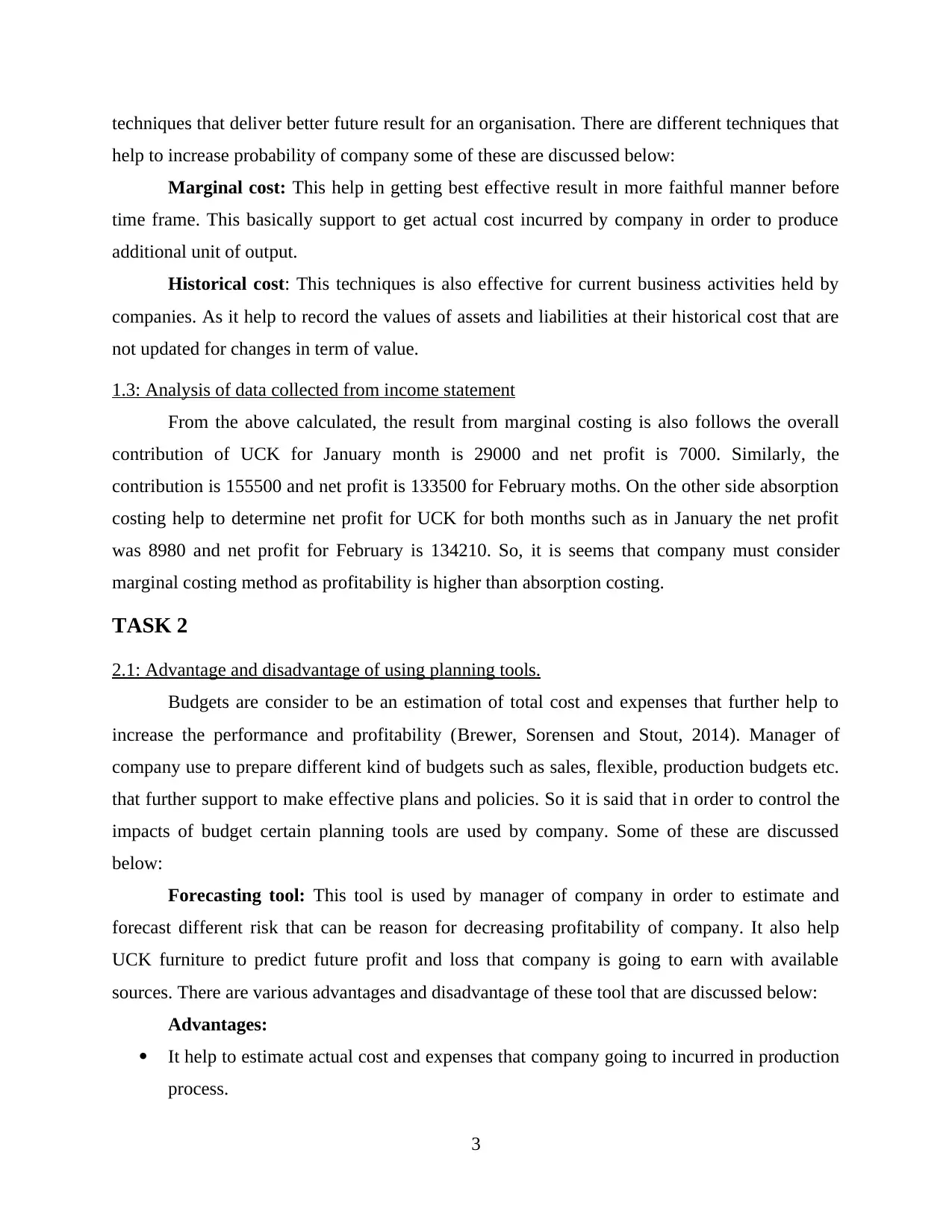

techniques that deliver better future result for an organisation. There are different techniques that

help to increase probability of company some of these are discussed below:

Marginal cost: This help in getting best effective result in more faithful manner before

time frame. This basically support to get actual cost incurred by company in order to produce

additional unit of output.

Historical cost: This techniques is also effective for current business activities held by

companies. As it help to record the values of assets and liabilities at their historical cost that are

not updated for changes in term of value.

1.3: Analysis of data collected from income statement

From the above calculated, the result from marginal costing is also follows the overall

contribution of UCK for January month is 29000 and net profit is 7000. Similarly, the

contribution is 155500 and net profit is 133500 for February moths. On the other side absorption

costing help to determine net profit for UCK for both months such as in January the net profit

was 8980 and net profit for February is 134210. So, it is seems that company must consider

marginal costing method as profitability is higher than absorption costing.

TASK 2

2.1: Advantage and disadvantage of using planning tools.

Budgets are consider to be an estimation of total cost and expenses that further help to

increase the performance and profitability (Brewer, Sorensen and Stout, 2014). Manager of

company use to prepare different kind of budgets such as sales, flexible, production budgets etc.

that further support to make effective plans and policies. So it is said that in order to control the

impacts of budget certain planning tools are used by company. Some of these are discussed

below:

Forecasting tool: This tool is used by manager of company in order to estimate and

forecast different risk that can be reason for decreasing profitability of company. It also help

UCK furniture to predict future profit and loss that company is going to earn with available

sources. There are various advantages and disadvantage of these tool that are discussed below:

Advantages:

It help to estimate actual cost and expenses that company going to incurred in production

process.

3

help to increase probability of company some of these are discussed below:

Marginal cost: This help in getting best effective result in more faithful manner before

time frame. This basically support to get actual cost incurred by company in order to produce

additional unit of output.

Historical cost: This techniques is also effective for current business activities held by

companies. As it help to record the values of assets and liabilities at their historical cost that are

not updated for changes in term of value.

1.3: Analysis of data collected from income statement

From the above calculated, the result from marginal costing is also follows the overall

contribution of UCK for January month is 29000 and net profit is 7000. Similarly, the

contribution is 155500 and net profit is 133500 for February moths. On the other side absorption

costing help to determine net profit for UCK for both months such as in January the net profit

was 8980 and net profit for February is 134210. So, it is seems that company must consider

marginal costing method as profitability is higher than absorption costing.

TASK 2

2.1: Advantage and disadvantage of using planning tools.

Budgets are consider to be an estimation of total cost and expenses that further help to

increase the performance and profitability (Brewer, Sorensen and Stout, 2014). Manager of

company use to prepare different kind of budgets such as sales, flexible, production budgets etc.

that further support to make effective plans and policies. So it is said that in order to control the

impacts of budget certain planning tools are used by company. Some of these are discussed

below:

Forecasting tool: This tool is used by manager of company in order to estimate and

forecast different risk that can be reason for decreasing profitability of company. It also help

UCK furniture to predict future profit and loss that company is going to earn with available

sources. There are various advantages and disadvantage of these tool that are discussed below:

Advantages:

It help to estimate actual cost and expenses that company going to incurred in production

process.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

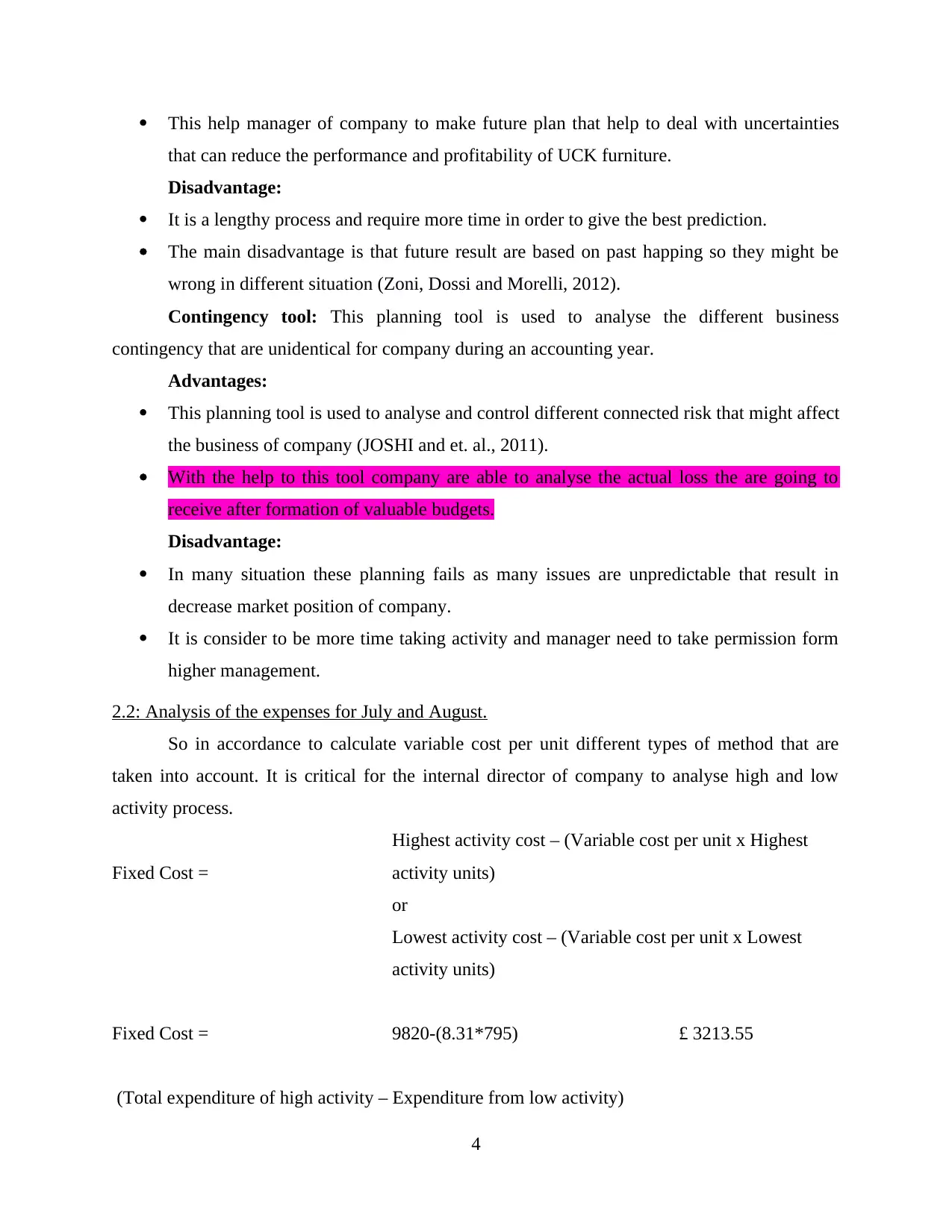

This help manager of company to make future plan that help to deal with uncertainties

that can reduce the performance and profitability of UCK furniture.

Disadvantage:

It is a lengthy process and require more time in order to give the best prediction.

The main disadvantage is that future result are based on past happing so they might be

wrong in different situation (Zoni, Dossi and Morelli, 2012).

Contingency tool: This planning tool is used to analyse the different business

contingency that are unidentical for company during an accounting year.

Advantages:

This planning tool is used to analyse and control different connected risk that might affect

the business of company (JOSHI and et. al., 2011).

With the help to this tool company are able to analyse the actual loss the are going to

receive after formation of valuable budgets.

Disadvantage:

In many situation these planning fails as many issues are unpredictable that result in

decrease market position of company.

It is consider to be more time taking activity and manager need to take permission form

higher management.

2.2: Analysis of the expenses for July and August.

So in accordance to calculate variable cost per unit different types of method that are

taken into account. It is critical for the internal director of company to analyse high and low

activity process.

Fixed Cost =

Highest activity cost – (Variable cost per unit x Highest

activity units)

or

Lowest activity cost – (Variable cost per unit x Lowest

activity units)

Fixed Cost = 9820-(8.31*795) £ 3213.55

(Total expenditure of high activity – Expenditure from low activity)

4

that can reduce the performance and profitability of UCK furniture.

Disadvantage:

It is a lengthy process and require more time in order to give the best prediction.

The main disadvantage is that future result are based on past happing so they might be

wrong in different situation (Zoni, Dossi and Morelli, 2012).

Contingency tool: This planning tool is used to analyse the different business

contingency that are unidentical for company during an accounting year.

Advantages:

This planning tool is used to analyse and control different connected risk that might affect

the business of company (JOSHI and et. al., 2011).

With the help to this tool company are able to analyse the actual loss the are going to

receive after formation of valuable budgets.

Disadvantage:

In many situation these planning fails as many issues are unpredictable that result in

decrease market position of company.

It is consider to be more time taking activity and manager need to take permission form

higher management.

2.2: Analysis of the expenses for July and August.

So in accordance to calculate variable cost per unit different types of method that are

taken into account. It is critical for the internal director of company to analyse high and low

activity process.

Fixed Cost =

Highest activity cost – (Variable cost per unit x Highest

activity units)

or

Lowest activity cost – (Variable cost per unit x Lowest

activity units)

Fixed Cost = 9820-(8.31*795) £ 3213.55

(Total expenditure of high activity – Expenditure from low activity)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

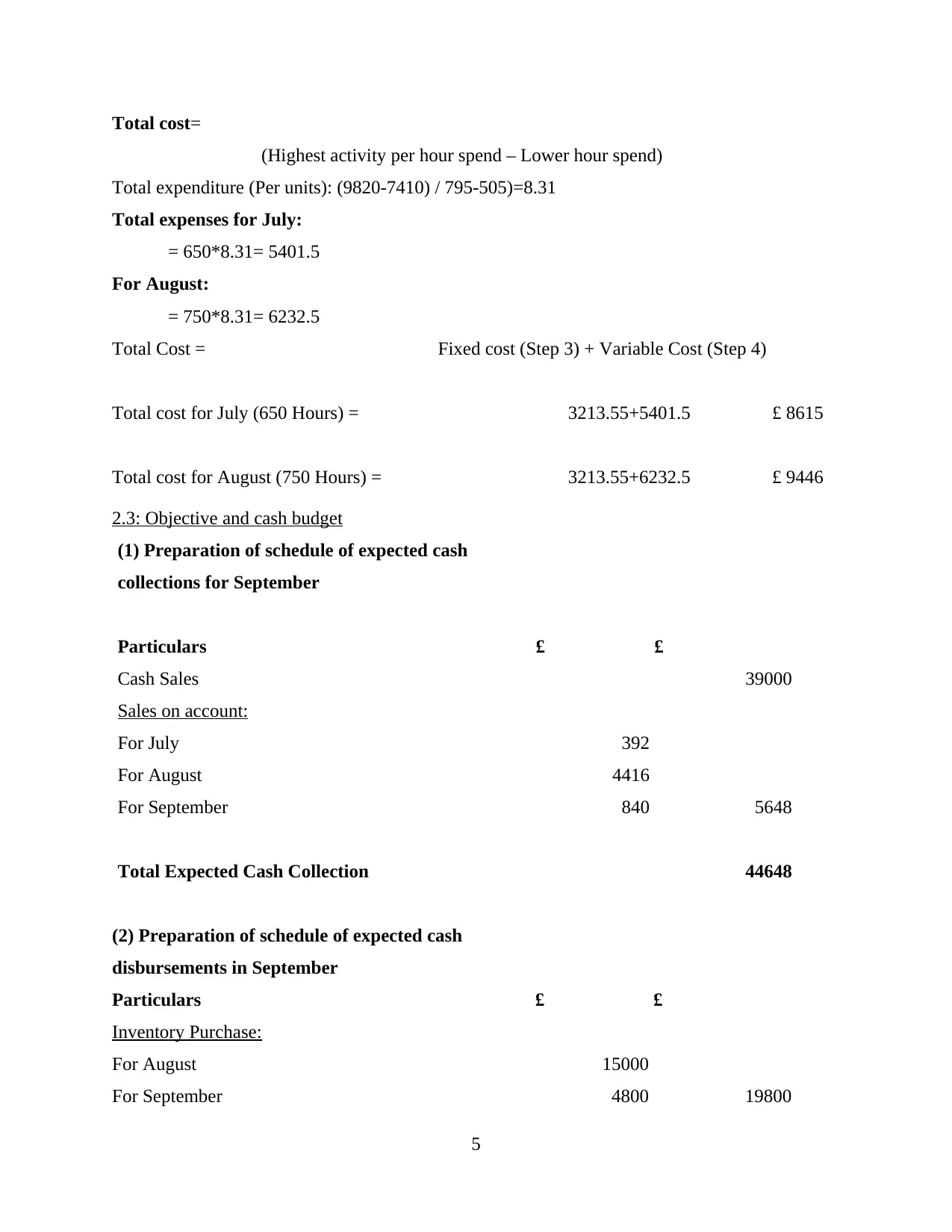

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

Total Cost = Fixed cost (Step 3) + Variable Cost (Step 4)

Total cost for July (650 Hours) = 3213.55+5401.5 £ 8615

Total cost for August (750 Hours) = 3213.55+6232.5 £ 9446

2.3: Objective and cash budget

(1) Preparation of schedule of expected cash

collections for September

Particulars £ £

Cash Sales 39000

Sales on account:

For July 392

For August 4416

For September 840 5648

Total Expected Cash Collection 44648

(2) Preparation of schedule of expected cash

disbursements in September

Particulars £ £

Inventory Purchase:

For August 15000

For September 4800 19800

5

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

Total Cost = Fixed cost (Step 3) + Variable Cost (Step 4)

Total cost for July (650 Hours) = 3213.55+5401.5 £ 8615

Total cost for August (750 Hours) = 3213.55+6232.5 £ 9446

2.3: Objective and cash budget

(1) Preparation of schedule of expected cash

collections for September

Particulars £ £

Cash Sales 39000

Sales on account:

For July 392

For August 4416

For September 840 5648

Total Expected Cash Collection 44648

(2) Preparation of schedule of expected cash

disbursements in September

Particulars £ £

Inventory Purchase:

For August 15000

For September 4800 19800

5

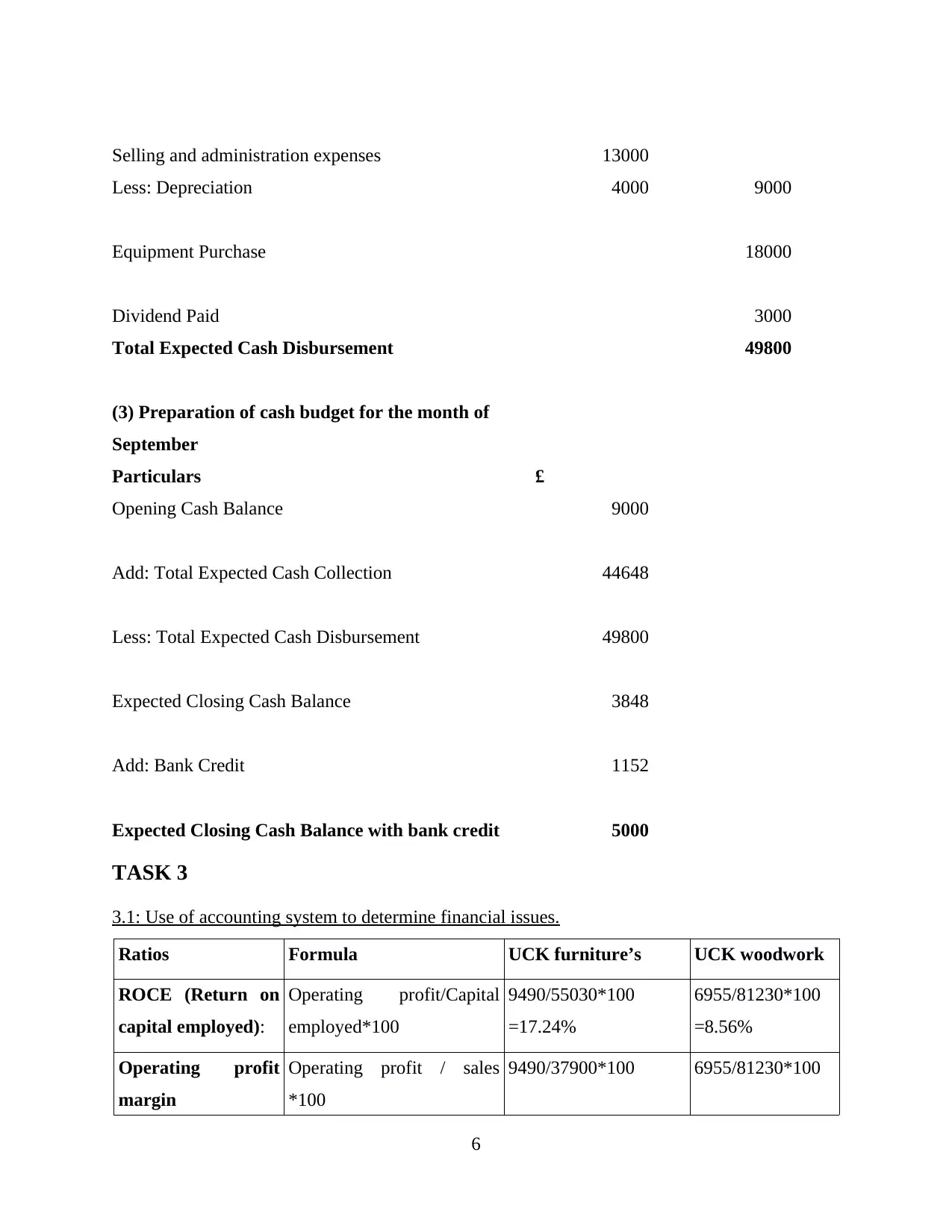

Selling and administration expenses 13000

Less: Depreciation 4000 9000

Equipment Purchase 18000

Dividend Paid 3000

Total Expected Cash Disbursement 49800

(3) Preparation of cash budget for the month of

September

Particulars £

Opening Cash Balance 9000

Add: Total Expected Cash Collection 44648

Less: Total Expected Cash Disbursement 49800

Expected Closing Cash Balance 3848

Add: Bank Credit 1152

Expected Closing Cash Balance with bank credit 5000

TASK 3

3.1: Use of accounting system to determine financial issues.

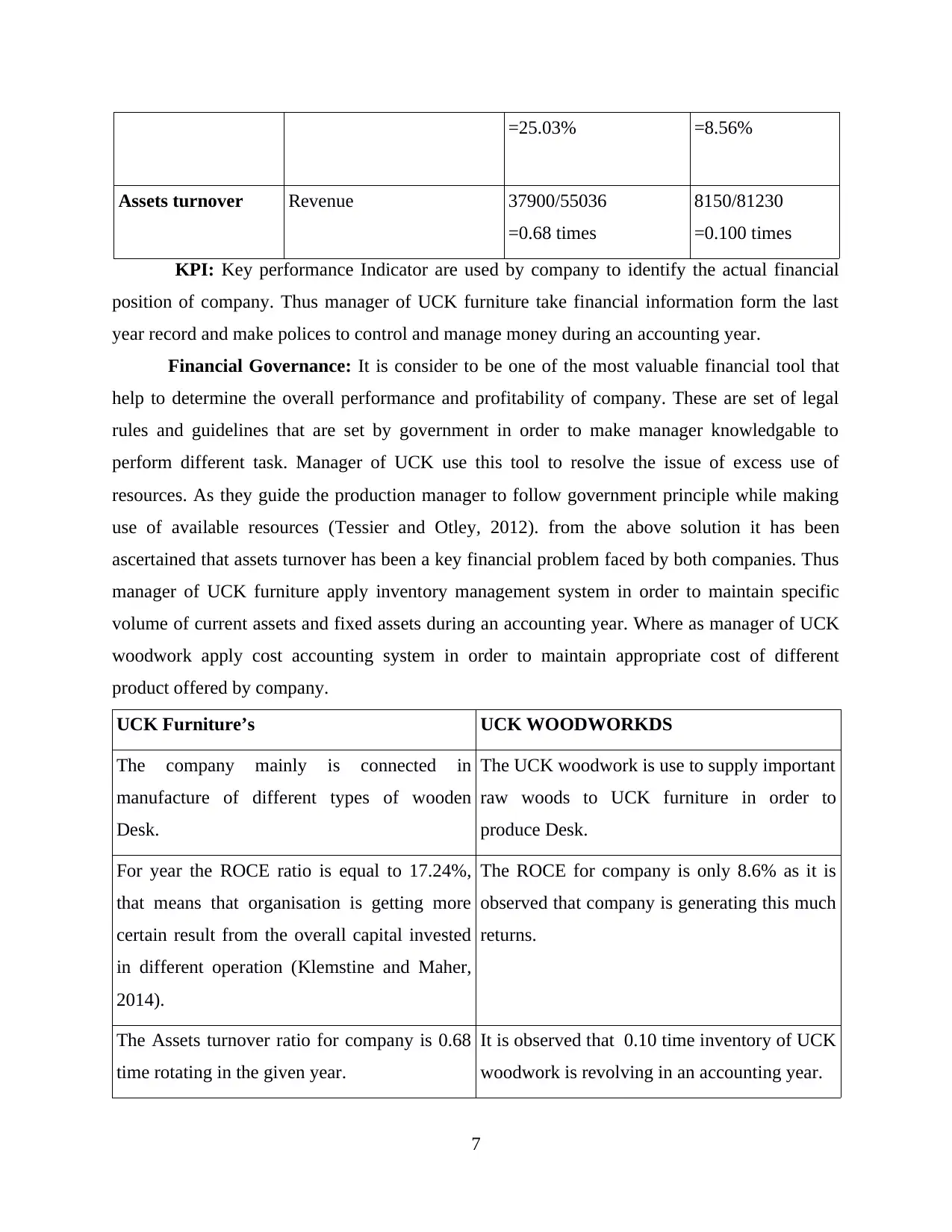

Ratios Formula UCK furniture’s UCK woodwork

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/37900*100 6955/81230*100

6

Less: Depreciation 4000 9000

Equipment Purchase 18000

Dividend Paid 3000

Total Expected Cash Disbursement 49800

(3) Preparation of cash budget for the month of

September

Particulars £

Opening Cash Balance 9000

Add: Total Expected Cash Collection 44648

Less: Total Expected Cash Disbursement 49800

Expected Closing Cash Balance 3848

Add: Bank Credit 1152

Expected Closing Cash Balance with bank credit 5000

TASK 3

3.1: Use of accounting system to determine financial issues.

Ratios Formula UCK furniture’s UCK woodwork

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/37900*100 6955/81230*100

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=25.03% =8.56%

Assets turnover Revenue 37900/55036

=0.68 times

8150/81230

=0.100 times

KPI: Key performance Indicator are used by company to identify the actual financial

position of company. Thus manager of UCK furniture take financial information form the last

year record and make polices to control and manage money during an accounting year.

Financial Governance: It is consider to be one of the most valuable financial tool that

help to determine the overall performance and profitability of company. These are set of legal

rules and guidelines that are set by government in order to make manager knowledgable to

perform different task. Manager of UCK use this tool to resolve the issue of excess use of

resources. As they guide the production manager to follow government principle while making

use of available resources (Tessier and Otley, 2012). from the above solution it has been

ascertained that assets turnover has been a key financial problem faced by both companies. Thus

manager of UCK furniture apply inventory management system in order to maintain specific

volume of current assets and fixed assets during an accounting year. Where as manager of UCK

woodwork apply cost accounting system in order to maintain appropriate cost of different

product offered by company.

UCK Furniture’s UCK WOODWORKDS

The company mainly is connected in

manufacture of different types of wooden

Desk.

The UCK woodwork is use to supply important

raw woods to UCK furniture in order to

produce Desk.

For year the ROCE ratio is equal to 17.24%,

that means that organisation is getting more

certain result from the overall capital invested

in different operation (Klemstine and Maher,

2014).

The ROCE for company is only 8.6% as it is

observed that company is generating this much

returns.

The Assets turnover ratio for company is 0.68

time rotating in the given year.

It is observed that 0.10 time inventory of UCK

woodwork is revolving in an accounting year.

7

Assets turnover Revenue 37900/55036

=0.68 times

8150/81230

=0.100 times

KPI: Key performance Indicator are used by company to identify the actual financial

position of company. Thus manager of UCK furniture take financial information form the last

year record and make polices to control and manage money during an accounting year.

Financial Governance: It is consider to be one of the most valuable financial tool that

help to determine the overall performance and profitability of company. These are set of legal

rules and guidelines that are set by government in order to make manager knowledgable to

perform different task. Manager of UCK use this tool to resolve the issue of excess use of

resources. As they guide the production manager to follow government principle while making

use of available resources (Tessier and Otley, 2012). from the above solution it has been

ascertained that assets turnover has been a key financial problem faced by both companies. Thus

manager of UCK furniture apply inventory management system in order to maintain specific

volume of current assets and fixed assets during an accounting year. Where as manager of UCK

woodwork apply cost accounting system in order to maintain appropriate cost of different

product offered by company.

UCK Furniture’s UCK WOODWORKDS

The company mainly is connected in

manufacture of different types of wooden

Desk.

The UCK woodwork is use to supply important

raw woods to UCK furniture in order to

produce Desk.

For year the ROCE ratio is equal to 17.24%,

that means that organisation is getting more

certain result from the overall capital invested

in different operation (Klemstine and Maher,

2014).

The ROCE for company is only 8.6% as it is

observed that company is generating this much

returns.

The Assets turnover ratio for company is 0.68

time rotating in the given year.

It is observed that 0.10 time inventory of UCK

woodwork is revolving in an accounting year.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.2: Evaluating financial issues faced by UCK furniture.

Financial problem are consider to be situation that may reduce the performance of

company. There are various financial problems that needs to be resolved otherwise it may

reduces the performance of company (Lim, 2011). Thus different management accounting

system are useful in order to maintain financial sustainability and financial performance of

company. Such as price optimisation system are helpful in increasing sales for company and

improving net profit and earning during an accounting year. Job costing system are helpful in

controlling different cost that are utilize by company in order to complete different jobs.

3.3: Analysis of planning tools that is used in management accounting.

In order to examine the whole profitability level for an organisation planning tools are

taken into account by the respective internal manager (Van der Stede, 2015). Budgets are

prepared by manager of company in order to get estimate about the future expenses and help in

improving profitability. Standard costing is consider to be important accounting technique that is

used by manager of UCK furniture in order to determine the actual differences between actual

cost of product manufacture during a time frame. And costs that should occurred for these

product.

CONCLUSION

In the conclusion, it has been stated that management accounting is the process of

analysing and calculating overall actual growth of an organisation. With proper total cost

analysis company are able to control cost and attain high profit in upcoming time. Planning tool

are useful to make plan for future so that any risk or contingency can be resolved. Advantages

and disadvantages of using planning tool that help to control budgets that help to accomplish

future growth and sustainability.

8

Financial problem are consider to be situation that may reduce the performance of

company. There are various financial problems that needs to be resolved otherwise it may

reduces the performance of company (Lim, 2011). Thus different management accounting

system are useful in order to maintain financial sustainability and financial performance of

company. Such as price optimisation system are helpful in increasing sales for company and

improving net profit and earning during an accounting year. Job costing system are helpful in

controlling different cost that are utilize by company in order to complete different jobs.

3.3: Analysis of planning tools that is used in management accounting.

In order to examine the whole profitability level for an organisation planning tools are

taken into account by the respective internal manager (Van der Stede, 2015). Budgets are

prepared by manager of company in order to get estimate about the future expenses and help in

improving profitability. Standard costing is consider to be important accounting technique that is

used by manager of UCK furniture in order to determine the actual differences between actual

cost of product manufacture during a time frame. And costs that should occurred for these

product.

CONCLUSION

In the conclusion, it has been stated that management accounting is the process of

analysing and calculating overall actual growth of an organisation. With proper total cost

analysis company are able to control cost and attain high profit in upcoming time. Planning tool

are useful to make plan for future so that any risk or contingency can be resolved. Advantages

and disadvantages of using planning tool that help to control budgets that help to accomplish

future growth and sustainability.

8

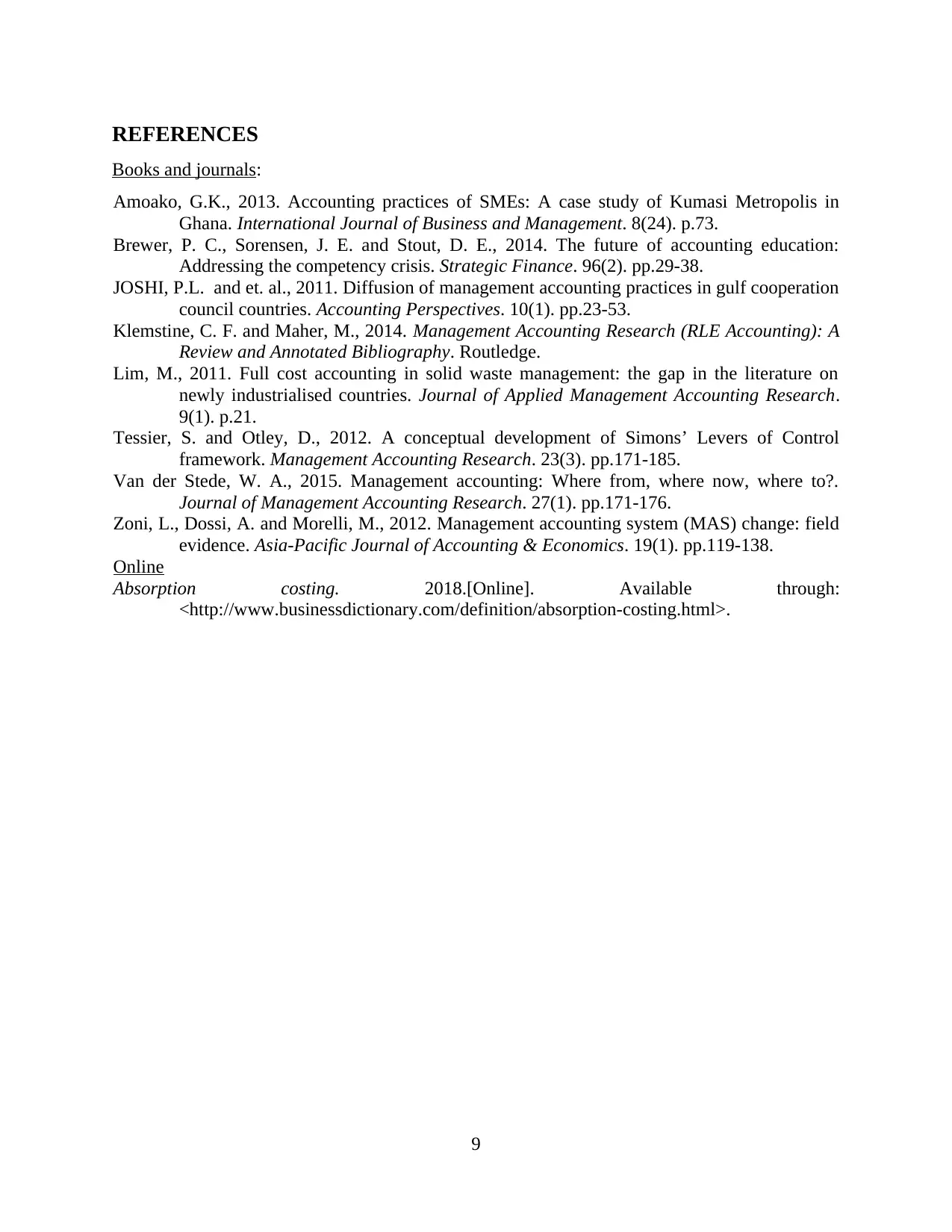

REFERENCES

Books and journals:

Amoako, G.K., 2013. Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). p.73.

Brewer, P. C., Sorensen, J. E. and Stout, D. E., 2014. The future of accounting education:

Addressing the competency crisis. Strategic Finance. 96(2). pp.29-38.

JOSHI, P.L. and et. al., 2011. Diffusion of management accounting practices in gulf cooperation

council countries. Accounting Perspectives. 10(1). pp.23-53.

Klemstine, C. F. and Maher, M., 2014. Management Accounting Research (RLE Accounting): A

Review and Annotated Bibliography. Routledge.

Lim, M., 2011. Full cost accounting in solid waste management: the gap in the literature on

newly industrialised countries. Journal of Applied Management Accounting Research.

9(1). p.21.

Tessier, S. and Otley, D., 2012. A conceptual development of Simons’ Levers of Control

framework. Management Accounting Research. 23(3). pp.171-185.

Van der Stede, W. A., 2015. Management accounting: Where from, where now, where to?.

Journal of Management Accounting Research. 27(1). pp.171-176.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Online

Absorption costing. 2018.[Online]. Available through:

<http://www.businessdictionary.com/definition/absorption-costing.html>.

9

Books and journals:

Amoako, G.K., 2013. Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). p.73.

Brewer, P. C., Sorensen, J. E. and Stout, D. E., 2014. The future of accounting education:

Addressing the competency crisis. Strategic Finance. 96(2). pp.29-38.

JOSHI, P.L. and et. al., 2011. Diffusion of management accounting practices in gulf cooperation

council countries. Accounting Perspectives. 10(1). pp.23-53.

Klemstine, C. F. and Maher, M., 2014. Management Accounting Research (RLE Accounting): A

Review and Annotated Bibliography. Routledge.

Lim, M., 2011. Full cost accounting in solid waste management: the gap in the literature on

newly industrialised countries. Journal of Applied Management Accounting Research.

9(1). p.21.

Tessier, S. and Otley, D., 2012. A conceptual development of Simons’ Levers of Control

framework. Management Accounting Research. 23(3). pp.171-185.

Van der Stede, W. A., 2015. Management accounting: Where from, where now, where to?.

Journal of Management Accounting Research. 27(1). pp.171-176.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Online

Absorption costing. 2018.[Online]. Available through:

<http://www.businessdictionary.com/definition/absorption-costing.html>.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.