Tax Adjustments for Sole Traders

VerifiedAdded on 2021/04/27

|20

|2145

|63

AI Summary

This assignment covers various aspects of tax adjustments for sole traders. It starts by explaining the concept of trade profits and losses, then delves into specific taxable and non-taxable income sources such as salaries, subscriptions to golf clubs, legal fees for short leases, and training courses. The document also discusses impairments of debts and allowances for debtors, including write-offs of trade debts and non-trade loans to customers or employees. Furthermore, it touches on other adjustments like using a private residence for business purposes, business calls from personal phones, and expenses met from personal funds. The assignment includes example questions, such as determining the amount of leasing costs disallowed due to high CO2 emissions in a car used for business purposes. It emphasizes the importance of accurately calculating trade profits and losses by considering these various tax adjustments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Trading income

• Self-employed/sole traders: individuals whose profits arise from a

trade, profession or vocation

• What constitutes a trade? This has been reviewed several times by

the Courts.

• In June 1955, the Royal Commission on the Taxation of Profits and

Income used these judicial decisions to establish what they

regarded to be the following main criteria in identifying the 'badges

of trade':

-1.The subject matter of the transaction; there are 3 reasons for

purchasing an asset:

1. For personal use – not subject to tax

2. As an investment – capital in nature and not subject to income tax

3. For resale at a profit (that constitutes a trade): therefore subject to income

tax

-

• Self-employed/sole traders: individuals whose profits arise from a

trade, profession or vocation

• What constitutes a trade? This has been reviewed several times by

the Courts.

• In June 1955, the Royal Commission on the Taxation of Profits and

Income used these judicial decisions to establish what they

regarded to be the following main criteria in identifying the 'badges

of trade':

-1.The subject matter of the transaction; there are 3 reasons for

purchasing an asset:

1. For personal use – not subject to tax

2. As an investment – capital in nature and not subject to income tax

3. For resale at a profit (that constitutes a trade): therefore subject to income

tax

-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Badges of trade

2.The length of the period of ownership: the longer the period

between date of acquisition and date of disposal, the more likely the

transaction will not be treated as trade.

3.The frequency or number of similar transactions by the same person;

usually the more transactions there are, the more likely that they will

be regarded as trading activities.

E.g. An individual acquired 1,000,000 toilet rolls and resold them at a

profit. In this case, he was judged to have made a trading profit and

single transaction was enough.

One could argue this was an investment but usually to be

considered as an investment, goods must be either income

producing (such as land or shares) or liable to be held for aesthetic

reasons (such as works of art)

2.The length of the period of ownership: the longer the period

between date of acquisition and date of disposal, the more likely the

transaction will not be treated as trade.

3.The frequency or number of similar transactions by the same person;

usually the more transactions there are, the more likely that they will

be regarded as trading activities.

E.g. An individual acquired 1,000,000 toilet rolls and resold them at a

profit. In this case, he was judged to have made a trading profit and

single transaction was enough.

One could argue this was an investment but usually to be

considered as an investment, goods must be either income

producing (such as land or shares) or liable to be held for aesthetic

reasons (such as works of art)

Badges of trade

• 4.Supplementary work and marketing; For example, in CIR v

Livingston and Others [1926] 11TC538 a sea vessel was purchased

as a joint venture by three individuals. The Lord President stated, at

pages 542 and 543:

• “The Respondents began by getting together a capital stock

sufficient (1) to buy a second-hand vessel, and (2) to convert her

into a marketable drifter. They bought the vessel and caused it to be

converted at their expense with that object in view, and they

successfully put her on the market. From beginning to end, these

operations seem to me to be the same as those which characterise

the trade of converting and refitting second-hand articles for sale…

The profit made by the venture arose, not from the mere

appreciation of the capital value of an isolated purchase for resale,

but from the expenditure on the subject purchased of money laid out

upon it for the purpose of making it marketable at a profit. That

seems to me of the very essence of trade”.'

• 4.Supplementary work and marketing; For example, in CIR v

Livingston and Others [1926] 11TC538 a sea vessel was purchased

as a joint venture by three individuals. The Lord President stated, at

pages 542 and 543:

• “The Respondents began by getting together a capital stock

sufficient (1) to buy a second-hand vessel, and (2) to convert her

into a marketable drifter. They bought the vessel and caused it to be

converted at their expense with that object in view, and they

successfully put her on the market. From beginning to end, these

operations seem to me to be the same as those which characterise

the trade of converting and refitting second-hand articles for sale…

The profit made by the venture arose, not from the mere

appreciation of the capital value of an isolated purchase for resale,

but from the expenditure on the subject purchased of money laid out

upon it for the purpose of making it marketable at a profit. That

seems to me of the very essence of trade”.'

Badges of trade

• 5.The circumstances that were responsible for the sale;

a forced sale to raise cash for an emergency is an

indication that the transaction was not of a trading

nature.

• 6.Motive; intention to profit indicates trading. For e.g, an

individual hedging against devaluation of sterling by

purchasing silver bullion. On resale, a profit arises and is

regarded as trading profit since the motive for the

transaction was to make a profit in sterling terms.

• 7. Method of finance: If the purchaser has to borrow

money to buy an asset such that he has to sell that asset

quickly to repay the loan, it may be inferred that trading

was taking place.

• 5.The circumstances that were responsible for the sale;

a forced sale to raise cash for an emergency is an

indication that the transaction was not of a trading

nature.

• 6.Motive; intention to profit indicates trading. For e.g, an

individual hedging against devaluation of sterling by

purchasing silver bullion. On resale, a profit arises and is

regarded as trading profit since the motive for the

transaction was to make a profit in sterling terms.

• 7. Method of finance: If the purchaser has to borrow

money to buy an asset such that he has to sell that asset

quickly to repay the loan, it may be inferred that trading

was taking place.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Badges of trade

• 8. Existence of similar trading transactions or interests

If there is an existing trade, then a similarity to the

transaction which is being considered may point to that

transaction having a trading character. For e.g, a builder

who builds and sells a number of houses may be held to

be trading even if he retains one or more houses for

longer than usual and claims that they were held as an

investment

• Tax adjusted trading profit: the net profit per the financial

accounts often different from taxable trading profit figure.

Adjustments need to be made.

• 8. Existence of similar trading transactions or interests

If there is an existing trade, then a similarity to the

transaction which is being considered may point to that

transaction having a trading character. For e.g, a builder

who builds and sells a number of houses may be held to

be trading even if he retains one or more houses for

longer than usual and claims that they were held as an

investment

• Tax adjusted trading profit: the net profit per the financial

accounts often different from taxable trading profit figure.

Adjustments need to be made.

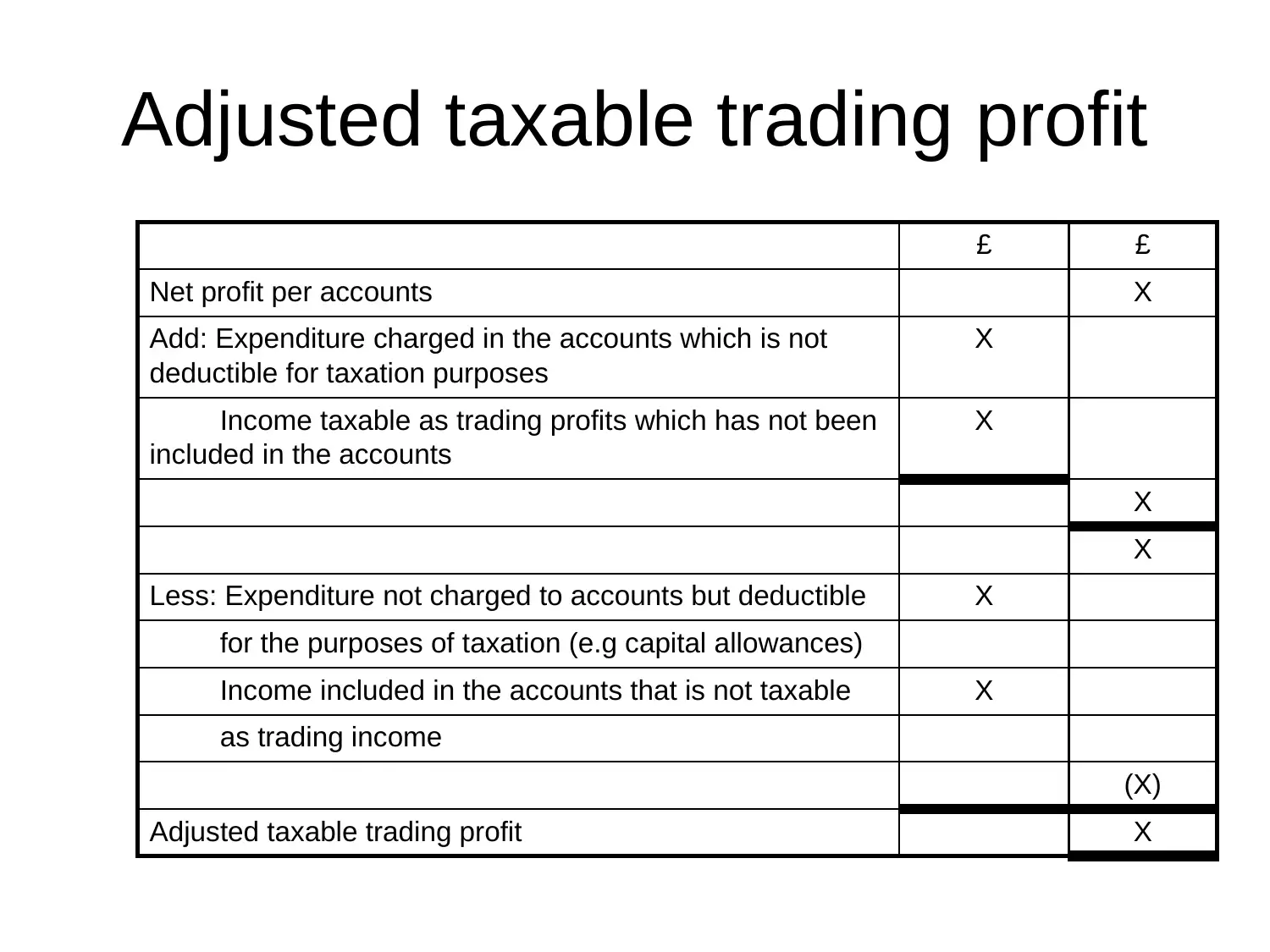

Adjusted taxable trading profit

£ £

Net profit per accounts X

Add: Expenditure charged in the accounts which is not

deductible for taxation purposes

X

Income taxable as trading profits which has not been

included in the accounts

X

X

X

Less: Expenditure not charged to accounts but deductible X

for the purposes of taxation (e.g capital allowances)

Income included in the accounts that is not taxable X

as trading income

(X)

Adjusted taxable trading profit X

£ £

Net profit per accounts X

Add: Expenditure charged in the accounts which is not

deductible for taxation purposes

X

Income taxable as trading profits which has not been

included in the accounts

X

X

X

Less: Expenditure not charged to accounts but deductible X

for the purposes of taxation (e.g capital allowances)

Income included in the accounts that is not taxable X

as trading income

(X)

Adjusted taxable trading profit X

Allowable expenditure

• Tax rule: Expenditure incurred wholly and exclusively for

the purposes of trade is allowable

• Expenditure may not be allowable: remoteness test and

duality principle

• Remoteness test: expenditure regarded too remote from

the trade.

• Duality principle: expenditure has more than one

purpose and one of them is not trading. Illustration: a

self-employed trader was unable to eat lunch at home

and claimed the extra cost of eating out as a tax

deduction. This was not allowed. The duality of the case

lay in the fact that the taxpayer needed to eat to live as

well, not just to work.

• Tax rule: Expenditure incurred wholly and exclusively for

the purposes of trade is allowable

• Expenditure may not be allowable: remoteness test and

duality principle

• Remoteness test: expenditure regarded too remote from

the trade.

• Duality principle: expenditure has more than one

purpose and one of them is not trading. Illustration: a

self-employed trader was unable to eat lunch at home

and claimed the extra cost of eating out as a tax

deduction. This was not allowed. The duality of the case

lay in the fact that the taxpayer needed to eat to live as

well, not just to work.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Allowable expenditure

• Excessive salary paid to sole trader’s family: business

owners often employ their spouses or family members in

their business. Any salary paid to the latter must not be

excessive, i.e., it must be at the commercial rate for the

work performed. Excessive salary payments are

disallowed.

• Interest payable: interest on borrowings such as

business account overdrafts, credit cards or hire

purchase contracts is allowable trading expense

calculated on accruals basis

• Interest payable: interest paid on overdue tax is never

allowable. Interest received on overpaid tax not taxable.

• Excessive salary paid to sole trader’s family: business

owners often employ their spouses or family members in

their business. Any salary paid to the latter must not be

excessive, i.e., it must be at the commercial rate for the

work performed. Excessive salary payments are

disallowed.

• Interest payable: interest on borrowings such as

business account overdrafts, credit cards or hire

purchase contracts is allowable trading expense

calculated on accruals basis

• Interest payable: interest paid on overdue tax is never

allowable. Interest received on overpaid tax not taxable.

Allowable expenditure

• Subscriptions:

– Trade or professional association subscriptions normally

deductible since they will be made wholly and exclusively for the

purposes of the trade

• Charitable donations: to be allowable, expenses must

be: • Wholly and exclusively for trading purposes

• Local and reasonable in size in relation to the business making the

donation

• Made to an educational, religious, cultural, recreational or

benevolent organisation

• If donation is disallowed but payment was made to a charity, the

taxpayer can claim relief under Gift Aid Scheme

• Subscriptions and donations to political parties are not

deductible

• Subscriptions:

– Trade or professional association subscriptions normally

deductible since they will be made wholly and exclusively for the

purposes of the trade

• Charitable donations: to be allowable, expenses must

be: • Wholly and exclusively for trading purposes

• Local and reasonable in size in relation to the business making the

donation

• Made to an educational, religious, cultural, recreational or

benevolent organisation

• If donation is disallowed but payment was made to a charity, the

taxpayer can claim relief under Gift Aid Scheme

• Subscriptions and donations to political parties are not

deductible

Non-Allowable expenditure

• Appropriations: withdrawal of funds from a

business and most common e.g’s are:

– Business owner’s salary

– Interest paid to owner on capital invested in

business

– Drawings by sole trader or partner

– Any private element of expenditure relating to

owner’s motor car, telephone

Such appropriations are disallowed expenses.

• Appropriations: withdrawal of funds from a

business and most common e.g’s are:

– Business owner’s salary

– Interest paid to owner on capital invested in

business

– Drawings by sole trader or partner

– Any private element of expenditure relating to

owner’s motor car, telephone

Such appropriations are disallowed expenses.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Non-Allowable expenditure

• Expenditure on capital assets not allowable.

• Expenditure on P&M attracts capital allowances (to be

covered later)

• Legal cases have shown the following in respect of

repair (revenue) versus improvement (capital)

expenditure:

1. Cost of initial repairs in order to make an asset

usable is not deductible

2. Cost of initial repairs is deductible if asset can be put

into use before any repairs are carried out

3. To be allowable, it needs to be proven that the

restoration renews a subsidiary part of an asset. For

e.g the replacement of an old stand with a new one at

a football club was held to be expenditure on a new

asset and thus capital expenditure.

• Expenditure on capital assets not allowable.

• Expenditure on P&M attracts capital allowances (to be

covered later)

• Legal cases have shown the following in respect of

repair (revenue) versus improvement (capital)

expenditure:

1. Cost of initial repairs in order to make an asset

usable is not deductible

2. Cost of initial repairs is deductible if asset can be put

into use before any repairs are carried out

3. To be allowable, it needs to be proven that the

restoration renews a subsidiary part of an asset. For

e.g the replacement of an old stand with a new one at

a football club was held to be expenditure on a new

asset and thus capital expenditure.

Non-charitable gifts

• Entertaining and gifts:

– Entertainment expenditure not allowed.

– Only exception: Expenditure relating to employees, provided it is

not incidental to the entertainment of others

• Gifts to employees:

– Allowable trading expenditure

– If gift falls within the benefit rules, to be assessed as employment

income for employee

• Gifts to customers:

– Allowable if they cost less than £50 per year, are not of food,

drink, tobacco or vouchers exchangeable for goods and carry a

conspicuous advertisement of the business making the gift

– If total of gifts in tax year exceed £50, the full cost of the item is

disallowable, not just the excess

• Entertaining and gifts:

– Entertainment expenditure not allowed.

– Only exception: Expenditure relating to employees, provided it is

not incidental to the entertainment of others

• Gifts to employees:

– Allowable trading expenditure

– If gift falls within the benefit rules, to be assessed as employment

income for employee

• Gifts to customers:

– Allowable if they cost less than £50 per year, are not of food,

drink, tobacco or vouchers exchangeable for goods and carry a

conspicuous advertisement of the business making the gift

– If total of gifts in tax year exceed £50, the full cost of the item is

disallowable, not just the excess

Legal and professional charges

• General principle: if incurred for the purposes of the

trade, it is allowable.

– E.g are legal fees chasing trade debts, charges incurred in

defending the title to fixed assets

• Capital expenditure: disallowable

– E.g are fees associated with acquiring new fixed assets.

– Exceptions:

(1) Fees and other costs of obtaining long-term debt finance are

allowable for a sole trader

(2) Cost of registering patents is allowable

(3) Expense of renewing a short lease (< 50 years) is allowable,

although the legal expenses incurred on the initial granting of the

lease are not.

• General principle: if incurred for the purposes of the

trade, it is allowable.

– E.g are legal fees chasing trade debts, charges incurred in

defending the title to fixed assets

• Capital expenditure: disallowable

– E.g are fees associated with acquiring new fixed assets.

– Exceptions:

(1) Fees and other costs of obtaining long-term debt finance are

allowable for a sole trader

(2) Cost of registering patents is allowable

(3) Expense of renewing a short lease (< 50 years) is allowable,

although the legal expenses incurred on the initial granting of the

lease are not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

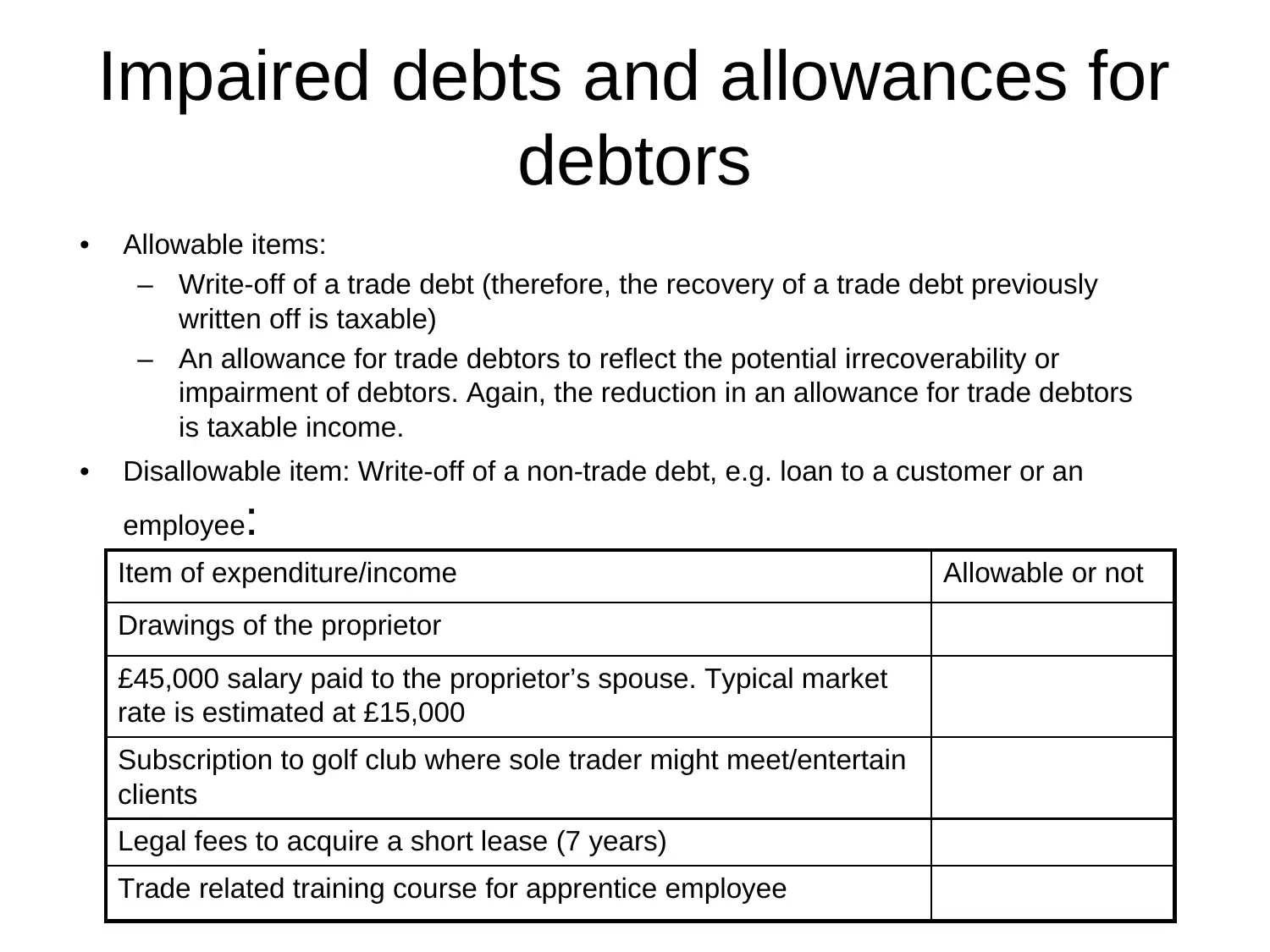

Impaired debts and allowances for

debtors

• Allowable items:

– Write-off of a trade debt (therefore, the recovery of a trade debt previously

written off is taxable)

– An allowance for trade debtors to reflect the potential irrecoverability or

impairment of debtors. Again, the reduction in an allowance for trade debtors

is taxable income.

• Disallowable item: Write-off of a non-trade debt, e.g. loan to a customer or an

employee:

Item of expenditure/income Allowable or not

Drawings of the proprietor

£45,000 salary paid to the proprietor’s spouse. Typical market

rate is estimated at £15,000

Subscription to golf club where sole trader might meet/entertain

clients

Legal fees to acquire a short lease (7 years)

Trade related training course for apprentice employee

debtors

• Allowable items:

– Write-off of a trade debt (therefore, the recovery of a trade debt previously

written off is taxable)

– An allowance for trade debtors to reflect the potential irrecoverability or

impairment of debtors. Again, the reduction in an allowance for trade debtors

is taxable income.

• Disallowable item: Write-off of a non-trade debt, e.g. loan to a customer or an

employee:

Item of expenditure/income Allowable or not

Drawings of the proprietor

£45,000 salary paid to the proprietor’s spouse. Typical market

rate is estimated at £15,000

Subscription to golf club where sole trader might meet/entertain

clients

Legal fees to acquire a short lease (7 years)

Trade related training course for apprentice employee

Other adjustments

• The following also are deductible:

– Where a business owner uses their private residence

partly for business purposes for e.g, the business

portion of running expenses is allowable

– Business calls from the private telephone of the sole

trader

– Expenses that are wholly and exclusively for the trade

that have been met from the private funds of the

owner

– Allowable trading element of lease premiums paid on

short leases

• The following also are deductible:

– Where a business owner uses their private residence

partly for business purposes for e.g, the business

portion of running expenses is allowable

– Business calls from the private telephone of the sole

trader

– Expenses that are wholly and exclusively for the trade

that have been met from the private funds of the

owner

– Allowable trading element of lease premiums paid on

short leases

Other adjustments

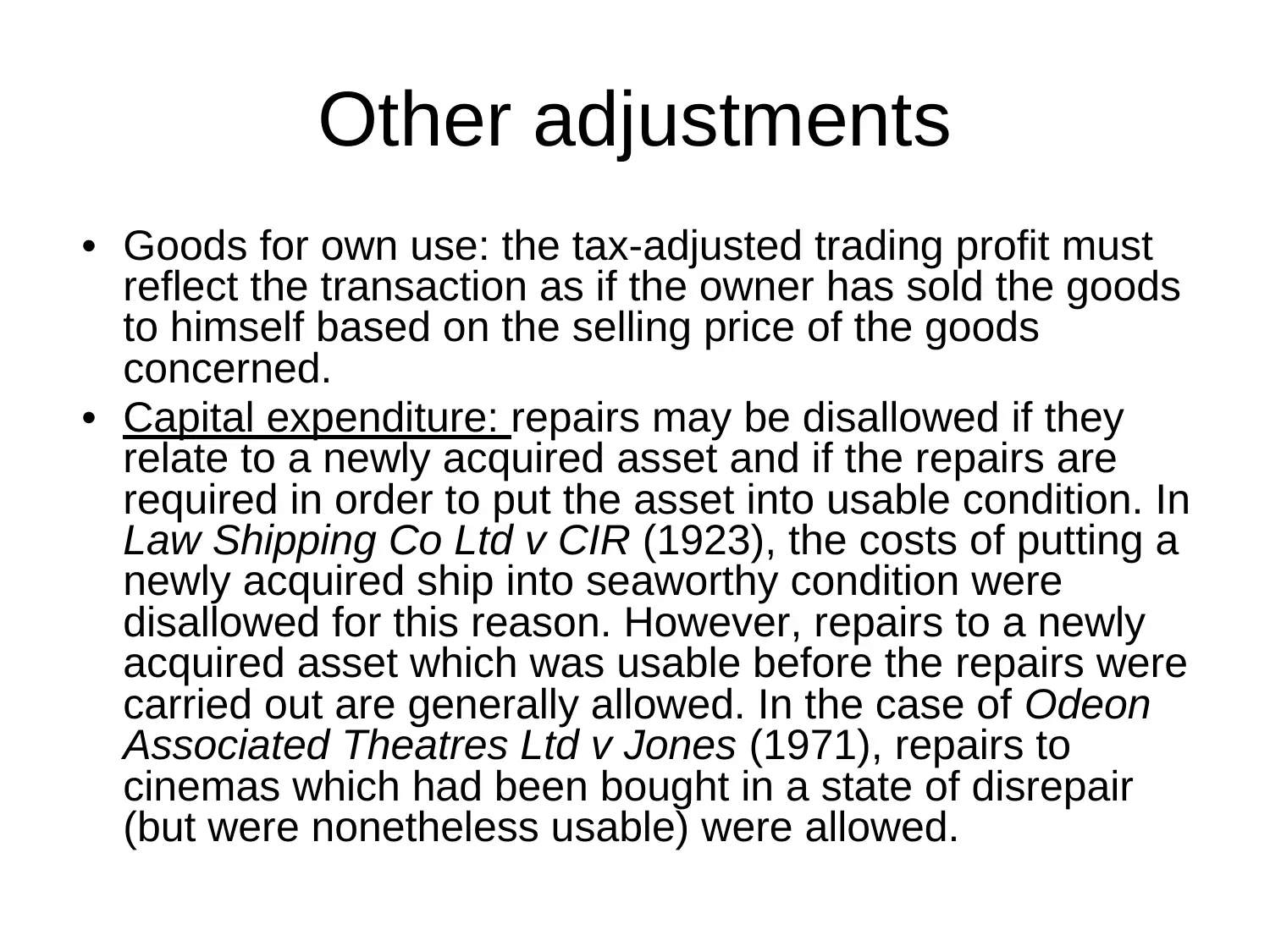

• Goods for own use: the tax-adjusted trading profit must

reflect the transaction as if the owner has sold the goods

to himself based on the selling price of the goods

concerned.

• Capital expenditure: repairs may be disallowed if they

relate to a newly acquired asset and if the repairs are

required in order to put the asset into usable condition. In

Law Shipping Co Ltd v CIR (1923), the costs of putting a

newly acquired ship into seaworthy condition were

disallowed for this reason. However, repairs to a newly

acquired asset which was usable before the repairs were

carried out are generally allowed. In the case of Odeon

Associated Theatres Ltd v Jones (1971), repairs to

cinemas which had been bought in a state of disrepair

(but were nonetheless usable) were allowed.

• Goods for own use: the tax-adjusted trading profit must

reflect the transaction as if the owner has sold the goods

to himself based on the selling price of the goods

concerned.

• Capital expenditure: repairs may be disallowed if they

relate to a newly acquired asset and if the repairs are

required in order to put the asset into usable condition. In

Law Shipping Co Ltd v CIR (1923), the costs of putting a

newly acquired ship into seaworthy condition were

disallowed for this reason. However, repairs to a newly

acquired asset which was usable before the repairs were

carried out are generally allowed. In the case of Odeon

Associated Theatres Ltd v Jones (1971), repairs to

cinemas which had been bought in a state of disrepair

(but were nonetheless usable) were allowed.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Other adjustments

• Lease charges for cars with CO2 emissions

exceeding 110 g/km:

– There is a restriction on the leasing costs of a

car with CO2 emissions exceeding 110 g/km.

– 15% of the leasing costs will be disallowed in

the profits adjustment.

• Lease charges for cars with CO2 emissions

exceeding 110 g/km:

– There is a restriction on the leasing costs of a

car with CO2 emissions exceeding 110 g/km.

– 15% of the leasing costs will be disallowed in

the profits adjustment.

Other adjustments

E.g: Mandy is a sole trader. In May

2019, she leased a car for use in her

business. The leasing costs for 2019/20

were £4,000. The car had CO2 emissions

of 121 g/km.

What is the amount of the leasing costs

that will be disallowed in the adjustment of

profits calculation?

E.g: Mandy is a sole trader. In May

2019, she leased a car for use in her

business. The leasing costs for 2019/20

were £4,000. The car had CO2 emissions

of 121 g/km.

What is the amount of the leasing costs

that will be disallowed in the adjustment of

profits calculation?

Other adjustments

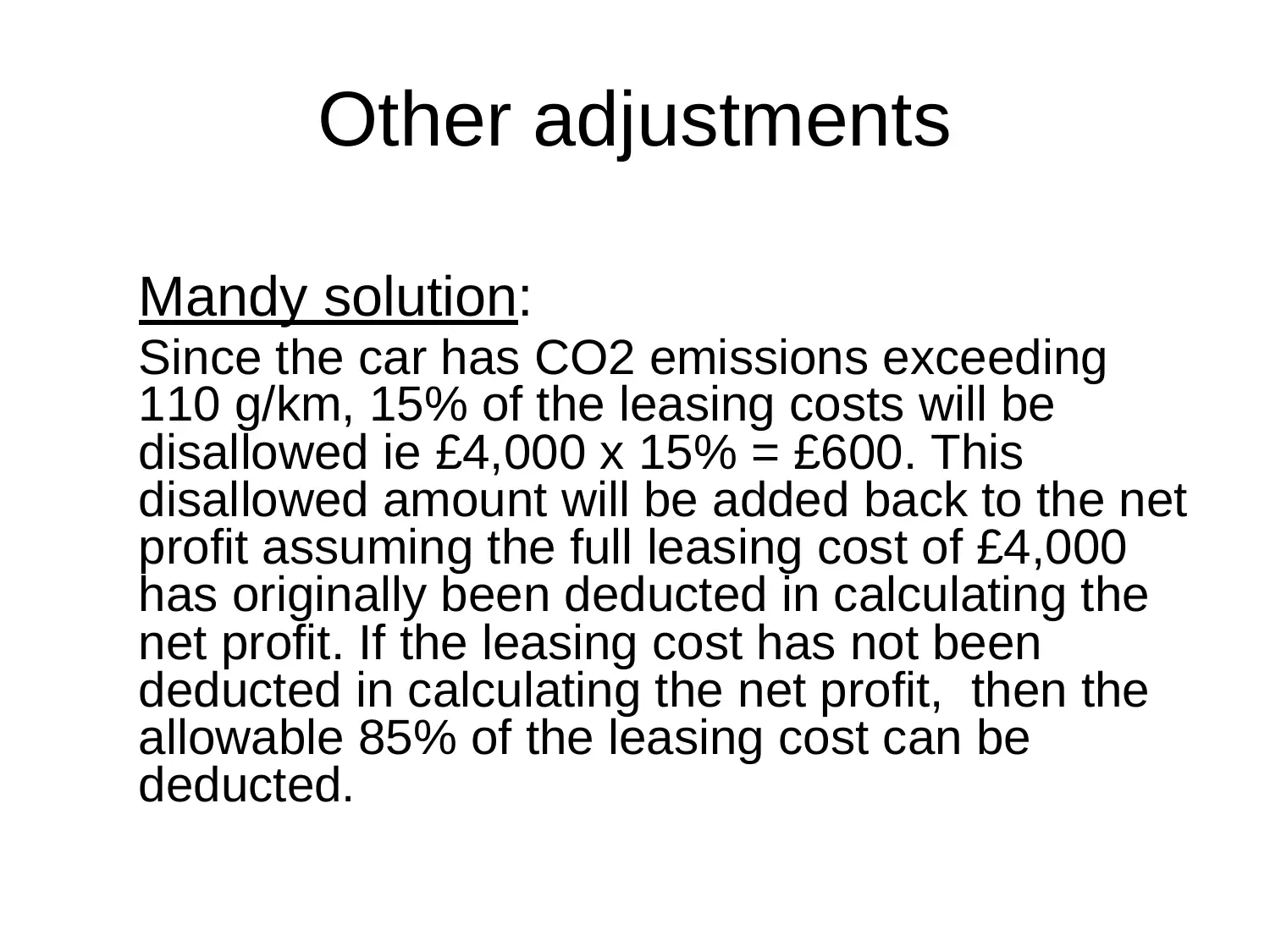

Mandy solution:

Since the car has CO2 emissions exceeding

110 g/km, 15% of the leasing costs will be

disallowed ie £4,000 x 15% = £600. This

disallowed amount will be added back to the net

profit assuming the full leasing cost of £4,000

has originally been deducted in calculating the

net profit. If the leasing cost has not been

deducted in calculating the net profit, then the

allowable 85% of the leasing cost can be

deducted.

Mandy solution:

Since the car has CO2 emissions exceeding

110 g/km, 15% of the leasing costs will be

disallowed ie £4,000 x 15% = £600. This

disallowed amount will be added back to the net

profit assuming the full leasing cost of £4,000

has originally been deducted in calculating the

net profit. If the leasing cost has not been

deducted in calculating the net profit, then the

allowable 85% of the leasing cost can be

deducted.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Example

• Go through John tutorial question

• Go through Steven tutorial question

• Do the William Wise question as

homework.

• Do the S Pring question as homework.

• Go through John tutorial question

• Go through Steven tutorial question

• Do the William Wise question as

homework.

• Do the S Pring question as homework.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.